Auditing for Fraud Detection and Risk Management

VerifiedAdded on 2020/03/02

|15

|2779

|41

AI Summary

This assignment delves into the detection of fraud and unethical activities within a company by examining its financial statements. It focuses on identifying accounting irregularities, such as manipulating profits and revenue to mislead stakeholders, and analyzes the inherent risks associated with these practices. The assignment emphasizes the role of auditors in assessing financial information, understanding risk factors related to key business processes, and applying auditing techniques to uncover potential fraud.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

AUDIT, ASSURANCE, AND COMPLIANCES

1

1

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Contents

Introduction...........................................................................................................................................3

Case Study`s Summary..........................................................................................................................4

Question 1.............................................................................................................................................5

Question 2.............................................................................................................................................8

Intentional Misstatement..................................................................................................................8

International and domestic reporting................................................................................................9

Question 3...........................................................................................................................................10

Key fraud risk factor:.......................................................................................................................10

Identification of key fraud risk factors.............................................................................................11

Conclusion...........................................................................................................................................12

References...........................................................................................................................................13

2

Introduction...........................................................................................................................................3

Case Study`s Summary..........................................................................................................................4

Question 1.............................................................................................................................................5

Question 2.............................................................................................................................................8

Intentional Misstatement..................................................................................................................8

International and domestic reporting................................................................................................9

Question 3...........................................................................................................................................10

Key fraud risk factor:.......................................................................................................................10

Identification of key fraud risk factors.............................................................................................11

Conclusion...........................................................................................................................................12

References...........................................................................................................................................13

2

Introduction

DIPL is an Australian company and the main business process of the company is printing.

Magazines and books are mainly printed by the company. Besides this, the printing of

advertisements for the publishing and educational industry is also used to be done by the

company. In addition to this analyzed the financial statement of the company and it is used to

verify the legitimacy of the statements. The operations are done in the financial accounts for

getting the attention of the shareholders. In this report, inherent risk factors are also being

discussed. There is some case study have to follow for preparing this report.

3

DIPL is an Australian company and the main business process of the company is printing.

Magazines and books are mainly printed by the company. Besides this, the printing of

advertisements for the publishing and educational industry is also used to be done by the

company. In addition to this analyzed the financial statement of the company and it is used to

verify the legitimacy of the statements. The operations are done in the financial accounts for

getting the attention of the shareholders. In this report, inherent risk factors are also being

discussed. There is some case study have to follow for preparing this report.

3

Case Study`s Summary

The case study of Double Ink Printers limited describes the audit which is managed by the

Stewart and Kathy. The business of DIPL is printing of books and magazines, advertising

material for advertising, educational and publishing industries but it is based on the print-on-

demand basis. Detailed information related to the business of DILP is given in case of study,

in addition to this financial information of the company is also given in the report. It also

analyses the ratio of the company to measure the performance of the company and also

measure the financial condition of the company. This information is very useful as it plays a

virtual role in auditing process and also helps in access the business`s information. Besides

this changes in the board meetings and discussion in the annual meeting, and IT system, etc.

has been described in this case study for a better process.

4

The case study of Double Ink Printers limited describes the audit which is managed by the

Stewart and Kathy. The business of DIPL is printing of books and magazines, advertising

material for advertising, educational and publishing industries but it is based on the print-on-

demand basis. Detailed information related to the business of DILP is given in case of study,

in addition to this financial information of the company is also given in the report. It also

analyses the ratio of the company to measure the performance of the company and also

measure the financial condition of the company. This information is very useful as it plays a

virtual role in auditing process and also helps in access the business`s information. Besides

this changes in the board meetings and discussion in the annual meeting, and IT system, etc.

has been described in this case study for a better process.

