University Audit Assurance and Compliance Report for DIPL Analysis

VerifiedAdded on 2020/03/04

|11

|2064

|177

Report

AI Summary

This report, focusing on audit assurance and compliance, analyzes the financial reporting of DIPL. It begins with applying analytical procedures to the financial information, examining ratios such as current ratio, profit margin, and solvency ratio across multiple years to identify trends and their impact on audit planning. The report then identifies inherent risk factors arising from the nature of DIPL's business operations, including issues related to employee competency, IT implementation, and CEO succession. These risks are linked to potential material misstatements in the financial reports. Finally, the report identifies and explains two key fraud risk factors related to misstatements arising from fraudulent financial reporting, such as asset loss and financial reporting fraud, providing a comprehensive overview of the audit process and risk assessment.

Running head: AUDIT ASSURANCE AND COMPLIANCE

Audit Assurance and Compliance

Name of Student:

Name of University:

Author’s Note:

Audit Assurance and Compliance

Name of Student:

Name of University:

Author’s Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1AUDIT ASSURANCE AND COMPLIANCE

Table of Contents

Answer to Question 1:.....................................................................................................................2

Answer to Question 2:.....................................................................................................................3

Answer to Question 3:.....................................................................................................................6

Reference.........................................................................................................................................8

List of Appendix..............................................................................................................................9

Table of Contents

Answer to Question 1:.....................................................................................................................2

Answer to Question 2:.....................................................................................................................3

Answer to Question 3:.....................................................................................................................6

Reference.........................................................................................................................................8

List of Appendix..............................................................................................................................9

2AUDIT ASSURANCE AND COMPLIANCE

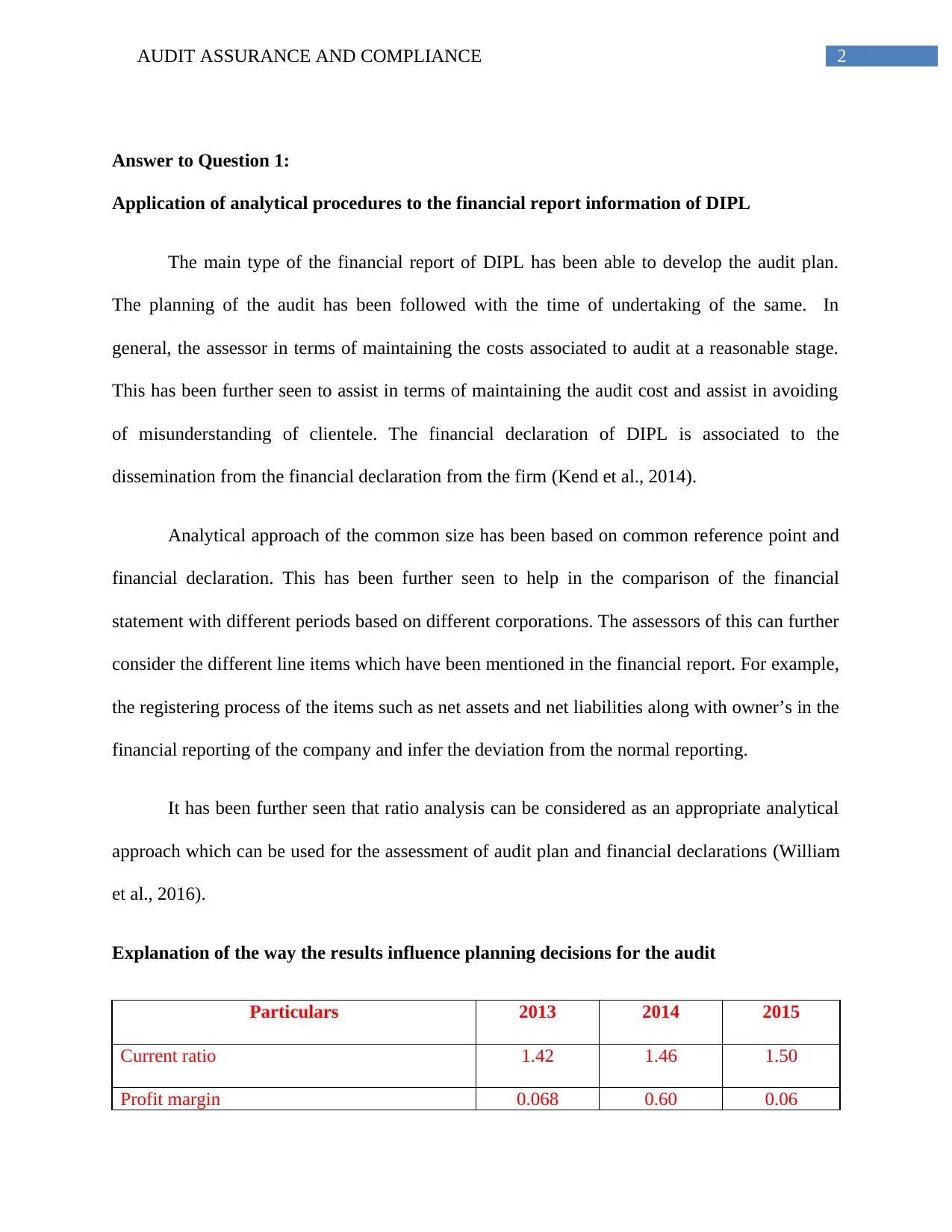

Answer to Question 1:

Application of analytical procedures to the financial report information of DIPL

The main type of the financial report of DIPL has been able to develop the audit plan.

