HI5020 Corporate Accounting: Financial Statement Analysis of Peet Ltd

VerifiedAdded on 2024/06/03

|19

|2430

|71

Report

AI Summary

This report provides a detailed analysis of Peet Limited's financial performance, focusing on their cash flow statement, other comprehensive income statement, and corporate taxes. The analysis of the cash flow statement includes a breakdown of cash flows from operating, investing, and financing activities, with a comparative analysis of the years 2015, 2016, and 2017. The report also identifies items included in the other comprehensive income statement, such as realized and unrealized gains/losses on cash flow hedges, and explains why these items are not recorded directly in the income statement. Furthermore, it examines Peet Group Limited's tax expenses, deferred tax liabilities, and income tax payments, highlighting the differences between tax expenses and tax payables. The report concludes by reflecting on the challenges and insights gained during the analysis, including the surprising discrepancies in asset and liability valuation and the distinct treatment of tax expenses versus tax payments. Desklib offers a wealth of solved assignments and past papers for students seeking to deepen their understanding of corporate accounting.

HI5020 Corporate Accounting

1

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

Introduction.................................................................................................................................................3

Cash Flow Statement...................................................................................................................................4

Other Comprehensive Income Statement....................................................................................................7

Corporate Taxes..........................................................................................................................................8

Conclusion.................................................................................................................................................10

Bibliography...............................................................................................................................................11

Appendix...................................................................................................................................................12

2

Introduction.................................................................................................................................................3

Cash Flow Statement...................................................................................................................................4

Other Comprehensive Income Statement....................................................................................................7

Corporate Taxes..........................................................................................................................................8

Conclusion.................................................................................................................................................10

Bibliography...............................................................................................................................................11

Appendix...................................................................................................................................................12

2

Introduction

The main aim of the report is to analyze the financial performance of the organization and gain

the knowledge about the financial statements that how the transactions are recorded and what are

its implications. With this the various items which are recorded in the cash flow statement are

also determined and the understanding about the each item is also depicted. The various types of

the taxes which are used by the organizations are also examined so that the practical knowledge

about the treatment of the taxes can be gained. Peet Limited is taken for the analysis of the

overall report. Peet Limited is the organization who is operating in Australian real estate market.

It was founded in 1895 and the headquarters are based on Perth, Australia. The basic areas where

the Peet operates are the development of land for building new houses, the development of the

town houses and commercial real estate development.

3

The main aim of the report is to analyze the financial performance of the organization and gain

the knowledge about the financial statements that how the transactions are recorded and what are

its implications. With this the various items which are recorded in the cash flow statement are

also determined and the understanding about the each item is also depicted. The various types of

the taxes which are used by the organizations are also examined so that the practical knowledge

about the treatment of the taxes can be gained. Peet Limited is taken for the analysis of the

overall report. Peet Limited is the organization who is operating in Australian real estate market.

It was founded in 1895 and the headquarters are based on Perth, Australia. The basic areas where

the Peet operates are the development of land for building new houses, the development of the

town houses and commercial real estate development.

