Audit, Assurance and Compliance Report: Financial Analysis of DIPL

VerifiedAdded on 2020/03/01

|14

|2717

|309

Report

AI Summary

This report presents an analysis of the audit, assurance, and compliance aspects of Double Ink Printers Limited (DIPL). It begins with a detailed application of analytical procedures, including profitability, liquidity, efficiency, and solvency analyses, using financial data from 2013 to 2015. The report then examines the impact of analytical review on audit planning, specifically for the year ending June 30, 2015, identifying potential risks and areas requiring further investigation. The subsequent sections delve into the identification of inherent risk factors arising from DIPL's business operations, such as financial and information technology risks, and their potential for material misstatement. Finally, the report outlines key risk factors related to misstatements in financial reporting, including debt covenants and the nature of the control environment, and assesses their effects on the conduct of the audit, emphasizing the need for careful verification and analysis in the audit plan.

Running head: AUDIT, ASSURANCE AND COMPLIANCE

Audit, Assurance and Compliance

Name of the Student:

Name of the University:

Author Note:

Audit, Assurance and Compliance

Name of the Student:

Name of the University:

Author Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2AUDIT, ASSURANCE AND COMPLIANCE

Table of Contents

Question 1........................................................................................................................................2

Part A...........................................................................................................................................2

Application of analytical procedures to the financial report information of Double Ink Printers

Limited.........................................................................................................................................2

Profitability analysis................................................................................................................2

Liquidity Analysis...................................................................................................................4

Efficiency Analysis..................................................................................................................5

Solvency Analysis...................................................................................................................6

Part B...........................................................................................................................................7

Impact of analytical review on audit planning for the year ending 30th of June 2015.................7

Question 2........................................................................................................................................9

Identification of inherent risk factors that arise from the nature of business operations of Double

Ink Printers Limited.........................................................................................................................9

Question 3......................................................................................................................................10

Part A.........................................................................................................................................10

Key risk factors related to misstatement in financial reporting.................................................10

Part B.........................................................................................................................................11

Effect of risk factors on conduct of audit..................................................................................11

Reference List................................................................................................................................12

Table of Contents

Question 1........................................................................................................................................2

Part A...........................................................................................................................................2

Application of analytical procedures to the financial report information of Double Ink Printers

Limited.........................................................................................................................................2

Profitability analysis................................................................................................................2

Liquidity Analysis...................................................................................................................4

Efficiency Analysis..................................................................................................................5

Solvency Analysis...................................................................................................................6

Part B...........................................................................................................................................7

Impact of analytical review on audit planning for the year ending 30th of June 2015.................7

Question 2........................................................................................................................................9

Identification of inherent risk factors that arise from the nature of business operations of Double

Ink Printers Limited.........................................................................................................................9

Question 3......................................................................................................................................10

Part A.........................................................................................................................................10

Key risk factors related to misstatement in financial reporting.................................................10

Part B.........................................................................................................................................11

Effect of risk factors on conduct of audit..................................................................................11

Reference List................................................................................................................................12

3AUDIT, ASSURANCE AND COMPLIANCE

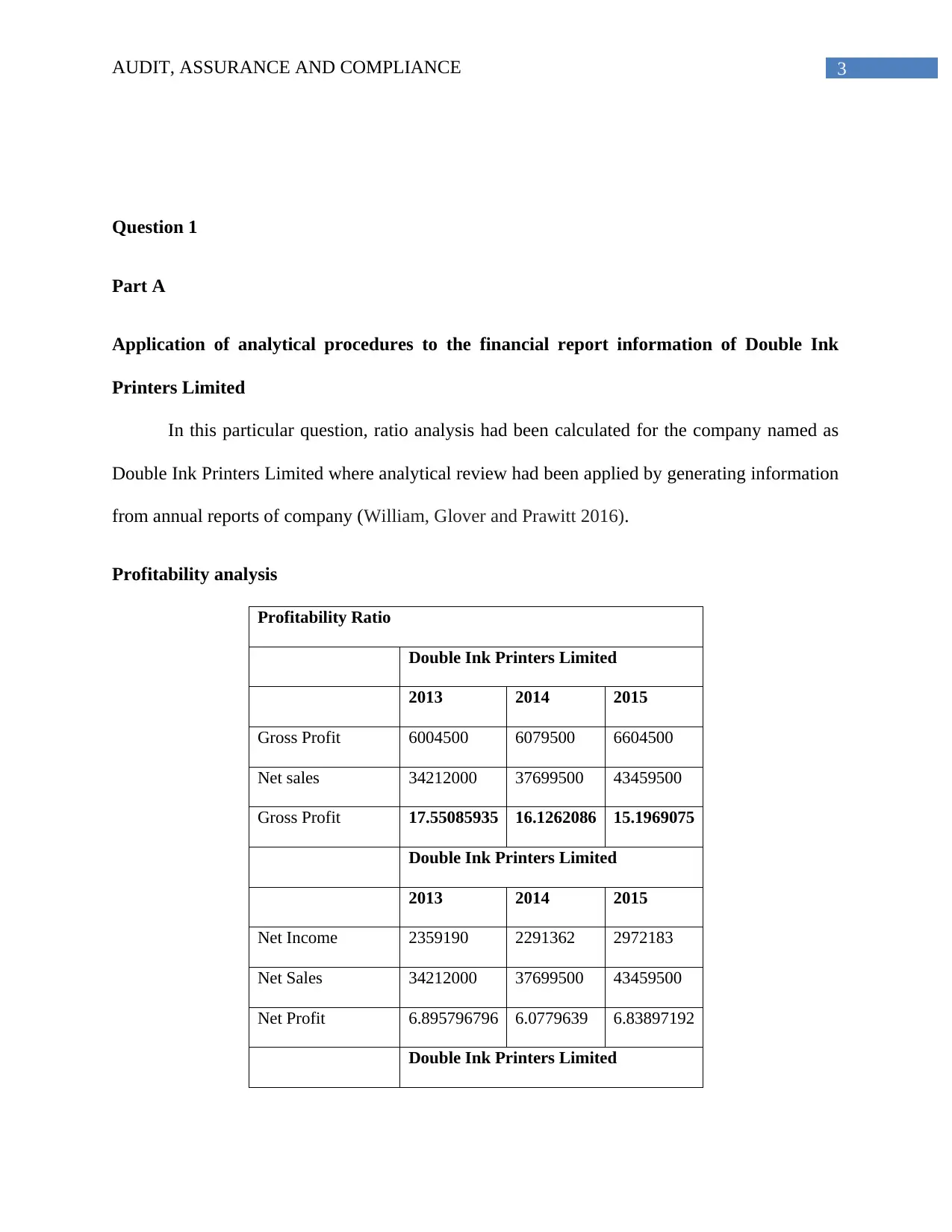

Question 1

Part A

Application of analytical procedures to the financial report information of Double Ink

Printers Limited

In this particular question, ratio analysis had been calculated for the company named as

Double Ink Printers Limited where analytical review had been applied by generating information

from annual reports of company (William, Glover and Prawitt 2016).

