Auditing and Assurance: DIPL Case Study and Financial Analysis Report

VerifiedAdded on 2020/03/07

|9

|2505

|187

Report

AI Summary

This report provides an in-depth analysis of auditing and assurance principles, focusing on a case study of the company DIPL. It begins by exploring the application of analytical techniques to financial statements to develop an audit plan, emphasizing the importance of comparative assessments and identifying variances. The report then delves into different categories of audit risk, including inherent risks, and how these risks can lead to material misstatements in financial declarations. Furthermore, the report examines fraud risk, detailing how factors such as employee dissatisfaction and pressure to meet financial targets can contribute to fraudulent activities. It highlights specific examples within the DIPL case study, such as the pressure to implement new accounting systems and the implications of loan agreements, to illustrate these risks. The analysis underscores the importance of understanding and managing these risks to ensure the accuracy and reliability of financial statements. The report also references key financial ratios to evaluate the financial condition of the company. The report uses various sources to support the analysis.

Running head: AUDITING AND ASSURANCE

Auditing and Assurance

University Name

Student Name

Authors’ Note

Auditing and Assurance

University Name

Student Name

Authors’ Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2AUDITING AND ASSURANCE

Answer to Question 1:

Employment of analytical techniques to pecuniary declarations of the firm DIPL

Analytical procedure to the financial declaration of the corporation DIPL can assist in

developing the overall audit plan. However, this audit plan can be taken into account as a

specific directive that need to be tracked during the period of carrying out the audit (Duncan

and Whittington 2014). Particularly, audit plan assists assessors in sustaining audit costs at

reasonable stage and helps in avoiding misinterpretation and miscommunication with the

client of the company.

Analytical tactic of common sizing assists in evaluating financial statements to a certain

common point of reference (Baylis et al. 2017). However, this in order helps in undertaking a

comparative assessment of financial pronouncements in terms of diverse time period

otherwise in terms of different companies. Appraisers can consider different kinds or

categories of items stated in the financial declaration, check the manner of presenting

pecuniary reports. For instance, the manner of recording items namely net assets elsewise

liabilities together with equity of different owners in the financial reporting. However,

variance of financial declaration from specific point of reference assists in the process of

recognizing the deviation and at the same time assist in evaluating the overall cause of the

detected variance in a bid to understand the main reason (Homb et al. 2014). Furthermore,

the technique of analysing using key financial ratio can be regarded as a suitable analytical

method that can be aptly utilized for the purpose of comparing different financial

pronouncements and at the same time analysing specific plan of financial audit.

Illustration of manner in which financial outcomes can influence on audit plan decisions

In essence, specific outcomes of planning decisions for audit planning can be especially

affected by the analytical tactic adopted for deciphering information from the pecuniary

Answer to Question 1:

Employment of analytical techniques to pecuniary declarations of the firm DIPL

Analytical procedure to the financial declaration of the corporation DIPL can assist in

developing the overall audit plan. However, this audit plan can be taken into account as a

specific directive that need to be tracked during the period of carrying out the audit (Duncan

and Whittington 2014). Particularly, audit plan assists assessors in sustaining audit costs at

reasonable stage and helps in avoiding misinterpretation and miscommunication with the

client of the company.

Analytical tactic of common sizing assists in evaluating financial statements to a certain

common point of reference (Baylis et al. 2017). However, this in order helps in undertaking a

comparative assessment of financial pronouncements in terms of diverse time period

otherwise in terms of different companies. Appraisers can consider different kinds or

categories of items stated in the financial declaration, check the manner of presenting

pecuniary reports. For instance, the manner of recording items namely net assets elsewise

liabilities together with equity of different owners in the financial reporting. However,

variance of financial declaration from specific point of reference assists in the process of

recognizing the deviation and at the same time assist in evaluating the overall cause of the

detected variance in a bid to understand the main reason (Homb et al. 2014). Furthermore,

the technique of analysing using key financial ratio can be regarded as a suitable analytical

method that can be aptly utilized for the purpose of comparing different financial

pronouncements and at the same time analysing specific plan of financial audit.