4

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

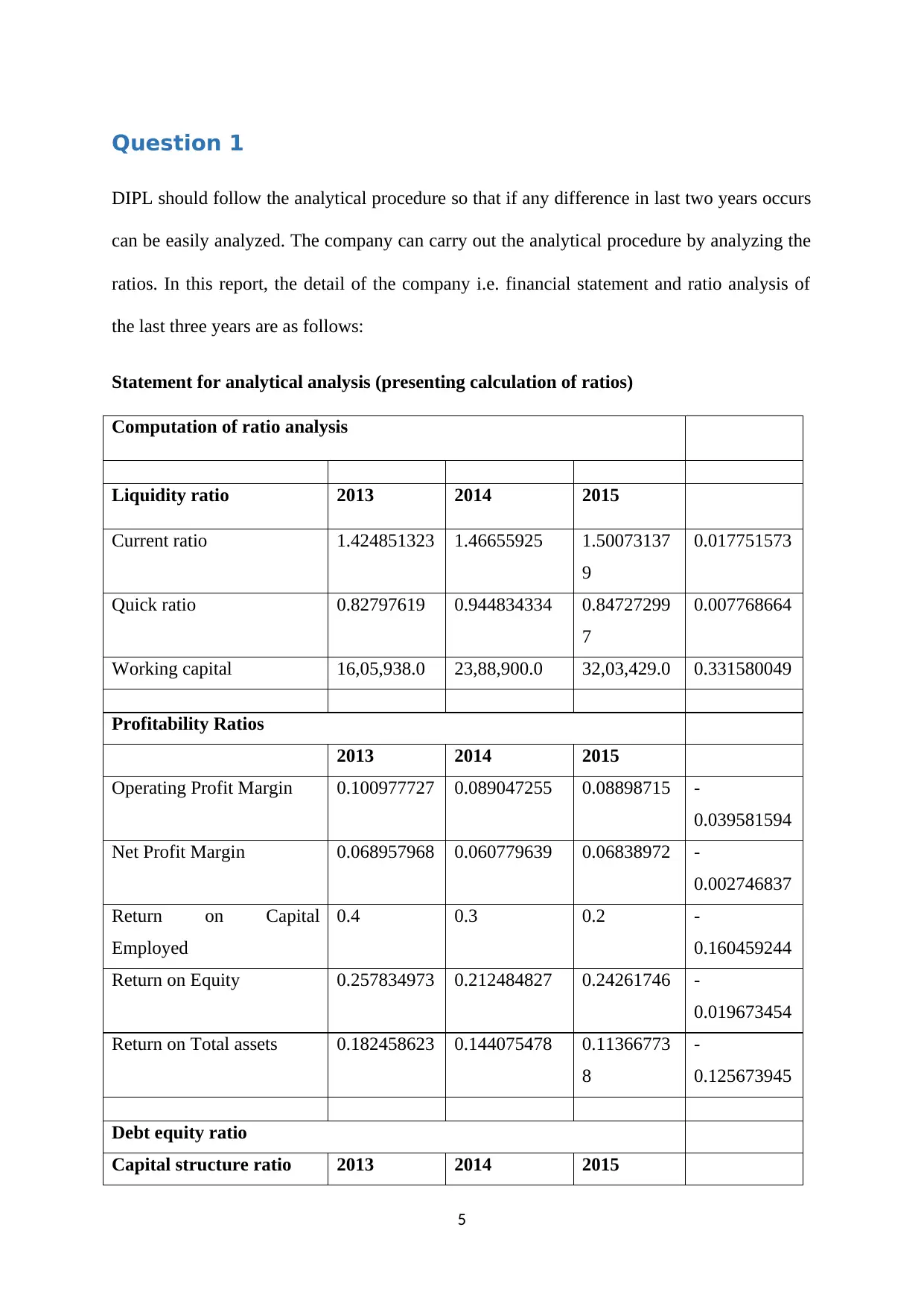

Question 1

DIPL should follow the analytical procedure so that if any difference in last two years occurs

can be easily analyzed. The company can carry out the analytical procedure by analyzing the

ratios. In this report, the detail of the company i.e. financial statement and ratio analysis of

the last three years are as follows:

Statement for analytical analysis (presenting calculation of ratios)

Computation of ratio analysis

Liquidity ratio 2013 2014 2015

Current ratio 1.424851323 1.46655925 1.50073137

9

0.017751573

Quick ratio 0.82797619 0.944834334 0.84727299

7

0.007768664

Working capital 16,05,938.0 23,88,900.0 32,03,429.0 0.331580049

Profitability Ratios

2013 2014 2015

Operating Profit Margin 0.100977727 0.089047255 0.08898715 -

0.039581594

Net Profit Margin 0.068957968 0.060779639 0.06838972 -

0.002746837

Return on Capital

Employed

0.4 0.3 0.2 -

0.160459244

Return on Equity 0.257834973 0.212484827 0.24261746 -

0.019673454

Return on Total assets 0.182458623 0.144075478 0.11366773

8

-

0.125673945

Debt equity ratio

Capital structure ratio 2013 2014 2015

5

DIPL should follow the analytical procedure so that if any difference in last two years occurs

can be easily analyzed. The company can carry out the analytical procedure by analyzing the

ratios. In this report, the detail of the company i.e. financial statement and ratio analysis of

the last three years are as follows:

