Fraud Risk Assessment in DIPL

VerifiedAdded on 2020/03/04

|10

|2217

|43

AI Summary

This assignment examines potential fraud risks within the context of DIPL, specifically addressing the challenges auditors face in identifying such risks. It delves into two key areas: inadequate segregation of duties that can facilitate fraudulent activities and the implementation of a new IT system without proper reconciliation, potentially driven by personal motives of directors. The assignment emphasizes the crucial role of auditors in mitigating these risks through measures like ensuring work segregation, conducting thorough reconciliations, and scrutinizing management justifications for haste.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

By student name

Professor

University

Date: 16 August, 2017.

Professor

University

Date: 16 August, 2017.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1

Contents

Question no 1…………………………………………………………………...2

Question no 2…………………………………………………………………...5

Question no 3…………………………………………………………….....….7

Refrences.....………………………………………………………………....... 9

1 | P a g e

Contents

Question no 1…………………………………………………………………...2

Question no 2…………………………………………………………………...5

Question no 3…………………………………………………………….....….7

Refrences.....………………………………………………………………....... 9

1 | P a g e

2

Question no 1

Audit is an independent examination of the financial statements and books of accounts

prepared by the management by the auditors of the company to check whether the financials are

showing correct and unbiased view of the state of affairs and to express their opinion thereof. Audit is

generally conducted using the substantive and analytical procedures. Substantive audit procedures are

of great relevance in ascertaining whether all the audit procedures an d cares and check have been

applied consistently and thoroughly while preparing the books of accounts and preparation of financial

summary. It generally includes vouching of incomes and expenses and verification of assets and

liabilities. But when these 2 measures are not sufficient and does not gives the confidence on the

arithmetical accuracy of the books of accounts then the auditor has to switch to analytical procedures

which includes ratio analysis, trend analysis, variance analysis and a study of fluctuation in the numbers

based on the past financial statements. For this, generally the data points include the past years

financial data, the industry trend and average, the budgeted numbers and the forecasted numbers. IN

case of DIPL limited, the auditors have also changed as compared to the last year, so substantive

procedures would not be enough & the new auditors would have to resort to the analytical audit

procedures to gain the confidence on the transparency of the accounts prepared and the verification of

the opening balances of the client. If post all this comparison, we would come to know that still the

decision cannot be taken whether the books are to materially misstated, then the auditors would have

to increase their scope of check and would have to apply further analytical procedures keeping into

consideration the maintenance of the internal financial control in the company by the management. If

the internal financial controls are adequate, less is the amount of risk, less will be the deviation of the

actual from the standard and hence, less is the extent of checking reqd., however, in the other case,

weak the leave of internal control maintained by DIPL, the more is the level of analytical procedures to

be applied. Further, the management needs to answer all the queries raised b the new auditors in case

of any clarifications. There are various ways in which the auditor can use these analytical procedures for

ascertaining the credit viability of the company. The examination of the financial statements of previous

year can be done, by derivation important key financial ratios that help the auditor in forming an

opinion on the financial viability of the company. In addition, comparison with the set industry standards

can be done accordingly, by trend analysis and making forecasts and budgeting. If the auditor finds from

any deviation from the expected standards then he needs to find the reason of the same and approach

the management to comment on the same. These are few basic tools of analytical analysis, that can help

the auditor in making a statement (Bae 2017). In the given case study, financial information of past years

2 | P a g e

Question no 1

Audit is an independent examination of the financial statements and books of accounts

prepared by the management by the auditors of the company to check whether the financials are

showing correct and unbiased view of the state of affairs and to express their opinion thereof. Audit is

generally conducted using the substantive and analytical procedures. Substantive audit procedures are

of great relevance in ascertaining whether all the audit procedures an d cares and check have been

applied consistently and thoroughly while preparing the books of accounts and preparation of financial

summary. It generally includes vouching of incomes and expenses and verification of assets and

liabilities. But when these 2 measures are not sufficient and does not gives the confidence on the

arithmetical accuracy of the books of accounts then the auditor has to switch to analytical procedures

which includes ratio analysis, trend analysis, variance analysis and a study of fluctuation in the numbers

based on the past financial statements. For this, generally the data points include the past years

financial data, the industry trend and average, the budgeted numbers and the forecasted numbers. IN

case of DIPL limited, the auditors have also changed as compared to the last year, so substantive

procedures would not be enough & the new auditors would have to resort to the analytical audit

procedures to gain the confidence on the transparency of the accounts prepared and the verification of

the opening balances of the client. If post all this comparison, we would come to know that still the

decision cannot be taken whether the books are to materially misstated, then the auditors would have

to increase their scope of check and would have to apply further analytical procedures keeping into

consideration the maintenance of the internal financial control in the company by the management. If

the internal financial controls are adequate, less is the amount of risk, less will be the deviation of the

actual from the standard and hence, less is the extent of checking reqd., however, in the other case,

weak the leave of internal control maintained by DIPL, the more is the level of analytical procedures to

be applied. Further, the management needs to answer all the queries raised b the new auditors in case

of any clarifications. There are various ways in which the auditor can use these analytical procedures for

ascertaining the credit viability of the company. The examination of the financial statements of previous

year can be done, by derivation important key financial ratios that help the auditor in forming an

opinion on the financial viability of the company. In addition, comparison with the set industry standards

can be done accordingly, by trend analysis and making forecasts and budgeting. If the auditor finds from

any deviation from the expected standards then he needs to find the reason of the same and approach

the management to comment on the same. These are few basic tools of analytical analysis, that can help

the auditor in making a statement (Bae 2017). In the given case study, financial information of past years

