Ask a question from expert

HI6026 - Audit, Assurance and Compliance, Preliminary Analytical

8 Pages2059 Words214 Views

Holmes Institute Sydney

Audit, Assurance and Compliance (HI6026)

Added on 2020-03-13

About This Document

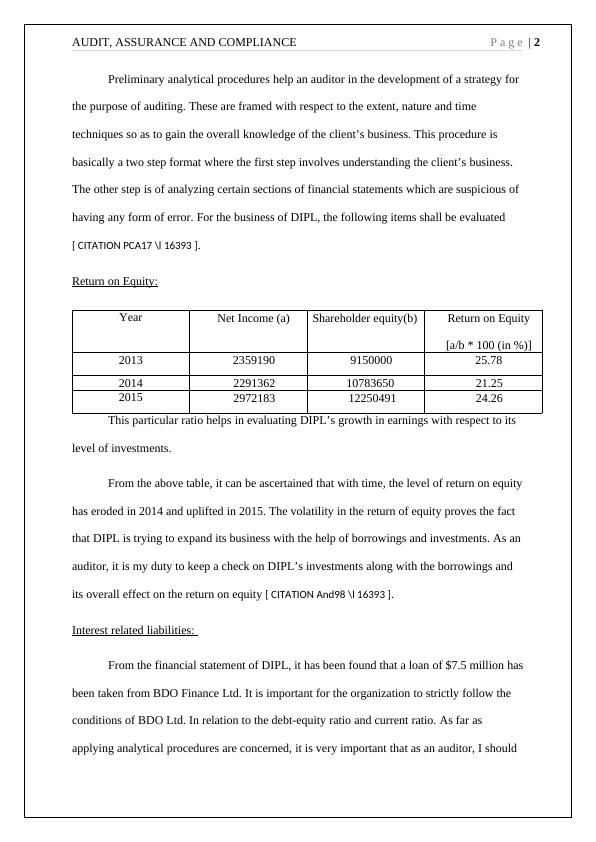

In the HI6026 Assignment, we will discuss Audit, Assurance, And Compliance. Preliminary analytical procedures help an auditor in the development of a strategy for auditing. Inherent risk is those risk that lies beyond the control of an auditor’s audit procedures and methods of control. As per the background information of DIPL, its two fraud risk factors are loans taken from BDO Finance Ltd. and another is the adoption of a new IT system in their course of operations.

HI6026 - Audit, Assurance and Compliance, Preliminary Analytical

Holmes Institute Sydney

Audit, Assurance and Compliance (HI6026)

Added on 2020-03-13

BookmarkShareRelated Documents

End of preview

Want to access all the pages? Upload your documents or become a member.

AUDIT, ASSURANCE AND COMPLIANCE 1 AUDIT, ASSURANCE AND COMPLIANCE Audit, Assurance and Compliance

|6

|1244

|225

Auditing Theory and Practice : Assignment

|9

|1974

|201

HI6026 - Audit Assurance and Compliance

|15

|3083

|131

Audit, Assurance and Compliance Assignment - HI6026

|13

|2797

|63

Auditing and Assurance Services- Project Report

|10

|2670

|156

Audit, Assurance And Compliance | Assignment On DIPL

|9

|2402

|46