Property Pathway Programme: High Street Market and Yield Analysis

VerifiedAdded on 2023/06/13

|21

|5789

|259

Practical Assignment

AI Summary

This assignment involves a practical real estate market analysis, beginning with a hand-drawn sketch of a high street market, detailing occupiers, trade types, and vacant units. It then delves into property yield analysis, explaining the importance of yields in real estate valuation and how they reflect investor risk. The document discusses income yields, property-specific yields, and the factors influencing them, including risk, growth, and depreciation. An illustrative example demonstrates how to calculate property value based on net operating income and capitalization rates. Finally, the assignment covers term and reversion valuation, comparing fully let freeholds and reversionary freeholds, and providing an analysis of reversionary freehold value using the term and reversion approach. Desklib offers this assignment as a resource for students studying real estate, providing insights and solutions to enhance their understanding.

REAL ESTATE

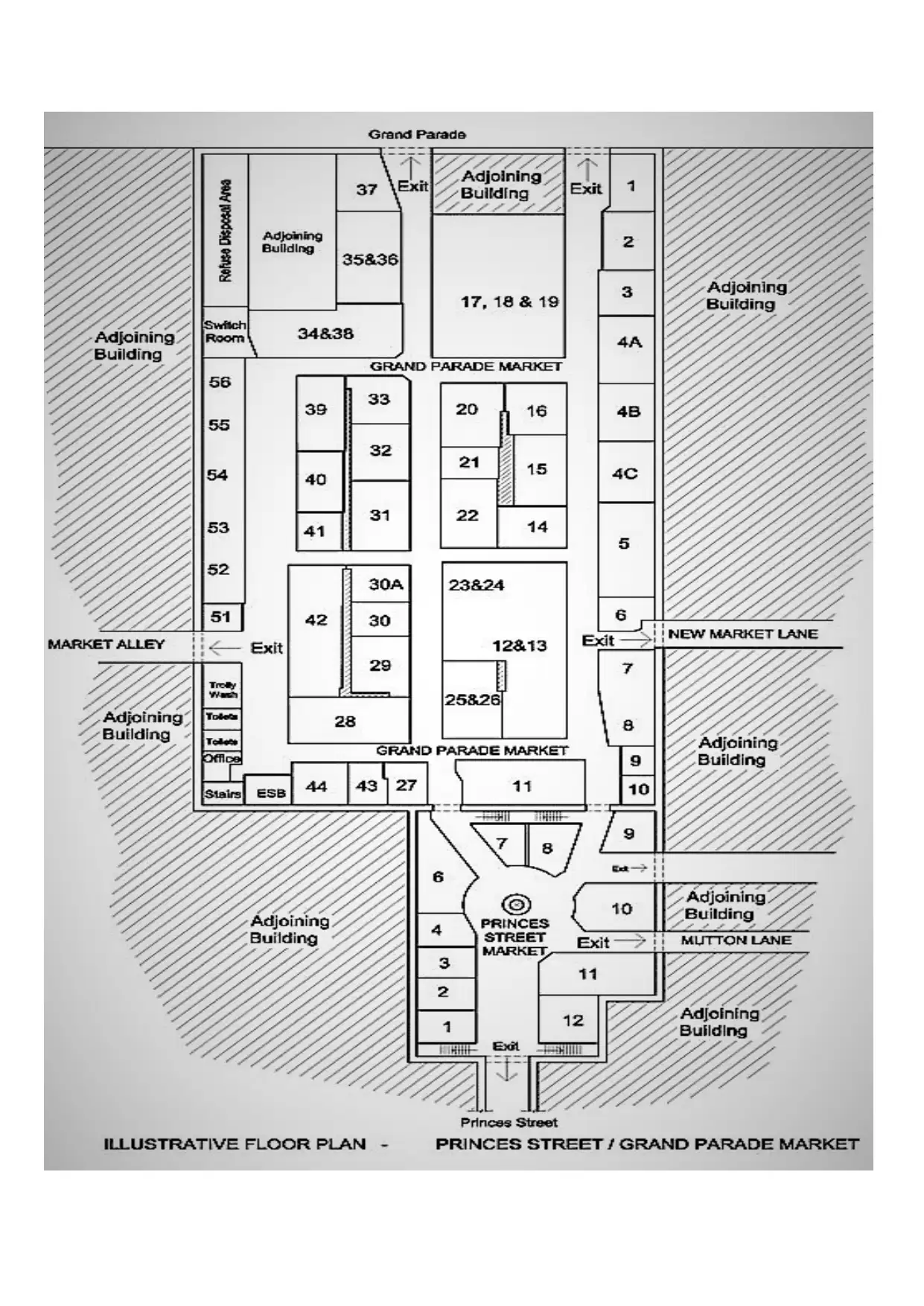

TASK – 1

SKETCH OF A HIGH STREET MARKET

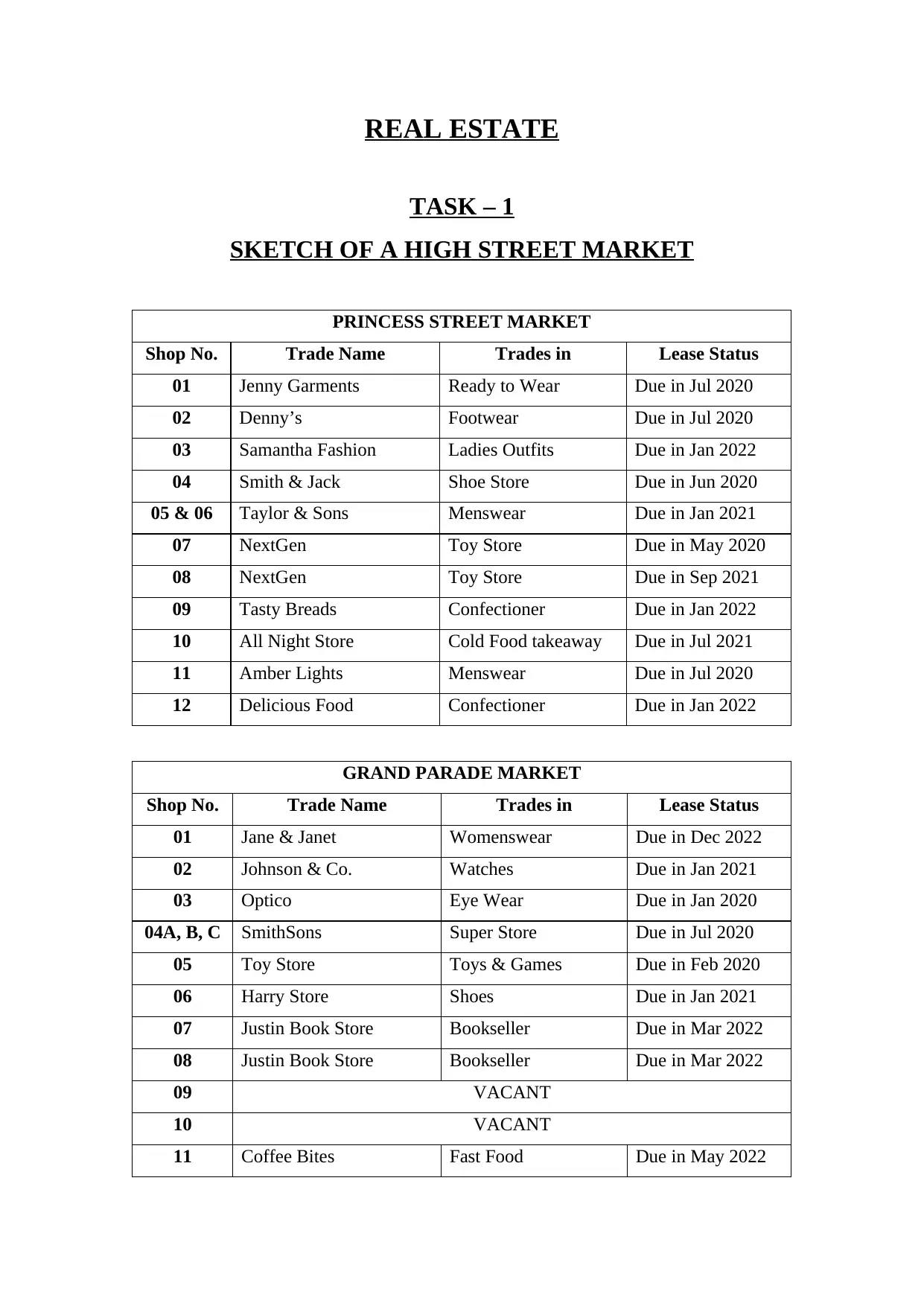

PRINCESS STREET MARKET

Shop No. Trade Name Trades in Lease Status

01 Jenny Garments Ready to Wear Due in Jul 2020

02 Denny’s Footwear Due in Jul 2020

03 Samantha Fashion Ladies Outfits Due in Jan 2022

04 Smith & Jack Shoe Store Due in Jun 2020

05 & 06 Taylor & Sons Menswear Due in Jan 2021

07 NextGen Toy Store Due in May 2020

08 NextGen Toy Store Due in Sep 2021

09 Tasty Breads Confectioner Due in Jan 2022

10 All Night Store Cold Food takeaway Due in Jul 2021

11 Amber Lights Menswear Due in Jul 2020

12 Delicious Food Confectioner Due in Jan 2022

GRAND PARADE MARKET

Shop No. Trade Name Trades in Lease Status