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Cash Flow Statement

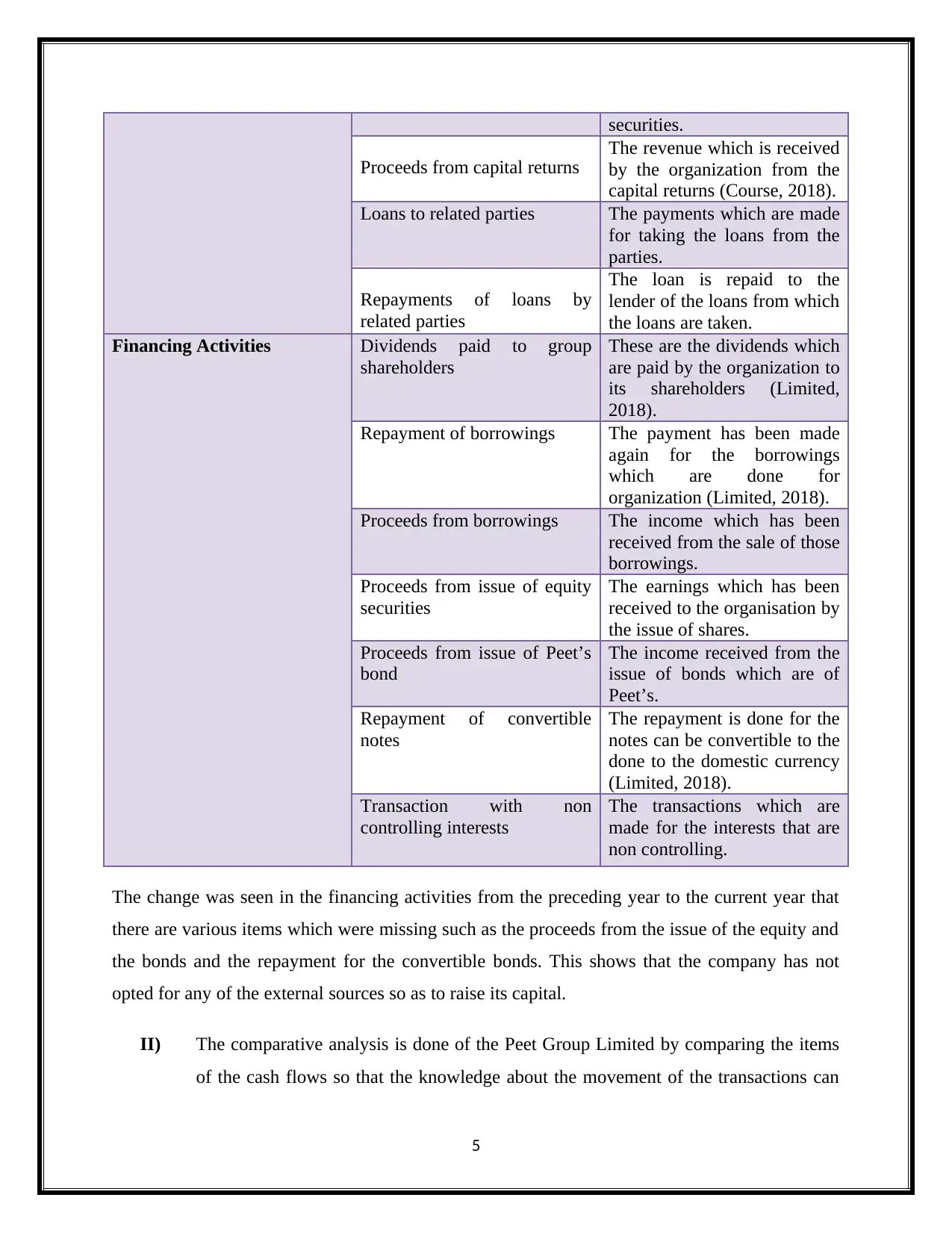

I) The cash flows statement shows all the transactions that impact the movement of the

cash in the economy. There are various items that may impact the inflow and the

outflow of the cash in economy such as:

Cash Flows From Items Description

Operating Activities Receipts from customers These are the receipts which

are received from the

customers for the purchase of

materials.

Payments to suppliers and

employees

The payment to the employees

is the salaries to the

employees for their

contribution and payment are

also made to the suppliers for

acquiring the products

(Kennon, 2018).

Payment of purchase of land The payment which is made

by the organization so as to

purchase the land.

Interest and other finance cost

paid

It is the amount which is

charged for and of the funds

which are taken as the lent.

Distribution of dividends

received from associates and

joint ventures

The dividend which is

received is distributed to the

shareholders of the

organization (Course, 2018).

Interest Received It is the amount that has been

earned by the organization but

yet to be received in the form

of cash.

Income tax paid The taxes which are paid

every year according to the

taxation rules.

Investing Activities Payments for property, plant

and equipments

The payments made by the

organization for purchasing

the property, equipments and

the plant (Merritt, 2018).

Payments for investments in

associates

The payments made for

purchasing the financial

4

I) The cash flows statement shows all the transactions that impact the movement of the

cash in the economy. There are various items that may impact the inflow and the

outflow of the cash in economy such as:

Cash Flows From Items Description

Operating Activities Receipts from customers These are the receipts which

are received from the

customers for the purchase of

materials.

