HI6028 Taxation, Theory, Practice & Law: Detailed Case Study Analysis

VerifiedAdded on 2020/01/07

|9

|2665

|139

Report

AI Summary

This report delves into the intricacies of Australian taxation law, focusing on key aspects such as residence, source of income, and ordinary income. It begins by defining taxation law and its significance in assessing taxable income, emphasizing the obligation of individuals to pay taxes in a timely manner. The report then presents two case studies. Case Study 1 examines the concept of Australian permanent residency, distinguishing between ordinary and non-ordinary residents and their respective tax obligations, including considerations for individuals working abroad and the implications of foreign-sourced income. Case Study 2 analyzes several court cases related to capital gains and ordinary income, providing insights into how profits from the sale of assets are classified for tax purposes. The cases discussed cover topics like the realization of capital assets, the treatment of land sales by mining companies and property developers, and the application of specific sections of the Income Tax Assessment Act. The report provides an overview of the tax implications for individuals and businesses. The report also mentions the impact of the Medicare levy and temporary budget repair levy on income tax calculations.

HI6028 Taxation, Theory,

Practice & Law

Practice & Law

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

CASE STUDY 1 – RESIDENCE AND SOURCE.........................................................................3

CASE STUDY 2 – ORDINARY INCOME....................................................................................6

Californian Copper Syndicate Ltd v Harris (Surveyor of taxes) (1904) 5 TC 159.....................6

Scottish Australian Mining Co Ltd v FC of T (1950) 81 CLR 188............................................6

FC of T v Whitfords Beach Pty Ltd (1982) 150 CLR.................................................................6

Statham & Anor v FC of T 89 ATC 4070...................................................................................7

Casimaty v FC of T 97 ATC 5135..............................................................................................7

Moana Sand Pty Ltd v FC of T 88 ATC 4897............................................................................7

Crow v FC of T 88 ATC 4620....................................................................................................8

McCurry & Anor v FC of T 98 ATC 4487.................................................................................8

CONCLUSION................................................................................................................................8

REFERENCES................................................................................................................................9

INTRODUCTION...........................................................................................................................3

CASE STUDY 1 – RESIDENCE AND SOURCE.........................................................................3

CASE STUDY 2 – ORDINARY INCOME....................................................................................6

Californian Copper Syndicate Ltd v Harris (Surveyor of taxes) (1904) 5 TC 159.....................6

Scottish Australian Mining Co Ltd v FC of T (1950) 81 CLR 188............................................6

FC of T v Whitfords Beach Pty Ltd (1982) 150 CLR.................................................................6

Statham & Anor v FC of T 89 ATC 4070...................................................................................7

Casimaty v FC of T 97 ATC 5135..............................................................................................7

Moana Sand Pty Ltd v FC of T 88 ATC 4897............................................................................7

Crow v FC of T 88 ATC 4620....................................................................................................8

McCurry & Anor v FC of T 98 ATC 4487.................................................................................8

CONCLUSION................................................................................................................................8

REFERENCES................................................................................................................................9

INTRODUCTION

Taxation law is the legal framework which is framed by the government in order to

analyse the taxable value of individual person. In this, calculation has been done for individual

person in order to analyse taxable income of individual person. It is the assessment on the

property, income, transaction and so on (Atasu and Wassenhove, 2012). This has been collected

by the government and individual have to submit tax to the government in the timely manner and

equal to amount which is imposed on them. In this legal act income of an every single has been

examined. If they are not able to pay them in a timely manner then authority is able to imposed

penalty on them.

CASE STUDY 1 – RESIDENCE AND SOURCE

As per the provision of Australian permanent resident, it states that the person who are

leaving in Australia holding a permanent residency visa but they are not considered as citizens of

Australia. A person who is holding a permanent residency visa may remain in Australia for

indefinitely year. A permanent residency can be revoked at the direction of the minister. For

example, it can be revoked in case of criminal misconduct.