Illustration of manner in which financial outcomes can influence on audit plan decisions

In essence, specific outcomes of planning decisions for audit planning can be especially

affected by the analytical tactic adopted for deciphering information from the pecuniary

3AUDITING AND ASSURANCE

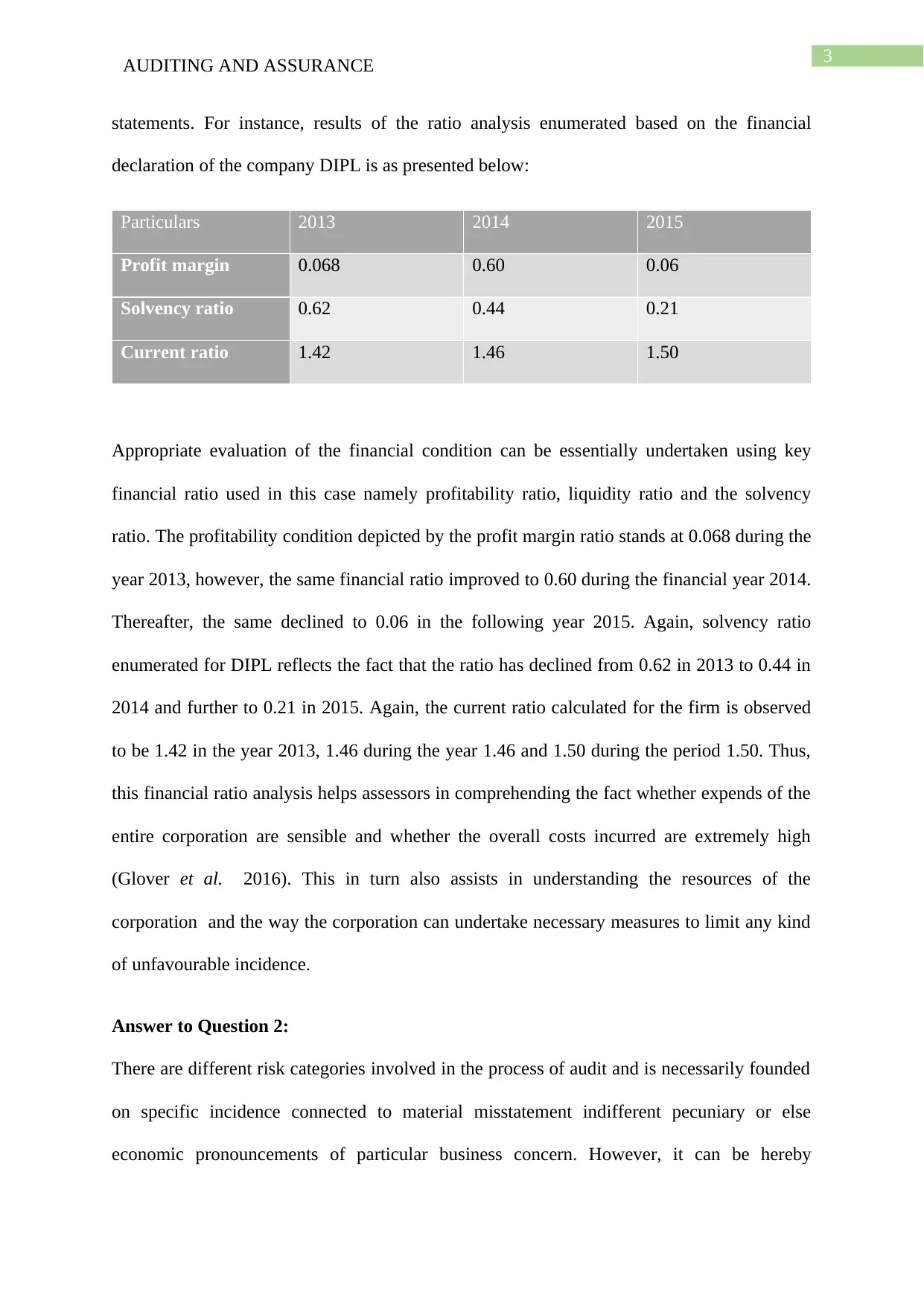

statements. For instance, results of the ratio analysis enumerated based on the financial

declaration of the company DIPL is as presented below:

Particulars 2013 2014 2015

Profit margin 0.068 0.60 0.06

Solvency ratio 0.62 0.44 0.21

Current ratio 1.42 1.46 1.50

Appropriate evaluation of the financial condition can be essentially undertaken using key

financial ratio used in this case namely profitability ratio, liquidity ratio and the solvency

ratio. The profitability condition depicted by the profit margin ratio stands at 0.068 during the

year 2013, however, the same financial ratio improved to 0.60 during the financial year 2014.