The planning of the audit has been followed with the time of undertaking of the same. In

general, the assessor in terms of maintaining the costs associated to audit at a reasonable stage.

This has been further seen to assist in terms of maintaining the audit cost and assist in avoiding

of misunderstanding of clientele. The financial declaration of DIPL is associated to the

dissemination from the financial declaration from the firm (Kend et al., 2014).

Analytical approach of the common size has been based on common reference point and

financial declaration. This has been further seen to help in the comparison of the financial

statement with different periods based on different corporations. The assessors of this can further

consider the different line items which have been mentioned in the financial report. For example,

the registering process of the items such as net assets and net liabilities along with owner’s in the

financial reporting of the company and infer the deviation from the normal reporting.

It has been further seen that ratio analysis can be considered as an appropriate analytical

approach which can be used for the assessment of audit plan and financial declarations (William

et al., 2016).

Explanation of the way the results influence planning decisions for the audit

Particulars 2013 2014 2015

Current ratio 1.42 1.46 1.50

Profit margin 0.068 0.60 0.06

Answer to Question 1:

Application of analytical procedures to the financial report information of DIPL

The main type of the financial report of DIPL has been able to develop the audit plan.

The planning of the audit has been followed with the time of undertaking of the same. In

general, the assessor in terms of maintaining the costs associated to audit at a reasonable stage.

This has been further seen to assist in terms of maintaining the audit cost and assist in avoiding

of misunderstanding of clientele. The financial declaration of DIPL is associated to the

dissemination from the financial declaration from the firm (Kend et al., 2014).

Analytical approach of the common size has been based on common reference point and

financial declaration. This has been further seen to help in the comparison of the financial

statement with different periods based on different corporations. The assessors of this can further

consider the different line items which have been mentioned in the financial report. For example,

the registering process of the items such as net assets and net liabilities along with owner’s in the

financial reporting of the company and infer the deviation from the normal reporting.

It has been further seen that ratio analysis can be considered as an appropriate analytical

approach which can be used for the assessment of audit plan and financial declarations (William

et al., 2016).

Explanation of the way the results influence planning decisions for the audit

Particulars 2013 2014 2015

Current ratio 1.42 1.46 1.50

Profit margin 0.068 0.60 0.06

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3AUDIT ASSURANCE AND COMPLIANCE