01 Jane & Janet Womenswear Due in Dec 2022

02 Johnson & Co. Watches Due in Jan 2021

03 Optico Eye Wear Due in Jan 2020

04A, B, C SmithSons Super Store Due in Jul 2020

05 Toy Store Toys & Games Due in Feb 2020

06 Harry Store Shoes Due in Jan 2021

07 Justin Book Store Bookseller Due in Mar 2022

08 Justin Book Store Bookseller Due in Mar 2022

09 VACANT

10 VACANT

11 Coffee Bites Fast Food Due in May 2022

TASK – 1

SKETCH OF A HIGH STREET MARKET

PRINCESS STREET MARKET

Shop No. Trade Name Trades in Lease Status

01 Jenny Garments Ready to Wear Due in Jul 2020

02 Denny’s Footwear Due in Jul 2020

03 Samantha Fashion Ladies Outfits Due in Jan 2022

04 Smith & Jack Shoe Store Due in Jun 2020

05 & 06 Taylor & Sons Menswear Due in Jan 2021

07 NextGen Toy Store Due in May 2020

08 NextGen Toy Store Due in Sep 2021

09 Tasty Breads Confectioner Due in Jan 2022

10 All Night Store Cold Food takeaway Due in Jul 2021

11 Amber Lights Menswear Due in Jul 2020

12 Delicious Food Confectioner Due in Jan 2022

GRAND PARADE MARKET

Shop No. Trade Name Trades in Lease Status

01 Jane & Janet Womenswear Due in Dec 2022

02 Johnson & Co. Watches Due in Jan 2021

03 Optico Eye Wear Due in Jan 2020

04A, B, C SmithSons Super Store Due in Jul 2020

05 Toy Store Toys & Games Due in Feb 2020

06 Harry Store Shoes Due in Jan 2021

07 Justin Book Store Bookseller Due in Mar 2022

08 Justin Book Store Bookseller Due in Mar 2022

09 VACANT

10 VACANT

11 Coffee Bites Fast Food Due in May 2022

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

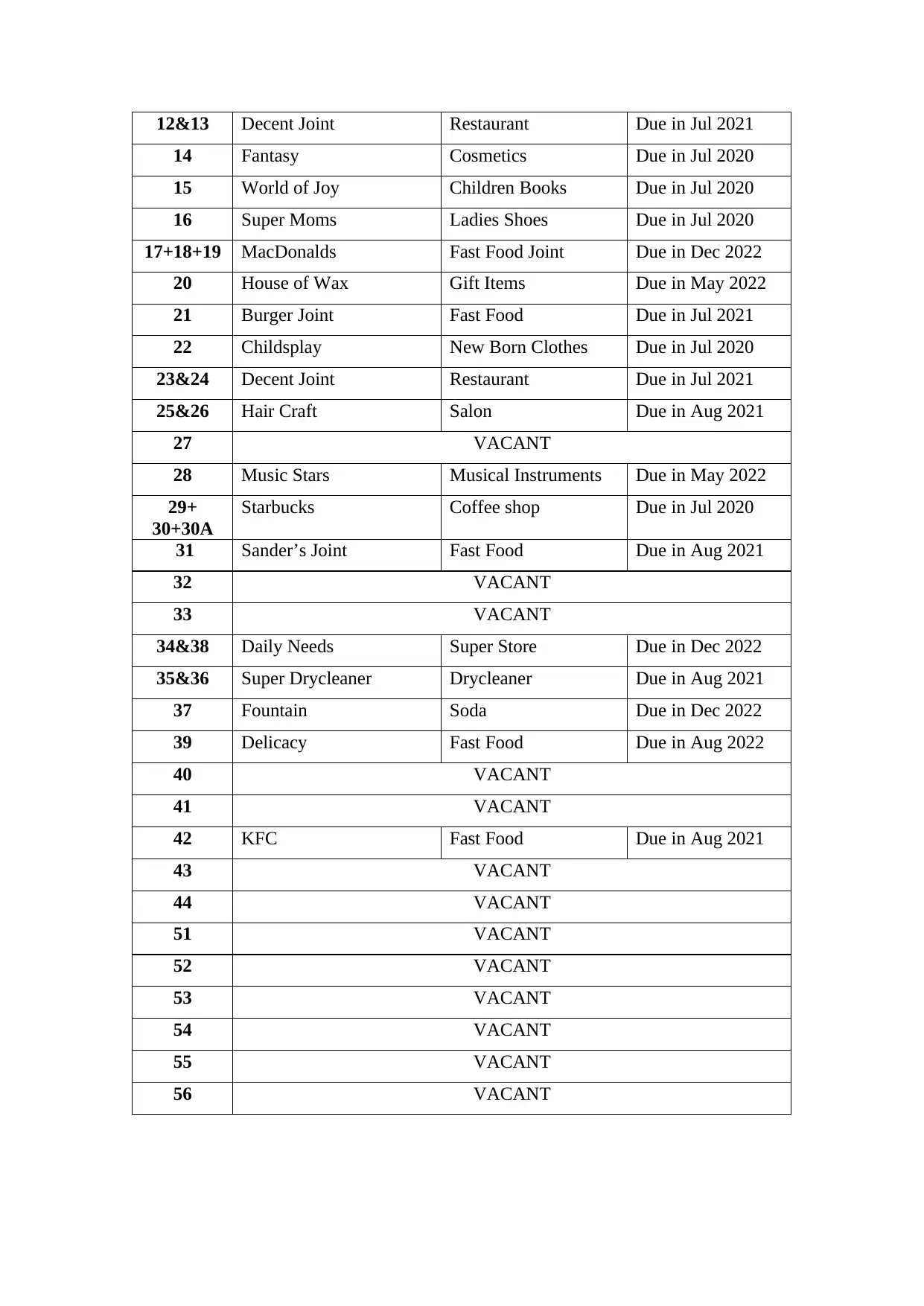

12&13 Decent Joint Restaurant Due in Jul 2021

14 Fantasy Cosmetics Due in Jul 2020

15 World of Joy Children Books Due in Jul 2020

16 Super Moms Ladies Shoes Due in Jul 2020

17+18+19 MacDonalds Fast Food Joint Due in Dec 2022