Payments to suppliers and

employees

The payment to the employees

is the salaries to the

employees for their

contribution and payment are

also made to the suppliers for

acquiring the products

(Kennon, 2018).

Payment of purchase of land The payment which is made

by the organization so as to

purchase the land.

Interest and other finance cost

paid

It is the amount which is

charged for and of the funds

which are taken as the lent.

Distribution of dividends

received from associates and

joint ventures

The dividend which is

received is distributed to the

shareholders of the

organization (Course, 2018).

Interest Received It is the amount that has been

earned by the organization but

yet to be received in the form

of cash.

Income tax paid The taxes which are paid

every year according to the

taxation rules.

Investing Activities Payments for property, plant

and equipments

The payments made by the

organization for purchasing

the property, equipments and

the plant (Merritt, 2018).

Payments for investments in

associates

The payments made for

purchasing the financial

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

securities.

Proceeds from capital returns

The revenue which is received

by the organization from the

capital returns (Course, 2018).

Loans to related parties The payments which are made

for taking the loans from the

parties.

Repayments of loans by

related parties

The loan is repaid to the

lender of the loans from which

the loans are taken.

Financing Activities Dividends paid to group

shareholders

These are the dividends which

are paid by the organization to

its shareholders (Limited,

2018).

Repayment of borrowings The payment has been made

again for the borrowings

which are done for

organization (Limited, 2018).

Proceeds from borrowings The income which has been

received from the sale of those

borrowings.

Proceeds from issue of equity

securities

The earnings which has been

received to the organisation by

the issue of shares.

Proceeds from issue of Peet’s

bond

The income received from the

issue of bonds which are of

Peet’s.

Repayment of convertible

notes

The repayment is done for the

notes can be convertible to the

done to the domestic currency

(Limited, 2018).

Transaction with non

controlling interests

The transactions which are

made for the interests that are

non controlling.

The change was seen in the financing activities from the preceding year to the current year that

there are various items which were missing such as the proceeds from the issue of the equity and

the bonds and the repayment for the convertible bonds. This shows that the company has not

opted for any of the external sources so as to raise its capital.

II) The comparative analysis is done of the Peet Group Limited by comparing the items

of the cash flows so that the knowledge about the movement of the transactions can

5

Proceeds from capital returns

The revenue which is received

by the organization from the

capital returns (Course, 2018).

Loans to related parties The payments which are made

for taking the loans from the

parties.

Repayments of loans by

related parties

The loan is repaid to the

lender of the loans from which

the loans are taken.

Financing Activities Dividends paid to group

shareholders

These are the dividends which

are paid by the organization to

its shareholders (Limited,

2018).

Repayment of borrowings The payment has been made

again for the borrowings

which are done for

organization (Limited, 2018).

Proceeds from borrowings The income which has been

received from the sale of those

borrowings.

Proceeds from issue of equity

securities

The earnings which has been

received to the organisation by

the issue of shares.

Proceeds from issue of Peet’s

bond

The income received from the

issue of bonds which are of

Peet’s.

Repayment of convertible

notes

The repayment is done for the

notes can be convertible to the

done to the domestic currency

(Limited, 2018).

Transaction with non

controlling interests

The transactions which are

made for the interests that are

non controlling.

The change was seen in the financing activities from the preceding year to the current year that

there are various items which were missing such as the proceeds from the issue of the equity and

the bonds and the repayment for the convertible bonds. This shows that the company has not

opted for any of the external sources so as to raise its capital.

II) The comparative analysis is done of the Peet Group Limited by comparing the items

of the cash flows so that the knowledge about the movement of the transactions can

5

be gained (Kennon, 2018). For the practical implementation the annual report of 2016

and the 2017 has been considered.

It can be evaluated that the operating activities of the organization in 2015 was $113300

which decreased in 2016 and was $17235 and it has increased in 2017 which amounted to be

$57227. So, it can be said that the company has various sources through which the operations

of the organization can go accordingly (Limited, 2018). When the analysis of the investing

activities was done it can be analyzed that the returns from the investment in 2015 was $ -

51699 and in 2016 it was $9027 and in 2017 as $1488 which shows that the results were

gained good in 2016 from last 3 years. The amount f the financing activities was $42661 in

2015 while in 2016 as $8012 and in 2017 it amounted to be -$40475 so it can be said that the

organization is much dependent upon the external sources for its daily operations (Limited,

2018).

