Fraud Risk Factors in Financial Statements

VerifiedAdded on 2020/03/04

|10

|2449

|39

AI Summary

This assignment delves into the identification of potential fraud risk factors within a company's financial statements. It examines instances where manipulated asset valuations, such as plant and equipment, may indicate fraudulent activity. The analysis also considers internal control weaknesses, including the sudden implementation of a new IT system and changes in depreciation policies, as red flags for potential fraud.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

AUDITING

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

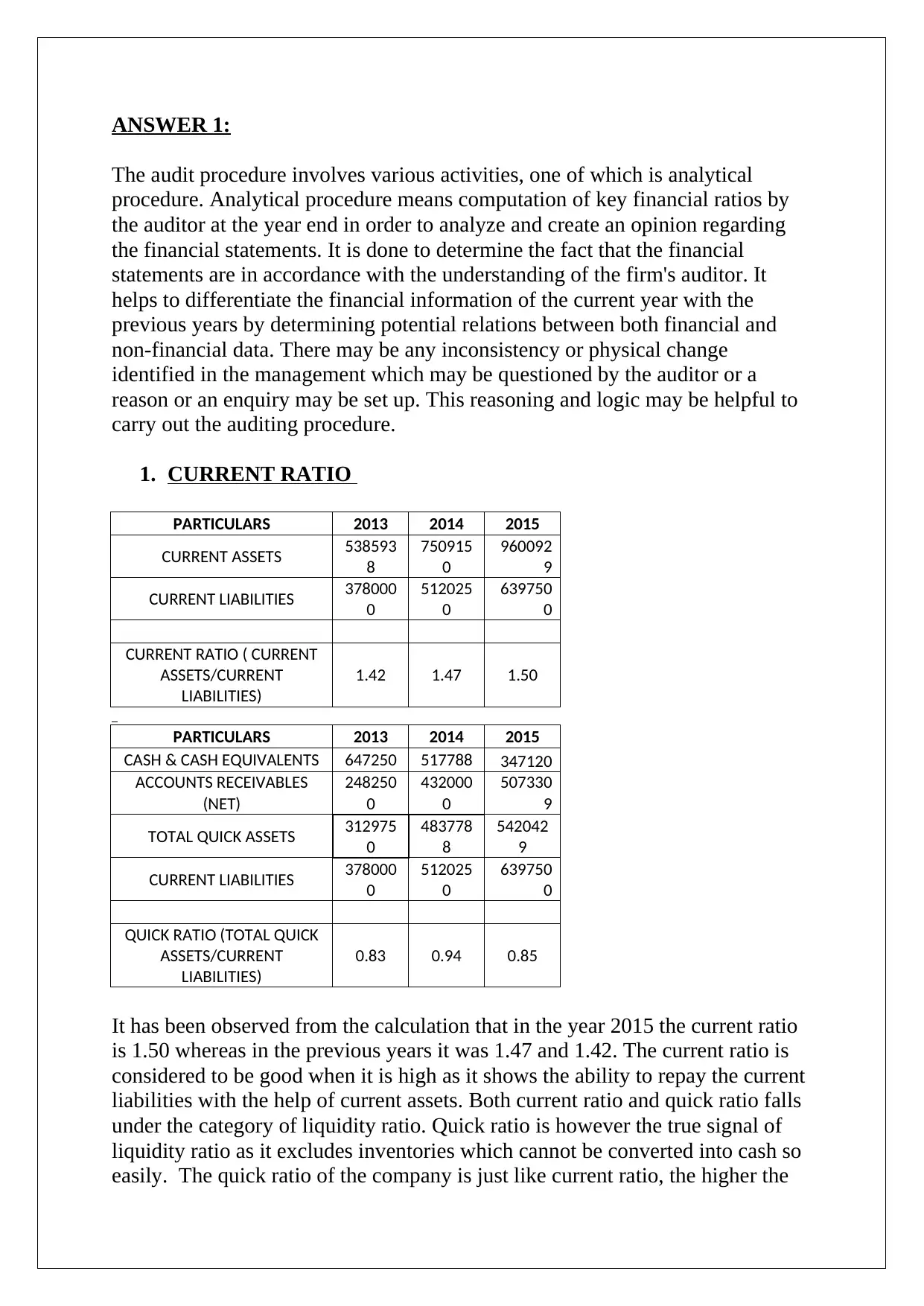

ANSWER 1:

The audit procedure involves various activities, one of which is analytical

procedure. Analytical procedure means computation of key financial ratios by

the auditor at the year end in order to analyze and create an opinion regarding

the financial statements. It is done to determine the fact that the financial

statements are in accordance with the understanding of the firm's auditor. It

helps to differentiate the financial information of the current year with the

previous years by determining potential relations between both financial and

non-financial data. There may be any inconsistency or physical change

identified in the management which may be questioned by the auditor or a

reason or an enquiry may be set up. This reasoning and logic may be helpful to

carry out the auditing procedure.

