HNBS 310 - Financial Accounting Assignment

VerifiedAdded on 2020/12/18

|18

|2649

|302

AI Summary

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

HNBS 310 Financial

Accounting

Accounting

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Table of Contents

Table of Contents.............................................................................................................................2

INTRODUCTION...........................................................................................................................1

SCENARIO 1..................................................................................................................................1

Question 1....................................................................................................................................1

Question2.....................................................................................................................................6

SCENARIO 2................................................................................................................................12

Question 1..................................................................................................................................12

Question 2..................................................................................................................................15

CONCLUSION..............................................................................................................................16

REFERENCES..............................................................................................................................17

Table of Contents.............................................................................................................................2

INTRODUCTION...........................................................................................................................1

SCENARIO 1..................................................................................................................................1

Question 1....................................................................................................................................1

Question2.....................................................................................................................................6

SCENARIO 2................................................................................................................................12

Question 1..................................................................................................................................12

Question 2..................................................................................................................................15

CONCLUSION..............................................................................................................................16

REFERENCES..............................................................................................................................17

INTRODUCTION

In business context, financial accounting is a key process of analysing, recording,

reporting the summaries financial and business transaction that are happened due to different

operation in a specific time frame (Financial accounting, 2019). Manager use to prepare various

financial statements according to GAAP guidelines so that exact strength and position can be

determined. The crucial financial statements are cash flow statement, trading profit and loss

account and balance sheet that are beneficial to report the company operating performance over a

specific accounting year. In this report, journal entries, ledger account and trail balance is

discussed. Report also cover, accounts for sole trader, partnership companies that are prepared

with the support of appropriate standards and principle. Additional in report, bank reconciliation

statements, control and suspense accounts and are being presented in according to guidelines.

SCENARIO 1

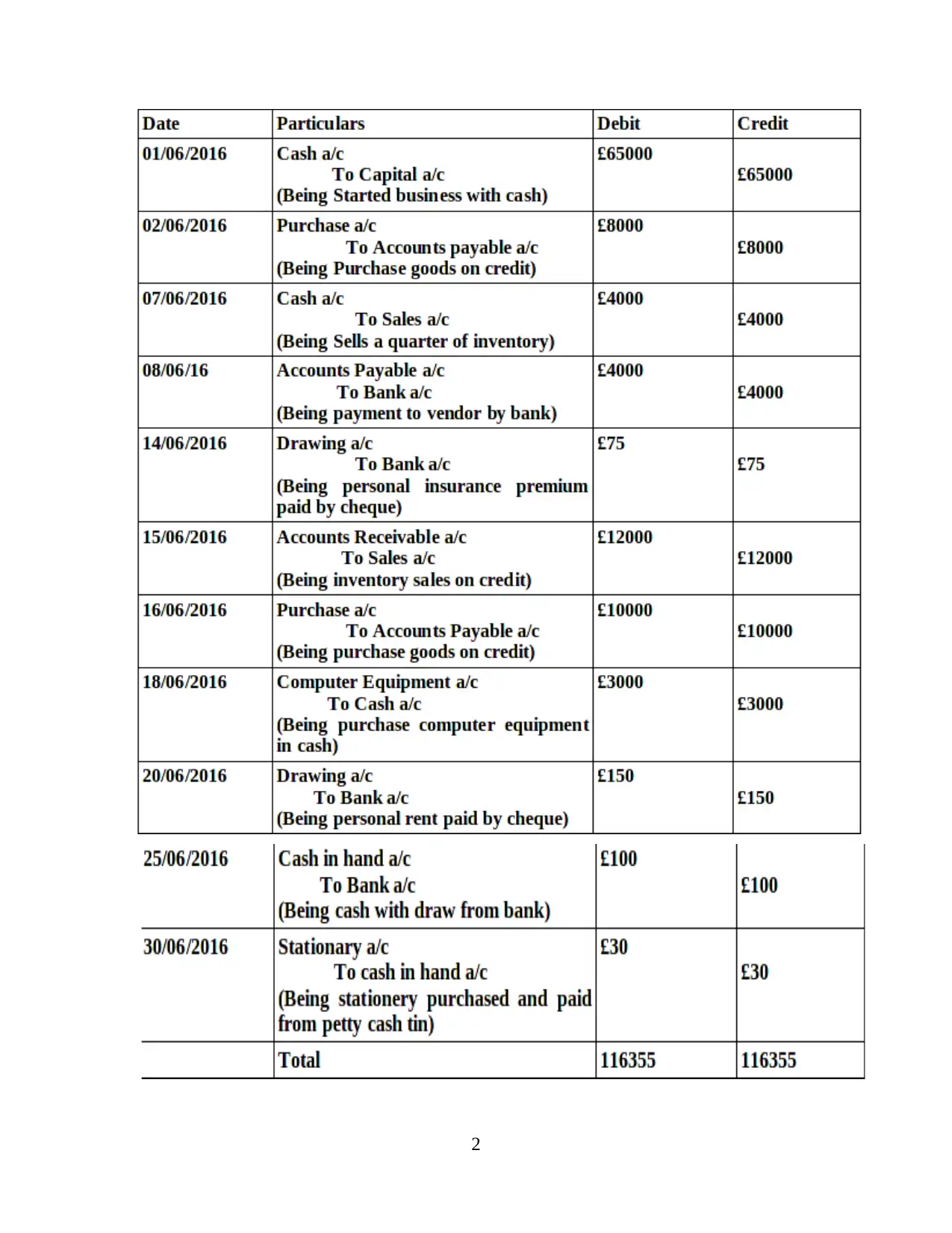

Question 1

Journal entries: The systematic way that is used to record the business transaction in

authentic records of a business transaction (Chen, 2015). The main concept behind making

accounting entries is to record each and every kind of business operation at least in two place

that is known as double entry. For instance, when there is sales on cash it will increase revenue

as well as cash accounts. There are different kind of journal entries such as adjustment entry,

compound and reversing entry.

1

In business context, financial accounting is a key process of analysing, recording,

reporting the summaries financial and business transaction that are happened due to different

operation in a specific time frame (Financial accounting, 2019). Manager use to prepare various

financial statements according to GAAP guidelines so that exact strength and position can be

determined. The crucial financial statements are cash flow statement, trading profit and loss

account and balance sheet that are beneficial to report the company operating performance over a

specific accounting year. In this report, journal entries, ledger account and trail balance is

discussed. Report also cover, accounts for sole trader, partnership companies that are prepared

with the support of appropriate standards and principle. Additional in report, bank reconciliation

statements, control and suspense accounts and are being presented in according to guidelines.

SCENARIO 1

Question 1

Journal entries: The systematic way that is used to record the business transaction in

authentic records of a business transaction (Chen, 2015). The main concept behind making

accounting entries is to record each and every kind of business operation at least in two place

that is known as double entry. For instance, when there is sales on cash it will increase revenue

as well as cash accounts. There are different kind of journal entries such as adjustment entry,

compound and reversing entry.