The permanent of resident enjoy so many rights and privileges of citizens which is also

related with legal and health care services (Beck and Grande, 2010). But they don't have right to

vote in federal or in territory relation unless and until they have been registered in the year of

1984. The permanent residents are not entitled with an Australian passport.

For identification of tax purpose first it is mandatory to understand residency status. For

determining the tax situation the person has to analyse the work whether they are Australian or

foreign resident. There are some benefits which is related with the permanence resident are as

below.

There are few limitations on employment in Australia. Such as some job opportunities,

require citizenship are opposed as permanent residence.

They have also right to apply for the Australian citizenship after accomplishing with

some criteria.

The children who are born inside Australia will be considered as Australian citizen by the

birth.

The people also get the right to travel to New Zealand without applying for a new

Zealand visa.

Taxation law is the legal framework which is framed by the government in order to

analyse the taxable value of individual person. In this, calculation has been done for individual

person in order to analyse taxable income of individual person. It is the assessment on the

property, income, transaction and so on (Atasu and Wassenhove, 2012). This has been collected

by the government and individual have to submit tax to the government in the timely manner and

equal to amount which is imposed on them. In this legal act income of an every single has been

examined. If they are not able to pay them in a timely manner then authority is able to imposed

penalty on them.

CASE STUDY 1 – RESIDENCE AND SOURCE

As per the provision of Australian permanent resident, it states that the person who are

leaving in Australia holding a permanent residency visa but they are not considered as citizens of

Australia. A person who is holding a permanent residency visa may remain in Australia for

indefinitely year. A permanent residency can be revoked at the direction of the minister. For

example, it can be revoked in case of criminal misconduct.

The permanent of resident enjoy so many rights and privileges of citizens which is also

related with legal and health care services (Beck and Grande, 2010). But they don't have right to

vote in federal or in territory relation unless and until they have been registered in the year of

1984. The permanent residents are not entitled with an Australian passport.

For identification of tax purpose first it is mandatory to understand residency status. For

determining the tax situation the person has to analyse the work whether they are Australian or

foreign resident. There are some benefits which is related with the permanence resident are as

below.

There are few limitations on employment in Australia. Such as some job opportunities,

require citizenship are opposed as permanent residence.

They have also right to apply for the Australian citizenship after accomplishing with

some criteria.

The children who are born inside Australia will be considered as Australian citizen by the

birth.

The people also get the right to travel to New Zealand without applying for a new

Zealand visa.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

In given case, Kit is a permanent resident of Australia. Whether he was born in Chile and

having the citizenship of Chilean. As per provision of Australia he is a non ordinary resident. His

income would be taxed in the income of Australia.

As income tax provision if any person is generating the revenue from any country then

he/she is liable to pay taxes in own country (Bird, 2011). In given case scenario kit spend most of

the year in Indonesia for work. Kit is getting the leave of one month from every four month it

means that every year 120 every years. According to the provision of tax, if any person resides

more than 360 days last in 10 year then he/she will be considered as non ordinary resident.

For determining the status of Kit it is also important to determine that whether he is

coming to Australia or leaving. He will be considered as Australian resident if he satisfy one of

the following three statutory test.

Domicile test – This clearly states that, the place where he has permanent home in

Australia. He has to satisfied that the place of abode is outside the Australia.

The test of 183 days – The person has to resides in Australia more than the half of the

income year. Whether they continuously leaves or take breaks between them. Then he

will be constructive as residence in Australia.

Superannuation test – This test ensures that, if employees are working at Australian posts

overseas will be treated as Australian resident.

Tax residency is also depend upon the whether they are going or coming for having a tax

treaty within Australia (Brigham and Ehrhardt, 2013). Following are the things which has also to

be checked.

If he leaves Australia for temporarily and not

setting the permanent home in any other

country

Then his income will be calculated as

Australian resident for tax

If leaving Australia permanently They will treated as foreign resident for the

purpose of tax and it will be calculated from

the date of departure

Visiting Australia less than six months either

for visiting for holidaying

Then there income will be calculated as foreign

resident

Visiting Australia for the purpose of working They will be considered as Australian resident

having the citizenship of Chilean. As per provision of Australia he is a non ordinary resident. His

income would be taxed in the income of Australia.