20 House of Wax Gift Items Due in May 2022

21 Burger Joint Fast Food Due in Jul 2021

22 Childsplay New Born Clothes Due in Jul 2020

23&24 Decent Joint Restaurant Due in Jul 2021

25&26 Hair Craft Salon Due in Aug 2021

27 VACANT

28 Music Stars Musical Instruments Due in May 2022

29+

30+30A

Starbucks Coffee shop Due in Jul 2020

31 Sander’s Joint Fast Food Due in Aug 2021

32 VACANT

33 VACANT

34&38 Daily Needs Super Store Due in Dec 2022

35&36 Super Drycleaner Drycleaner Due in Aug 2021

37 Fountain Soda Due in Dec 2022

39 Delicacy Fast Food Due in Aug 2022

40 VACANT

41 VACANT

42 KFC Fast Food Due in Aug 2021

43 VACANT

44 VACANT

51 VACANT

52 VACANT

53 VACANT

54 VACANT

55 VACANT

56 VACANT

14 Fantasy Cosmetics Due in Jul 2020

15 World of Joy Children Books Due in Jul 2020

16 Super Moms Ladies Shoes Due in Jul 2020

17+18+19 MacDonalds Fast Food Joint Due in Dec 2022

20 House of Wax Gift Items Due in May 2022

21 Burger Joint Fast Food Due in Jul 2021

22 Childsplay New Born Clothes Due in Jul 2020

23&24 Decent Joint Restaurant Due in Jul 2021

25&26 Hair Craft Salon Due in Aug 2021

27 VACANT

28 Music Stars Musical Instruments Due in May 2022

29+

30+30A

Starbucks Coffee shop Due in Jul 2020

31 Sander’s Joint Fast Food Due in Aug 2021

32 VACANT

33 VACANT

34&38 Daily Needs Super Store Due in Dec 2022

35&36 Super Drycleaner Drycleaner Due in Aug 2021

37 Fountain Soda Due in Dec 2022

39 Delicacy Fast Food Due in Aug 2022

40 VACANT

41 VACANT

42 KFC Fast Food Due in Aug 2021

43 VACANT

44 VACANT

51 VACANT

52 VACANT

53 VACANT

54 VACANT

55 VACANT

56 VACANT

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

TASK – 2

Rack Rented Premises

Yields have become important in many of the real estate contexts and property

valuations are now being based on information obtained from markets about the yields