Statement for analytical analysis (presenting calculation of ratios)

Computation of ratio analysis

Liquidity ratio 2013 2014 2015

Current ratio 1.424851323 1.46655925 1.50073137

9

0.017751573

Quick ratio 0.82797619 0.944834334 0.84727299

7

0.007768664

Working capital 16,05,938.0 23,88,900.0 32,03,429.0 0.331580049

Profitability Ratios

2013 2014 2015

Operating Profit Margin 0.100977727 0.089047255 0.08898715 -

0.039581594

Net Profit Margin 0.068957968 0.060779639 0.06838972 -

0.002746837

Return on Capital

Employed

0.4 0.3 0.2 -

0.160459244

Return on Equity 0.257834973 0.212484827 0.24261746 -

0.019673454

Return on Total assets 0.182458623 0.144075478 0.11366773

8

-

0.125673945

Debt equity ratio

Capital structure ratio 2013 2014 2015

5

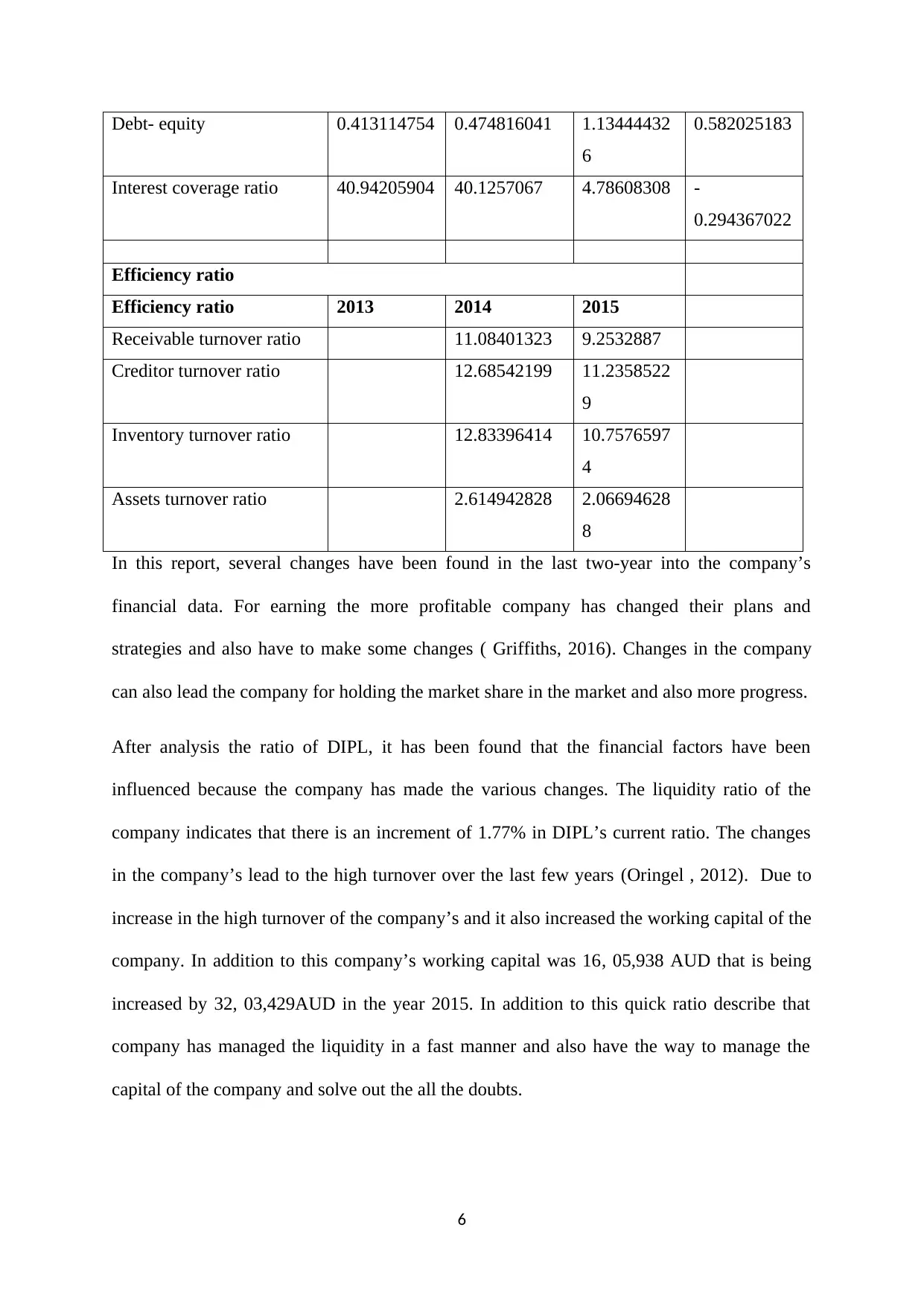

Debt- equity 0.413114754 0.474816041 1.13444432

6

0.582025183

Interest coverage ratio 40.94205904 40.1257067 4.78608308 -

0.294367022

Efficiency ratio

Efficiency ratio 2013 2014 2015

Receivable turnover ratio 11.08401323 9.2532887

Creditor turnover ratio 12.68542199 11.2358522

9

Inventory turnover ratio 12.83396414 10.7576597

4

Assets turnover ratio 2.614942828 2.06694628

8

In this report, several changes have been found in the last two-year into the company’s

financial data. For earning the more profitable company has changed their plans and

strategies and also have to make some changes ( Griffiths, 2016). Changes in the company

can also lead the company for holding the market share in the market and also more progress.

After analysis the ratio of DIPL, it has been found that the financial factors have been

influenced because the company has made the various changes. The liquidity ratio of the

company indicates that there is an increment of 1.77% in DIPL’s current ratio. The changes

in the company’s lead to the high turnover over the last few years (Oringel , 2012). Due to

increase in the high turnover of the company’s and it also increased the working capital of the

company. In addition to this company’s working capital was 16, 05,938 AUD that is being

increased by 32, 03,429AUD in the year 2015. In addition to this quick ratio describe that

company has managed the liquidity in a fast manner and also have the way to manage the

