Audit Assurance and Compliance Report: Financial Analysis of Firm DIPL

VerifiedAdded on 2020/03/01

|10

|2720

|45

Report

AI Summary

This report provides a comprehensive analysis of audit assurance and compliance, focusing on the financial analysis of a firm named DIPL. It begins by examining the implementation of analytical procedures to monetary assertions, highlighting how these procedures can improve audit design and support the assessment of financial statements. The report then delves into the discussion of inherent risks, including those related to employee performance, environmental factors, and CEO succession, and their potential impact on material misstatements in financial reports. Furthermore, the report explores fraud risks, such as those stemming from employee discontent and the pressure to meet financial performance targets, and their implications for asset loss. The analysis includes specific examples and financial ratios to illustrate the concepts and provides a detailed understanding of how various factors influence the audit process and the reliability of financial information. The report is intended to provide insights into how different types of risks can influence the operations of a business concern and how to mitigate those risks. It also includes the analysis of the financial health of the company.

Running head: AUDIT ASSURANCE AND COMPLIANCE

Audit Assurance and Compliance

University Name

Student Name

Authors’ Note

Audit Assurance and Compliance

University Name

Student Name

Authors’ Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2

AUDIT ASSURANCE AND COMPLIANCE

Table of Contents

Solution to Question 1:...............................................................................................................2

Solution to Question 2:...............................................................................................................4

Solution to Question 3:...............................................................................................................7

AUDIT ASSURANCE AND COMPLIANCE

Table of Contents

Solution to Question 1:...............................................................................................................2

Solution to Question 2:...............................................................................................................4

Solution to Question 3:...............................................................................................................7

3

AUDIT ASSURANCE AND COMPLIANCE

Solution to Question 1:

Implementation of analytical procedures to monetary assertions of firm DIPL

Proper implementation of analytical procedures to different pecuniary assertions of the firm

DIPL can support the process of improvement of the audit design. Fundamentally, audit plan

can reflect specific directive that need to be tracked during a specific time of executing the

audit practise. Fundamentally, stratagem of assessment also aids auditors in backing up audit

expenses at sensible stage and aids in illustrating misapprehension together with

miscommunication with diverse customers of specific firm.

Inspective tactic of common sizing backs evaluation of financial assertions in a specific

manner. This way of analytical procedure also aids management of firms to work on carrying

out comparative evaluation of economic assertions of firms from the perspective of different

periods (different phases of time) or else from the perspective of different business concerns.

Appraisers can also tell about different categories otherwise classes of elements recognized in

the financial statements and help in examining the manner of disclosing diverse economic

pronouncements (Chou 2015). As such, the mechanism of considering diverse elements of

economic statements for example, net assets as well as liabilities together with shareholders’

equity (Simnett et al. 2016). Nonetheless, modification in the financial statements considered

from a specific point of view backs the development of the system of identifying the

aberration, thus, this aids the process of analysis of the reason behind the deviation for

gaining a deep understanding as regards the main intent (William Jr et al. 2016). In essence,

this is mainly because this technique can be appositely executed for analysing financial

reports and all at the same time analysing comprehensive idea of financial analysis.

Detailed discussion of the way economic fallouts can affect audit process

AUDIT ASSURANCE AND COMPLIANCE

Solution to Question 1:

Implementation of analytical procedures to monetary assertions of firm DIPL

Proper implementation of analytical procedures to different pecuniary assertions of the firm

DIPL can support the process of improvement of the audit design. Fundamentally, audit plan

can reflect specific directive that need to be tracked during a specific time of executing the

audit practise. Fundamentally, stratagem of assessment also aids auditors in backing up audit

expenses at sensible stage and aids in illustrating misapprehension together with

miscommunication with diverse customers of specific firm.

Inspective tactic of common sizing backs evaluation of financial assertions in a specific

manner. This way of analytical procedure also aids management of firms to work on carrying

out comparative evaluation of economic assertions of firms from the perspective of different

periods (different phases of time) or else from the perspective of different business concerns.