2 | P a g e

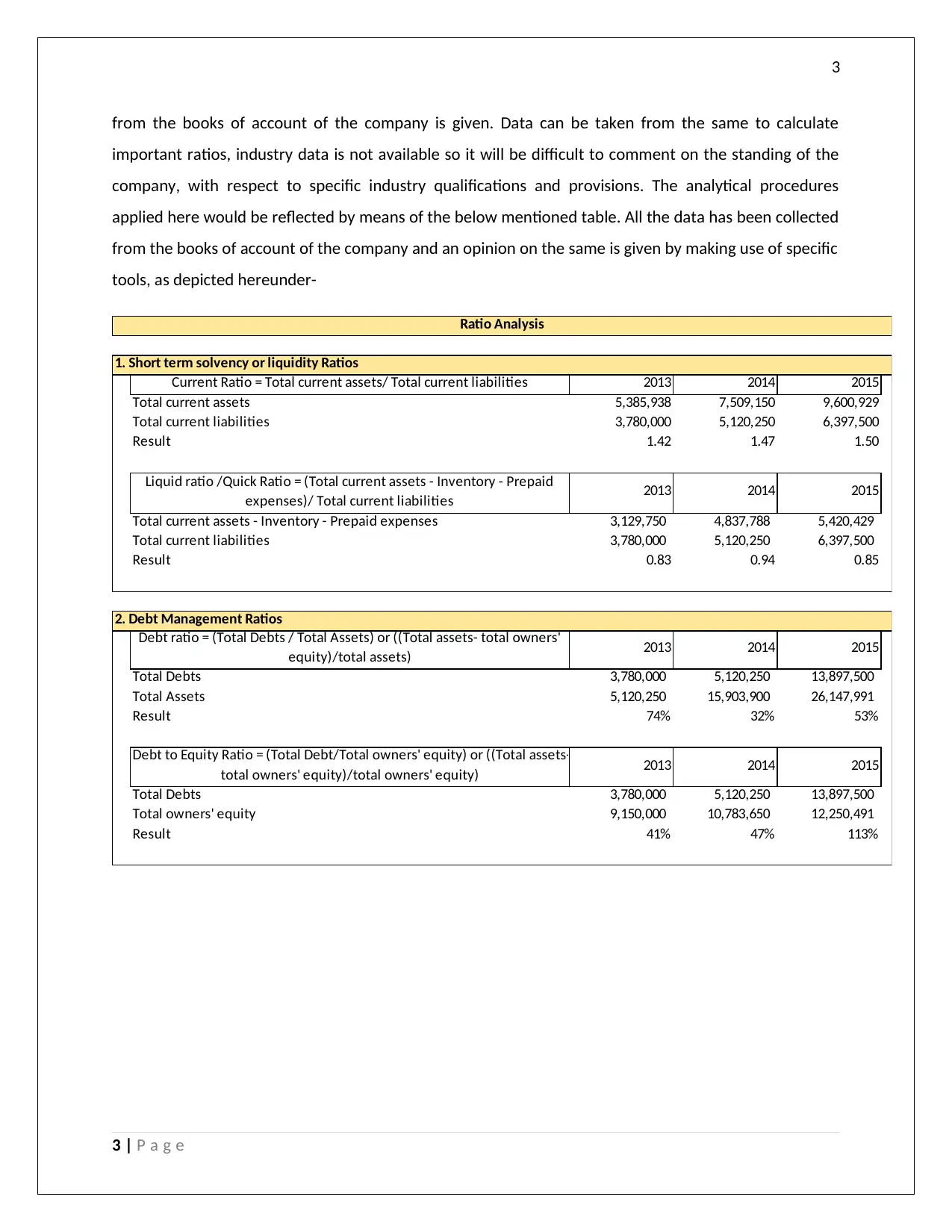

3

from the books of account of the company is given. Data can be taken from the same to calculate

important ratios, industry data is not available so it will be difficult to comment on the standing of the

company, with respect to specific industry qualifications and provisions. The analytical procedures

applied here would be reflected by means of the below mentioned table. All the data has been collected

from the books of account of the company and an opinion on the same is given by making use of specific

tools, as depicted hereunder-

1. Short term solvency or liquidity Ratios

2013 2014 2015

Total current assets 5,385,938 7,509,150 9,600,929

Total current liabilities 3,780,000 5,120,250 6,397,500

Result 1.42 1.47 1.50

2013 2014 2015

Total current assets - Inventory - Prepaid expenses 3,129,750 4,837,788 5,420,429

Total current liabilities 3,780,000 5,120,250 6,397,500

Result 0.83 0.94 0.85

2. Debt Management Ratios

2013 2014 2015

Total Debts 3,780,000 5,120,250 13,897,500

Total Assets 5,120,250 15,903,900 26,147,991

Result 74% 32% 53%

2013 2014 2015

Total Debts 3,780,000 5,120,250 13,897,500

Total owners' equity 9,150,000 10,783,650 12,250,491

Result 41% 47% 113%

Current Ratio = Total current assets/ Total current liabilities

Liquid ratio /Quick Ratio = (Total current assets - Inventory - Prepaid

expenses)/ Total current liabilities

Debt ratio = (Total Debts / Total Assets) or ((Total assets- total owners'

equity)/total assets)

Debt to Equity Ratio = (Total Debt/Total owners' equity) or ((Total assets-

total owners' equity)/total owners' equity)

Ratio Analysis

3 | P a g e

from the books of account of the company is given. Data can be taken from the same to calculate

important ratios, industry data is not available so it will be difficult to comment on the standing of the

company, with respect to specific industry qualifications and provisions. The analytical procedures

applied here would be reflected by means of the below mentioned table. All the data has been collected

from the books of account of the company and an opinion on the same is given by making use of specific

tools, as depicted hereunder-

1. Short term solvency or liquidity Ratios

2013 2014 2015

Total current assets 5,385,938 7,509,150 9,600,929

Total current liabilities 3,780,000 5,120,250 6,397,500

Result 1.42 1.47 1.50

2013 2014 2015

Total current assets - Inventory - Prepaid expenses 3,129,750 4,837,788 5,420,429

Total current liabilities 3,780,000 5,120,250 6,397,500

Result 0.83 0.94 0.85

2. Debt Management Ratios

2013 2014 2015

Total Debts 3,780,000 5,120,250 13,897,500

Total Assets 5,120,250 15,903,900 26,147,991

Result 74% 32% 53%

2013 2014 2015

Total Debts 3,780,000 5,120,250 13,897,500

Total owners' equity 9,150,000 10,783,650 12,250,491

Result 41% 47% 113%

Current Ratio = Total current assets/ Total current liabilities

Liquid ratio /Quick Ratio = (Total current assets - Inventory - Prepaid

expenses)/ Total current liabilities

Debt ratio = (Total Debts / Total Assets) or ((Total assets- total owners'

equity)/total assets)

