HI6025: A Report on the Implication of International Accounting

VerifiedAdded on 2024/05/31

|12

|2119

|398

Report

AI Summary

This report provides an overview of the implications of adopting International Financial Reporting Standards (IFRS) in Australia, focusing on the changes required for ASX-listed companies. It addresses the differences between Australian GAAP and IFRS, highlighting key policy changes in areas such as employee benefits, income tax, property, contingent liabilities, and financial instruments. The report examines the impact of IFRS on financial reporting, revenue recognition, and the valuation of assets and liabilities, emphasizing the need for Australian firms to adapt to international accounting standards for comparable financial information. It concludes that the transition to IFRS has made Australian companies more flexible and accountable, enabling them to better align with global financial reporting methodologies. The report references various studies and regulatory changes to support its analysis of the adaptability and implications of IFRS in the Australian business environment.

HI6025 Implication of International Accounting

1

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

1. Executive Summary:.........................................................................................................3

2. Implication of International Accounting Standards:.............................................................4

3. IFRS Policies changes:......................................................................................................5

Conclusion:..........................................................................................................................9

References:......................................................................................................................10

Appendix:.........................................................................................................................11

2

1. Executive Summary:.........................................................................................................3

2. Implication of International Accounting Standards:.............................................................4

3. IFRS Policies changes:......................................................................................................5

Conclusion:..........................................................................................................................9

References:......................................................................................................................10

Appendix:.........................................................................................................................11

2

1. Executive Summary:

The Australian Commission has needed to adopt IAS or IFRS in order to measure and harmonise

accounting and international financial reporting regulations and standards for ASX listed

companies as of 31 Dec 2005. Converting to IFRS and international accounting has indicated

much more than accounting changes, rules, laws and firms major concern was to understand the

corporate governance and accounting differences between Australian GAAP and IFRS in the

concern of IFRS and accounting standards. The purpose of this reading is to address such

mentioned above concern by producing and identifying empirical evidence of various features of

Australian accounting policies and IFRS in the context of Australian accounting standards.

Overall findings represent more relevant and identical process and impacts of international

accounting changes.

3

The Australian Commission has needed to adopt IAS or IFRS in order to measure and harmonise

accounting and international financial reporting regulations and standards for ASX listed

companies as of 31 Dec 2005. Converting to IFRS and international accounting has indicated

much more than accounting changes, rules, laws and firms major concern was to understand the

corporate governance and accounting differences between Australian GAAP and IFRS in the

concern of IFRS and accounting standards. The purpose of this reading is to address such

mentioned above concern by producing and identifying empirical evidence of various features of

Australian accounting policies and IFRS in the context of Australian accounting standards.

Overall findings represent more relevant and identical process and impacts of international

accounting changes.

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

2. Implication of International Accounting Standards:

The IAS/IFRS is an International Accounting Standards/International Financial Reporting

Standards) which is consisted of all sets of accounting principles and regulations in an

international manner. The adaptability of accounting laws aims and rules to establish accurate

and exact regulations within the Australian Union in order to draw up comparative and

competitive business transactions and annual reports and financial standards. Application of

international accounting standards represents an important and effective measurement of element

in the subject to describe and contain an effective and relevant Australian capital market, that

have impelled the Australian Commissions to address all sets of uniform accounting regulation

and international financial reporting standards for listed ASX companies (Firt & Gounopoulos,

2017).

The Australian Community Regulation has listed all the ASX companies under 1606.2002 in the

regulation of Australian Market to reform and regulate financial reporting standards for

producing and preparing financial consolidated statements as from December 31st, 2005. In

Australia. The Law Regulators had delegated the Government of Australia to implicate one or

more regulative and legislative laws and decrees interpreting all needs and requirements of AUS.

Regulations adopted by Australian firms within a year of the ruling coming into force.

At the beginning of the year 2003, ASX listed companies, banks and financial forces produce all

those interim and annual reports and consolidated financial reports accordingly with IAS/IFRS.