Appraisers can also tell about different categories otherwise classes of elements recognized in

the financial statements and help in examining the manner of disclosing diverse economic

pronouncements (Chou 2015). As such, the mechanism of considering diverse elements of

economic statements for example, net assets as well as liabilities together with shareholders’

equity (Simnett et al. 2016). Nonetheless, modification in the financial statements considered

from a specific point of view backs the development of the system of identifying the

aberration, thus, this aids the process of analysis of the reason behind the deviation for

gaining a deep understanding as regards the main intent (William Jr et al. 2016). In essence,

this is mainly because this technique can be appositely executed for analysing financial

reports and all at the same time analysing comprehensive idea of financial analysis.

Detailed discussion of the way economic fallouts can affect audit process

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

4

AUDIT ASSURANCE AND COMPLIANCE

Specific outcomes of planning for preparation as well as presentation of audit can be

exclusively effected by the exploratory tactic undertaken for the purpose of translation as

well as making out information from different reports published by the firm (William Jr et al.

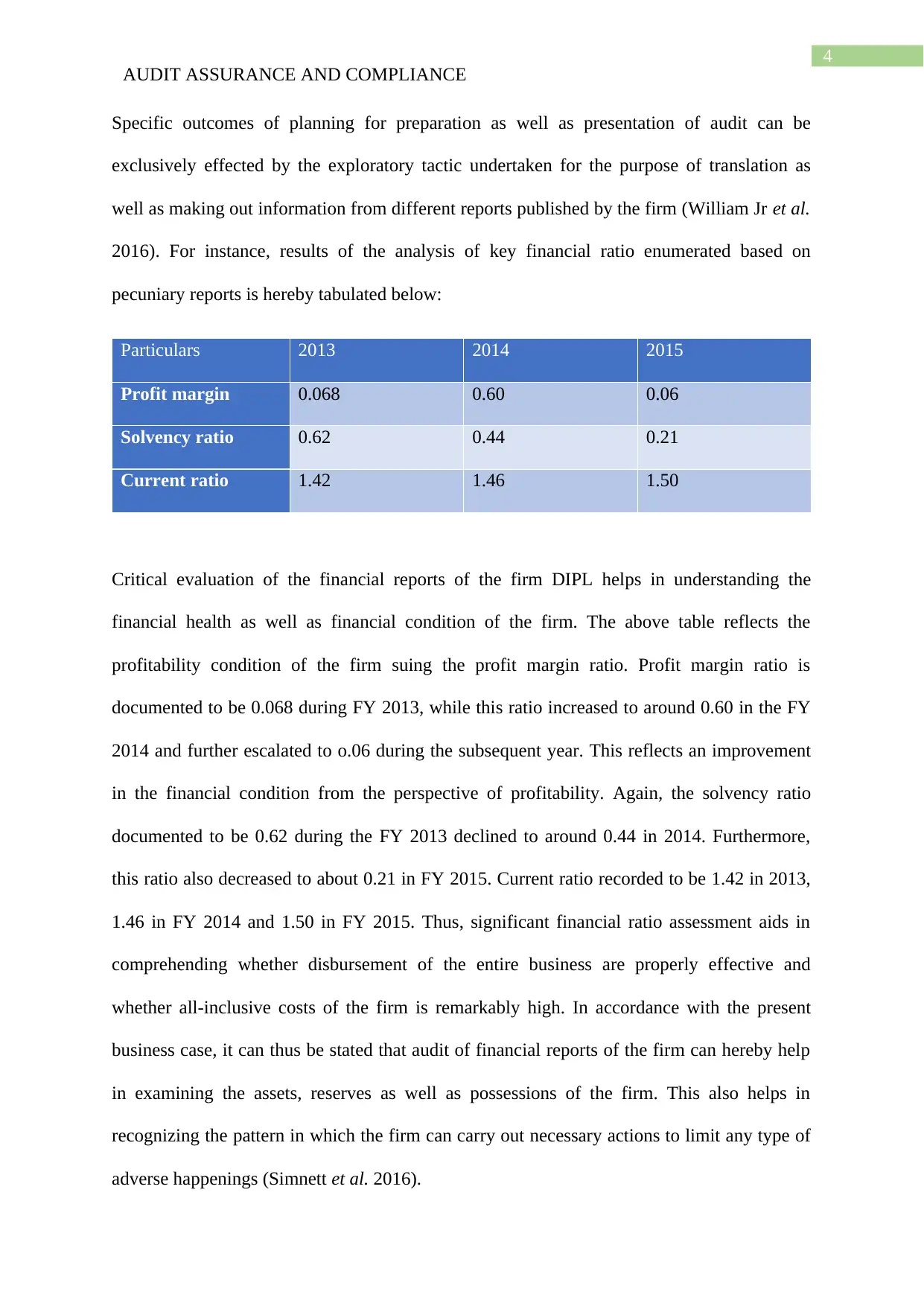

2016). For instance, results of the analysis of key financial ratio enumerated based on

pecuniary reports is hereby tabulated below:

Particulars 2013 2014 2015

Profit margin 0.068 0.60 0.06

Solvency ratio 0.62 0.44 0.21

Current ratio 1.42 1.46 1.50

Critical evaluation of the financial reports of the firm DIPL helps in understanding the

financial health as well as financial condition of the firm. The above table reflects the

profitability condition of the firm suing the profit margin ratio. Profit margin ratio is

documented to be 0.068 during FY 2013, while this ratio increased to around 0.60 in the FY

2014 and further escalated to o.06 during the subsequent year. This reflects an improvement

in the financial condition from the perspective of profitability. Again, the solvency ratio

documented to be 0.62 during the FY 2013 declined to around 0.44 in 2014. Furthermore,

this ratio also decreased to about 0.21 in FY 2015. Current ratio recorded to be 1.42 in 2013,

1.46 in FY 2014 and 1.50 in FY 2015. Thus, significant financial ratio assessment aids in