Thereafter, the same declined to 0.06 in the following year 2015. Again, solvency ratio

enumerated for DIPL reflects the fact that the ratio has declined from 0.62 in 2013 to 0.44 in

2014 and further to 0.21 in 2015. Again, the current ratio calculated for the firm is observed

to be 1.42 in the year 2013, 1.46 during the year 1.46 and 1.50 during the period 1.50. Thus,

this financial ratio analysis helps assessors in comprehending the fact whether expends of the

entire corporation are sensible and whether the overall costs incurred are extremely high

(Glover et al. 2016). This in turn also assists in understanding the resources of the

corporation and the way the corporation can undertake necessary measures to limit any kind

of unfavourable incidence.

Answer to Question 2:

There are different risk categories involved in the process of audit and is necessarily founded

on specific incidence connected to material misstatement indifferent pecuniary or else

economic pronouncements of particular business concern. However, it can be hereby

statements. For instance, results of the ratio analysis enumerated based on the financial

declaration of the company DIPL is as presented below:

Particulars 2013 2014 2015

Profit margin 0.068 0.60 0.06

Solvency ratio 0.62 0.44 0.21

Current ratio 1.42 1.46 1.50

Appropriate evaluation of the financial condition can be essentially undertaken using key

financial ratio used in this case namely profitability ratio, liquidity ratio and the solvency

ratio. The profitability condition depicted by the profit margin ratio stands at 0.068 during the

year 2013, however, the same financial ratio improved to 0.60 during the financial year 2014.

Thereafter, the same declined to 0.06 in the following year 2015. Again, solvency ratio

enumerated for DIPL reflects the fact that the ratio has declined from 0.62 in 2013 to 0.44 in

2014 and further to 0.21 in 2015. Again, the current ratio calculated for the firm is observed

to be 1.42 in the year 2013, 1.46 during the year 1.46 and 1.50 during the period 1.50. Thus,

this financial ratio analysis helps assessors in comprehending the fact whether expends of the

entire corporation are sensible and whether the overall costs incurred are extremely high

(Glover et al. 2016). This in turn also assists in understanding the resources of the

corporation and the way the corporation can undertake necessary measures to limit any kind

of unfavourable incidence.

Answer to Question 2:

There are different risk categories involved in the process of audit and is necessarily founded

on specific incidence connected to material misstatement indifferent pecuniary or else

economic pronouncements of particular business concern. However, it can be hereby

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

4AUDITING AND ASSURANCE

recognised that there exists diverse classes of unsystematic risk that can point out towards

different types of risks identified from financial pronouncements of the business. Again, there

also exists different categories of other risks that can be functional for both financial along

with different non-financial facets that in due course can be avoided in a specific corporation

(Arens et al. 2016). This in turn can help in representing both true as well as fair view of

different kinds of economic declarations. Nevertheless, the appraiser might possibly find it

quite demanding to detect specific risks. There exists diverse classes of correlated risks that

might arise due to omission together with different range of errors along with mistakes that

are necessarily unthinkable for different bookkeepers.