1

2

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

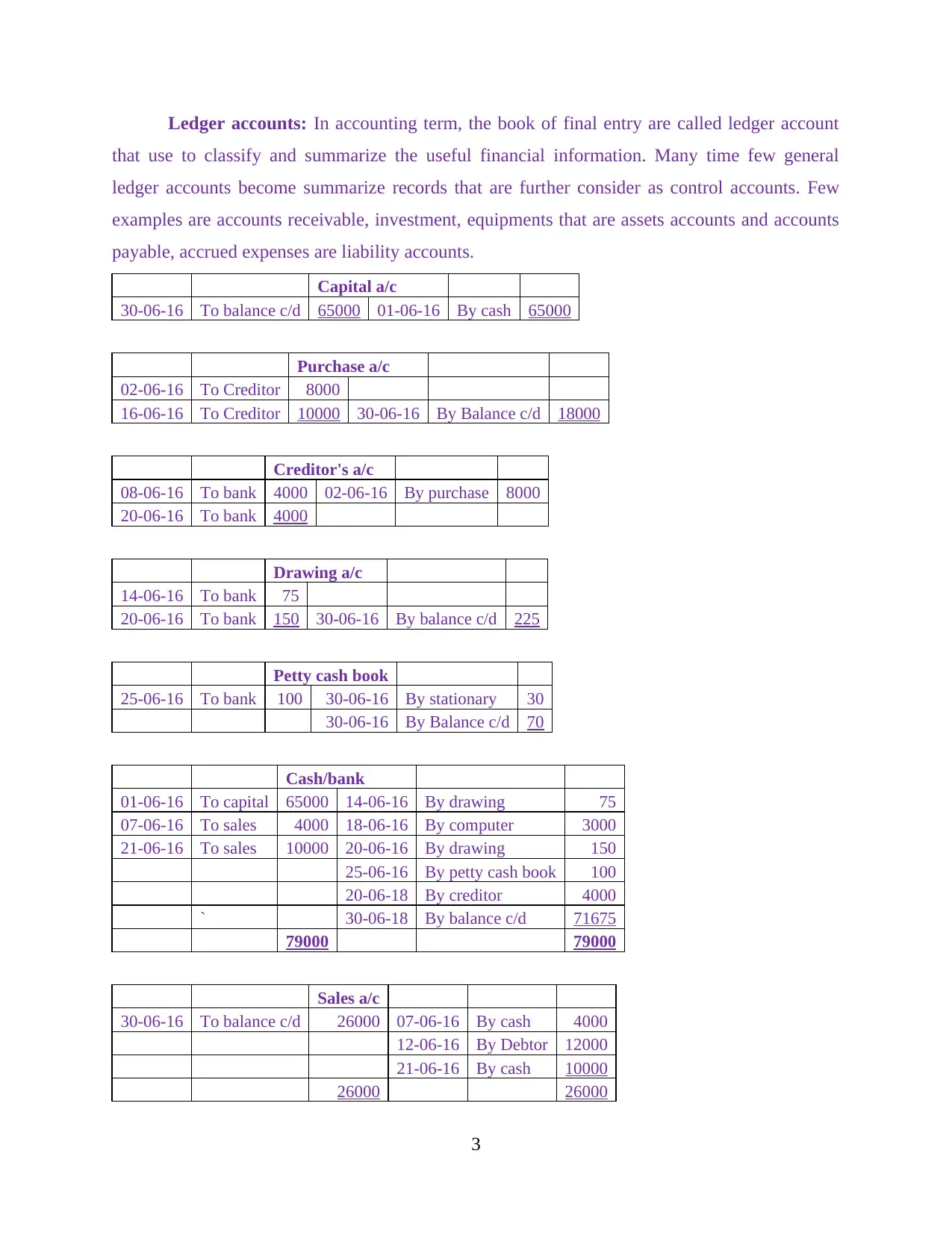

Ledger accounts: In accounting term, the book of final entry are called ledger account

that use to classify and summarize the useful financial information. Many time few general

ledger accounts become summarize records that are further consider as control accounts. Few

examples are accounts receivable, investment, equipments that are assets accounts and accounts

payable, accrued expenses are liability accounts.

Capital a/c

30-06-16 To balance c/d 65000 01-06-16 By cash 65000

Purchase a/c

02-06-16 To Creditor 8000

16-06-16 To Creditor 10000 30-06-16 By Balance c/d 18000

Creditor's a/c

08-06-16 To bank 4000 02-06-16 By purchase 8000

20-06-16 To bank 4000

Drawing a/c

14-06-16 To bank 75

20-06-16 To bank 150 30-06-16 By balance c/d 225

Petty cash book

25-06-16 To bank 100 30-06-16 By stationary 30

30-06-16 By Balance c/d 70

Cash/bank

01-06-16 To capital 65000 14-06-16 By drawing 75

07-06-16 To sales 4000 18-06-16 By computer 3000

21-06-16 To sales 10000 20-06-16 By drawing 150

25-06-16 By petty cash book 100

20-06-18 By creditor 4000

` 30-06-18 By balance c/d 71675

79000 79000

Sales a/c

30-06-16 To balance c/d 26000 07-06-16 By cash 4000

12-06-16 By Debtor 12000

21-06-16 By cash 10000

26000 26000

3

that use to classify and summarize the useful financial information. Many time few general

ledger accounts become summarize records that are further consider as control accounts. Few

examples are accounts receivable, investment, equipments that are assets accounts and accounts

payable, accrued expenses are liability accounts.

Capital a/c

30-06-16 To balance c/d 65000 01-06-16 By cash 65000

Purchase a/c

02-06-16 To Creditor 8000

16-06-16 To Creditor 10000 30-06-16 By Balance c/d 18000

Creditor's a/c

08-06-16 To bank 4000 02-06-16 By purchase 8000

20-06-16 To bank 4000

Drawing a/c

14-06-16 To bank 75

20-06-16 To bank 150 30-06-16 By balance c/d 225

Petty cash book

25-06-16 To bank 100 30-06-16 By stationary 30

30-06-16 By Balance c/d 70

Cash/bank

01-06-16 To capital 65000 14-06-16 By drawing 75

07-06-16 To sales 4000 18-06-16 By computer 3000

21-06-16 To sales 10000 20-06-16 By drawing 150

25-06-16 By petty cash book 100

20-06-18 By creditor 4000

` 30-06-18 By balance c/d 71675

79000 79000

Sales a/c

30-06-16 To balance c/d 26000 07-06-16 By cash 4000

12-06-16 By Debtor 12000

21-06-16 By cash 10000

26000 26000

3

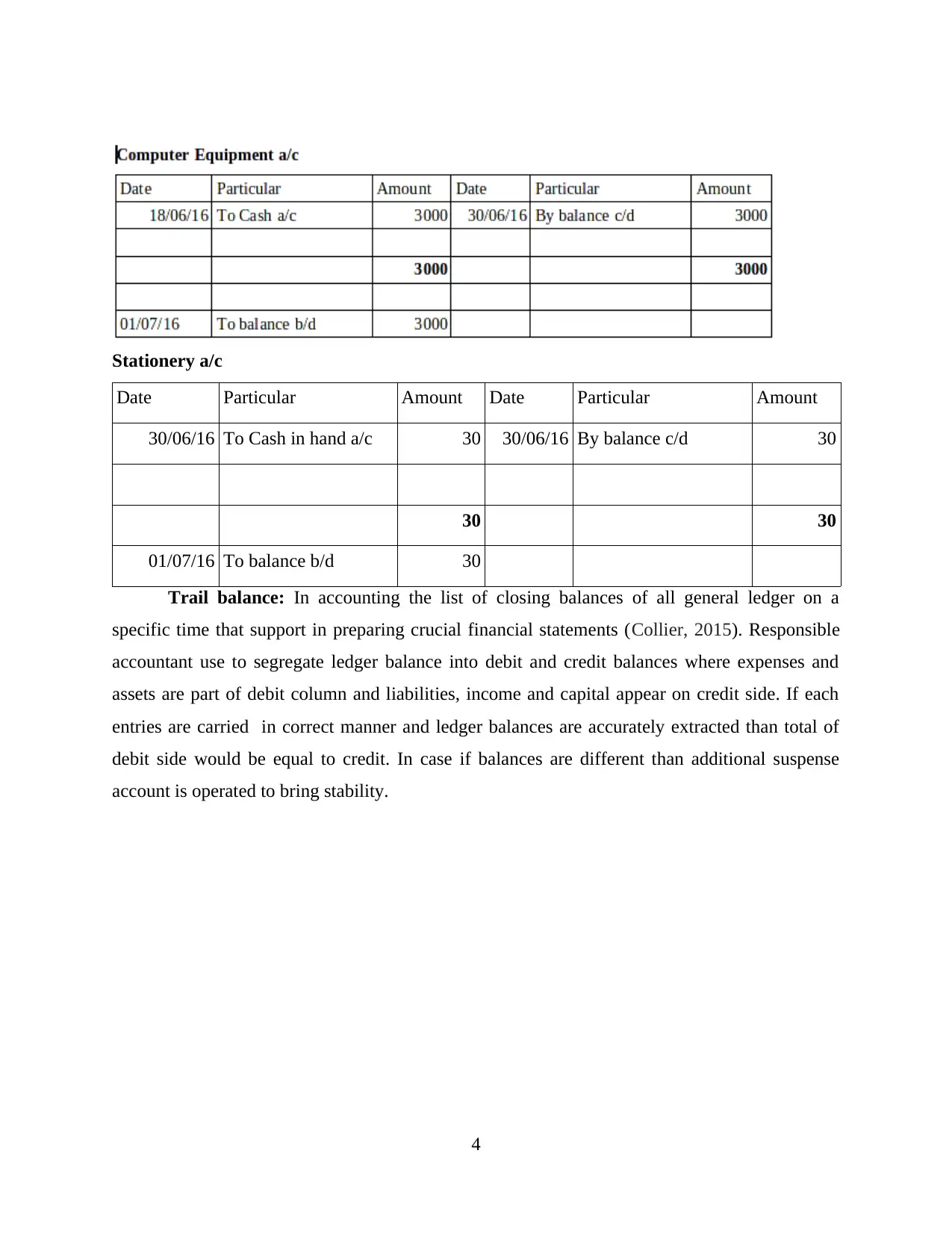

Stationery a/c

Date Particular Amount Date Particular Amount

30/06/16 To Cash in hand a/c 30 30/06/16 By balance c/d 30

30 30

01/07/16 To balance b/d 30

Trail balance: In accounting the list of closing balances of all general ledger on a