comprehending whether disbursement of the entire business are properly effective and

whether all-inclusive costs of the firm is remarkably high. In accordance with the present

business case, it can thus be stated that audit of financial reports of the firm can hereby help

in examining the assets, reserves as well as possessions of the firm. This also helps in

recognizing the pattern in which the firm can carry out necessary actions to limit any type of

adverse happenings (Simnett et al. 2016).

AUDIT ASSURANCE AND COMPLIANCE

Specific outcomes of planning for preparation as well as presentation of audit can be

exclusively effected by the exploratory tactic undertaken for the purpose of translation as

well as making out information from different reports published by the firm (William Jr et al.

2016). For instance, results of the analysis of key financial ratio enumerated based on

pecuniary reports is hereby tabulated below:

Particulars 2013 2014 2015

Profit margin 0.068 0.60 0.06

Solvency ratio 0.62 0.44 0.21

Current ratio 1.42 1.46 1.50

Critical evaluation of the financial reports of the firm DIPL helps in understanding the

financial health as well as financial condition of the firm. The above table reflects the

profitability condition of the firm suing the profit margin ratio. Profit margin ratio is

documented to be 0.068 during FY 2013, while this ratio increased to around 0.60 in the FY

2014 and further escalated to o.06 during the subsequent year. This reflects an improvement

in the financial condition from the perspective of profitability. Again, the solvency ratio

documented to be 0.62 during the FY 2013 declined to around 0.44 in 2014. Furthermore,

this ratio also decreased to about 0.21 in FY 2015. Current ratio recorded to be 1.42 in 2013,

1.46 in FY 2014 and 1.50 in FY 2015. Thus, significant financial ratio assessment aids in

comprehending whether disbursement of the entire business are properly effective and

whether all-inclusive costs of the firm is remarkably high. In accordance with the present

business case, it can thus be stated that audit of financial reports of the firm can hereby help

in examining the assets, reserves as well as possessions of the firm. This also helps in

recognizing the pattern in which the firm can carry out necessary actions to limit any type of

adverse happenings (Simnett et al. 2016).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

