TAXATION LAW: Analysis of Capital Gains, Fringe Benefits, and Tax

VerifiedAdded on 2020/03/07

|14

|2933

|162

Homework Assignment

AI Summary

This TAXATION LAW assignment addresses several key areas of income tax law. It begins with a detailed analysis of capital gains and losses, including the treatment of personal-use assets and collectible losses. The assignment then delves into the determination of Fringe Benefit Tax, specifically focusing on loan fringe benefits and the application of statutory interest rates. The third section examines the tax implications of rental property co-ownership, clarifying the treatment of losses and the impact of partnership agreements. The assignment also explores the concept of tax avoidance, referencing the IRC v Duke of Westminster case and its implications. Finally, it investigates whether the sale of timber by a taxpayer constitutes assessable income under the primary producer provisions of the Income Tax Assessment Act 1936, considering the relevant taxation rulings and legislation. The assignment provides a comprehensive overview of each topic, citing relevant legislation and case law to support its conclusions.

Running head: TAXATION LAW

Taxation

Name of the Student

Name of the University

Authors Note

Course ID

Taxation

Name of the Student

Name of the University

Authors Note

Course ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1TAXATION LAW

Table of Contents

Answer to question 1:.................................................................................................................2

Answer to question 2:.................................................................................................................3

Answer to question 3:.................................................................................................................5

Answer to question 4:.................................................................................................................7

Answer to question 5:.................................................................................................................8

Reference List:.........................................................................................................................11

Table of Contents

Answer to question 1:.................................................................................................................2

Answer to question 2:.................................................................................................................3

Answer to question 3:.................................................................................................................5

Answer to question 4:.................................................................................................................7

Answer to question 5:.................................................................................................................8

Reference List:.........................................................................................................................11

2TAXATION LAW

Answer to question 1:

Issues:

The present issues is concerned with the determination of net capital gains or losses

derived by the taxpayer under the ITAA 1997.

Legislation:

a. Section 108-20 of the Income Tax Assessment Act 1997

b. Section 108-10 of the Income Tax Assessment Act 1997

Computation of net capital loss for the year

Particulars Amount ($)

Loss on sale of Antique Chair $2,000

Loss on sale of Painting $8,000

Less: Gain on sale of Antique Vase $1,000

Total Collectable loss to be carried forward $9,000

Asset Description

Cost

Base

Capital

Proceeds

Capital

gains

Capital

loss

Antique Vase $2,000 $3,000 $1,000

Antique Chair $3,000 $1,000 $2,000

Painting $9,000 $1,000 $8,000

Home Sound System $12,000 $11,000 $1,000

Shares in listed company $5,000 $20,000 $15,000

Computation of Net capital gains for the year

Particulars Amount ($)

Gains on sale of shares $15,000

Applications:

a. As defined under section 108-20 of the Income Tax Assessment Act 1997, no loss

can be allowed for offset from the disposal of assets that are for personal use. Eric

Answer to question 1:

Issues:

The present issues is concerned with the determination of net capital gains or losses

derived by the taxpayer under the ITAA 1997.

Legislation:

a. Section 108-20 of the Income Tax Assessment Act 1997

b. Section 108-10 of the Income Tax Assessment Act 1997

Computation of net capital loss for the year

Particulars Amount ($)

Loss on sale of Antique Chair $2,000

Loss on sale of Painting $8,000

Less: Gain on sale of Antique Vase $1,000

Total Collectable loss to be carried forward $9,000

Asset Description

Cost

Base

Capital

Proceeds

Capital

gains

Capital

loss

Antique Vase $2,000 $3,000 $1,000

Antique Chair $3,000 $1,000 $2,000

Painting $9,000 $1,000 $8,000

Home Sound System $12,000 $11,000 $1,000

Shares in listed company $5,000 $20,000 $15,000

Computation of Net capital gains for the year

Particulars Amount ($)

Gains on sale of shares $15,000

Applications:

a. As defined under section 108-20 of the Income Tax Assessment Act 1997, no loss

can be allowed for offset from the disposal of assets that are for personal use. Eric

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3TAXATION LAW

suffered a loss of $1,000 from the disposal of home sound system and it cannot be

allowed for offset since the asset was personal use in nature.

b. As stated under section 108-10 of the Income Tax Assessment Act 1997, collectible

losses are not allowed to be offset against the ordinary gains from the sale of shares.