demanded by investors. In cases where cash-flow methods is being used exit yields find

extensive use for calculating the property’s value at the end of the period for which this

explicit prediction is being made, as per Baum & Baum, (2015). However, the focus of

this study is on the yield term, which is important for reflecting an investor’s risk

analysis of investment. The straightforward application of this factor is usually made

with an objective to arrive at the conversion of the annual net operating income from

the investment, state Erp & Akkermans (ed), (2012).

In the current real estate markets, situation is not that simple as it is made out to be.

Investors do not become sure about the value of the property they wish to invest in

when they are going to either sell or rent it, as per Kao, Sung & Chen (ed), (2014).

Hence, property valuation methods are necessary to estimate the most suitable value of

the proposed property in the market, asserts King, (2015). The accuracy of valuation can

only be tested when the investor receives an equivalent sale value or an approximate

purchase price, which, in all cases, represents the investor’s investment cost (See

illustration in Example-1). Financial theory on yields in financial market is becoming

crucial for it serves as a comparison tool between the general financial and property-

related financial theories, according to Sexton & Bogusz, (2013).

It is a universal phenomenon that values of properties keep changing over time. As

discussed in Persson (2003), the value of a property is usually attached with the

investor’s expectations from the valuation, as stated by Burn, Cartwright & Maudsley,

(2009). In actuality, the valuation of a property is based on the following four basic

conditions:

(a) need

(b) limited supply

(c) right of disposal and

(d) transferable assets in the market.

Rack Rented Premises

Yields have become important in many of the real estate contexts and property

valuations are now being based on information obtained from markets about the yields

demanded by investors. In cases where cash-flow methods is being used exit yields find

extensive use for calculating the property’s value at the end of the period for which this

explicit prediction is being made, as per Baum & Baum, (2015). However, the focus of

this study is on the yield term, which is important for reflecting an investor’s risk

analysis of investment. The straightforward application of this factor is usually made

with an objective to arrive at the conversion of the annual net operating income from

the investment, state Erp & Akkermans (ed), (2012).

In the current real estate markets, situation is not that simple as it is made out to be.

Investors do not become sure about the value of the property they wish to invest in

when they are going to either sell or rent it, as per Kao, Sung & Chen (ed), (2014).

Hence, property valuation methods are necessary to estimate the most suitable value of

the proposed property in the market, asserts King, (2015). The accuracy of valuation can

only be tested when the investor receives an equivalent sale value or an approximate

purchase price, which, in all cases, represents the investor’s investment cost (See

illustration in Example-1). Financial theory on yields in financial market is becoming

crucial for it serves as a comparison tool between the general financial and property-

related financial theories, according to Sexton & Bogusz, (2013).

It is a universal phenomenon that values of properties keep changing over time. As

discussed in Persson (2003), the value of a property is usually attached with the

investor’s expectations from the valuation, as stated by Burn, Cartwright & Maudsley,

(2009). In actuality, the valuation of a property is based on the following four basic

conditions:

(a) need

(b) limited supply

(c) right of disposal and

(d) transferable assets in the market.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Once any of these four conditions change, the expected yield is bound to follow the

movements of the change, but always in an opposite direction. Hence, to make a correct

assessment of the yield ratio, it becomes necessary that the above noted conditions

remain standard and are acceptable to all participants dealing in that property, say

Megarry et al, (2012). It must also be noted that although Going-concern has not been

considered as a basic condition for valuation, it is a strong pre-requisite for a good yield

since every business is directly connected with the property from which it is run. The

values of the properties are attributed to the value created by the business operations run

from that property and hence, the business and the property are inter-related, asserts

Bevans, (2008). Both the values generated are capitalised on the profits generated by the

business’ turnover and its calculation is directly related to the property’s valuation, says

Hinkel, (2010). Finally, the return on the investments must be compensated to the

investor for “foregoing the present benefits and accepting the future benefits and risks”.

This return in value is what is commonly termed as “interest” by lenders and “yield” by

investors.

Income Yields

The Current Income and Current Capital Value of a property is measured through use of

Income Yields. Although each financial instrument is required to use a different income

yield method for differentiating it from others, in case of property-specific yield

methods, a brief description of income yields, is being given. In the property market, the

income yield is also known as the initial yield and sometimes as All Risks Yield (ARY),

assert McFarlane, Hopkins & Nield, (2012). It represents the ratio of net rental income

to the purchase price or the current market value of the property under consideration.

The Years’ Purchase (YP) is the inverse ratio of the income yield and is equivalent to

the Present Value (PV) of $1 which is received annually and has been discounted at the

initial yield rate. According to Baum, (2009), income yield from a property is useful for

investors when they want to make assumptions about the market expectations of a risk,

its growth and the depreciation, according to Karadimitrio, Magalhaes & Verhage,

(2013). This relationship between the various factors is expressed by the following

comparatives:

(A) The higher the risk, the higher is income yield;

(B) The higher the income growth, the lower is income yield; and

(C) The higher the depreciation, the higher income yield.

movements of the change, but always in an opposite direction. Hence, to make a correct

assessment of the yield ratio, it becomes necessary that the above noted conditions

remain standard and are acceptable to all participants dealing in that property, say

Megarry et al, (2012). It must also be noted that although Going-concern has not been

considered as a basic condition for valuation, it is a strong pre-requisite for a good yield

since every business is directly connected with the property from which it is run. The

values of the properties are attributed to the value created by the business operations run

from that property and hence, the business and the property are inter-related, asserts

Bevans, (2008). Both the values generated are capitalised on the profits generated by the

business’ turnover and its calculation is directly related to the property’s valuation, says

Hinkel, (2010). Finally, the return on the investments must be compensated to the

investor for “foregoing the present benefits and accepting the future benefits and risks”.

