HI5017 Managerial Accounting: Costing, Decisions & Article Review

VerifiedAdded on 2023/03/30

|18

|2985

|274

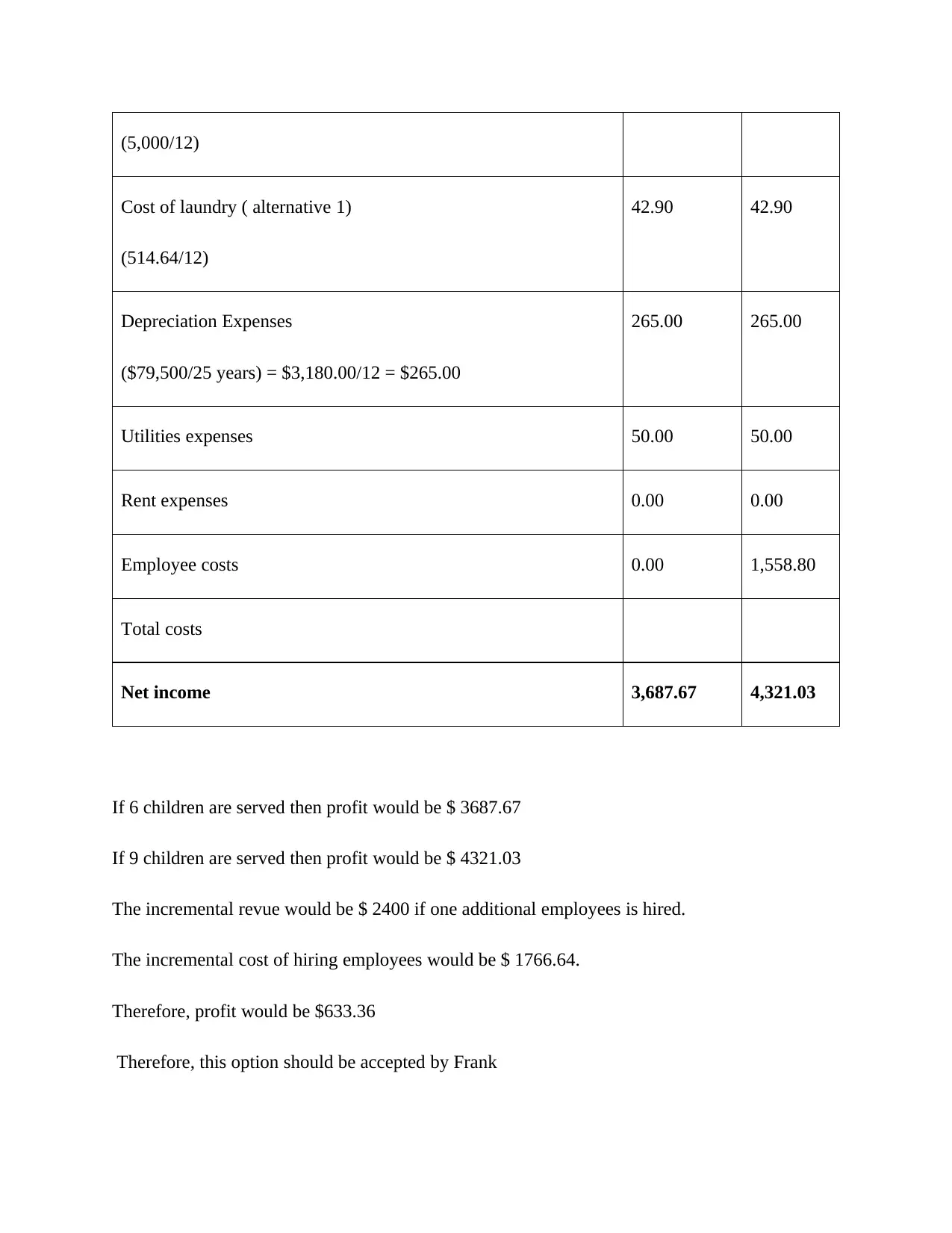

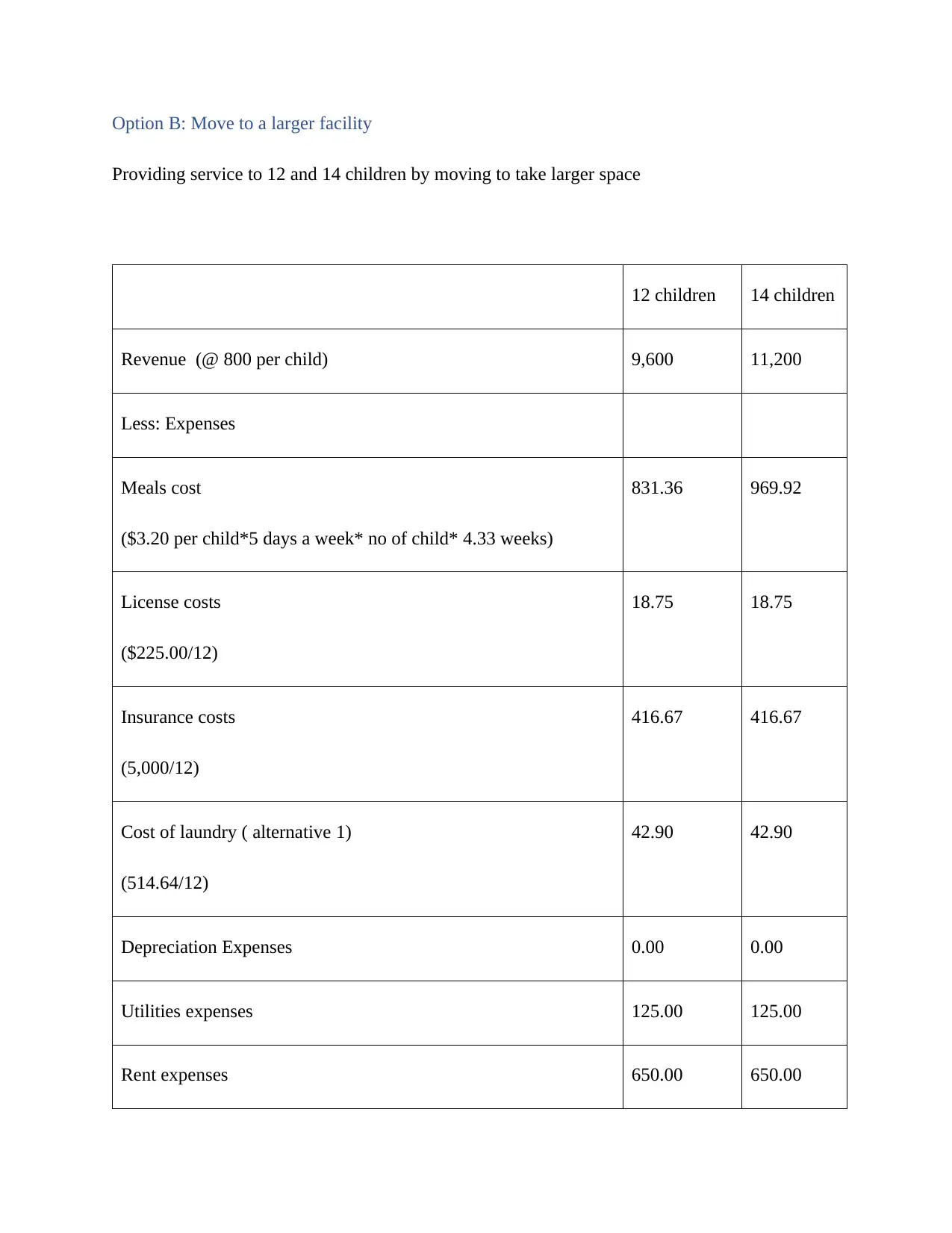