The same can be only offset against the collectible gains under section 108-10 of the

Income Tax Assessment Act 1997 (Barkoczy 2016).

c. As Eric has generated gains from the disposal of ordinary assets and there are no

present year ordinary, capital or any form of applicable discounts therefore the net

capital gains for Eric stands $15,000.

Conclusions:

It can be concluded that no loss can be allowed for offset from the disposal of assets

that are for personal use. Therefore, Eric had derived gains from the disposal of ordinary

assets.

Answer to question 2:

Issue:

The following is concerned with the determination of Fringe Benefit Tax of the

taxpayer under the Fringe Benefit Act 1986.

Legislations:

a. Fringe Benefit Tax Assessment Act 1986

b. taxation rulings of TR 93/6

Applications:

Computation of Fringe Benefit Tax

suffered a loss of $1,000 from the disposal of home sound system and it cannot be

allowed for offset since the asset was personal use in nature.

b. As stated under section 108-10 of the Income Tax Assessment Act 1997, collectible

losses are not allowed to be offset against the ordinary gains from the sale of shares.

The same can be only offset against the collectible gains under section 108-10 of the

Income Tax Assessment Act 1997 (Barkoczy 2016).

c. As Eric has generated gains from the disposal of ordinary assets and there are no

present year ordinary, capital or any form of applicable discounts therefore the net

capital gains for Eric stands $15,000.

Conclusions:

It can be concluded that no loss can be allowed for offset from the disposal of assets

that are for personal use. Therefore, Eric had derived gains from the disposal of ordinary

assets.

Answer to question 2:

Issue:

The following is concerned with the determination of Fringe Benefit Tax of the

taxpayer under the Fringe Benefit Act 1986.

Legislations:

a. Fringe Benefit Tax Assessment Act 1986

b. taxation rulings of TR 93/6

Applications:

Computation of Fringe Benefit Tax

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4TAXATION LAW

Taxable value of the loan fringe benefit

In the books of Brian for the year ended 2016/17

Computation under statutory interest rate and actual Interest rate

Statutory rate Actual rate

Particulars Amount ($)

Amount

($)

Amount of Loan 1000000 1000000

FBT Amount 40% business use 400000 400000

Statutory Interest rate @ 5.65% 2825.00 500.00

(Amount of loan x Statutory interest rate) - (Amount of loan

x Actual interest rate) / 12 x 60% business use

Taxable value of the loan fringe benefit 2325

FBT on end of the loan on payment of interest at the end of loan

Statutory rate Actual rate

Particulars Amount ($)

Amount

($)