This return in value is what is commonly termed as “interest” by lenders and “yield” by

investors.

Income Yields

The Current Income and Current Capital Value of a property is measured through use of

Income Yields. Although each financial instrument is required to use a different income

yield method for differentiating it from others, in case of property-specific yield

methods, a brief description of income yields, is being given. In the property market, the

income yield is also known as the initial yield and sometimes as All Risks Yield (ARY),

assert McFarlane, Hopkins & Nield, (2012). It represents the ratio of net rental income

to the purchase price or the current market value of the property under consideration.

The Years’ Purchase (YP) is the inverse ratio of the income yield and is equivalent to

the Present Value (PV) of $1 which is received annually and has been discounted at the

initial yield rate. According to Baum, (2009), income yield from a property is useful for

investors when they want to make assumptions about the market expectations of a risk,

its growth and the depreciation, according to Karadimitrio, Magalhaes & Verhage,

(2013). This relationship between the various factors is expressed by the following

comparatives:

(A) The higher the risk, the higher is income yield;

(B) The higher the income growth, the lower is income yield; and

(C) The higher the depreciation, the higher income yield.

Property-Specific Yields

As per the JLW Glossary of Property Terms, 1989, the words rate, return and yield are

often used as synonyms for describing the ratios between income and capital value or

cost in the property market. The difference among these terms is in the time path of the

data and their sources of value and capital. The Estates Gazette, 1993 defines them as

follows, and I quote:

“Yields are generally defined as annual percentage amounts expected to be produced

by an investment. They are also used as the measure for capitalization of income in the

specific context of investment valuation. The yield is therefore identified very much as a

measure of market expectation. Returns on capital, on the other hand, are defined as

the annual percentage amount produced by an investment by reference to its cost or

value. Returns can be distinguished from yields in that the value, on which they are

based, is not necessarily a market value. Rates of interest, finally, are simply the annual

percentage amounts payable on borrowed money and are further used in the context of

discounting to reflect the time value of money.” Unquote.

As illustrated in the example below, the universal formula used for evaluating the

property’s yield or cap rate is to divide the annual net operating income by the selling

price. The net operating income is obtained by reducing the actual or anticipated net

income by all the operating expenses, but before deducting the mortgage debt service

charges, as stated by Goodhart & Hofmann, (2007).

Illustrative Example – 1

Potential gross rents plus other income

= potential gross income less vacancy and credit losses

= effective gross income less operating expenses

= net operating income

Once the relevant capitalization rate or yield has been determined, an estimative of

property value can be obtained, by applying the universal valuation formula:

Value = Income / Cap Rate

Or: V = I / R

Now, considering the data provided, following shall be the Values –

VALUE if Yield is 5%

As per the JLW Glossary of Property Terms, 1989, the words rate, return and yield are

often used as synonyms for describing the ratios between income and capital value or

cost in the property market. The difference among these terms is in the time path of the

data and their sources of value and capital. The Estates Gazette, 1993 defines them as

follows, and I quote:

“Yields are generally defined as annual percentage amounts expected to be produced

by an investment. They are also used as the measure for capitalization of income in the

specific context of investment valuation. The yield is therefore identified very much as a

measure of market expectation. Returns on capital, on the other hand, are defined as

the annual percentage amount produced by an investment by reference to its cost or

value. Returns can be distinguished from yields in that the value, on which they are

based, is not necessarily a market value. Rates of interest, finally, are simply the annual

percentage amounts payable on borrowed money and are further used in the context of

discounting to reflect the time value of money.” Unquote.

As illustrated in the example below, the universal formula used for evaluating the

property’s yield or cap rate is to divide the annual net operating income by the selling

price. The net operating income is obtained by reducing the actual or anticipated net

income by all the operating expenses, but before deducting the mortgage debt service

charges, as stated by Goodhart & Hofmann, (2007).

Illustrative Example – 1

Potential gross rents plus other income

= potential gross income less vacancy and credit losses

= effective gross income less operating expenses

= net operating income

Once the relevant capitalization rate or yield has been determined, an estimative of

property value can be obtained, by applying the universal valuation formula:

Value = Income / Cap Rate

Or: V = I / R

Now, considering the data provided, following shall be the Values –

VALUE if Yield is 5%

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

= £65,000 / 5% = £65,000 / 0.05 = £1,300,000

LESS Purchaser’s Costs of £88,400 = £1,211,600

VALUE if Yield is 5.25%

= £65,000 / 5.25% = £65,000 / 0.0525 = £1,238,095

LESS Purchaser’s Costs of £84,190 = £1,153,905

Purchaser’s Costs are considered to be 6.8%

Diagram Showing the Flow of Finance

LESS Purchaser’s Costs of £88,400 = £1,211,600

VALUE if Yield is 5.25%

= £65,000 / 5.25% = £65,000 / 0.0525 = £1,238,095

LESS Purchaser’s Costs of £84,190 = £1,153,905

Purchaser’s Costs are considered to be 6.8%

Diagram Showing the Flow of Finance

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TASK – 3

TERM & REVERSION

The Fully Let Freehold

Of all the categories of property investment in use at present, the fully let freehold has

been considered as the least prone to variations and hence to an inaccurate valuation.