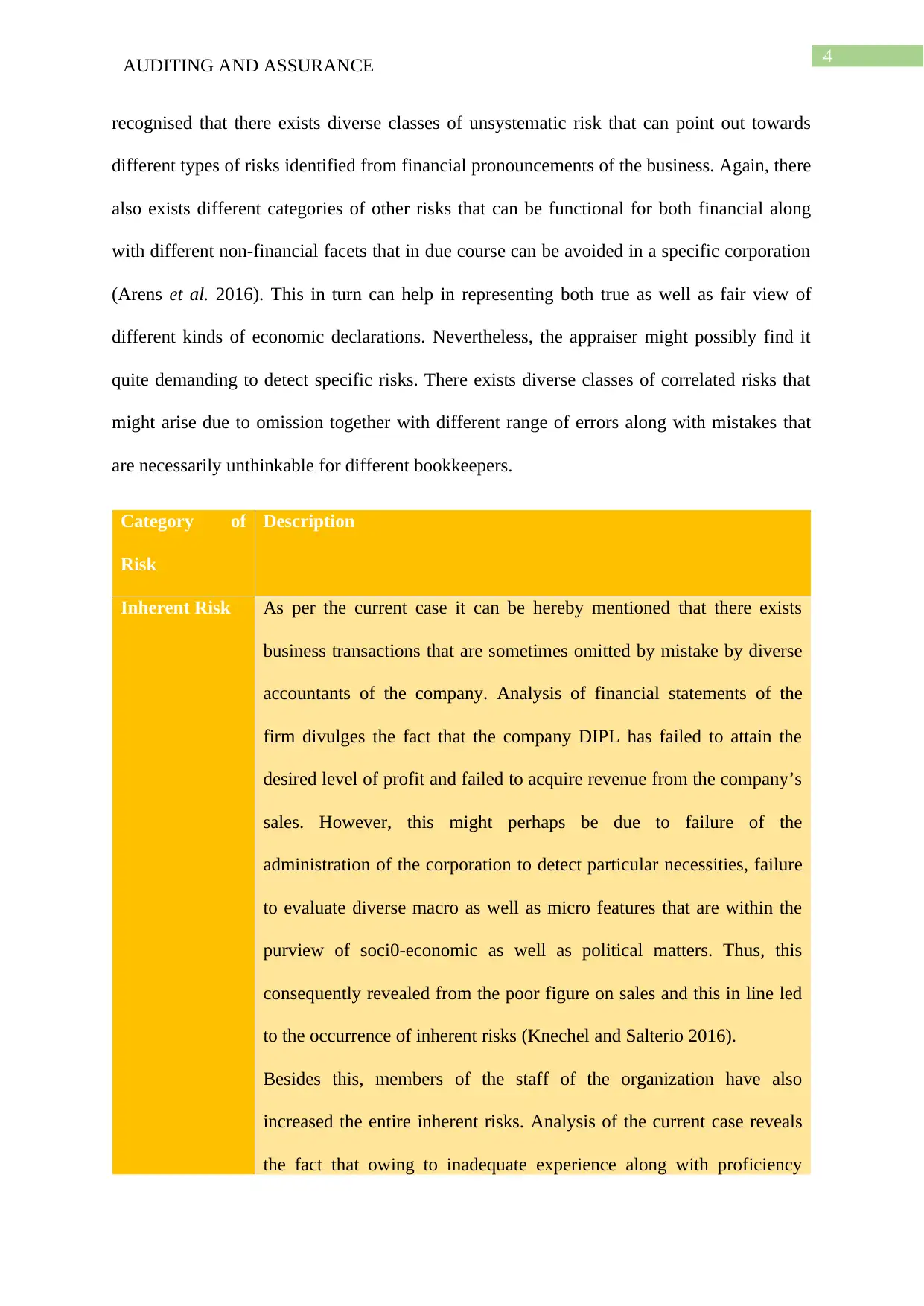

Category of

Risk

Description

Inherent Risk As per the current case it can be hereby mentioned that there exists

business transactions that are sometimes omitted by mistake by diverse

accountants of the company. Analysis of financial statements of the

firm divulges the fact that the company DIPL has failed to attain the

desired level of profit and failed to acquire revenue from the company’s

sales. However, this might perhaps be due to failure of the

administration of the corporation to detect particular necessities, failure

to evaluate diverse macro as well as micro features that are within the

purview of soci0-economic as well as political matters. Thus, this

consequently revealed from the poor figure on sales and this in line led

to the occurrence of inherent risks (Knechel and Salterio 2016).

Besides this, members of the staff of the organization have also

increased the entire inherent risks. Analysis of the current case reveals

the fact that owing to inadequate experience along with proficiency

recognised that there exists diverse classes of unsystematic risk that can point out towards

different types of risks identified from financial pronouncements of the business. Again, there

also exists different categories of other risks that can be functional for both financial along

with different non-financial facets that in due course can be avoided in a specific corporation

(Arens et al. 2016). This in turn can help in representing both true as well as fair view of

different kinds of economic declarations. Nevertheless, the appraiser might possibly find it

quite demanding to detect specific risks. There exists diverse classes of correlated risks that

might arise due to omission together with different range of errors along with mistakes that

are necessarily unthinkable for different bookkeepers.

Category of

Risk

Description

Inherent Risk As per the current case it can be hereby mentioned that there exists

business transactions that are sometimes omitted by mistake by diverse

accountants of the company. Analysis of financial statements of the

firm divulges the fact that the company DIPL has failed to attain the

desired level of profit and failed to acquire revenue from the company’s

sales. However, this might perhaps be due to failure of the

administration of the corporation to detect particular necessities, failure

to evaluate diverse macro as well as micro features that are within the

purview of soci0-economic as well as political matters. Thus, this

consequently revealed from the poor figure on sales and this in line led

to the occurrence of inherent risks (Knechel and Salterio 2016).