At the starting of international accounting standards in 2005, IFRS made changes into the

regulation of Cash flows, hedge recovery, adjustment and reclassification to reflect all

fluctuations of presentation, realisation and valuation of assets and liquidation required by IFRS

regulation. Such changes made compulsory or ASX listed companies, banks and financial

authorities from Dec 2005. Their adopted was also made compulsion for non-listed Companies

in form of both individual and comprehensive income statements (Firt & Gounopoulos, 2017).

4

The IAS/IFRS is an International Accounting Standards/International Financial Reporting

Standards) which is consisted of all sets of accounting principles and regulations in an

international manner. The adaptability of accounting laws aims and rules to establish accurate

and exact regulations within the Australian Union in order to draw up comparative and

competitive business transactions and annual reports and financial standards. Application of

international accounting standards represents an important and effective measurement of element

in the subject to describe and contain an effective and relevant Australian capital market, that

have impelled the Australian Commissions to address all sets of uniform accounting regulation

and international financial reporting standards for listed ASX companies (Firt & Gounopoulos,

2017).

The Australian Community Regulation has listed all the ASX companies under 1606.2002 in the

regulation of Australian Market to reform and regulate financial reporting standards for

producing and preparing financial consolidated statements as from December 31st, 2005. In

Australia. The Law Regulators had delegated the Government of Australia to implicate one or

more regulative and legislative laws and decrees interpreting all needs and requirements of AUS.

Regulations adopted by Australian firms within a year of the ruling coming into force.

At the beginning of the year 2003, ASX listed companies, banks and financial forces produce all

those interim and annual reports and consolidated financial reports accordingly with IAS/IFRS.

At the starting of international accounting standards in 2005, IFRS made changes into the

regulation of Cash flows, hedge recovery, adjustment and reclassification to reflect all

fluctuations of presentation, realisation and valuation of assets and liquidation required by IFRS

regulation. Such changes made compulsory or ASX listed companies, banks and financial

authorities from Dec 2005. Their adopted was also made compulsion for non-listed Companies

in form of both individual and comprehensive income statements (Firt & Gounopoulos, 2017).

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

3. IFRS Policies changes:

The changes in the transition of IAS/IFRS have meant to be fundamental and regulative changes

for many Australian and Non-listed companies. Conversion into accounting changes such as

changes in GAAP (Generally accepted accounting principles), accounting exercises has made

whole changes in financial reporting which have affected the perception of business performance

in the market. After changes in international accounting standards have made firm’s enabled to

prepare IFRS financial statement and annual report that allow them to implicate global financial

and accounting reporting methodologies and evaluated accounting facilities in the international

marketplace. IFRS and accounting standards have formulated and concerned to understand the

extent in order to define differences between prior accounting standards and after making

policies based on firms business and market performance. Such differences are emerging from

the adaptability of application of IAS/IFRS compared with Australian Accounting principles

affecting various accounting areas such as leasing, financial reporting, revenue recognition and

recognition & valuation of deferred taxes and port retirement accounting benefits (Jouber, et. al.,

2017).

The regulatory changes in international accounting has addressed regulation and by the adoption

of IAS/IFRS in Australian Financial statement. Australian firms have not shifted the national

accounting regulation but also revisited the question regarding reflection the importance of IFRS

and determining financial reporting outcomes. It has also created the application of overall

international convergence of accounting and financial principles and reporting. Australian firms

have also represented the comparable financial information with an effort of removing the

several differences between all accounting reporting and principles in order to the production of

two set of financial reports and regulation as closer as well as for preparation of comparable

financial information (Morris, 2017).

An overall study of IFRS changes defines possibilities of the implication of adaptability of IAS

and IFRS by looking at all potential influences of these accounting treatments and adjustments of

pooling accounting reports to make business position and performance more strong and effective.