5

AUDIT ASSURANCE AND COMPLIANCE

Solution to Question 2:

There are different categories of risk recognized in the process of audit and can be related to

material misstatements in financial reports. Even so, it can be mentioned here that there

remains different categories of unsystematic risk that can pull the attention to different types

of risks recognized from financial proclamation of business concerns. Besides this, there also

exists miscellaneous categories of risks that can also affect the business operations and thus

needs to be avoided by firms (Messier et al. 2014). Fundamentally, this can assist in

indicating both true and fair view of different classes of economic announcements. Inherent

risks might occur in this case. This inherent risk is the risk that essentially occur owing to

error or else omission in a pecuniary reports because of a feature excluding control failure.

However, in a monetary assessment, inherent risk is utmost probable to happen when

dealings are intricate, or in circumstances that need a high magnitude of judgment as regards

financial approximations. The auditor might plausibly find it very hard to detect the certain

risks. There also exists certain risks that occur because of exclusion of certain factors together

with certain faults or mistakes that are unlikely to be committed to be committed by different

expert accountants (Louwers et al. 2015).

The table below presents different types of inherent risks that might be faced by the business

concern DIPL along with detailed illustration of the same.

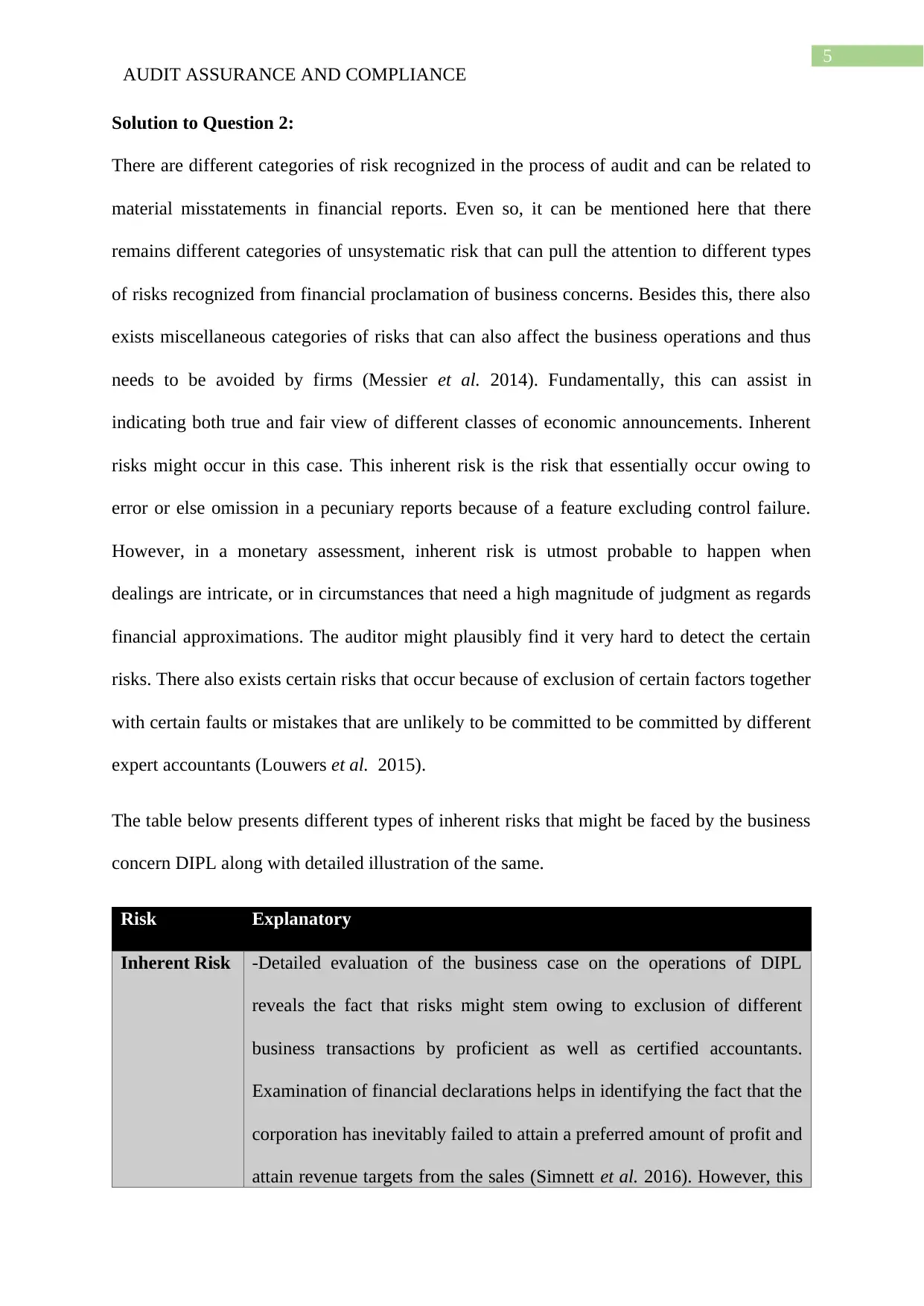

Risk Explanatory

Inherent Risk -Detailed evaluation of the business case on the operations of DIPL

reveals the fact that risks might stem owing to exclusion of different

business transactions by proficient as well as certified accountants.

Examination of financial declarations helps in identifying the fact that the

corporation has inevitably failed to attain a preferred amount of profit and

attain revenue targets from the sales (Simnett et al. 2016). However, this

AUDIT ASSURANCE AND COMPLIANCE

Solution to Question 2:

There are different categories of risk recognized in the process of audit and can be related to

material misstatements in financial reports. Even so, it can be mentioned here that there

remains different categories of unsystematic risk that can pull the attention to different types

of risks recognized from financial proclamation of business concerns. Besides this, there also