Besides this, members of the staff of the organization have also

increased the entire inherent risks. Analysis of the current case reveals

the fact that owing to inadequate experience along with proficiency

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

5AUDITING AND ASSURANCE

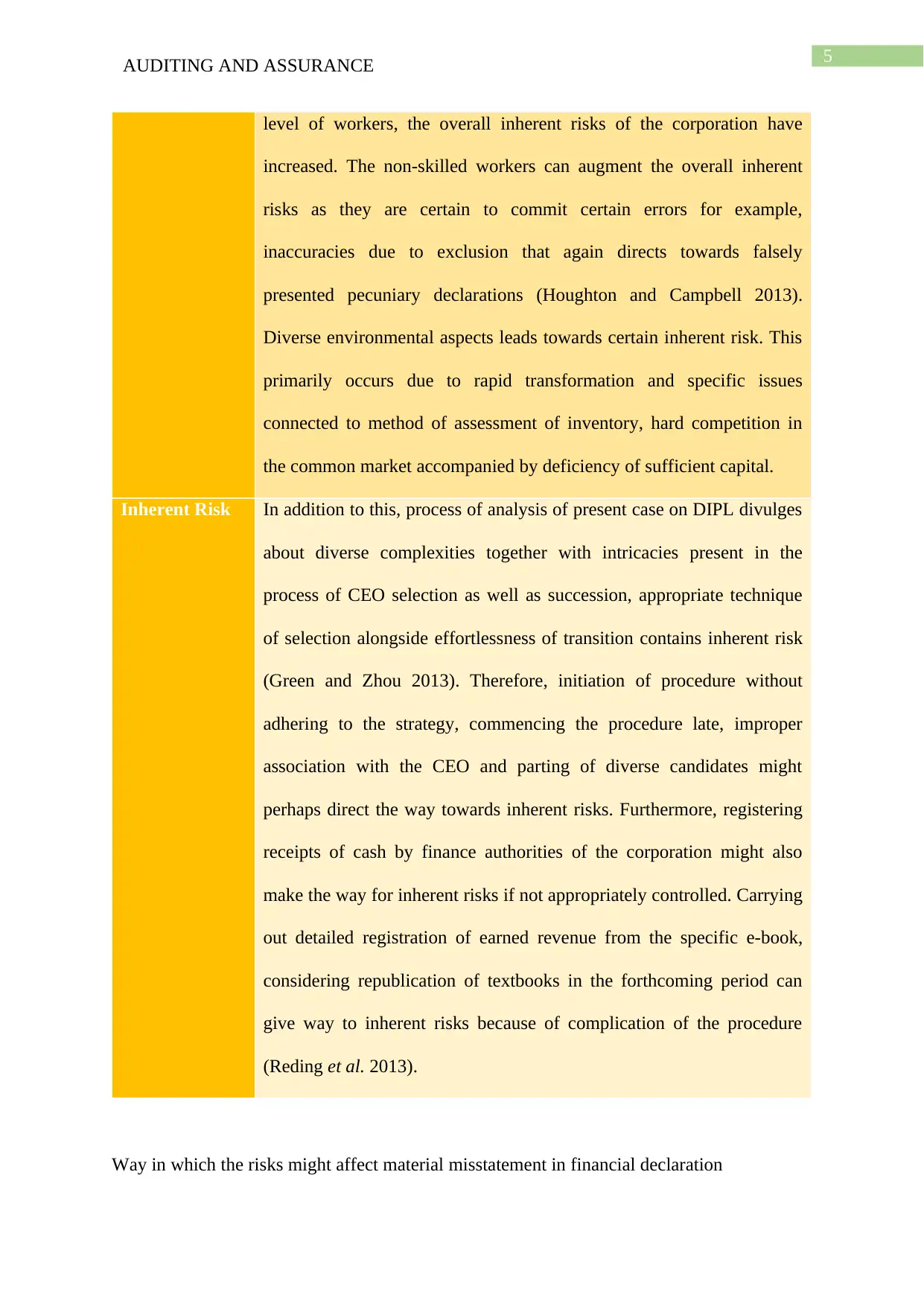

level of workers, the overall inherent risks of the corporation have

increased. The non-skilled workers can augment the overall inherent

risks as they are certain to commit certain errors for example,

inaccuracies due to exclusion that again directs towards falsely

presented pecuniary declarations (Houghton and Campbell 2013).