capital of the company and solve out the all the doubts.

6

6

0.582025183

Interest coverage ratio 40.94205904 40.1257067 4.78608308 -

0.294367022

Efficiency ratio

Efficiency ratio 2013 2014 2015

Receivable turnover ratio 11.08401323 9.2532887

Creditor turnover ratio 12.68542199 11.2358522

9

Inventory turnover ratio 12.83396414 10.7576597

4

Assets turnover ratio 2.614942828 2.06694628

8

In this report, several changes have been found in the last two-year into the company’s

financial data. For earning the more profitable company has changed their plans and

strategies and also have to make some changes ( Griffiths, 2016). Changes in the company

can also lead the company for holding the market share in the market and also more progress.

After analysis the ratio of DIPL, it has been found that the financial factors have been

influenced because the company has made the various changes. The liquidity ratio of the

company indicates that there is an increment of 1.77% in DIPL’s current ratio. The changes

in the company’s lead to the high turnover over the last few years (Oringel , 2012). Due to

increase in the high turnover of the company’s and it also increased the working capital of the

company. In addition to this company’s working capital was 16, 05,938 AUD that is being

increased by 32, 03,429AUD in the year 2015. In addition to this quick ratio describe that

company has managed the liquidity in a fast manner and also have the way to manage the

capital of the company and solve out the all the doubts.

6

In this case study DIPL analysis the profitability ratio, that the profit of the company is

reduced the last year because of the operational changes and changes in the external and

internal being made in the company. The profit margin of the company is reduced by 3.95%

in the year 2013, and the rate of the profit margin in this year is 1.009% while in the year

2015, the estimated rate is .88% (Dagwell, et al., 2012). In this financial condition of the

company is also intrepid due to the factors related to the profitability ratio. After falling in the

profitability condition of the company, it is been reprinted by ROE, return on total assets, Net

profit margin and ROCE.