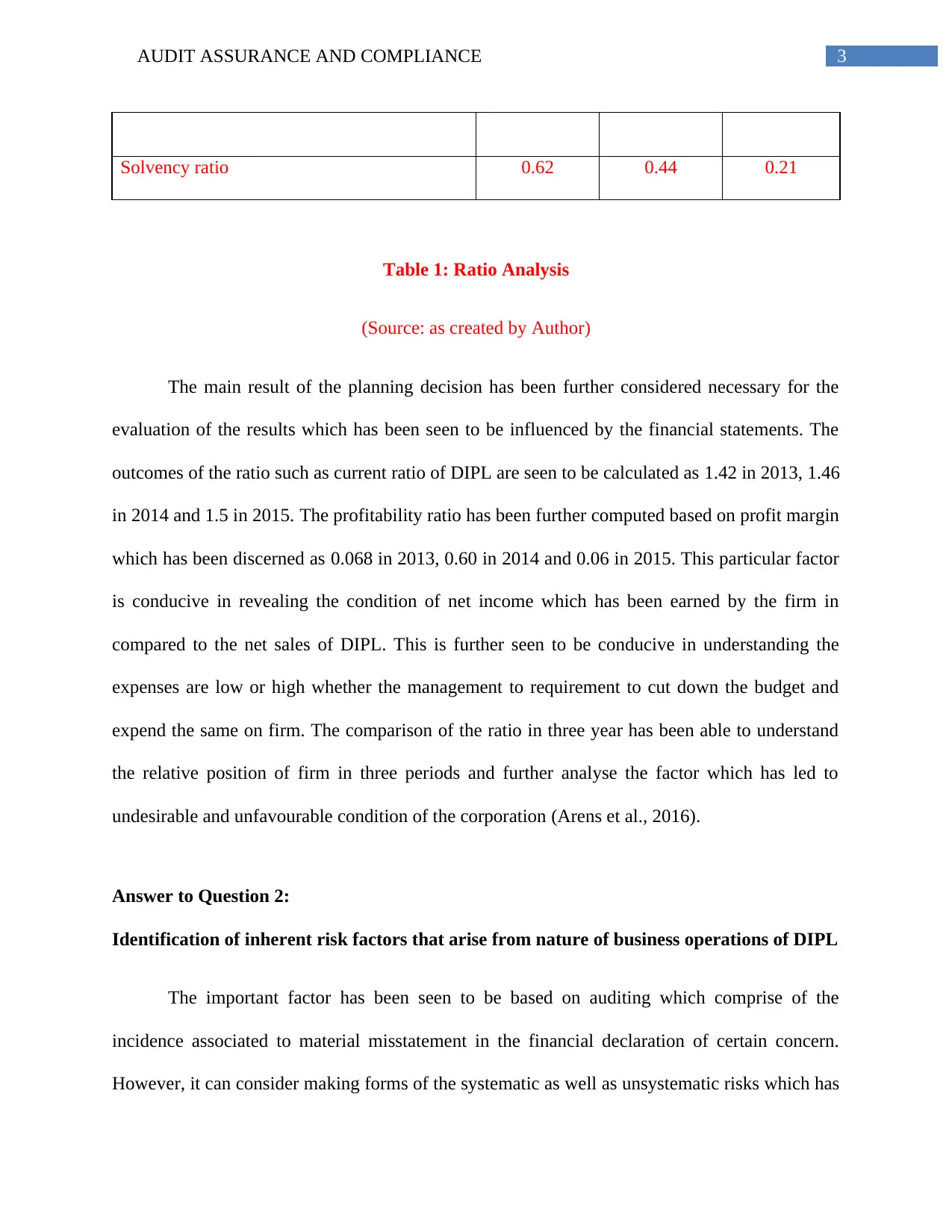

Solvency ratio 0.62 0.44 0.21

Table 1: Ratio Analysis

(Source: as created by Author)

The main result of the planning decision has been further considered necessary for the

evaluation of the results which has been seen to be influenced by the financial statements. The

outcomes of the ratio such as current ratio of DIPL are seen to be calculated as 1.42 in 2013, 1.46

in 2014 and 1.5 in 2015. The profitability ratio has been further computed based on profit margin

which has been discerned as 0.068 in 2013, 0.60 in 2014 and 0.06 in 2015. This particular factor

is conducive in revealing the condition of net income which has been earned by the firm in

compared to the net sales of DIPL. This is further seen to be conducive in understanding the

expenses are low or high whether the management to requirement to cut down the budget and

expend the same on firm. The comparison of the ratio in three year has been able to understand

the relative position of firm in three periods and further analyse the factor which has led to

undesirable and unfavourable condition of the corporation (Arens et al., 2016).

Answer to Question 2:

Identification of inherent risk factors that arise from nature of business operations of DIPL

The important factor has been seen to be based on auditing which comprise of the

incidence associated to material misstatement in the financial declaration of certain concern.

However, it can consider making forms of the systematic as well as unsystematic risks which has

Solvency ratio 0.62 0.44 0.21

Table 1: Ratio Analysis

(Source: as created by Author)

The main result of the planning decision has been further considered necessary for the

evaluation of the results which has been seen to be influenced by the financial statements. The

outcomes of the ratio such as current ratio of DIPL are seen to be calculated as 1.42 in 2013, 1.46

in 2014 and 1.5 in 2015. The profitability ratio has been further computed based on profit margin

which has been discerned as 0.068 in 2013, 0.60 in 2014 and 0.06 in 2015. This particular factor

is conducive in revealing the condition of net income which has been earned by the firm in

compared to the net sales of DIPL. This is further seen to be conducive in understanding the

expenses are low or high whether the management to requirement to cut down the budget and

expend the same on firm. The comparison of the ratio in three year has been able to understand

the relative position of firm in three periods and further analyse the factor which has led to

undesirable and unfavourable condition of the corporation (Arens et al., 2016).

Answer to Question 2:

Identification of inherent risk factors that arise from nature of business operations of DIPL

The important factor has been seen to be based on auditing which comprise of the

incidence associated to material misstatement in the financial declaration of certain concern.

However, it can consider making forms of the systematic as well as unsystematic risks which has

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4AUDIT ASSURANCE AND COMPLIANCE

been further seen to reflect the way financial misstatements are taken into consideration for

corporations. Despite of this, the risks associated may be seen to be based on both financial as

well as non-financial factors which can be possible for the financial and non-financial factors.

These factors can further avert a specific corporation for reflecting a true as well as fair view of

pertinent financial declarations. The identified risks can be further linked with the different risk

correlated based on the correlated to omit the risks of diverse errors which is not possible for a

particular bookkeeper. With essence of the risks diverse errors, the specific bookkeeping has

inherent risk which may be seen to take place from the nature of operations of DIPL (Messier et

al., 2014).

Based on the given considerations made in the study, it can be made certain that there has

been number of transactions which are related to accountants otherwise which has been not been

seen with corporation DIPL. The sequential direct lead in terms of the inconsistencies

particularly related to the ineffective planning of the sales activities. In addition to this, the

financial declarations have been seen to reveal the fact which the firm has failed to accomplish

the designated level of profit from the revenue based on sales. In particular the management

failure has been identified in terms of the specific requirements which have been further

identified with consequent adjustment of the functionalities.