As income tax provision if any person is generating the revenue from any country then

he/she is liable to pay taxes in own country (Bird, 2011). In given case scenario kit spend most of

the year in Indonesia for work. Kit is getting the leave of one month from every four month it

means that every year 120 every years. According to the provision of tax, if any person resides

more than 360 days last in 10 year then he/she will be considered as non ordinary resident.

For determining the status of Kit it is also important to determine that whether he is

coming to Australia or leaving. He will be considered as Australian resident if he satisfy one of

the following three statutory test.

Domicile test – This clearly states that, the place where he has permanent home in

Australia. He has to satisfied that the place of abode is outside the Australia.

The test of 183 days – The person has to resides in Australia more than the half of the

income year. Whether they continuously leaves or take breaks between them. Then he

will be constructive as residence in Australia.

Superannuation test – This test ensures that, if employees are working at Australian posts

overseas will be treated as Australian resident.

Tax residency is also depend upon the whether they are going or coming for having a tax

treaty within Australia (Brigham and Ehrhardt, 2013). Following are the things which has also to

be checked.

If he leaves Australia for temporarily and not

setting the permanent home in any other

country

Then his income will be calculated as

Australian resident for tax

If leaving Australia permanently They will treated as foreign resident for the

purpose of tax and it will be calculated from

the date of departure

Visiting Australia less than six months either

for visiting for holidaying

Then there income will be calculated as foreign

resident

Visiting Australia for the purpose of working They will be considered as Australian resident