6

and the 2017 has been considered.

It can be evaluated that the operating activities of the organization in 2015 was $113300

which decreased in 2016 and was $17235 and it has increased in 2017 which amounted to be

$57227. So, it can be said that the company has various sources through which the operations

of the organization can go accordingly (Limited, 2018). When the analysis of the investing

activities was done it can be analyzed that the returns from the investment in 2015 was $ -

51699 and in 2016 it was $9027 and in 2017 as $1488 which shows that the results were

gained good in 2016 from last 3 years. The amount f the financing activities was $42661 in

2015 while in 2016 as $8012 and in 2017 it amounted to be -$40475 so it can be said that the

organization is much dependent upon the external sources for its daily operations (Limited,

2018).

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Other Comprehensive Income Statement

III) The items included in the other comprehensive income statement of the Peet Group

Limited are as follows:

Realized losses on cash flow hedges transferred to profit and loss

Unrealized gains/loss on cash flow hedges

Share of other comprehensive income of associates

Income tax relating to the components of other comprehensive income

IV) The other comprehensive income statement includes the various items in the annual

reports and all the items carry its own merits and demerits (Petro, 2014).

Realized losses on cash flow hedges: These are losses which have been occurred in the

hedges of the cash flows and they are transferred to that of the profit and loss accounts.

Unrealized gains/loss on the cash flow hedges: These are the gains or the losses which

have been incurred by the organization on the cash flow hedges and are yet to be realized

(Limited, 2018).

Share of other comprehensive income of associates: It is the shares of the associates which

are not realized till the accounting period are reported in this statement.

Income tax related to other income: These are the income taxes which are paid by the

organization and are related to the other income than the income reported in the income

statement of the organization (Limited, 2018).

V) The items which are recorded in the other comprehensive income statement cannot be

recorded in the income statement as these are the values of the organization or the

transactions which were not realized when the financial accounts were closing so

these are stated in the other comprehensive income statement other than the income

statement (Kennon, 2018). Once these items will be realized they will be reported in

the income statement but not of the current period but will be in the next year so that

the balance can be maintained as well as the transparency can be achieved in the

financial statements of the organization (Petro, 2014).

7

III) The items included in the other comprehensive income statement of the Peet Group

Limited are as follows:

Realized losses on cash flow hedges transferred to profit and loss

Unrealized gains/loss on cash flow hedges

Share of other comprehensive income of associates

Income tax relating to the components of other comprehensive income

IV) The other comprehensive income statement includes the various items in the annual

reports and all the items carry its own merits and demerits (Petro, 2014).

Realized losses on cash flow hedges: These are losses which have been occurred in the

hedges of the cash flows and they are transferred to that of the profit and loss accounts.

Unrealized gains/loss on the cash flow hedges: These are the gains or the losses which

have been incurred by the organization on the cash flow hedges and are yet to be realized

(Limited, 2018).

Share of other comprehensive income of associates: It is the shares of the associates which

are not realized till the accounting period are reported in this statement.

Income tax related to other income: These are the income taxes which are paid by the

organization and are related to the other income than the income reported in the income

statement of the organization (Limited, 2018).

V) The items which are recorded in the other comprehensive income statement cannot be

recorded in the income statement as these are the values of the organization or the

transactions which were not realized when the financial accounts were closing so

these are stated in the other comprehensive income statement other than the income

statement (Kennon, 2018). Once these items will be realized they will be reported in

the income statement but not of the current period but will be in the next year so that

the balance can be maintained as well as the transparency can be achieved in the

financial statements of the organization (Petro, 2014).

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Corporate Taxes

VI) The tax expense of the Peet Group Limited for the accounting period 2017 is $18163.

The tax expense is the expense which is reported in the corporate income statement as

the line item. It is the liabilities which is owned by the organization to the government

and are shown as the expenses in the financial statements of the organization (Petro,

2014).