specific time that support in preparing crucial financial statements (Collier, 2015). Responsible

accountant use to segregate ledger balance into debit and credit balances where expenses and

assets are part of debit column and liabilities, income and capital appear on credit side. If each

entries are carried in correct manner and ledger balances are accurately extracted than total of

debit side would be equal to credit. In case if balances are different than additional suspense

account is operated to bring stability.

4

Date Particular Amount Date Particular Amount

30/06/16 To Cash in hand a/c 30 30/06/16 By balance c/d 30

30 30

01/07/16 To balance b/d 30

Trail balance: In accounting the list of closing balances of all general ledger on a

specific time that support in preparing crucial financial statements (Collier, 2015). Responsible

accountant use to segregate ledger balance into debit and credit balances where expenses and

assets are part of debit column and liabilities, income and capital appear on credit side. If each

entries are carried in correct manner and ledger balances are accurately extracted than total of

debit side would be equal to credit. In case if balances are different than additional suspense

account is operated to bring stability.

4

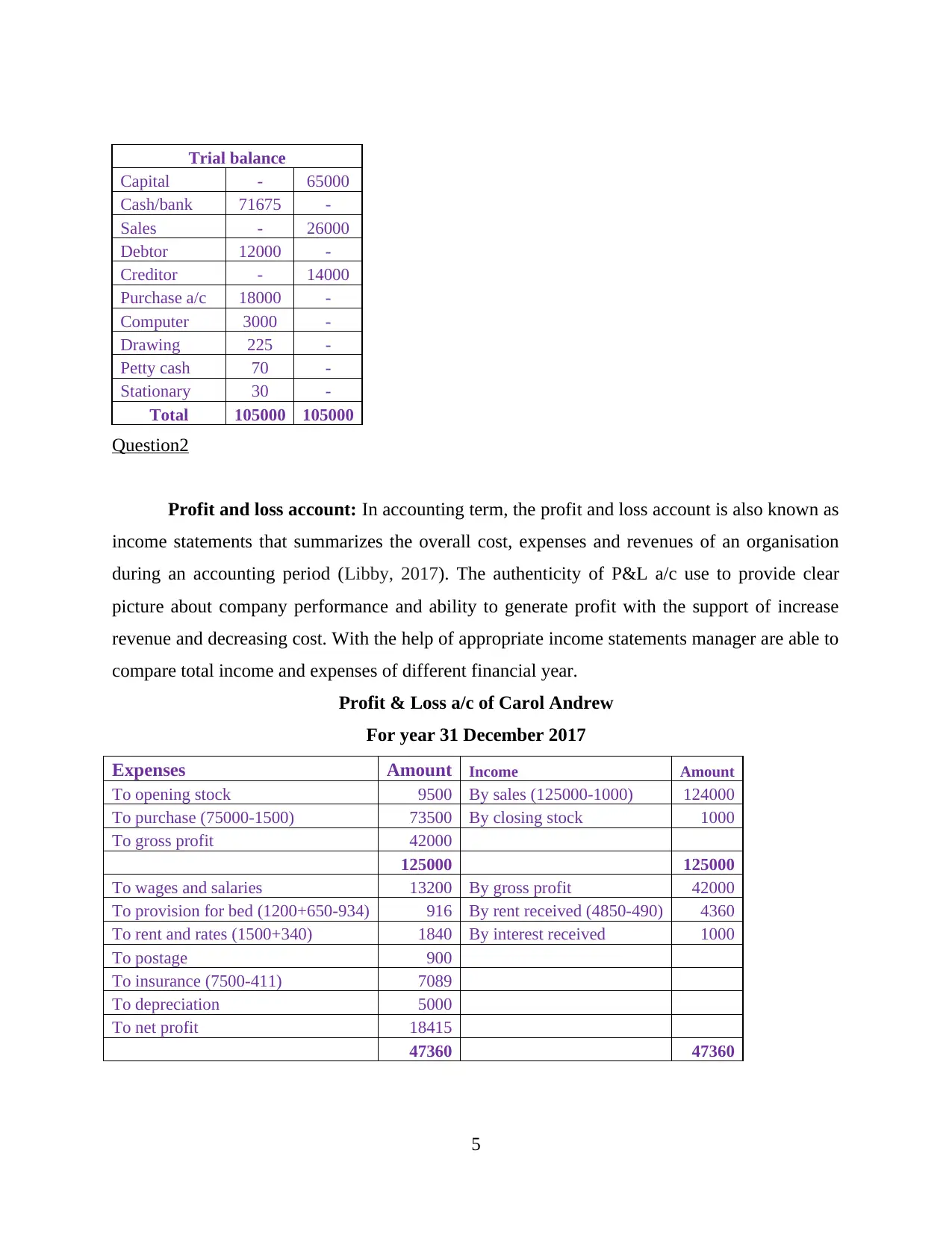

Trial balance

Capital - 65000

Cash/bank 71675 -

Sales - 26000

Debtor 12000 -

Creditor - 14000

Purchase a/c 18000 -

Computer 3000 -

Drawing 225 -

Petty cash 70 -

Stationary 30 -

Total 105000 105000

Question2

Profit and loss account: In accounting term, the profit and loss account is also known as

income statements that summarizes the overall cost, expenses and revenues of an organisation

during an accounting period (Libby, 2017). The authenticity of P&L a/c use to provide clear

picture about company performance and ability to generate profit with the support of increase

revenue and decreasing cost. With the help of appropriate income statements manager are able to

compare total income and expenses of different financial year.

Profit & Loss a/c of Carol Andrew

For year 31 December 2017

Expenses Amount Income Amount

To opening stock 9500 By sales (125000-1000) 124000

To purchase (75000-1500) 73500 By closing stock 1000

To gross profit 42000

125000 125000

To wages and salaries 13200 By gross profit 42000

To provision for bed (1200+650-934) 916 By rent received (4850-490) 4360

To rent and rates (1500+340) 1840 By interest received 1000

To postage 900

To insurance (7500-411) 7089

To depreciation 5000

To net profit 18415

47360 47360

5

Capital - 65000

Cash/bank 71675 -

Sales - 26000

Debtor 12000 -

Creditor - 14000

Purchase a/c 18000 -

Computer 3000 -

Drawing 225 -

Petty cash 70 -

Stationary 30 -

Total 105000 105000

Question2

Profit and loss account: In accounting term, the profit and loss account is also known as

income statements that summarizes the overall cost, expenses and revenues of an organisation

during an accounting period (Libby, 2017). The authenticity of P&L a/c use to provide clear

picture about company performance and ability to generate profit with the support of increase

revenue and decreasing cost. With the help of appropriate income statements manager are able to

compare total income and expenses of different financial year.