The normal approach adopted when dealing with a fully let freehold interest of the

investor for market value purposes is to consider the rent passing (which is also known

as the ERV) and divide it by the capitalisation rate (also known as ARY-all-risks

yield), as per Ashworth & Perera, (2015). In this method, there are no major differences

in its application by different investors, hence the chances of any differentiated

valuations by the users, based on the same data base are almost negligible. However,

since the valuation method relies on the strength of the comparable data, the comparable

data may create a small difference in cases where the market is dominated by

reversionary freeholds. Hence, the quantity and quality of the comparable transactions

is the key to the comparable valuations, assert Fair & Raymond (ed), (2013).

However, as per Myers, (2012), in cases where the comparable data cannot be directly

applied, the adaptations used should be intuitive. Take for example, a case where the

reversionary freehold comparable is showing a yield of 6%, then the question is how to

apply this information to a fully let property? What are the consequences, asks Taylor,

(2008), when the comparable has been let on 5-year review but the subject property has

been let on a 3-year review? But since the model has been based on rent and

capitalisation rate, only the capitalisation rate should be adjusted to deal with the

ambiguity between the subjective and the comparable, hence the use of ‘all-risks yield’,

which is used so that all risks are hidden in the yield.

The Reversionary Freehold

There are three conventional techniques used for valuing the reversionary freeholds and

these are the –

(A) Term and Reversion

(B) The Equivalent Yield and

TERM & REVERSION

The Fully Let Freehold

Of all the categories of property investment in use at present, the fully let freehold has

been considered as the least prone to variations and hence to an inaccurate valuation.

The normal approach adopted when dealing with a fully let freehold interest of the

investor for market value purposes is to consider the rent passing (which is also known

as the ERV) and divide it by the capitalisation rate (also known as ARY-all-risks

yield), as per Ashworth & Perera, (2015). In this method, there are no major differences

in its application by different investors, hence the chances of any differentiated

valuations by the users, based on the same data base are almost negligible. However,

since the valuation method relies on the strength of the comparable data, the comparable

data may create a small difference in cases where the market is dominated by

reversionary freeholds. Hence, the quantity and quality of the comparable transactions

is the key to the comparable valuations, assert Fair & Raymond (ed), (2013).

However, as per Myers, (2012), in cases where the comparable data cannot be directly

applied, the adaptations used should be intuitive. Take for example, a case where the

reversionary freehold comparable is showing a yield of 6%, then the question is how to

apply this information to a fully let property? What are the consequences, asks Taylor,

(2008), when the comparable has been let on 5-year review but the subject property has

been let on a 3-year review? But since the model has been based on rent and

capitalisation rate, only the capitalisation rate should be adjusted to deal with the

ambiguity between the subjective and the comparable, hence the use of ‘all-risks yield’,

which is used so that all risks are hidden in the yield.

The Reversionary Freehold

There are three conventional techniques used for valuing the reversionary freeholds and

these are the –

(A) Term and Reversion

(B) The Equivalent Yield and

(C) The Layer (or hard core) Approach.

The basis used in most of the market valuations tend to suggest that the term and

reversion approach has found the most common application among users, whereas the

other two are the lesser used methods, explain Smith & Jaggar, (2007).

Analysis

For our analysis of the Reversionary Freehold Value, we are considering a freehold

office investment, where the property has been let at a net fixed rent of £150,000 p.a.

and where the final 6 years of the historic lease are still to run. The net ERV of the

building has been fixed at £300,000 p.a. An identical space in the building next door has

also been recently let on 5-yearly reviews at its ERV and has been subsequently sold for

£5,000,000. The Capitalisation Rate (k) is calculated as £300,000 / £5,000,000 and is

found to be 6%

In the UK, according to Kao, Sung & Chen (ed), (2014), the purchaser’s costs are

deducted from the valuations after the application of the capitalisation rate. Because of

this factor, when an analysis of the property’s transactions are carried out for calculating

the capitalisation rate, all these costs are added back to the contract price for

determining the full outlay of the property. For the purpose of this study, as explained

by Burn, Cartwright & Maudsley, (2009), the purchaser’s costs in the UK are taken at

5.75%, and these consist of 4% stamp duty tax and 1.75% for professional fees.

However, in order to keep calculations simple, it is better to ignore all purchaser’s costs

for the purpose of calculations in this study, assert Erp & Akkermans (ed), (2012).

If the valuation is about a fully let property, the capitalisation rate can be applied

directly. In cases where perfect comparable data is available, there can be no arguments

over the method being used and direct capital comparisons are all which an investor

requires. However, the subject property of our example is a reversionary property and

hence an adjustment technique is required in order to reconcile any imperfect

comparable data, as illustrated below, as stated by King, (2015).

Term and Reversion

Term rent £150,000

YP 6 years @ 5% 5.0757

The basis used in most of the market valuations tend to suggest that the term and

reversion approach has found the most common application among users, whereas the

other two are the lesser used methods, explain Smith & Jaggar, (2007).

Analysis

For our analysis of the Reversionary Freehold Value, we are considering a freehold

office investment, where the property has been let at a net fixed rent of £150,000 p.a.

and where the final 6 years of the historic lease are still to run. The net ERV of the

building has been fixed at £300,000 p.a. An identical space in the building next door has

also been recently let on 5-yearly reviews at its ERV and has been subsequently sold for

£5,000,000. The Capitalisation Rate (k) is calculated as £300,000 / £5,000,000 and is

found to be 6%

In the UK, according to Kao, Sung & Chen (ed), (2014), the purchaser’s costs are

deducted from the valuations after the application of the capitalisation rate. Because of

this factor, when an analysis of the property’s transactions are carried out for calculating

the capitalisation rate, all these costs are added back to the contract price for

determining the full outlay of the property. For the purpose of this study, as explained

by Burn, Cartwright & Maudsley, (2009), the purchaser’s costs in the UK are taken at

5.75%, and these consist of 4% stamp duty tax and 1.75% for professional fees.