The efficiency ratios and the capital structure ratio has been studied for analysis the growth

and performance of the company. In addition to this with the help capital structure ratio,

equity ratio is being increased by 58.20%. Changes in the debt-equity ratio, due to

fluctuations in the company’s liabilities and assets in last two years ( Thibodeau & Freier,

2013). In last year interest expenses, interest coverage ratio of the company is also decreased

because of the high charges made on interest.

In this report, various ratios such as inventory turnover ratio, Assets turnover ratio, receivable

turnover ratio, efficiency ratio and Creditor turnover ratio of the company are calculated so

that the performance of the company can be evaluated its short-term obligation and working

capital.

In this report, it has been determined that many changes are done in the business strategies,

operations, and functions, several changes in this ratio have been taken place. It has become

the difficult job for the auditors to access the changes occurs in the business (Warren &

Reeve, 2017). It has been an analysis that the changes occur due to mistake and inaccuracies

made by Jay and associates. It is the main responsibility of access the inaccuracies and

mistake done by Stewart and Kathy.

7

reduced the last year because of the operational changes and changes in the external and

internal being made in the company. The profit margin of the company is reduced by 3.95%

in the year 2013, and the rate of the profit margin in this year is 1.009% while in the year

2015, the estimated rate is .88% (Dagwell, et al., 2012). In this financial condition of the

company is also intrepid due to the factors related to the profitability ratio. After falling in the

profitability condition of the company, it is been reprinted by ROE, return on total assets, Net

profit margin and ROCE.

The efficiency ratios and the capital structure ratio has been studied for analysis the growth

and performance of the company. In addition to this with the help capital structure ratio,

equity ratio is being increased by 58.20%. Changes in the debt-equity ratio, due to

fluctuations in the company’s liabilities and assets in last two years ( Thibodeau & Freier,

2013). In last year interest expenses, interest coverage ratio of the company is also decreased

because of the high charges made on interest.

In this report, various ratios such as inventory turnover ratio, Assets turnover ratio, receivable

turnover ratio, efficiency ratio and Creditor turnover ratio of the company are calculated so

that the performance of the company can be evaluated its short-term obligation and working

capital.

In this report, it has been determined that many changes are done in the business strategies,

operations, and functions, several changes in this ratio have been taken place. It has become

the difficult job for the auditors to access the changes occurs in the business (Warren &

Reeve, 2017). It has been an analysis that the changes occur due to mistake and inaccuracies

made by Jay and associates. It is the main responsibility of access the inaccuracies and

mistake done by Stewart and Kathy.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

8

Question 2

Risk assessment is essential for the business, as though assessing the factors which can cause

or has caused risk can be determined and the effects which can be caused by the risk can also

be mitigated. DIPL contacted Stewart and Kathy for the auditing purpose (Wilson, 2015). It

is requisite by Stewart and Kathy to pursue risk assessment for the company so that the

aspects of risks could be evaluated and the decision could be made in context to the plans to

eliminate or mitigate risk aspects. In the case study`s analysis, it can be assessed that inherent

risk can be faced by DIPL in perspective to auditing compliances. The inherent risk factors

are discussed below-

Intentional Misstatement

Inherent risk can ensue because of the financial statement prepared by the accountant

deprived of considering the guidelines for preparing books of accounts (Oringel , 2012). In

addition to this, inherent risk can also occur due to the fraudulent activities followed by the

accountant for preparing financial statements of the company. The case study analysis reveals

that the revenue of company has increased over last year ( Hoelzer, 2011). Moreover, some

other aspects also signify company`s growth. On the other hand, the profitability of company

has been shown less in the financial statement. Portraying less profitability can be a reason to

save the amount from paying high tax return to the Australian government. For this reason,

may be the company has started pursuing fraudulent activities to show the reduced profit

amount in the books of accounts. So that the company may not have to pay higher tax

amount. For that reason, it may be conceivable that false transactions have been recorded in

the accounts book of the company (to represent decreased profit).