1. CURRENT RATIO

PARTICULARS 2013 2014 2015

CURRENT ASSETS 538593

8

750915

0

960092

9

CURRENT LIABILITIES 378000

0

512025

0

639750

0

CURRENT RATIO ( CURRENT

ASSETS/CURRENT

LIABILITIES)

1.42 1.47 1.50

PARTICULARS 2013 2014 2015

CASH & CASH EQUIVALENTS 647250 517788 347120

ACCOUNTS RECEIVABLES

(NET)

248250

0

432000

0

507330

9

TOTAL QUICK ASSETS 312975

0

483778

8

542042

9

CURRENT LIABILITIES 378000

0

512025

0

639750

0

QUICK RATIO (TOTAL QUICK

ASSETS/CURRENT

LIABILITIES)

0.83 0.94 0.85

It has been observed from the calculation that in the year 2015 the current ratio

is 1.50 whereas in the previous years it was 1.47 and 1.42. The current ratio is

considered to be good when it is high as it shows the ability to repay the current

liabilities with the help of current assets. Both current ratio and quick ratio falls

under the category of liquidity ratio. Quick ratio is however the true signal of

liquidity ratio as it excludes inventories which cannot be converted into cash so

easily. The quick ratio of the company is just like current ratio, the higher the

The audit procedure involves various activities, one of which is analytical

procedure. Analytical procedure means computation of key financial ratios by

the auditor at the year end in order to analyze and create an opinion regarding

the financial statements. It is done to determine the fact that the financial

statements are in accordance with the understanding of the firm's auditor. It

helps to differentiate the financial information of the current year with the

previous years by determining potential relations between both financial and

non-financial data. There may be any inconsistency or physical change

identified in the management which may be questioned by the auditor or a

reason or an enquiry may be set up. This reasoning and logic may be helpful to

carry out the auditing procedure.

1. CURRENT RATIO

PARTICULARS 2013 2014 2015

CURRENT ASSETS 538593

8

750915

0

960092

9

CURRENT LIABILITIES 378000

0

512025

0

639750

0

CURRENT RATIO ( CURRENT

ASSETS/CURRENT

LIABILITIES)

1.42 1.47 1.50

PARTICULARS 2013 2014 2015

CASH & CASH EQUIVALENTS 647250 517788 347120

ACCOUNTS RECEIVABLES

(NET)

248250

0

432000

0

507330

9

TOTAL QUICK ASSETS 312975

0

483778

8

542042

9

CURRENT LIABILITIES 378000

0

512025

0

639750

0

QUICK RATIO (TOTAL QUICK

ASSETS/CURRENT

LIABILITIES)

0.83 0.94 0.85

It has been observed from the calculation that in the year 2015 the current ratio

is 1.50 whereas in the previous years it was 1.47 and 1.42. The current ratio is

considered to be good when it is high as it shows the ability to repay the current

liabilities with the help of current assets. Both current ratio and quick ratio falls

under the category of liquidity ratio. Quick ratio is however the true signal of

liquidity ratio as it excludes inventories which cannot be converted into cash so

easily. The quick ratio of the company is just like current ratio, the higher the

better. It has been observed that in 2015 it was 0.85 but in the previous year it

was more favorable as it was a little more higher.