Debt to Equity Ratio = (Total Debt/Total owners' equity) or ((Total assets-

total owners' equity)/total owners' equity)

Ratio Analysis

3 | P a g e

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

4

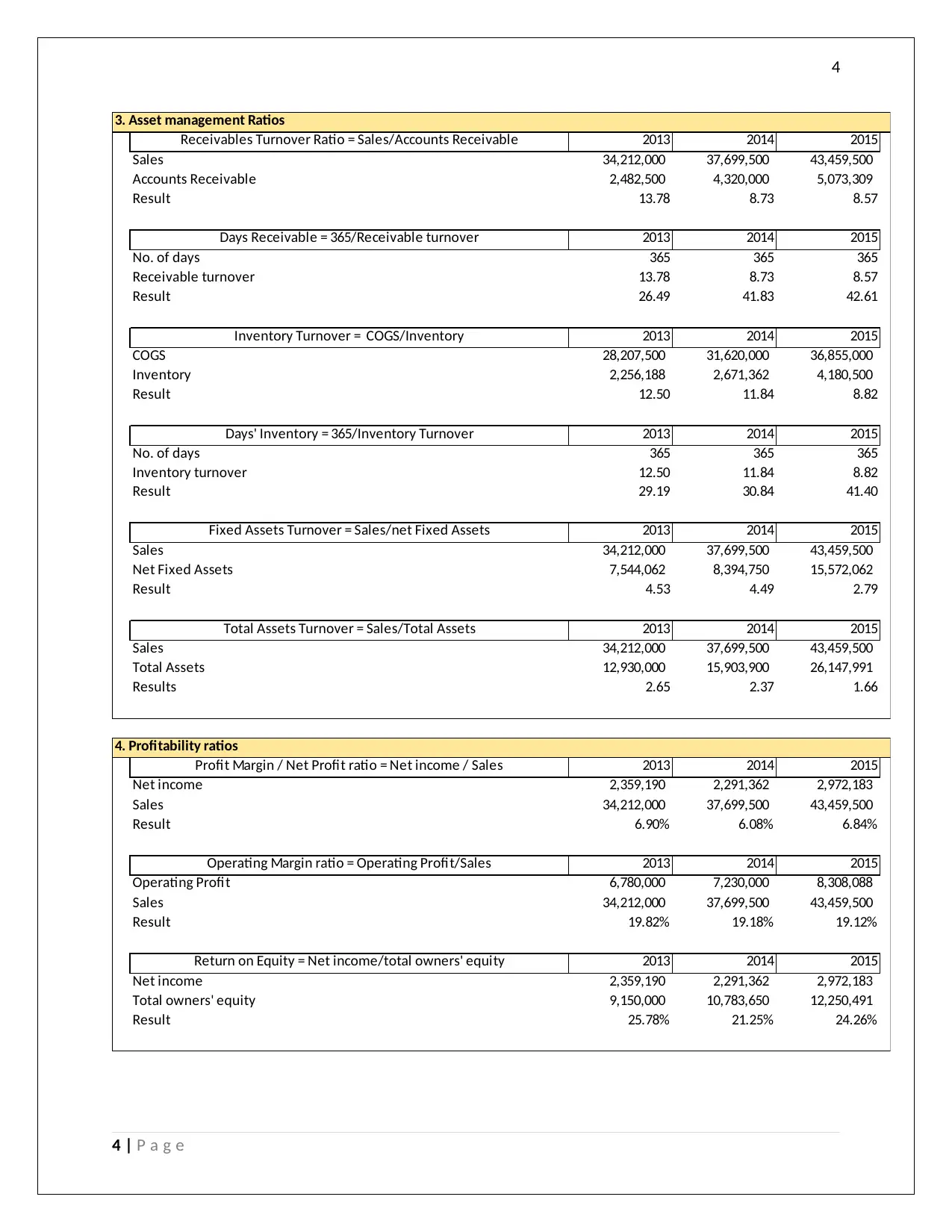

3. Asset management Ratios

2013 2014 2015

Sales 34,212,000 37,699,500 43,459,500

Accounts Receivable 2,482,500 4,320,000 5,073,309

Result 13.78 8.73 8.57

2013 2014 2015

No. of days 365 365 365

Receivable turnover 13.78 8.73 8.57

Result 26.49 41.83 42.61

2013 2014 2015

COGS 28,207,500 31,620,000 36,855,000

Inventory 2,256,188 2,671,362 4,180,500

Result 12.50 11.84 8.82

2013 2014 2015

No. of days 365 365 365

Inventory turnover 12.50 11.84 8.82

Result 29.19 30.84 41.40

2013 2014 2015

Sales 34,212,000 37,699,500 43,459,500

Net Fixed Assets 7,544,062 8,394,750 15,572,062

Result 4.53 4.49 2.79

2013 2014 2015

Sales 34,212,000 37,699,500 43,459,500

Total Assets 12,930,000 15,903,900 26,147,991

Results 2.65 2.37 1.66

4. Profitability ratios

2013 2014 2015

Net income 2,359,190 2,291,362 2,972,183

Sales 34,212,000 37,699,500 43,459,500

Result 6.90% 6.08% 6.84%

2013 2014 2015

Operating Profit 6,780,000 7,230,000 8,308,088

Sales 34,212,000 37,699,500 43,459,500

Result 19.82% 19.18% 19.12%

2013 2014 2015

Net income 2,359,190 2,291,362 2,972,183

Total owners' equity 9,150,000 10,783,650 12,250,491

Result 25.78% 21.25% 24.26%

Inventory Turnover = COGS/Inventory

Days' Inventory = 365/Inventory Turnover

Fixed Assets Turnover = Sales/net Fixed Assets

Total Assets Turnover = Sales/Total Assets

Profit Margin / Net Profit ratio = Net income / Sales

Operating Margin ratio = Operating Profit/Sales

Return on Equity = Net income/total owners' equity

Receivables Turnover Ratio = Sales/Accounts Receivable

Days Receivable = 365/Receivable turnover

4 | P a g e

3. Asset management Ratios

2013 2014 2015

Sales 34,212,000 37,699,500 43,459,500

Accounts Receivable 2,482,500 4,320,000 5,073,309

Result 13.78 8.73 8.57

2013 2014 2015

No. of days 365 365 365

Receivable turnover 13.78 8.73 8.57

Result 26.49 41.83 42.61

2013 2014 2015

COGS 28,207,500 31,620,000 36,855,000

Inventory 2,256,188 2,671,362 4,180,500

Result 12.50 11.84 8.82

2013 2014 2015

No. of days 365 365 365