VII) The amount of the tax expenses are not same as that of the tax rate times of the firm

as these are the rates which are shown in the financial accounts of the organization as

the taxes but these are those taxes which cannot be easily adaptable and acceptable

according to the various policies of the organization (Petro, 2014). The rate is termed

as the effective one when both organization as well as the individuals pays the taxes

according to the nominal rules and regulations determined by the government. So, it

can be said that the company does not reveals about the taxation rates applicable

within the organizational structure.

VIII) The company has recorded the deferred tax liabilities but not the deferred tax assets.

The amount of the deferred tax liability is $39698 (Limited, 2018). The deferred taxes

are recorded in the annual reports financial statements of the organization because

they show the differences which are temporary in nature for the rates of the taxes

which is applicable when the liabilities of the organisation are recovered and the

settlement of the assets are done by the organization (Merritt, 2018). The deferred tax

assets are recorded so as to set off the unused losses of the taxes and the authority for

the tax liability should be same for the particular period.

IX) Yes, the income tax is paid by the organization which is amounted to be $17952. The

income tax is the tax liability which has to be paid by every individual from its

income earned (Kimball, 2018). The amount of the tax payable is not same as that of

the tax expenses as the income tax payables are the legal responsibilities on the

individuals which have to be paid irrespective of the nature that the company is

earning profits or incurring losses. While the tax expenses are also the liability but in

the organisation it is treated as the earnings of the organisation (Course, 2018). The

income tax payables are calculated by the taxation rules while the tax expenses are

8

VI) The tax expense of the Peet Group Limited for the accounting period 2017 is $18163.

The tax expense is the expense which is reported in the corporate income statement as

the line item. It is the liabilities which is owned by the organization to the government

and are shown as the expenses in the financial statements of the organization (Petro,

2014).

VII) The amount of the tax expenses are not same as that of the tax rate times of the firm

as these are the rates which are shown in the financial accounts of the organization as

the taxes but these are those taxes which cannot be easily adaptable and acceptable

according to the various policies of the organization (Petro, 2014). The rate is termed

as the effective one when both organization as well as the individuals pays the taxes

according to the nominal rules and regulations determined by the government. So, it

can be said that the company does not reveals about the taxation rates applicable

within the organizational structure.

VIII) The company has recorded the deferred tax liabilities but not the deferred tax assets.

The amount of the deferred tax liability is $39698 (Limited, 2018). The deferred taxes

are recorded in the annual reports financial statements of the organization because

they show the differences which are temporary in nature for the rates of the taxes

which is applicable when the liabilities of the organisation are recovered and the

settlement of the assets are done by the organization (Merritt, 2018). The deferred tax

assets are recorded so as to set off the unused losses of the taxes and the authority for

the tax liability should be same for the particular period.

IX) Yes, the income tax is paid by the organization which is amounted to be $17952. The

income tax is the tax liability which has to be paid by every individual from its

income earned (Kimball, 2018). The amount of the tax payable is not same as that of

the tax expenses as the income tax payables are the legal responsibilities on the

individuals which have to be paid irrespective of the nature that the company is

earning profits or incurring losses. While the tax expenses are also the liability but in

the organisation it is treated as the earnings of the organisation (Course, 2018). The

income tax payables are calculated by the taxation rules while the tax expenses are

8

according to the accounting standards so the difference between the two can be seen

and recorded separately in the different statement.

X) No, the tax expenses which are recorded in the income statement is not same as that

of the income tax payables which are recorded in the cash flow statements of the

organisation (Kimball, 2018). There is the reason behind the same that as stated

earlier that the organisations treats the income tax expense as the income for the

organisation but the payables are the responsibilities which are legal in nature so the

difference in their treatment occurs. The differences occur as they are various

statutory provisions due to which the amounts cannot be recorded equally in the

statements. The payment of the taxes is recorded in cash flow as this statement shows

the proper way through which the cash transactions of the organization can be

maintained and utilized (Kennon, 2018).