Such analyses propose the implications of the application of IFRS schedule and principles which

shows why the companies should voluntarily decide to shift all set of accounting standards and

5

The changes in the transition of IAS/IFRS have meant to be fundamental and regulative changes

for many Australian and Non-listed companies. Conversion into accounting changes such as

changes in GAAP (Generally accepted accounting principles), accounting exercises has made

whole changes in financial reporting which have affected the perception of business performance

in the market. After changes in international accounting standards have made firm’s enabled to

prepare IFRS financial statement and annual report that allow them to implicate global financial

and accounting reporting methodologies and evaluated accounting facilities in the international

marketplace. IFRS and accounting standards have formulated and concerned to understand the

extent in order to define differences between prior accounting standards and after making

policies based on firms business and market performance. Such differences are emerging from

the adaptability of application of IAS/IFRS compared with Australian Accounting principles

affecting various accounting areas such as leasing, financial reporting, revenue recognition and

recognition & valuation of deferred taxes and port retirement accounting benefits (Jouber, et. al.,

2017).

The regulatory changes in international accounting has addressed regulation and by the adoption

of IAS/IFRS in Australian Financial statement. Australian firms have not shifted the national

accounting regulation but also revisited the question regarding reflection the importance of IFRS

and determining financial reporting outcomes. It has also created the application of overall

international convergence of accounting and financial principles and reporting. Australian firms

have also represented the comparable financial information with an effort of removing the

several differences between all accounting reporting and principles in order to the production of

two set of financial reports and regulation as closer as well as for preparation of comparable

financial information (Morris, 2017).

An overall study of IFRS changes defines possibilities of the implication of adaptability of IAS

and IFRS by looking at all potential influences of these accounting treatments and adjustments of

pooling accounting reports to make business position and performance more strong and effective.

Such analyses propose the implications of the application of IFRS schedule and principles which

shows why the companies should voluntarily decide to shift all set of accounting standards and

5

their characteristics of adopting non-listed companies as well as the significance of adaptability

of business firm’s performance (Cereola, et. al., 2017).