Inventory turnover 12.50 11.84 8.82

Result 29.19 30.84 41.40

2013 2014 2015

Sales 34,212,000 37,699,500 43,459,500

Net Fixed Assets 7,544,062 8,394,750 15,572,062

Result 4.53 4.49 2.79

2013 2014 2015

Sales 34,212,000 37,699,500 43,459,500

Total Assets 12,930,000 15,903,900 26,147,991

Results 2.65 2.37 1.66

4. Profitability ratios

2013 2014 2015

Net income 2,359,190 2,291,362 2,972,183

Sales 34,212,000 37,699,500 43,459,500

Result 6.90% 6.08% 6.84%

2013 2014 2015

Operating Profit 6,780,000 7,230,000 8,308,088

Sales 34,212,000 37,699,500 43,459,500

Result 19.82% 19.18% 19.12%

2013 2014 2015

Net income 2,359,190 2,291,362 2,972,183

Total owners' equity 9,150,000 10,783,650 12,250,491

Result 25.78% 21.25% 24.26%

Inventory Turnover = COGS/Inventory

Days' Inventory = 365/Inventory Turnover

Fixed Assets Turnover = Sales/net Fixed Assets

Total Assets Turnover = Sales/Total Assets

Profit Margin / Net Profit ratio = Net income / Sales

Operating Margin ratio = Operating Profit/Sales

Return on Equity = Net income/total owners' equity

Receivables Turnover Ratio = Sales/Accounts Receivable

Days Receivable = 365/Receivable turnover

4 | P a g e

5

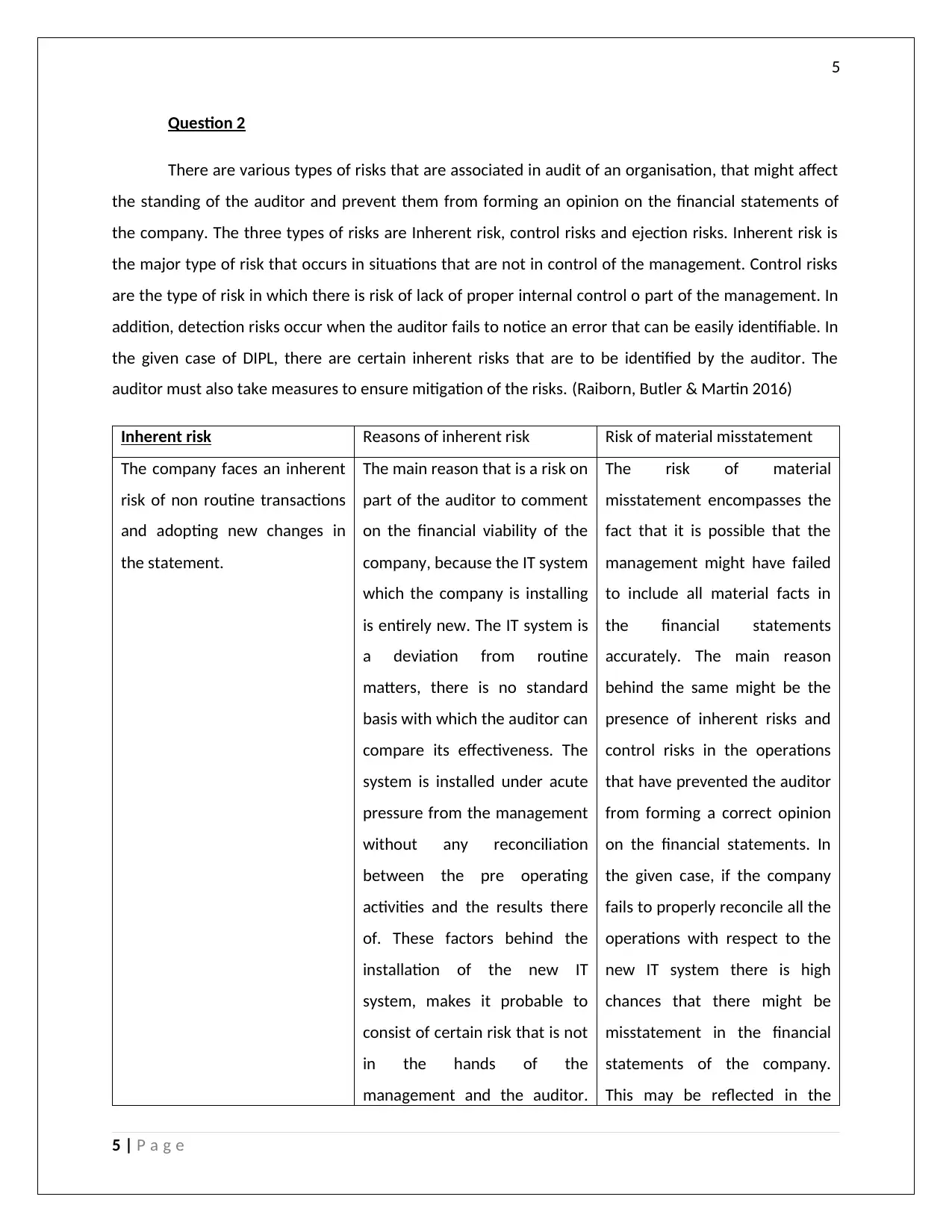

Question 2

There are various types of risks that are associated in audit of an organisation, that might affect

the standing of the auditor and prevent them from forming an opinion on the financial statements of

the company. The three types of risks are Inherent risk, control risks and ejection risks. Inherent risk is

the major type of risk that occurs in situations that are not in control of the management. Control risks

are the type of risk in which there is risk of lack of proper internal control o part of the management. In

addition, detection risks occur when the auditor fails to notice an error that can be easily identifiable. In

the given case of DIPL, there are certain inherent risks that are to be identified by the auditor. The

auditor must also take measures to ensure mitigation of the risks. (Raiborn, Butler & Martin 2016)

Inherent risk Reasons of inherent risk Risk of material misstatement

The company faces an inherent

risk of non routine transactions

and adopting new changes in

the statement.