exists miscellaneous categories of risks that can also affect the business operations and thus

needs to be avoided by firms (Messier et al. 2014). Fundamentally, this can assist in

indicating both true and fair view of different classes of economic announcements. Inherent

risks might occur in this case. This inherent risk is the risk that essentially occur owing to

error or else omission in a pecuniary reports because of a feature excluding control failure.

However, in a monetary assessment, inherent risk is utmost probable to happen when

dealings are intricate, or in circumstances that need a high magnitude of judgment as regards

financial approximations. The auditor might plausibly find it very hard to detect the certain

risks. There also exists certain risks that occur because of exclusion of certain factors together

with certain faults or mistakes that are unlikely to be committed to be committed by different

expert accountants (Louwers et al. 2015).

The table below presents different types of inherent risks that might be faced by the business

concern DIPL along with detailed illustration of the same.

Risk Explanatory

Inherent Risk -Detailed evaluation of the business case on the operations of DIPL

reveals the fact that risks might stem owing to exclusion of different

business transactions by proficient as well as certified accountants.

Examination of financial declarations helps in identifying the fact that the

corporation has inevitably failed to attain a preferred amount of profit and

attain revenue targets from the sales (Simnett et al. 2016). However, this

6

AUDIT ASSURANCE AND COMPLIANCE

might occur on account of sheer failure of the management and the board

to perceive certain necessities, evaluate different macro and micro issues

involved in the environment of the business. This essentially includes the

socio- economic along with political factors present in the business

environ of the company DIPL (William Jr et al. 2016). Thus, this can be

witnessed from lower amount of sales and leads to events of risks.

-The workforces also augmented the inherent risks. Critical analysis of

the business case also helps in understanding the fact that lack of

efficiency and experience of the employees also leads to incidence of

inherent risks. The non-proficient employees can also escalate the overall

inherent risks by committing different slips and errors (Simnett et al.