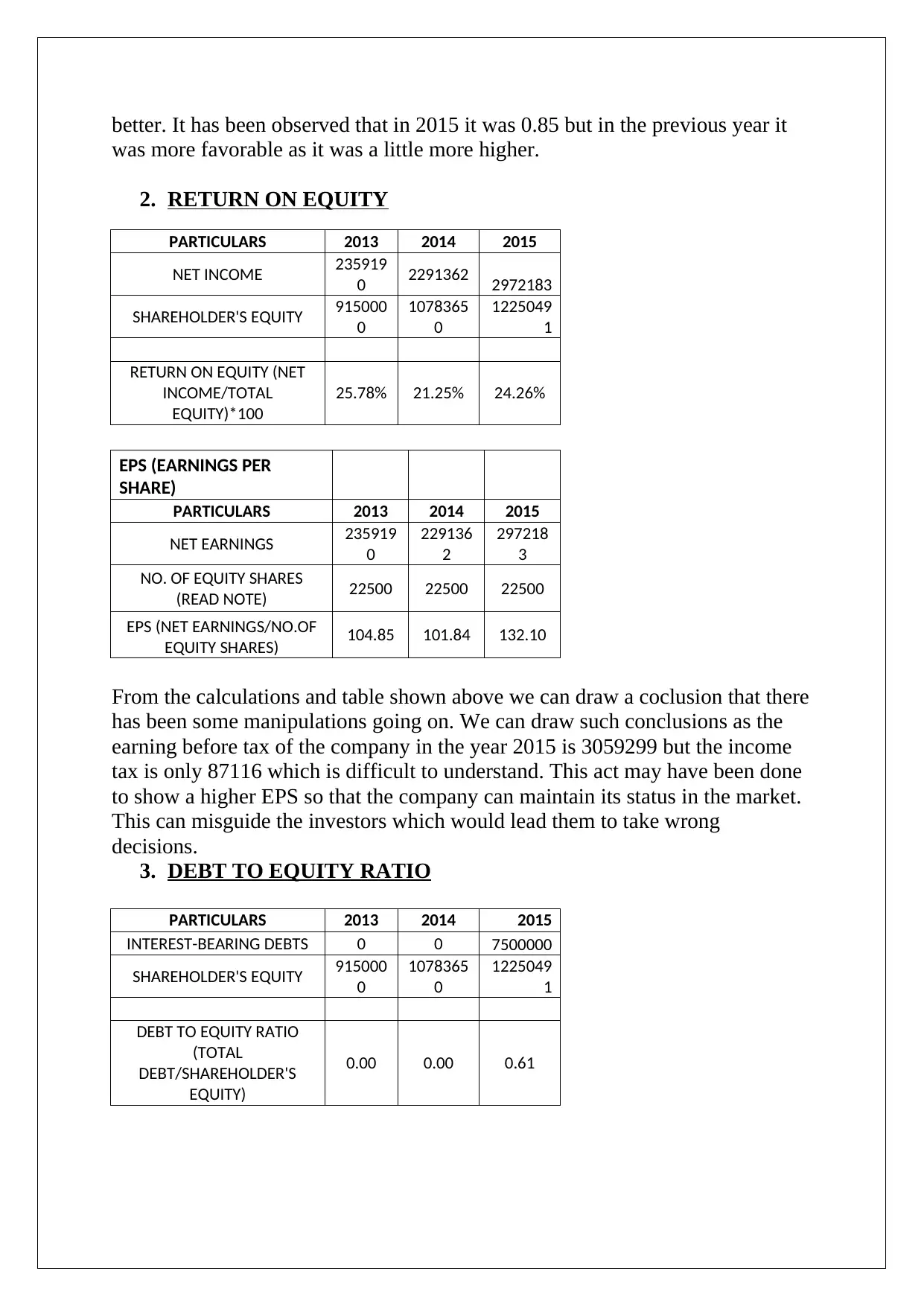

2. RETURN ON EQUITY

PARTICULARS 2013 2014 2015

NET INCOME 235919

0 2291362 2972183

SHAREHOLDER'S EQUITY 915000

0

1078365

0

1225049

1

RETURN ON EQUITY (NET

INCOME/TOTAL

EQUITY)*100

25.78% 21.25% 24.26%

EPS (EARNINGS PER

SHARE)

PARTICULARS 2013 2014 2015

NET EARNINGS 235919

0

229136

2

297218

3

NO. OF EQUITY SHARES

(READ NOTE) 22500 22500 22500

EPS (NET EARNINGS/NO.OF

EQUITY SHARES) 104.85 101.84 132.10

From the calculations and table shown above we can draw a coclusion that there

has been some manipulations going on. We can draw such conclusions as the

earning before tax of the company in the year 2015 is 3059299 but the income

tax is only 87116 which is difficult to understand. This act may have been done

to show a higher EPS so that the company can maintain its status in the market.

This can misguide the investors which would lead them to take wrong

decisions.