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

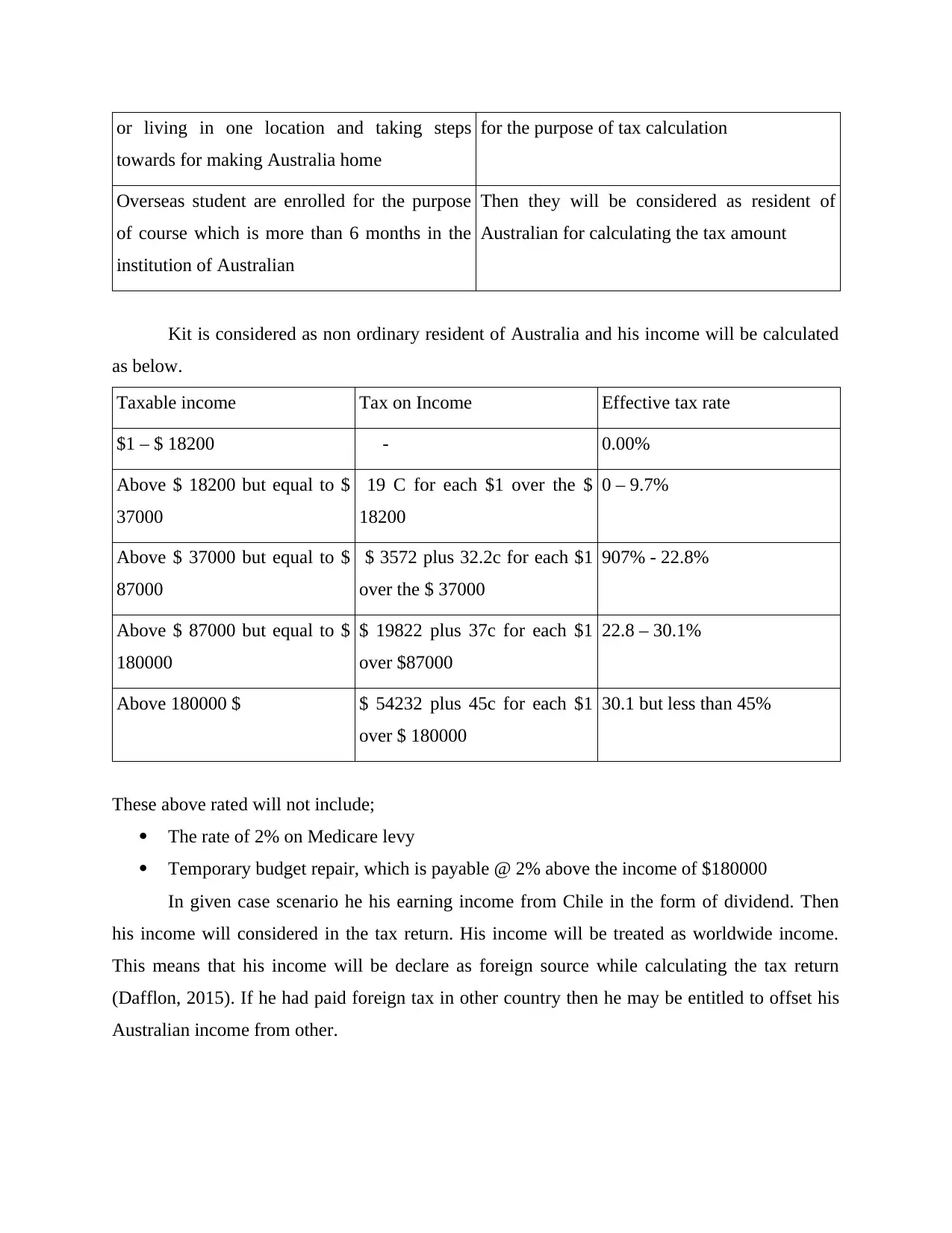

or living in one location and taking steps

towards for making Australia home

for the purpose of tax calculation

Overseas student are enrolled for the purpose

of course which is more than 6 months in the

institution of Australian

Then they will be considered as resident of

Australian for calculating the tax amount

Kit is considered as non ordinary resident of Australia and his income will be calculated

as below.

Taxable income Tax on Income Effective tax rate

$1 – $ 18200 - 0.00%

Above $ 18200 but equal to $

37000

19 C for each $1 over the $

18200

0 – 9.7%

Above $ 37000 but equal to $

87000

$ 3572 plus 32.2c for each $1

over the $ 37000

907% - 22.8%

Above $ 87000 but equal to $

180000

$ 19822 plus 37c for each $1

over $87000

22.8 – 30.1%

Above 180000 $ $ 54232 plus 45c for each $1

over $ 180000

30.1 but less than 45%

These above rated will not include;

The rate of 2% on Medicare levy

Temporary budget repair, which is payable @ 2% above the income of $180000

In given case scenario he his earning income from Chile in the form of dividend. Then

his income will considered in the tax return. His income will be treated as worldwide income.

This means that his income will be declare as foreign source while calculating the tax return

(Dafflon, 2015). If he had paid foreign tax in other country then he may be entitled to offset his

Australian income from other.

towards for making Australia home

for the purpose of tax calculation

Overseas student are enrolled for the purpose

of course which is more than 6 months in the

institution of Australian

Then they will be considered as resident of

Australian for calculating the tax amount

Kit is considered as non ordinary resident of Australia and his income will be calculated

as below.

Taxable income Tax on Income Effective tax rate

$1 – $ 18200 - 0.00%

Above $ 18200 but equal to $

37000

19 C for each $1 over the $

18200

0 – 9.7%

Above $ 37000 but equal to $

87000

$ 3572 plus 32.2c for each $1

over the $ 37000

907% - 22.8%

Above $ 87000 but equal to $

180000

$ 19822 plus 37c for each $1

over $87000

22.8 – 30.1%

Above 180000 $ $ 54232 plus 45c for each $1

over $ 180000

30.1 but less than 45%

These above rated will not include;

The rate of 2% on Medicare levy

Temporary budget repair, which is payable @ 2% above the income of $180000

In given case scenario he his earning income from Chile in the form of dividend. Then

his income will considered in the tax return. His income will be treated as worldwide income.