2016). For instance, imprecision might owing to exclusion and this can

eventually lead to falsified presentations in the financial statements.

There are different environmental facets that too become the root cause

of inherent risks. This primarily takes place due to rapid transformations

in business environs, stiff competition as well as inadequacy of capital

(Simnett et al. 2016).

Inherent Risk Detailed analysis of the business case on DIPL aids in gaining deep

understanding regarding the fact that possibility of occurrence of inherent

risks exists in the process of undertaking CEO succession (Messier et al.

2014). Therefore, a proper exercise of assessing ease of change also

covers inherent risk involved in different operations. Therefore, initiation

of exercise without adhering to specific strategies, commencement of

certain operations late, incorrect connection with the chief executive

officer and nomination of CEO also may lead to incidence of inherent

AUDIT ASSURANCE AND COMPLIANCE

might occur on account of sheer failure of the management and the board

to perceive certain necessities, evaluate different macro and micro issues

involved in the environment of the business. This essentially includes the

socio- economic along with political factors present in the business

environ of the company DIPL (William Jr et al. 2016). Thus, this can be

witnessed from lower amount of sales and leads to events of risks.

-The workforces also augmented the inherent risks. Critical analysis of

the business case also helps in understanding the fact that lack of

efficiency and experience of the employees also leads to incidence of

inherent risks. The non-proficient employees can also escalate the overall

inherent risks by committing different slips and errors (Simnett et al.

2016). For instance, imprecision might owing to exclusion and this can

eventually lead to falsified presentations in the financial statements.

There are different environmental facets that too become the root cause

of inherent risks. This primarily takes place due to rapid transformations

in business environs, stiff competition as well as inadequacy of capital

(Simnett et al. 2016).

Inherent Risk Detailed analysis of the business case on DIPL aids in gaining deep

understanding regarding the fact that possibility of occurrence of inherent

risks exists in the process of undertaking CEO succession (Messier et al.

2014). Therefore, a proper exercise of assessing ease of change also

covers inherent risk involved in different operations. Therefore, initiation

of exercise without adhering to specific strategies, commencement of

certain operations late, incorrect connection with the chief executive

officer and nomination of CEO also may lead to incidence of inherent

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

7

AUDIT ASSURANCE AND COMPLIANCE

risk (Louwers et al. 2015).

Also, registering cash proceeds of the firm by different finance

professional of DIPL too can lead to incidence of risk (Knechel 2016).

Carrying out detailed cataloguing of acquired sales proceeds from

definite e-book, considering reissuance of texts or else guidebook in the

upcoming period can add to the possibility of occurrence of inherent risks

as a upshot of the complexity involved in the technique (Knechel and

Salterio 2016).

Possible reasons behind occurrence of inherent risks related to material misstatements in the

financial pronouncements of the firm include:-

- Too much work related stress and overload of work on employees along with the

management of the firm

- Risk of carrying out tasks by professional accountants in a faulty or erroneous manner

that might lead to misrepresentation in the financial statements (Elder et al. 2011)

- Trustworthiness of the complete management and board (Glover et al. 2016)

- Strain on the entire management of the firm

- Features and nature of functionality of operations of the business concern (Edgley et

al. 2015)

Solution to Question 3:

Fraud risks can essentially lead to loss of assets and reserves of the corporation DIPL. In

essence, discontentment of employees owing to excessive stress of work can direct

employees to contain different fraudulent arrangement (Arens et al. 2016). In addition to this,

expectancies of administration of corporation as regards financial results and to achieve a

AUDIT ASSURANCE AND COMPLIANCE

risk (Louwers et al. 2015).

Also, registering cash proceeds of the firm by different finance

professional of DIPL too can lead to incidence of risk (Knechel 2016).

