Internal Verification of Assessment Decisions - BTEC(RQF)

VerifiedAdded on 2023/02/13

|32

|5757

|32

AI Summary

This document provides information about the internal verification process for assessment decisions in BTEC(RQF) qualifications. It includes a checklist, criteria, and feedback for assessors. The document also discusses the Pearson HND in Business program and Unit 5 - Accounting Principles. The assignment titled 'Accounting in Context and Budgetary Control' is mentioned as well.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Higher Nationals

Internal verification of assessment decisions – BTEC(RQF)

INTERNALVERIFICATION–ASSESSMENTDECISIONS

Programmetitle Pearson HND in Business

Assessor InternalVerifier

Unit(s) Unit 5 – Accounting Principles

Assignmenttitle Accounting in Context and Budgetary Control.

Student’sname

Listwhichassessmentcrit

eriatheAssessorhasawar

ded.

Pass Merit Distinction

INTERNALVERIFIERCHECKLIST

Dotheassessmentcriteriaawardedmatcht

hoseshownintheassignmentbrief? Y/N

Isthe Pass/Merit/Distinction

gradeawardedjustified bythe assessor’s

comments on the student work?

Y/N

Hastheworkbeenassessedaccur

ately? Y/N

Isthefeedbacktothestudent:

Givedetails:

• Constructive?

• Linkedtorelevantassessment

criteria?

• Identifyingopportunitiesf

or improvedperformance?

• Agreeingactions?

Y/

NY/

N

Y/

NY/

N

Doesthe

assessmentdecisionneedamending? Y/N

Assessorsignature Date

InternalVerifiersignature Date

Programme Leader

signature(ifrequired) Date

Internal verification of assessment decisions – BTEC(RQF)

INTERNALVERIFICATION–ASSESSMENTDECISIONS

Programmetitle Pearson HND in Business

Assessor InternalVerifier

Unit(s) Unit 5 – Accounting Principles

Assignmenttitle Accounting in Context and Budgetary Control.

Student’sname

Listwhichassessmentcrit

eriatheAssessorhasawar

ded.

Pass Merit Distinction

INTERNALVERIFIERCHECKLIST

Dotheassessmentcriteriaawardedmatcht

hoseshownintheassignmentbrief? Y/N

Isthe Pass/Merit/Distinction

gradeawardedjustified bythe assessor’s

comments on the student work?

Y/N

Hastheworkbeenassessedaccur

ately? Y/N

Isthefeedbacktothestudent:

Givedetails:

• Constructive?

• Linkedtorelevantassessment

criteria?

• Identifyingopportunitiesf

or improvedperformance?

• Agreeingactions?

Y/

NY/

N

Y/

NY/

N

Doesthe

assessmentdecisionneedamending? Y/N

Assessorsignature Date

InternalVerifiersignature Date

Programme Leader

signature(ifrequired) Date

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Confirm actioncompleted

Remedialactiontaken

Givedetails:

Assessorsignature Date

InternalVerifiersi

gnature Date

Programme

Leadersignature(ifrequi

red)

Date

Remedialactiontaken

Givedetails:

Assessorsignature Date

InternalVerifiersi

gnature Date

Programme

Leadersignature(ifrequi

red)

Date

Higher Nationals - SummativeAssignmentFeedbackForm

StudentName/ID

UnitTitle Unit 5 – Accounting Principles

AssignmentNumber Assignment 1 of 2 Assessor

SubmissionDate DateReceived1stsub

mission

Re-submissionDate DateReceived2ndsubmissio

n

AssessorFeedback:

LO1 Examine the context and purpose of accounting

Pass, Merit & Distinction

Descripts

P1 P2 M1 D1

LO2 Prepare basic financial statements for unincorporated and small business organisations in accordance

with accounting principles, conventions, and standards

Pass, Merit & Distinction

Descripts

P3 M2 D2

LO3 Interpret financial statements

Pass, Merit & Distinction

Descripts

P4 P5 M3 D2

LO4 Prepare budgets for planning, control and decision-making using spreadsheets.

Pass, Merit & Distinction

Descripts

P6 P7 M4 D3

Grade: AssessorSignature: Date:

StudentName/ID

UnitTitle Unit 5 – Accounting Principles

AssignmentNumber Assignment 1 of 2 Assessor

SubmissionDate DateReceived1stsub

mission

Re-submissionDate DateReceived2ndsubmissio

n

AssessorFeedback:

LO1 Examine the context and purpose of accounting

Pass, Merit & Distinction

Descripts

P1 P2 M1 D1

LO2 Prepare basic financial statements for unincorporated and small business organisations in accordance

with accounting principles, conventions, and standards

Pass, Merit & Distinction

Descripts

P3 M2 D2

LO3 Interpret financial statements

Pass, Merit & Distinction

Descripts

P4 P5 M3 D2

LO4 Prepare budgets for planning, control and decision-making using spreadsheets.

Pass, Merit & Distinction

Descripts

P6 P7 M4 D3

Grade: AssessorSignature: Date:

ResubmissionFeedback:

Grade: AssessorSignature: Date:

InternalVerifier’sComments:

Signature&Date:

* Please note that grade decisions are provisional. They are only confirmed once internal and external moderation has taken place and grades decisions have

been agreed at the assessment board.

Assignment Feedback

Formative Feedback: Assessor to Student

Action Plan

Summative feedback

Feedback: Student to Assessor

Grade: AssessorSignature: Date:

InternalVerifier’sComments:

Signature&Date:

* Please note that grade decisions are provisional. They are only confirmed once internal and external moderation has taken place and grades decisions have

been agreed at the assessment board.

Assignment Feedback

Formative Feedback: Assessor to Student

Action Plan

Summative feedback

Feedback: Student to Assessor

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Assessor signature Date

Student signature Date

Pearson

Higher Nationals in

Business

Unit 5: Accounting Principles

Assignment 01

Student signature Date

Pearson

Higher Nationals in

Business

Unit 5: Accounting Principles

Assignment 01

General Guidelines

1. A Cover page or title page – You should always attach a title page to your assignment. Use previous

page as your cover sheet and make sure all the details are accurately filled.

2. Attach this brief as the first section of your assignment.

3. All the assignments should be prepared using a word processing software.

4. All the assignments should be printed on A4 sized papers. Use single side printing.

5. Allow 1” for top, bottom , right margins and 1.25” for the left margin of each page.

Word Processing Rules

1. The font size should be 12 point, and should be in the style of Time New Roman.

2. Use 1.5 line spacing. Left justify all paragraphs.

3. Ensure that all the headings are consistent in terms of the font size and font style.

4. Use footer function in the word processor to insert Your Name, Subject, Assignment No, and

Page Number on each page. This is useful if individual sheets become detached for any reason.

5. Use word processing application spell check and grammar check function to help editing your

assignment.

Important Points:

1. It is strictly prohibited to use textboxes to add texts in the assignments, except for the compulsory

information. eg: Figures, tables of comparison etc. Adding text boxes in the body except for the

before mentioned compulsory information will result in rejection of your work.

2. Avoid using page borders in your assignment body.

3. Carefully check the hand in date and the instructions given in the assignment. Late submissions will

not be accepted.

4. Ensure that you give yourself enough time to complete the assignment by the due date.

5. Excuses of any nature will not be accepted for failure to hand in the work on time.

6. You must take responsibility for managing your own time effectively.

7. If you are unable to hand in your assignment on time and have valid reasons such as illness, you may

apply (in writing) for an extension.

8. Failure to achieve at least PASS criteria will result in a REFERRAL grade .

1. A Cover page or title page – You should always attach a title page to your assignment. Use previous

page as your cover sheet and make sure all the details are accurately filled.

2. Attach this brief as the first section of your assignment.

3. All the assignments should be prepared using a word processing software.

4. All the assignments should be printed on A4 sized papers. Use single side printing.

5. Allow 1” for top, bottom , right margins and 1.25” for the left margin of each page.

Word Processing Rules

1. The font size should be 12 point, and should be in the style of Time New Roman.

2. Use 1.5 line spacing. Left justify all paragraphs.

3. Ensure that all the headings are consistent in terms of the font size and font style.

4. Use footer function in the word processor to insert Your Name, Subject, Assignment No, and

Page Number on each page. This is useful if individual sheets become detached for any reason.

5. Use word processing application spell check and grammar check function to help editing your

assignment.

Important Points:

1. It is strictly prohibited to use textboxes to add texts in the assignments, except for the compulsory

information. eg: Figures, tables of comparison etc. Adding text boxes in the body except for the

before mentioned compulsory information will result in rejection of your work.

2. Avoid using page borders in your assignment body.

3. Carefully check the hand in date and the instructions given in the assignment. Late submissions will

not be accepted.

4. Ensure that you give yourself enough time to complete the assignment by the due date.

5. Excuses of any nature will not be accepted for failure to hand in the work on time.

6. You must take responsibility for managing your own time effectively.

7. If you are unable to hand in your assignment on time and have valid reasons such as illness, you may

apply (in writing) for an extension.

8. Failure to achieve at least PASS criteria will result in a REFERRAL grade .

9. Non-submission of work without valid reasons will lead to an automatic RE FERRAL. You will

then be asked to complete an alternative assignment.

10. If you use other people’s work or ideas in your assignment, reference them properly using

HARVARD referencing system to avoid plagiarism. You have to provide both in-text citation and a

reference list.

11. If you are proven to be guilty of plagiarism or any academic misconduct, your grade could be

reduced to A REFERRAL or at worst you could be expelled from the course

then be asked to complete an alternative assignment.

10. If you use other people’s work or ideas in your assignment, reference them properly using

HARVARD referencing system to avoid plagiarism. You have to provide both in-text citation and a

reference list.

11. If you are proven to be guilty of plagiarism or any academic misconduct, your grade could be

reduced to A REFERRAL or at worst you could be expelled from the course

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Student Declaration

I hereby, declare that I know what plagiarism entails, namely to use another’s work and to present it as my own

without attributing the sources in the correct way. I further understand what it means to copy another’s work.

1. I know that plagiarism is a punishable offence because it constitutes theft.

2. I understand the plagiarism and copying policy of the Edexcel UK.

3. I know what the consequences will be if I plagiaries or copy another’s work in any of the assignments for this

program.

4. I declare therefore that all work presented by me for every aspect of my program, will be my own, and where I

have made use of another’s work, I will attribute the source in the correct way.

5. I acknowledge that the attachment of this document signed or not, constitutes a binding agreement between

myself and Edexcel UK.

6. I understand that my assignment will not be considered as submitted if this document is not attached to the

attached.

Student’s Signature: Date: 18/12/2022

(ms.shone01@gmail.com) (18/12/2022)

I hereby, declare that I know what plagiarism entails, namely to use another’s work and to present it as my own

without attributing the sources in the correct way. I further understand what it means to copy another’s work.

1. I know that plagiarism is a punishable offence because it constitutes theft.

2. I understand the plagiarism and copying policy of the Edexcel UK.

3. I know what the consequences will be if I plagiaries or copy another’s work in any of the assignments for this

program.

4. I declare therefore that all work presented by me for every aspect of my program, will be my own, and where I

have made use of another’s work, I will attribute the source in the correct way.

5. I acknowledge that the attachment of this document signed or not, constitutes a binding agreement between

myself and Edexcel UK.

6. I understand that my assignment will not be considered as submitted if this document is not attached to the

attached.

Student’s Signature: Date: 18/12/2022

(ms.shone01@gmail.com) (18/12/2022)

Higher National Certificate/Diploma in Business

Assignment Brief

Student Name /ID Number

Unit Number and Title Unit 5: Accounting Principles

Academic Year

Unit Tutor

Assignment Title Accounting in Context and Budgetary Control and Production and

Interpretation of Financial Statements

Issue Date

Submission Date

IV Name & Date

Submission format

The submission is in the form of a portfolio of evidence compiled from the evidence produced for two

assignments that include the following.

Section A

A blog that should make use of headings, sub-sections, columns and appropriate business-related images and

illustrations. This format offers the opportunity to present academic and theoretical information in a practical,

contextualised and creatively written way. The recommended word limit for the case study is 1,500–2,000 words,

although you will not be penalised for going under or exceeding the total word limit. All work must be supported

with research and referenced correctly using the Harvard referencing system (or alternative referencing system).

You will need to provide a bibliography using the Harvard referencing system (or an alternative referencing

system). Inaccurate use of referencing may lead to issues of plagiarism if not applied correctly.

Section B

You will also submit budget reports (Sales budget, Production budget & Cash budget) with

relevantinterpretations. You will insert sections of your spreadsheet into the memorandum. The recommended

word limit for the memorandum is 1,000–1,500 words, although you will not be penalised for going under or

exceeding the total word limit. Referencing for both submissions should use the Harvard system (or an alternative

system).

Assignment Brief

Student Name /ID Number

Unit Number and Title Unit 5: Accounting Principles

Academic Year

Unit Tutor

Assignment Title Accounting in Context and Budgetary Control and Production and

Interpretation of Financial Statements

Issue Date

Submission Date

IV Name & Date

Submission format

The submission is in the form of a portfolio of evidence compiled from the evidence produced for two

assignments that include the following.

Section A

A blog that should make use of headings, sub-sections, columns and appropriate business-related images and

illustrations. This format offers the opportunity to present academic and theoretical information in a practical,

contextualised and creatively written way. The recommended word limit for the case study is 1,500–2,000 words,

although you will not be penalised for going under or exceeding the total word limit. All work must be supported

with research and referenced correctly using the Harvard referencing system (or alternative referencing system).

You will need to provide a bibliography using the Harvard referencing system (or an alternative referencing

system). Inaccurate use of referencing may lead to issues of plagiarism if not applied correctly.

Section B

You will also submit budget reports (Sales budget, Production budget & Cash budget) with

relevantinterpretations. You will insert sections of your spreadsheet into the memorandum. The recommended

word limit for the memorandum is 1,000–1,500 words, although you will not be penalised for going under or

exceeding the total word limit. Referencing for both submissions should use the Harvard system (or an alternative

system).

The submission is in the form of a portfolio of evidence compiled from the evidence produced for two

assignments that include the following.