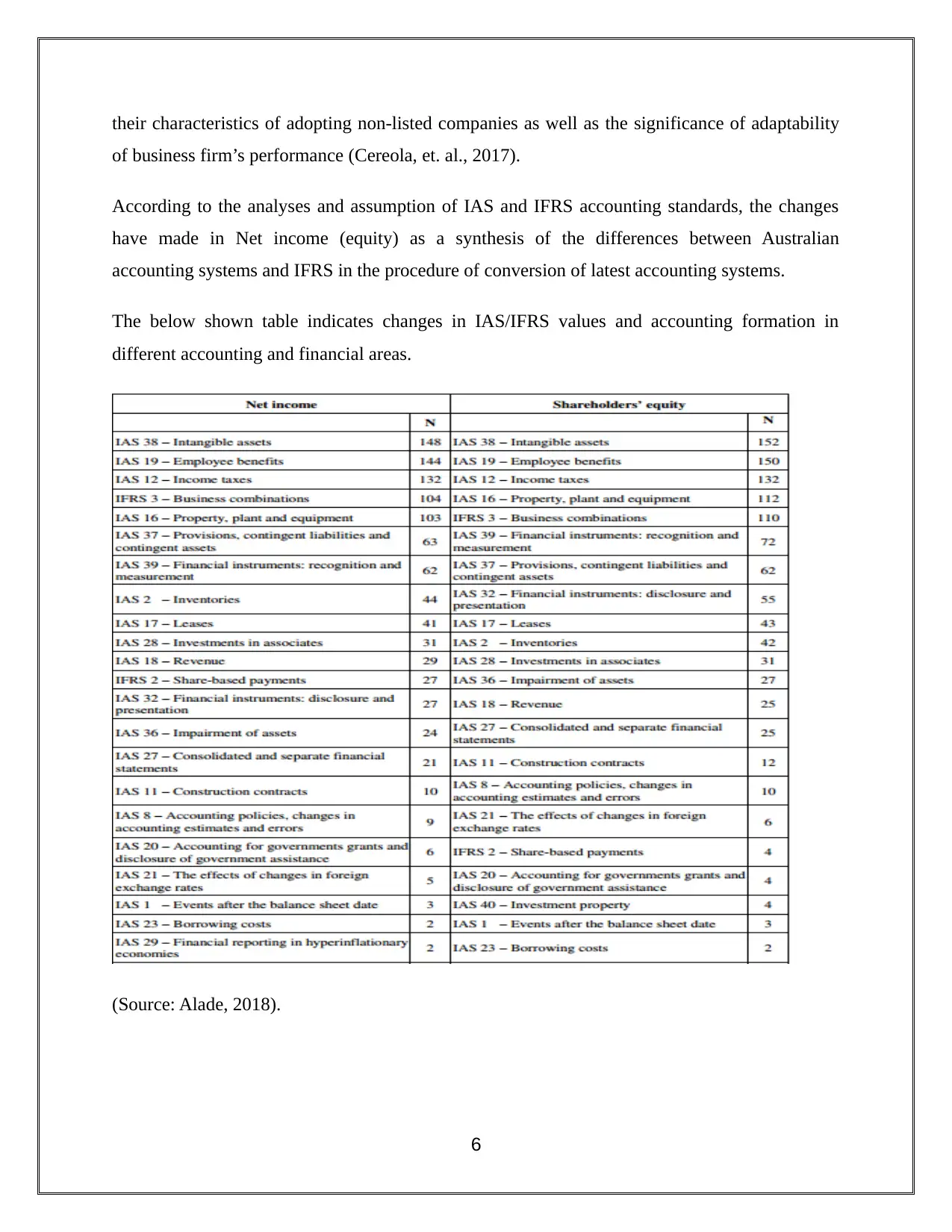

According to the analyses and assumption of IAS and IFRS accounting standards, the changes

have made in Net income (equity) as a synthesis of the differences between Australian

accounting systems and IFRS in the procedure of conversion of latest accounting systems.

The below shown table indicates changes in IAS/IFRS values and accounting formation in

different accounting and financial areas.

(Source: Alade, 2018).

6

of business firm’s performance (Cereola, et. al., 2017).

According to the analyses and assumption of IAS and IFRS accounting standards, the changes

have made in Net income (equity) as a synthesis of the differences between Australian

accounting systems and IFRS in the procedure of conversion of latest accounting systems.

The below shown table indicates changes in IAS/IFRS values and accounting formation in

different accounting and financial areas.

(Source: Alade, 2018).

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

IFRS 19-Employee benefit:

Australian GAAP requires the liability for it measurement for TFR(Reserve for employee

termination indemnity) to record all nominal value and to calculate as per the requirement of

civil and business accounting code. The gains and loss regulated and determined by actuarial

computation to recognise as revenue and profit in the financial statement of accounting value and

operations. The adjustment made related to measurement and recognition and indemnification of

new actuarial liabilities for the benefits and revenue associated with the Australian firms for the

employees. After changes in IFRS 19 regulation for employee’s benefits creates 0.62% equity

lower than another identity (Loyeung, et. al., 2016).

IFRS -12 Income Tax

Under Australian GAAP, deferred taxes can be valued as per assets and liabilities including

calculation of temporary differences between the book and fair value of all assets and liabilities

to compute taxable income. The adoption of IFRS 12 is not able to provide any special

computation to the accrual of all deferred tax liabilities (Bryce, et. al., 2015).

IFRS 16- Business property, plant and equipment:

Under GAAP and IFRS regulation, assets, property and plants can be valued at generally adopted

records and costing methods, corresponding to the all purchase price including direct variable

and fair of the property of bringing the property and assets over useful depreciated life and value

of assets. Under international GAAP, a most samples of financial statement of companies revalue

specific property plant and essential equipment of assets based on historical costs and required

all specific laws of Australian countries to relocate financial resources (Firt & Gounopoulos,

2017).

IFRS 37- Provision, contingent liabilities and assets:

Under Australian GAAP, the overall provision for contingent liabilities and contingent assets

concerns all cost and revenue can be charged to determine their value and nature, whose

determination and existence can be probably valued. When the financial impact of financial

7

Australian GAAP requires the liability for it measurement for TFR(Reserve for employee

termination indemnity) to record all nominal value and to calculate as per the requirement of

civil and business accounting code. The gains and loss regulated and determined by actuarial

computation to recognise as revenue and profit in the financial statement of accounting value and

operations. The adjustment made related to measurement and recognition and indemnification of

new actuarial liabilities for the benefits and revenue associated with the Australian firms for the

employees. After changes in IFRS 19 regulation for employee’s benefits creates 0.62% equity

lower than another identity (Loyeung, et. al., 2016).