Amount of Loan 1000000 1000000

FBT Amount 40% business use 400000 400000

Statutory Interest rate @ 5.65% 33900.00 6000.00

(Amount of loan x Statutory interest rate) - (Amount of loan

x Actual interest rate) x 60% business use

Taxable value of the loan fringe benefit 27900

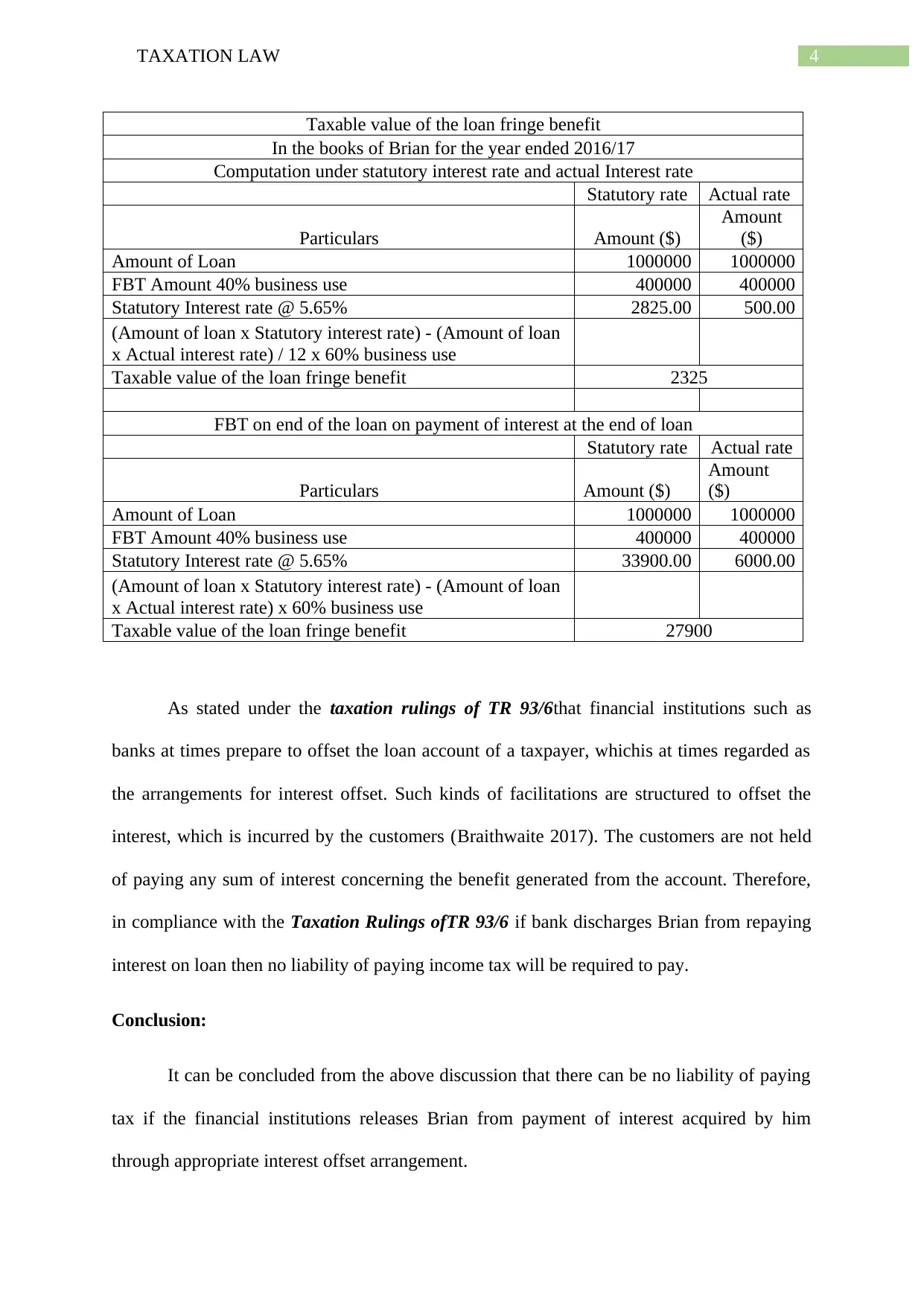

As stated under the taxation rulings of TR 93/6that financial institutions such as

banks at times prepare to offset the loan account of a taxpayer, whichis at times regarded as

the arrangements for interest offset. Such kinds of facilitations are structured to offset the

interest, which is incurred by the customers (Braithwaite 2017). The customers are not held

of paying any sum of interest concerning the benefit generated from the account. Therefore,

in compliance with the Taxation Rulings ofTR 93/6 if bank discharges Brian from repaying

interest on loan then no liability of paying income tax will be required to pay.

Conclusion:

It can be concluded from the above discussion that there can be no liability of paying

tax if the financial institutions releases Brian from payment of interest acquired by him

through appropriate interest offset arrangement.

