Historical Cost versus Fair Value Accounting: PPE and Intangibles

VerifiedAdded on 2020/05/28

|17

|3947

|42

Report

AI Summary

This report delves into the debate between historical cost and fair value accounting methods for non-financial assets, focusing on plant, property, and equipment (PPE) and intangible assets. It explains the measurement concepts of both methods, evaluating their benefits and challenges, such as timeliness, comparability, and potential for manipulation. The report analyzes the valuation policies of three companies—BHP Billiton, Anglesey Mining, and Hudbay Minerals—listed on different stock exchanges, comparing their approaches to PPE and intangible asset valuation based on their financial reports. The analysis includes a discussion of the consistency of valuation practices and concludes with an opinion on the free choice between historical cost and fair value accounting, providing a comprehensive overview of the practical application and implications of each method.

Running head: HISTORICAL COST VERSUS FAIR VALUE ACCOUNTING

Historical cost versus fair value accounting

Name of the University

Name of the Student

Authors Note

Historical cost versus fair value accounting

Name of the University

Name of the Student

Authors Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1HISTORICAL COST VERSUS FAIR VALUE ACCOUNTING

Table of Contents

Executive summary:...................................................................................................................2

Introduction:...............................................................................................................................3

Discussion:.................................................................................................................................4

Explanation of the measurement concepts in relation to historical cost and fair value

accounting:.................................................................................................................................4

Evaluate the benefits and challenges of using historical cost and fair value accounting for

PPE and intangibles:..................................................................................................................5

Valuation policies of non-financial assets groups of three listed companies:...........................7

Analysis of consistency of valuation practices across three companies:.................................11

Framing an opinion on the free choice between historical cost and fair value accounting for

PPE and intangibles:................................................................................................................12

Conclusion:..............................................................................................................................13

References list:.........................................................................................................................14

Table of Contents

Executive summary:...................................................................................................................2

Introduction:...............................................................................................................................3

Discussion:.................................................................................................................................4

Explanation of the measurement concepts in relation to historical cost and fair value

accounting:.................................................................................................................................4

Evaluate the benefits and challenges of using historical cost and fair value accounting for

PPE and intangibles:..................................................................................................................5

Valuation policies of non-financial assets groups of three listed companies:...........................7

Analysis of consistency of valuation practices across three companies:.................................11

Framing an opinion on the free choice between historical cost and fair value accounting for

PPE and intangibles:................................................................................................................12

Conclusion:..............................................................................................................................13

References list:.........................................................................................................................14

2HISTORICAL COST VERSUS FAIR VALUE ACCOUNTING

Executive summary:

The report is prepared to demonstrate the accounting method that is used for non financial

assets by three different organizations listed on different stock exchanges. Analysis has been

done regarding the concepts of fair value and historical accounting method practices by

organizations in valuing their intangible assets and plant, property and equipment. Three

companies that selected are BHP billion limited listed on ASX, Hudbay minerals listed on

NSX and Anglesey limited listed on LSE. Evaluation of their accounting method in valuating

non financial assets is by analyzing their respective financial report.

Executive summary:

The report is prepared to demonstrate the accounting method that is used for non financial

assets by three different organizations listed on different stock exchanges. Analysis has been

done regarding the concepts of fair value and historical accounting method practices by

organizations in valuing their intangible assets and plant, property and equipment. Three

companies that selected are BHP billion limited listed on ASX, Hudbay minerals listed on

NSX and Anglesey limited listed on LSE. Evaluation of their accounting method in valuating

non financial assets is by analyzing their respective financial report.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3HISTORICAL COST VERSUS FAIR VALUE ACCOUNTING

Introduction:

The report is prepared to conduct a detailed analysis of given research topic that is

“Historical cost versus fair value of accounting for non-financial assets”. It has been

ascertained that there is an ongoing debate between these two methods of accounting by

reviewing literature. Free choice between historical accounting and fair value accounting

have been debated and mandating any particular method is considered from one perspective

and do not considering the perspective of users of financial statements. Report has

demonstrated the explanation of measurement concepts of both the accounting method for

valuing non-financial assets. Challenges and benefits of using one particular accounting

method have also been explained.

Concerning the explanation of practical valuation practices of these two methods of

accounting, three companies from three different stock exchanges have been selected. Three

companies that are selected are BHP Billiton Limited from Australian stock exchange,

Anglesey Mineral limited from London stock exchange and Hudbay Minerals from New

York stock exchange. All these three companies operate in mineral and exploration. BHP

Billiton limited is an Australian multinational, mining and petroleum based public company

having headquarter in Melbourne (bhp.com 2018). Anglesey limited is a mining company

that is based on United Kingdom and has direct shipping deposits of iron ore in Quebec and

Labrador (angleseymining.co.uk 2018). Hudbay Mining Corporation is a mining company

that is based in Canada and has been exploring and mining for over eighty years in Manitoba

(Hudbayminerals.com 2018).