Profit & Loss a/c of Carol Andrew

For year 31 December 2017

Expenses Amount Income Amount

To opening stock 9500 By sales (125000-1000) 124000

To purchase (75000-1500) 73500 By closing stock 1000

To gross profit 42000

125000 125000

To wages and salaries 13200 By gross profit 42000

To provision for bed (1200+650-934) 916 By rent received (4850-490) 4360

To rent and rates (1500+340) 1840 By interest received 1000

To postage 900

To insurance (7500-411) 7089

To depreciation 5000

To net profit 18415

47360 47360

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

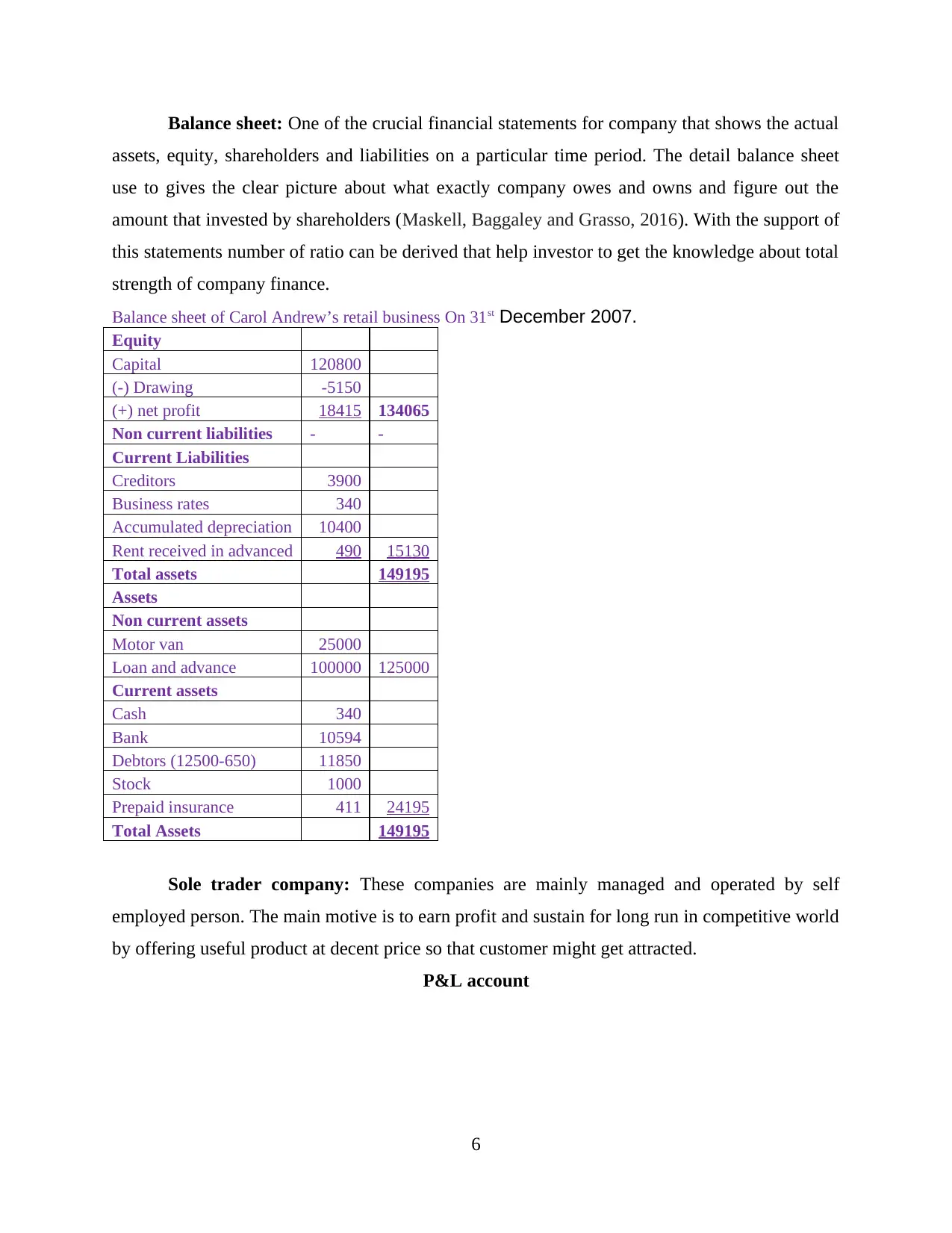

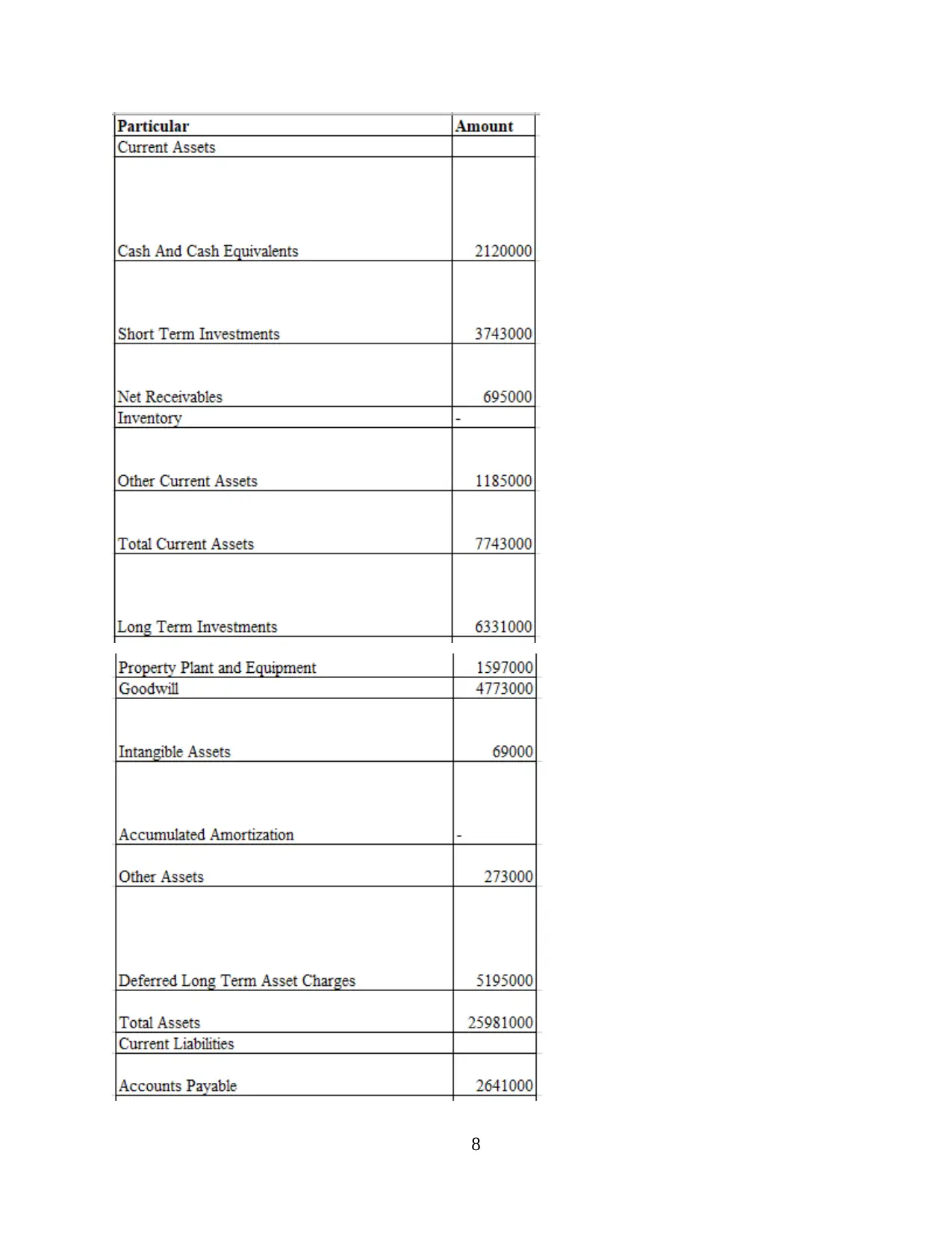

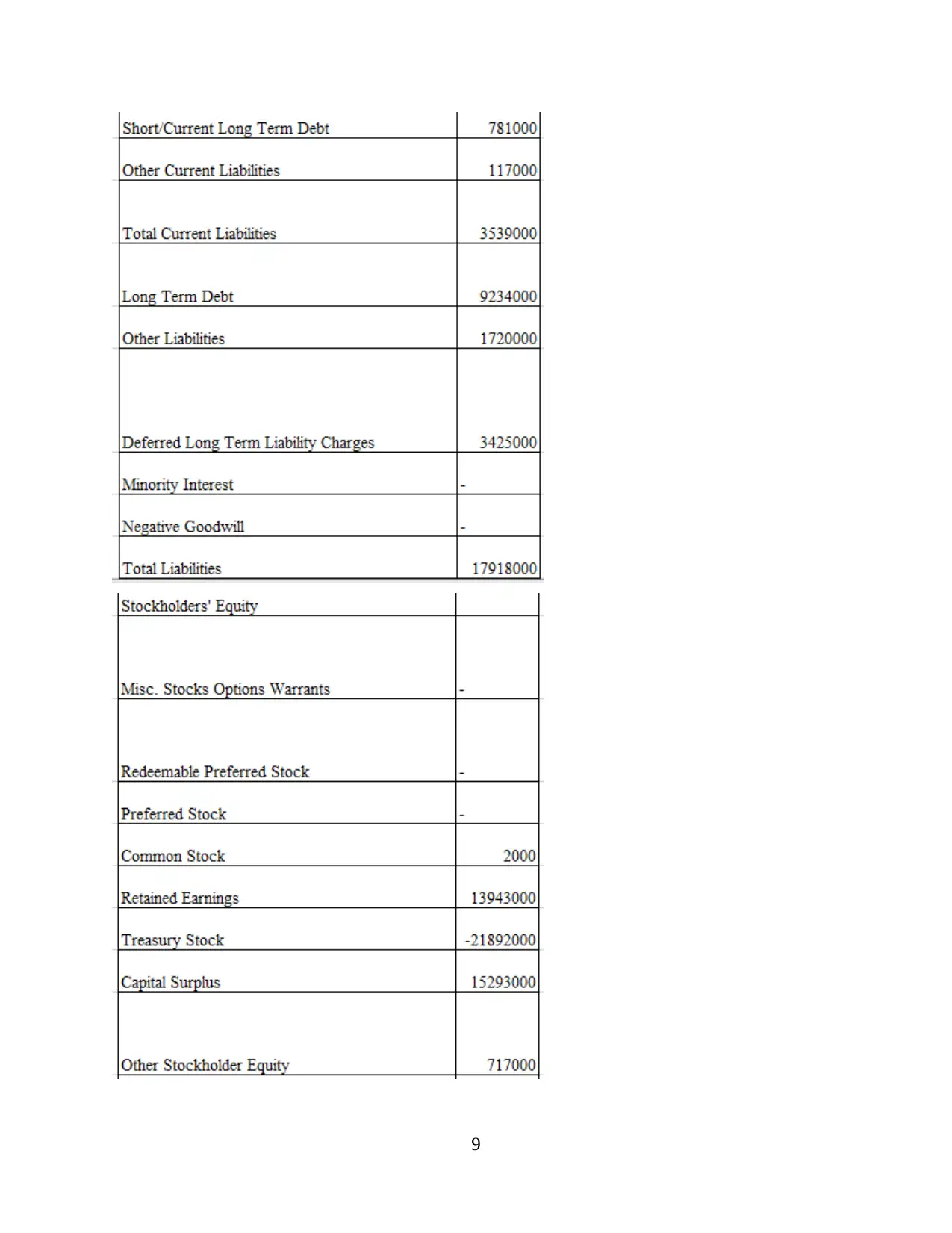

Balance sheet: One of the crucial financial statements for company that shows the actual

assets, equity, shareholders and liabilities on a particular time period. The detail balance sheet

use to gives the clear picture about what exactly company owes and owns and figure out the