One of the other reason of portraying the company`s impressive performance and growth

through the ratios is to attract or impress the shareholders or the investors to influence them;

9

Risk assessment is essential for the business, as though assessing the factors which can cause

or has caused risk can be determined and the effects which can be caused by the risk can also

be mitigated. DIPL contacted Stewart and Kathy for the auditing purpose (Wilson, 2015). It

is requisite by Stewart and Kathy to pursue risk assessment for the company so that the

aspects of risks could be evaluated and the decision could be made in context to the plans to

eliminate or mitigate risk aspects. In the case study`s analysis, it can be assessed that inherent

risk can be faced by DIPL in perspective to auditing compliances. The inherent risk factors

are discussed below-

Intentional Misstatement

Inherent risk can ensue because of the financial statement prepared by the accountant

deprived of considering the guidelines for preparing books of accounts (Oringel , 2012). In

addition to this, inherent risk can also occur due to the fraudulent activities followed by the

accountant for preparing financial statements of the company. The case study analysis reveals

that the revenue of company has increased over last year ( Hoelzer, 2011). Moreover, some

other aspects also signify company`s growth. On the other hand, the profitability of company

has been shown less in the financial statement. Portraying less profitability can be a reason to

save the amount from paying high tax return to the Australian government. For this reason,

may be the company has started pursuing fraudulent activities to show the reduced profit

amount in the books of accounts. So that the company may not have to pay higher tax

amount. For that reason, it may be conceivable that false transactions have been recorded in

the accounts book of the company (to represent decreased profit).

One of the other reason of portraying the company`s impressive performance and growth

through the ratios is to attract or impress the shareholders or the investors to influence them;

9

that company has the sound financial condition and the shareholders can get a high return on

investment. This aspect can impact on the shareholders and can evoke them to invest more

(Dagwell, et al., 2012). It has been evaluated that the interest charges are also increased

through high rate. This aspect also led to one of the fraudulent activity practiced by the

company. On the other hand, it might be possible that interest charges have been increased

due to the huge amount of loan. Financial statement of the DIPL has become more complex

due to such particular activities pursued by the company. The company has also used a high

rate of depreciation over its assets (Belmont, 2011). Besides this, it has also been analyzed

through the company`s case study, that employees were paid high wages; which was not

worthy. Therefore, this can be determined that because of the misstatement in books of

accounts inherent risk can occur in the company.

International and domestic reporting

DIPL manages the functions or operations of its business in the Australia only. The company

operates in the Australia individually. On the other hand, it is essential for the company to

comply with the GAAP and IFRS`s guiding principles and rules for preparing accounts of

books or financial statements; so that requirements at the international level could be

achieved by the company (Greite, 2013). Through following such accounting standards and

rules, the company may get favor from FDIC in relation to massive investments. This will

help the company for acquiring more financial support and this amount can also be used to

solve several problems or issues. DIPL`s case study denotes that company has not followed

the rules and regulations for preparing the books of accounts. The noncompliance of such

rules can raise risk for the company in terms of practicing business (Belmont, 2011). Thus, it

is requisite for the company to follow the accounting standards so that authenticity could be

maintained in the books of accounts.

10

investment. This aspect can impact on the shareholders and can evoke them to invest more

(Dagwell, et al., 2012). It has been evaluated that the interest charges are also increased

through high rate. This aspect also led to one of the fraudulent activity practiced by the

company. On the other hand, it might be possible that interest charges have been increased

due to the huge amount of loan. Financial statement of the DIPL has become more complex

due to such particular activities pursued by the company. The company has also used a high

rate of depreciation over its assets (Belmont, 2011). Besides this, it has also been analyzed

through the company`s case study, that employees were paid high wages; which was not

worthy. Therefore, this can be determined that because of the misstatement in books of

accounts inherent risk can occur in the company.

International and domestic reporting

DIPL manages the functions or operations of its business in the Australia only. The company

operates in the Australia individually. On the other hand, it is essential for the company to

comply with the GAAP and IFRS`s guiding principles and rules for preparing accounts of

books or financial statements; so that requirements at the international level could be

achieved by the company (Greite, 2013). Through following such accounting standards and

rules, the company may get favor from FDIC in relation to massive investments. This will

help the company for acquiring more financial support and this amount can also be used to

solve several problems or issues. DIPL`s case study denotes that company has not followed

the rules and regulations for preparing the books of accounts. The noncompliance of such

rules can raise risk for the company in terms of practicing business (Belmont, 2011). Thus, it

is requisite for the company to follow the accounting standards so that authenticity could be

maintained in the books of accounts.