Introduction:

The report is prepared to conduct a detailed analysis of given research topic that is

“Historical cost versus fair value of accounting for non-financial assets”. It has been

ascertained that there is an ongoing debate between these two methods of accounting by

reviewing literature. Free choice between historical accounting and fair value accounting

have been debated and mandating any particular method is considered from one perspective

and do not considering the perspective of users of financial statements. Report has

demonstrated the explanation of measurement concepts of both the accounting method for

valuing non-financial assets. Challenges and benefits of using one particular accounting

method have also been explained.

Concerning the explanation of practical valuation practices of these two methods of

accounting, three companies from three different stock exchanges have been selected. Three

companies that are selected are BHP Billiton Limited from Australian stock exchange,

Anglesey Mineral limited from London stock exchange and Hudbay Minerals from New

York stock exchange. All these three companies operate in mineral and exploration. BHP

Billiton limited is an Australian multinational, mining and petroleum based public company

having headquarter in Melbourne (bhp.com 2018). Anglesey limited is a mining company

that is based on United Kingdom and has direct shipping deposits of iron ore in Quebec and

Labrador (angleseymining.co.uk 2018). Hudbay Mining Corporation is a mining company

that is based in Canada and has been exploring and mining for over eighty years in Manitoba

(Hudbayminerals.com 2018).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4HISTORICAL COST VERSUS FAIR VALUE ACCOUNTING

Discussion:

Explanation of the measurement concepts in relation to historical cost and fair value

accounting:

A fair value disclosure or measurement is permitted by IFRS 13 Fair value

measurement and the reporting entities are provided a single platform for making disclosure

about their fair value measurement. Fair value under this standard is defined as the basis of

notion of exit price and makes use of fair value hierarchy that provides a measurement that is

market based rather than entity based. Estimating the price for executing an orderly

transactions to transfer the liabilities or sell the assets between market participants at the

under the present market conditions is the objective of fair value measurement. Reporting

entities are required to determine the valuation premise for non-financial assets that is

regarded as appropriate for measurement. The measurement of fair value of an item of plant,

equipment and property is done at its existing or current use when the economic benefits of

such assets available to market participants cannot be accessed (Allee et al. 2015). When

there is availability of sufficient data for measuring the fair value so that it helps in

minimization of observable inputs use and maximizes the use of relevant observable inputs,

the entity should use valuation techniques.

Now, historical cost accounting can be seen as a measurement basis used in

accounting under which the price of assets is based on original cost or nominal price. The

measurement of historical cost accounting is drawn from the initial cost that is incurred on

item. Information those are prepared based on historical costing are relevant to organizations

for some purpose. This method of accounting seems inferior to fair value accounting as

described in the conceptual framework of financial accounting reporting standard. The

interpretation of historical cost accounting is done in a way in terms of assets price should not

Discussion:

Explanation of the measurement concepts in relation to historical cost and fair value

accounting:

A fair value disclosure or measurement is permitted by IFRS 13 Fair value

measurement and the reporting entities are provided a single platform for making disclosure

about their fair value measurement. Fair value under this standard is defined as the basis of

notion of exit price and makes use of fair value hierarchy that provides a measurement that is

market based rather than entity based. Estimating the price for executing an orderly

transactions to transfer the liabilities or sell the assets between market participants at the

under the present market conditions is the objective of fair value measurement. Reporting

entities are required to determine the valuation premise for non-financial assets that is

regarded as appropriate for measurement. The measurement of fair value of an item of plant,

equipment and property is done at its existing or current use when the economic benefits of

such assets available to market participants cannot be accessed (Allee et al. 2015). When

there is availability of sufficient data for measuring the fair value so that it helps in

minimization of observable inputs use and maximizes the use of relevant observable inputs,

the entity should use valuation techniques.

Now, historical cost accounting can be seen as a measurement basis used in

accounting under which the price of assets is based on original cost or nominal price. The

measurement of historical cost accounting is drawn from the initial cost that is incurred on

item. Information those are prepared based on historical costing are relevant to organizations

for some purpose. This method of accounting seems inferior to fair value accounting as

described in the conceptual framework of financial accounting reporting standard. The

interpretation of historical cost accounting is done in a way in terms of assets price should not

5HISTORICAL COST VERSUS FAIR VALUE ACCOUNTING

be more than recoverable amount from its selling and usage. Recoverable amount is regarded

as higher of the value in use and realizable value of assets. Recognition of gain under this

method of accounting is realisable when increase in value of assets is more than the amount

of historical cost. There can be reliable measurement of historical cost that can be identified

from the transactions of actual prices. It can be explained with the help of an instance,

purchase price of items of stock can be identified on clear basis and there can be objective

measurement of amount owed to the business and amount received. Fair value accounting for

non-financial assets provides with the benefits of increased content of information and

relevance of value. On the reliability dimensions, fair value is likely to be dominated by

historical cost. Opportunity cost of investment is reflected by the historical cost accounting

method. Classification of organization in the application of historical cost is done if there is

recognition of one asset class at historical costs. It has been ascertained from research that

fair value accounting is used by 5% of companies that are operating in UK while for one

asset class within the group, all companies are using historical cost basis (DeFond et al.