Diverse environmental aspects leads towards certain inherent risk. This

primarily occurs due to rapid transformation and specific issues

connected to method of assessment of inventory, hard competition in

the common market accompanied by deficiency of sufficient capital.

Inherent Risk In addition to this, process of analysis of present case on DIPL divulges

about diverse complexities together with intricacies present in the

process of CEO selection as well as succession, appropriate technique

of selection alongside effortlessness of transition contains inherent risk

(Green and Zhou 2013). Therefore, initiation of procedure without

adhering to the strategy, commencing the procedure late, improper

association with the CEO and parting of diverse candidates might

perhaps direct the way towards inherent risks. Furthermore, registering

receipts of cash by finance authorities of the corporation might also

make the way for inherent risks if not appropriately controlled. Carrying

out detailed registration of earned revenue from the specific e-book,

considering republication of textbooks in the forthcoming period can

give way to inherent risks because of complication of the procedure

(Reding et al. 2013).

Way in which the risks might affect material misstatement in financial declaration

level of workers, the overall inherent risks of the corporation have

increased. The non-skilled workers can augment the overall inherent

risks as they are certain to commit certain errors for example,

inaccuracies due to exclusion that again directs towards falsely

presented pecuniary declarations (Houghton and Campbell 2013).

Diverse environmental aspects leads towards certain inherent risk. This

primarily occurs due to rapid transformation and specific issues

connected to method of assessment of inventory, hard competition in

the common market accompanied by deficiency of sufficient capital.

Inherent Risk In addition to this, process of analysis of present case on DIPL divulges

about diverse complexities together with intricacies present in the

process of CEO selection as well as succession, appropriate technique

of selection alongside effortlessness of transition contains inherent risk

(Green and Zhou 2013). Therefore, initiation of procedure without

adhering to the strategy, commencing the procedure late, improper

association with the CEO and parting of diverse candidates might

perhaps direct the way towards inherent risks. Furthermore, registering

receipts of cash by finance authorities of the corporation might also

make the way for inherent risks if not appropriately controlled. Carrying

out detailed registration of earned revenue from the specific e-book,

considering republication of textbooks in the forthcoming period can

give way to inherent risks because of complication of the procedure

(Reding et al. 2013).

Way in which the risks might affect material misstatement in financial declaration

6AUDITING AND ASSURANCE

Identified inherent risks can be regarded as the proneness of a specific assertion in relation to

material misstatement.

Extreme pressure on workforce as well as management (Christensen et al. 2016)

Risks of errors in addition to inaccurate misrepresentation

Reliability of the complete administration

Pressure on management

Nature of business

Answer to Question 3:

It can be hereby mentioned that fraud risk directs the way towards significant losses of assets

due to incidence of fraud. However, discontentment of workers stemming from extreme work

pressure can prompt the members of the staff to engage in the act of fraudulent actions.

Furthermore, anticipations of the specific management as regards financial results and

expectations to achieve particular level of performance directs the way towards occurrence of

fraud risk (Kilgore et al. 2014). In addition to this, there are occurs the necessity to

pronounce particular financial results that in turn can help in averting risks of presenting

falsified statements.

Risk Description

Fraud

risk

This risks might perhaps take place due to the engagement of the dissatisfied workers

in different fraudulent activities. In this particular case on functionalities of the firm

DIPL focuses on the excessive pressure of the board to acquire a new system for

accounting. However, it can be hereby mentioned that this too much pressure on the

members of the staff to undertake the task of installing the new technologically

Identified inherent risks can be regarded as the proneness of a specific assertion in relation to

material misstatement.

Extreme pressure on workforce as well as management (Christensen et al. 2016)

Risks of errors in addition to inaccurate misrepresentation

Reliability of the complete administration

Pressure on management

Nature of business

Answer to Question 3:

It can be hereby mentioned that fraud risk directs the way towards significant losses of assets

due to incidence of fraud. However, discontentment of workers stemming from extreme work

pressure can prompt the members of the staff to engage in the act of fraudulent actions.

Furthermore, anticipations of the specific management as regards financial results and

expectations to achieve particular level of performance directs the way towards occurrence of

fraud risk (Kilgore et al. 2014). In addition to this, there are occurs the necessity to

pronounce particular financial results that in turn can help in averting risks of presenting

falsified statements.