IFRS -12 Income Tax

Under Australian GAAP, deferred taxes can be valued as per assets and liabilities including

calculation of temporary differences between the book and fair value of all assets and liabilities

to compute taxable income. The adoption of IFRS 12 is not able to provide any special

computation to the accrual of all deferred tax liabilities (Bryce, et. al., 2015).

IFRS 16- Business property, plant and equipment:

Under GAAP and IFRS regulation, assets, property and plants can be valued at generally adopted

records and costing methods, corresponding to the all purchase price including direct variable

and fair of the property of bringing the property and assets over useful depreciated life and value

of assets. Under international GAAP, a most samples of financial statement of companies revalue

specific property plant and essential equipment of assets based on historical costs and required

all specific laws of Australian countries to relocate financial resources (Firt & Gounopoulos,

2017).

IFRS 37- Provision, contingent liabilities and assets:

Under Australian GAAP, the overall provision for contingent liabilities and contingent assets

concerns all cost and revenue can be charged to determine their value and nature, whose

determination and existence can be probably valued. When the financial impact of financial

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

liability and assets can be determined by valid expectations in third parties, the provided amount

of assets and liabilities can be affected reasonably according to implicit obligations.

IFRS 39- Financial instrument: recognition and measurement:

The differences between Australian GAAP and IFRS accounting standards can be summarized

with the effect of instruments for GAAP defined as hedging and non-hedging activities in the

application of recognition and measurement of financial instruments.

IFRS 2- inventories:

According to the implication of accounting rules and condition as per Australian firms’ financial

statements, the companies determine the cost of inventories as per LIFO method but IFRS does

not allow to the valuation of inventories with the LIFO, it wants alternative valuation of FIFO

and weighted average method in order to make inventory process more flexible.

Above provide justification implicates and concludes that companies are able to adjust and

arrange all financial statements of the firms according to the treatment of IFRS policies and

procedures. Above given example of treatments and adjustments of assets and liabilities in

financial statements provide effective knowledge for the companies to initiate and adopt more

flexible policies of accounting treatments (Li, et. al., 2017).

8

of assets and liabilities can be affected reasonably according to implicit obligations.

IFRS 39- Financial instrument: recognition and measurement:

The differences between Australian GAAP and IFRS accounting standards can be summarized

with the effect of instruments for GAAP defined as hedging and non-hedging activities in the

application of recognition and measurement of financial instruments.

IFRS 2- inventories:

According to the implication of accounting rules and condition as per Australian firms’ financial

statements, the companies determine the cost of inventories as per LIFO method but IFRS does

not allow to the valuation of inventories with the LIFO, it wants alternative valuation of FIFO

and weighted average method in order to make inventory process more flexible.

Above provide justification implicates and concludes that companies are able to adjust and

arrange all financial statements of the firms according to the treatment of IFRS policies and

procedures. Above given example of treatments and adjustments of assets and liabilities in

financial statements provide effective knowledge for the companies to initiate and adopt more

flexible policies of accounting treatments (Li, et. al., 2017).

8

Conclusion:

The beginning year of 2005, the Australian companies and commission have required judging

and in initiate adaptability of IFRS process and policies in order to make business more flexible.

All transition to IFRS policies and international accounting standards has made firms more

flexible and accountable to cover differences between their primary and secondary needs. This

report has been made to describe accessibility and liability of the Australian firms and companies

whether they are ASX listed or non-listed. This report has also described set of standards which

are essential to be implicated in international accounting regulations and policies before making

mandatory policies requested by Australian commission.

9

The beginning year of 2005, the Australian companies and commission have required judging

and in initiate adaptability of IFRS process and policies in order to make business more flexible.