2014).

Evaluate the benefits and challenges of using historical cost and fair value accounting

for PPE and intangibles:

Benefits of historical cost and fair value accounting:

Timeliness:

Timeliness is one of the benefits that arise from the fair value accounting that are used

for the valuation of non-financial assets. Any reporting change in plant, equipment and

property fair value has the potential of providing timely to interest users of financial

statements such as investors and creditors. The information relating to the valuation of such

assets is considered reliable. For determining the fair value of assets, investors requires

be more than recoverable amount from its selling and usage. Recoverable amount is regarded

as higher of the value in use and realizable value of assets. Recognition of gain under this

method of accounting is realisable when increase in value of assets is more than the amount

of historical cost. There can be reliable measurement of historical cost that can be identified

from the transactions of actual prices. It can be explained with the help of an instance,

purchase price of items of stock can be identified on clear basis and there can be objective

measurement of amount owed to the business and amount received. Fair value accounting for

non-financial assets provides with the benefits of increased content of information and

relevance of value. On the reliability dimensions, fair value is likely to be dominated by

historical cost. Opportunity cost of investment is reflected by the historical cost accounting

method. Classification of organization in the application of historical cost is done if there is

recognition of one asset class at historical costs. It has been ascertained from research that

fair value accounting is used by 5% of companies that are operating in UK while for one

asset class within the group, all companies are using historical cost basis (DeFond et al.

2014).

Evaluate the benefits and challenges of using historical cost and fair value accounting

for PPE and intangibles:

Benefits of historical cost and fair value accounting:

Timeliness:

Timeliness is one of the benefits that arise from the fair value accounting that are used

for the valuation of non-financial assets. Any reporting change in plant, equipment and

property fair value has the potential of providing timely to interest users of financial

statements such as investors and creditors. The information relating to the valuation of such

assets is considered reliable. For determining the fair value of assets, investors requires

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6HISTORICAL COST VERSUS FAIR VALUE ACCOUNTING

current appraisal of non-financial assets. Current changes in the plant, equipment and

property under the fair value method also provided information to other users of financial

statement (Chabrak 2016). On other hand, the capacity of influencing decisions is also

provided by historical cost as long as the fair value is reasonably estimated by book value of

assets. However, the capacity of influencing user’s decision influenced under this method of

accounting because of existence of deviation of fair value from book value.

Comparability:

Comparability of information in different reporting time is enhanced using fair value

method and on other hand, comparability can be hindered by the measurement of historical

cost basis. This is because latter fails to make the identification similarities between similar

items. One of the important implications regarding comparability is the issue of allowing

versus plant, equipment and property revaluations. Under the convergence model of plant,

equipment and property, revaluations concerning such non-financial assets will continue to

exist (Cascino and Gassen 2015).

Enhanced information disclosure:

Since under the fair value accounting, valuations of assets are done at their current

market value, it helps in capturing the present value of future cash flows associated with such

assets. As opposed to historical cost method, fair value helps in enhancement of informative

power of financial report. Organizations are required to make an extensive discourse about

the assumptions that are made, risk exposure, methodology used, any issues and related

sensitivities leading to thorough financial statements (Christensen et al. 2015).

Challenges of fair value accounting and historical accounting:

Creation of large swings of value:

current appraisal of non-financial assets. Current changes in the plant, equipment and

property under the fair value method also provided information to other users of financial

statement (Chabrak 2016). On other hand, the capacity of influencing decisions is also

provided by historical cost as long as the fair value is reasonably estimated by book value of

assets. However, the capacity of influencing user’s decision influenced under this method of

accounting because of existence of deviation of fair value from book value.

Comparability:

Comparability of information in different reporting time is enhanced using fair value

method and on other hand, comparability can be hindered by the measurement of historical

cost basis. This is because latter fails to make the identification similarities between similar

items. One of the important implications regarding comparability is the issue of allowing

versus plant, equipment and property revaluations. Under the convergence model of plant,

equipment and property, revaluations concerning such non-financial assets will continue to

exist (Cascino and Gassen 2015).

Enhanced information disclosure:

Since under the fair value accounting, valuations of assets are done at their current

market value, it helps in capturing the present value of future cash flows associated with such

assets. As opposed to historical cost method, fair value helps in enhancement of informative

power of financial report. Organizations are required to make an extensive discourse about

the assumptions that are made, risk exposure, methodology used, any issues and related

sensitivities leading to thorough financial statements (Christensen et al. 2015).

Challenges of fair value accounting and historical accounting:

Creation of large swings of value:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7HISTORICAL COST VERSUS FAIR VALUE ACCOUNTING

Fair value accounting does not benefits some type of business and such business are

those that have their assets always fluctuating by large amount throughout the year. There can

be creation of misleading gains and loss for assets due to volatility in assets that do not reflect

actual value. The changes in level of pricing are not taken into consideration under historical

cost accounting and hence change in money value is not reflected. Consequently, it fails to

give actual picture of statement of affairs of company.