Carrying out detailed cataloguing of acquired sales proceeds from

definite e-book, considering reissuance of texts or else guidebook in the

upcoming period can add to the possibility of occurrence of inherent risks

as a upshot of the complexity involved in the technique (Knechel and

Salterio 2016).

Possible reasons behind occurrence of inherent risks related to material misstatements in the

financial pronouncements of the firm include:-

- Too much work related stress and overload of work on employees along with the

management of the firm

- Risk of carrying out tasks by professional accountants in a faulty or erroneous manner

that might lead to misrepresentation in the financial statements (Elder et al. 2011)

- Trustworthiness of the complete management and board (Glover et al. 2016)

- Strain on the entire management of the firm

- Features and nature of functionality of operations of the business concern (Edgley et

al. 2015)

Solution to Question 3:

Fraud risks can essentially lead to loss of assets and reserves of the corporation DIPL. In

essence, discontentment of employees owing to excessive stress of work can direct

employees to contain different fraudulent arrangement (Arens et al. 2016). In addition to this,

expectancies of administration of corporation as regards financial results and to achieve a

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

8

AUDIT ASSURANCE AND COMPLIANCE

certain level of performance can also lead to occurrence of different incidence of fraud (Chou

2015). Added to this, there too occurs the necessity to communicate financial result that in

line can help in evading risks reflecting made-up affirmations (Baylis et al. 2017).

Recognition of

Risk

Illustration

Fraud Risk Analysis of the business case on DIPL helps in understanding the fact

that risks in business might crop up owing to involvement of

discontented workers in diverse deceitful tasks. Assessment of

functionalities of the business firms helps in laying stress on the fact

that there exists excessive strain on workers to adopt the task of

implementing advanced and progressive IT prompted accounting

system (Chou 2015). However, this can lead to fraudulent actions and

manage the clearance tasks in an appropriate manner. Thus, this can

help in carrying out misstatement in financial statements (Arens et al.

2016). Analysis of the case also helps in understanding the

inappropriate way of managing the entire course of executing the action

of establishing innovative accounting plan and give way to unfitting

suppositions regarding explicit corporate dealings during the end of the

year (Arens et al. 2016). Yet again, this also reveals the manner towards

incurring loss on account of material misstatement along with fraud

risk.

Fraud Risk Analytical evaluation of business case on DIPL discloses the fact that a

totally different event of risk might perhaps take place on account of

different fraudulent actions (Baylis et al. 2017). This mainly occurs

owing to events involved in the process of arrangement together with

AUDIT ASSURANCE AND COMPLIANCE

certain level of performance can also lead to occurrence of different incidence of fraud (Chou

2015). Added to this, there too occurs the necessity to communicate financial result that in

line can help in evading risks reflecting made-up affirmations (Baylis et al. 2017).

Recognition of

Risk

Illustration

Fraud Risk Analysis of the business case on DIPL helps in understanding the fact

that risks in business might crop up owing to involvement of

discontented workers in diverse deceitful tasks. Assessment of

functionalities of the business firms helps in laying stress on the fact

that there exists excessive strain on workers to adopt the task of

implementing advanced and progressive IT prompted accounting

system (Chou 2015). However, this can lead to fraudulent actions and

manage the clearance tasks in an appropriate manner. Thus, this can

help in carrying out misstatement in financial statements (Arens et al.

2016). Analysis of the case also helps in understanding the

inappropriate way of managing the entire course of executing the action

of establishing innovative accounting plan and give way to unfitting

suppositions regarding explicit corporate dealings during the end of the

year (Arens et al. 2016). Yet again, this also reveals the manner towards

incurring loss on account of material misstatement along with fraud

risk.

Fraud Risk Analytical evaluation of business case on DIPL discloses the fact that a

totally different event of risk might perhaps take place on account of

different fraudulent actions (Baylis et al. 2017). This mainly occurs

owing to events involved in the process of arrangement together with

9

AUDIT ASSURANCE AND COMPLIANCE

presentation of different financial pronouncements. Mainly, once there

exists huge anticipation from large number of outside sponsors

regarding publicizing precise financial suggestions and realizing pre-

determined performance goals (Baylis et al. 2017). This too leads

towards risks of committing material misstatement in the financial

assertions of the corporation. Furthermore, the attainment of the pre-

determined goals to achieve the necessities to get credit and gather debt

also involves high level of risk of incorrect financial statement

(Christensen et al. 2016).