amount that invested by shareholders (Maskell, Baggaley and Grasso, 2016). With the support of

this statements number of ratio can be derived that help investor to get the knowledge about total

strength of company finance.

Balance sheet of Carol Andrew’s retail business On 31st December 2007.

Equity

Capital 120800

(-) Drawing -5150

(+) net profit 18415 134065

Non current liabilities - -

Current Liabilities

Creditors 3900

Business rates 340

Accumulated depreciation 10400

Rent received in advanced 490 15130

Total assets 149195

Assets

Non current assets

Motor van 25000

Loan and advance 100000 125000

Current assets

Cash 340

Bank 10594

Debtors (12500-650) 11850

Stock 1000

Prepaid insurance 411 24195

Total Assets 149195

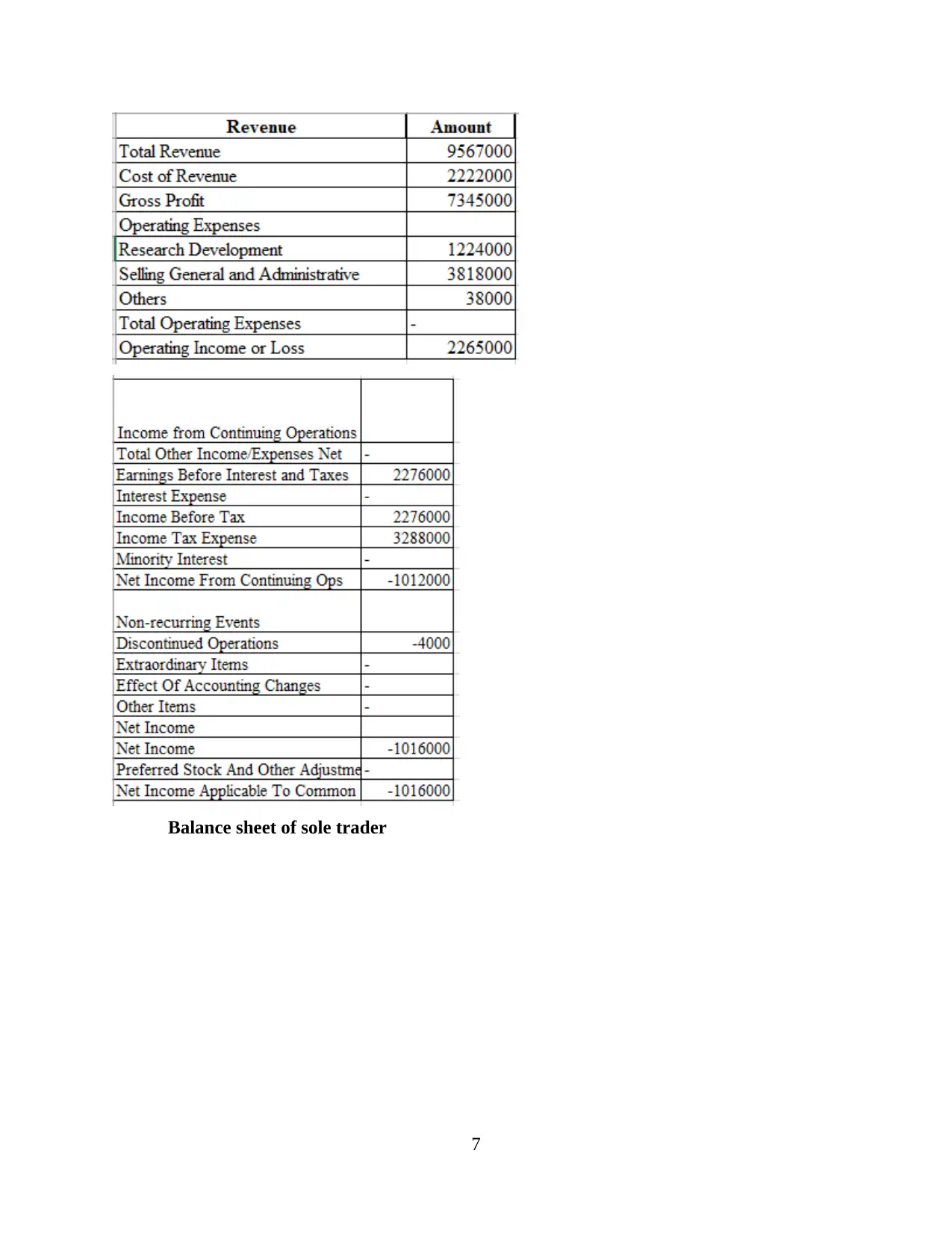

Sole trader company: These companies are mainly managed and operated by self

employed person. The main motive is to earn profit and sustain for long run in competitive world

by offering useful product at decent price so that customer might get attracted.