Manipulation:

Estimates made about non-financial assets can come with risks because of the

possibility that reporting entity will make any manipulation it their assets pricing. This would

influence both quoted and traded prices and hence in this regarded, historical cost is

considered better. Under historical costing, the income statement does not reveal true profits

and there is a probability that profits would be overstated during inflation period.

Misleading information:

It is certainly possible that the fundamental value of assets will not be indicative by

observed value of assets that are used under fair value accounting. Not all the publicly

available information might be reflected in the formation of estimates as market has the

probability of being inefficient. In this regard, historical costing method would be considered

suitable. Market deviation can also be caused due to other factors such as behavioural bias,

irrationality and prevalence of arbitrage (Whittington 2014).

Valuation policies of non-financial assets groups of three listed companies:

In this particular section, there companies have been selected from the three different

stock exchange that is Australian stock exchange, London stock exchange and New York

stock exchange for the evaluation of valuation policies of intangibles and PPE. These

Fair value accounting does not benefits some type of business and such business are

those that have their assets always fluctuating by large amount throughout the year. There can

be creation of misleading gains and loss for assets due to volatility in assets that do not reflect

actual value. The changes in level of pricing are not taken into consideration under historical

cost accounting and hence change in money value is not reflected. Consequently, it fails to

give actual picture of statement of affairs of company.

Manipulation:

Estimates made about non-financial assets can come with risks because of the

possibility that reporting entity will make any manipulation it their assets pricing. This would

influence both quoted and traded prices and hence in this regarded, historical cost is

considered better. Under historical costing, the income statement does not reveal true profits

and there is a probability that profits would be overstated during inflation period.

Misleading information:

It is certainly possible that the fundamental value of assets will not be indicative by

observed value of assets that are used under fair value accounting. Not all the publicly

available information might be reflected in the formation of estimates as market has the

probability of being inefficient. In this regard, historical costing method would be considered

suitable. Market deviation can also be caused due to other factors such as behavioural bias,

irrationality and prevalence of arbitrage (Whittington 2014).

Valuation policies of non-financial assets groups of three listed companies:

In this particular section, there companies have been selected from the three different

stock exchange that is Australian stock exchange, London stock exchange and New York

stock exchange for the evaluation of valuation policies of intangibles and PPE. These