10

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Question 3

Some of the factors which describe the misstatement in company’s financial statement are a

measure to access the cause of the risk. Some of the factors are discussed below:

Key fraud risk factor:

Interest amount- Company’s interest amount in the year 2013 was 84379.0 AUD, whereas in

the year 2015 the interest amount was 808038.0 AUD. It means the changes occur in the

amount of interest over two years is 285.87%. In addition to this going through the

description provided in the context to company’s loan, it can be an analysis that in order to

manage the capital structure and liquidity position, very huge amount of loan has been taken

by the company (Belmont, 2011). Even though it also notice that the huge amount of loan

interest is also at high rate and company has utilized this huge amount of loan in manage the

tax return. Besides this company revenue has also been increased in comparison to last year,

that is the reason that why the company has to pay high tax return to government of Australia.

This is the reason the company has figure out the higher amount of interest to decrease the

profit amount at the end of the final statement so that they can pay the less tax to the

government of Australia.

Debt to equity ratio- the process of analysis of company’s debt to equity ratio is has been

done. By going through analysis, process it has been a measure that in the year 2014

company’s debt to equity ratio was 0.47% and in the year 2015, this ratio increased by 1.13%

( Griffiths, 2016). In addition to this for starting a new project not huge much amount is

required. This amount was shown to affect the stakeholders and government and also for the

other stakeholder’s decision.

11

Some of the factors which describe the misstatement in company’s financial statement are a

measure to access the cause of the risk. Some of the factors are discussed below:

Key fraud risk factor:

Interest amount- Company’s interest amount in the year 2013 was 84379.0 AUD, whereas in

the year 2015 the interest amount was 808038.0 AUD. It means the changes occur in the

amount of interest over two years is 285.87%. In addition to this going through the

description provided in the context to company’s loan, it can be an analysis that in order to

manage the capital structure and liquidity position, very huge amount of loan has been taken

by the company (Belmont, 2011). Even though it also notice that the huge amount of loan

interest is also at high rate and company has utilized this huge amount of loan in manage the

tax return. Besides this company revenue has also been increased in comparison to last year,

that is the reason that why the company has to pay high tax return to government of Australia.

This is the reason the company has figure out the higher amount of interest to decrease the

profit amount at the end of the final statement so that they can pay the less tax to the

government of Australia.

Debt to equity ratio- the process of analysis of company’s debt to equity ratio is has been

done. By going through analysis, process it has been a measure that in the year 2014

company’s debt to equity ratio was 0.47% and in the year 2015, this ratio increased by 1.13%

( Griffiths, 2016). In addition to this for starting a new project not huge much amount is

required. This amount was shown to affect the stakeholders and government and also for the

other stakeholder’s decision.

11

Identification of key fraud risk factors

In this report, each and every aspect of the company’s financial factors is ducted by the

auditors so that there is less possibility of fraud in related factors ( Fazal, 2011). Auditor has

to follow the report over the process related to finance department process, purchase and

inventory , cash receipts, e-book revenue process, printing process all these factors which are

related to company’s key risk inherent factors also being analyzed by the auditor. Finally,

these all information is being accessed from the financial statement and from BOD’s meeting

and also from company’s new financial decisions.

12

In this report, each and every aspect of the company’s financial factors is ducted by the

auditors so that there is less possibility of fraud in related factors ( Fazal, 2011). Auditor has

to follow the report over the process related to finance department process, purchase and

inventory , cash receipts, e-book revenue process, printing process all these factors which are

related to company’s key risk inherent factors also being analyzed by the auditor. Finally,

these all information is being accessed from the financial statement and from BOD’s meeting

and also from company’s new financial decisions.

12

Conclusion

In this report, it has been observed that company has practiced fraud and unethical activities.

As the company has not followed the accounting standards and accounting principle while

preparing the financial statement. The profit of the company is showing less due to saving the

tax, in another hand they revenue of the company is showed the higher amount. These tactics

are used by the company to intact the shareholders and investors so that investors can take

more interest in investing more amount in the company. These types of fraud activate can

become a big reason for inherent risk for the company.

13

In this report, it has been observed that company has practiced fraud and unethical activities.