Taxable value of the loan fringe benefit

In the books of Brian for the year ended 2016/17

Computation under statutory interest rate and actual Interest rate

Statutory rate Actual rate

Particulars Amount ($)

Amount

($)

Amount of Loan 1000000 1000000

FBT Amount 40% business use 400000 400000

Statutory Interest rate @ 5.65% 2825.00 500.00

(Amount of loan x Statutory interest rate) - (Amount of loan

x Actual interest rate) / 12 x 60% business use

Taxable value of the loan fringe benefit 2325

FBT on end of the loan on payment of interest at the end of loan

Statutory rate Actual rate

Particulars Amount ($)

Amount

($)

Amount of Loan 1000000 1000000

FBT Amount 40% business use 400000 400000

Statutory Interest rate @ 5.65% 33900.00 6000.00

(Amount of loan x Statutory interest rate) - (Amount of loan

x Actual interest rate) x 60% business use

Taxable value of the loan fringe benefit 27900

As stated under the taxation rulings of TR 93/6that financial institutions such as

banks at times prepare to offset the loan account of a taxpayer, whichis at times regarded as

the arrangements for interest offset. Such kinds of facilitations are structured to offset the

interest, which is incurred by the customers (Braithwaite 2017). The customers are not held

of paying any sum of interest concerning the benefit generated from the account. Therefore,

in compliance with the Taxation Rulings ofTR 93/6 if bank discharges Brian from repaying

interest on loan then no liability of paying income tax will be required to pay.

Conclusion:

It can be concluded from the above discussion that there can be no liability of paying

tax if the financial institutions releases Brian from payment of interest acquired by him

through appropriate interest offset arrangement.

5TAXATION LAW

Answer to question 3:

Issue:

The present scenario of Jack and Jill is based on the determination of taxable position

of the loss incurred from the rental property.

Legislation:

a. Taxation rulings of TR 93/32

b. F.C. of T. v McDonald (1987) 18 ATR 957

c. Section 51 of the ITAA 1997

Application:

As evident both Jack and Jill entered into the agreement of purchasing a rental

property as joint tenant. The agreement contained that Jack will be entitled to 10% of the

profit from the property and Jill shall be getting 90% of the profit from the rental property.

The agreement further stated that Jack shall be entitled to bear 100% of the loss incurred from

the rental property.

As defined under the Taxation rulings of TR 93/32, Co-owners of rental property is

regarded as partnership for the purpose of income tax however, it will not be regarded as

partnership under the general law except the ownership accounts for carrying on or of a

business. From the given scenario of Jack and his wife Jill it can be ascertained that co-

ownership of rental property between them constitute partnership for the purpose of income

tax however not a partnership under the General Law (Caoet al. 2015). The rulings lays down

that the taxable position of the co-owners does not accounts for carrying on of a business.

Answer to question 3:

Issue:

The present scenario of Jack and Jill is based on the determination of taxable position

of the loss incurred from the rental property.

Legislation:

a. Taxation rulings of TR 93/32

b. F.C. of T. v McDonald (1987) 18 ATR 957

c. Section 51 of the ITAA 1997

Application:

As evident both Jack and Jill entered into the agreement of purchasing a rental

property as joint tenant. The agreement contained that Jack will be entitled to 10% of the

profit from the property and Jill shall be getting 90% of the profit from the rental property.

The agreement further stated that Jack shall be entitled to bear 100% of the loss incurred from

the rental property.

As defined under the Taxation rulings of TR 93/32, Co-owners of rental property is

regarded as partnership for the purpose of income tax however, it will not be regarded as

partnership under the general law except the ownership accounts for carrying on or of a

business. From the given scenario of Jack and his wife Jill it can be ascertained that co-

ownership of rental property between them constitute partnership for the purpose of income

tax however not a partnership under the General Law (Caoet al. 2015). The rulings lays down

that the taxable position of the co-owners does not accounts for carrying on of a business.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6TAXATION LAW

As defined under the taxation rulings TR 92/32 that the co-owners of the rental

property Jack and his wife Jill are not considered as the partners under the general law and

the partnership agreement among them either in oral or writing does bear any impact on the

share of income or loss arising out of the property. Hence, the co-owners of the rental

property Jack and Jill holds the property as “joint tenants or tenants in common”

(Saad2014). Such rental becomes the categorization of the co-owners interest.