8HISTORICAL COST VERSUS FAIR VALUE ACCOUNTING

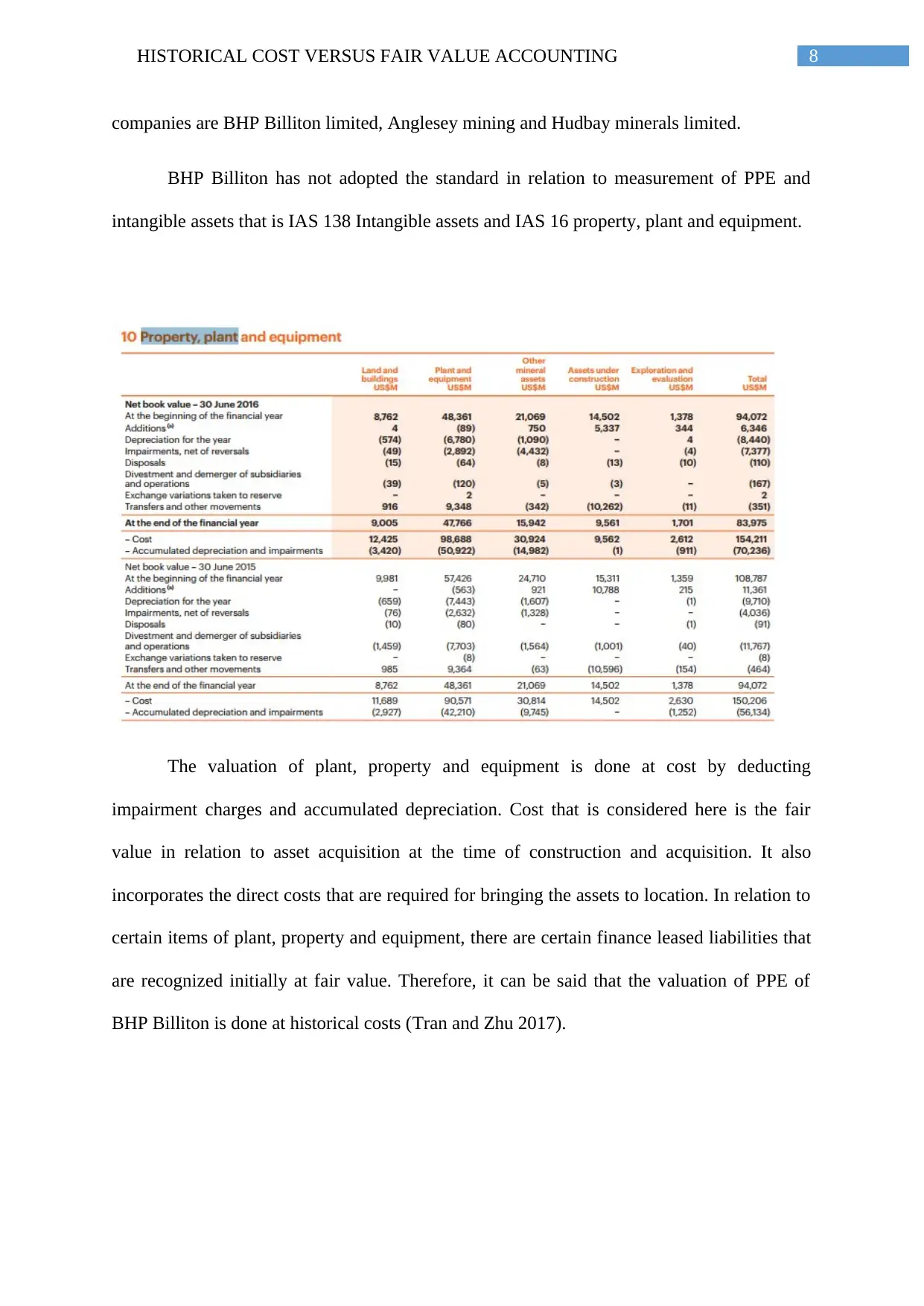

companies are BHP Billiton limited, Anglesey mining and Hudbay minerals limited.

BHP Billiton has not adopted the standard in relation to measurement of PPE and

intangible assets that is IAS 138 Intangible assets and IAS 16 property, plant and equipment.

The valuation of plant, property and equipment is done at cost by deducting

impairment charges and accumulated depreciation. Cost that is considered here is the fair

value in relation to asset acquisition at the time of construction and acquisition. It also

incorporates the direct costs that are required for bringing the assets to location. In relation to

certain items of plant, property and equipment, there are certain finance leased liabilities that

are recognized initially at fair value. Therefore, it can be said that the valuation of PPE of

BHP Billiton is done at historical costs (Tran and Zhu 2017).

companies are BHP Billiton limited, Anglesey mining and Hudbay minerals limited.

BHP Billiton has not adopted the standard in relation to measurement of PPE and

intangible assets that is IAS 138 Intangible assets and IAS 16 property, plant and equipment.

The valuation of plant, property and equipment is done at cost by deducting

impairment charges and accumulated depreciation. Cost that is considered here is the fair

value in relation to asset acquisition at the time of construction and acquisition. It also

incorporates the direct costs that are required for bringing the assets to location. In relation to

certain items of plant, property and equipment, there are certain finance leased liabilities that

are recognized initially at fair value. Therefore, it can be said that the valuation of PPE of

BHP Billiton is done at historical costs (Tran and Zhu 2017).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9HISTORICAL COST VERSUS FAIR VALUE ACCOUNTING