3. DEBT TO EQUITY RATIO

PARTICULARS 2013 2014 2015

INTEREST-BEARING DEBTS 0 0 7500000

SHAREHOLDER'S EQUITY 915000

0

1078365

0

1225049

1

DEBT TO EQUITY RATIO

(TOTAL

DEBT/SHAREHOLDER'S

EQUITY)

0.00 0.00 0.61

was more favorable as it was a little more higher.

2. RETURN ON EQUITY

PARTICULARS 2013 2014 2015

NET INCOME 235919

0 2291362 2972183

SHAREHOLDER'S EQUITY 915000

0

1078365

0

1225049

1

RETURN ON EQUITY (NET

INCOME/TOTAL

EQUITY)*100

25.78% 21.25% 24.26%

EPS (EARNINGS PER

SHARE)

PARTICULARS 2013 2014 2015

NET EARNINGS 235919

0

229136

2

297218

3

NO. OF EQUITY SHARES

(READ NOTE) 22500 22500 22500

EPS (NET EARNINGS/NO.OF

EQUITY SHARES) 104.85 101.84 132.10

From the calculations and table shown above we can draw a coclusion that there

has been some manipulations going on. We can draw such conclusions as the

earning before tax of the company in the year 2015 is 3059299 but the income

tax is only 87116 which is difficult to understand. This act may have been done

to show a higher EPS so that the company can maintain its status in the market.

This can misguide the investors which would lead them to take wrong

decisions.

3. DEBT TO EQUITY RATIO

PARTICULARS 2013 2014 2015

INTEREST-BEARING DEBTS 0 0 7500000

SHAREHOLDER'S EQUITY 915000

0

1078365

0

1225049

1

DEBT TO EQUITY RATIO

(TOTAL

DEBT/SHAREHOLDER'S

EQUITY)