Risk Description

Fraud

risk

This risks might perhaps take place due to the engagement of the dissatisfied workers

in different fraudulent activities. In this particular case on functionalities of the firm

DIPL focuses on the excessive pressure of the board to acquire a new system for

accounting. However, it can be hereby mentioned that this too much pressure on the

members of the staff to undertake the task of installing the new technologically

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

7AUDITING AND ASSURANCE

advanced and IT induced system of IT might perhaps direct the way towards

fraudulent actions (Chou 2015). Subsequently, this refers to the fact that the workers

might perhaps get involved in diverse fraudulent actions and manage the process of

settlement in an inappropriate manner and consequently commit material

misstatement. Nevertheless, this current case study also explicates illustratively that

the inappropriate process of dealing with the entire process of executing the work of

installing the new system of accounting might turn to inappropriate appropriation of

specific business transactions during the closing of the year (Pizzini et al. 2014).

Again, this sequentially might possibly direct towards occurrence of incidence of loss

owing to material misstatement along with fraud risk.

Fraud

risk

Besides this, another risk that might perhaps stem comprises of fraudulent actions

involved in the process of preparation as well as presentation of financial

pronouncements. Particularly, at the time when there is extreme anticipation from

outside sponsors to announce particular financial facts otherwise to attain particular

performance targets by the management leads to risk of material misstatement

(Svanström 2013). In addition to this, attainment of specific goals in a bid to qualify

to procure debt also involves huge risk of unfitting financial declarations. However,

declarations as regards the financial condition of the corporation DIPL divulges about

the revenue of the corporation and this represents the fact that the company has raised

the overall revenue of the firm during the specific period that is between the year 2013

and the year 2015. Besides this, the calculated gross profit along with the net profit

can also be observed to have risen. Nevertheless, the current case study divulges the

fact that this specific corporation DIPL has garnered loan worth 7.5 million from the

organization BDO Finance. Apart from this, this case under consideration also

replicates that this specific loan has a specified loan contract that calls for the need of

advanced and IT induced system of IT might perhaps direct the way towards

fraudulent actions (Chou 2015). Subsequently, this refers to the fact that the workers

might perhaps get involved in diverse fraudulent actions and manage the process of

settlement in an inappropriate manner and consequently commit material

misstatement. Nevertheless, this current case study also explicates illustratively that

the inappropriate process of dealing with the entire process of executing the work of

installing the new system of accounting might turn to inappropriate appropriation of

specific business transactions during the closing of the year (Pizzini et al. 2014).

Again, this sequentially might possibly direct towards occurrence of incidence of loss

owing to material misstatement along with fraud risk.

Fraud

risk

Besides this, another risk that might perhaps stem comprises of fraudulent actions

involved in the process of preparation as well as presentation of financial

pronouncements. Particularly, at the time when there is extreme anticipation from

outside sponsors to announce particular financial facts otherwise to attain particular

performance targets by the management leads to risk of material misstatement

(Svanström 2013). In addition to this, attainment of specific goals in a bid to qualify

to procure debt also involves huge risk of unfitting financial declarations. However,

declarations as regards the financial condition of the corporation DIPL divulges about

the revenue of the corporation and this represents the fact that the company has raised

the overall revenue of the firm during the specific period that is between the year 2013

and the year 2015. Besides this, the calculated gross profit along with the net profit

can also be observed to have risen. Nevertheless, the current case study divulges the

fact that this specific corporation DIPL has garnered loan worth 7.5 million from the

organization BDO Finance. Apart from this, this case under consideration also

replicates that this specific loan has a specified loan contract that calls for the need of

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

8AUDITING AND ASSURANCE

maintaining a particular current ratio of roughly 1.5 together with debt equity ratio

lesser than 1. Thus, this in turn reflects that these factors necessitates the business

firms to keep a certain financial ratio that subsequently can help in acquiring credit.

Therefore, this can consequently lead to different fraudulent activities and direct the

way towards inappropriate representation of financial condition. Essentially, failure of

the business to maintain the specific yardstick can in due course make the corporation

non-qualified to obtain funds from BDO Finance.

As per the given case study, it can hereby mentioned that procedure of valuation of diverse

inventory of raw material at specific average cost was not appropriate as the current paper

cost was substantially over and above the average cost. Again, risk of detecting fraudulent

activities engaged in the process of execution of accounting system using information

technology in the process of accounting can be undertaken by observing diverse actions at

different stages (Edgley et al. 2015). Initially, the risk associated to reporting economic

declarations can be detected by undertaking analysis of financial declarations by diverse

assessors, tracking systems of control periodically.

maintaining a particular current ratio of roughly 1.5 together with debt equity ratio

lesser than 1. Thus, this in turn reflects that these factors necessitates the business

firms to keep a certain financial ratio that subsequently can help in acquiring credit.