P&L account

6

assets, equity, shareholders and liabilities on a particular time period. The detail balance sheet

use to gives the clear picture about what exactly company owes and owns and figure out the

amount that invested by shareholders (Maskell, Baggaley and Grasso, 2016). With the support of

this statements number of ratio can be derived that help investor to get the knowledge about total

strength of company finance.

Balance sheet of Carol Andrew’s retail business On 31st December 2007.

Equity

Capital 120800

(-) Drawing -5150

(+) net profit 18415 134065

Non current liabilities - -

Current Liabilities

Creditors 3900

Business rates 340

Accumulated depreciation 10400

Rent received in advanced 490 15130

Total assets 149195

Assets

Non current assets

Motor van 25000

Loan and advance 100000 125000

Current assets

Cash 340

Bank 10594

Debtors (12500-650) 11850

Stock 1000

Prepaid insurance 411 24195

Total Assets 149195

Sole trader company: These companies are mainly managed and operated by self

employed person. The main motive is to earn profit and sustain for long run in competitive world

by offering useful product at decent price so that customer might get attracted.

P&L account

6

Balance sheet of sole trader

7

7

8

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

9

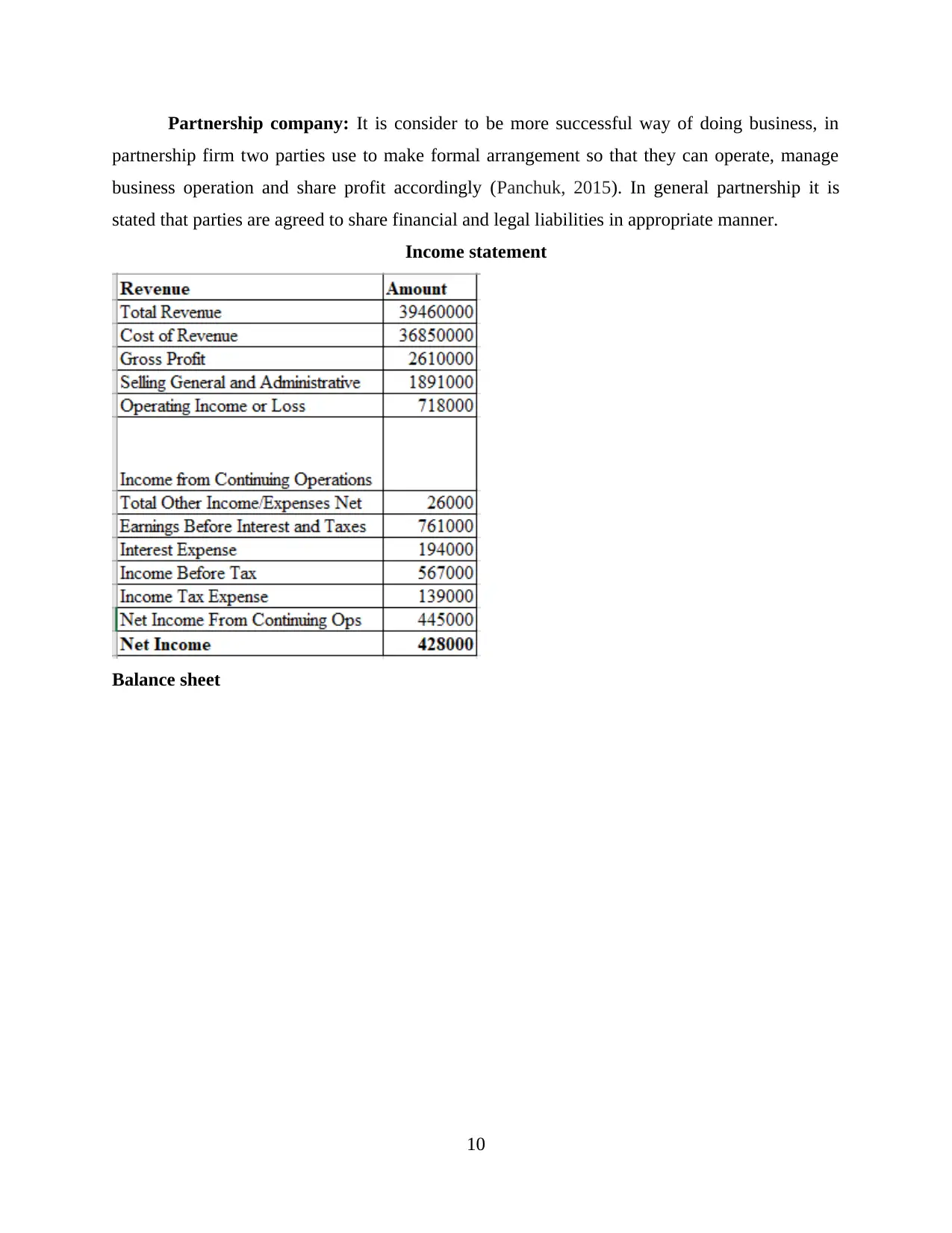

Partnership company: It is consider to be more successful way of doing business, in

partnership firm two parties use to make formal arrangement so that they can operate, manage

business operation and share profit accordingly (Panchuk, 2015). In general partnership it is

stated that parties are agreed to share financial and legal liabilities in appropriate manner.

Income statement

Balance sheet

10

partnership firm two parties use to make formal arrangement so that they can operate, manage

business operation and share profit accordingly (Panchuk, 2015). In general partnership it is

stated that parties are agreed to share financial and legal liabilities in appropriate manner.