The main reason that is a risk on

part of the auditor to comment

on the financial viability of the

company, because the IT system

which the company is installing

is entirely new. The IT system is

a deviation from routine

matters, there is no standard

basis with which the auditor can

compare its effectiveness. The

system is installed under acute

pressure from the management

without any reconciliation

between the pre operating

activities and the results there

of. These factors behind the

installation of the new IT

system, makes it probable to

consist of certain risk that is not

in the hands of the

management and the auditor.

The risk of material

misstatement encompasses the

fact that it is possible that the

management might have failed

to include all material facts in

the financial statements

accurately. The main reason

behind the same might be the

presence of inherent risks and

control risks in the operations

that have prevented the auditor

from forming a correct opinion

on the financial statements. In

the given case, if the company

fails to properly reconcile all the

operations with respect to the

new IT system there is high

chances that there might be

misstatement in the financial

statements of the company.

This may be reflected in the

5 | P a g e

Question 2

There are various types of risks that are associated in audit of an organisation, that might affect

the standing of the auditor and prevent them from forming an opinion on the financial statements of

the company. The three types of risks are Inherent risk, control risks and ejection risks. Inherent risk is

the major type of risk that occurs in situations that are not in control of the management. Control risks

are the type of risk in which there is risk of lack of proper internal control o part of the management. In

addition, detection risks occur when the auditor fails to notice an error that can be easily identifiable. In

the given case of DIPL, there are certain inherent risks that are to be identified by the auditor. The

auditor must also take measures to ensure mitigation of the risks. (Raiborn, Butler & Martin 2016)

Inherent risk Reasons of inherent risk Risk of material misstatement

The company faces an inherent

risk of non routine transactions

and adopting new changes in

the statement.

The main reason that is a risk on

part of the auditor to comment

on the financial viability of the

company, because the IT system

which the company is installing

is entirely new. The IT system is

a deviation from routine

matters, there is no standard

basis with which the auditor can

compare its effectiveness. The

system is installed under acute

pressure from the management

without any reconciliation

between the pre operating

activities and the results there

of. These factors behind the

installation of the new IT

system, makes it probable to

consist of certain risk that is not

in the hands of the

management and the auditor.

The risk of material

misstatement encompasses the

fact that it is possible that the

management might have failed

to include all material facts in

the financial statements

accurately. The main reason

behind the same might be the

presence of inherent risks and

control risks in the operations

that have prevented the auditor

from forming a correct opinion

on the financial statements. In

the given case, if the company

fails to properly reconcile all the

operations with respect to the

new IT system there is high

chances that there might be

misstatement in the financial

statements of the company.