Citing the reference of F.C. of T. v McDonald (1987) 18 ATR 957 where the

taxpayers and his spouse owned lawfully and constructively two units as the joint tenants

(Woellner et al. 2016). The agreement among them stated that the net profit from rental

property would be dispersed 25 percent to Mr McDonald and 75 percent to Mrs McDonald

with the entire amount of loss would be shouldered by Mr McDonald. This led to questions

that whether the operational loss on the rental property was entirely acquired by the taxpayer

or each of the taxpayer and his wife acquired half of the loss. There was no such provision

concerning the deductibility of loss. The judgement stated that there was no form of

partnership under general law and a noteworthy relationship between the husband and wife

was that of the co-ownership (Robin 2017). As the parties were jointly owners under the

terms of law and justice the loss suffered on letting the propertiesmust be shared equally with

consequences that the respondents fall under the obligation of deducting half of the loss

suffered.

As evident in the scenario of Jack and Jill, it can be stated that the loss must be

equally allocated for income tax purpose and does not allow deduction by virtue of

agreement. As a fact, Jack was indulged in two noteworthy detriments. Initially he provided

large part of his earnings entitlement and additionally he indemnified his wife Jill against all

sort of loss from the investment. The supposition of distribution of loss was intentionally

made by Jack and purely formed a domestic preparation where he pursued to advance the

As defined under the taxation rulings TR 92/32 that the co-owners of the rental

property Jack and his wife Jill are not considered as the partners under the general law and

the partnership agreement among them either in oral or writing does bear any impact on the

share of income or loss arising out of the property. Hence, the co-owners of the rental

property Jack and Jill holds the property as “joint tenants or tenants in common”

(Saad2014). Such rental becomes the categorization of the co-owners interest.

Citing the reference of F.C. of T. v McDonald (1987) 18 ATR 957 where the

taxpayers and his spouse owned lawfully and constructively two units as the joint tenants

(Woellner et al. 2016). The agreement among them stated that the net profit from rental

property would be dispersed 25 percent to Mr McDonald and 75 percent to Mrs McDonald

with the entire amount of loss would be shouldered by Mr McDonald. This led to questions

that whether the operational loss on the rental property was entirely acquired by the taxpayer

or each of the taxpayer and his wife acquired half of the loss. There was no such provision

concerning the deductibility of loss. The judgement stated that there was no form of

partnership under general law and a noteworthy relationship between the husband and wife

was that of the co-ownership (Robin 2017). As the parties were jointly owners under the

terms of law and justice the loss suffered on letting the propertiesmust be shared equally with

consequences that the respondents fall under the obligation of deducting half of the loss

suffered.

As evident in the scenario of Jack and Jill, it can be stated that the loss must be

equally allocated for income tax purpose and does not allow deduction by virtue of

agreement. As a fact, Jack was indulged in two noteworthy detriments. Initially he provided

large part of his earnings entitlement and additionally he indemnified his wife Jill against all

sort of loss from the investment. The supposition of distribution of loss was intentionally

made by Jack and purely formed a domestic preparation where he pursued to advance the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION LAW

finance of his wife as section 51 does not allows for deductions merely virtue of the

agreement.

Conversely, if Jack and his wife decides to sell the property, the cost base and reduced

cost base of the rental property should be accounted in the amount, which paid by them

together. Being the co-owners of the property, the capital gains or loss will be accounted

based on the ownership interest of the property.

Conclusion:

To conclude with it is ascertained that there was no form of partnership under general

law and the losses must be shared equally with obligation of deducting half of the loss

suffered by Jack and Jill.

Answer to question 4:

IRC v Duke of Westminster [1936] AC 1is regularly quoted on the event of tax

avoidance (Blakelock and King 2017). The case laid down the principles that every

individual is allowed to order his affairs with the objective that the tax assigning is made in

the stated Act, is less than it would be. Despite the fact that the ruling stood as a matter of

attraction for others in seeking tax avoidance by lawfully creating a complex structures, it has

been weakened by the succeeding events where courts have observed on the overall impacts.