0.00 0.00 0.61

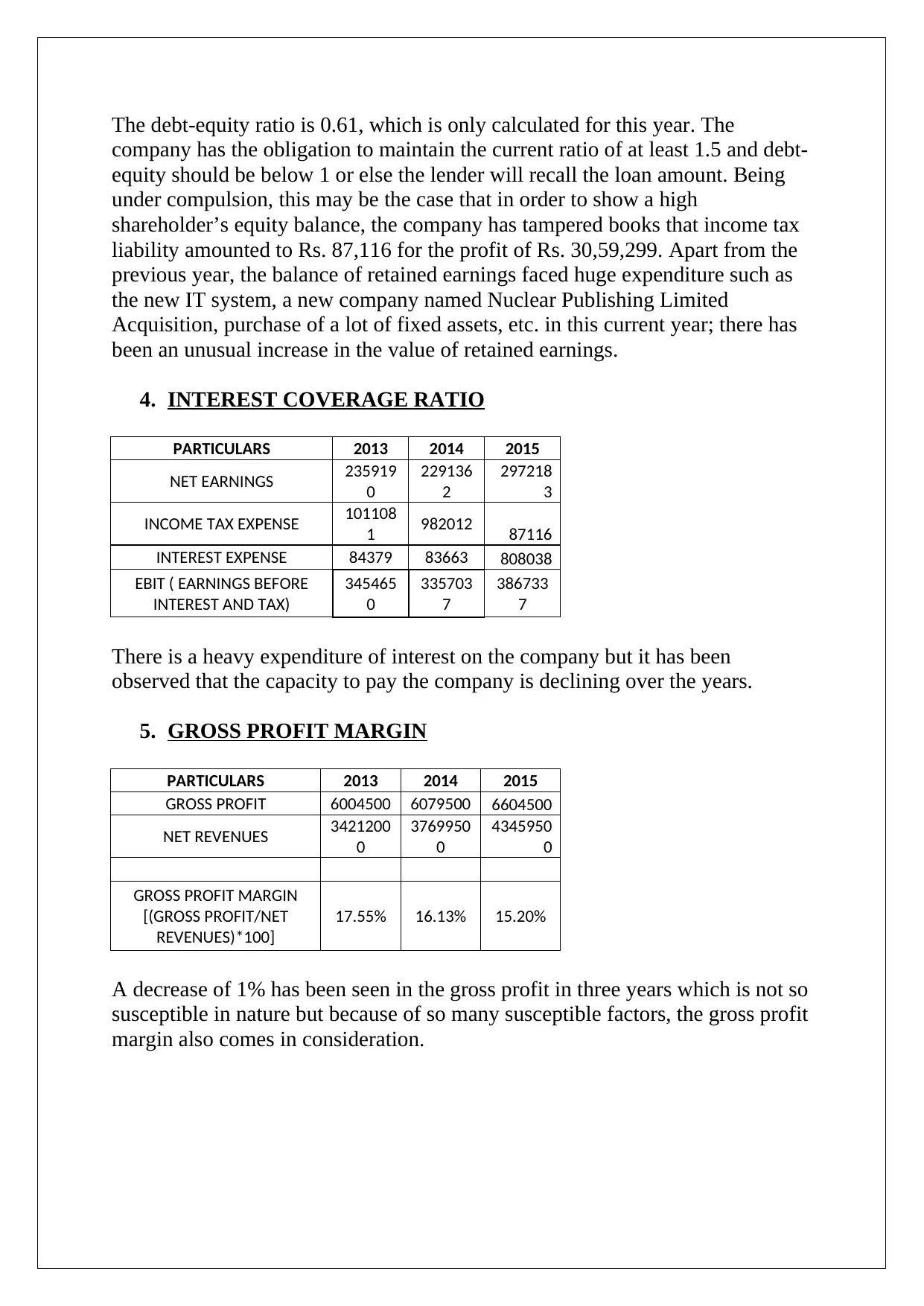

The debt-equity ratio is 0.61, which is only calculated for this year. The

company has the obligation to maintain the current ratio of at least 1.5 and debt-

equity should be below 1 or else the lender will recall the loan amount. Being

under compulsion, this may be the case that in order to show a high

shareholder’s equity balance, the company has tampered books that income tax

liability amounted to Rs. 87,116 for the profit of Rs. 30,59,299. Apart from the

previous year, the balance of retained earnings faced huge expenditure such as

the new IT system, a new company named Nuclear Publishing Limited

Acquisition, purchase of a lot of fixed assets, etc. in this current year; there has

been an unusual increase in the value of retained earnings.

4. INTEREST COVERAGE RATIO

PARTICULARS 2013 2014 2015

NET EARNINGS 235919

0

229136

2

297218

3

INCOME TAX EXPENSE 101108

1 982012 87116

INTEREST EXPENSE 84379 83663 808038

EBIT ( EARNINGS BEFORE

INTEREST AND TAX)

345465

0

335703

7

386733

7

There is a heavy expenditure of interest on the company but it has been

observed that the capacity to pay the company is declining over the years.

5. GROSS PROFIT MARGIN

PARTICULARS 2013 2014 2015

GROSS PROFIT 6004500 6079500 6604500

NET REVENUES 3421200

0

3769950

0

4345950

0

GROSS PROFIT MARGIN

[(GROSS PROFIT/NET

REVENUES)*100]

17.55% 16.13% 15.20%

A decrease of 1% has been seen in the gross profit in three years which is not so

susceptible in nature but because of so many susceptible factors, the gross profit

margin also comes in consideration.

company has the obligation to maintain the current ratio of at least 1.5 and debt-

equity should be below 1 or else the lender will recall the loan amount. Being

under compulsion, this may be the case that in order to show a high

shareholder’s equity balance, the company has tampered books that income tax

liability amounted to Rs. 87,116 for the profit of Rs. 30,59,299. Apart from the

previous year, the balance of retained earnings faced huge expenditure such as

the new IT system, a new company named Nuclear Publishing Limited

Acquisition, purchase of a lot of fixed assets, etc. in this current year; there has

been an unusual increase in the value of retained earnings.

4. INTEREST COVERAGE RATIO

PARTICULARS 2013 2014 2015

NET EARNINGS 235919

0

229136

2

297218

3

INCOME TAX EXPENSE 101108

1 982012 87116

INTEREST EXPENSE 84379 83663 808038

EBIT ( EARNINGS BEFORE

INTEREST AND TAX)

345465

0

335703

7

386733

7

There is a heavy expenditure of interest on the company but it has been

observed that the capacity to pay the company is declining over the years.

5. GROSS PROFIT MARGIN

PARTICULARS 2013 2014 2015

GROSS PROFIT 6004500 6079500 6604500

NET REVENUES 3421200

0

3769950

0

4345950

0

GROSS PROFIT MARGIN

[(GROSS PROFIT/NET

REVENUES)*100]

17.55% 16.13% 15.20%

A decrease of 1% has been seen in the gross profit in three years which is not so

susceptible in nature but because of so many susceptible factors, the gross profit

margin also comes in consideration.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

ANSWER 2:

It is important in the audit procedure to identify whether there are

misconceptions or not this is done through the risk assessment procedures. It is

considered significant as auditing means identifying the misstatements in the

financial statements.