This may be reflected in the

5 | P a g e

6

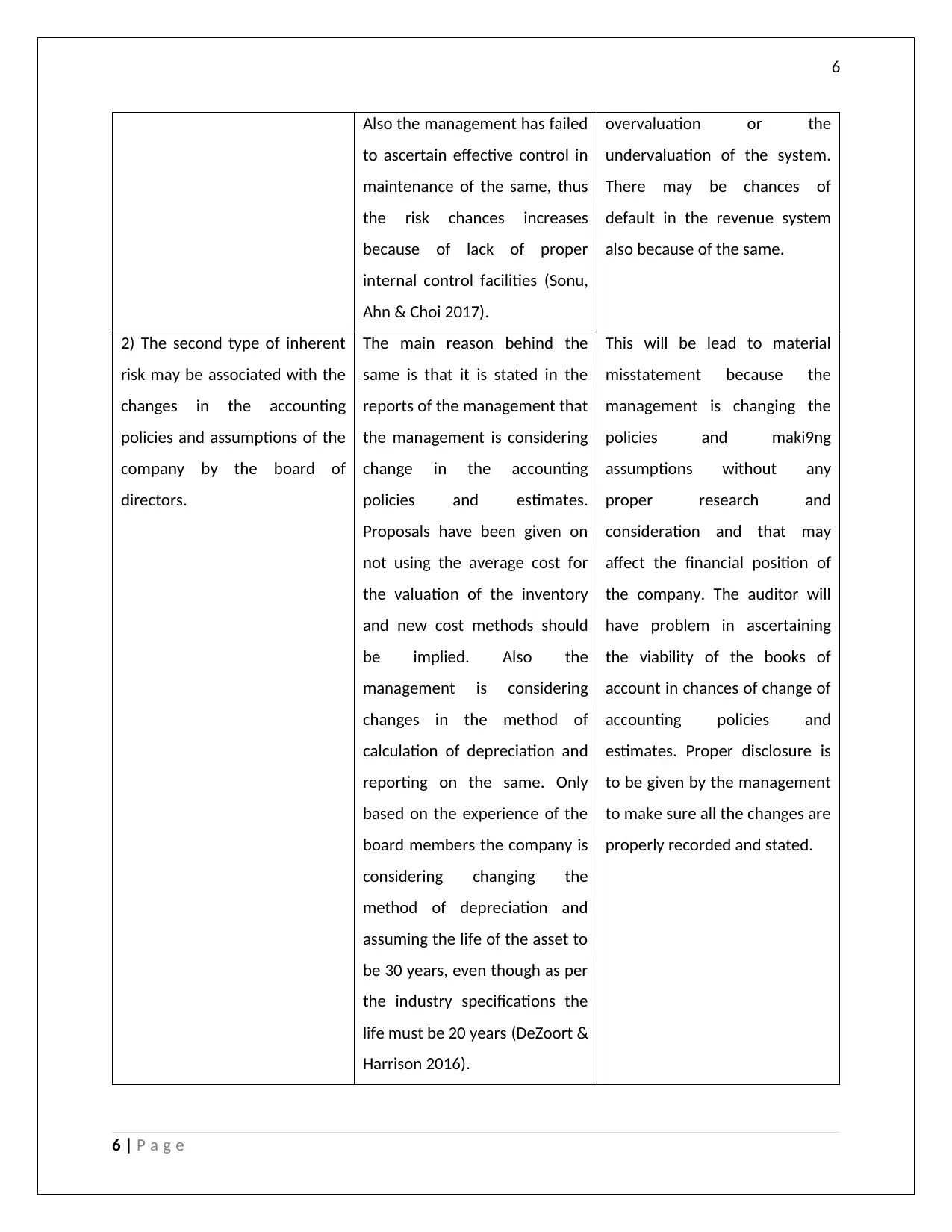

Also the management has failed

to ascertain effective control in

maintenance of the same, thus

the risk chances increases

because of lack of proper

internal control facilities (Sonu,

Ahn & Choi 2017).

overvaluation or the

undervaluation of the system.

There may be chances of

default in the revenue system

also because of the same.

2) The second type of inherent

risk may be associated with the

changes in the accounting

policies and assumptions of the

company by the board of

directors.

The main reason behind the

same is that it is stated in the

reports of the management that

the management is considering

change in the accounting

policies and estimates.

Proposals have been given on

not using the average cost for

the valuation of the inventory

and new cost methods should

be implied. Also the

management is considering

changes in the method of

calculation of depreciation and

reporting on the same. Only

based on the experience of the

board members the company is

considering changing the

method of depreciation and

assuming the life of the asset to

be 30 years, even though as per

the industry specifications the

life must be 20 years (DeZoort &

Harrison 2016).

This will be lead to material

misstatement because the

management is changing the

policies and maki9ng

assumptions without any

proper research and

consideration and that may

affect the financial position of

the company. The auditor will

have problem in ascertaining

the viability of the books of

account in chances of change of

accounting policies and

estimates. Proper disclosure is

to be given by the management

to make sure all the changes are

properly recorded and stated.

6 | P a g e

Also the management has failed

to ascertain effective control in

maintenance of the same, thus

the risk chances increases

because of lack of proper

internal control facilities (Sonu,

Ahn & Choi 2017).

overvaluation or the

undervaluation of the system.

There may be chances of

default in the revenue system

also because of the same.

2) The second type of inherent

risk may be associated with the

changes in the accounting

policies and assumptions of the

company by the board of

directors.

The main reason behind the

same is that it is stated in the

reports of the management that

the management is considering

change in the accounting

policies and estimates.

Proposals have been given on

not using the average cost for

the valuation of the inventory

and new cost methods should

be implied. Also the

management is considering

changes in the method of

calculation of depreciation and

reporting on the same. Only

based on the experience of the

board members the company is

considering changing the

method of depreciation and

assuming the life of the asset to

be 30 years, even though as per

the industry specifications the

life must be 20 years (DeZoort &

Harrison 2016).

This will be lead to material

misstatement because the

management is changing the

policies and maki9ng

assumptions without any

proper research and

consideration and that may

affect the financial position of

the company. The auditor will

have problem in ascertaining

the viability of the books of

account in chances of change of

accounting policies and

estimates. Proper disclosure is

to be given by the management

to make sure all the changes are

properly recorded and stated.