Apart from the workers, DIPL has escalated the overall risk. Due to the lack of

proficiency and experience of the employees the inherent risk has increased substantially. This

has been observed due to the competency of member of the staff. The non-proficient workforce

can enhance the inherent risk to commit mistakes. The errors of the exclusion and the instances

have been considered based on misstated in the pecuniary announcement.

been further seen to reflect the way financial misstatements are taken into consideration for

corporations. Despite of this, the risks associated may be seen to be based on both financial as

well as non-financial factors which can be possible for the financial and non-financial factors.

These factors can further avert a specific corporation for reflecting a true as well as fair view of

pertinent financial declarations. The identified risks can be further linked with the different risk

correlated based on the correlated to omit the risks of diverse errors which is not possible for a

particular bookkeeper. With essence of the risks diverse errors, the specific bookkeeping has

inherent risk which may be seen to take place from the nature of operations of DIPL (Messier et

al., 2014).

Based on the given considerations made in the study, it can be made certain that there has

been number of transactions which are related to accountants otherwise which has been not been

seen with corporation DIPL. The sequential direct lead in terms of the inconsistencies

particularly related to the ineffective planning of the sales activities. In addition to this, the

financial declarations have been seen to reveal the fact which the firm has failed to accomplish

the designated level of profit from the revenue based on sales. In particular the management

failure has been identified in terms of the specific requirements which have been further

identified with consequent adjustment of the functionalities.

Apart from the workers, DIPL has escalated the overall risk. Due to the lack of

proficiency and experience of the employees the inherent risk has increased substantially. This

has been observed due to the competency of member of the staff. The non-proficient workforce

can enhance the inherent risk to commit mistakes. The errors of the exclusion and the instances

have been considered based on misstated in the pecuniary announcement.

5AUDIT ASSURANCE AND COMPLIANCE

The significant facts of the contribution towards the existing risks can be categorised

based on sections specifically devised for the environmental concerns along with external facets,

material misstatements in previous periods along with falsified exercises. Based on the

evaluation of the given case it has been seen that DIPL has been able to reflect on the significant

amount of inherent risks in the process of succession of CEO. In general CEO may be considered

as a different candidate and other individuals. However, some of the inherent risks involves

quality of procedure for selection and transition handling process. Hence, there are several risks

associated for the commencement of the process without complying with the strategy, inadequate

CEO involvement and the departure of candidates (Waldron, 2016).

Based on analysis of the case it is further revealed that the various types of

implementations for novel IT procedure have generated certain problems. DIPL did not had

sufficient number of staffs to handle the execution and carrying out of the reconciliation before

the new arrangement prior to the ear end. The initial testing process has revealed that the

transactions were not apportioned the correct time. This led to several incidents of material

misstatements and ministers of other inherent risks for omission in specific financial declaration.

In addition to this the recording of cash receipts were seen to be done by professional’s

expertise in finance we’re not able to handle the risks in an appropriate manner. The total

member of the staff needed to follow the proper sequence for Accounts Receivable and

registering the Accounts Receivable ledger for proper maintenance of the same. In addition to

this the bank reconciliation also needs to be regarded in an appropriate manner. The registering

of the revenues generated from the ebook and taking account of the reprint of textbooks may lead

to diverse nature of inherent risks due to several complexities involved in the process.

The significant facts of the contribution towards the existing risks can be categorised

based on sections specifically devised for the environmental concerns along with external facets,

material misstatements in previous periods along with falsified exercises. Based on the

evaluation of the given case it has been seen that DIPL has been able to reflect on the significant

amount of inherent risks in the process of succession of CEO. In general CEO may be considered

as a different candidate and other individuals. However, some of the inherent risks involves

quality of procedure for selection and transition handling process. Hence, there are several risks

associated for the commencement of the process without complying with the strategy, inadequate

CEO involvement and the departure of candidates (Waldron, 2016).

Based on analysis of the case it is further revealed that the various types of

implementations for novel IT procedure have generated certain problems. DIPL did not had

sufficient number of staffs to handle the execution and carrying out of the reconciliation before

the new arrangement prior to the ear end. The initial testing process has revealed that the

transactions were not apportioned the correct time. This led to several incidents of material

misstatements and ministers of other inherent risks for omission in specific financial declaration.

In addition to this the recording of cash receipts were seen to be done by professional’s

expertise in finance we’re not able to handle the risks in an appropriate manner. The total

member of the staff needed to follow the proper sequence for Accounts Receivable and

registering the Accounts Receivable ledger for proper maintenance of the same. In addition to

this the bank reconciliation also needs to be regarded in an appropriate manner. The registering

of the revenues generated from the ebook and taking account of the reprint of textbooks may lead

to diverse nature of inherent risks due to several complexities involved in the process.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6AUDIT ASSURANCE AND COMPLIANCE

Additionally, the evaluation process of raw material inventory was not seem to be

suitable since present cost of the paper was significantly higher than the average cost.