Profitability analysis

Profitability Ratio

Double Ink Printers Limited

2013 2014 2015

Gross Profit 6004500 6079500 6604500

Net sales 34212000 37699500 43459500

Gross Profit 17.55085935 16.1262086 15.1969075

Double Ink Printers Limited

2013 2014 2015

Net Income 2359190 2291362 2972183

Net Sales 34212000 37699500 43459500

Net Profit 6.895796796 6.0779639 6.83897192

Double Ink Printers Limited

Question 1

Part A

Application of analytical procedures to the financial report information of Double Ink

Printers Limited

In this particular question, ratio analysis had been calculated for the company named as

Double Ink Printers Limited where analytical review had been applied by generating information

from annual reports of company (William, Glover and Prawitt 2016).

Profitability analysis

Profitability Ratio

Double Ink Printers Limited

2013 2014 2015

Gross Profit 6004500 6079500 6604500

Net sales 34212000 37699500 43459500

Gross Profit 17.55085935 16.1262086 15.1969075

Double Ink Printers Limited

2013 2014 2015

Net Income 2359190 2291362 2972183

Net Sales 34212000 37699500 43459500

Net Profit 6.895796796 6.0779639 6.83897192

Double Ink Printers Limited

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

4AUDIT, ASSURANCE AND COMPLIANCE

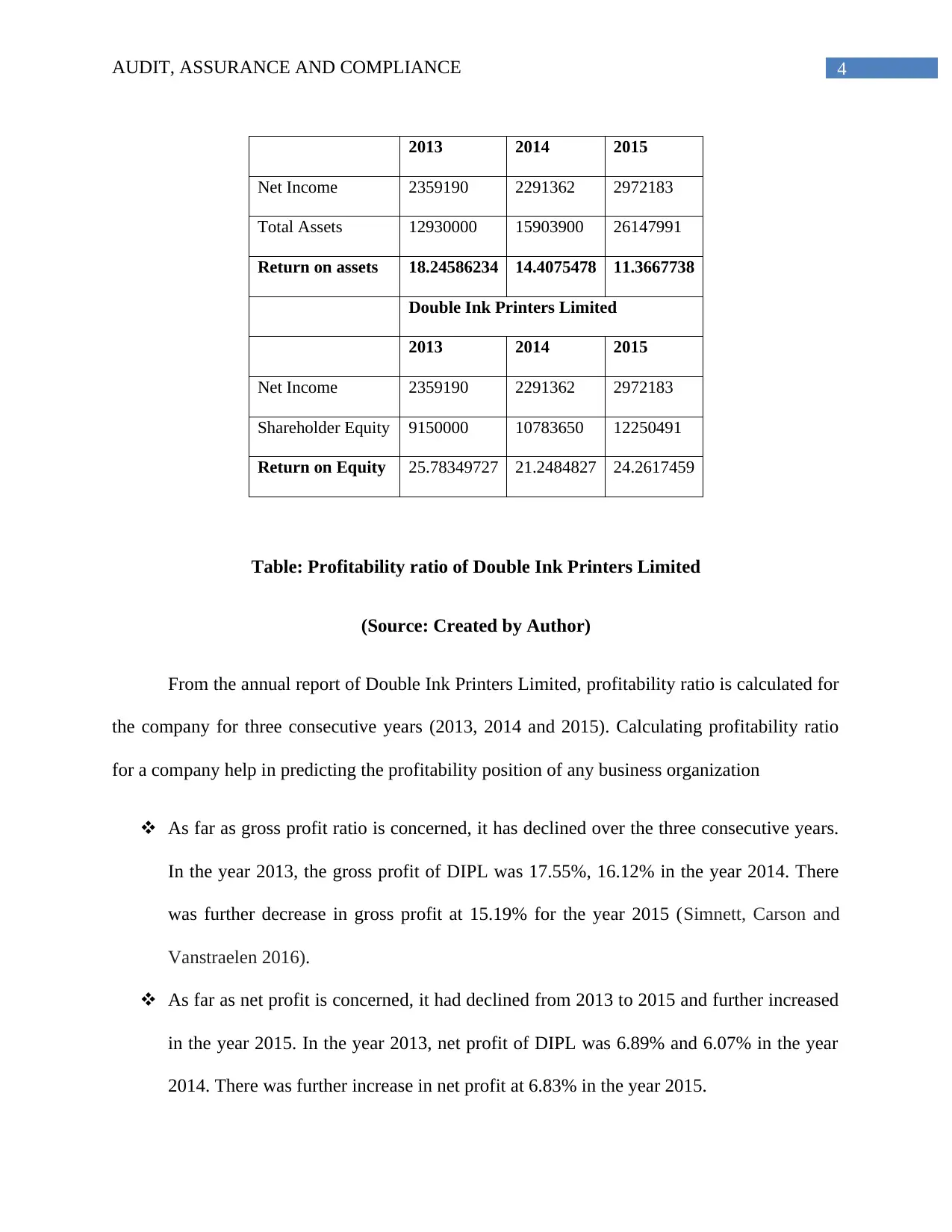

2013 2014 2015

Net Income 2359190 2291362 2972183

Total Assets 12930000 15903900 26147991

Return on assets 18.24586234 14.4075478 11.3667738

Double Ink Printers Limited

2013 2014 2015

Net Income 2359190 2291362 2972183

Shareholder Equity 9150000 10783650 12250491

Return on Equity 25.78349727 21.2484827 24.2617459

Table: Profitability ratio of Double Ink Printers Limited

(Source: Created by Author)

From the annual report of Double Ink Printers Limited, profitability ratio is calculated for

the company for three consecutive years (2013, 2014 and 2015). Calculating profitability ratio

for a company help in predicting the profitability position of any business organization

As far as gross profit ratio is concerned, it has declined over the three consecutive years.

In the year 2013, the gross profit of DIPL was 17.55%, 16.12% in the year 2014. There

was further decrease in gross profit at 15.19% for the year 2015 (Simnett, Carson and

Vanstraelen 2016).

As far as net profit is concerned, it had declined from 2013 to 2015 and further increased

in the year 2015. In the year 2013, net profit of DIPL was 6.89% and 6.07% in the year

2014. There was further increase in net profit at 6.83% in the year 2015.

2013 2014 2015

Net Income 2359190 2291362 2972183

Total Assets 12930000 15903900 26147991

Return on assets 18.24586234 14.4075478 11.3667738

Double Ink Printers Limited

2013 2014 2015

Net Income 2359190 2291362 2972183

Shareholder Equity 9150000 10783650 12250491

Return on Equity 25.78349727 21.2484827 24.2617459

Table: Profitability ratio of Double Ink Printers Limited

(Source: Created by Author)

From the annual report of Double Ink Printers Limited, profitability ratio is calculated for

the company for three consecutive years (2013, 2014 and 2015). Calculating profitability ratio

for a company help in predicting the profitability position of any business organization

As far as gross profit ratio is concerned, it has declined over the three consecutive years.