The inherent risk is one of the main types of audit risk. It is the risk arising from

misleading information or faults in financial statements because of some

reasons, but not due to the failure of control. Inherent risks can be exposed to a

large number of similar transactions, heavy usage of sampling, human intuition,

and the disclosure to misconceptions which can be material or contribute to a

material misstatement as a number of small misconceptions. The auditor

assesses such risk-based on their intuition and judgment and their understanding

of the nature and function of the entity (Cahill & Kane, 2011).

Keeping in mind the present case of Double Ink Printer Limited (DIPL), where

books are being discontinued on June 30, there are two underlying risk factors

which arise from the nature and operation of the company:

Control over Inventory: Inventories are usually the stock of the

company. However, this company has a very few stock of stationeries

such as paper, ink and binding materials. On receiving, the inventory is

kept in the warehouse and the entries are done by the accounts payable

clerk, specifying the value and quantity of the inventories in the books.

The observed risk in this case:-

A. Inventories are very easy to manipulate and it is observed that the

warehouse is usually closed for two days at the end of the year only. A

periodic stock calculation should take place instead of only at the end of

the year because keeping stock and storing it till the year-end will not

reveal the regularity or irregularities of the stock at the end of the months.

B. In this case, there is a very common risk of theft because the absence of

the goods can either be ignored or they can be claimed in the form of

anomalies, so the employees remain on the safe side.

C. It has nowhere been told that when the inventory is being obtained, there

is a physical examination of the goods. Only one in charge is being

appointed who passes the entrance on arrival. However, this is a

susceptible point because it may be that the responsible person can record

the entry of fewer inventories in his books rather than what he is actually

receiving, and then he sells that unnamed goods to external parties

individually and in fact enjoy full earnings without paying for any cost of

production (Fountain, n.d.).

misconceptions or not this is done through the risk assessment procedures. It is

considered significant as auditing means identifying the misstatements in the

financial statements.

The inherent risk is one of the main types of audit risk. It is the risk arising from

misleading information or faults in financial statements because of some

reasons, but not due to the failure of control. Inherent risks can be exposed to a

large number of similar transactions, heavy usage of sampling, human intuition,

and the disclosure to misconceptions which can be material or contribute to a

material misstatement as a number of small misconceptions. The auditor

assesses such risk-based on their intuition and judgment and their understanding

of the nature and function of the entity (Cahill & Kane, 2011).

Keeping in mind the present case of Double Ink Printer Limited (DIPL), where

books are being discontinued on June 30, there are two underlying risk factors

which arise from the nature and operation of the company:

Control over Inventory: Inventories are usually the stock of the

company. However, this company has a very few stock of stationeries

such as paper, ink and binding materials. On receiving, the inventory is

kept in the warehouse and the entries are done by the accounts payable

clerk, specifying the value and quantity of the inventories in the books.

The observed risk in this case:-

A. Inventories are very easy to manipulate and it is observed that the

warehouse is usually closed for two days at the end of the year only. A

periodic stock calculation should take place instead of only at the end of

the year because keeping stock and storing it till the year-end will not

reveal the regularity or irregularities of the stock at the end of the months.

B. In this case, there is a very common risk of theft because the absence of

the goods can either be ignored or they can be claimed in the form of

anomalies, so the employees remain on the safe side.

C. It has nowhere been told that when the inventory is being obtained, there

is a physical examination of the goods. Only one in charge is being

appointed who passes the entrance on arrival. However, this is a

susceptible point because it may be that the responsible person can record

the entry of fewer inventories in his books rather than what he is actually

receiving, and then he sells that unnamed goods to external parties

individually and in fact enjoy full earnings without paying for any cost of

production (Fountain, n.d.).

CEO was newly appointed and also the audit team of the firm was

changed in jan 2015: It is a doubtful act that the new CEo was appointed

in the firm in the middle of the year and there were no reasons or

explanations stated. The previous CEO wasn't on the threshold of being

replaced but was semi-retired. An inquiry is to be made for finding and

analyzing the right reasons for such steps by having a word with the

previous CEO or the other members of the company. In addition, the

Board has now formed an internal audit department which shows that

there was no such internal audit process taking place previously. It is in a

way sensitive because it can cause problems with the company or the

operation of the company and also maybe the level of misappropriations

are increasing, which the company is not able to identify, but only the

results are being faced. All this can create a pressure on the firm

altogether, so it was necessary to create a separate audit department to

improve the areas which are affected because of mistakes or fraud (Griffin,

2009).