As an example the court in the later part undertook more restrictive approach under the

WT Ramsay v. IRC principle. If a transaction comprises of pre-arranged false phases that

does not serve any sort of business purpose other than avoiding tax, the correct approach was

to levy tax to the consequence of the business wholly (Vann 2016).

In the current age this principles in Australia lays down that if a person attains success

in ordering them with the purpose of acquiring this results then the Commissioners of Inland

Revenue or the fellow taxpayers in their ingenuity cannot be compelled to pay any additional

finance of his wife as section 51 does not allows for deductions merely virtue of the

agreement.

Conversely, if Jack and his wife decides to sell the property, the cost base and reduced

cost base of the rental property should be accounted in the amount, which paid by them

together. Being the co-owners of the property, the capital gains or loss will be accounted

based on the ownership interest of the property.

Conclusion:

To conclude with it is ascertained that there was no form of partnership under general

law and the losses must be shared equally with obligation of deducting half of the loss

suffered by Jack and Jill.

Answer to question 4:

IRC v Duke of Westminster [1936] AC 1is regularly quoted on the event of tax

avoidance (Blakelock and King 2017). The case laid down the principles that every

individual is allowed to order his affairs with the objective that the tax assigning is made in

the stated Act, is less than it would be. Despite the fact that the ruling stood as a matter of

attraction for others in seeking tax avoidance by lawfully creating a complex structures, it has

been weakened by the succeeding events where courts have observed on the overall impacts.

As an example the court in the later part undertook more restrictive approach under the

WT Ramsay v. IRC principle. If a transaction comprises of pre-arranged false phases that

does not serve any sort of business purpose other than avoiding tax, the correct approach was

to levy tax to the consequence of the business wholly (Vann 2016).

In the current age this principles in Australia lays down that if a person attains success

in ordering them with the purpose of acquiring this results then the Commissioners of Inland

Revenue or the fellow taxpayers in their ingenuity cannot be compelled to pay any additional

8TAXATION LAW

amount of tax. It is understood that it allows the persons and corporations to structure their

monetary agreements for the purpose of lowering the tax unless the structure is within the

structure of act (Anderson, Dickfos and Brown 2016).

Answer to question 5:

Issues:

The present issue ascertains whether or not sale of timber by the taxpayer constitutes

assessable income under primary producer under subsection 6 (1) of the Income Tax

Assessment Act 1936.

Legislations:

a. Subsection 6 (1) of the Income Tax Assessment Act 1936

b. Taxation rulings of TR 95/6

c. Subsection 36(1)

d. section 26 (f)

e. McCauley v. The Federal Commissioner of Taxation (1944) 69 CLR 235

Application:

In the existing situation, it is observed that Bill is owner a large piece of land with

large number of pine trees. In the initial stages, Bill intended to use the land for grazing sheep

and wanted to clear the land. Bill founds a logging company, which was willing to pay

$1,000 for every 100 meters of timber that the company will take from his land. As defined

under the taxation rulings of TR 95/6 that extent to which the receipts is generated from the

sale of time represents taxable income whether or not the assesse was engaged in the

activities of forestry industry (Fry 2017). The rulings is particularly implemented on those

people that are engaged in the activities of forest operations and on an individual that are not

amount of tax. It is understood that it allows the persons and corporations to structure their

monetary agreements for the purpose of lowering the tax unless the structure is within the

structure of act (Anderson, Dickfos and Brown 2016).

Answer to question 5:

Issues:

The present issue ascertains whether or not sale of timber by the taxpayer constitutes

assessable income under primary producer under subsection 6 (1) of the Income Tax

Assessment Act 1936.