Risk and way it might affect the risk of material misstatement in the financial report

The identified the natures of the inherent risks are associated to material misstatement.

Excessive pressure on employees and management: - In general due to excessive burden on

staff members the bookkeeping gets affected. There has been certain attributes namely

propensity to encounter issues associated to cash flow, low liquidity with were operating

outcomes.

Integrity of the entire management:- DIPL lacks in terms of integrity and requisite and is also

expected to prepare for the loss of reputation.

Unusual pressure on management: - in several cases the material misstatements leads to

pecuniary declarations.

Nature of entity business: The leading growth process of DIPL has been considered with

competitive scenario. However, these factors might affect the overall inherent risk involved in

the business and audit planning structure (Arens et al., 2015).

Answer to Question 3:

A) Identification and explanation of two key fraud risk factors relating to

misstatements arising from fraudulent financial reporting

Additionally, the evaluation process of raw material inventory was not seem to be

suitable since present cost of the paper was significantly higher than the average cost.

Risk and way it might affect the risk of material misstatement in the financial report

The identified the natures of the inherent risks are associated to material misstatement.

Excessive pressure on employees and management: - In general due to excessive burden on

staff members the bookkeeping gets affected. There has been certain attributes namely

propensity to encounter issues associated to cash flow, low liquidity with were operating

outcomes.

Integrity of the entire management:- DIPL lacks in terms of integrity and requisite and is also

expected to prepare for the loss of reputation.

Unusual pressure on management: - in several cases the material misstatements leads to

pecuniary declarations.

Nature of entity business: The leading growth process of DIPL has been considered with

competitive scenario. However, these factors might affect the overall inherent risk involved in

the business and audit planning structure (Arens et al., 2015).

Answer to Question 3:

A) Identification and explanation of two key fraud risk factors relating to

misstatements arising from fraudulent financial reporting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7AUDIT ASSURANCE AND COMPLIANCE