Income statement

Balance sheet

10

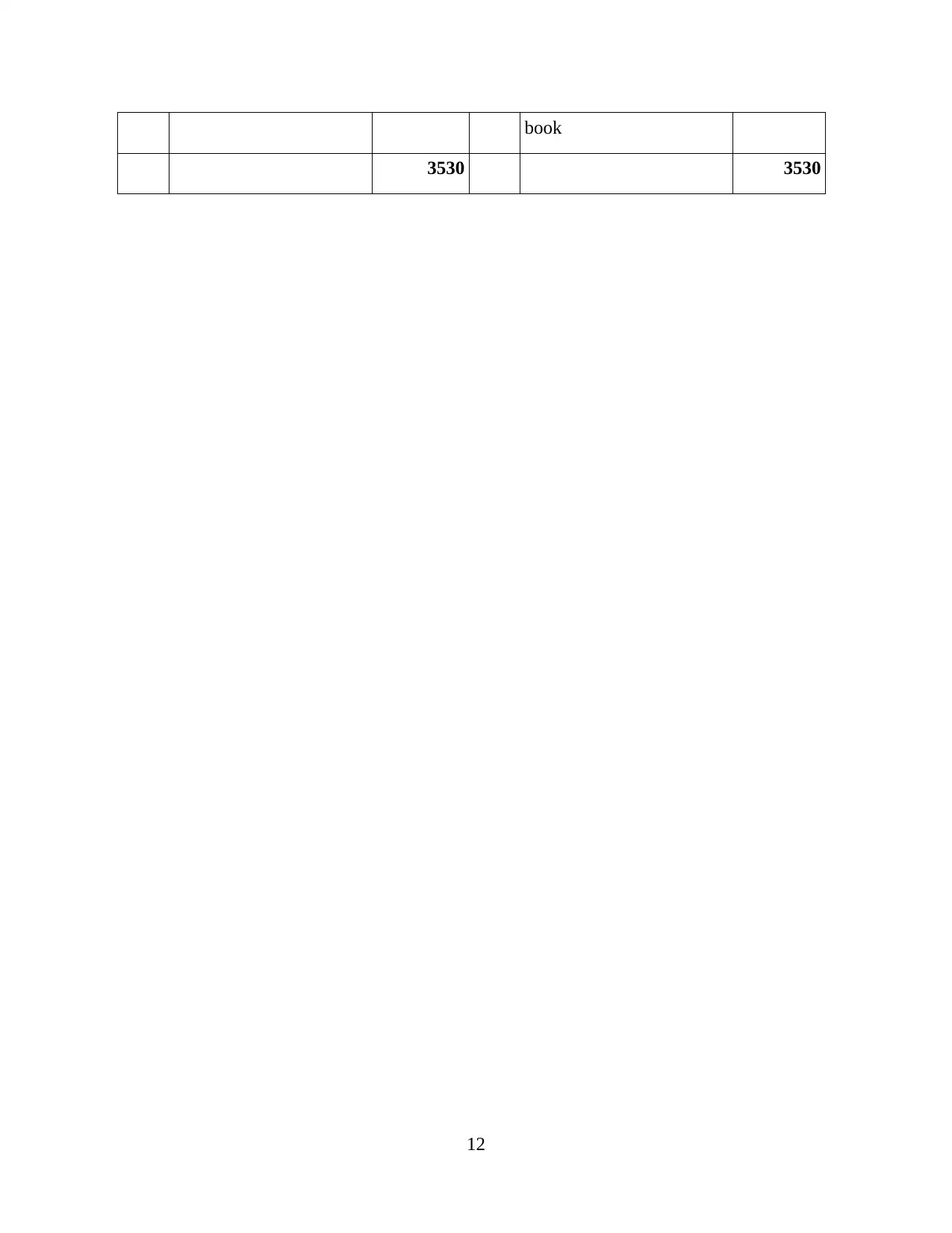

SCENARIO 2

Question 1

A) Updated cash book

Revised cash Book (as per bank column)

Date Particulars

Dr.

balance Date Particulars

Cr.

Balance

Balance as per cash book 1760 Insurance paid 170

Cheque not yet presented 270 Monthly bill 56

Transfer from mr patel 1070 Cheque from arif 186

Drawings 105 bank charges 25

Dividend received 325 By balance as per pass 3093

11

Question 1

A) Updated cash book

Revised cash Book (as per bank column)

Date Particulars

Dr.

balance Date Particulars

Cr.

Balance

Balance as per cash book 1760 Insurance paid 170

Cheque not yet presented 270 Monthly bill 56

Transfer from mr patel 1070 Cheque from arif 186

Drawings 105 bank charges 25

Dividend received 325 By balance as per pass 3093

11

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

book

3530 3530

12

3530 3530

12

b) Different term with example and actual differences:

Direct debit: In business scenario, direct debit is a type of pre authorised option for

making payment. An account holder use to give permission to bank to pay variable or fixed

amount to other bank, utility company etc. depending upon the actual bill to for the specific

period. Now a days direct debit is in demand as customer consider it as the simplest, fastest,

safest and most convenient way to make payment at regular interval. There are various benefit of

making payment through this option such as:

Convenient: It is automatic type of payment option so bills are never delayed, lost or

forgotten.

Cost: Many times companies are also offered different types of incentive by bank or other

businesses by making payment through direct debits.

Customer protection: It is consider to be the most safest payment option as customer do

not have to make any kind detail to be entered.

Companies use direct debit option for different purposes that are defined below:

Regular bills for variable amount: With the support of direct debit companies are able

to pay all important bills on time at the end of moths. For example, ABC company use to

give direct debit option for paying telephone bills on regular interval in a month on

specific date. These amount keeps on changing and bank detected the right amount

according to bills provided by telephone company.

Fixed subscription or membership: As discussed above it is the safest and easiest

method of making recurring payments such as newspaper bills, gym membership etc.

Paying an account: In many companies, manager use to provide direct debit the best

option for spreading the total cost or paying an expenses equal of accounts.

Standing order: It is also a type direct debit in which an instruction are given to bank to

make payment to specific individual or organisation. In this option person use to fix the amount

and decide the date on which payment must be made to party. For example, fixed and regular

payment for rent, donations, charity and some time regular payments into saving options. At the

same time opting this option have different risk such as an outstanding bill of gas connection

paid twice than the payment can no be refunded and utility provider would adjust in next billed

amount.

13

Direct debit: In business scenario, direct debit is a type of pre authorised option for

making payment. An account holder use to give permission to bank to pay variable or fixed

amount to other bank, utility company etc. depending upon the actual bill to for the specific

period. Now a days direct debit is in demand as customer consider it as the simplest, fastest,

safest and most convenient way to make payment at regular interval. There are various benefit of

making payment through this option such as:

Convenient: It is automatic type of payment option so bills are never delayed, lost or

forgotten.

Cost: Many times companies are also offered different types of incentive by bank or other

businesses by making payment through direct debits.

Customer protection: It is consider to be the most safest payment option as customer do

not have to make any kind detail to be entered.

Companies use direct debit option for different purposes that are defined below:

Regular bills for variable amount: With the support of direct debit companies are able

to pay all important bills on time at the end of moths. For example, ABC company use to

give direct debit option for paying telephone bills on regular interval in a month on

specific date. These amount keeps on changing and bank detected the right amount

according to bills provided by telephone company.

Fixed subscription or membership: As discussed above it is the safest and easiest

method of making recurring payments such as newspaper bills, gym membership etc.

Paying an account: In many companies, manager use to provide direct debit the best

option for spreading the total cost or paying an expenses equal of accounts.

Standing order: It is also a type direct debit in which an instruction are given to bank to

make payment to specific individual or organisation. In this option person use to fix the amount

and decide the date on which payment must be made to party. For example, fixed and regular

payment for rent, donations, charity and some time regular payments into saving options. At the

same time opting this option have different risk such as an outstanding bill of gas connection

paid twice than the payment can no be refunded and utility provider would adjust in next billed

amount.

13

Bank charges: In fast and changing environment, bank use to provide number of

services to their customer in order to ease their work and save time (Barth, Li and McClure,

2018). By providing these services bank charge specific amount from customer for maintenance

or further updates. Different services such as ATM card, internet and mobile banking, message

banking, overdrafts etc. are provided by bank to customer on which they use to charge fixed or

variable charges for respective accounts. Fixed charges remain the same throughout the time

period customer have account in certain bank such as, internet and message banking. On the

other side variable changes such as card issuance fee, ATM withdrawal charges after free

transaction etc.

Dishonour of cheque: Many times there are situation in which bank use to reject the

cheque which are presented by customer to make specific payments. There is a systematic

guidelines that is provided by bank regarding cheque, in case if there is any mistake found then

bank use to neglect particular cheque. There are different are different reason for rejection or

dishonour of cheque like:

Mismatch of signature.

Insufficient balance in accounts.

Wrong date or torn cheque.

Differences

Direct Debit Standing Orders Bank Charges Dishonour Cheque

It gives strength to

customer such as bank

give special rights to

them for making

payment. It is safest

and convenient option

by which different

bills can be paid on a

single time with secure

way.

This is basal facilities

that can be opted or

ignored by clients as

per their needs.

All those legal charges

that are charged by

bank from customer

by providing list of

services.

It is a situation

when customer are

able not able to

meet the guidelines

for banking and

there are some issue

with their cheque.

Thus bank

dishonour these

cheques.

14

services to their customer in order to ease their work and save time (Barth, Li and McClure,

2018). By providing these services bank charge specific amount from customer for maintenance

or further updates. Different services such as ATM card, internet and mobile banking, message

banking, overdrafts etc. are provided by bank to customer on which they use to charge fixed or

variable charges for respective accounts. Fixed charges remain the same throughout the time

period customer have account in certain bank such as, internet and message banking. On the

other side variable changes such as card issuance fee, ATM withdrawal charges after free

transaction etc.

Dishonour of cheque: Many times there are situation in which bank use to reject the

cheque which are presented by customer to make specific payments. There is a systematic

guidelines that is provided by bank regarding cheque, in case if there is any mistake found then

bank use to neglect particular cheque. There are different are different reason for rejection or

dishonour of cheque like:

Mismatch of signature.

Insufficient balance in accounts.

Wrong date or torn cheque.

Differences

Direct Debit Standing Orders Bank Charges Dishonour Cheque

It gives strength to

customer such as bank

give special rights to

them for making

payment. It is safest

and convenient option

by which different

bills can be paid on a

single time with secure

way.

This is basal facilities

that can be opted or

ignored by clients as

per their needs.

All those legal charges

that are charged by

bank from customer

by providing list of

services.

It is a situation

when customer are

able not able to

meet the guidelines

for banking and

there are some issue

with their cheque.

Thus bank

dishonour these

cheques.