Section C

A constructed set of financial statements (income statement and statement of financial position) for the business

in question. The word count is 2,000–2,500 words, although you will not be penalised for going under or

exceeding the total word limit. A bibliography should be provided using the Harvard referencing system (or an

alternative system). Inaccurate use of referencing may lead to issues of plagiarism if not applied correctly.

Section D

A detailed letter to a named client. The letter must be clear worded, well-structured and should make use of

appropriate business language and terminology. The letter can also include clearly labelled tables and charts.

The word count is 2,000–2,500 words, although you will not be penalised for going under or exceeding the total

word limit. A bibliography should be provided using the Harvard referencing system (or an alternative system).

Inaccurate use of referencing may lead to issues of plagiarism if not applied correctly.

Unit Learning Outcomes:

LO1 Examine the context and purpose of accounting.

LO4 Prepare budgets for planning, control and decision-making using spreadsheets.

LO2 Prepare basic financial statements for unincorporated and small business organisations inaccordance with

accounting principles, conventions, and standards.

LO3 Interpret financial statements.

Learning Outcomes and Assessment Criteria

Pass Merit Distinction

LO1 Examine the context and purpose of accounting

P1 Examine the purpose of

the accounting function

within an organisation. M1 Evaluate the context and

purpose of the accounting

function in meeting

organisational, stakeholder

and societal needs and

expectations.

D1 Critically evaluate the role of

accounting in informing decision making

to meet organisational, stakeholder and

societal needs within complex operating

environments.

P2 Assess the accounting

function within the

organisation in the context of

regulatory and ethical

constraints.

LO4 Prepare budgets for planning, control and decision- D3 Justify budgetary control solutions

assignments that include the following.

Section C

A constructed set of financial statements (income statement and statement of financial position) for the business

in question. The word count is 2,000–2,500 words, although you will not be penalised for going under or

exceeding the total word limit. A bibliography should be provided using the Harvard referencing system (or an

alternative system). Inaccurate use of referencing may lead to issues of plagiarism if not applied correctly.

Section D

A detailed letter to a named client. The letter must be clear worded, well-structured and should make use of

appropriate business language and terminology. The letter can also include clearly labelled tables and charts.

The word count is 2,000–2,500 words, although you will not be penalised for going under or exceeding the total

word limit. A bibliography should be provided using the Harvard referencing system (or an alternative system).

Inaccurate use of referencing may lead to issues of plagiarism if not applied correctly.

Unit Learning Outcomes:

LO1 Examine the context and purpose of accounting.

LO4 Prepare budgets for planning, control and decision-making using spreadsheets.

LO2 Prepare basic financial statements for unincorporated and small business organisations inaccordance with

accounting principles, conventions, and standards.

LO3 Interpret financial statements.

Learning Outcomes and Assessment Criteria

Pass Merit Distinction

LO1 Examine the context and purpose of accounting

P1 Examine the purpose of

the accounting function

within an organisation. M1 Evaluate the context and

purpose of the accounting

function in meeting

organisational, stakeholder

and societal needs and

expectations.

D1 Critically evaluate the role of

accounting in informing decision making

to meet organisational, stakeholder and

societal needs within complex operating

environments.

P2 Assess the accounting

function within the

organisation in the context of

regulatory and ethical

constraints.

LO4 Prepare budgets for planning, control and decision- D3 Justify budgetary control solutions

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

making using spreadsheets.

and their impact on organisational

decision making to ensure efficient and

effective deployment of resources.

P6 Prepare a cash budget

from given data for an

organisation using a

spreadsheet.

M4 Identify corrective actions

to problems revealed by

budgetary planning and

control for effective

organisational decision

making.

P7 Discuss the benefits and

limitations of budgets and

budgetary planning, and

control for an organisation.

Pass Merit Distinction

LO2 Prepare basic financial statements for unincorporated and

small business organisations in accordance with accounting

principles, conventions, and standards.

D2 Critically evaluate financial

statements to assess organisational

performance using a range of measures

and benchmarks to make justified

conclusions.

P3 Prepare financial

statements from a given trial

balance for sole traders,

partnerships and not-for-

profit organisations, to meet

accounting principles,

conventions and standards.

M2 Produce financial

statements from a given trial

balance, making appropriate

adjustments.

LO3 Interpret financial statements.

P4 Calculate and present

financial ratios from a set of

final accounts.

M3 Evaluate the performance

of an organisation over time,

using financial ratios with

reference to relevant

benchmarks.

P5 Compare the performance

of an organisation over time

using financial ratios.

and their impact on organisational

decision making to ensure efficient and

effective deployment of resources.

P6 Prepare a cash budget

from given data for an

organisation using a

spreadsheet.

M4 Identify corrective actions

to problems revealed by

budgetary planning and

control for effective

organisational decision

making.

P7 Discuss the benefits and

limitations of budgets and

budgetary planning, and

control for an organisation.

Pass Merit Distinction

LO2 Prepare basic financial statements for unincorporated and

small business organisations in accordance with accounting

principles, conventions, and standards.

D2 Critically evaluate financial

statements to assess organisational

performance using a range of measures

and benchmarks to make justified

conclusions.

P3 Prepare financial

statements from a given trial

balance for sole traders,

partnerships and not-for-

profit organisations, to meet

accounting principles,

conventions and standards.

M2 Produce financial

statements from a given trial

balance, making appropriate

adjustments.

LO3 Interpret financial statements.

P4 Calculate and present

financial ratios from a set of

final accounts.

M3 Evaluate the performance

of an organisation over time,

using financial ratios with

reference to relevant

benchmarks.

P5 Compare the performance

of an organisation over time

using financial ratios.

Assignment Brief and Guidance:

Section A

Your supervisor, one of the firm’s Key Account Managers, has asked you to prepare a blog that

will be used to market and promote its accounting services to new and existing clients. The

working title you have been given for the blog is ‘The role of accounting in an organisation’. The

blog must be presented as an online blog in an engaging and practical way, covering relevant

academic theory, making use of, for example, headings, images and illustrations. Your blog

should include the following, but is not limited to:

the purpose and scope of accounting in complex operating environments

a critical evaluation of the accounting function in informing decision making and

meeting stakeholder and societal needs and expectations

the main branches of accounting and job skillsets and competencies

accounting systems and the role of technology in modern-day accounting

issues of ethics, regulation and compliance and the extent to which they are

constraints or threats to the organisation.

Section B

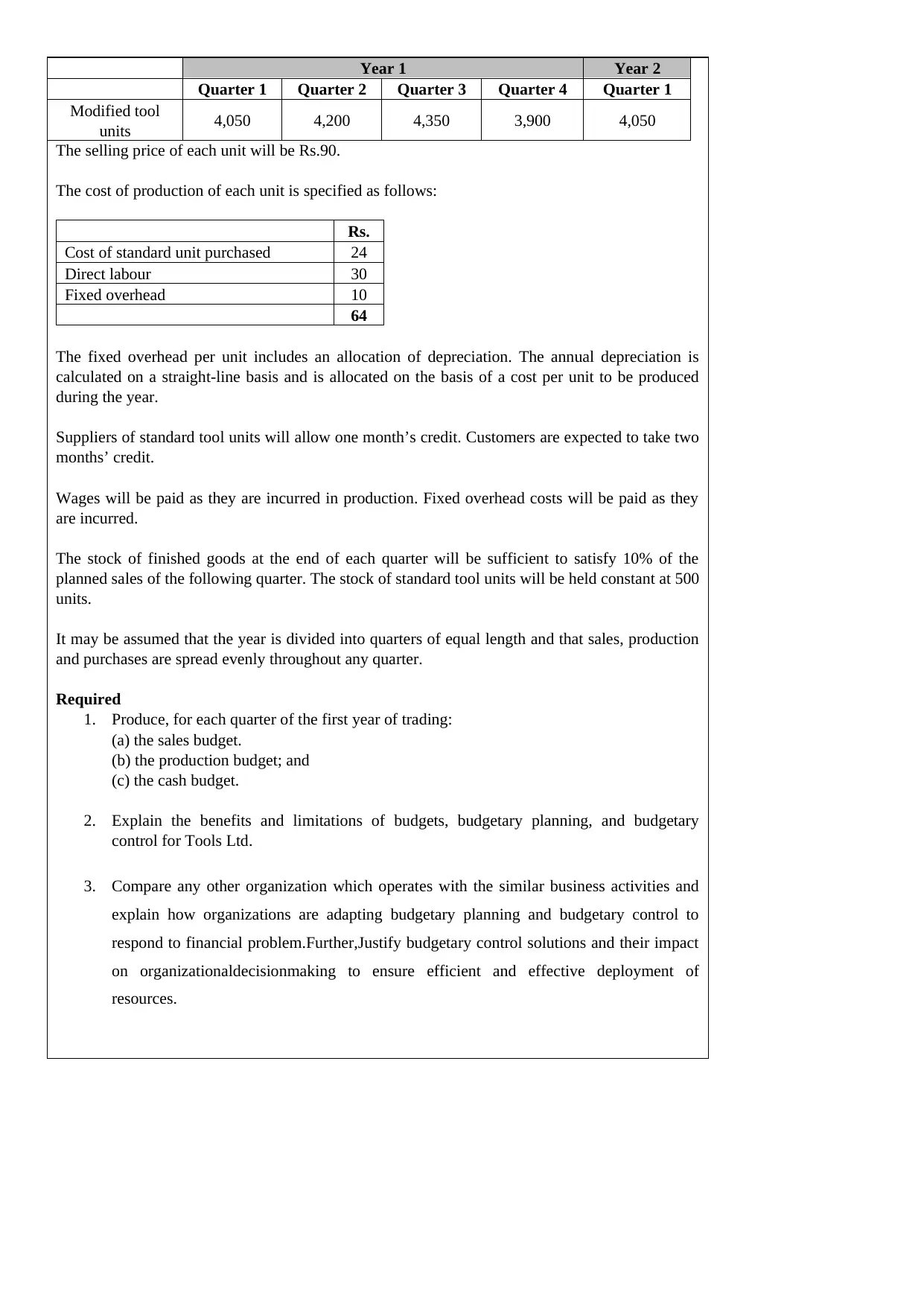

Tools Ltd is a new business which has been formed to buy standard machine tool units and adapt

them to the specific needs of customers.

The business will acquire fixed assets costing Rs.100,000 and a stock of 500 standard tool units on

the first day of business. The fixed assets are expected to have a five-year life with no residual

value at the end of that time.

Sales are forecast as follows:

Section A

Your supervisor, one of the firm’s Key Account Managers, has asked you to prepare a blog that

will be used to market and promote its accounting services to new and existing clients. The

working title you have been given for the blog is ‘The role of accounting in an organisation’. The

blog must be presented as an online blog in an engaging and practical way, covering relevant

academic theory, making use of, for example, headings, images and illustrations. Your blog

should include the following, but is not limited to:

the purpose and scope of accounting in complex operating environments

a critical evaluation of the accounting function in informing decision making and

meeting stakeholder and societal needs and expectations

the main branches of accounting and job skillsets and competencies

accounting systems and the role of technology in modern-day accounting

issues of ethics, regulation and compliance and the extent to which they are

constraints or threats to the organisation.

Section B

Tools Ltd is a new business which has been formed to buy standard machine tool units and adapt

them to the specific needs of customers.

The business will acquire fixed assets costing Rs.100,000 and a stock of 500 standard tool units on

the first day of business. The fixed assets are expected to have a five-year life with no residual

value at the end of that time.

Sales are forecast as follows:

The selling price of each unit will be Rs.90.

The cost of production of each unit is specified as follows:

Rs.

Cost of standard unit purchased 24

Direct labour 30

Fixed overhead 10

64

The fixed overhead per unit includes an allocation of depreciation. The annual depreciation is

calculated on a straight-line basis and is allocated on the basis of a cost per unit to be produced

during the year.

Suppliers of standard tool units will allow one month’s credit. Customers are expected to take two

months’ credit.

Wages will be paid as they are incurred in production. Fixed overhead costs will be paid as they

are incurred.

The stock of finished goods at the end of each quarter will be sufficient to satisfy 10% of the

planned sales of the following quarter. The stock of standard tool units will be held constant at 500

units.

It may be assumed that the year is divided into quarters of equal length and that sales, production

and purchases are spread evenly throughout any quarter.

Required

1. Produce, for each quarter of the first year of trading:

(a) the sales budget.

(b) the production budget; and

(c) the cash budget.

2. Explain the benefits and limitations of budgets, budgetary planning, and budgetary

control for Tools Ltd.

3. Compare any other organization which operates with the similar business activities and

explain how organizations are adapting budgetary planning and budgetary control to

respond to financial problem.Further,Justify budgetary control solutions and their impact

on organizationaldecisionmaking to ensure efficient and effective deployment of

resources.

Year 1 Year 2

Quarter 1 Quarter 2 Quarter 3 Quarter 4 Quarter 1

Modified tool

units 4,050 4,200 4,350 3,900 4,050

The cost of production of each unit is specified as follows:

Rs.

Cost of standard unit purchased 24

Direct labour 30

Fixed overhead 10

64

The fixed overhead per unit includes an allocation of depreciation. The annual depreciation is

calculated on a straight-line basis and is allocated on the basis of a cost per unit to be produced

during the year.

Suppliers of standard tool units will allow one month’s credit. Customers are expected to take two

months’ credit.

Wages will be paid as they are incurred in production. Fixed overhead costs will be paid as they

are incurred.

The stock of finished goods at the end of each quarter will be sufficient to satisfy 10% of the

planned sales of the following quarter. The stock of standard tool units will be held constant at 500

units.

It may be assumed that the year is divided into quarters of equal length and that sales, production

and purchases are spread evenly throughout any quarter.

Required

1. Produce, for each quarter of the first year of trading:

(a) the sales budget.

(b) the production budget; and

(c) the cash budget.

2. Explain the benefits and limitations of budgets, budgetary planning, and budgetary

control for Tools Ltd.

3. Compare any other organization which operates with the similar business activities and

explain how organizations are adapting budgetary planning and budgetary control to

respond to financial problem.Further,Justify budgetary control solutions and their impact

on organizationaldecisionmaking to ensure efficient and effective deployment of

resources.