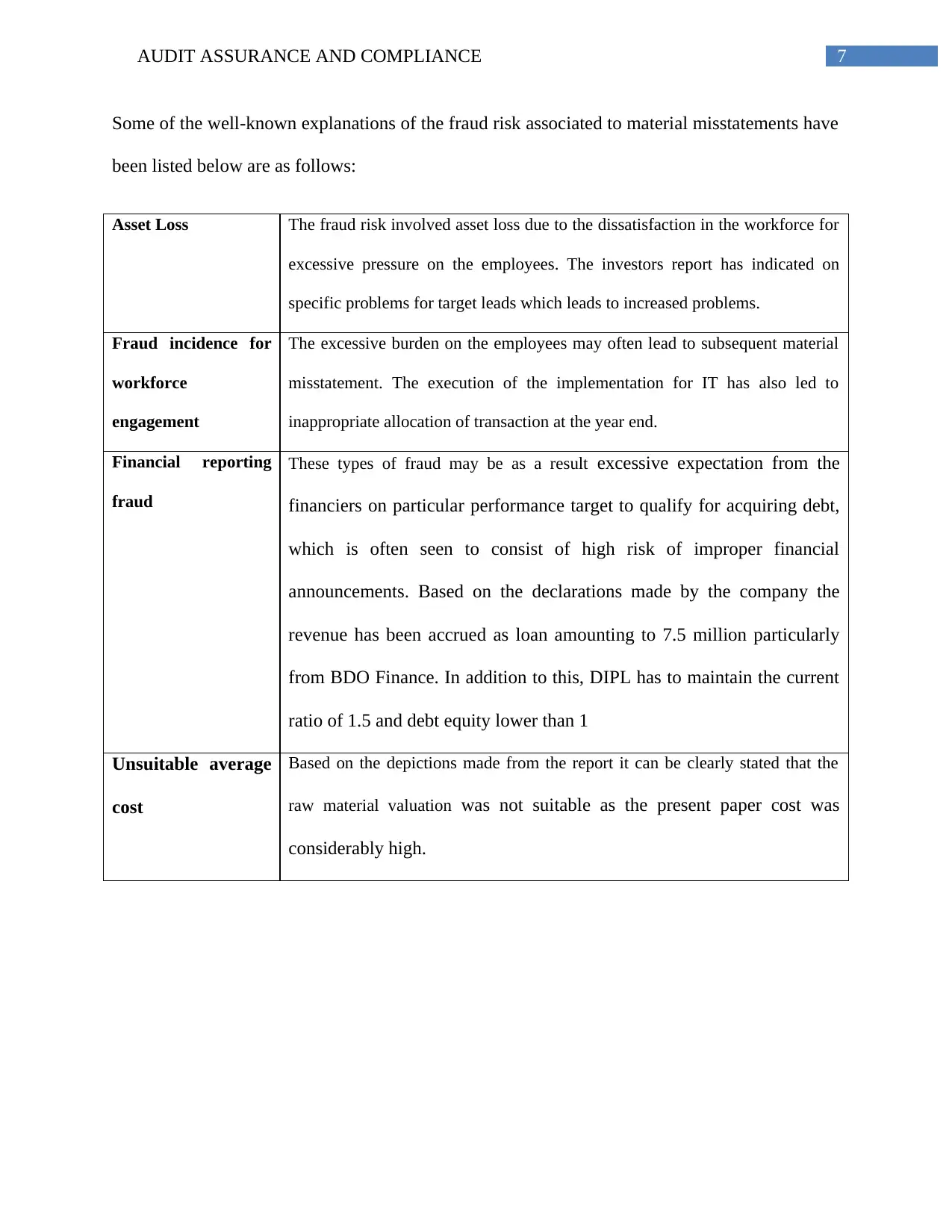

Some of the well-known explanations of the fraud risk associated to material misstatements have

been listed below are as follows:

Asset Loss The fraud risk involved asset loss due to the dissatisfaction in the workforce for

excessive pressure on the employees. The investors report has indicated on

specific problems for target leads which leads to increased problems.

Fraud incidence for

workforce

engagement

The excessive burden on the employees may often lead to subsequent material

misstatement. The execution of the implementation for IT has also led to

inappropriate allocation of transaction at the year end.

Financial reporting

fraud

These types of fraud may be as a result excessive expectation from the

financiers on particular performance target to qualify for acquiring debt,

which is often seen to consist of high risk of improper financial

announcements. Based on the declarations made by the company the

revenue has been accrued as loan amounting to 7.5 million particularly

from BDO Finance. In addition to this, DIPL has to maintain the current

ratio of 1.5 and debt equity lower than 1

Unsuitable average

cost

Based on the depictions made from the report it can be clearly stated that the

raw material valuation was not suitable as the present paper cost was

considerably high.

Some of the well-known explanations of the fraud risk associated to material misstatements have

been listed below are as follows:

Asset Loss The fraud risk involved asset loss due to the dissatisfaction in the workforce for

excessive pressure on the employees. The investors report has indicated on

specific problems for target leads which leads to increased problems.

Fraud incidence for

workforce

engagement

The excessive burden on the employees may often lead to subsequent material

misstatement. The execution of the implementation for IT has also led to

inappropriate allocation of transaction at the year end.

Financial reporting

fraud

These types of fraud may be as a result excessive expectation from the

financiers on particular performance target to qualify for acquiring debt,

which is often seen to consist of high risk of improper financial

announcements. Based on the declarations made by the company the

revenue has been accrued as loan amounting to 7.5 million particularly

from BDO Finance. In addition to this, DIPL has to maintain the current

ratio of 1.5 and debt equity lower than 1

Unsuitable average

cost

Based on the depictions made from the report it can be clearly stated that the

raw material valuation was not suitable as the present paper cost was

considerably high.

8AUDIT ASSURANCE AND COMPLIANCE

Reference

Arens, A. A., Elder, R. J., Beasley, M. S., & Hogan, C. E. (2016). Auditing and assurance

services. Pearson.

Arens, A. A., Elder, R. J., Beasley, M. S., & Jones, J. (2015). Auditing: The Art and Science of

Assurance Engagements. Pearson Canada.

Kend, M., Houghton, K. A., & Jubb, C. (2014). Competition issues in the market for audit and

assurance services: are the concerns justified?. Australian Accounting Review, 24(4),

313-320.

Messier, W. F., Glover, S. M., & Prawitt, D. F. (2014). Jasa audit dan assurance: pendekatan

sistematis. Jakarta: Sa-lemba Empat.

Waldron, M. (2016). The Future of Audit. CFA Institute Magazine, 27(3), 55-55.

William Jr, M., Glover, S., & Prawitt, D. (2016). Auditing and assurance services: A systematic

approach. McGraw-Hill Education.

Reference

Arens, A. A., Elder, R. J., Beasley, M. S., & Hogan, C. E. (2016). Auditing and assurance

services. Pearson.

Arens, A. A., Elder, R. J., Beasley, M. S., & Jones, J. (2015). Auditing: The Art and Science of

Assurance Engagements. Pearson Canada.

Kend, M., Houghton, K. A., & Jubb, C. (2014). Competition issues in the market for audit and

assurance services: are the concerns justified?. Australian Accounting Review, 24(4),

313-320.

Messier, W. F., Glover, S. M., & Prawitt, D. F. (2014). Jasa audit dan assurance: pendekatan

sistematis. Jakarta: Sa-lemba Empat.

Waldron, M. (2016). The Future of Audit. CFA Institute Magazine, 27(3), 55-55.