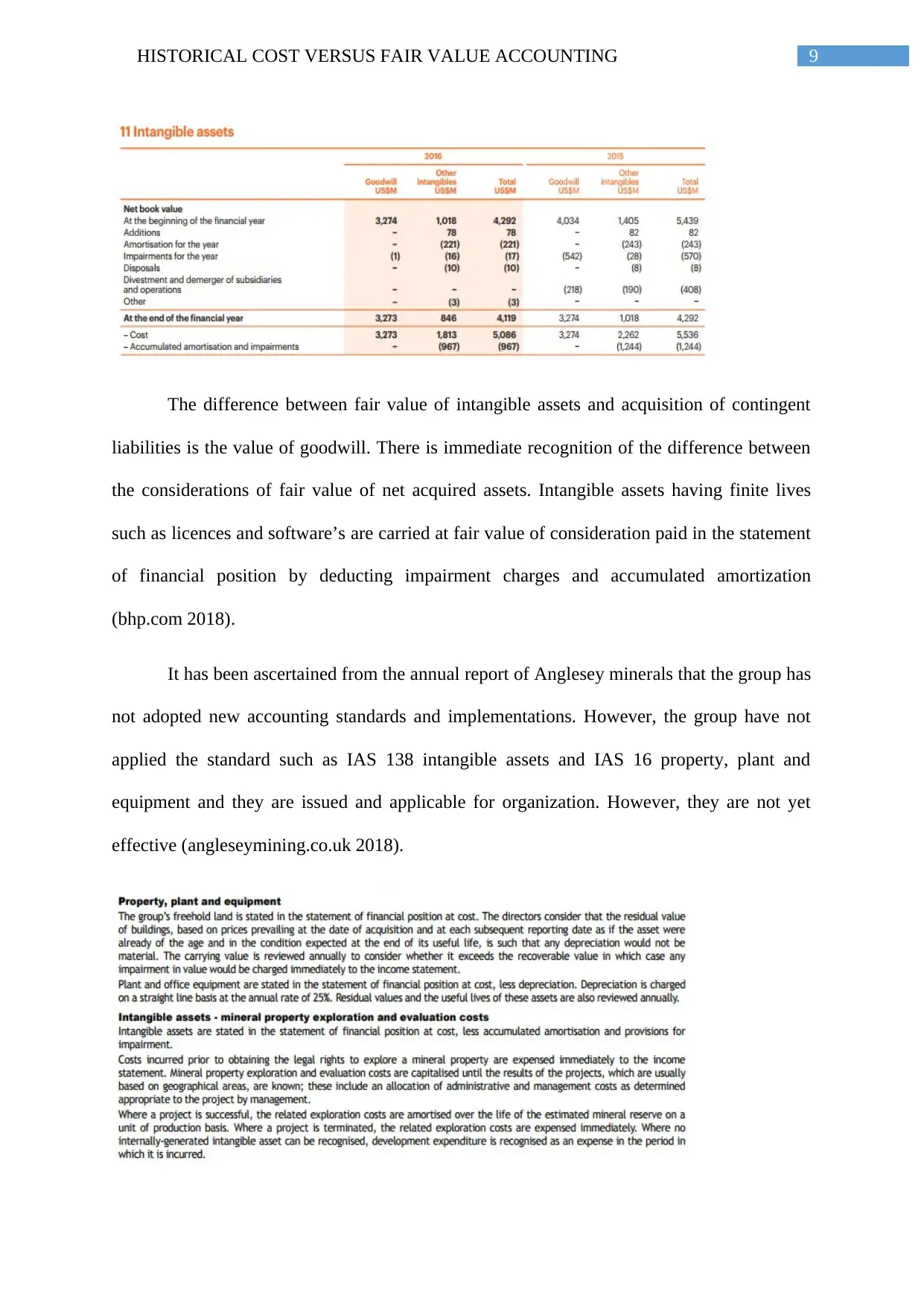

The difference between fair value of intangible assets and acquisition of contingent

liabilities is the value of goodwill. There is immediate recognition of the difference between

the considerations of fair value of net acquired assets. Intangible assets having finite lives

such as licences and software’s are carried at fair value of consideration paid in the statement

of financial position by deducting impairment charges and accumulated amortization

(bhp.com 2018).

It has been ascertained from the annual report of Anglesey minerals that the group has

not adopted new accounting standards and implementations. However, the group have not

applied the standard such as IAS 138 intangible assets and IAS 16 property, plant and

equipment and they are issued and applicable for organization. However, they are not yet

effective (angleseymining.co.uk 2018).

The difference between fair value of intangible assets and acquisition of contingent

liabilities is the value of goodwill. There is immediate recognition of the difference between

the considerations of fair value of net acquired assets. Intangible assets having finite lives

such as licences and software’s are carried at fair value of consideration paid in the statement

of financial position by deducting impairment charges and accumulated amortization

(bhp.com 2018).

It has been ascertained from the annual report of Anglesey minerals that the group has

not adopted new accounting standards and implementations. However, the group have not

applied the standard such as IAS 138 intangible assets and IAS 16 property, plant and

equipment and they are issued and applicable for organization. However, they are not yet

effective (angleseymining.co.uk 2018).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10HISTORICAL COST VERSUS FAIR VALUE ACCOUNTING