In the year 2013, the gross profit of DIPL was 17.55%, 16.12% in the year 2014. There

was further decrease in gross profit at 15.19% for the year 2015 (Simnett, Carson and

Vanstraelen 2016).

As far as net profit is concerned, it had declined from 2013 to 2015 and further increased

in the year 2015. In the year 2013, net profit of DIPL was 6.89% and 6.07% in the year

2014. There was further increase in net profit at 6.83% in the year 2015.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

5AUDIT, ASSURANCE AND COMPLIANCE

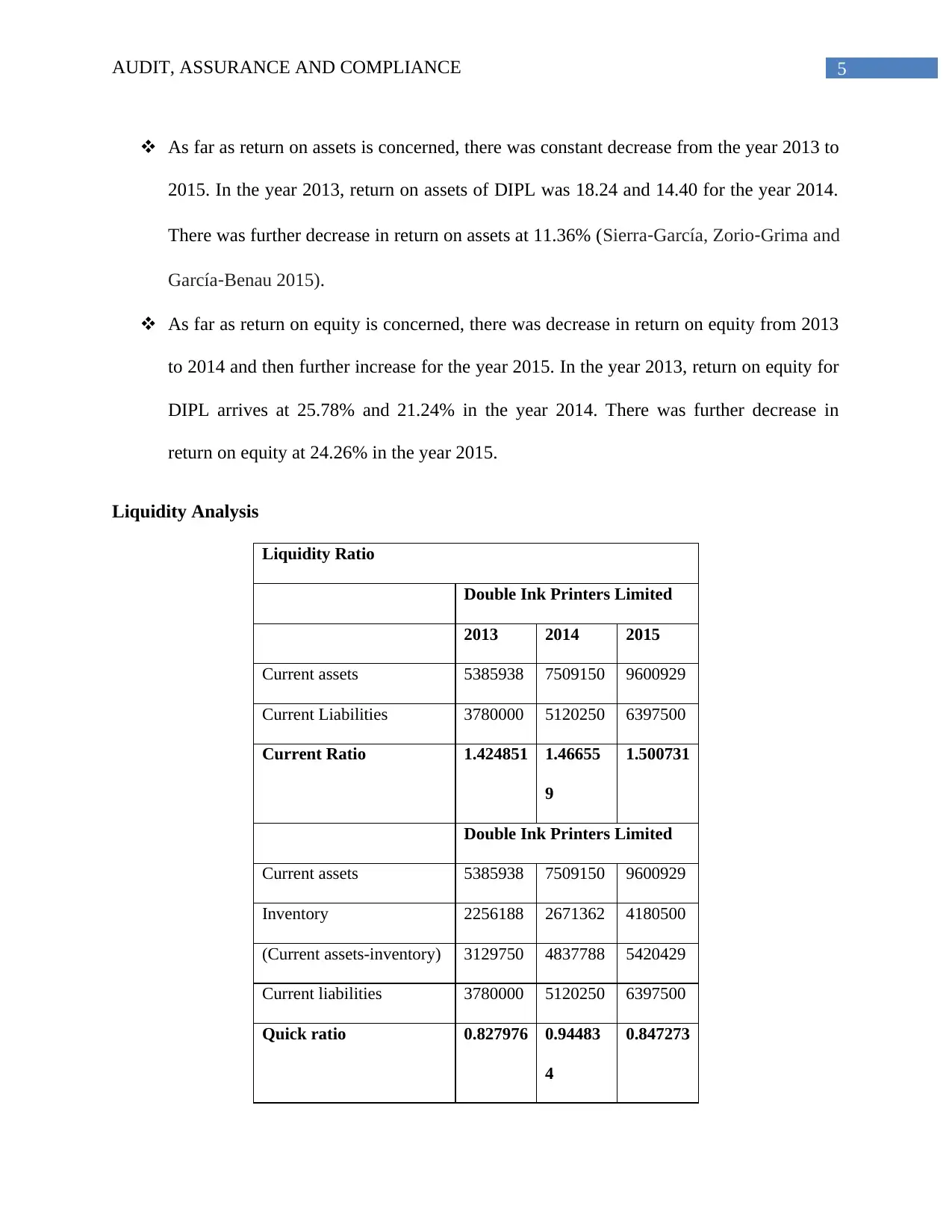

As far as return on assets is concerned, there was constant decrease from the year 2013 to

2015. In the year 2013, return on assets of DIPL was 18.24 and 14.40 for the year 2014.

There was further decrease in return on assets at 11.36% (Sierra‐García, Zorio‐Grima and

García‐Benau 2015).

As far as return on equity is concerned, there was decrease in return on equity from 2013

to 2014 and then further increase for the year 2015. In the year 2013, return on equity for

DIPL arrives at 25.78% and 21.24% in the year 2014. There was further decrease in

return on equity at 24.26% in the year 2015.

Liquidity Analysis

Liquidity Ratio

Double Ink Printers Limited

2013 2014 2015

Current assets 5385938 7509150 9600929

Current Liabilities 3780000 5120250 6397500

Current Ratio 1.424851 1.46655

9

1.500731

Double Ink Printers Limited

Current assets 5385938 7509150 9600929

Inventory 2256188 2671362 4180500

(Current assets-inventory) 3129750 4837788 5420429

Current liabilities 3780000 5120250 6397500

Quick ratio 0.827976 0.94483

4

0.847273

As far as return on assets is concerned, there was constant decrease from the year 2013 to

2015. In the year 2013, return on assets of DIPL was 18.24 and 14.40 for the year 2014.

There was further decrease in return on assets at 11.36% (Sierra‐García, Zorio‐Grima and

García‐Benau 2015).

As far as return on equity is concerned, there was decrease in return on equity from 2013

to 2014 and then further increase for the year 2015. In the year 2013, return on equity for

DIPL arrives at 25.78% and 21.24% in the year 2014. There was further decrease in

return on equity at 24.26% in the year 2015.

