Financial Accounting (1&2) Project Report - HNBS 310

VerifiedAdded on 2020/12/08

|10

|2269

|296

Report

AI Summary

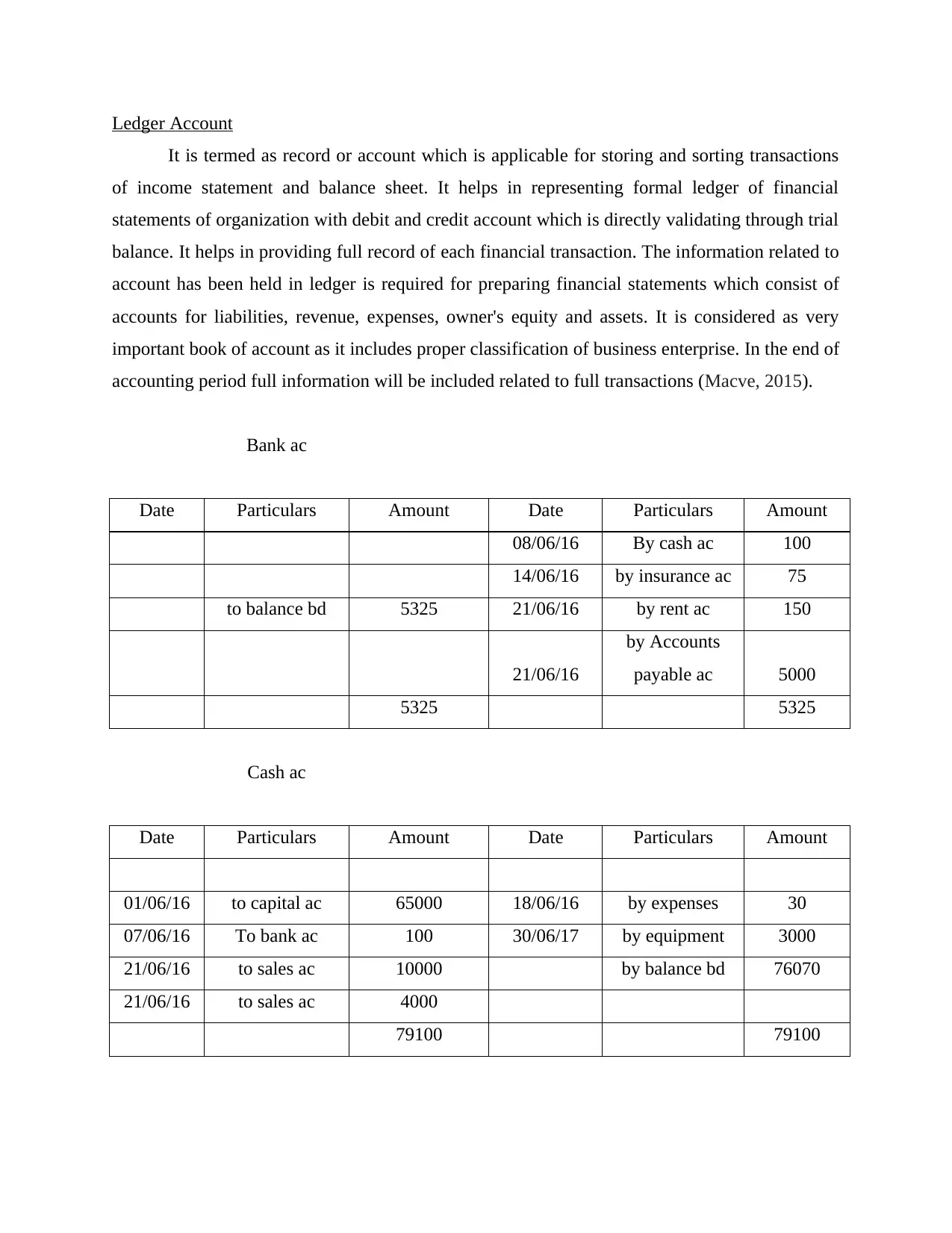