Even so, financial assertions as regards specific financial state of affairs

of the concern also suggests about profit of the business concern

(Christensen et al. 2016). This too helps in identifying the fact that the

business concern has increased the entire proceeds of the corporation

during a specific period of time that is necessarily between financial

year 2013 and 2015. Besides this, the calculated sales revenue (gross)

along with the sales revenue (net) can also be observed to have

increased. Nonetheless, this current business case replicates that DIPL

has secured loans amounting to 7.5 million from BDO Finance. This

loan agreement also has certain contract terms that calls for the need of

satisfying a certain level of current ratio of nearly 1.5 plus debt equity

ratio of lower than almost 1. Thus, it can be hereby inferred that these

identified facets require the corporation to maintain a certain financial

ration that can help in acquiring credit (Duncan and Whittington 2014).

This too can lead towards diverse fraudulent actions and give way to

inappropriate replication of financial condition.

AUDIT ASSURANCE AND COMPLIANCE

presentation of different financial pronouncements. Mainly, once there

exists huge anticipation from large number of outside sponsors

regarding publicizing precise financial suggestions and realizing pre-

determined performance goals (Baylis et al. 2017). This too leads

towards risks of committing material misstatement in the financial

assertions of the corporation. Furthermore, the attainment of the pre-

determined goals to achieve the necessities to get credit and gather debt

also involves high level of risk of incorrect financial statement

(Christensen et al. 2016).

Even so, financial assertions as regards specific financial state of affairs

of the concern also suggests about profit of the business concern

(Christensen et al. 2016). This too helps in identifying the fact that the

business concern has increased the entire proceeds of the corporation

during a specific period of time that is necessarily between financial

year 2013 and 2015. Besides this, the calculated sales revenue (gross)

along with the sales revenue (net) can also be observed to have

increased. Nonetheless, this current business case replicates that DIPL

has secured loans amounting to 7.5 million from BDO Finance. This

loan agreement also has certain contract terms that calls for the need of

satisfying a certain level of current ratio of nearly 1.5 plus debt equity

ratio of lower than almost 1. Thus, it can be hereby inferred that these

identified facets require the corporation to maintain a certain financial

ration that can help in acquiring credit (Duncan and Whittington 2014).

This too can lead towards diverse fraudulent actions and give way to

inappropriate replication of financial condition.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

10

AUDIT ASSURANCE AND COMPLIANCE

Consistent with the given business case, it can be hereby mentioned that exercise of

approximation of inventory of specifically raw material at precise average cost was not

proper as the charge of paper was substantially beyond the average cost (Edgley et al. 2015).

In addition to this, risk of recognizing fraudulent deeds involved in executing accounting

arrangement using IT in tasks of book keeping can be presumed by observing diverse

arrangements at different phases (Duncan and Whittington 2014). At the inception, the risk

associated to the registering economic assertions can be recognized by undertaking inquiry of

financial assertions by assessors, outlining schemes of control directly.

AUDIT ASSURANCE AND COMPLIANCE

Consistent with the given business case, it can be hereby mentioned that exercise of

approximation of inventory of specifically raw material at precise average cost was not

proper as the charge of paper was substantially beyond the average cost (Edgley et al. 2015).

In addition to this, risk of recognizing fraudulent deeds involved in executing accounting

arrangement using IT in tasks of book keeping can be presumed by observing diverse

arrangements at different phases (Duncan and Whittington 2014). At the inception, the risk

associated to the registering economic assertions can be recognized by undertaking inquiry of

financial assertions by assessors, outlining schemes of control directly.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.