6 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

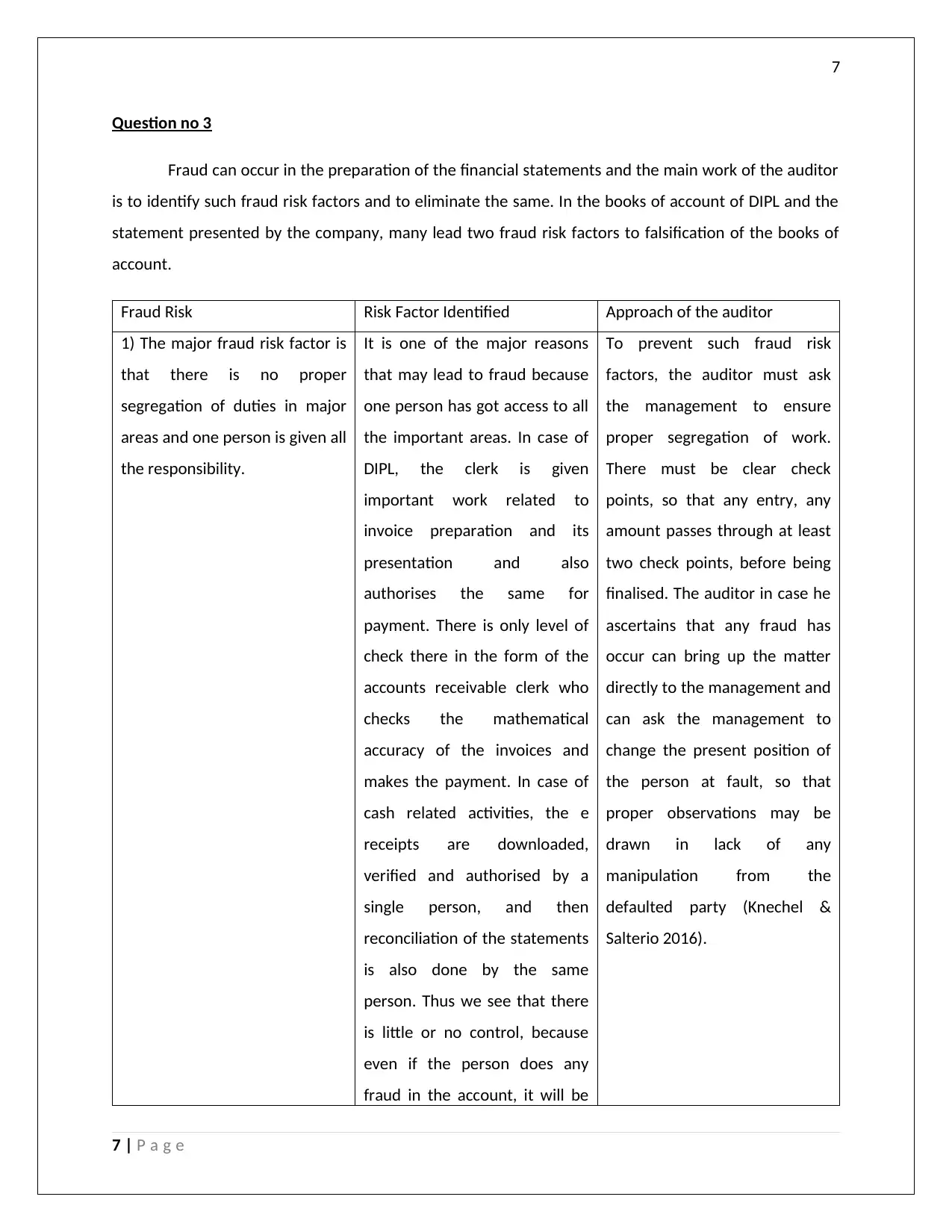

Question no 3

Fraud can occur in the preparation of the financial statements and the main work of the auditor

is to identify such fraud risk factors and to eliminate the same. In the books of account of DIPL and the

statement presented by the company, many lead two fraud risk factors to falsification of the books of

account.

Fraud Risk Risk Factor Identified Approach of the auditor

1) The major fraud risk factor is

that there is no proper

segregation of duties in major

areas and one person is given all

the responsibility.

It is one of the major reasons

that may lead to fraud because

one person has got access to all

the important areas. In case of

DIPL, the clerk is given

important work related to

invoice preparation and its

presentation and also

authorises the same for

payment. There is only level of

check there in the form of the

accounts receivable clerk who

checks the mathematical

accuracy of the invoices and

makes the payment. In case of

cash related activities, the e

receipts are downloaded,

verified and authorised by a

single person, and then

reconciliation of the statements

is also done by the same

person. Thus we see that there

is little or no control, because

even if the person does any

fraud in the account, it will be

To prevent such fraud risk

factors, the auditor must ask

the management to ensure

proper segregation of work.

There must be clear check

points, so that any entry, any

amount passes through at least

two check points, before being

finalised. The auditor in case he

ascertains that any fraud has

occur can bring up the matter

directly to the management and

can ask the management to

change the present position of

the person at fault, so that

proper observations may be

drawn in lack of any

manipulation from the

defaulted party (Knechel &

Salterio 2016).

7 | P a g e

Question no 3

Fraud can occur in the preparation of the financial statements and the main work of the auditor

is to identify such fraud risk factors and to eliminate the same. In the books of account of DIPL and the

statement presented by the company, many lead two fraud risk factors to falsification of the books of

account.

Fraud Risk Risk Factor Identified Approach of the auditor

1) The major fraud risk factor is

that there is no proper

segregation of duties in major

areas and one person is given all

the responsibility.

It is one of the major reasons

that may lead to fraud because

one person has got access to all

the important areas. In case of

DIPL, the clerk is given

important work related to

invoice preparation and its

presentation and also

authorises the same for

payment. There is only level of

check there in the form of the

accounts receivable clerk who

checks the mathematical

accuracy of the invoices and

makes the payment. In case of

cash related activities, the e

receipts are downloaded,

verified and authorised by a

single person, and then

reconciliation of the statements

is also done by the same

person. Thus we see that there

is little or no control, because

even if the person does any

fraud in the account, it will be

To prevent such fraud risk

factors, the auditor must ask

the management to ensure

proper segregation of work.

There must be clear check

points, so that any entry, any

amount passes through at least

two check points, before being

finalised. The auditor in case he

ascertains that any fraud has

occur can bring up the matter

directly to the management and

can ask the management to

change the present position of

the person at fault, so that

proper observations may be

drawn in lack of any

manipulation from the

defaulted party (Knechel &

Salterio 2016).