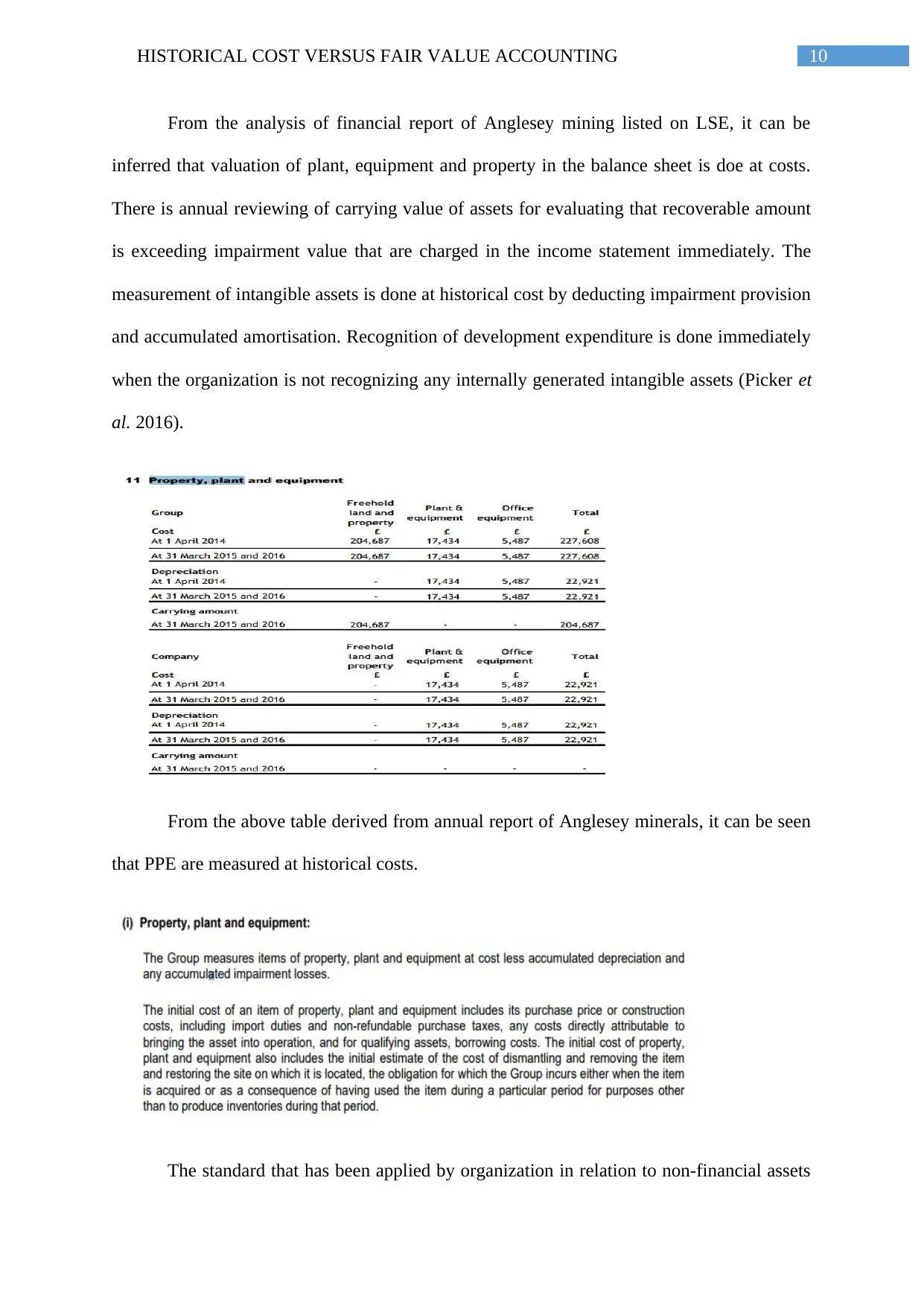

From the analysis of financial report of Anglesey mining listed on LSE, it can be

inferred that valuation of plant, equipment and property in the balance sheet is doe at costs.

There is annual reviewing of carrying value of assets for evaluating that recoverable amount

is exceeding impairment value that are charged in the income statement immediately. The

measurement of intangible assets is done at historical cost by deducting impairment provision

and accumulated amortisation. Recognition of development expenditure is done immediately

when the organization is not recognizing any internally generated intangible assets (Picker et

al. 2016).

From the above table derived from annual report of Anglesey minerals, it can be seen

that PPE are measured at historical costs.

The standard that has been applied by organization in relation to non-financial assets

From the analysis of financial report of Anglesey mining listed on LSE, it can be

inferred that valuation of plant, equipment and property in the balance sheet is doe at costs.

There is annual reviewing of carrying value of assets for evaluating that recoverable amount

is exceeding impairment value that are charged in the income statement immediately. The

measurement of intangible assets is done at historical cost by deducting impairment provision

and accumulated amortisation. Recognition of development expenditure is done immediately

when the organization is not recognizing any internally generated intangible assets (Picker et

al. 2016).

From the above table derived from annual report of Anglesey minerals, it can be seen

that PPE are measured at historical costs.

The standard that has been applied by organization in relation to non-financial assets

11HISTORICAL COST VERSUS FAIR VALUE ACCOUNTING

are IAS 138, Intangible assets and IAS 16, plant, property and equipment. It has been

ascertained from the analysis of annual report of Hudbay minerals that items of PPE is

measured by group at cost by deducting any impairment losses that are accumulated over

years and accumulated depreciation (Hudbayminerals.com 2018). However, the initial costs

incurred on such assets does not incorporate cost of construction, price of purchasing, any

direct costs, non refundable purchase taxes and import duties.