Liquidity Analysis

Liquidity Ratio

Double Ink Printers Limited

2013 2014 2015

Current assets 5385938 7509150 9600929

Current Liabilities 3780000 5120250 6397500

Current Ratio 1.424851 1.46655

9

1.500731

Double Ink Printers Limited

Current assets 5385938 7509150 9600929

Inventory 2256188 2671362 4180500

(Current assets-inventory) 3129750 4837788 5420429

Current liabilities 3780000 5120250 6397500

Quick ratio 0.827976 0.94483

4

0.847273

6AUDIT, ASSURANCE AND COMPLIANCE

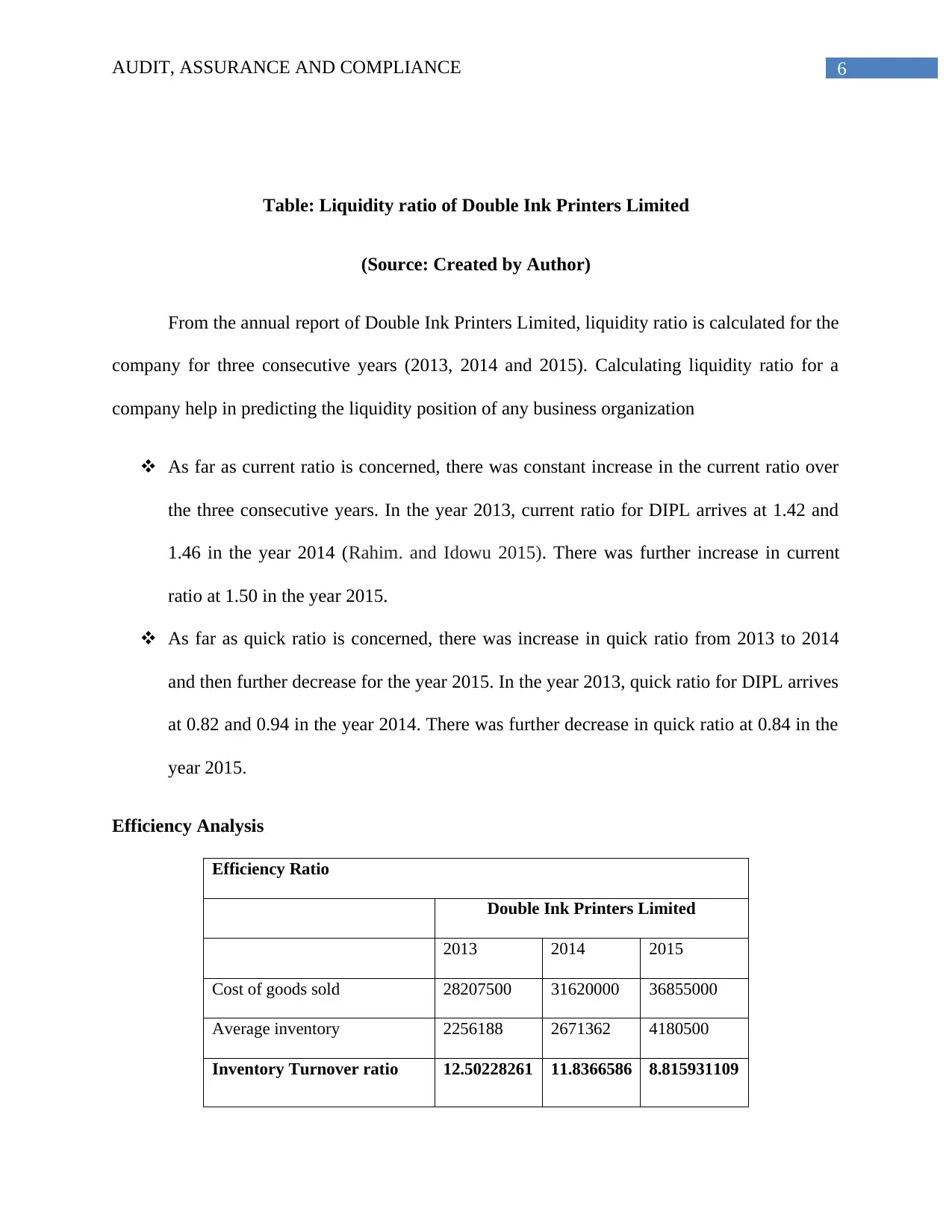

Table: Liquidity ratio of Double Ink Printers Limited

(Source: Created by Author)

From the annual report of Double Ink Printers Limited, liquidity ratio is calculated for the

company for three consecutive years (2013, 2014 and 2015). Calculating liquidity ratio for a

company help in predicting the liquidity position of any business organization

As far as current ratio is concerned, there was constant increase in the current ratio over

the three consecutive years. In the year 2013, current ratio for DIPL arrives at 1.42 and

1.46 in the year 2014 (Rahim. and Idowu 2015). There was further increase in current

ratio at 1.50 in the year 2015.

As far as quick ratio is concerned, there was increase in quick ratio from 2013 to 2014

and then further decrease for the year 2015. In the year 2013, quick ratio for DIPL arrives

at 0.82 and 0.94 in the year 2014. There was further decrease in quick ratio at 0.84 in the

year 2015.

Efficiency Analysis

Efficiency Ratio

Double Ink Printers Limited

2013 2014 2015

Cost of goods sold 28207500 31620000 36855000

Average inventory 2256188 2671362 4180500

Inventory Turnover ratio 12.50228261 11.8366586 8.815931109

Table: Liquidity ratio of Double Ink Printers Limited

(Source: Created by Author)

From the annual report of Double Ink Printers Limited, liquidity ratio is calculated for the

company for three consecutive years (2013, 2014 and 2015). Calculating liquidity ratio for a

company help in predicting the liquidity position of any business organization

As far as current ratio is concerned, there was constant increase in the current ratio over

the three consecutive years. In the year 2013, current ratio for DIPL arrives at 1.42 and

1.46 in the year 2014 (Rahim. and Idowu 2015). There was further increase in current

ratio at 1.50 in the year 2015.

As far as quick ratio is concerned, there was increase in quick ratio from 2013 to 2014

and then further decrease for the year 2015. In the year 2013, quick ratio for DIPL arrives

at 0.82 and 0.94 in the year 2014. There was further decrease in quick ratio at 0.84 in the

year 2015.