William Jr, M., Glover, S., & Prawitt, D. (2016). Auditing and assurance services: A systematic

approach. McGraw-Hill Education.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9AUDIT ASSURANCE AND COMPLIANCE

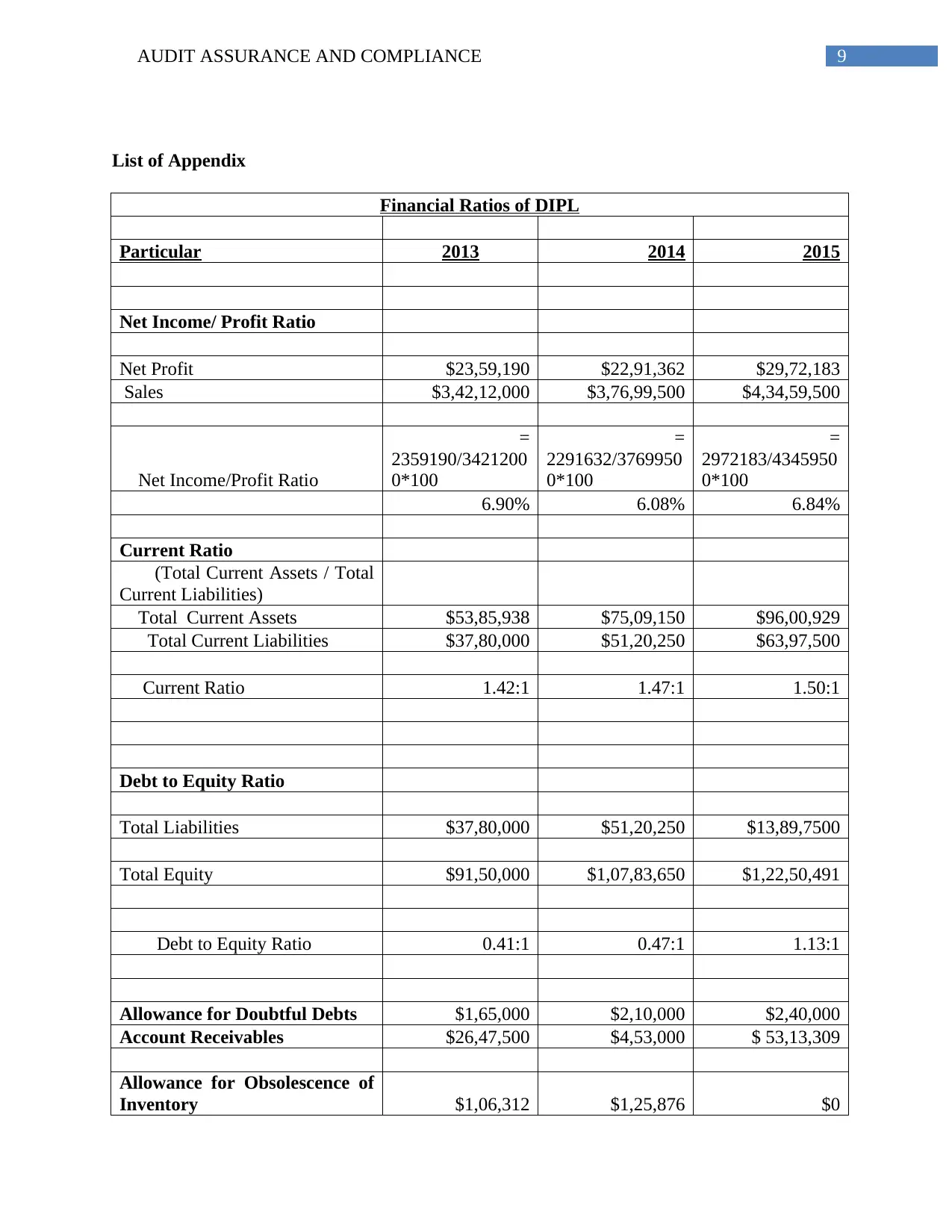

List of Appendix

Financial Ratios of DIPL

Particular 2013 2014 2015

Net Income/ Profit Ratio

Net Profit $23,59,190 $22,91,362 $29,72,183

Sales $3,42,12,000 $3,76,99,500 $4,34,59,500

Net Income/Profit Ratio

=

2359190/3421200

0*100

=

2291632/3769950

0*100

=

2972183/4345950

0*100

6.90% 6.08% 6.84%

Current Ratio

(Total Current Assets / Total

Current Liabilities)

Total Current Assets $53,85,938 $75,09,150 $96,00,929

Total Current Liabilities $37,80,000 $51,20,250 $63,97,500

Current Ratio 1.42:1 1.47:1 1.50:1

Debt to Equity Ratio

Total Liabilities $37,80,000 $51,20,250 $13,89,7500

Total Equity $91,50,000 $1,07,83,650 $1,22,50,491

Debt to Equity Ratio 0.41:1 0.47:1 1.13:1

Allowance for Doubtful Debts $1,65,000 $2,10,000 $2,40,000

Account Receivables $26,47,500 $4,53,000 $ 53,13,309

Allowance for Obsolescence of

Inventory $1,06,312 $1,25,876 $0

List of Appendix

Financial Ratios of DIPL

Particular 2013 2014 2015

Net Income/ Profit Ratio

Net Profit $23,59,190 $22,91,362 $29,72,183

Sales $3,42,12,000 $3,76,99,500 $4,34,59,500

Net Income/Profit Ratio

=

2359190/3421200

0*100

=

2291632/3769950

0*100

=

2972183/4345950

0*100

6.90% 6.08% 6.84%

Current Ratio

(Total Current Assets / Total

Current Liabilities)