changed in jan 2015: It is a doubtful act that the new CEo was appointed

in the firm in the middle of the year and there were no reasons or

explanations stated. The previous CEO wasn't on the threshold of being

replaced but was semi-retired. An inquiry is to be made for finding and

analyzing the right reasons for such steps by having a word with the

previous CEO or the other members of the company. In addition, the

Board has now formed an internal audit department which shows that

there was no such internal audit process taking place previously. It is in a

way sensitive because it can cause problems with the company or the

operation of the company and also maybe the level of misappropriations

are increasing, which the company is not able to identify, but only the

results are being faced. All this can create a pressure on the firm

altogether, so it was necessary to create a separate audit department to

improve the areas which are affected because of mistakes or fraud (Griffin,

2009).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ANSWER 3:

Any act that has been done with a wrong intention by two or more people is

known as fraud and the person committing such fraud is known as a fraudster.;

this may be an employee, a third party or top-level management who uses it to

enjoy the benefit unlawfully. Fraud risk factors are factors that indicate pressure

or incentives that can result in consequences fraudulent activities. Fraudulent

risk factors can usually be classified into three situations that usually take place

where fraud occurs - Incentives, Opportunities and Attitudes/Rationalizations.

Based on the given case study, follow two major fraud risk factors for which

DIPL is susceptible, which are:-

New IT System adoption: In order to automate the full accounting

process, the board under extremely high pressure invested in the new IT

system. It was a huge burden for the company to set up a new IT system

when it was the time to close the books for the company. The IT manager

claimed that a sudden change in the entire system of recording accounting

transaction is messing up the entire scenario because neither the

employees were currently well trained nor proper testing of the new

system was done or handling of the installation was being made (Hooks,

2011).

This type of action is an opportunity to conduct fraud because it can finally be

said clearly that during the transfer of accounting information in the

computerized system, the transactions were lost or because of lack of

knowledge and the inability of the employees or the mechanisms of the system.

Apart from this, in this way, the person intending to commit fraud can

transfigure the cash balance or ignore the fraudulent transactions that may have

been conducted in the relevant financial year. For example, a director did some

transactions with the third party in the name of the company and sold the goods

to enjoy the full amount on his own personal account. Taking advantage of his

position, he portrayed this scenario in such a way that the goods which were

sold by him for his personal profit were actually considered lost in the

management's eyes. It was observed that there was a newly set up internal team

that was formed without any reasons all of a sudden. Therefore, under heavy

pressure, it may be that in June 2015, a new IT system was formed so that such

fraud activities could be ignored and in the end, the answerability of the

accounting department could be blamed for such mistake.

Valuation of plant and equipment: There is a relative increment of Rs.

5,25,000 in the value of plant and equipment from 2013 to 2014 whereas

Any act that has been done with a wrong intention by two or more people is

known as fraud and the person committing such fraud is known as a fraudster.;

this may be an employee, a third party or top-level management who uses it to

enjoy the benefit unlawfully. Fraud risk factors are factors that indicate pressure

or incentives that can result in consequences fraudulent activities. Fraudulent

risk factors can usually be classified into three situations that usually take place

where fraud occurs - Incentives, Opportunities and Attitudes/Rationalizations.

Based on the given case study, follow two major fraud risk factors for which

DIPL is susceptible, which are:-

New IT System adoption: In order to automate the full accounting

process, the board under extremely high pressure invested in the new IT

system. It was a huge burden for the company to set up a new IT system

when it was the time to close the books for the company. The IT manager

claimed that a sudden change in the entire system of recording accounting

transaction is messing up the entire scenario because neither the

employees were currently well trained nor proper testing of the new

system was done or handling of the installation was being made (Hooks,

2011).

This type of action is an opportunity to conduct fraud because it can finally be

said clearly that during the transfer of accounting information in the

computerized system, the transactions were lost or because of lack of

knowledge and the inability of the employees or the mechanisms of the system.

Apart from this, in this way, the person intending to commit fraud can

transfigure the cash balance or ignore the fraudulent transactions that may have

been conducted in the relevant financial year. For example, a director did some

transactions with the third party in the name of the company and sold the goods

to enjoy the full amount on his own personal account. Taking advantage of his

position, he portrayed this scenario in such a way that the goods which were

sold by him for his personal profit were actually considered lost in the

management's eyes. It was observed that there was a newly set up internal team

that was formed without any reasons all of a sudden. Therefore, under heavy

pressure, it may be that in June 2015, a new IT system was formed so that such

fraud activities could be ignored and in the end, the answerability of the

accounting department could be blamed for such mistake.