Efficiency Analysis

Efficiency Ratio

Double Ink Printers Limited

2013 2014 2015

Cost of goods sold 28207500 31620000 36855000

Average inventory 2256188 2671362 4180500

Inventory Turnover ratio 12.50228261 11.8366586 8.815931109

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

7AUDIT, ASSURANCE AND COMPLIANCE

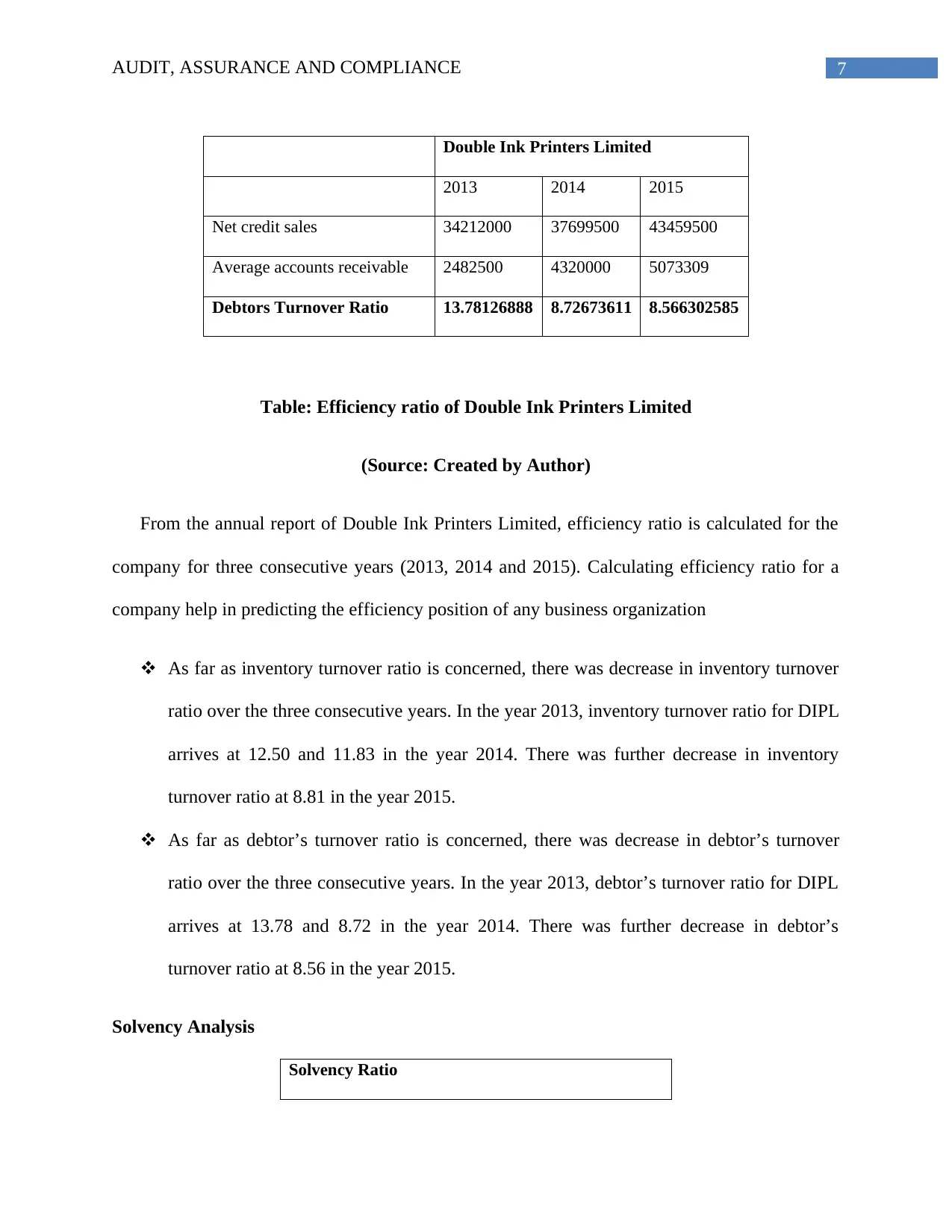

Double Ink Printers Limited

2013 2014 2015

Net credit sales 34212000 37699500 43459500

Average accounts receivable 2482500 4320000 5073309

Debtors Turnover Ratio 13.78126888 8.72673611 8.566302585

Table: Efficiency ratio of Double Ink Printers Limited

(Source: Created by Author)

From the annual report of Double Ink Printers Limited, efficiency ratio is calculated for the

company for three consecutive years (2013, 2014 and 2015). Calculating efficiency ratio for a

company help in predicting the efficiency position of any business organization

As far as inventory turnover ratio is concerned, there was decrease in inventory turnover

ratio over the three consecutive years. In the year 2013, inventory turnover ratio for DIPL

arrives at 12.50 and 11.83 in the year 2014. There was further decrease in inventory

turnover ratio at 8.81 in the year 2015.

As far as debtor’s turnover ratio is concerned, there was decrease in debtor’s turnover

ratio over the three consecutive years. In the year 2013, debtor’s turnover ratio for DIPL

arrives at 13.78 and 8.72 in the year 2014. There was further decrease in debtor’s

turnover ratio at 8.56 in the year 2015.

Solvency Analysis

Solvency Ratio

Double Ink Printers Limited

2013 2014 2015

Net credit sales 34212000 37699500 43459500

Average accounts receivable 2482500 4320000 5073309

Debtors Turnover Ratio 13.78126888 8.72673611 8.566302585

Table: Efficiency ratio of Double Ink Printers Limited

(Source: Created by Author)

From the annual report of Double Ink Printers Limited, efficiency ratio is calculated for the

company for three consecutive years (2013, 2014 and 2015). Calculating efficiency ratio for a

company help in predicting the efficiency position of any business organization

As far as inventory turnover ratio is concerned, there was decrease in inventory turnover

ratio over the three consecutive years. In the year 2013, inventory turnover ratio for DIPL

arrives at 12.50 and 11.83 in the year 2014. There was further decrease in inventory

turnover ratio at 8.81 in the year 2015.

As far as debtor’s turnover ratio is concerned, there was decrease in debtor’s turnover

ratio over the three consecutive years. In the year 2013, debtor’s turnover ratio for DIPL

arrives at 13.78 and 8.72 in the year 2014. There was further decrease in debtor’s

turnover ratio at 8.56 in the year 2015.