However, in order to keep calculations simple, it is better to ignore all purchaser’s costs

for the purpose of calculations in this study, assert Erp & Akkermans (ed), (2012).

If the valuation is about a fully let property, the capitalisation rate can be applied

directly. In cases where perfect comparable data is available, there can be no arguments

over the method being used and direct capital comparisons are all which an investor

requires. However, the subject property of our example is a reversionary property and

hence an adjustment technique is required in order to reconcile any imperfect

comparable data, as illustrated below, as stated by King, (2015).

Term and Reversion

Term rent £150,000

YP 6 years @ 5% 5.0757

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Term and Reversion Valuation is £761,350

Reversion to ERV £300,000

YP perp. @ 6% 16.6667

PV 6 years @ 6% 0.7050

Valuation is £3,524,800

Final Valuation is taken as £4,286,150

Analysis

Initial yield = £150,000 / £4,286,160 = 3.50%

Reversionary yield = £300,000 / £4,286,160 = 7.00%

The equivalent yield is the single yield applied to both parts of the valuation to get the

same answer. In this case it is 5.97%.

a. The term yield has derived from the fully let comparable and then is adjusted to

represent the security of the term income. This security is derived from the fact that

the default risk from the tenant is less as he is less likely to vacate the premises

while paying less than the ERV.

b. The capitalisation rate of the reversion has been based on the fact that the property

shall become fully let in 6 years’ time and the comparison is also with a fully let

property, hence the yield can be applied directly, states Bevans, (2008).

c. An alternative application of this technique may adopt the same 1% differentials

between the term and reversion yield.

d. This methodology does not attempt to identify the nature of any changes in the rent

and whether this can be caused by a rent review or a lease expiry, says Myers,

(2012).

Reversion to ERV £300,000

YP perp. @ 6% 16.6667

PV 6 years @ 6% 0.7050

Valuation is £3,524,800

Final Valuation is taken as £4,286,150

Analysis

Initial yield = £150,000 / £4,286,160 = 3.50%

Reversionary yield = £300,000 / £4,286,160 = 7.00%

The equivalent yield is the single yield applied to both parts of the valuation to get the

same answer. In this case it is 5.97%.

a. The term yield has derived from the fully let comparable and then is adjusted to

represent the security of the term income. This security is derived from the fact that

the default risk from the tenant is less as he is less likely to vacate the premises

while paying less than the ERV.

b. The capitalisation rate of the reversion has been based on the fact that the property

shall become fully let in 6 years’ time and the comparison is also with a fully let

property, hence the yield can be applied directly, states Bevans, (2008).

c. An alternative application of this technique may adopt the same 1% differentials

between the term and reversion yield.

d. This methodology does not attempt to identify the nature of any changes in the rent