Year 1 Year 2

Quarter 1 Quarter 2 Quarter 3 Quarter 4 Quarter 1

Modified tool

units 4,050 4,200 4,350 3,900 4,050

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Section C

a. Prepare final accounts for sloe traders, partnerships and limited companies in according with

appropriate principles, conventions and standards. (Please refer the excel sheet forrequired

information).

b. Prepare Cash flow statement of Ruba PLC. Find the cash balance for the year ended by using

relevant accounting formats. (Please refer the excel sheet for required information).

c. Compare the essential features of each financial statement (Complete set of Financial

Statements) to analyse the differences between them in terms of purpose, structure, content

Etc.

Section D

These local businesses do not make use of contemporary software to support its book-keeping and

accounting function. This is something which concerns you as you feel that it represents an

opportunity for the business to save time and resource. Your supervisor, one of the firm’s Key

Account Managers, has asked you to compile the year-end financial statements ready for

submission and provide, for your client. You should prepare some detailed analysis of the figures

produced, which will be presented in the form of a letter.

a. Calculate and interpret following ratios from the given information in the excel sheet.

Investor ratios

Liquidity ratios

Leverage ratios

Profitability ratios

b. critically evaluate the performance to the business year on year (making reference to data you

have calculated, and data provided from the previous year), with reference to relevant

benchmarks as well as any limitations of using financial ratios as performance measures with

a justified conclusions and recommendations for your client.

the

a. Prepare final accounts for sloe traders, partnerships and limited companies in according with

appropriate principles, conventions and standards. (Please refer the excel sheet forrequired

information).

b. Prepare Cash flow statement of Ruba PLC. Find the cash balance for the year ended by using

relevant accounting formats. (Please refer the excel sheet for required information).

c. Compare the essential features of each financial statement (Complete set of Financial

Statements) to analyse the differences between them in terms of purpose, structure, content

Etc.

Section D

These local businesses do not make use of contemporary software to support its book-keeping and

accounting function. This is something which concerns you as you feel that it represents an

opportunity for the business to save time and resource. Your supervisor, one of the firm’s Key

Account Managers, has asked you to compile the year-end financial statements ready for

submission and provide, for your client. You should prepare some detailed analysis of the figures

produced, which will be presented in the form of a letter.

a. Calculate and interpret following ratios from the given information in the excel sheet.

Investor ratios

Liquidity ratios

Leverage ratios

Profitability ratios

b. critically evaluate the performance to the business year on year (making reference to data you

have calculated, and data provided from the previous year), with reference to relevant

benchmarks as well as any limitations of using financial ratios as performance measures with

a justified conclusions and recommendations for your client.

the

Grading Rubric

Grading Criteria Achieved Feedback

P1 Examine the purpose of the accounting

function within an organisation.

P2 Assess the accounting function within

the organisation in the context of

regulatory and ethical constraints.

P6 Prepare a cash budget from given data

for an organisation using a spreadsheet.

P7 Discuss the benefits and limitations of

budgets and budgetary planning, and

control for an organisation.

M1 Evaluate the context and purpose of

the accounting function in meeting

organisational, stakeholder and societal

needs and expectations.

M4 Identify corrective actions to

problems revealed by budgetary planning

and control for effective organisational

decision making.

D1 Critically evaluate the role of

accounting in informing decision making

to meet organisational, stakeholder and

societal needs within complex operating

environments.

Grading Criteria Achieved Feedback

P1 Examine the purpose of the accounting

function within an organisation.

P2 Assess the accounting function within

the organisation in the context of

regulatory and ethical constraints.

P6 Prepare a cash budget from given data

for an organisation using a spreadsheet.

P7 Discuss the benefits and limitations of

budgets and budgetary planning, and

control for an organisation.

M1 Evaluate the context and purpose of

the accounting function in meeting

organisational, stakeholder and societal

needs and expectations.

M4 Identify corrective actions to

problems revealed by budgetary planning

and control for effective organisational

decision making.

D1 Critically evaluate the role of

accounting in informing decision making

to meet organisational, stakeholder and

societal needs within complex operating

environments.

D3 Justify budgetary control solutions and

their impact on organisational decision

making to ensure efficient and effective

deployment of resources.

P3Prepare financial statements from a given

trial balance for sole traders, partnerships

and not-for-profit organisations, to meet

accounting principles, conventions and

standards.

P4 Calculate and present financial ratios

from a set of final accounts.

P5 Compare the performance of an

organisation over time using financial ratios.

M2 Produce financial statements from a

given trial balance, making appropriate

adjustments.

M3 Evaluate the performance of an

organisation over time, using financial ratios

with reference to relevant benchmarks.

D2 Critically evaluate financial statements

to assess organisational performance using a

range of measures and benchmarks to make

justified conclusions.

their impact on organisational decision

making to ensure efficient and effective

deployment of resources.

P3Prepare financial statements from a given

trial balance for sole traders, partnerships

and not-for-profit organisations, to meet

accounting principles, conventions and

standards.

P4 Calculate and present financial ratios

from a set of final accounts.

P5 Compare the performance of an

organisation over time using financial ratios.

M2 Produce financial statements from a

given trial balance, making appropriate

adjustments.

M3 Evaluate the performance of an

organisation over time, using financial ratios

with reference to relevant benchmarks.

D2 Critically evaluate financial statements

to assess organisational performance using a

range of measures and benchmarks to make

justified conclusions.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

PART – A

The link for the block is attached below:

https://shonemahen.blogspot.com/2022/11/the-role-of-accounting-in-organization.html

The link for the block is attached below:

https://shonemahen.blogspot.com/2022/11/the-role-of-accounting-in-organization.html

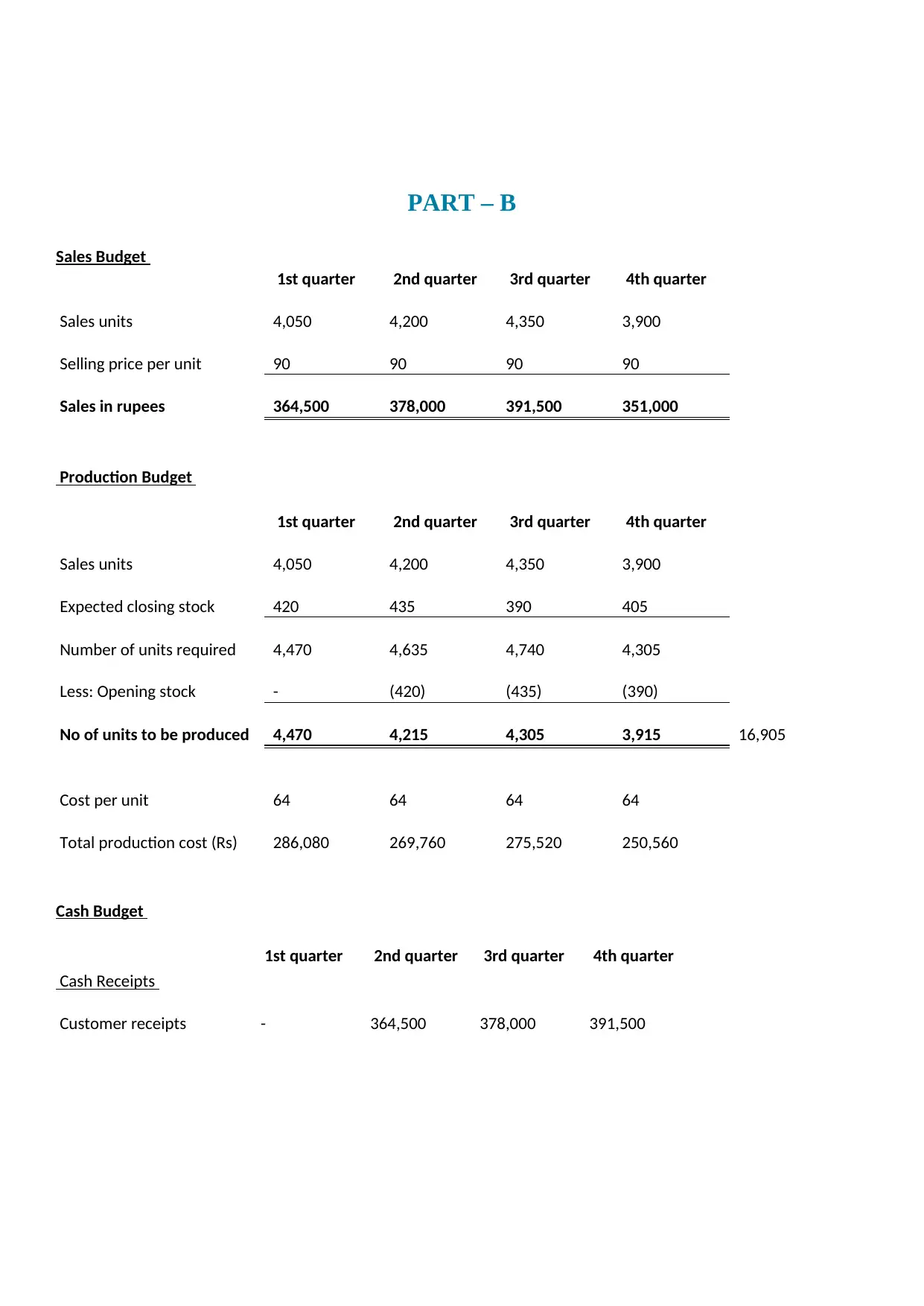

PART – B

Sales Budget

1st quarter 2nd quarter 3rd quarter 4th quarter

Sales units 4,050 4,200 4,350 3,900

Selling price per unit 90 90 90 90

Sales in rupees 364,500 378,000 391,500 351,000

Production Budget

1st quarter 2nd quarter 3rd quarter 4th quarter

Sales units 4,050 4,200 4,350 3,900

Expected closing stock 420 435 390 405

Number of units required 4,470 4,635 4,740 4,305

Less: Opening stock - (420) (435) (390)

No of units to be produced 4,470 4,215 4,305 3,915 16,905

Cost per unit 64 64 64 64

Total production cost (Rs) 286,080 269,760 275,520 250,560

Cash Budget

1st quarter 2nd quarter 3rd quarter 4th quarter

Cash Receipts

Customer receipts - 364,500 378,000 391,500

Sales Budget

1st quarter 2nd quarter 3rd quarter 4th quarter

Sales units 4,050 4,200 4,350 3,900

Selling price per unit 90 90 90 90

Sales in rupees 364,500 378,000 391,500 351,000

Production Budget

1st quarter 2nd quarter 3rd quarter 4th quarter

Sales units 4,050 4,200 4,350 3,900

Expected closing stock 420 435 390 405

Number of units required 4,470 4,635 4,740 4,305

Less: Opening stock - (420) (435) (390)

No of units to be produced 4,470 4,215 4,305 3,915 16,905

Cost per unit 64 64 64 64

Total production cost (Rs) 286,080 269,760 275,520 250,560

Cash Budget

1st quarter 2nd quarter 3rd quarter 4th quarter

Cash Receipts

Customer receipts - 364,500 378,000 391,500

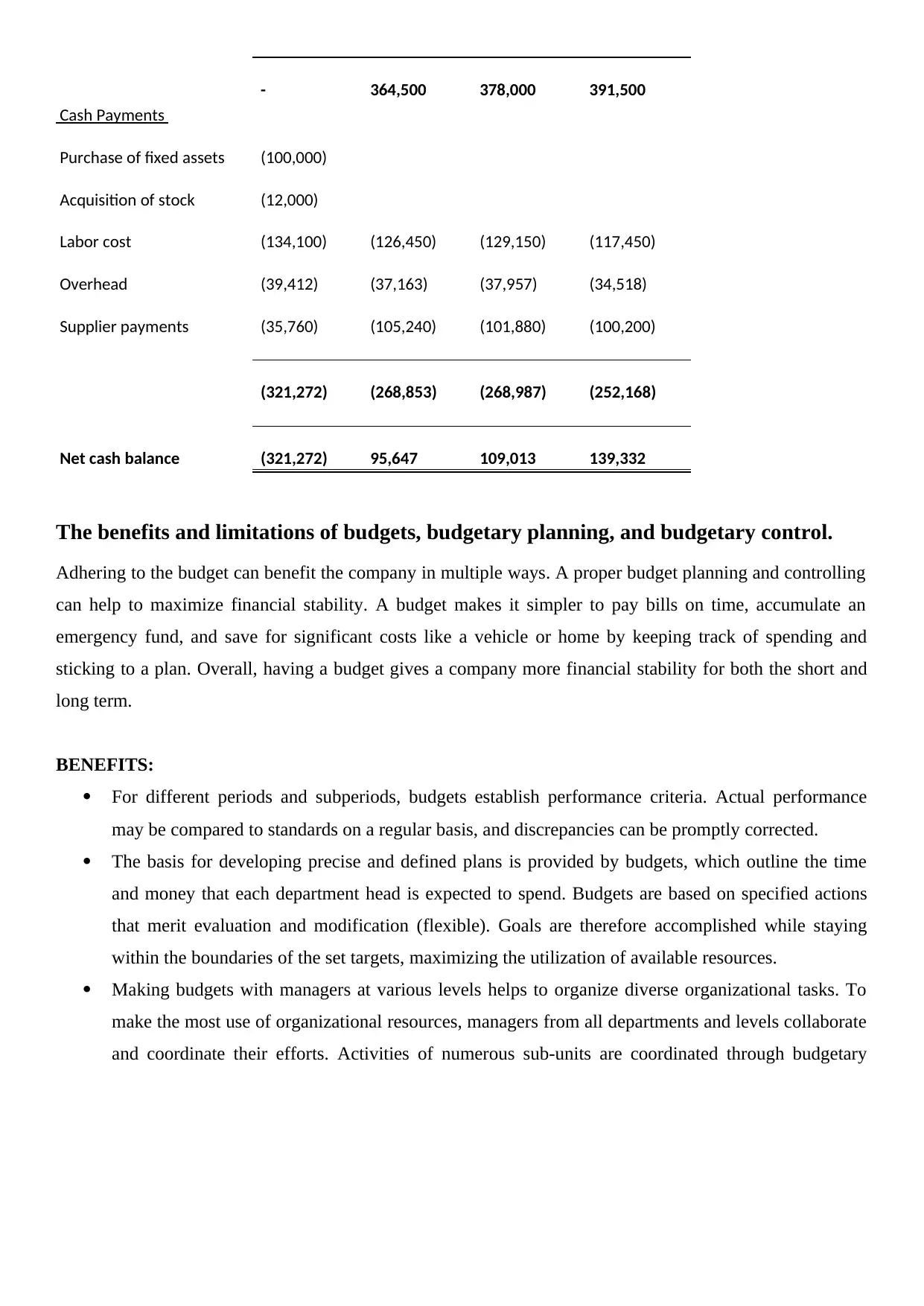

- 364,500 378,000 391,500

Cash Payments

Purchase of fixed assets (100,000)

Acquisition of stock (12,000)

Labor cost (134,100) (126,450) (129,150) (117,450)

Overhead (39,412) (37,163) (37,957) (34,518)

Supplier payments (35,760) (105,240) (101,880) (100,200)

(321,272) (268,853) (268,987) (252,168)

Net cash balance (321,272) 95,647 109,013 139,332

The benefits and limitations of budgets, budgetary planning, and budgetary control.