Solvency Analysis

Solvency Ratio

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

8AUDIT, ASSURANCE AND COMPLIANCE

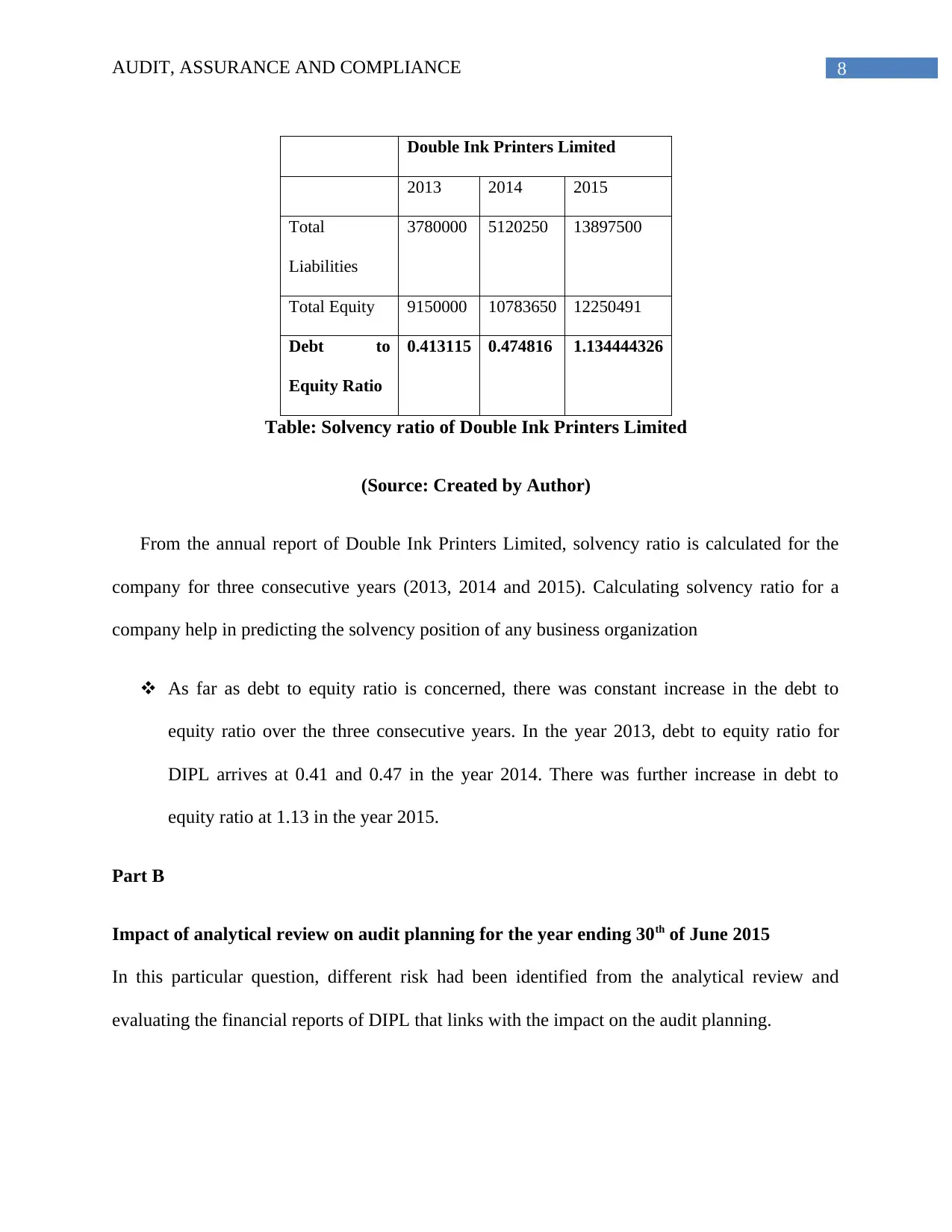

Double Ink Printers Limited

2013 2014 2015

Total

Liabilities

3780000 5120250 13897500

Total Equity 9150000 10783650 12250491

Debt to

Equity Ratio

0.413115 0.474816 1.134444326

Table: Solvency ratio of Double Ink Printers Limited

(Source: Created by Author)

From the annual report of Double Ink Printers Limited, solvency ratio is calculated for the

company for three consecutive years (2013, 2014 and 2015). Calculating solvency ratio for a

company help in predicting the solvency position of any business organization

As far as debt to equity ratio is concerned, there was constant increase in the debt to

equity ratio over the three consecutive years. In the year 2013, debt to equity ratio for

DIPL arrives at 0.41 and 0.47 in the year 2014. There was further increase in debt to

equity ratio at 1.13 in the year 2015.

Part B

Impact of analytical review on audit planning for the year ending 30th of June 2015

In this particular question, different risk had been identified from the analytical review and

evaluating the financial reports of DIPL that links with the impact on the audit planning.

Double Ink Printers Limited

2013 2014 2015

Total

Liabilities

3780000 5120250 13897500

Total Equity 9150000 10783650 12250491

Debt to

Equity Ratio

0.413115 0.474816 1.134444326

Table: Solvency ratio of Double Ink Printers Limited

(Source: Created by Author)

From the annual report of Double Ink Printers Limited, solvency ratio is calculated for the

company for three consecutive years (2013, 2014 and 2015). Calculating solvency ratio for a

company help in predicting the solvency position of any business organization

As far as debt to equity ratio is concerned, there was constant increase in the debt to

equity ratio over the three consecutive years. In the year 2013, debt to equity ratio for

DIPL arrives at 0.41 and 0.47 in the year 2014. There was further increase in debt to

equity ratio at 1.13 in the year 2015.

Part B

Impact of analytical review on audit planning for the year ending 30th of June 2015

In this particular question, different risk had been identified from the analytical review and

evaluating the financial reports of DIPL that links with the impact on the audit planning.

9AUDIT, ASSURANCE AND COMPLIANCE

On analysis, it is noted that the profitability of DIPL had not improved in the year 2015.

There had been decline in the profits of DIPL that lead to issue of going concern ability

for business organization. Therefore, detailed analysis need to make for DIPL where the

company should plan for exploring the future prospects (Louwers et al. 2015).

On analysis, it is noted that the current ratio of DIPL has improved in the year 2015. By

this, it is understood that there is proper writing back of allowance for any loss present

for stock or inventory. Hence, in-depth analysis needs to perform on inventory allowance

for checking over the validity of actions (Lenz and Hahn 2015).

On analysis, it is noted there is increased financial risk present at DIPL. In this case, the

disclosures are related to risk that need to be analyzed after checking the fact whether

information for the same had been properly declared in the reports.

On analysis, it is noted that there is decline in the efficiency of management at debt to

equity ratio where the company failed to manage the current assets and should make an

effort for identifying the possible reason to do so (Knechel and Salterio 2016).

On analysis, it is noted that the profitability of DIPL had not improved in the year 2015.

There had been decline in the profits of DIPL that lead to issue of going concern ability

for business organization. Therefore, detailed analysis need to make for DIPL where the

company should plan for exploring the future prospects (Louwers et al. 2015).

On analysis, it is noted that the current ratio of DIPL has improved in the year 2015. By

this, it is understood that there is proper writing back of allowance for any loss present

for stock or inventory. Hence, in-depth analysis needs to perform on inventory allowance

for checking over the validity of actions (Lenz and Hahn 2015).

On analysis, it is noted there is increased financial risk present at DIPL. In this case, the

disclosures are related to risk that need to be analyzed after checking the fact whether

information for the same had been properly declared in the reports.

