Taxation Law Application Scenarios

VerifiedAdded on 2020/04/07

|10

|1292

|44

AI Summary

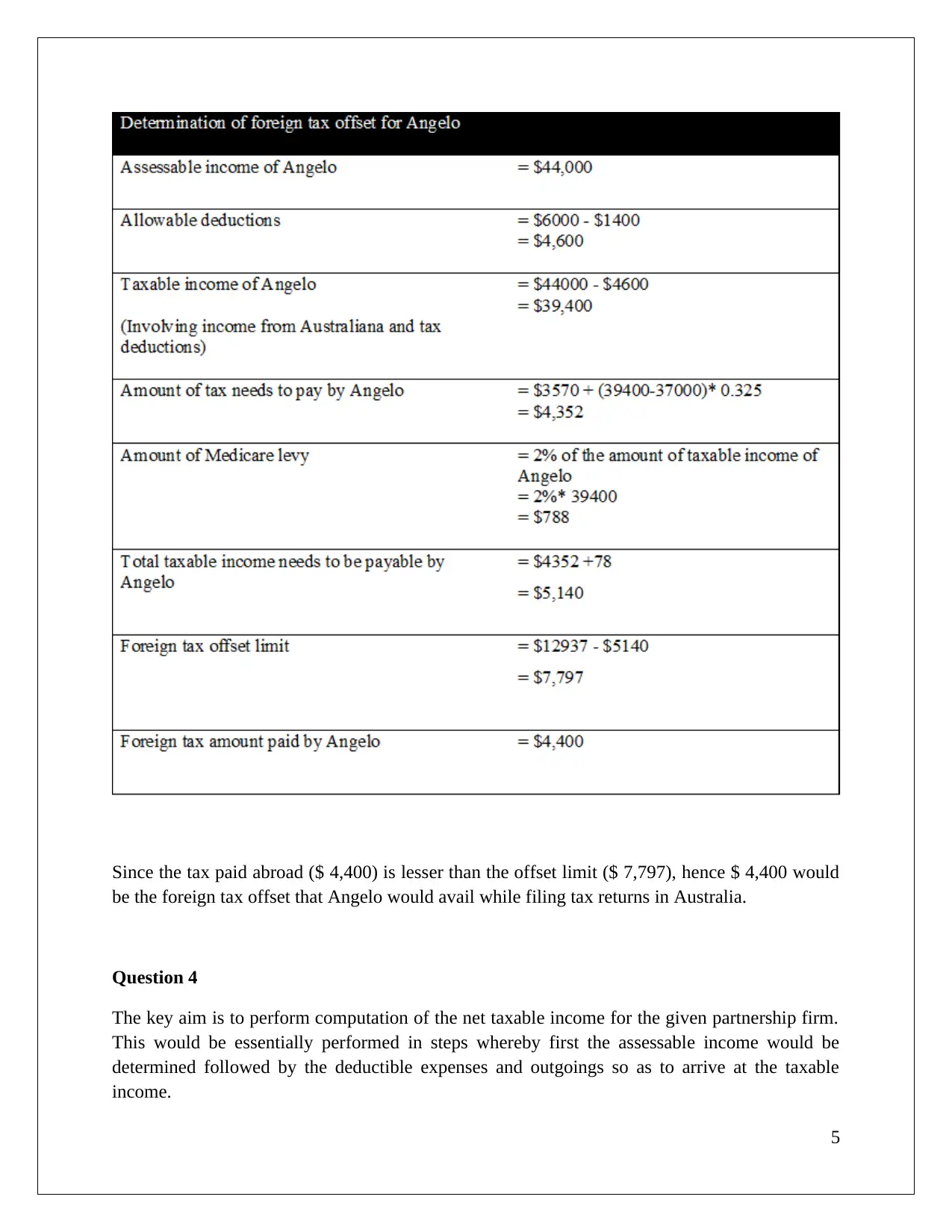

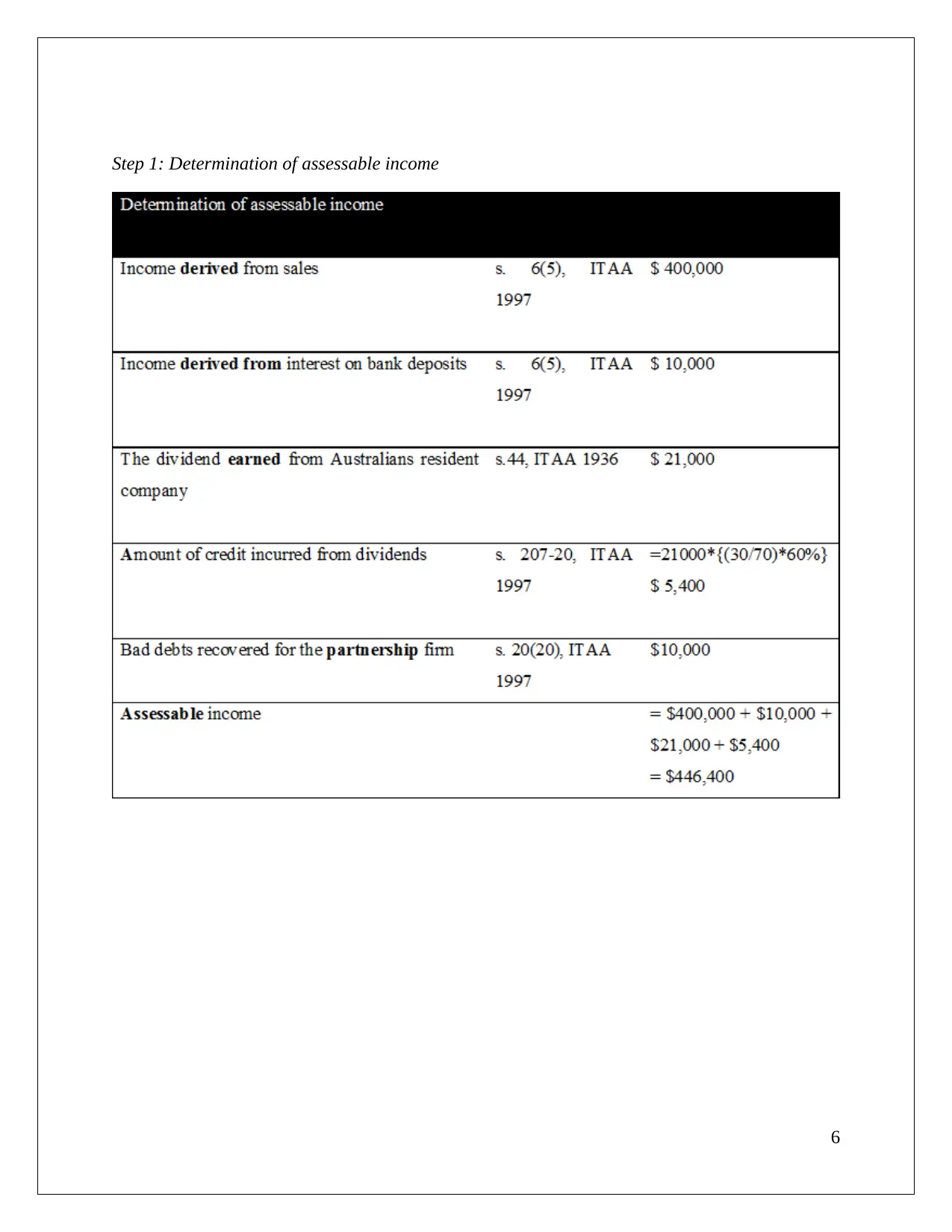

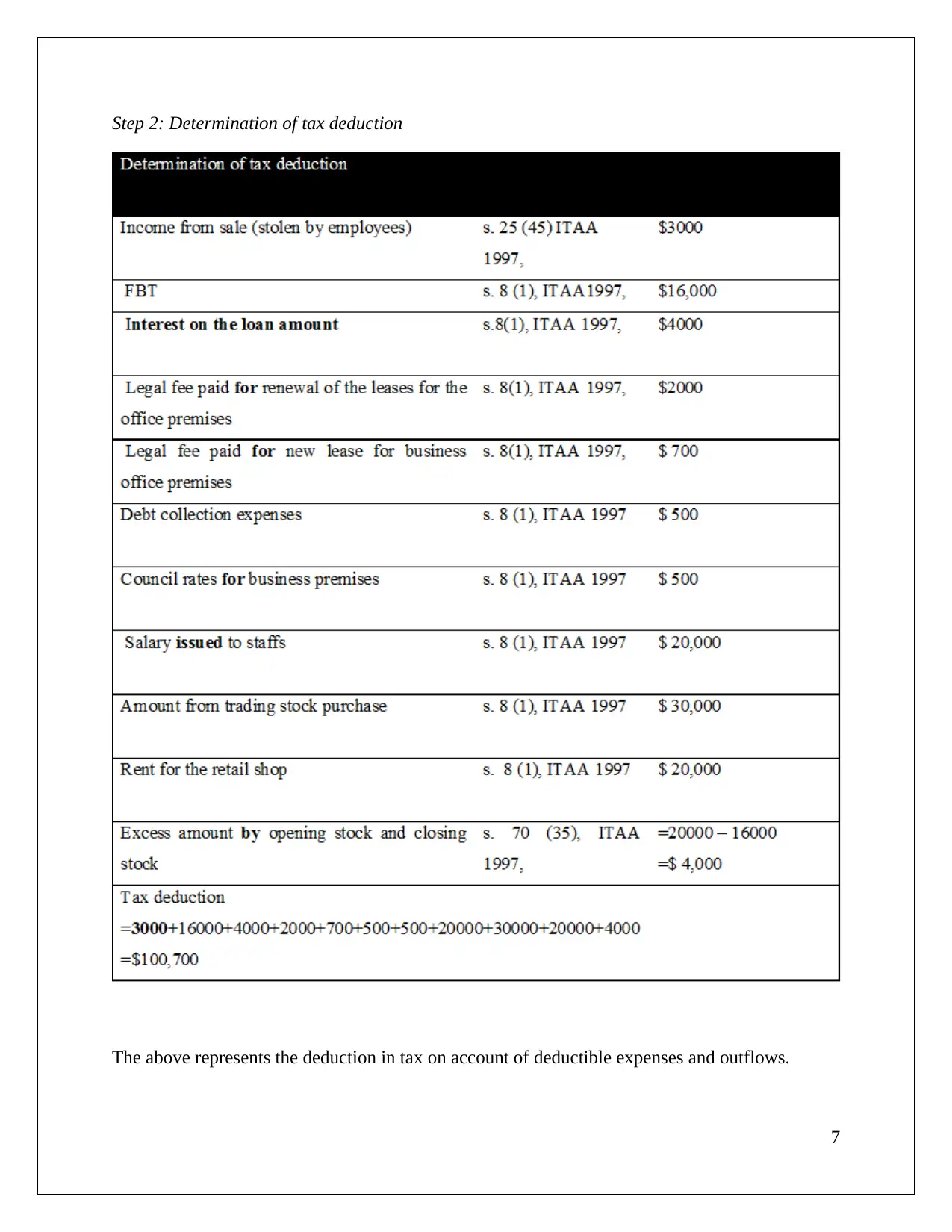

This assignment focuses on applying Australian taxation law principles to practical scenarios. It involves calculating the foreign tax offset for Angelo, who paid taxes to foreign authorities, and determining the net taxable income for a partnership firm by analyzing assessable income, deductible expenses, and outgoings. The solution provides step-by-step calculations and references relevant tax laws and guidelines.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

© 2024 | Zucol Services PVT LTD | All rights reserved.