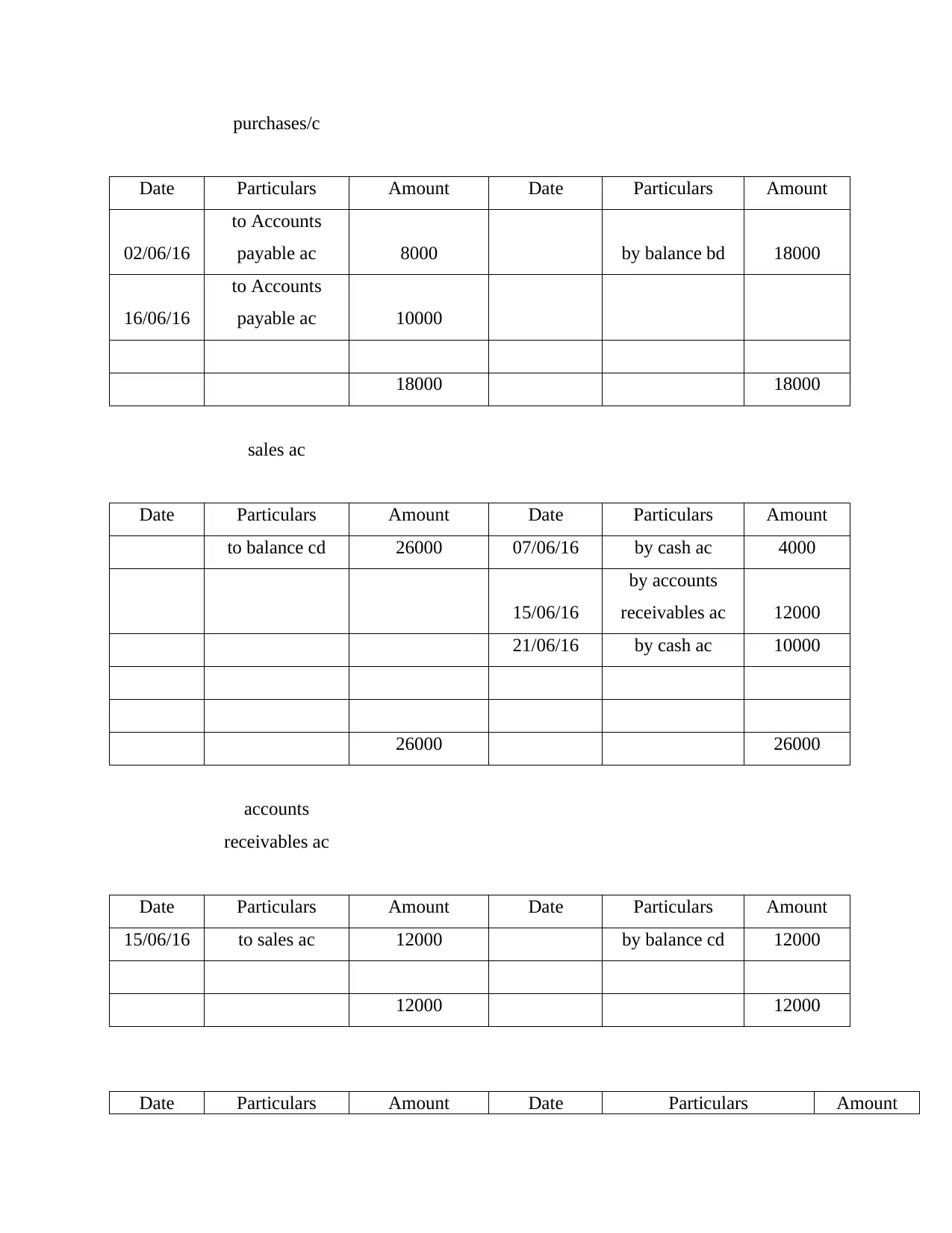