and whether this can be caused by a rent review or a lease expiry, says Myers,

(2012).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

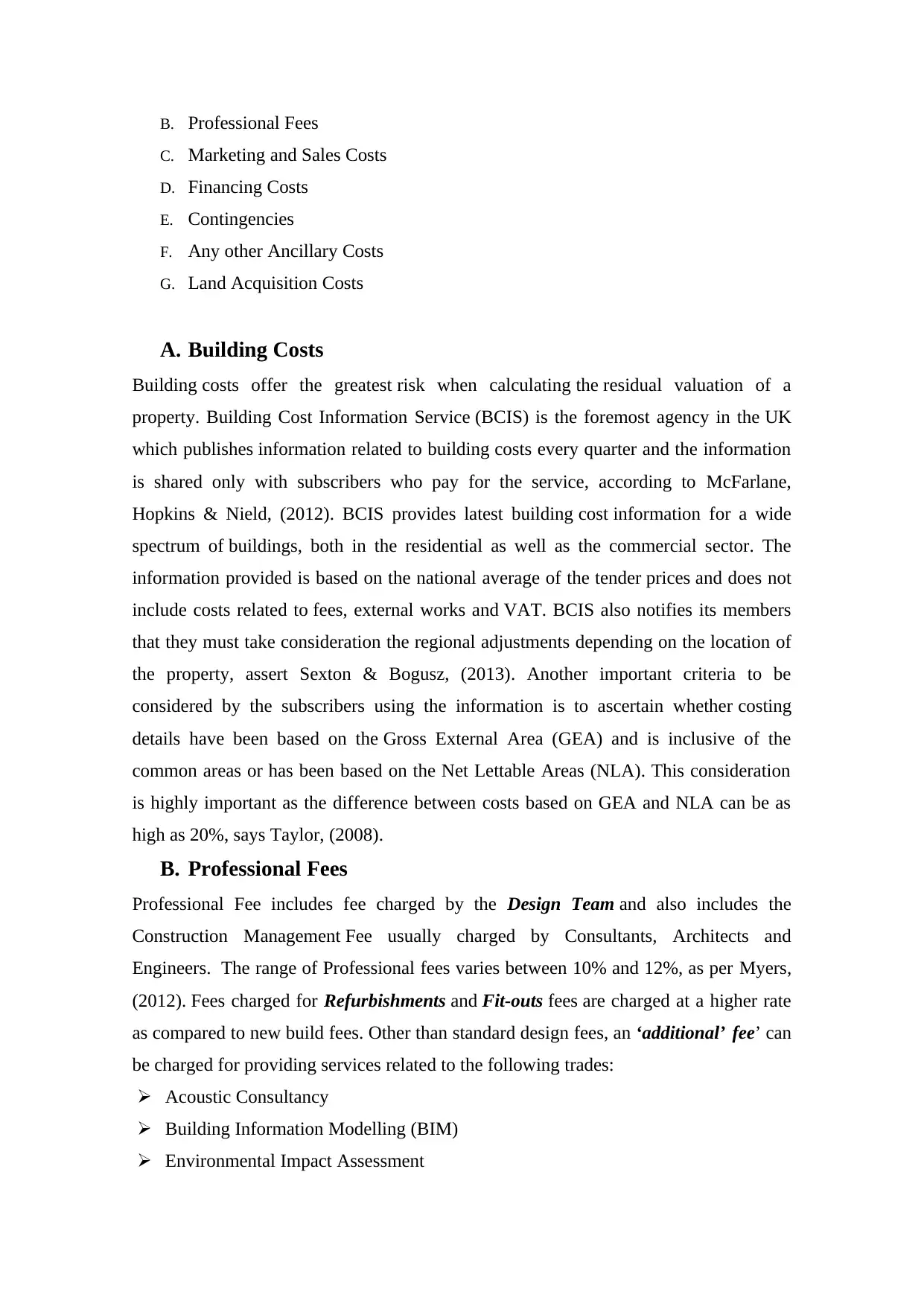

Diagram showing Term and Reversion Trend

TASK – 4

OUTLINE RESIDUAL VALUATION

Residual valuation is the process of valuing land with development potential. The sum

of money available for the purchase of land can be calculated from the value of the

completed development minus the costs of development (including profit), as per

Megarry et al, (2012). The complexity lies in the calculation of inflation, finance terms,

interest and cash flow against a programme timeframe. The equation for the residual

method of valuation, in its simplest form, is as follows, states Baum, (2009):

Value of Land / Property = GDV – (Construction + Fees + Profit)

here

Value of Land / Property refers to Purchase price of land / property / site

GDV refers to Gross Development Value

Construction refers to Building and construction costs

Fees refers to Fees and transaction costs

Profit refers to Developers profit required

Gross Development Value (GDV)

GDV, asserts Myers, (2012), comprises of the following components:

A. Building Costs

TASK – 4

OUTLINE RESIDUAL VALUATION

Residual valuation is the process of valuing land with development potential. The sum

of money available for the purchase of land can be calculated from the value of the

completed development minus the costs of development (including profit), as per

Megarry et al, (2012). The complexity lies in the calculation of inflation, finance terms,

interest and cash flow against a programme timeframe. The equation for the residual

method of valuation, in its simplest form, is as follows, states Baum, (2009):

Value of Land / Property = GDV – (Construction + Fees + Profit)

here

Value of Land / Property refers to Purchase price of land / property / site

GDV refers to Gross Development Value

Construction refers to Building and construction costs

Fees refers to Fees and transaction costs

Profit refers to Developers profit required

Gross Development Value (GDV)

GDV, asserts Myers, (2012), comprises of the following components:

A. Building Costs

B. Professional Fees

C. Marketing and Sales Costs

D. Financing Costs

E. Contingencies

F. Any other Ancillary Costs

G. Land Acquisition Costs

A. Building Costs

Building costs offer the greatest risk when calculating the residual valuation of a

property. Building Cost Information Service (BCIS) is the foremost agency in the UK

which publishes information related to building costs every quarter and the information

is shared only with subscribers who pay for the service, according to McFarlane,

Hopkins & Nield, (2012). BCIS provides latest building cost information for a wide

spectrum of buildings, both in the residential as well as the commercial sector. The

information provided is based on the national average of the tender prices and does not

include costs related to fees, external works and VAT. BCIS also notifies its members

that they must take consideration the regional adjustments depending on the location of

the property, assert Sexton & Bogusz, (2013). Another important criteria to be

considered by the subscribers using the information is to ascertain whether costing

details have been based on the Gross External Area (GEA) and is inclusive of the

common areas or has been based on the Net Lettable Areas (NLA). This consideration

is highly important as the difference between costs based on GEA and NLA can be as

high as 20%, says Taylor, (2008).

B. Professional Fees

Professional Fee includes fee charged by the Design Team and also includes the

Construction Management Fee usually charged by Consultants, Architects and

Engineers. The range of Professional fees varies between 10% and 12%, as per Myers,

(2012). Fees charged for Refurbishments and Fit-outs fees are charged at a higher rate

as compared to new build fees. Other than standard design fees, an ‘additional’ fee’ can

be charged for providing services related to the following trades:

Acoustic Consultancy

Building Information Modelling (BIM)

Environmental Impact Assessment

C. Marketing and Sales Costs

D. Financing Costs

E. Contingencies

F. Any other Ancillary Costs

G. Land Acquisition Costs

A. Building Costs

Building costs offer the greatest risk when calculating the residual valuation of a

property. Building Cost Information Service (BCIS) is the foremost agency in the UK

which publishes information related to building costs every quarter and the information

is shared only with subscribers who pay for the service, according to McFarlane,

Hopkins & Nield, (2012). BCIS provides latest building cost information for a wide

spectrum of buildings, both in the residential as well as the commercial sector. The

information provided is based on the national average of the tender prices and does not

include costs related to fees, external works and VAT. BCIS also notifies its members

that they must take consideration the regional adjustments depending on the location of

the property, assert Sexton & Bogusz, (2013). Another important criteria to be

considered by the subscribers using the information is to ascertain whether costing

details have been based on the Gross External Area (GEA) and is inclusive of the

common areas or has been based on the Net Lettable Areas (NLA). This consideration

is highly important as the difference between costs based on GEA and NLA can be as

high as 20%, says Taylor, (2008).

B. Professional Fees

Professional Fee includes fee charged by the Design Team and also includes the

Construction Management Fee usually charged by Consultants, Architects and

Engineers. The range of Professional fees varies between 10% and 12%, as per Myers,

(2012). Fees charged for Refurbishments and Fit-outs fees are charged at a higher rate

as compared to new build fees. Other than standard design fees, an ‘additional’ fee’ can

be charged for providing services related to the following trades:

Acoustic Consultancy

Building Information Modelling (BIM)

Environmental Impact Assessment

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 21

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.