HI3042 Taxation Law T2 2017 Individual Assignment Case Study 1 3 Issue 3 Legal provisions 3 Application of cited provisions and calculations 3 Application of cited provisions 3 Case study 4 3 Issue 3

Added on 2020-04-07

10 Pages1678 Words497 Views

HI3042 Taxation LawT2 2017 Individual Assignment

TABLE OF CONTENTSCase study 1...............................................................................................................................3Issue........................................................................................................................................3Legal provisions.....................................................................................................................3Application of cited provisions..............................................................................................3Conclusion..............................................................................................................................3Case study 2...............................................................................................................................3Issue........................................................................................................................................3Legal provisions.....................................................................................................................3Application of cited provisions..............................................................................................3Conclusion..............................................................................................................................3Case Study 3...............................................................................................................................3Issue........................................................................................................................................3Legal provisions.....................................................................................................................3Application of cited provisions and calculations...................................................................3Case study 4...............................................................................................................................3Issue........................................................................................................................................3Legal provisions.....................................................................................................................3Application of cited provisions and calculations...................................................................3References..................................................................................................................................4

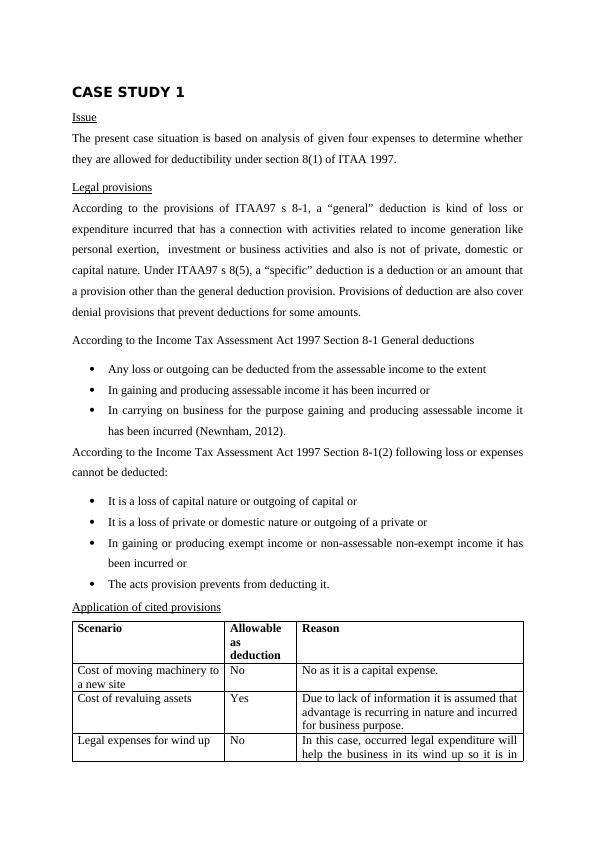

CASE STUDY 1IssueThe present case situation is based on analysis of given four expenses to determine whetherthey are allowed for deductibility under section 8(1) of ITAA 1997.Legal provisionsAccording to the provisions of ITAA97 s 8-1, a “general” deduction is kind of loss orexpenditure incurred that has a connection with activities related to income generation likepersonal exertion, investment or business activities and also is not of private, domestic orcapital nature. Under ITAA97 s 8(5), a “specific” deduction is a deduction or an amount thata provision other than the general deduction provision. Provisions of deduction are also coverdenial provisions that prevent deductions for some amounts. According to the Income Tax Assessment Act 1997 Section 8-1 General deductionsAny loss or outgoing can be deducted from the assessable income to the extentIn gaining and producing assessable income it has been incurred or In carrying on business for the purpose gaining and producing assessable income ithas been incurred (Newnham, 2012).According to the Income Tax Assessment Act 1997 Section 8-1(2) following loss or expensescannot be deducted:It is a loss of capital nature or outgoing of capital orIt is a loss of private or domestic nature or outgoing of a private orIn gaining or producing exempt income or non-assessable non-exempt income it hasbeen incurred orThe acts provision prevents from deducting it.Application of cited provisionsScenarioAllowableasdeductionReasonCost of moving machinery toa new siteNoNo as it is a capital expense.Cost of revaluing assets YesDue to lack of information it is assumed thatadvantage is recurring in nature and incurredfor business purpose.Legal expenses for wind upNoIn this case, occurred legal expenditure willhelp the business in its wind up so it is in

End of preview

Want to access all the pages? Upload your documents or become a member.

Related Documents

HA3042 Assessment 2 Australian taxation law TABLE OF CONTENTSlg...

|10

|1522

|91

HI3042- Taxation Law Assignmentlg...

|10

|1743

|33

HI3042 - Assignment On Taxation Lawlg...

|14

|1855

|55

Taxation Law Assessment Act, 1997lg...

|13

|3001

|130

HI3042 Taxation Law T2 2017 Assignmentlg...

|14

|1682

|53

The Taxation Assignmentlg...

|12

|2158

|54