XI) While evaluating the treatment of the taxes in the report there were surprising as well

as the difficulties which were faced. The surprising was that the value for the

realization of the assets as well as the liabilities is not recorded by the organisation

while evaluating the amount of foreign exchange translation. The Peet Group Limited

also recorded the deferred tax liabilities but the value of the deferred tax assets were

not recorded by the organisaton (Kennon, 2018). With that the amount of the

operating activities included the GST amount but the GST paid was not separately

shown in the cash flow statement of the organization (Kimball, 2018). The difficulty

which was faced was that there are various taxes which were paid by the organisation

so while doing the evaluation there were the complexities which were faced. With

this it also gave the new insight that the profitability of the organisation can be

identified from the comprehensive statement of the incomes and the costs (Kennon,

2018). With that the treatment of the tax expenses and the tax paid are different was

also one of the new insight that was gained from the treatment of the taxes (Course,

2018).

9

and recorded separately in the different statement.

X) No, the tax expenses which are recorded in the income statement is not same as that

of the income tax payables which are recorded in the cash flow statements of the

organisation (Kimball, 2018). There is the reason behind the same that as stated

earlier that the organisations treats the income tax expense as the income for the

organisation but the payables are the responsibilities which are legal in nature so the

difference in their treatment occurs. The differences occur as they are various

statutory provisions due to which the amounts cannot be recorded equally in the

statements. The payment of the taxes is recorded in cash flow as this statement shows

the proper way through which the cash transactions of the organization can be

maintained and utilized (Kennon, 2018).

XI) While evaluating the treatment of the taxes in the report there were surprising as well

as the difficulties which were faced. The surprising was that the value for the

realization of the assets as well as the liabilities is not recorded by the organisation

while evaluating the amount of foreign exchange translation. The Peet Group Limited

also recorded the deferred tax liabilities but the value of the deferred tax assets were

not recorded by the organisaton (Kennon, 2018). With that the amount of the

operating activities included the GST amount but the GST paid was not separately

shown in the cash flow statement of the organization (Kimball, 2018). The difficulty

which was faced was that there are various taxes which were paid by the organisation

so while doing the evaluation there were the complexities which were faced. With

this it also gave the new insight that the profitability of the organisation can be

identified from the comprehensive statement of the incomes and the costs (Kennon,

2018). With that the treatment of the tax expenses and the tax paid are different was

also one of the new insight that was gained from the treatment of the taxes (Course,

2018).

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Conclusion

From the above discussion it can be concluded that the corporate pay various types of taxes but

the treatment and importance of all the taxes are different. There was fluctuations which were

seen in the cash flow statement of the Peet Group Limited but the organisation has enough

sources as it is raising its capital from external sources. The other comprehensive income

statement includes the values which are not yet realized and the corporate taxes are evaluated

which gave the better understanding about the treatment and the allocation of various taxes

within the organisation. Hence, it can be stated that the overall organization maintained the

transparency in their financial accounts so that the profitability can be achieved.

10

From the above discussion it can be concluded that the corporate pay various types of taxes but

the treatment and importance of all the taxes are different. There was fluctuations which were

seen in the cash flow statement of the Peet Group Limited but the organisation has enough

sources as it is raising its capital from external sources. The other comprehensive income

statement includes the values which are not yet realized and the corporate taxes are evaluated

which gave the better understanding about the treatment and the allocation of various taxes

within the organisation. Hence, it can be stated that the overall organization maintained the

transparency in their financial accounts so that the profitability can be achieved.

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Bibliography

Course, A. (2018). What are Financing Activities. Accounting Course .

Kennon, J. (2018). Interest and Expense on the Income Statement. The Balance .

Kimball, T. (2018). Payroll Tax Expense vs. Payroll Tax Payable. Chron .

Limited, P. (2018). Financial Reports. Peet Limited .

Merritt, C. (2018). Tax Payable vs. Deferred Income Tax Liability. Chron .

Petro, F. G. (2014). A Logical Approach to the statement of cash flows. American

Journal Of Business Education .

11

Course, A. (2018). What are Financing Activities. Accounting Course .

Kennon, J. (2018). Interest and Expense on the Income Statement. The Balance .

Kimball, T. (2018). Payroll Tax Expense vs. Payroll Tax Payable. Chron .

Limited, P. (2018). Financial Reports. Peet Limited .