Adhering to the budget can benefit the company in multiple ways. A proper budget planning and controlling

can help to maximize financial stability. A budget makes it simpler to pay bills on time, accumulate an

emergency fund, and save for significant costs like a vehicle or home by keeping track of spending and

sticking to a plan. Overall, having a budget gives a company more financial stability for both the short and

long term.

BENEFITS:

For different periods and subperiods, budgets establish performance criteria. Actual performance

may be compared to standards on a regular basis, and discrepancies can be promptly corrected.

The basis for developing precise and defined plans is provided by budgets, which outline the time

and money that each department head is expected to spend. Budgets are based on specified actions

that merit evaluation and modification (flexible). Goals are therefore accomplished while staying

within the boundaries of the set targets, maximizing the utilization of available resources.

Making budgets with managers at various levels helps to organize diverse organizational tasks. To

make the most use of organizational resources, managers from all departments and levels collaborate

and coordinate their efforts. Activities of numerous sub-units are coordinated through budgetary

Cash Payments

Purchase of fixed assets (100,000)

Acquisition of stock (12,000)

Labor cost (134,100) (126,450) (129,150) (117,450)

Overhead (39,412) (37,163) (37,957) (34,518)

Supplier payments (35,760) (105,240) (101,880) (100,200)

(321,272) (268,853) (268,987) (252,168)

Net cash balance (321,272) 95,647 109,013 139,332

The benefits and limitations of budgets, budgetary planning, and budgetary control.

Adhering to the budget can benefit the company in multiple ways. A proper budget planning and controlling

can help to maximize financial stability. A budget makes it simpler to pay bills on time, accumulate an

emergency fund, and save for significant costs like a vehicle or home by keeping track of spending and

sticking to a plan. Overall, having a budget gives a company more financial stability for both the short and

long term.

BENEFITS:

For different periods and subperiods, budgets establish performance criteria. Actual performance

may be compared to standards on a regular basis, and discrepancies can be promptly corrected.

The basis for developing precise and defined plans is provided by budgets, which outline the time

and money that each department head is expected to spend. Budgets are based on specified actions

that merit evaluation and modification (flexible). Goals are therefore accomplished while staying

within the boundaries of the set targets, maximizing the utilization of available resources.

Making budgets with managers at various levels helps to organize diverse organizational tasks. To

make the most use of organizational resources, managers from all departments and levels collaborate

and coordinate their efforts. Activities of numerous sub-units are coordinated through budgetary

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

control to bring them closer to organization's goals. As example, the budget for sales must be linked

with the budget for purchases, which must then be coordinated with the budget for labour. This

necessitates open communication between the various departments, which makes coordination

easier.

Budgets outline who is responsible for spending money when, where, and how, as well as any

potential revenue-generating sectors. Financial forecasts assist top managers in granting power to

subordinates to complete budgeted tasks within the parameters anticipated in the budget.

A way to detect departures from the expected performance is provided by budgets, which compare

departmental and individual performance to benchmarks. In order to correct irregularities and

identify their causes to prevent recurrence, managers can take appropriate measures. This gives

organizational activity, direction under regulated circumstances.

LIMITATIONS:

Budgets emphasize future expectations, but they also have the influence of past activities. Events that

weren't relevant in the past might not be included in budgets in the future even if they turn out to be

relevant over time. Making zero-base budgeting, where significant activities are examined for each

budgeted period and included in the budgets, is another way to solve this issue.

Managers may disregard organizational goals in order to stay within the parameters of budgeted

goals and achieve budgeted goals at the expense of organizational goals.

The prospect of innovation and change may be impeded when funds are allocated to various

operational budgets because it may not be able to secure extra funding and resources to take

advantage of environmental opportunities.

Budgetary allocations must be changed since they are based on forecasts of the future, thus they will

need to be adjusted if the events do not occur as expected. Therefore, future uncertainties may have

an impact on how reliable budgets are. This does not, however, minimize the significance of

budgets.

How other organizations are adhering to the budget planning and budgetary control.

with the budget for purchases, which must then be coordinated with the budget for labour. This

necessitates open communication between the various departments, which makes coordination

easier.

Budgets outline who is responsible for spending money when, where, and how, as well as any

potential revenue-generating sectors. Financial forecasts assist top managers in granting power to

subordinates to complete budgeted tasks within the parameters anticipated in the budget.

A way to detect departures from the expected performance is provided by budgets, which compare

departmental and individual performance to benchmarks. In order to correct irregularities and

identify their causes to prevent recurrence, managers can take appropriate measures. This gives

organizational activity, direction under regulated circumstances.

LIMITATIONS:

Budgets emphasize future expectations, but they also have the influence of past activities. Events that

weren't relevant in the past might not be included in budgets in the future even if they turn out to be

relevant over time. Making zero-base budgeting, where significant activities are examined for each

budgeted period and included in the budgets, is another way to solve this issue.

Managers may disregard organizational goals in order to stay within the parameters of budgeted

goals and achieve budgeted goals at the expense of organizational goals.

The prospect of innovation and change may be impeded when funds are allocated to various

operational budgets because it may not be able to secure extra funding and resources to take

advantage of environmental opportunities.

Budgetary allocations must be changed since they are based on forecasts of the future, thus they will

need to be adjusted if the events do not occur as expected. Therefore, future uncertainties may have

an impact on how reliable budgets are. This does not, however, minimize the significance of

budgets.

How other organizations are adhering to the budget planning and budgetary control.

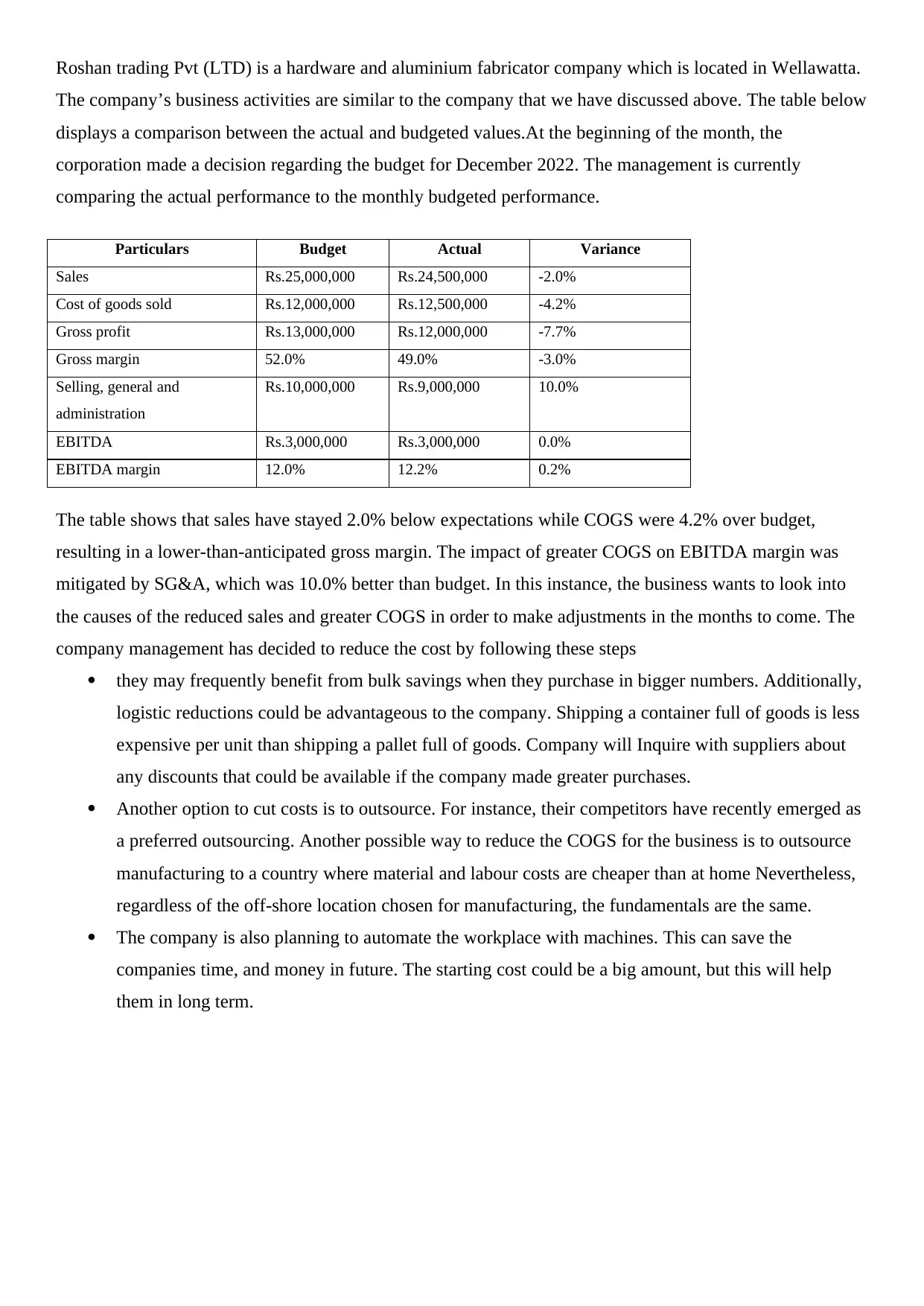

Roshan trading Pvt (LTD) is a hardware and aluminium fabricator company which is located in Wellawatta.

The company’s business activities are similar to the company that we have discussed above. The table below

displays a comparison between the actual and budgeted values.At the beginning of the month, the

corporation made a decision regarding the budget for December 2022. The management is currently

comparing the actual performance to the monthly budgeted performance.

Particulars Budget Actual Variance

Sales Rs.25,000,000 Rs.24,500,000 -2.0%

Cost of goods sold Rs.12,000,000 Rs.12,500,000 -4.2%

Gross profit Rs.13,000,000 Rs.12,000,000 -7.7%

Gross margin 52.0% 49.0% -3.0%

Selling, general and

administration

Rs.10,000,000 Rs.9,000,000 10.0%

EBITDA Rs.3,000,000 Rs.3,000,000 0.0%

EBITDA margin 12.0% 12.2% 0.2%

The table shows that sales have stayed 2.0% below expectations while COGS were 4.2% over budget,

resulting in a lower-than-anticipated gross margin. The impact of greater COGS on EBITDA margin was

mitigated by SG&A, which was 10.0% better than budget. In this instance, the business wants to look into

the causes of the reduced sales and greater COGS in order to make adjustments in the months to come. The

company management has decided to reduce the cost by following these steps

they may frequently benefit from bulk savings when they purchase in bigger numbers. Additionally,

logistic reductions could be advantageous to the company. Shipping a container full of goods is less

expensive per unit than shipping a pallet full of goods. Company will Inquire with suppliers about

any discounts that could be available if the company made greater purchases.

Another option to cut costs is to outsource. For instance, their competitors have recently emerged as

a preferred outsourcing. Another possible way to reduce the COGS for the business is to outsource

manufacturing to a country where material and labour costs are cheaper than at home Nevertheless,

regardless of the off-shore location chosen for manufacturing, the fundamentals are the same.

The company is also planning to automate the workplace with machines. This can save the

companies time, and money in future. The starting cost could be a big amount, but this will help

them in long term.

The company’s business activities are similar to the company that we have discussed above. The table below

displays a comparison between the actual and budgeted values.At the beginning of the month, the

corporation made a decision regarding the budget for December 2022. The management is currently

comparing the actual performance to the monthly budgeted performance.

Particulars Budget Actual Variance

Sales Rs.25,000,000 Rs.24,500,000 -2.0%

Cost of goods sold Rs.12,000,000 Rs.12,500,000 -4.2%

Gross profit Rs.13,000,000 Rs.12,000,000 -7.7%

Gross margin 52.0% 49.0% -3.0%

Selling, general and

administration

Rs.10,000,000 Rs.9,000,000 10.0%

EBITDA Rs.3,000,000 Rs.3,000,000 0.0%

EBITDA margin 12.0% 12.2% 0.2%

The table shows that sales have stayed 2.0% below expectations while COGS were 4.2% over budget,

resulting in a lower-than-anticipated gross margin. The impact of greater COGS on EBITDA margin was

mitigated by SG&A, which was 10.0% better than budget. In this instance, the business wants to look into

the causes of the reduced sales and greater COGS in order to make adjustments in the months to come. The

company management has decided to reduce the cost by following these steps

they may frequently benefit from bulk savings when they purchase in bigger numbers. Additionally,

logistic reductions could be advantageous to the company. Shipping a container full of goods is less

expensive per unit than shipping a pallet full of goods. Company will Inquire with suppliers about

any discounts that could be available if the company made greater purchases.

Another option to cut costs is to outsource. For instance, their competitors have recently emerged as

a preferred outsourcing. Another possible way to reduce the COGS for the business is to outsource

manufacturing to a country where material and labour costs are cheaper than at home Nevertheless,

regardless of the off-shore location chosen for manufacturing, the fundamentals are the same.