Valuation of plant and equipment: There is a relative increment of Rs.

5,25,000 in the value of plant and equipment from 2013 to 2014 whereas

in account a purchase of Rs. 76,50,000 of plant and equipment takes

place in 2015. Also, the loan advanced by the firm BDO Finance Limited

is Rs.75,00,000. Thus, the clear understanding of the purpose of such a

big amount of loan is not being made. Also, it should be sensitized that

under what circumstances, the company has decided to take such a large

amount in form of loan as well as on the other side, it is suddenly

showing the high value of the assets in its books. In addition, the

company made an extraordinary hasty decision to adopt a new

computerized accounting system in June 2015. Also, the following points

need to be considered:-

A. It may be that by showing the high value of assets in their books, the

company wants to show its stakeholders a strong financial status so that

they can enjoy easy public funding in the coming future.

B. In the board year meeting, the estimated life of the printing presses was

changed to 30 years instead of 20 years, which is generally adopted in the

industries for general depreciation purposes. Changing the projected life

from 20 years to 30 years will definitely show lesser depreciation but it

may also be that it is to compensate for the overall high depreciating sum

over the last two years.

C. Apart from this, such a decision is taken on the basis of the experience of

the CEO, which is actually going against the policy adopted in the

printing industry.

It is susceptible in a way that such valuation can be done for winning the trust of

the stakeholders and also for the purpose of enjoying easy funding which may

be used for many fraudulent activities in near future. Thus, such extraordinary

transactions and not reasonable decisions are an indication of fraudulent risk

factors which may be affecting the firm in future.

place in 2015. Also, the loan advanced by the firm BDO Finance Limited

is Rs.75,00,000. Thus, the clear understanding of the purpose of such a

big amount of loan is not being made. Also, it should be sensitized that

under what circumstances, the company has decided to take such a large

amount in form of loan as well as on the other side, it is suddenly

showing the high value of the assets in its books. In addition, the

company made an extraordinary hasty decision to adopt a new

computerized accounting system in June 2015. Also, the following points

need to be considered:-

A. It may be that by showing the high value of assets in their books, the

company wants to show its stakeholders a strong financial status so that

they can enjoy easy public funding in the coming future.

B. In the board year meeting, the estimated life of the printing presses was

changed to 30 years instead of 20 years, which is generally adopted in the

industries for general depreciation purposes. Changing the projected life

from 20 years to 30 years will definitely show lesser depreciation but it

may also be that it is to compensate for the overall high depreciating sum

over the last two years.

C. Apart from this, such a decision is taken on the basis of the experience of

the CEO, which is actually going against the policy adopted in the

printing industry.

It is susceptible in a way that such valuation can be done for winning the trust of

the stakeholders and also for the purpose of enjoying easy funding which may

be used for many fraudulent activities in near future. Thus, such extraordinary

transactions and not reasonable decisions are an indication of fraudulent risk

factors which may be affecting the firm in future.

References:

Basu, S. (2009). Fundamentals of auditing. Delhi: Pearson.

Blank, R. (2014). The Basics of Quality Auditing. Hoboken: Taylor and Francis.

Boynton, W., & Johnson, R. (2006). Modern Auditing. Hoboken: John Wiley and Sons.

Cahill, L., & Kane, R. (2011). Environmental health and safety audits. Lanham, MD:

Government Institutes.

Fountain, L. Leading the internal audit function.

Griffin, M. (2009). MBA fundamentals. New York, NY: Kaplan.

Hooks, K. (2011). Auditing and assurance services. Hoboken, NJ: Wiley.

Basu, S. (2009). Fundamentals of auditing. Delhi: Pearson.

Blank, R. (2014). The Basics of Quality Auditing. Hoboken: Taylor and Francis.

Boynton, W., & Johnson, R. (2006). Modern Auditing. Hoboken: John Wiley and Sons.

Cahill, L., & Kane, R. (2011). Environmental health and safety audits. Lanham, MD:

Government Institutes.

Fountain, L. Leading the internal audit function.

Griffin, M. (2009). MBA fundamentals. New York, NY: Kaplan.

Hooks, K. (2011). Auditing and assurance services. Hoboken, NJ: Wiley.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.