14

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

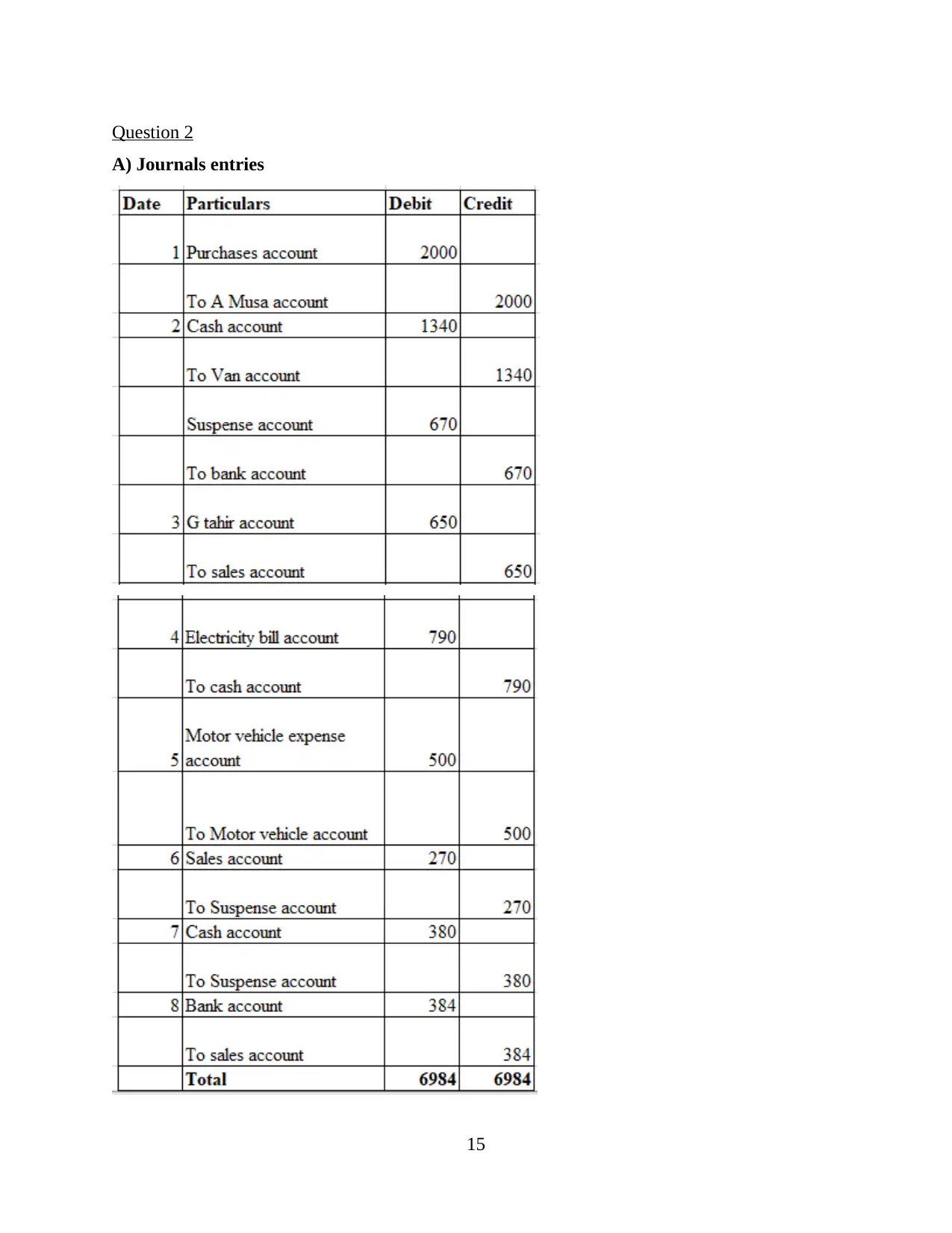

Question 2

A) Journals entries

15

A) Journals entries

15

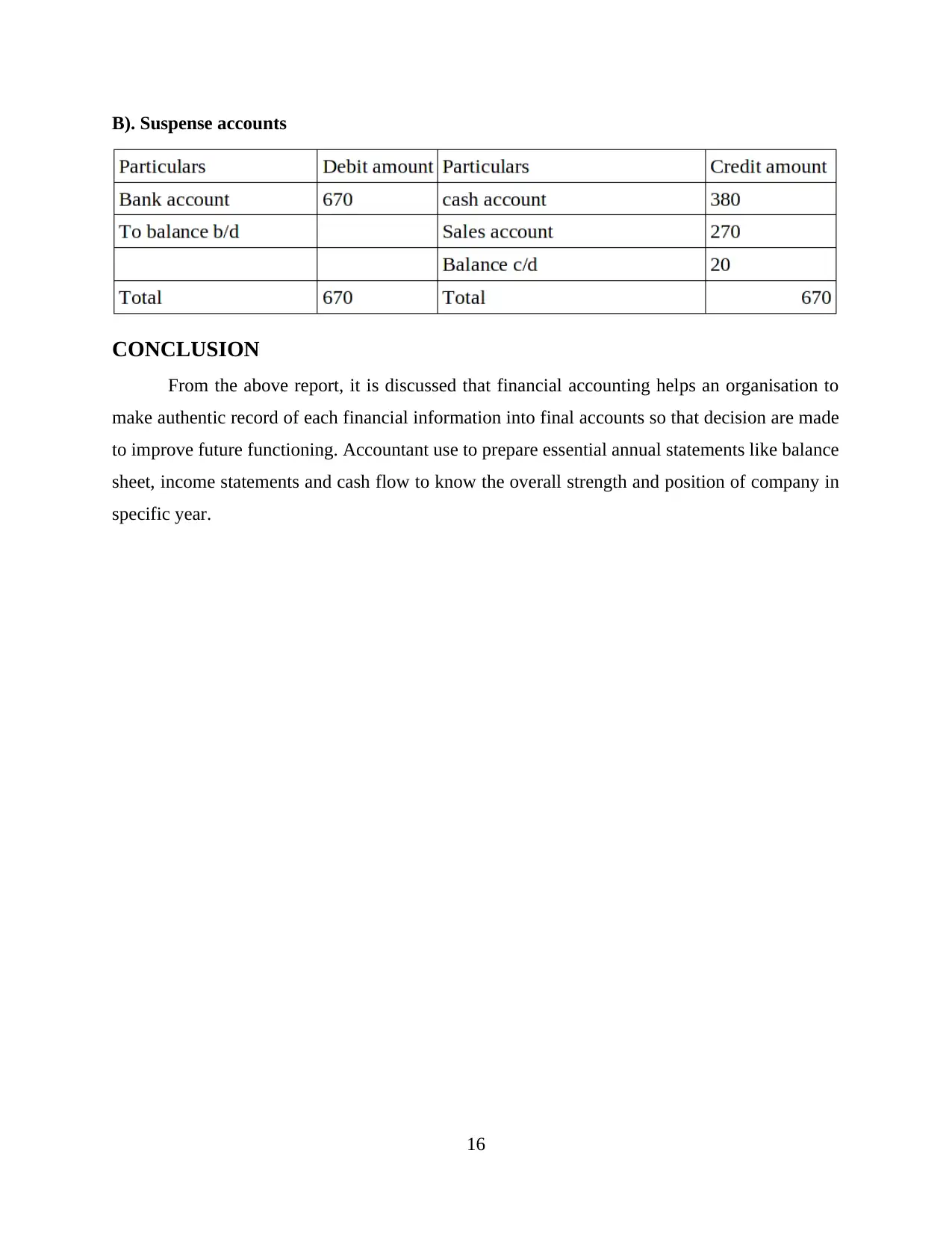

B). Suspense accounts

CONCLUSION

From the above report, it is discussed that financial accounting helps an organisation to

make authentic record of each financial information into final accounts so that decision are made

to improve future functioning. Accountant use to prepare essential annual statements like balance

sheet, income statements and cash flow to know the overall strength and position of company in

specific year.

16

CONCLUSION

From the above report, it is discussed that financial accounting helps an organisation to

make authentic record of each financial information into final accounts so that decision are made

to improve future functioning. Accountant use to prepare essential annual statements like balance

sheet, income statements and cash flow to know the overall strength and position of company in

specific year.

16

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.