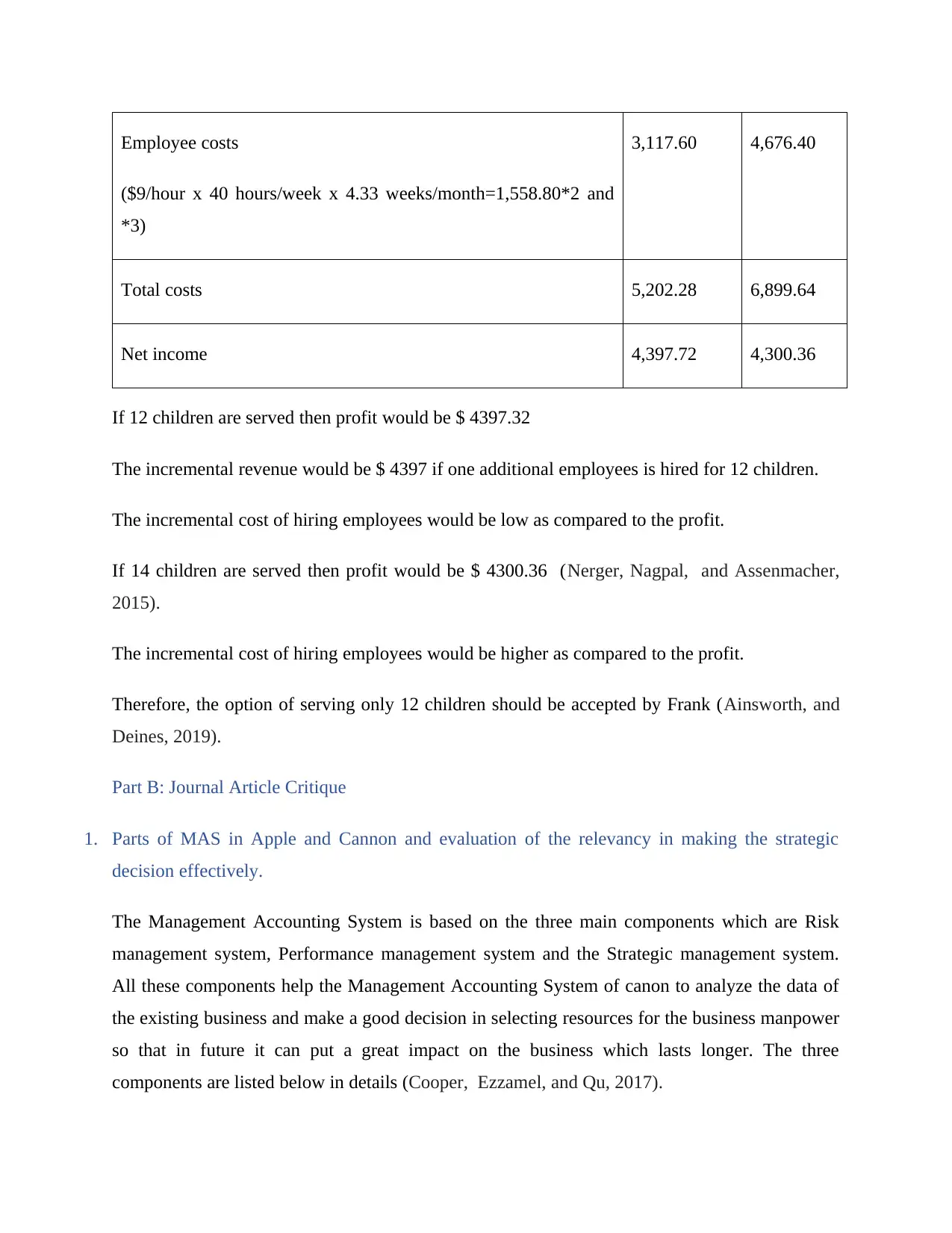

Case Study

AI Summary

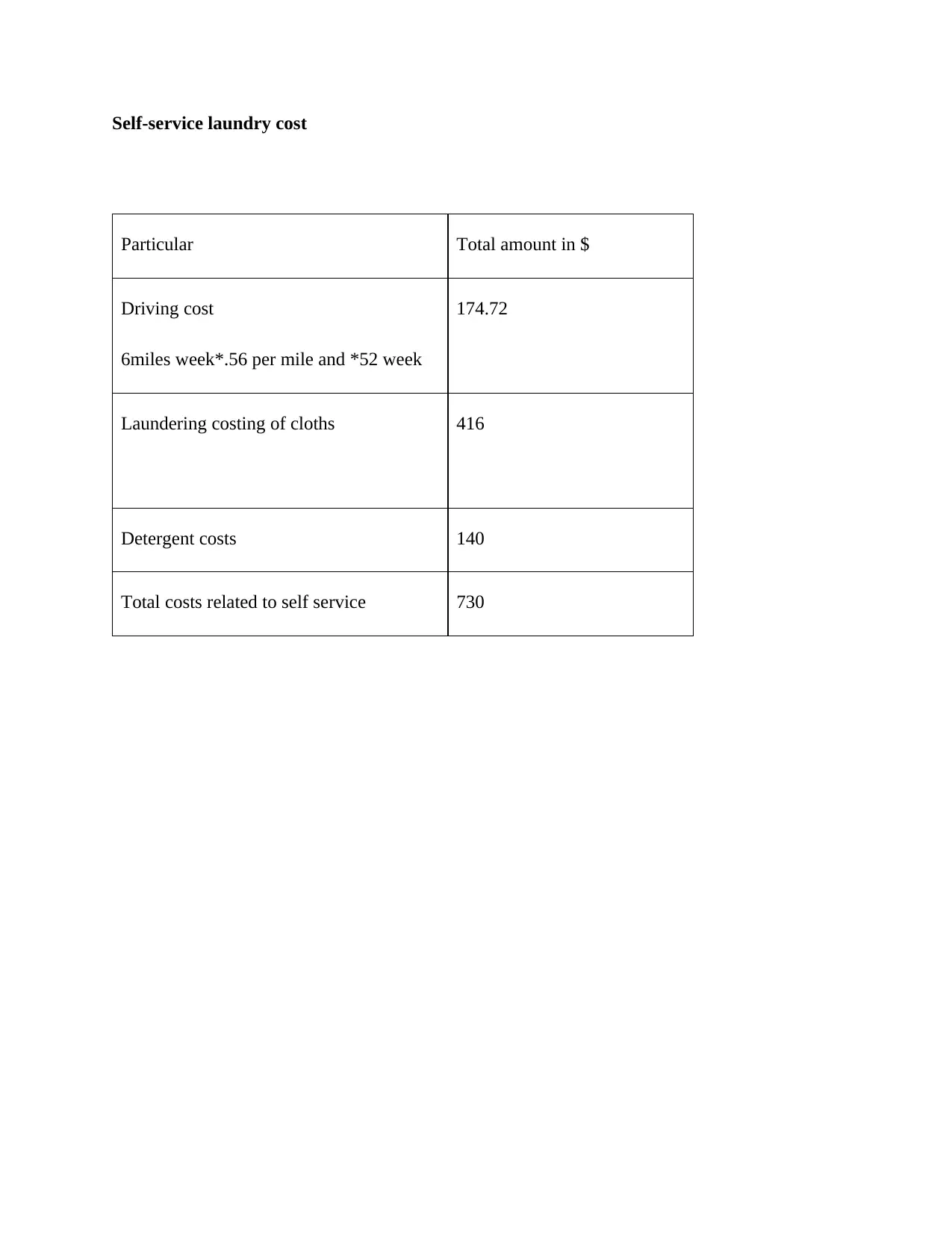

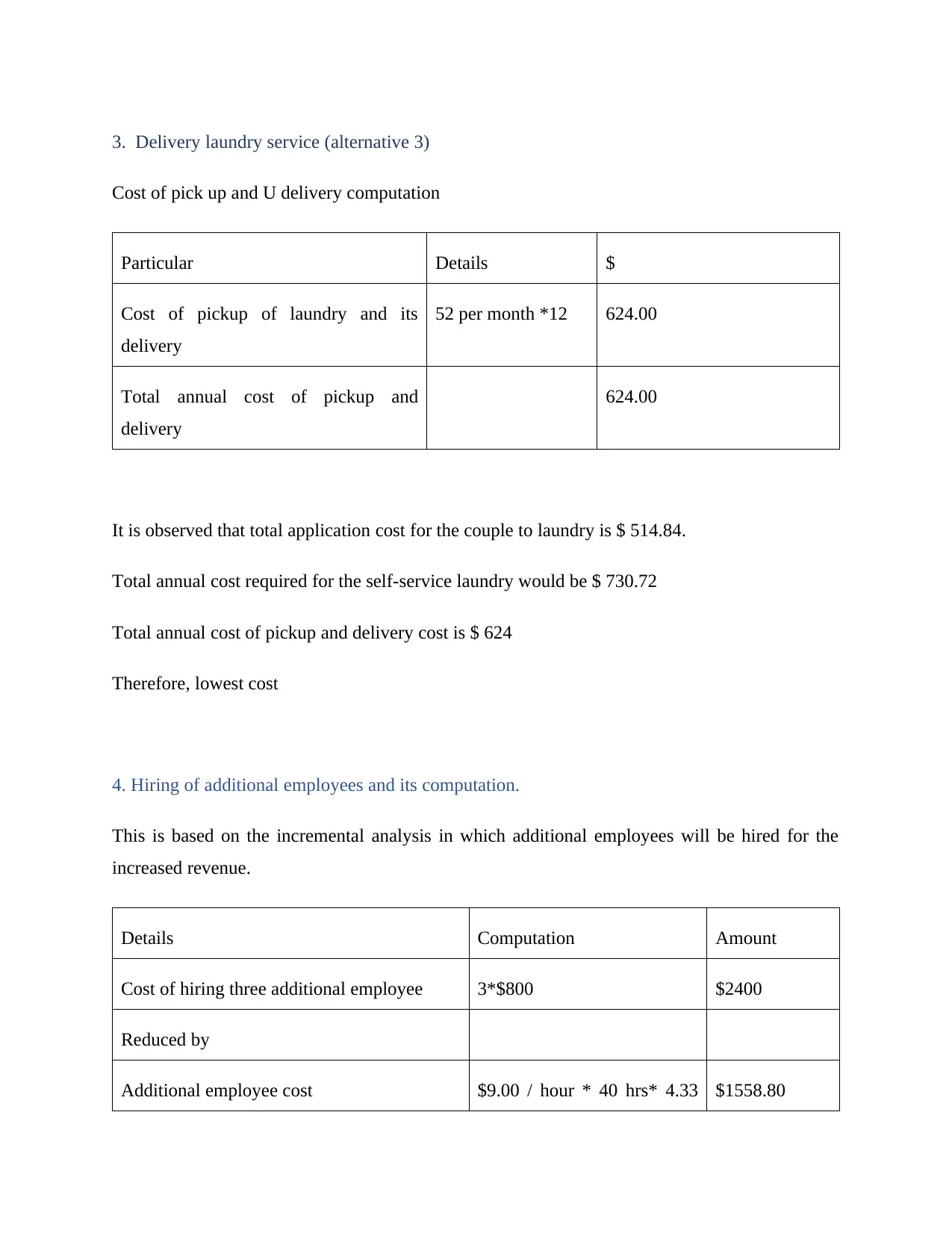

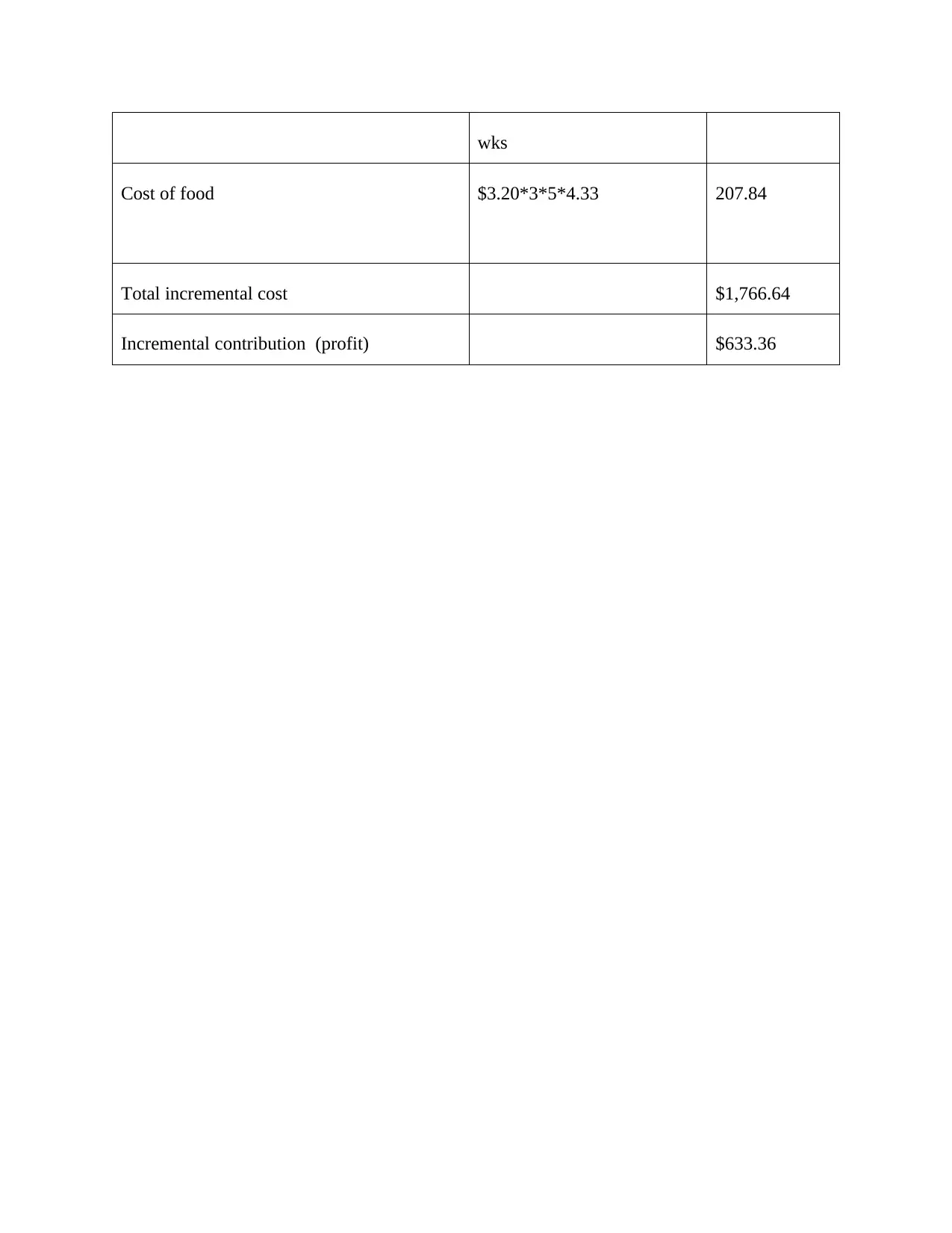

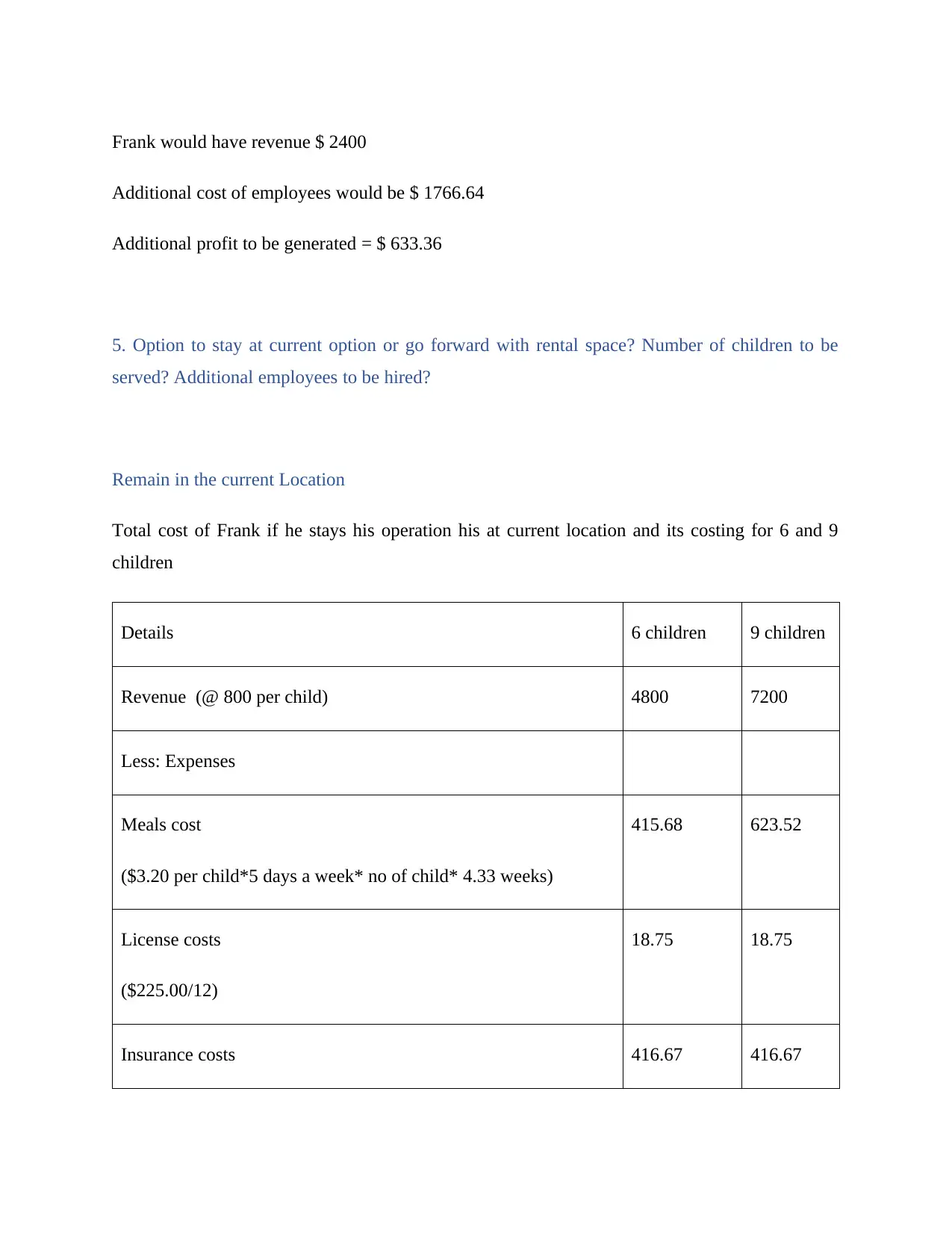

This assignment provides a comprehensive analysis of managerial accounting concepts through a case study and journal article critique. The case study involves cost analysis and decision-making for a hypothetical couple, evaluating different laundry options and business expansion scenarios, including hiring additional employees and assessing the profitability of serving varying numbers of children in a childcare setting. The analysis incorporates various costing methods such as fixed, variable, and incremental costs to determine optimal business strategies. The journal article critique examines the Management Accounting Systems (MAS) in Apple and Canon, evaluating their relevance in strategic decision-making and innovation processes. The critique also identifies lessons learned from the article and their implications for companies, focusing on innovation, information transmission, and the role of leadership accounting schemes in fostering innovation and achieving strategic objectives.

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.