Merritt, C. (2018). Tax Payable vs. Deferred Income Tax Liability. Chron .

Petro, F. G. (2014). A Logical Approach to the statement of cash flows. American

Journal Of Business Education .

11

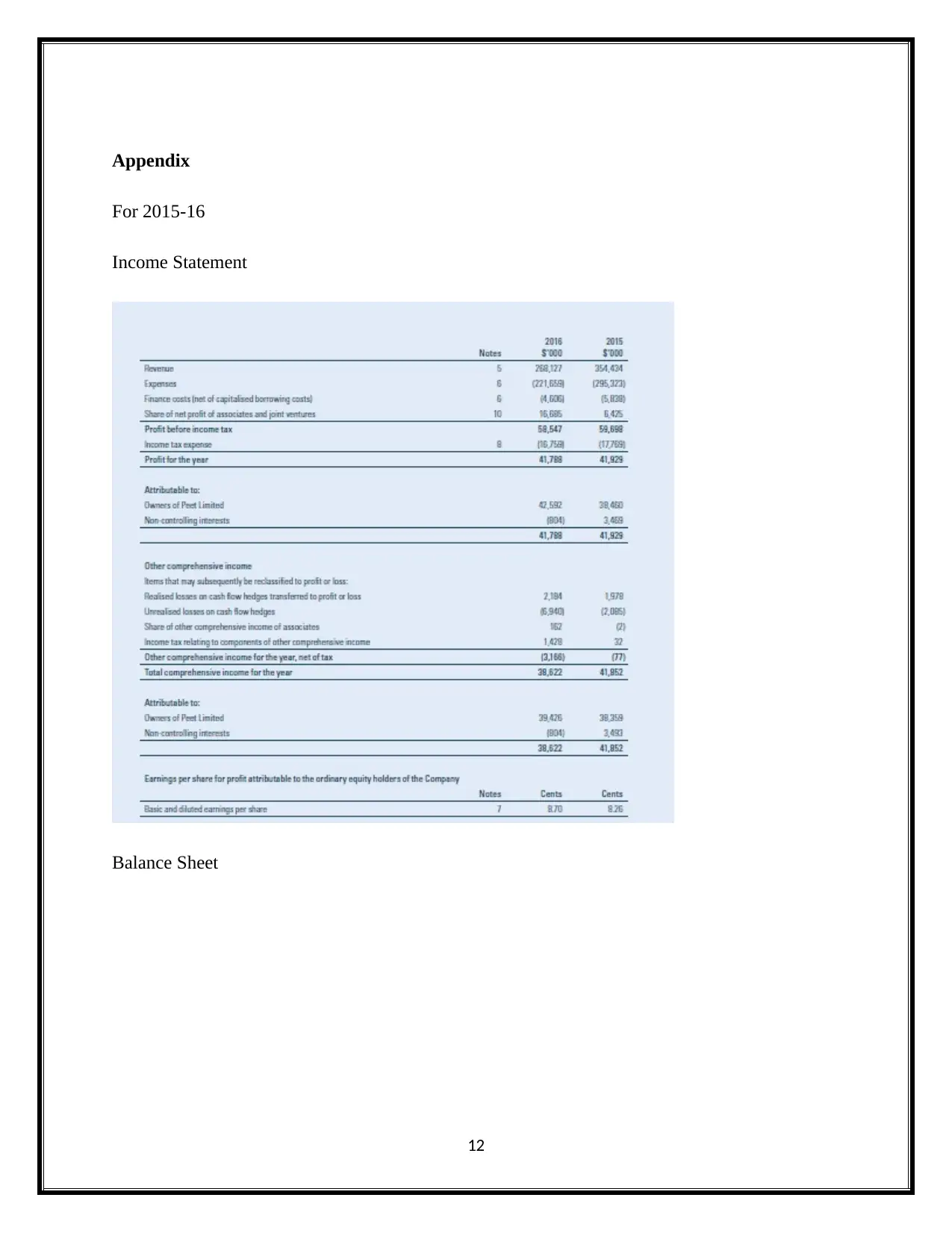

Appendix

For 2015-16

Income Statement

Balance Sheet

12

For 2015-16

Income Statement

Balance Sheet

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.