This means that his income will be declare as foreign source while calculating the tax return

(Dafflon, 2015). If he had paid foreign tax in other country then he may be entitled to offset his

Australian income from other.

CASE STUDY 2 – ORDINARY INCOME

Californian Copper Syndicate Ltd v Harris (Surveyor of taxes) (1904) 5 TC 159

According to Australian Taxation capital gain, it tells that when any person has raised

the income from any disposal of assets. The income which is held by the person for at least one

year then their income will be discounted 50% or by 33% for the superannuation funds. The

person can set off his capital loss income again the capital gains or it will be forwarded for next

eight years.

In given case scenario, this case was related with the issues of realisation of capital

assets. The profits which has been received from sale of land is exploited for minerals. The

income of person will be considered as ordinary income or not.

The decision of court is that the profit which is raised in the form of sale of land, will be

considered as capital in nature.

Scottish Australian Mining Co Ltd v FC of T (1950) 81 CLR 188

This case is related with problem of income of business and the sole of land. These land

were used by the mining company which would be considered as ordinary income or any

realisation of capital assets.

The decision of the court is that the authority for proposition have mere realisation of

capital assets and these can be used in the way of capital account. As per the report of

commonwealth this case had taken two years for resolving the issues and appeal was made by

the company when the judgement of court were given. The appeal has been made with in 7

weeks after the judgement. This case was also explain that there is a substantial commercial

which was considered as composition of capital assets.

FC of T v Whitfords Beach Pty Ltd (1982) 150 CLR

This case is related with the issue of business income and the subdivision of sale of land

of income will considered as ordinary income or in capital nature. This will cover in whether in

section in 25 (1) or 26 (a).

As per section 25(1), if income are received from the isolated transaction then these

income will be considered under this section of IT act. Isolated income are those transaction

which are received from outside the ordinary course of business and these kind of business is

Californian Copper Syndicate Ltd v Harris (Surveyor of taxes) (1904) 5 TC 159

According to Australian Taxation capital gain, it tells that when any person has raised

the income from any disposal of assets. The income which is held by the person for at least one

year then their income will be discounted 50% or by 33% for the superannuation funds. The

person can set off his capital loss income again the capital gains or it will be forwarded for next

eight years.

In given case scenario, this case was related with the issues of realisation of capital

assets. The profits which has been received from sale of land is exploited for minerals. The

income of person will be considered as ordinary income or not.

The decision of court is that the profit which is raised in the form of sale of land, will be

considered as capital in nature.

Scottish Australian Mining Co Ltd v FC of T (1950) 81 CLR 188

This case is related with problem of income of business and the sole of land. These land

were used by the mining company which would be considered as ordinary income or any

realisation of capital assets.

The decision of the court is that the authority for proposition have mere realisation of

capital assets and these can be used in the way of capital account. As per the report of

commonwealth this case had taken two years for resolving the issues and appeal was made by

the company when the judgement of court were given. The appeal has been made with in 7

weeks after the judgement. This case was also explain that there is a substantial commercial

which was considered as composition of capital assets.

FC of T v Whitfords Beach Pty Ltd (1982) 150 CLR

This case is related with the issue of business income and the subdivision of sale of land

of income will considered as ordinary income or in capital nature. This will cover in whether in

section in 25 (1) or 26 (a).

As per section 25(1), if income are received from the isolated transaction then these

income will be considered under this section of IT act. Isolated income are those transaction

which are received from outside the ordinary course of business and these kind of business is

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

carried out by the owners. When these transaction are carried out by a non-business taxpayers

then these transaction will also considered as isolated income.

The judgement was given by court is that, it is important for the taxpayer was non-

exempt from the sale of land under subsection 25(1) and it had been realizing the capital assets

and constituting the business for the land development.

As per section 25(1) the gross income of tax payer will be considered as in this section.