The company is also planning to automate the workplace with machines. This can save the

companies time, and money in future. The starting cost could be a big amount, but this will help

them in long term.

Budgeting is crucial for the success of any business. By sitting down and thinking about the wisest ways to

spend your money, you can create a budget. This procedure is guided by facts and numbers. The overall

budget should be divided into smaller ones. company need one for things like operations costs, revenue,

acquisitions of new property and equipment, marketing, new hires, and production, to name a few. they may

make informed decisions based on a balanced assessment of the requirements of all sections of the

organization by taking a comprehensive look at all of these areas of the firm.The budget provides insight

into a company's performance. Your income serves as the basis of your budget. If you discover that you are

falling short of your income goals and must reduce your spending, this is a sign that you need to focus your

money in a wiser way. To increase income levels, for instance, you can reallocate monies from other budget

categories to marketing and sales.Your budget will reflect growth if it includes plans for expansion as well

as equipment and property acquisitions. Such a budget enables you to concentrate on saving money for

expanding rather than just surviving your organization. Due to your attention being on your future bottom

line as well as your current bottom line, you are better able to make judgments. These are some key points

that could help an organization to make effective decision makings when it comes to budgeting and running

a successful business.

PART – C

Sales 71,000

(-) Cost of sale 7,700

Opening stocks 30,000

Purchases 6,900

spend your money, you can create a budget. This procedure is guided by facts and numbers. The overall

budget should be divided into smaller ones. company need one for things like operations costs, revenue,

acquisitions of new property and equipment, marketing, new hires, and production, to name a few. they may

make informed decisions based on a balanced assessment of the requirements of all sections of the

organization by taking a comprehensive look at all of these areas of the firm.The budget provides insight

into a company's performance. Your income serves as the basis of your budget. If you discover that you are

falling short of your income goals and must reduce your spending, this is a sign that you need to focus your

money in a wiser way. To increase income levels, for instance, you can reallocate monies from other budget

categories to marketing and sales.Your budget will reflect growth if it includes plans for expansion as well

as equipment and property acquisitions. Such a budget enables you to concentrate on saving money for

expanding rather than just surviving your organization. Due to your attention being on your future bottom

line as well as your current bottom line, you are better able to make judgments. These are some key points

that could help an organization to make effective decision makings when it comes to budgeting and running

a successful business.

PART – C

Sales 71,000

(-) Cost of sale 7,700

Opening stocks 30,000

Purchases 6,900

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Closing stocks 30,800

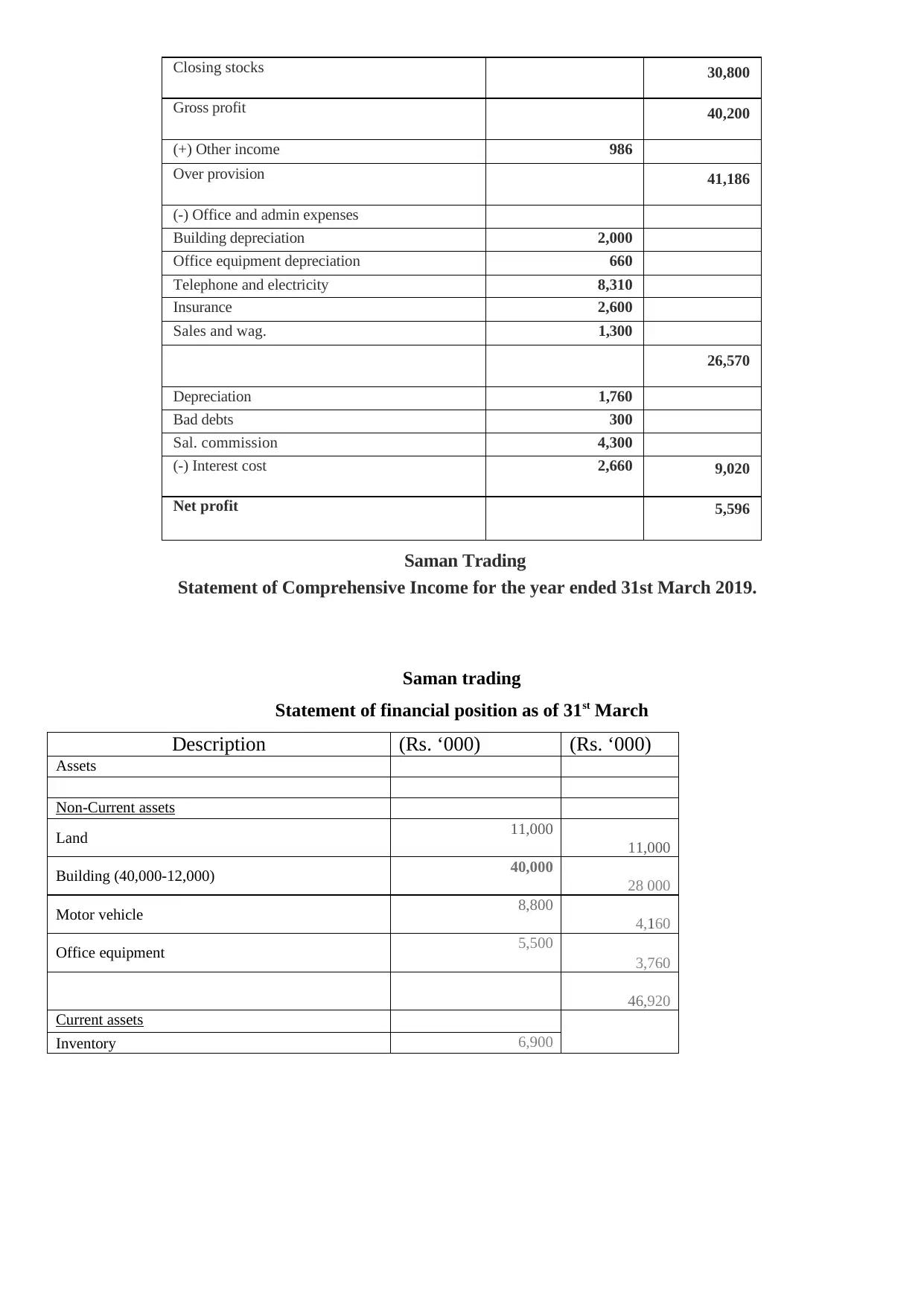

Gross profit 40,200

(+) Other income 986

Over provision 41,186

(-) Office and admin expenses

Building depreciation 2,000

Office equipment depreciation 660

Telephone and electricity 8,310

Insurance 2,600

Sales and wag. 1,300

26,570

Depreciation 1,760

Bad debts 300

Sal. commission 4,300

(-) Interest cost 2,660 9,020

Net profit 5,596

Saman Trading

Statement of Comprehensive Income for the year ended 31st March 2019.

Saman trading

Statement of financial position as of 31st March

Description (Rs. ‘000) (Rs. ‘000)

Assets

Non-Current assets

Land 11,000

11,000

Building (40,000-12,000) 40,000

28 000

Motor vehicle 8,800

4,160

Office equipment 5,500

3,760

46,920

Current assets

Inventory 6,900

Gross profit 40,200

(+) Other income 986

Over provision 41,186

(-) Office and admin expenses

Building depreciation 2,000

Office equipment depreciation 660

Telephone and electricity 8,310

Insurance 2,600

Sales and wag. 1,300

26,570

Depreciation 1,760

Bad debts 300

Sal. commission 4,300

(-) Interest cost 2,660 9,020

Net profit 5,596

Saman Trading

Statement of Comprehensive Income for the year ended 31st March 2019.

Saman trading

Statement of financial position as of 31st March

Description (Rs. ‘000) (Rs. ‘000)

Assets

Non-Current assets

Land 11,000

11,000

Building (40,000-12,000) 40,000

28 000

Motor vehicle 8,800

4,160

Office equipment 5,500

3,760

46,920

Current assets

Inventory 6,900

Trade receivables 12,446

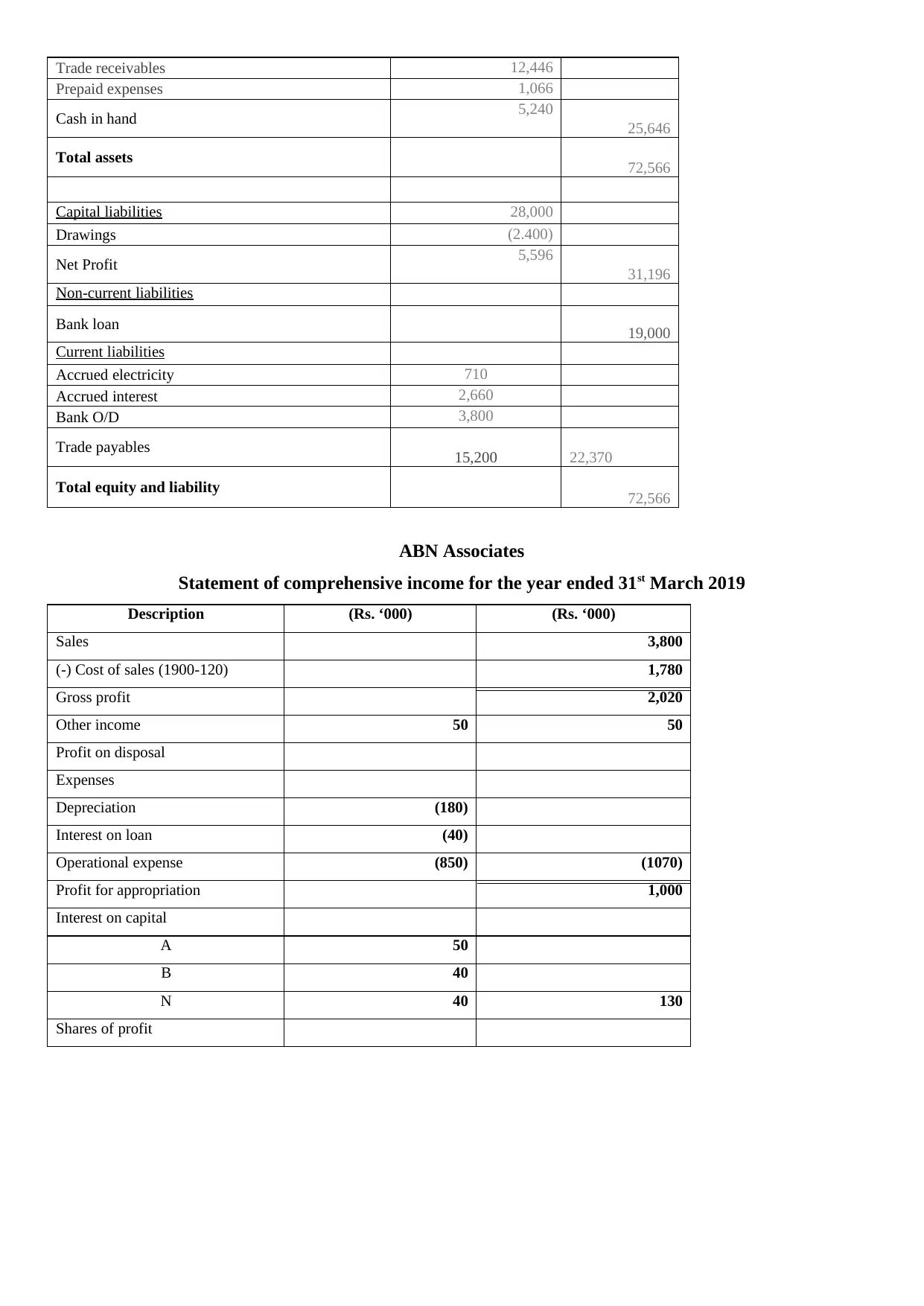

Prepaid expenses 1,066

Cash in hand 5,240

25,646

Total assets 72,566

Capital liabilities 28,000

Drawings (2.400)

Net Profit 5,596

31,196

Non-current liabilities

Bank loan 19,000

Current liabilities

Accrued electricity 710

Accrued interest 2,660

Bank O/D 3,800

Trade payables 15,200 22,370

Total equity and liability 72,566

ABN Associates

Statement of comprehensive income for the year ended 31st March 2019

Description (Rs. ‘000) (Rs. ‘000)

Sales 3,800

(-) Cost of sales (1900-120) 1,780

Gross profit 2,020

Other income 50 50

Profit on disposal

Expenses

Depreciation (180)

Interest on loan (40)

Operational expense (850) (1070)

Profit for appropriation 1,000

Interest on capital

A 50

B 40

N 40 130

Shares of profit

Prepaid expenses 1,066

Cash in hand 5,240

25,646

Total assets 72,566

Capital liabilities 28,000

Drawings (2.400)

Net Profit 5,596

31,196

Non-current liabilities

Bank loan 19,000

Current liabilities

Accrued electricity 710

Accrued interest 2,660

Bank O/D 3,800

Trade payables 15,200 22,370

Total equity and liability 72,566

ABN Associates

Statement of comprehensive income for the year ended 31st March 2019

Description (Rs. ‘000) (Rs. ‘000)

Sales 3,800

(-) Cost of sales (1900-120) 1,780

Gross profit 2,020

Other income 50 50

Profit on disposal

Expenses

Depreciation (180)

Interest on loan (40)

Operational expense (850) (1070)