Therefore, this can consequently lead to different fraudulent activities and direct the

way towards inappropriate representation of financial condition. Essentially, failure of

the business to maintain the specific yardstick can in due course make the corporation

non-qualified to obtain funds from BDO Finance.

As per the given case study, it can hereby mentioned that procedure of valuation of diverse

inventory of raw material at specific average cost was not appropriate as the current paper

cost was substantially over and above the average cost. Again, risk of detecting fraudulent

activities engaged in the process of execution of accounting system using information

technology in the process of accounting can be undertaken by observing diverse actions at

different stages (Edgley et al. 2015). Initially, the risk associated to reporting economic

declarations can be detected by undertaking analysis of financial declarations by diverse

assessors, tracking systems of control periodically.

9AUDITING AND ASSURANCE

Reference

Arens, A.A., Elder, R.J., Beasley, M.S. and Hogan, C.E., 2016. Auditing and assurance

services. Pearson.

Baylis, R.M., Burnap, P., Clatworthy, M.A., Gad, M.A. and Pong, C.K., 2017. Private

lenders’ demand for audit. Journal of Accounting and Economics.

Chou, D.C., 2015. Cloud computing risk and audit issues. Computer Standards & Interfaces,

42, pp.137-142.

Christensen, B.E., Glover, S.M., Omer, T.C. and Shelley, M.K., 2016. Understanding audit

quality: Insights from audit professionals and investors. Contemporary Accounting Research,

33(4), pp.1648-1684.

Duncan, B. and Whittington, M., 2014, September. Compliance with standards, assurance

and audit: Does this equal security?. In Proceedings of the 7th International Conference on

Security of Information and Networks (p. 77). ACM.

Edgley, C., Jones, M.J. and Atkins, J., 2015. The adoption of the materiality concept in social

and environmental reporting assurance: A field study approach. The British Accounting

Review, 47(1), pp.1-18.

Glover, S.M., Prawitt, D.F. and Messier, W.F., 2016. Auditing and Assurance Services: A

Systematic Approach 10th.

Green, W. and Zhou, S., 2013. An international examination of assurance practices on carbon

emissions disclosures. Australian Accounting Review, 23(1), pp.54-66.

Homb, N.M., Sheybani, S., Derby, D. and Wood, K., 2014. Audit and feedback intervention:

An examination of differences in chiropractic record-keeping compliance. Journal of

Chiropractic Education, 28(2), pp.123-129.

Reference

Arens, A.A., Elder, R.J., Beasley, M.S. and Hogan, C.E., 2016. Auditing and assurance

services. Pearson.

Baylis, R.M., Burnap, P., Clatworthy, M.A., Gad, M.A. and Pong, C.K., 2017. Private

lenders’ demand for audit. Journal of Accounting and Economics.

Chou, D.C., 2015. Cloud computing risk and audit issues. Computer Standards & Interfaces,

42, pp.137-142.

Christensen, B.E., Glover, S.M., Omer, T.C. and Shelley, M.K., 2016. Understanding audit

quality: Insights from audit professionals and investors. Contemporary Accounting Research,

33(4), pp.1648-1684.

Duncan, B. and Whittington, M., 2014, September. Compliance with standards, assurance

and audit: Does this equal security?. In Proceedings of the 7th International Conference on

Security of Information and Networks (p. 77). ACM.

Edgley, C., Jones, M.J. and Atkins, J., 2015. The adoption of the materiality concept in social

and environmental reporting assurance: A field study approach. The British Accounting

Review, 47(1), pp.1-18.

Glover, S.M., Prawitt, D.F. and Messier, W.F., 2016. Auditing and Assurance Services: A

Systematic Approach 10th.

Green, W. and Zhou, S., 2013. An international examination of assurance practices on carbon

emissions disclosures. Australian Accounting Review, 23(1), pp.54-66.

Homb, N.M., Sheybani, S., Derby, D. and Wood, K., 2014. Audit and feedback intervention:

An examination of differences in chiropractic record-keeping compliance. Journal of

Chiropractic Education, 28(2), pp.123-129.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.