Statham & Anor v FC of T 89 ATC 4070

This case law is related with when the sale of land is made by the person and the net

proceed received from this will be accepted as assessable income under subsection 25(1) or 26

(a).

It was establish from the report that mere realization on the assets to render profit is nor

necessary for taxable. The profits which has been arises for carrying the business will be

considered as taxable income.

Casimaty v FC of T 97 ATC 5135

The sale of property of land will be assessable either in section 25(1) or 25A.

The income which is related with the sale and acquisition of property using in farming.

Conducting of business through realization of assets. In the present case scenario, the taxpayer is

argued with legal authorities that sale of part of property is generated through realization of

assets rather then through conduct of organization. As per the section 25 (1), the profit or income

which is generated from sale of property is not involved in this section. The earning which is

generated from organization are become capital assets for assesses but profit from realization is

included as well.

Moana Sand Pty Ltd v FC of T 88 ATC 4897

This case is related with the for the year ending 30th June, 1980, section 25(1) or 26 (a)

will be apply to include in the payer income. From the sale of land taxpayer had received the

amount of $ 3,70,000 and it is less relevant as compare with the cost.

The decision of court was held that the profit will be considered section of 26 (a),

because it the result of profit making carry out. It is not necessary that the profit which has been

raised by the taxpayer is for particular purpose and the section of 26(a) will apply.

then these transaction will also considered as isolated income.

The judgement was given by court is that, it is important for the taxpayer was non-

exempt from the sale of land under subsection 25(1) and it had been realizing the capital assets

and constituting the business for the land development.

As per section 25(1) the gross income of tax payer will be considered as in this section.

Statham & Anor v FC of T 89 ATC 4070

This case law is related with when the sale of land is made by the person and the net

proceed received from this will be accepted as assessable income under subsection 25(1) or 26

(a).

It was establish from the report that mere realization on the assets to render profit is nor

necessary for taxable. The profits which has been arises for carrying the business will be

considered as taxable income.

Casimaty v FC of T 97 ATC 5135

The sale of property of land will be assessable either in section 25(1) or 25A.

The income which is related with the sale and acquisition of property using in farming.

Conducting of business through realization of assets. In the present case scenario, the taxpayer is

argued with legal authorities that sale of part of property is generated through realization of

assets rather then through conduct of organization. As per the section 25 (1), the profit or income

which is generated from sale of property is not involved in this section. The earning which is

generated from organization are become capital assets for assesses but profit from realization is

included as well.

Moana Sand Pty Ltd v FC of T 88 ATC 4897

This case is related with the for the year ending 30th June, 1980, section 25(1) or 26 (a)

will be apply to include in the payer income. From the sale of land taxpayer had received the

amount of $ 3,70,000 and it is less relevant as compare with the cost.

The decision of court was held that the profit will be considered section of 26 (a),

because it the result of profit making carry out. It is not necessary that the profit which has been

raised by the taxpayer is for particular purpose and the section of 26(a) will apply.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Crow v FC of T 88 ATC 4620

In this case law, the question were raised that whether the subsection 25(1) or 26(a) will

be operated into the taxable income of the taxpayer profits in which the profit is made by him

from the sale of property.

The decision was that, this case is distinguish from the case of mining. The property can

be used as for a long purpose for farming the business in making the long term profits.

McCurry & Anor v FC of T 98 ATC 4487

The profit related with the sale of property will be considered under section 25(1)?

The judgement of court is held that in profit making scheme taxpayer has entered into

such schemes and these are the part of commercial dealing. In this case the business is not

carried out by the taxpayers and the profits which has been raised will be considered as

commercial dealing. Profit making undertaking is such a dealing in this case.

CONCLUSION

On the basis of above report it has been concluded that, tax is the legal term on the law

which is imposed on each and every person. This the calculation of income of every person and

calculated amount have to be submitted to the government in a timely manner.

In this case law, the question were raised that whether the subsection 25(1) or 26(a) will

be operated into the taxable income of the taxpayer profits in which the profit is made by him

from the sale of property.