Profit for appropriation 1,000

Interest on capital

A 50

B 40

N 40 130

Shares of profit

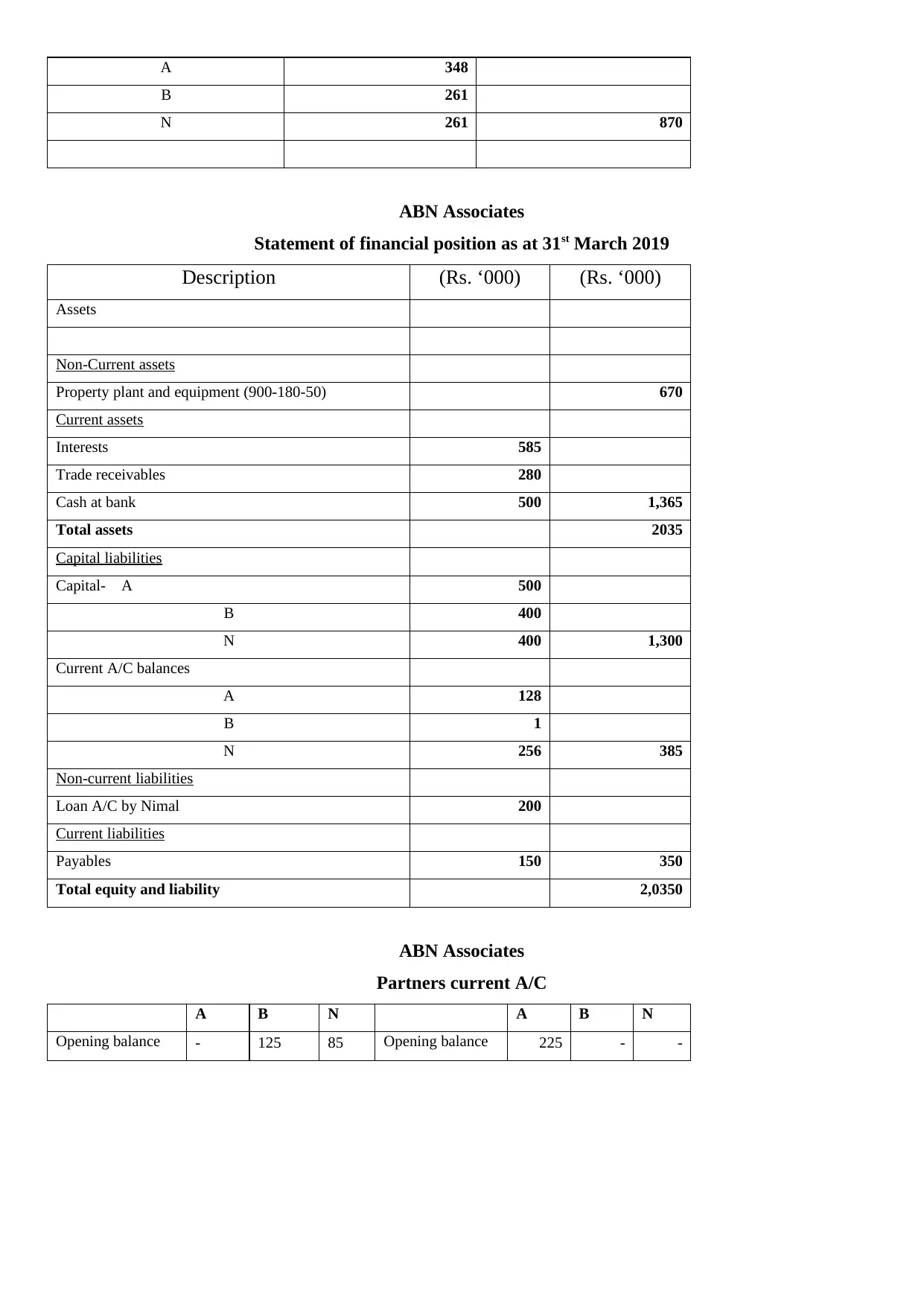

A 348

B 261

N 261 870

ABN Associates

Statement of financial position as at 31st March 2019

Description (Rs. ‘000) (Rs. ‘000)

Assets

Non-Current assets

Property plant and equipment (900-180-50) 670

Current assets

Interests 585

Trade receivables 280

Cash at bank 500 1,365

Total assets 2035

Capital liabilities

Capital- A 500

B 400

N 400 1,300

Current A/C balances

A 128

B 1

N 256 385

Non-current liabilities

Loan A/C by Nimal 200

Current liabilities

Payables 150 350

Total equity and liability 2,0350

ABN Associates

Partners current A/C

A B N A B N

Opening balance - 125 85 Opening balance 225 - -

B 261

N 261 870

ABN Associates

Statement of financial position as at 31st March 2019

Description (Rs. ‘000) (Rs. ‘000)