Legislations:

a. Subsection 6 (1) of the Income Tax Assessment Act 1936

b. Taxation rulings of TR 95/6

c. Subsection 36(1)

d. section 26 (f)

e. McCauley v. The Federal Commissioner of Taxation (1944) 69 CLR 235

Application:

In the existing situation, it is observed that Bill is owner a large piece of land with

large number of pine trees. In the initial stages, Bill intended to use the land for grazing sheep

and wanted to clear the land. Bill founds a logging company, which was willing to pay

$1,000 for every 100 meters of timber that the company will take from his land. As defined

under the taxation rulings of TR 95/6 that extent to which the receipts is generated from the

sale of time represents taxable income whether or not the assesse was engaged in the

activities of forestry industry (Fry 2017). The rulings is particularly implemented on those

people that are engaged in the activities of forest operations and on an individual that are not

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9TAXATION LAW

engaged in the forest operations but sells the timber. According to the subsection 6 (1) of the

Income Tax Assessment Act 1936, a taxpayer who is engaged in the functions of forest

operations is concerned as the primary producer for income tax purpose if the forest

operations becomes the part of carrying on of a business (Slemrod and Bakija 2017).

As evident from the present scenario that Bill be considered as the primary producer

in compliance with the subsection 6 (1) of the Income Tax Assessment Act 1936 primary

production because he engaged in the operations of felling of trees in a plantation which was

owned by him (Sikka 2017). Furthermore, the forest functions comprised of felling of trees in

a plantation or forest in spite of the fact that taxpayer was not engaged in the activities of

plantation or tended the trees.

As Bill was the owner of land and did not planted the pine trees however the total

amount of receipts derived by him from the disposal of felled timber forms the part of

assessable income in the year such income was derived by him from the sale of felled timber

(McCluskey and Franzsen 2017). The selling of standing timber where the taxpayer sells the

trees that have not been planted by him and tended with the objective of sale constitute

assessable income. As defined under subsection 36(1), although the sales formed the part of

assets of a business the value of trees will be regarded as the taxable income of the taxpayer.

Conversely, if Bill were simply paid a lump sum amount of $50,000 by permitting the

logging company with the right of removing the needed amount of timber from his land such

receipt of sum would be regarded as “Royalties”. As stated under section 26 (f) receipt of

royalties by the taxpayer by granting the right of cutting the trees for timber on the land held

by the taxpayer will be regarded as the taxable income in the income year in which the trees

were cut for timber. Citing the reference of McCauley v. The Federal Commissioner of

Taxation (1944) 69 CLR 235payment received by the grantor or the right given to cut trees

engaged in the forest operations but sells the timber. According to the subsection 6 (1) of the

Income Tax Assessment Act 1936, a taxpayer who is engaged in the functions of forest

operations is concerned as the primary producer for income tax purpose if the forest

operations becomes the part of carrying on of a business (Slemrod and Bakija 2017).

As evident from the present scenario that Bill be considered as the primary producer

in compliance with the subsection 6 (1) of the Income Tax Assessment Act 1936 primary

production because he engaged in the operations of felling of trees in a plantation which was

owned by him (Sikka 2017). Furthermore, the forest functions comprised of felling of trees in

a plantation or forest in spite of the fact that taxpayer was not engaged in the activities of

plantation or tended the trees.

As Bill was the owner of land and did not planted the pine trees however the total

amount of receipts derived by him from the disposal of felled timber forms the part of

assessable income in the year such income was derived by him from the sale of felled timber

(McCluskey and Franzsen 2017). The selling of standing timber where the taxpayer sells the

trees that have not been planted by him and tended with the objective of sale constitute

assessable income. As defined under subsection 36(1), although the sales formed the part of

assets of a business the value of trees will be regarded as the taxable income of the taxpayer.

Conversely, if Bill were simply paid a lump sum amount of $50,000 by permitting the

logging company with the right of removing the needed amount of timber from his land such

receipt of sum would be regarded as “Royalties”. As stated under section 26 (f) receipt of

royalties by the taxpayer by granting the right of cutting the trees for timber on the land held

by the taxpayer will be regarded as the taxable income in the income year in which the trees

were cut for timber. Citing the reference of McCauley v. The Federal Commissioner of

Taxation (1944) 69 CLR 235payment received by the grantor or the right given to cut trees

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10TAXATION LAW

for timber is ascertained on the amount of timber removed given under the right to do

so(Hegemannet al. 2017). Under section 26 (f), the sum received by Bill as royalties will be

regarded as taxable income.