All transition to IFRS policies and international accounting standards has made firms more

flexible and accountable to cover differences between their primary and secondary needs. This

report has been made to describe accessibility and liability of the Australian firms and companies

whether they are ASX listed or non-listed. This report has also described set of standards which

are essential to be implicated in international accounting regulations and policies before making

mandatory policies requested by Australian commission.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

References:

1. Li, S., Sougiannis, T., & Wang, I. (2017). Mandatory IFRS Adoption and the Usefulness

of Accounting Information in Predicting Future Earnings and Cash Flows.

2. Firth, M., & Gounopoulos, D. (2017). IFRS adoption and management earnings forecasts

of Australian IPOs.

3. Cereola, S. J., Nichols, N. B., & Street, D. L. (2017). Geographic segment disclosures

under IFRS 8: Changes in materiality and fineness by European, Australian and New

Zealand blue chip companies. Research in Accounting Regulation, 29(2), 119-128.

4. Alade, M. E. (2018). Effect of International Financial Reporting Standards Adoption on

Value Relevance of Accounting Information of Nigerian Listed Firms (Doctoral

dissertation).

5. Scholten, R., Lambooy, T., Renes, R., & Bartels, W. (2017). Accounting for Future

Generations. Does the IFRS Framework Sufficiently Encourage Energy Companies to

Reflect on Climate Change in the Valuation of Their Production Assets, Taking into

Account the New Initiative of the Task Force on Climate-Related Financial Disclosures?

An Exploratory Qualitative Comparative Case Study Approach.

6. Joubert, M., Garvie, L., & Parle, G. (2017). Implications of the New Accounting Standard

for Leases AASB 16 (IFRS 16) with the Inclusion of Operating Leases in the Balance

Sheet. The Journal of New Business Ideas & Trends, 15(2), 1-11.

7. Bryce, M., Ali, M. J., & Mather, P. R. (2015). Accounting quality in the pre-/post-IFRS

adoption periods and the impact on audit committee effectiveness—Evidence from

Australia. Pacific-Basin Finance Journal, 35, 163-181.

8. Morris, R. D. (2017). Discussion of: The Phoenix Rises: The Australian Accounting

Standards Board and IFRS Adoption. Journal of International Accounting

Research, 16(2), 155-157.

9. Loyeung, A., Matolcsy, Z., Weber, J., & Wells, P. (2016). The cost of implementing new

accounting standards: The case of IFRS adoption in Australia. Australian Journal of

Management, 41(4), 611-632.

10

1. Li, S., Sougiannis, T., & Wang, I. (2017). Mandatory IFRS Adoption and the Usefulness

of Accounting Information in Predicting Future Earnings and Cash Flows.

2. Firth, M., & Gounopoulos, D. (2017). IFRS adoption and management earnings forecasts

of Australian IPOs.

3. Cereola, S. J., Nichols, N. B., & Street, D. L. (2017). Geographic segment disclosures

under IFRS 8: Changes in materiality and fineness by European, Australian and New

Zealand blue chip companies. Research in Accounting Regulation, 29(2), 119-128.

4. Alade, M. E. (2018). Effect of International Financial Reporting Standards Adoption on

Value Relevance of Accounting Information of Nigerian Listed Firms (Doctoral

dissertation).

5. Scholten, R., Lambooy, T., Renes, R., & Bartels, W. (2017). Accounting for Future

Generations. Does the IFRS Framework Sufficiently Encourage Energy Companies to

Reflect on Climate Change in the Valuation of Their Production Assets, Taking into

Account the New Initiative of the Task Force on Climate-Related Financial Disclosures?

An Exploratory Qualitative Comparative Case Study Approach.

6. Joubert, M., Garvie, L., & Parle, G. (2017). Implications of the New Accounting Standard

for Leases AASB 16 (IFRS 16) with the Inclusion of Operating Leases in the Balance

Sheet. The Journal of New Business Ideas & Trends, 15(2), 1-11.

7. Bryce, M., Ali, M. J., & Mather, P. R. (2015). Accounting quality in the pre-/post-IFRS

adoption periods and the impact on audit committee effectiveness—Evidence from

Australia. Pacific-Basin Finance Journal, 35, 163-181.

8. Morris, R. D. (2017). Discussion of: The Phoenix Rises: The Australian Accounting

Standards Board and IFRS Adoption. Journal of International Accounting

Research, 16(2), 155-157.