The decision was that, this case is distinguish from the case of mining. The property can

be used as for a long purpose for farming the business in making the long term profits.

McCurry & Anor v FC of T 98 ATC 4487

The profit related with the sale of property will be considered under section 25(1)?

The judgement of court is held that in profit making scheme taxpayer has entered into

such schemes and these are the part of commercial dealing. In this case the business is not

carried out by the taxpayers and the profits which has been raised will be considered as

commercial dealing. Profit making undertaking is such a dealing in this case.

CONCLUSION

On the basis of above report it has been concluded that, tax is the legal term on the law

which is imposed on each and every person. This the calculation of income of every person and

calculated amount have to be submitted to the government in a timely manner.

REFERENCES

Books and journals

Atasu, A. and Wassenhove, L. N., 2012. An Operations Perspective on Product Take‐Back

Legislation for E‐Waste: Theory, Practice, and Research Needs.Production and

Operations Management. 21(3). pp.407-422.

Beck, U. and Grande, E., 2010. Varieties of second modernity: the cosmopolitan turn in social

and political theory and research.The British journal of sociology.61(3). pp.409-443.

Bird, R. M., 2011. Subnational taxation in developing countries: a review of the

literature.Journal of International Commerce, Economics and Policy.2(01). pp.139-161.

Brigham, E. F. and Ehrhardt, M. C., 2013.Financial management: Theory & practice. Cengage

Learning.

Dafflon, B., 2015. The assignment of functions to decentralized government: from theory to

practice.Handbook of multilevel finance, Edward Elgar, Cheltenham. pp.163-199.

Martinez-Vazquez, J., Vulovic, V. and Liu, Y., 2011. Direct versus indirect taxation: Trends,

theory and economic significance.The Elgar Guide to Tax Systems, Edward Elgar

Publishing. pp.37-92.

McGee, R. W. ed., 2011. The ethics of tax evasion: Perspectives in theory and practice. Springer

Science & Business Media.

Meyer, J. W., 2010. World society, institutional theories, and the actor.Annual review of

sociology.36. pp.1-20.

Online

Work out your residency status for tax purposes. 2012. [Online]. Available through:

<https://www.ato.gov.au/individuals/international-tax-for-individuals/work-out-your-

tax-residency/>. [Accessed on 2nd May 2017].

Books and journals

Atasu, A. and Wassenhove, L. N., 2012. An Operations Perspective on Product Take‐Back

Legislation for E‐Waste: Theory, Practice, and Research Needs.Production and

Operations Management. 21(3). pp.407-422.

Beck, U. and Grande, E., 2010. Varieties of second modernity: the cosmopolitan turn in social

and political theory and research.The British journal of sociology.61(3). pp.409-443.

Bird, R. M., 2011. Subnational taxation in developing countries: a review of the

literature.Journal of International Commerce, Economics and Policy.2(01). pp.139-161.

Brigham, E. F. and Ehrhardt, M. C., 2013.Financial management: Theory & practice. Cengage

Learning.

Dafflon, B., 2015. The assignment of functions to decentralized government: from theory to

practice.Handbook of multilevel finance, Edward Elgar, Cheltenham. pp.163-199.

Martinez-Vazquez, J., Vulovic, V. and Liu, Y., 2011. Direct versus indirect taxation: Trends,

theory and economic significance.The Elgar Guide to Tax Systems, Edward Elgar

Publishing. pp.37-92.

McGee, R. W. ed., 2011. The ethics of tax evasion: Perspectives in theory and practice. Springer

Science & Business Media.

Meyer, J. W., 2010. World society, institutional theories, and the actor.Annual review of

sociology.36. pp.1-20.

Online

Work out your residency status for tax purposes. 2012. [Online]. Available through:

<https://www.ato.gov.au/individuals/international-tax-for-individuals/work-out-your-

tax-residency/>. [Accessed on 2nd May 2017].

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.