Conclusion:

It can be concluded in compliance with subsection 36(1)that disposal of felled timber

forms the part of assessable income of the taxpayer and will be held liable for tax from the

receipt of sum on sale of timber.

for timber is ascertained on the amount of timber removed given under the right to do

so(Hegemannet al. 2017). Under section 26 (f), the sum received by Bill as royalties will be

regarded as taxable income.

Conclusion:

It can be concluded in compliance with subsection 36(1)that disposal of felled timber

forms the part of assessable income of the taxpayer and will be held liable for tax from the

receipt of sum on sale of timber.

11TAXATION LAW

Reference List:

Anderson, C., Dickfos, J. and Brown, C., 2016. The Australian Taxation Office-what role

does it play in anti-phoenix activity?. INSOLVENCY LAW JOURNAL, 24(2), pp.127-140.

Barkoczy, S., 2016. Foundations of Taxation Law 2016. OUP Catalogue.

Blakelock, S. and King, P., 2017. Taxation law: The advance of ATO data matching. Proctor,

The, 37(6), p.18.

Braithwaite, V. ed., 2017. Taxing democracy: Understanding tax avoidance and evasion.

Routledge.

Cao, L., Hosking, A., Kouparitsas, M., Mullaly, D., Rimmer, X., Shi, Q., Stark, W. and

Wende, S., 2015. Understanding the economy-wide efficiency and incidence of major

Australian taxes. Treasury WP, 1.

Fry, M., 2017. Australian taxation of offshore hubs: an examination of the law on the ability

of Australia to tax economic activity in offshore hubs and the position of the Australian

Taxation Office. The APPEA Journal, 57(1), pp.49-63.

Hegemann, A., Kunoth, A., Rupp, K. and Sureth-Sloane, C., 2017. Hold or sell? How capital

gains taxation affects holding decisions. Review of Managerial Science, 11(3), pp.571-603.

McCluskey, W.J. and Franzsen, R.C., 2017. Land value taxation: An applied analysis.

Routledge.

ROBIN, H., 2017. AUSTRALIAN TAXATION LAW 2017. OXFORD University Press.

Saad, N., 2014. Tax knowledge, tax complexity and tax compliance: Taxpayers’

view. Procedia-Social and Behavioral Sciences, 109, pp.1069-1075.

Reference List:

Anderson, C., Dickfos, J. and Brown, C., 2016. The Australian Taxation Office-what role

does it play in anti-phoenix activity?. INSOLVENCY LAW JOURNAL, 24(2), pp.127-140.

Barkoczy, S., 2016. Foundations of Taxation Law 2016. OUP Catalogue.

Blakelock, S. and King, P., 2017. Taxation law: The advance of ATO data matching. Proctor,

The, 37(6), p.18.

Braithwaite, V. ed., 2017. Taxing democracy: Understanding tax avoidance and evasion.

Routledge.

Cao, L., Hosking, A., Kouparitsas, M., Mullaly, D., Rimmer, X., Shi, Q., Stark, W. and

Wende, S., 2015. Understanding the economy-wide efficiency and incidence of major

Australian taxes. Treasury WP, 1.

Fry, M., 2017. Australian taxation of offshore hubs: an examination of the law on the ability

of Australia to tax economic activity in offshore hubs and the position of the Australian

Taxation Office. The APPEA Journal, 57(1), pp.49-63.

Hegemann, A., Kunoth, A., Rupp, K. and Sureth-Sloane, C., 2017. Hold or sell? How capital

gains taxation affects holding decisions. Review of Managerial Science, 11(3), pp.571-603.

McCluskey, W.J. and Franzsen, R.C., 2017. Land value taxation: An applied analysis.

Routledge.

ROBIN, H., 2017. AUSTRALIAN TAXATION LAW 2017. OXFORD University Press.

Saad, N., 2014. Tax knowledge, tax complexity and tax compliance: Taxpayers’

view. Procedia-Social and Behavioral Sciences, 109, pp.1069-1075.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.