9. Loyeung, A., Matolcsy, Z., Weber, J., & Wells, P. (2016). The cost of implementing new

accounting standards: The case of IFRS adoption in Australia. Australian Journal of

Management, 41(4), 611-632.

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

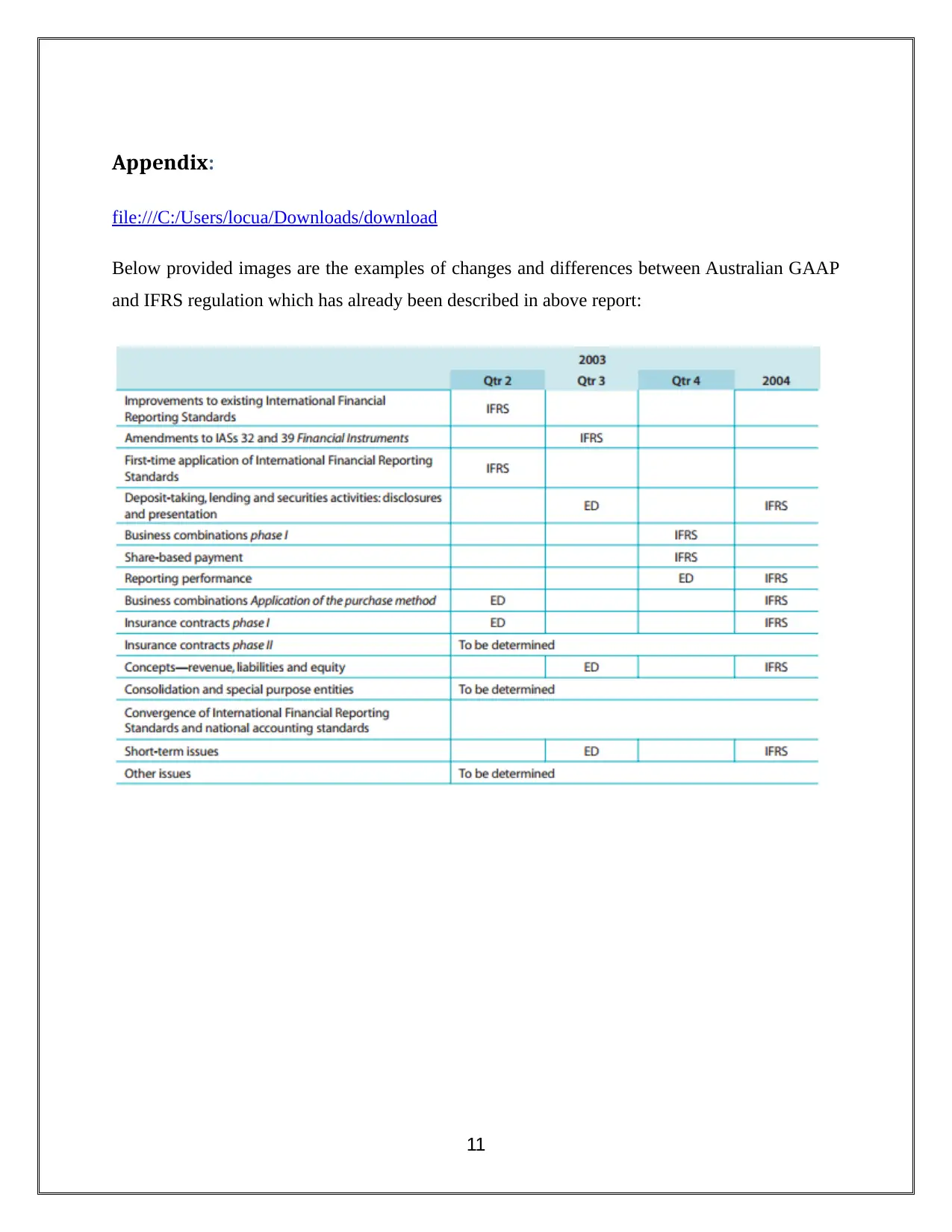

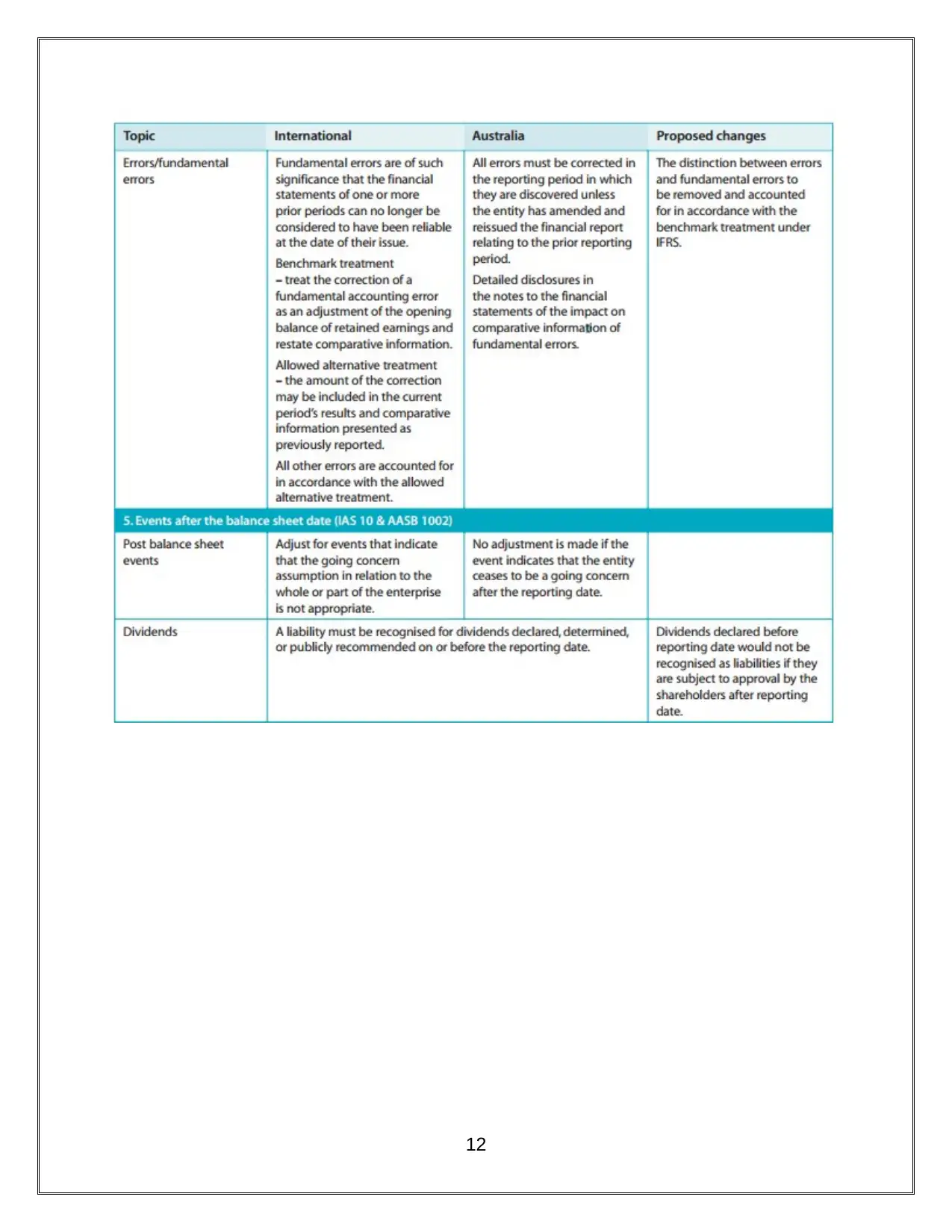

Appendix:

file:///C:/Users/locua/Downloads/download

Below provided images are the examples of changes and differences between Australian GAAP

and IFRS regulation which has already been described in above report:

11

file:///C:/Users/locua/Downloads/download

Below provided images are the examples of changes and differences between Australian GAAP

and IFRS regulation which has already been described in above report:

11

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.