7 | P a g e

8

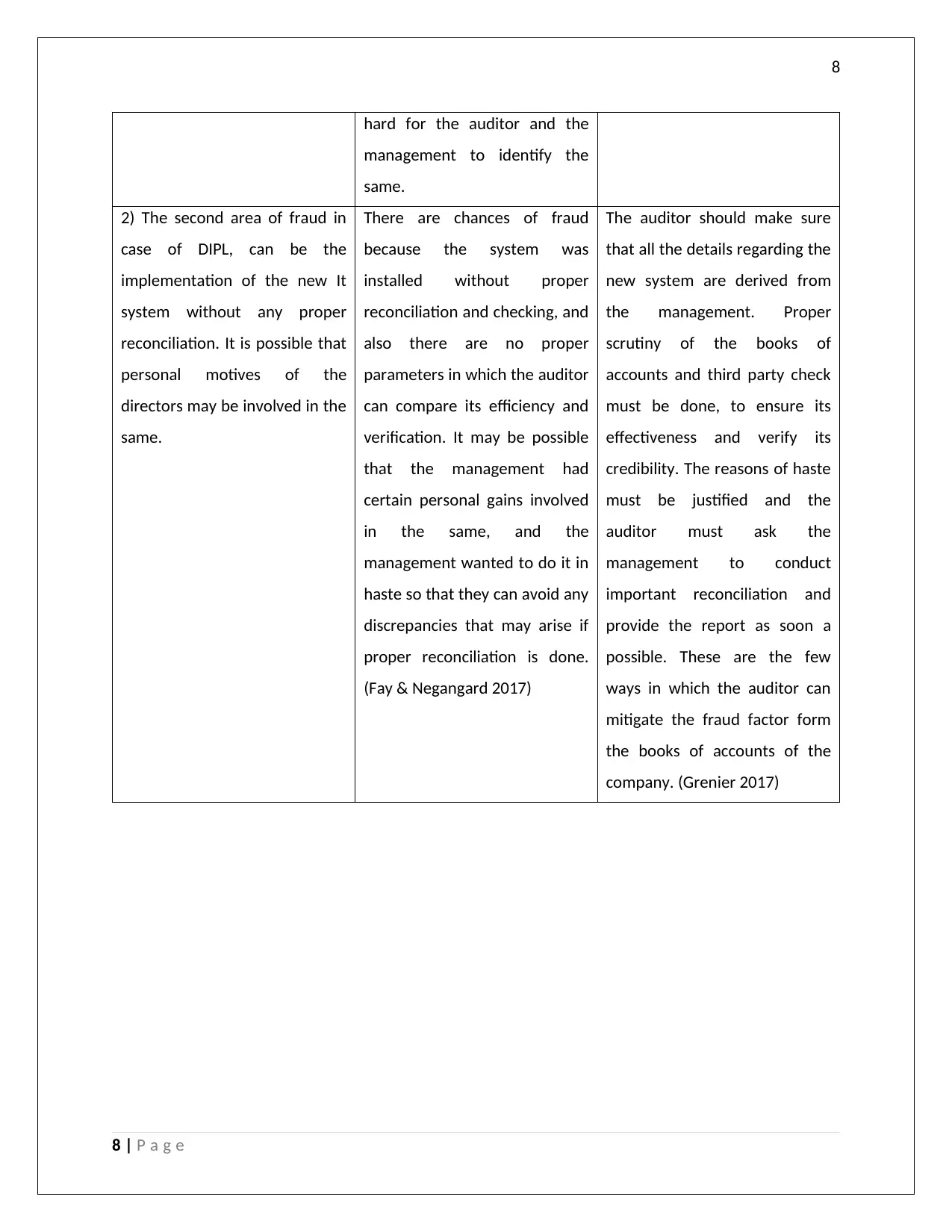

hard for the auditor and the

management to identify the

same.

2) The second area of fraud in

case of DIPL, can be the

implementation of the new It

system without any proper

reconciliation. It is possible that

personal motives of the

directors may be involved in the

same.

There are chances of fraud

because the system was

installed without proper

reconciliation and checking, and

also there are no proper

parameters in which the auditor

can compare its efficiency and

verification. It may be possible

that the management had

certain personal gains involved

in the same, and the

management wanted to do it in

haste so that they can avoid any

discrepancies that may arise if

proper reconciliation is done.

(Fay & Negangard 2017)

The auditor should make sure

that all the details regarding the

new system are derived from

the management. Proper

scrutiny of the books of

accounts and third party check

must be done, to ensure its

effectiveness and verify its

credibility. The reasons of haste

must be justified and the

auditor must ask the

management to conduct

important reconciliation and

provide the report as soon a

possible. These are the few

ways in which the auditor can

mitigate the fraud factor form

the books of accounts of the

company. (Grenier 2017)

8 | P a g e

hard for the auditor and the

management to identify the

same.

2) The second area of fraud in

case of DIPL, can be the

implementation of the new It

system without any proper

reconciliation. It is possible that

personal motives of the

directors may be involved in the

same.

There are chances of fraud

because the system was

installed without proper

reconciliation and checking, and

also there are no proper

parameters in which the auditor

can compare its efficiency and

verification. It may be possible

that the management had

certain personal gains involved

in the same, and the

management wanted to do it in

haste so that they can avoid any

discrepancies that may arise if

proper reconciliation is done.

(Fay & Negangard 2017)

The auditor should make sure

that all the details regarding the

new system are derived from

the management. Proper

scrutiny of the books of

accounts and third party check

must be done, to ensure its

effectiveness and verify its

credibility. The reasons of haste

must be justified and the

auditor must ask the

management to conduct

important reconciliation and

provide the report as soon a

possible. These are the few

ways in which the auditor can

mitigate the fraud factor form

the books of accounts of the

company. (Grenier 2017)

8 | P a g e

9

References

Bae, SH 2017, 'The Association Between Corporate Tax Avoidance And Audit Efforts: Evidence From

Korea', Journal of Applied Business Research, vol 33, no. 1, pp. 153-172.

DeZoort, FT & Harrison, PD 2016, 'Understanding Auditors sense of Responsibility for detecting fraud

within organization', Journal of Business Ethics, pp. 1-18.

Fay, R & Negangard, EM 2017, 'Manual journal entry testing : Data analytics and the risk of fraud',

Journal of Accounting Education, vol 38, pp. 37-49.

Grenier, J 2017, 'Encouraging Professional Skepticism in the Industry Specialization Era', Journal of

Business Ethics, vol 142, no. 2, pp. 241-256.

Knechel, WB & Salterio, SE 2016, Auditing:Assurance and Risk, 4th edn, Routledge, New York.

Raiborn, C, Butler, JB & Martin, K 2016, 'The internal audit function: A prerequisite for Good

Governance', Journal of Corporate Accounting and Finance, vol 28, no. 2, pp. 10-21.

Sonu, CH, Ahn, H & Choi, A 2017, 'Audit fee pressure and audit risk: evidence from the financial crisis of

2008', Asia-Pacific Journal of Accounting & Economics , vol 24, no. 1-2, pp. 127-144.

9 | P a g e

References

Bae, SH 2017, 'The Association Between Corporate Tax Avoidance And Audit Efforts: Evidence From

Korea', Journal of Applied Business Research, vol 33, no. 1, pp. 153-172.

DeZoort, FT & Harrison, PD 2016, 'Understanding Auditors sense of Responsibility for detecting fraud

within organization', Journal of Business Ethics, pp. 1-18.

Fay, R & Negangard, EM 2017, 'Manual journal entry testing : Data analytics and the risk of fraud',

Journal of Accounting Education, vol 38, pp. 37-49.

Grenier, J 2017, 'Encouraging Professional Skepticism in the Industry Specialization Era', Journal of

Business Ethics, vol 142, no. 2, pp. 241-256.

Knechel, WB & Salterio, SE 2016, Auditing:Assurance and Risk, 4th edn, Routledge, New York.

Raiborn, C, Butler, JB & Martin, K 2016, 'The internal audit function: A prerequisite for Good

Governance', Journal of Corporate Accounting and Finance, vol 28, no. 2, pp. 10-21.

Sonu, CH, Ahn, H & Choi, A 2017, 'Audit fee pressure and audit risk: evidence from the financial crisis of

2008', Asia-Pacific Journal of Accounting & Economics , vol 24, no. 1-2, pp. 127-144.

9 | P a g e

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.