Assets

Non-Current assets

Property plant and equipment (900-180-50) 670

Current assets

Interests 585

Trade receivables 280

Cash at bank 500 1,365

Total assets 2035

Capital liabilities

Capital- A 500

B 400

N 400 1,300

Current A/C balances

A 128

B 1

N 256 385

Non-current liabilities

Loan A/C by Nimal 200

Current liabilities

Payables 150 350

Total equity and liability 2,0350

ABN Associates

Partners current A/C

A B N A B N

Opening balance - 125 85 Opening balance 225 - -

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

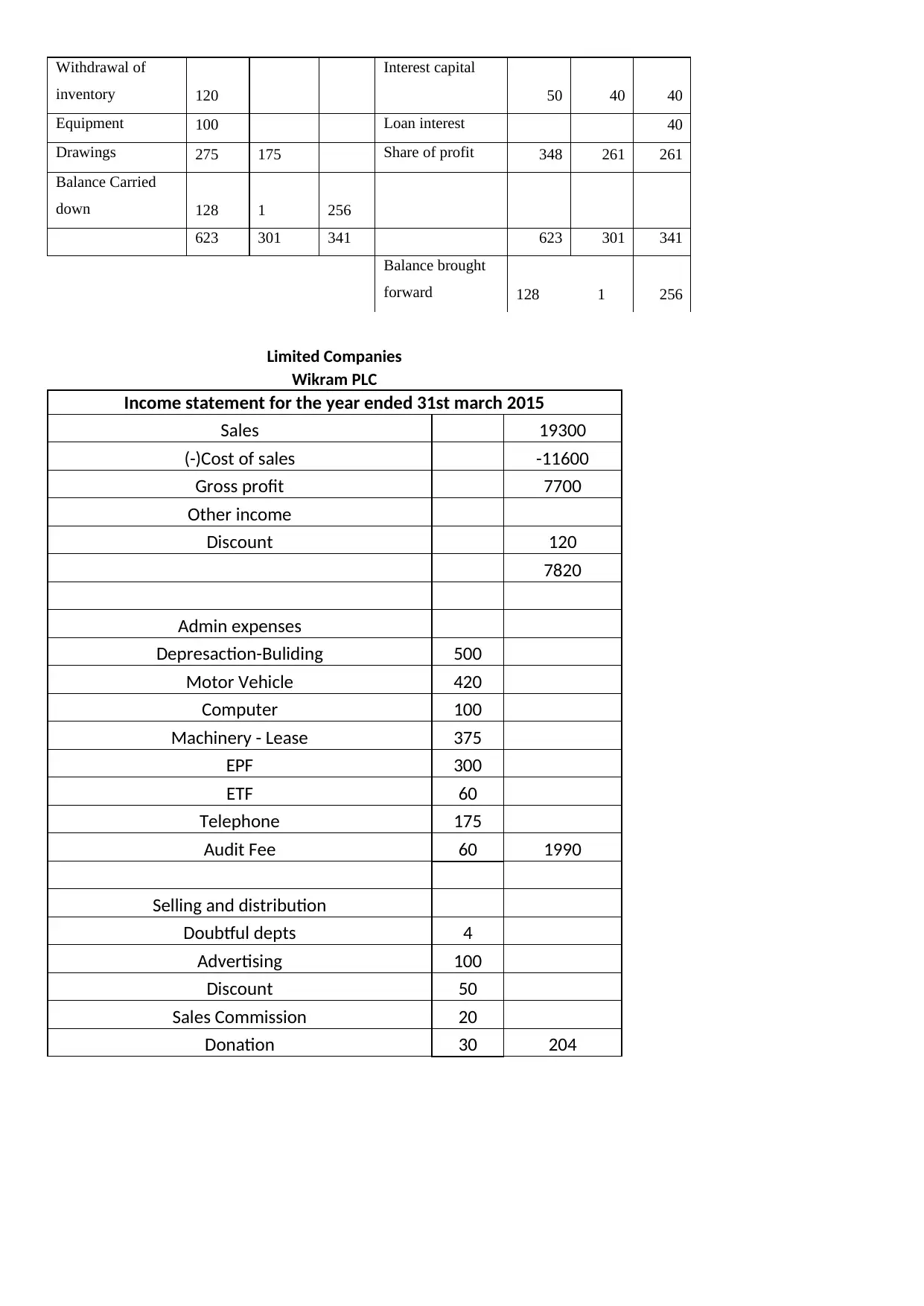

Withdrawal of

inventory 120

Interest capital

50 40 40

Equipment 100 Loan interest 40

Drawings 275 175 Share of profit 348 261 261

Balance Carried

down 128 1 256

623 301 341 623 301 341

Balance brought

forward 128 1 256

Limited Companies

Wikram PLC

Income statement for the year ended 31st march 2015

Sales 19300

(-)Cost of sales -11600

Gross profit 7700

Other income

Discount 120

7820

Admin expenses

Depresaction-Buliding 500

Motor Vehicle 420

Computer 100

Machinery - Lease 375

EPF 300

ETF 60

Telephone 175

Audit Fee 60 1990

Selling and distribution

Doubtful depts 4

Advertising 100

Discount 50

Sales Commission 20

Donation 30 204

inventory 120

Interest capital

50 40 40

Equipment 100 Loan interest 40

Drawings 275 175 Share of profit 348 261 261

Balance Carried

down 128 1 256

623 301 341 623 301 341

Balance brought

forward 128 1 256

Limited Companies

Wikram PLC

Income statement for the year ended 31st march 2015

Sales 19300

(-)Cost of sales -11600

Gross profit 7700

Other income

Discount 120

7820

Admin expenses

Depresaction-Buliding 500

Motor Vehicle 420

Computer 100

Machinery - Lease 375

EPF 300

ETF 60

Telephone 175

Audit Fee 60 1990

Selling and distribution

Doubtful depts 4

Advertising 100

Discount 50

Sales Commission 20

Donation 30 204

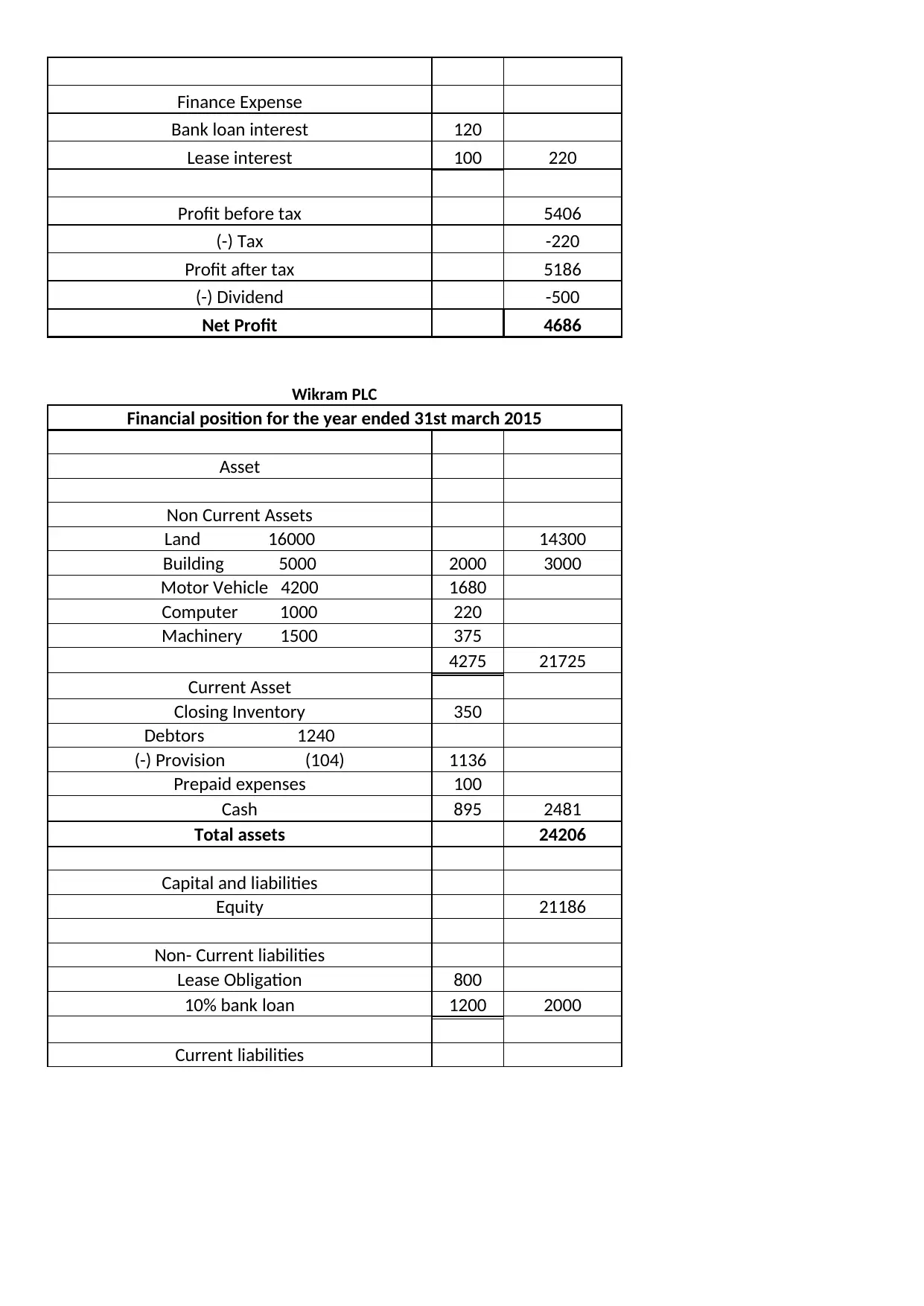

Finance Expense

Bank loan interest 120

Lease interest 100 220

Profit before tax 5406

(-) Tax -220

Profit after tax 5186

(-) Dividend -500

Net Profit 4686

Wikram PLC

Financial position for the year ended 31st march 2015

Asset

Non Current Assets

Land 16000 14300

Building 5000 2000 3000

Motor Vehicle 4200 1680

Computer 1000 220

Machinery 1500 375

4275 21725

Current Asset

Closing Inventory 350

Debtors 1240

(-) Provision (104) 1136

Prepaid expenses 100

Cash 895 2481

Total assets 24206

Capital and liabilities

Equity 21186

Non- Current liabilities

Lease Obligation 800

10% bank loan 1200 2000

Current liabilities

Bank loan interest 120

Lease interest 100 220

Profit before tax 5406

(-) Tax -220

Profit after tax 5186

(-) Dividend -500

Net Profit 4686

Wikram PLC

Financial position for the year ended 31st march 2015

Asset

Non Current Assets

Land 16000 14300

Building 5000 2000 3000

Motor Vehicle 4200 1680

Computer 1000 220

Machinery 1500 375

4275 21725

Current Asset

Closing Inventory 350

Debtors 1240

(-) Provision (104) 1136

Prepaid expenses 100

Cash 895 2481

Total assets 24206

Capital and liabilities

Equity 21186

Non- Current liabilities

Lease Obligation 800

10% bank loan 1200 2000

Current liabilities

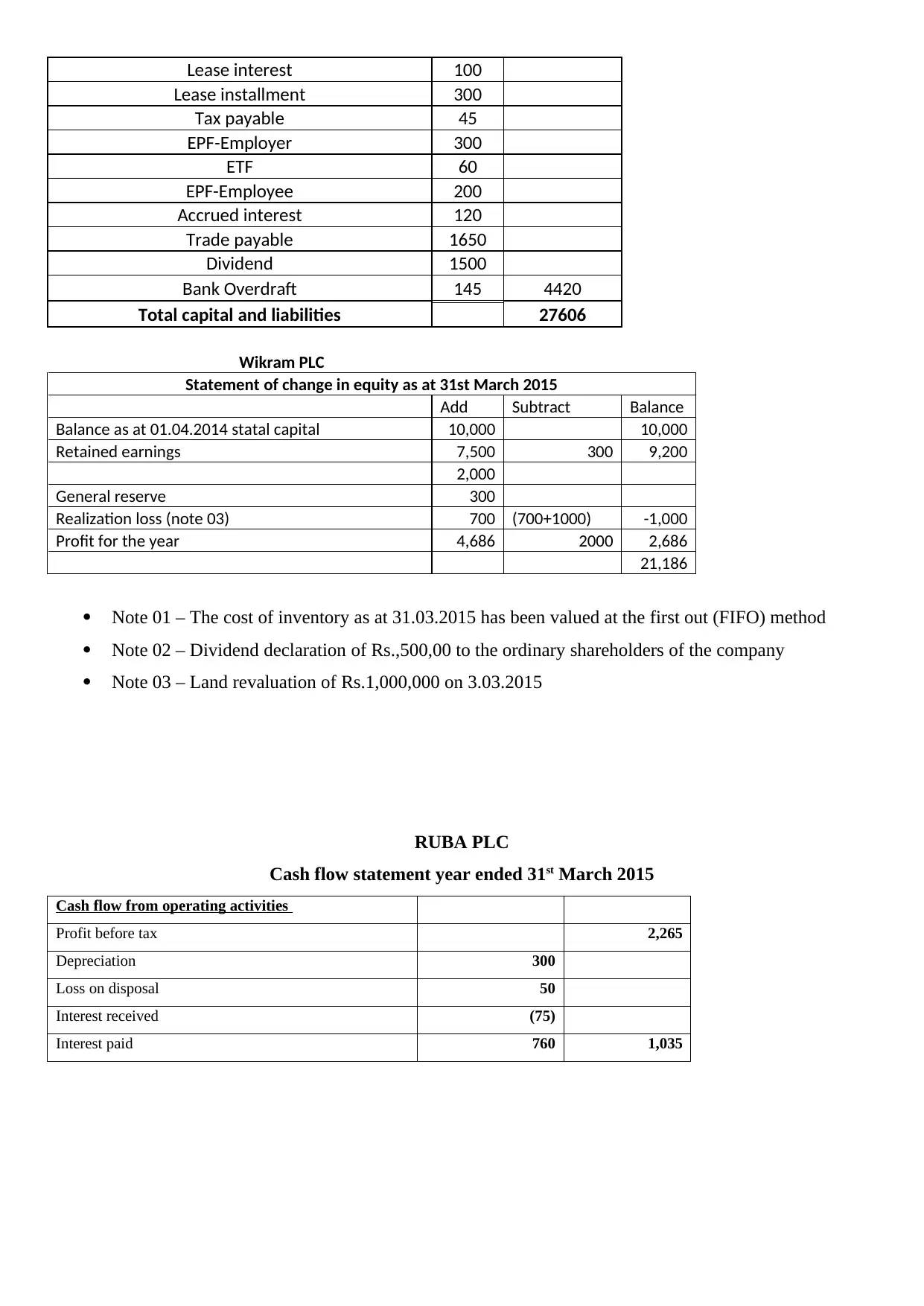

Lease interest 100

Lease installment 300

Tax payable 45

EPF-Employer 300

ETF 60

EPF-Employee 200

Accrued interest 120

Trade payable 1650

Dividend 1500

Bank Overdraft 145 4420

Total capital and liabilities 27606

Wikram PLC

Statement of change in equity as at 31st March 2015

Add Subtract Balance

Balance as at 01.04.2014 statal capital 10,000 10,000

Retained earnings 7,500 300 9,200

2,000

General reserve 300

Realization loss (note 03) 700 (700+1000) -1,000

Profit for the year 4,686 2000 2,686

21,186

Note 01 – The cost of inventory as at 31.03.2015 has been valued at the first out (FIFO) method

Note 02 – Dividend declaration of Rs.,500,00 to the ordinary shareholders of the company

Note 03 – Land revaluation of Rs.1,000,000 on 3.03.2015

RUBA PLC

Cash flow statement year ended 31st March 2015

Cash flow from operating activities

Profit before tax 2,265

Depreciation 300

Loss on disposal 50

Interest received (75)

Interest paid 760 1,035

Lease installment 300

Tax payable 45

EPF-Employer 300

ETF 60

EPF-Employee 200

Accrued interest 120

Trade payable 1650

Dividend 1500

Bank Overdraft 145 4420

Total capital and liabilities 27606

Wikram PLC

Statement of change in equity as at 31st March 2015

Add Subtract Balance

Balance as at 01.04.2014 statal capital 10,000 10,000

Retained earnings 7,500 300 9,200

2,000

General reserve 300

Realization loss (note 03) 700 (700+1000) -1,000

Profit for the year 4,686 2000 2,686

21,186

Note 01 – The cost of inventory as at 31.03.2015 has been valued at the first out (FIFO) method

Note 02 – Dividend declaration of Rs.,500,00 to the ordinary shareholders of the company

Note 03 – Land revaluation of Rs.1,000,000 on 3.03.2015

RUBA PLC

Cash flow statement year ended 31st March 2015

Cash flow from operating activities

Profit before tax 2,265

Depreciation 300

Loss on disposal 50

Interest received (75)

Interest paid 760 1,035

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

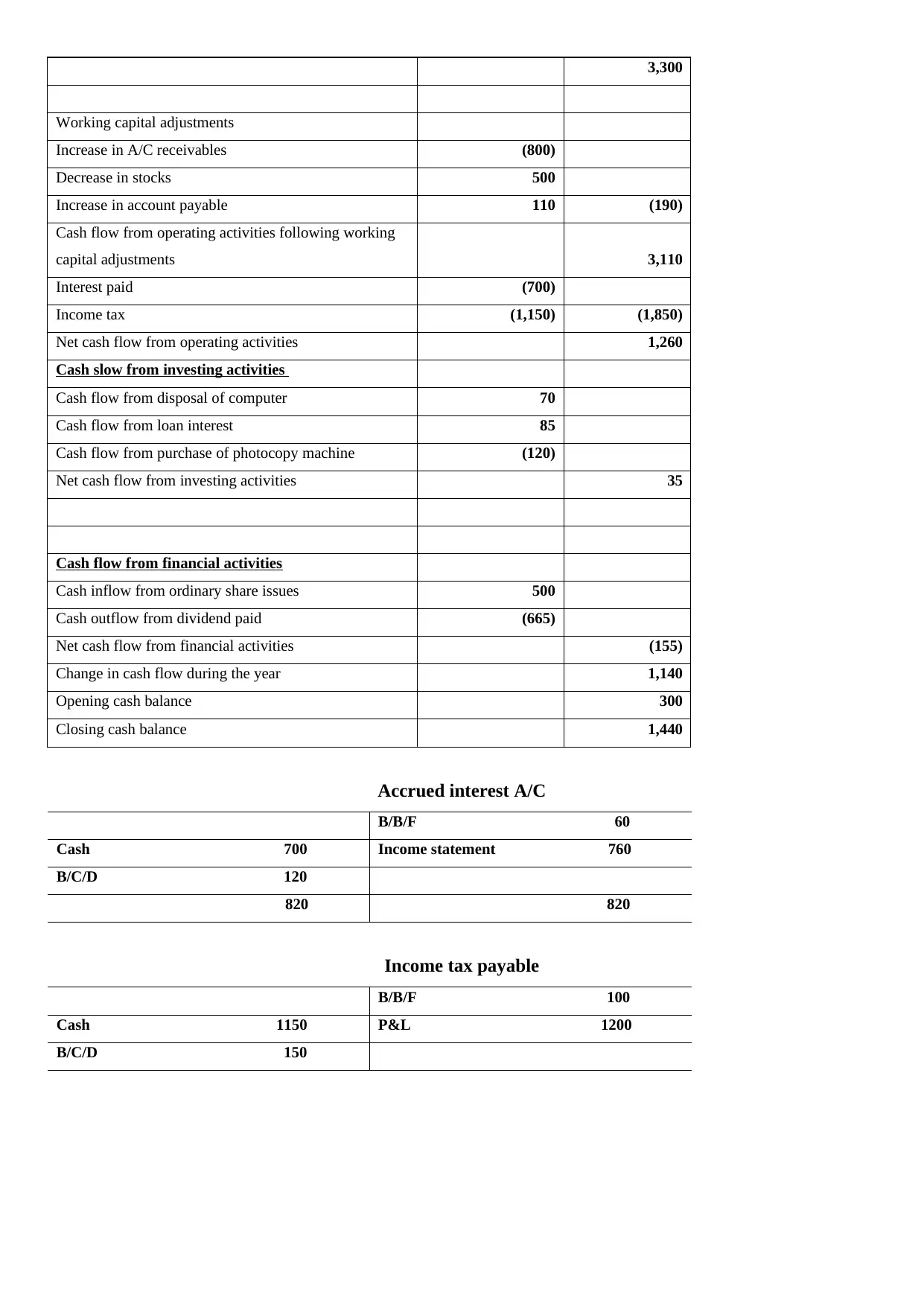

3,300

Working capital adjustments

Increase in A/C receivables (800)

Decrease in stocks 500

Increase in account payable 110 (190)

Cash flow from operating activities following working

capital adjustments 3,110

Interest paid (700)

Income tax (1,150) (1,850)

Net cash flow from operating activities 1,260

Cash slow from investing activities

Cash flow from disposal of computer 70

Cash flow from loan interest 85

Cash flow from purchase of photocopy machine (120)

Net cash flow from investing activities 35

Cash flow from financial activities

Cash inflow from ordinary share issues 500

Cash outflow from dividend paid (665)

Net cash flow from financial activities (155)

Change in cash flow during the year 1,140

Opening cash balance 300

Closing cash balance 1,440

Accrued interest A/C

B/B/F 60

Cash 700 Income statement 760

B/C/D 120

820 820

Income tax payable

B/B/F 100

Cash 1150 P&L 1200

B/C/D 150

Working capital adjustments

Increase in A/C receivables (800)

Decrease in stocks 500

Increase in account payable 110 (190)

Cash flow from operating activities following working

capital adjustments 3,110

Interest paid (700)

Income tax (1,150) (1,850)

Net cash flow from operating activities 1,260

Cash slow from investing activities

Cash flow from disposal of computer 70

Cash flow from loan interest 85

Cash flow from purchase of photocopy machine (120)

Net cash flow from investing activities 35

Cash flow from financial activities

Cash inflow from ordinary share issues 500

Cash outflow from dividend paid (665)

Net cash flow from financial activities (155)