On analysis, it is noted that there is decline in the efficiency of management at debt to

equity ratio where the company failed to manage the current assets and should make an

effort for identifying the possible reason to do so (Knechel and Salterio 2016).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

10AUDIT, ASSURANCE AND COMPLIANCE

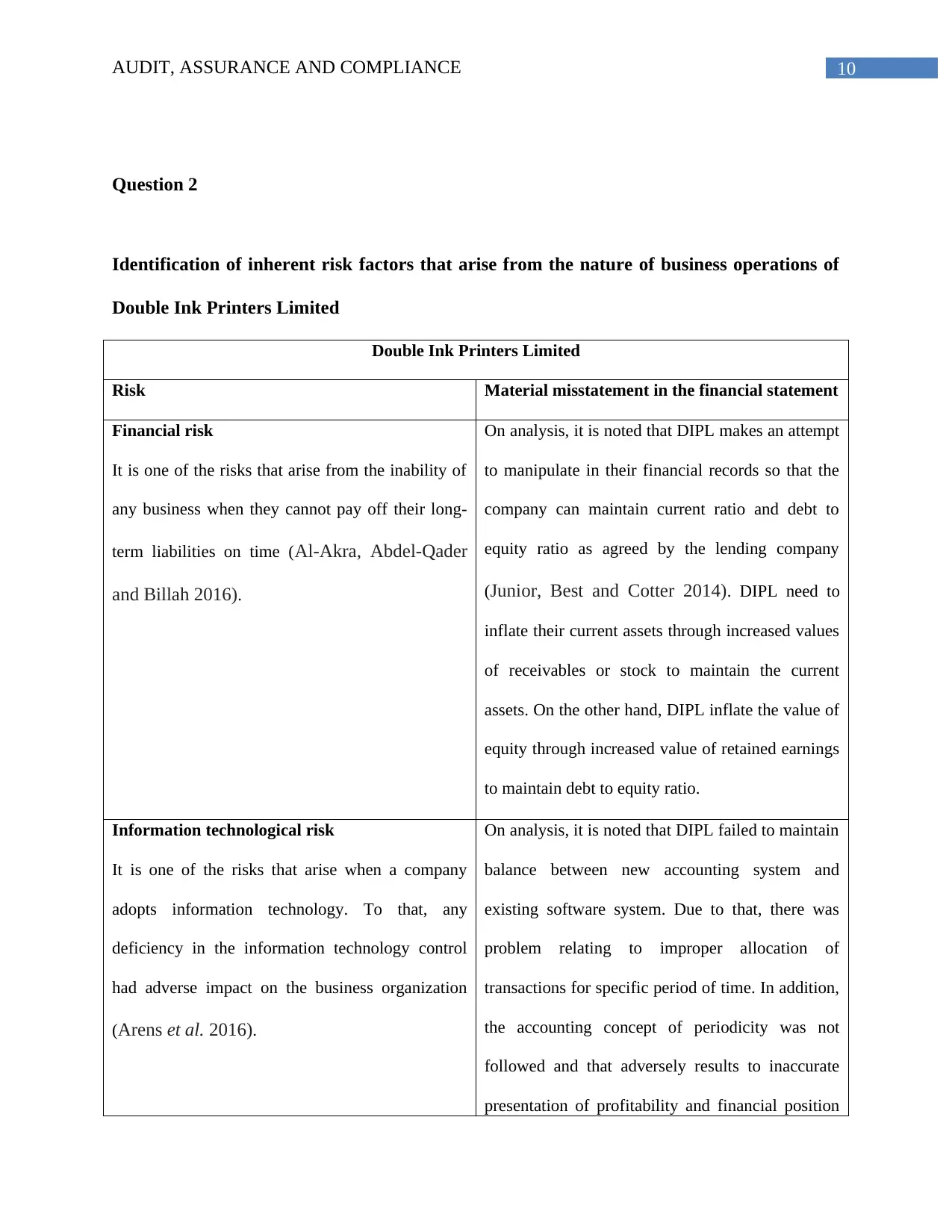

Question 2

Identification of inherent risk factors that arise from the nature of business operations of

Double Ink Printers Limited

Double Ink Printers Limited

Risk Material misstatement in the financial statement

Financial risk

It is one of the risks that arise from the inability of

any business when they cannot pay off their long-

term liabilities on time (Al-Akra, Abdel-Qader

and Billah 2016).

On analysis, it is noted that DIPL makes an attempt

to manipulate in their financial records so that the

company can maintain current ratio and debt to

equity ratio as agreed by the lending company

(Junior, Best and Cotter 2014). DIPL need to

inflate their current assets through increased values

of receivables or stock to maintain the current

assets. On the other hand, DIPL inflate the value of

equity through increased value of retained earnings

to maintain debt to equity ratio.

Information technological risk

It is one of the risks that arise when a company

adopts information technology. To that, any

deficiency in the information technology control

had adverse impact on the business organization

(Arens et al. 2016).

On analysis, it is noted that DIPL failed to maintain

balance between new accounting system and

existing software system. Due to that, there was

problem relating to improper allocation of

transactions for specific period of time. In addition,

the accounting concept of periodicity was not

followed and that adversely results to inaccurate

presentation of profitability and financial position

Question 2

Identification of inherent risk factors that arise from the nature of business operations of

Double Ink Printers Limited

Double Ink Printers Limited

Risk Material misstatement in the financial statement

Financial risk

It is one of the risks that arise from the inability of

any business when they cannot pay off their long-

term liabilities on time (Al-Akra, Abdel-Qader

and Billah 2016).

On analysis, it is noted that DIPL makes an attempt

to manipulate in their financial records so that the

company can maintain current ratio and debt to

equity ratio as agreed by the lending company

(Junior, Best and Cotter 2014). DIPL need to

inflate their current assets through increased values

of receivables or stock to maintain the current

assets. On the other hand, DIPL inflate the value of

equity through increased value of retained earnings

to maintain debt to equity ratio.

Information technological risk

It is one of the risks that arise when a company

adopts information technology. To that, any

deficiency in the information technology control

had adverse impact on the business organization

(Arens et al. 2016).

On analysis, it is noted that DIPL failed to maintain

balance between new accounting system and

existing software system. Due to that, there was

problem relating to improper allocation of

transactions for specific period of time. In addition,

the accounting concept of periodicity was not

followed and that adversely results to inaccurate

presentation of profitability and financial position

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

11AUDIT, ASSURANCE AND COMPLIANCE

of DIPL (Eilifsen et al. 2013).