As the company has not followed the accounting standards and accounting principle while

preparing the financial statement. The profit of the company is showing less due to saving the

tax, in another hand they revenue of the company is showed the higher amount. These tactics

are used by the company to intact the shareholders and investors so that investors can take

more interest in investing more amount in the company. These types of fraud activate can

become a big reason for inherent risk for the company.

13

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

References

Fazal, H., 2011. What is Audit risk?. [Online]

Available at: http://pakaccountants.com/what-is-audit-risk/

Griffiths, P., 2016. Risk-Based Auditing. s.l. CRC Press.

Handsworth, A., 2012. Risk Management Audit Guide. s.l. Xlibris Corporation.

Hoelzer, D., 2011. Audit Principles, Risk Assessment, and Effective Reporting.

s.l.:EnclaveForensics.

Perler, J. & Howard M. , S. M., 2010. Financial Shenanigans: How to Detect Accounting

Gimmicks & Fraud in Financial Reports, s.l. McGraw Hill Education.

Thibodeau, J. & Freier, D., 2013. Auditing and Accounting Cases: Investigating Issues of

Fraud and Professional Ethics. s.l.:Wiley.

Belmont, D. P., 2011. Managing Hedge Fund Risk and Financing: Adapting to a New

EraSep. s.l.:Wiley.

Dagwell, R., Lambert, C. & Wines, G., 2012. Corporate Accounting in Australia.

s.l.:Pearson.

. F., 2012. Business Ethics and Corporate Governance. s.l.:Pearson Education.

Gramling, A. A., Johnstone, . M. & L. E., 2012. Auditing. s.l.:Cengage Learning.

Greite, S., 2013. The Development of the Australian Accounting Standards After the End of

the G4+1. s.l. Grin Verlag.

Johnstone, K., Gramling, A. & Ritte, L. E., 2013. Auditing: A Risk-Based Approach to

Conducting a Quality Audit. s.l.:Cengage Learning.

Kimmel, P. D. & Weygandt , J. J., 2013. Accounting Principles. s.l.:s.n.

Oringel , J., 2012. Effective Auditing For Corporates. s.l.:A&C Black.

Warren, C. S. & Reeve, J. M., 2017. Accounting. s.l.:South-Western College Pub.

Wilson, R. M., 2015. Researching accounting education. s.l.:Routledge.

14

Fazal, H., 2011. What is Audit risk?. [Online]

Available at: http://pakaccountants.com/what-is-audit-risk/

Griffiths, P., 2016. Risk-Based Auditing. s.l. CRC Press.

Handsworth, A., 2012. Risk Management Audit Guide. s.l. Xlibris Corporation.

Hoelzer, D., 2011. Audit Principles, Risk Assessment, and Effective Reporting.

s.l.:EnclaveForensics.

Perler, J. & Howard M. , S. M., 2010. Financial Shenanigans: How to Detect Accounting

Gimmicks & Fraud in Financial Reports, s.l. McGraw Hill Education.

Thibodeau, J. & Freier, D., 2013. Auditing and Accounting Cases: Investigating Issues of

Fraud and Professional Ethics. s.l.:Wiley.

Belmont, D. P., 2011. Managing Hedge Fund Risk and Financing: Adapting to a New

EraSep. s.l.:Wiley.

Dagwell, R., Lambert, C. & Wines, G., 2012. Corporate Accounting in Australia.

s.l.:Pearson.

. F., 2012. Business Ethics and Corporate Governance. s.l.:Pearson Education.

Gramling, A. A., Johnstone, . M. & L. E., 2012. Auditing. s.l.:Cengage Learning.

Greite, S., 2013. The Development of the Australian Accounting Standards After the End of

the G4+1. s.l. Grin Verlag.

Johnstone, K., Gramling, A. & Ritte, L. E., 2013. Auditing: A Risk-Based Approach to

Conducting a Quality Audit. s.l.:Cengage Learning.

Kimmel, P. D. & Weygandt , J. J., 2013. Accounting Principles. s.l.:s.n.

Oringel , J., 2012. Effective Auditing For Corporates. s.l.:A&C Black.

Warren, C. S. & Reeve, J. M., 2017. Accounting. s.l.:South-Western College Pub.

Wilson, R. M., 2015. Researching accounting education. s.l.:Routledge.

14

15

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.