Total Current Assets $53,85,938 $75,09,150 $96,00,929

Total Current Liabilities $37,80,000 $51,20,250 $63,97,500

Current Ratio 1.42:1 1.47:1 1.50:1

Debt to Equity Ratio

Total Liabilities $37,80,000 $51,20,250 $13,89,7500

Total Equity $91,50,000 $1,07,83,650 $1,22,50,491

Debt to Equity Ratio 0.41:1 0.47:1 1.13:1

Allowance for Doubtful Debts $1,65,000 $2,10,000 $2,40,000

Account Receivables $26,47,500 $4,53,000 $ 53,13,309

Allowance for Obsolescence of

Inventory $1,06,312 $1,25,876 $0

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10AUDIT ASSURANCE AND COMPLIANCE

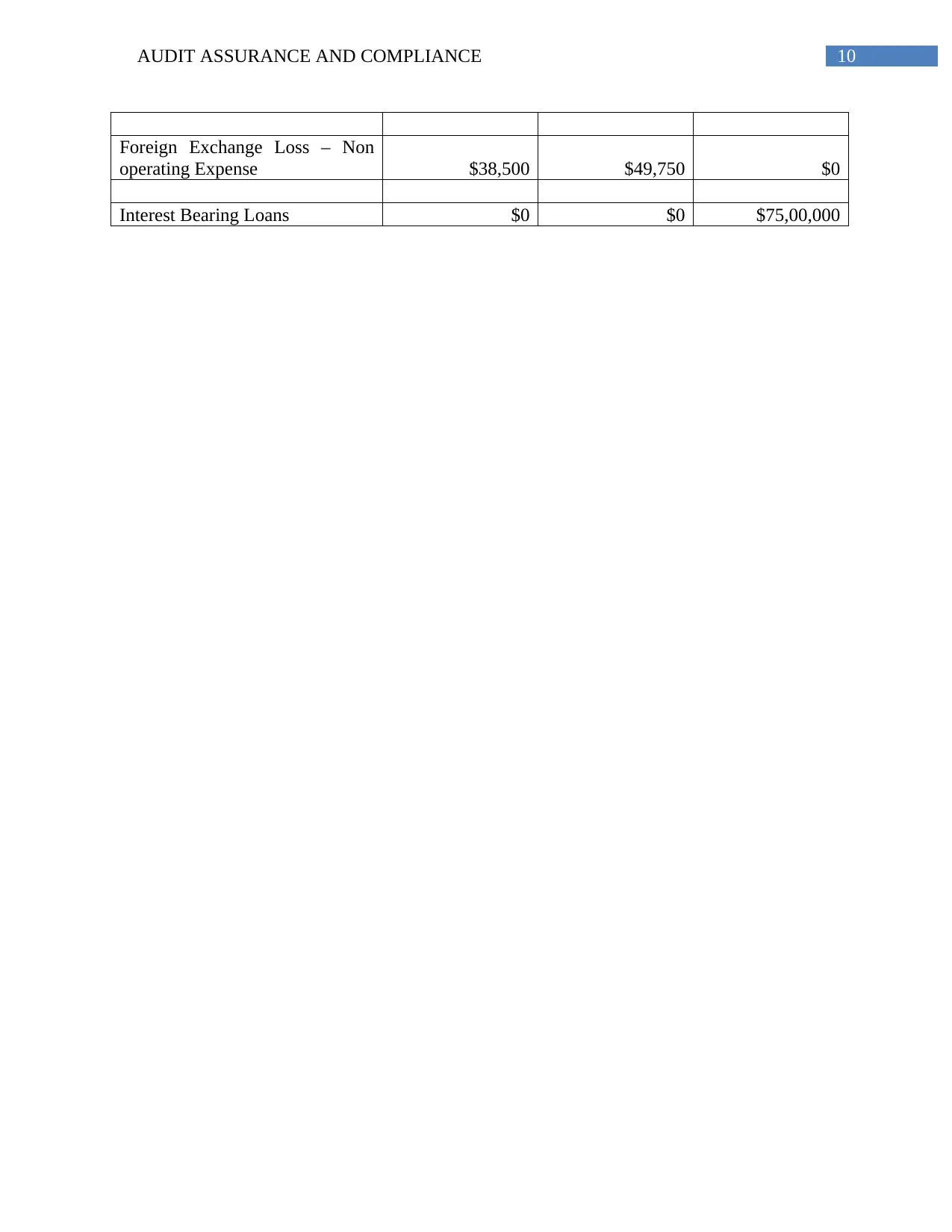

Foreign Exchange Loss – Non

operating Expense $38,500 $49,750 $0

Interest Bearing Loans $0 $0 $75,00,000

Foreign Exchange Loss – Non

operating Expense $38,500 $49,750 $0

Interest Bearing Loans $0 $0 $75,00,000

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.