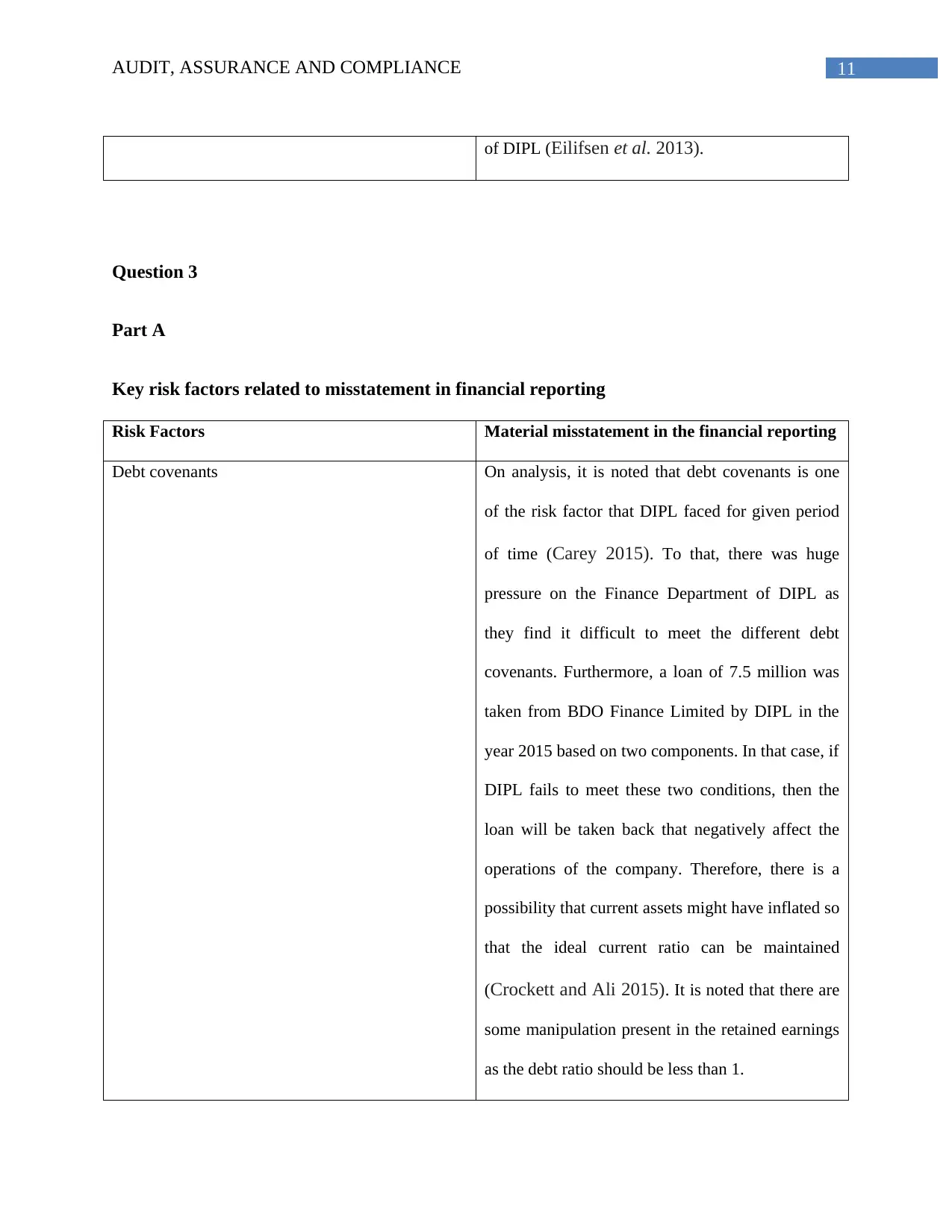

Question 3

Part A

Key risk factors related to misstatement in financial reporting

Risk Factors Material misstatement in the financial reporting

Debt covenants On analysis, it is noted that debt covenants is one

of the risk factor that DIPL faced for given period

of time (Carey 2015). To that, there was huge

pressure on the Finance Department of DIPL as

they find it difficult to meet the different debt

covenants. Furthermore, a loan of 7.5 million was

taken from BDO Finance Limited by DIPL in the

year 2015 based on two components. In that case, if

DIPL fails to meet these two conditions, then the

loan will be taken back that negatively affect the

operations of the company. Therefore, there is a

possibility that current assets might have inflated so

that the ideal current ratio can be maintained

(Crockett and Ali 2015). It is noted that there are

some manipulation present in the retained earnings

as the debt ratio should be less than 1.

of DIPL (Eilifsen et al. 2013).

Question 3

Part A

Key risk factors related to misstatement in financial reporting

Risk Factors Material misstatement in the financial reporting

Debt covenants On analysis, it is noted that debt covenants is one

of the risk factor that DIPL faced for given period

of time (Carey 2015). To that, there was huge

pressure on the Finance Department of DIPL as

they find it difficult to meet the different debt

covenants. Furthermore, a loan of 7.5 million was

taken from BDO Finance Limited by DIPL in the

year 2015 based on two components. In that case, if

DIPL fails to meet these two conditions, then the

loan will be taken back that negatively affect the

operations of the company. Therefore, there is a

possibility that current assets might have inflated so

that the ideal current ratio can be maintained

(Crockett and Ali 2015). It is noted that there are

some manipulation present in the retained earnings

as the debt ratio should be less than 1.

12AUDIT, ASSURANCE AND COMPLIANCE

Nature of control environment On analysis, it is noted that nature of control

environment is one of the risk factor that was faced

by DIPL for specified time period. Nature of

control environment lead to existence of fraudulent

practices in financial reporting that exists due to

poor defined job description of poor segregation of

work. In addition, there is a possibility that stock

can be manipulated through portraying less stock at

the time of arrival of cash. Hence, there is improper

system used at the time of documentation that helps

in preventing fraudulent activities (Cohen and

Simnett 2014).

Part B

Effect of risk factors on conduct of audit

Effect of debt covenants on audit plan- DIPL need to balance their current assets and

current liabilities after checking whether there is any inflation present in current assets or

deflation in current liabilities (Christopher 2015). Therefore, the balance of equity need to

be analyzed through careful verification of retained earnings.

Effect of control environment on audit plan- DIPL need to check the balance of stock or

inventory. The quantity of orders placed for the purchase of stock need to match with the

quantity received and there should be no manipulation present and conducted by any

accounts payable clerks (Carson, Redmayne and Liao 2014).

Nature of control environment On analysis, it is noted that nature of control

environment is one of the risk factor that was faced

by DIPL for specified time period. Nature of

control environment lead to existence of fraudulent

practices in financial reporting that exists due to

poor defined job description of poor segregation of

work. In addition, there is a possibility that stock

can be manipulated through portraying less stock at

the time of arrival of cash. Hence, there is improper

system used at the time of documentation that helps

in preventing fraudulent activities (Cohen and

Simnett 2014).

Part B

Effect of risk factors on conduct of audit

Effect of debt covenants on audit plan- DIPL need to balance their current assets and

current liabilities after checking whether there is any inflation present in current assets or

deflation in current liabilities (Christopher 2015). Therefore, the balance of equity need to

be analyzed through careful verification of retained earnings.

Effect of control environment on audit plan- DIPL need to check the balance of stock or

inventory. The quantity of orders placed for the purchase of stock need to match with the

quantity received and there should be no manipulation present and conducted by any

accounts payable clerks (Carson, Redmayne and Liao 2014).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14