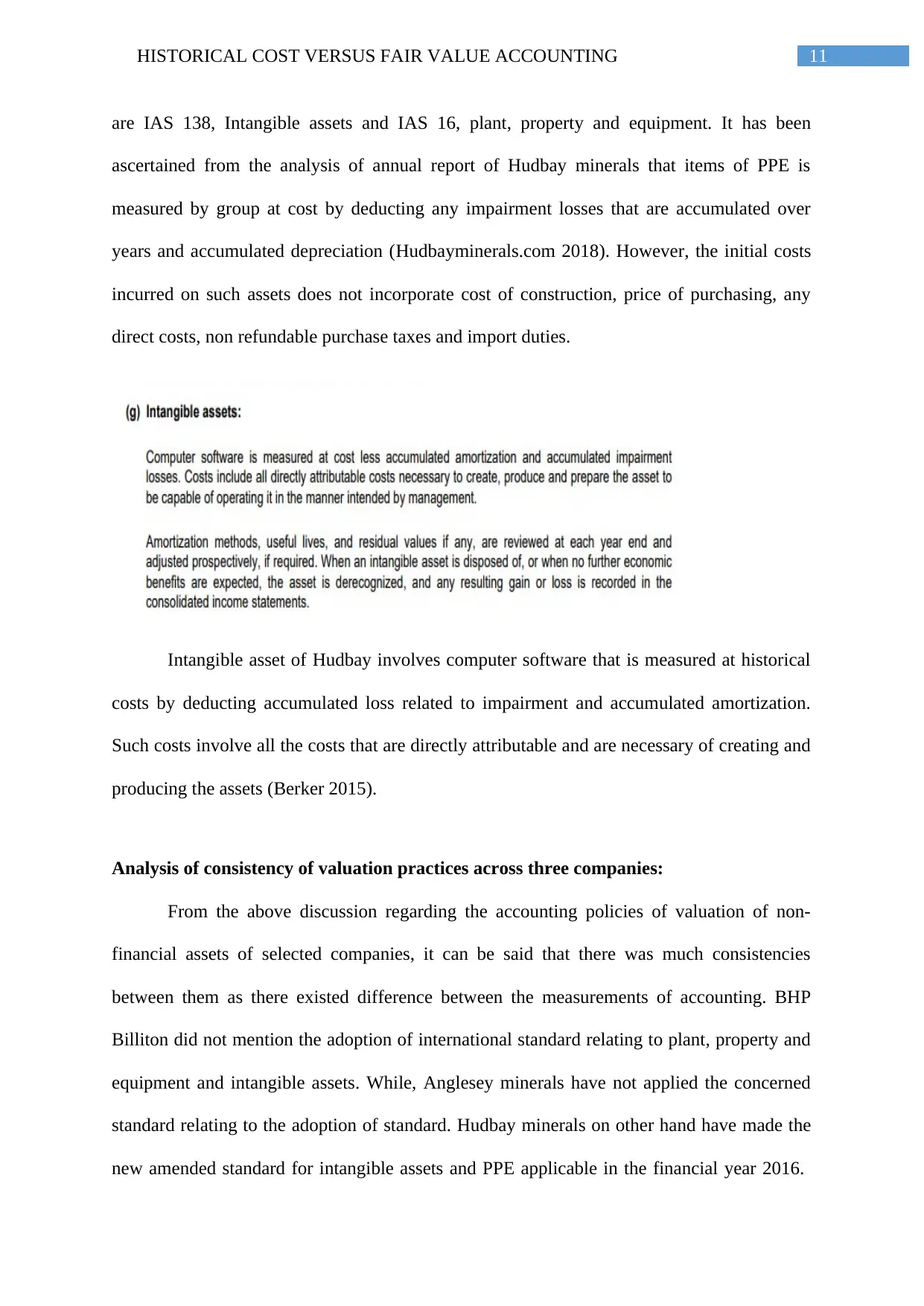

Intangible asset of Hudbay involves computer software that is measured at historical

costs by deducting accumulated loss related to impairment and accumulated amortization.

Such costs involve all the costs that are directly attributable and are necessary of creating and

producing the assets (Berker 2015).

Analysis of consistency of valuation practices across three companies:

From the above discussion regarding the accounting policies of valuation of non-

financial assets of selected companies, it can be said that there was much consistencies

between them as there existed difference between the measurements of accounting. BHP

Billiton did not mention the adoption of international standard relating to plant, property and

equipment and intangible assets. While, Anglesey minerals have not applied the concerned

standard relating to the adoption of standard. Hudbay minerals on other hand have made the

new amended standard for intangible assets and PPE applicable in the financial year 2016.

are IAS 138, Intangible assets and IAS 16, plant, property and equipment. It has been

ascertained from the analysis of annual report of Hudbay minerals that items of PPE is

measured by group at cost by deducting any impairment losses that are accumulated over

years and accumulated depreciation (Hudbayminerals.com 2018). However, the initial costs

incurred on such assets does not incorporate cost of construction, price of purchasing, any

direct costs, non refundable purchase taxes and import duties.

Intangible asset of Hudbay involves computer software that is measured at historical

costs by deducting accumulated loss related to impairment and accumulated amortization.

Such costs involve all the costs that are directly attributable and are necessary of creating and

producing the assets (Berker 2015).

Analysis of consistency of valuation practices across three companies:

From the above discussion regarding the accounting policies of valuation of non-

financial assets of selected companies, it can be said that there was much consistencies

between them as there existed difference between the measurements of accounting. BHP

Billiton did not mention the adoption of international standard relating to plant, property and

equipment and intangible assets. While, Anglesey minerals have not applied the concerned

standard relating to the adoption of standard. Hudbay minerals on other hand have made the

new amended standard for intangible assets and PPE applicable in the financial year 2016.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.