Change in cash flow during the year 1,140

Opening cash balance 300

Closing cash balance 1,440

Accrued interest A/C

B/B/F 60

Cash 700 Income statement 760

B/C/D 120

820 820

Income tax payable

B/B/F 100

Cash 1150 P&L 1200

B/C/D 150

1300 1300

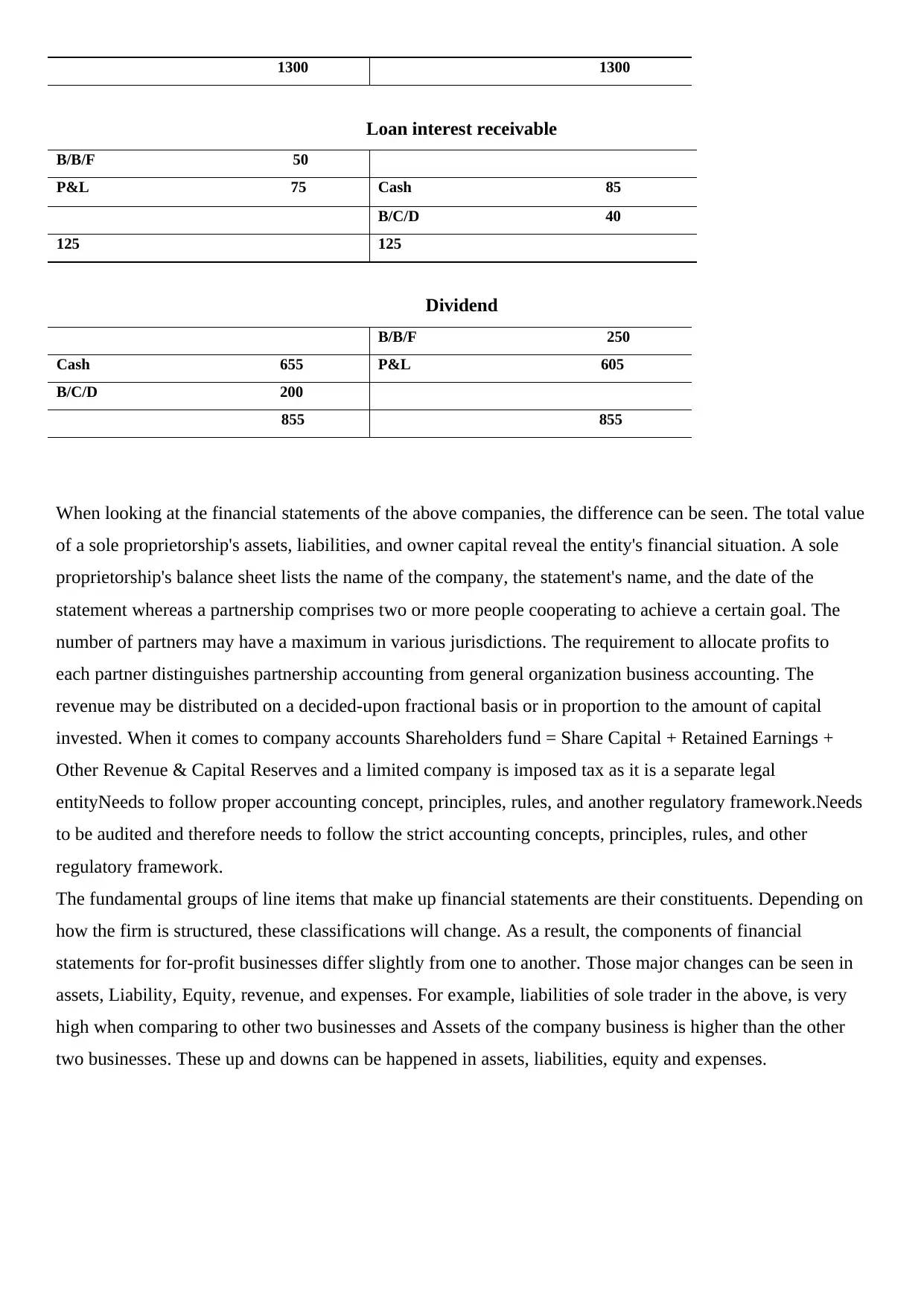

Loan interest receivable

B/B/F 50

P&L 75 Cash 85

B/C/D 40

125 125

Dividend

B/B/F 250

Cash 655 P&L 605

B/C/D 200

855 855

When looking at the financial statements of the above companies, the difference can be seen. The total value

of a sole proprietorship's assets, liabilities, and owner capital reveal the entity's financial situation. A sole

proprietorship's balance sheet lists the name of the company, the statement's name, and the date of the

statement whereas a partnership comprises two or more people cooperating to achieve a certain goal. The

number of partners may have a maximum in various jurisdictions. The requirement to allocate profits to

each partner distinguishes partnership accounting from general organization business accounting. The

revenue may be distributed on a decided-upon fractional basis or in proportion to the amount of capital

invested. When it comes to company accounts Shareholders fund = Share Capital + Retained Earnings +

Other Revenue & Capital Reserves and a limited company is imposed tax as it is a separate legal

entityNeeds to follow proper accounting concept, principles, rules, and another regulatory framework.Needs

to be audited and therefore needs to follow the strict accounting concepts, principles, rules, and other

regulatory framework.

The fundamental groups of line items that make up financial statements are their constituents. Depending on

how the firm is structured, these classifications will change. As a result, the components of financial

statements for for-profit businesses differ slightly from one to another. Those major changes can be seen in

assets, Liability, Equity, revenue, and expenses. For example, liabilities of sole trader in the above, is very

high when comparing to other two businesses and Assets of the company business is higher than the other

two businesses. These up and downs can be happened in assets, liabilities, equity and expenses.

Loan interest receivable

B/B/F 50

P&L 75 Cash 85

B/C/D 40

125 125

Dividend

B/B/F 250

Cash 655 P&L 605

B/C/D 200

855 855

When looking at the financial statements of the above companies, the difference can be seen. The total value

of a sole proprietorship's assets, liabilities, and owner capital reveal the entity's financial situation. A sole

proprietorship's balance sheet lists the name of the company, the statement's name, and the date of the

statement whereas a partnership comprises two or more people cooperating to achieve a certain goal. The

number of partners may have a maximum in various jurisdictions. The requirement to allocate profits to

each partner distinguishes partnership accounting from general organization business accounting. The

revenue may be distributed on a decided-upon fractional basis or in proportion to the amount of capital

invested. When it comes to company accounts Shareholders fund = Share Capital + Retained Earnings +

Other Revenue & Capital Reserves and a limited company is imposed tax as it is a separate legal

entityNeeds to follow proper accounting concept, principles, rules, and another regulatory framework.Needs

to be audited and therefore needs to follow the strict accounting concepts, principles, rules, and other

regulatory framework.

The fundamental groups of line items that make up financial statements are their constituents. Depending on

how the firm is structured, these classifications will change. As a result, the components of financial

statements for for-profit businesses differ slightly from one to another. Those major changes can be seen in

assets, Liability, Equity, revenue, and expenses. For example, liabilities of sole trader in the above, is very

high when comparing to other two businesses and Assets of the company business is higher than the other

two businesses. These up and downs can be happened in assets, liabilities, equity and expenses.

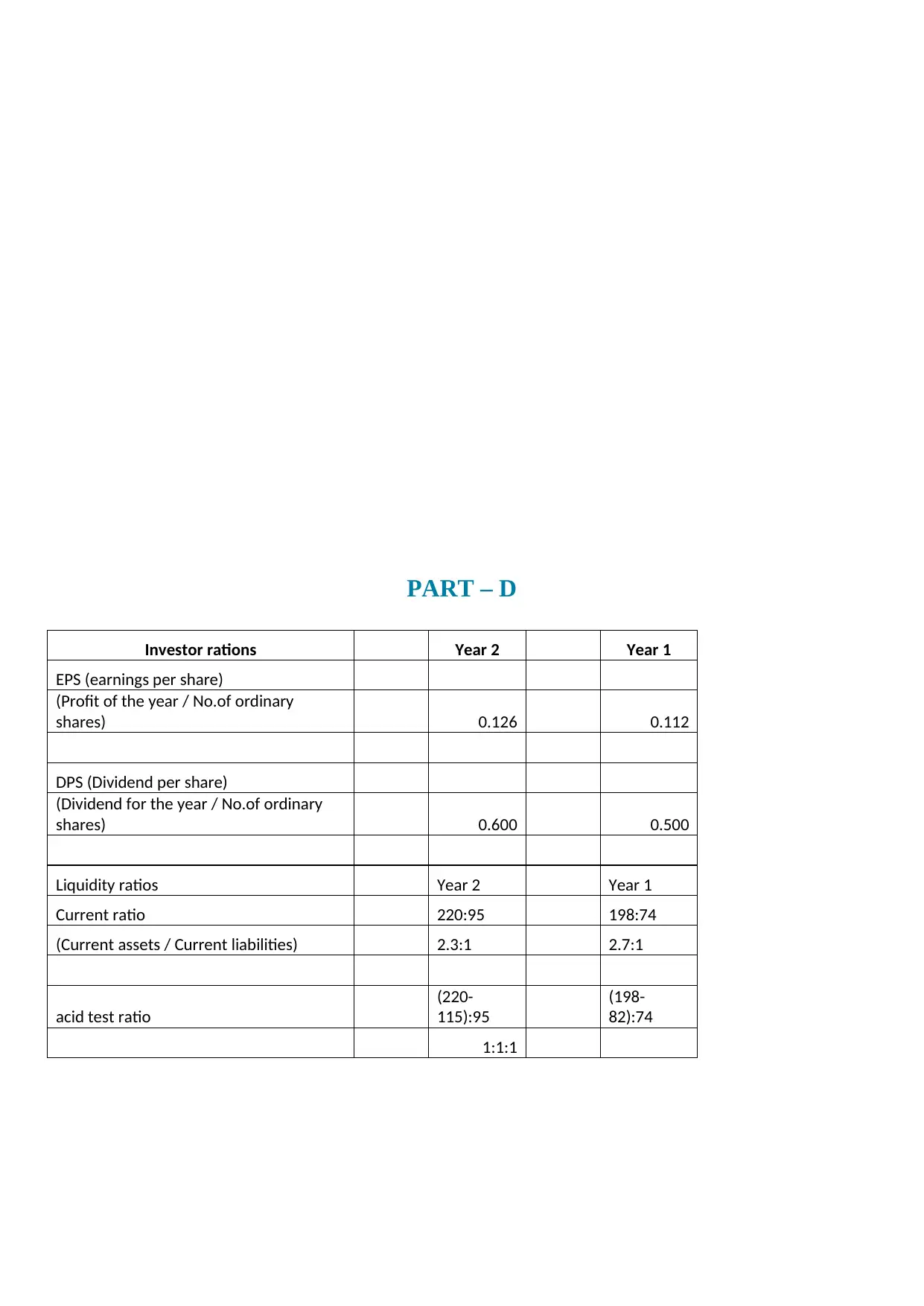

PART – D

Investor rations Year 2 Year 1

EPS (earnings per share)

(Profit of the year / No.of ordinary

shares) 0.126 0.112

DPS (Dividend per share)

(Dividend for the year / No.of ordinary

shares) 0.600 0.500

Liquidity ratios Year 2 Year 1

Current ratio 220:95 198:74

(Current assets / Current liabilities) 2.3:1 2.7:1

acid test ratio

(220-

115):95

(198-

82):74

1:1:1

Investor rations Year 2 Year 1

EPS (earnings per share)

(Profit of the year / No.of ordinary

shares) 0.126 0.112

DPS (Dividend per share)

(Dividend for the year / No.of ordinary

shares) 0.600 0.500

Liquidity ratios Year 2 Year 1

Current ratio 220:95 198:74

(Current assets / Current liabilities) 2.3:1 2.7:1

acid test ratio

(220-

115):95

(198-

82):74

1:1:1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

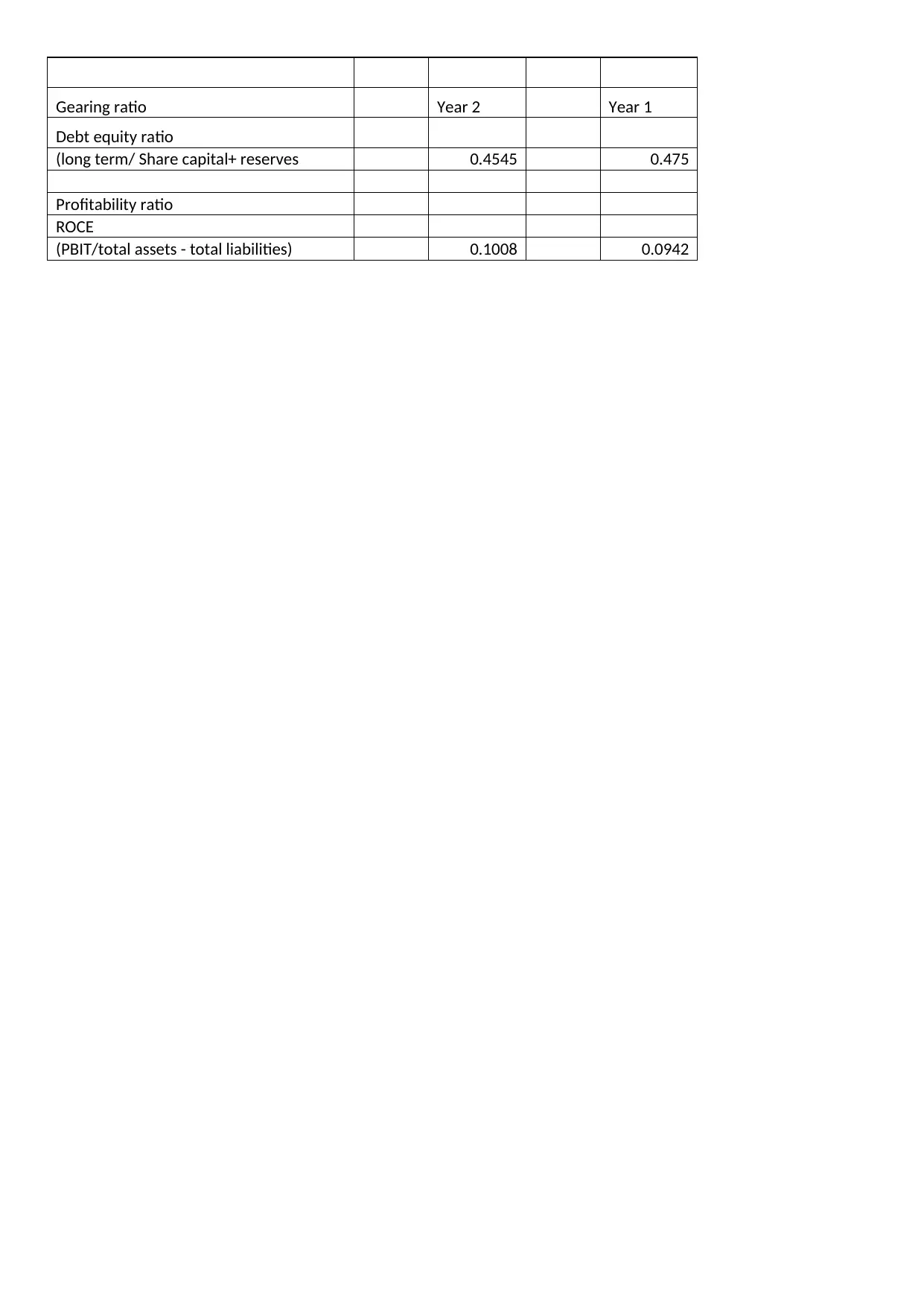

Gearing ratio Year 2 Year 1

Debt equity ratio

(long term/ Share capital+ reserves 0.4545 0.475

Profitability ratio

ROCE

(PBIT/total assets - total liabilities) 0.1008 0.0942

Debt equity ratio

(long term/ Share capital+ reserves 0.4545 0.475

Profitability ratio

ROCE

(PBIT/total assets - total liabilities) 0.1008 0.0942

1 out of 32

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.