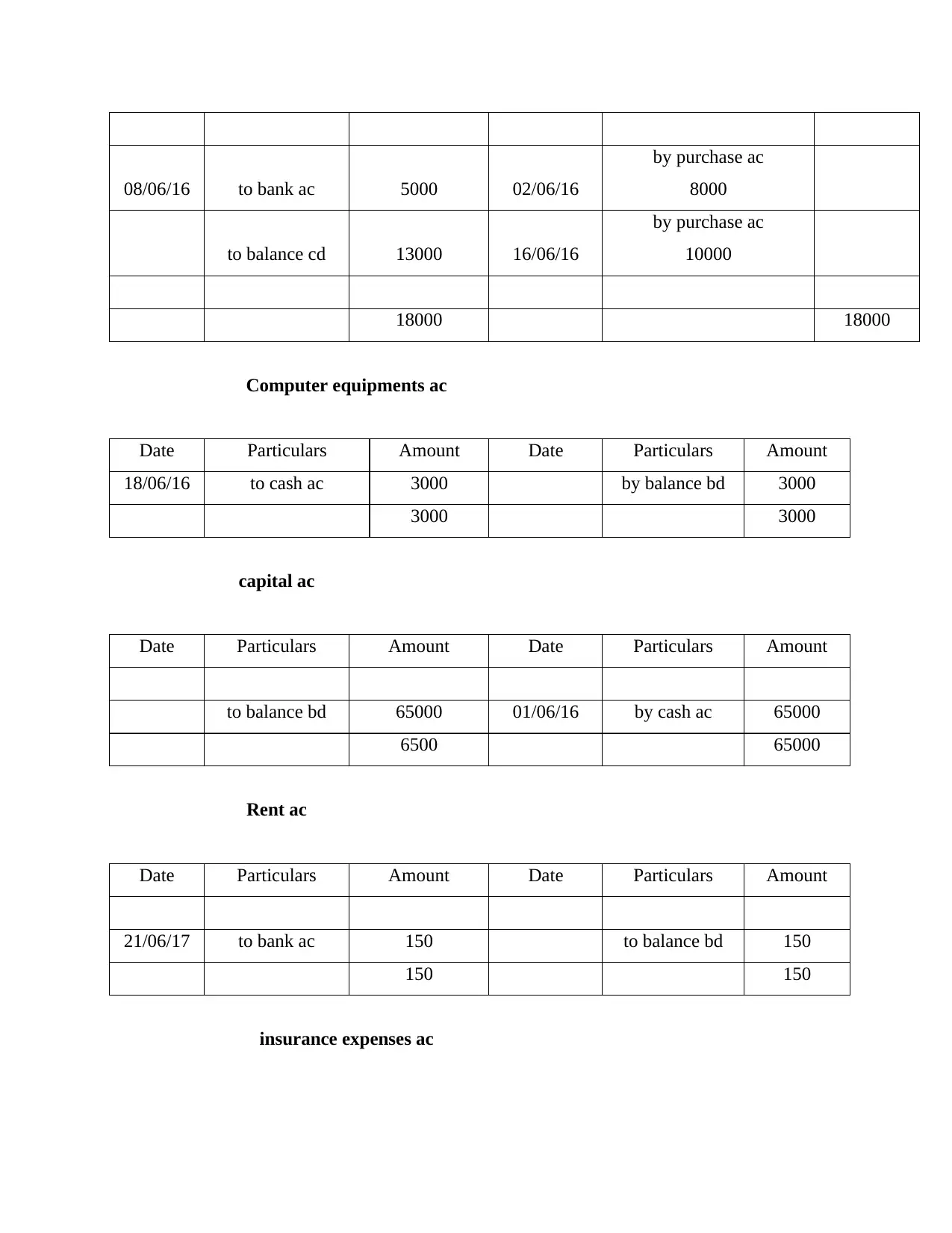

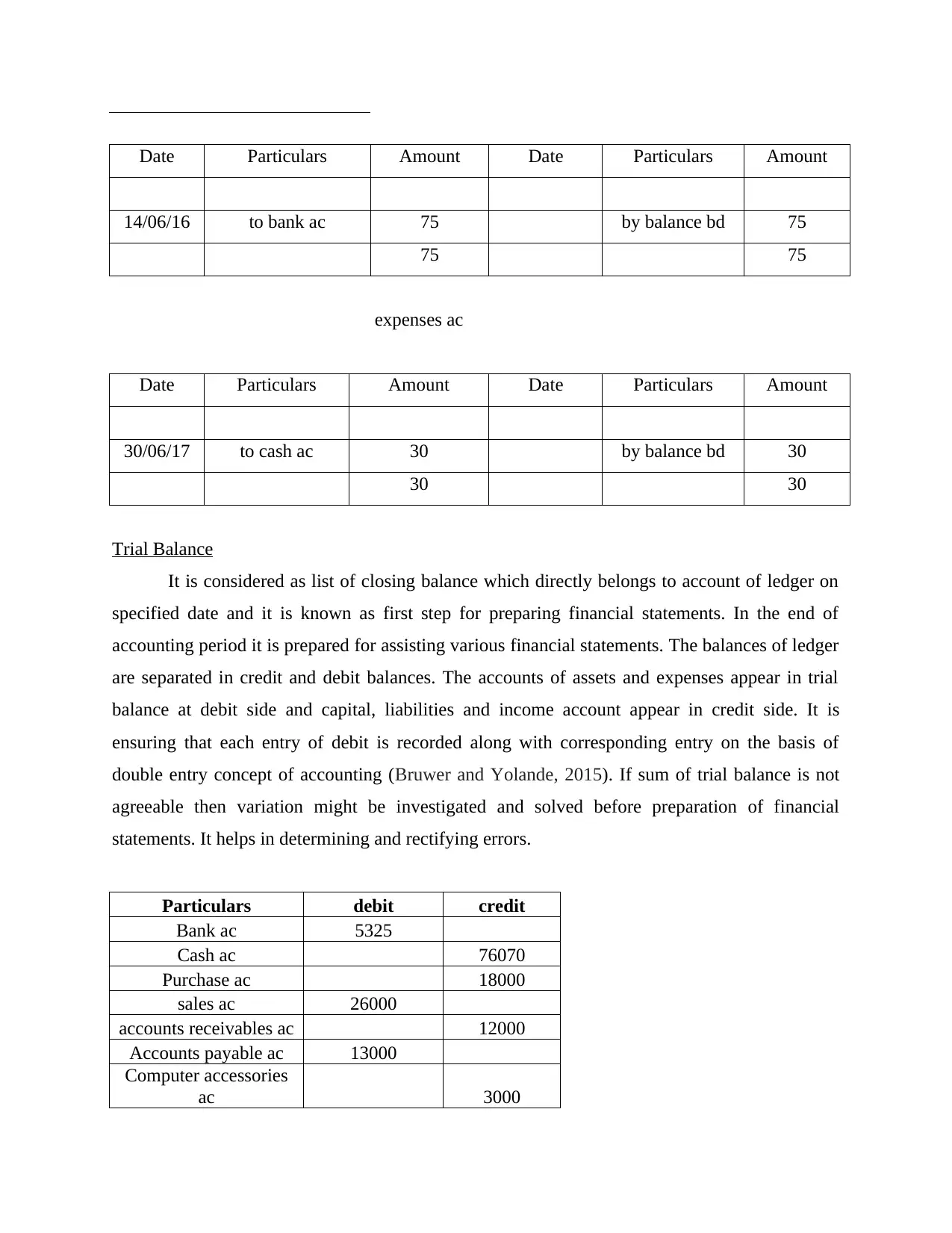

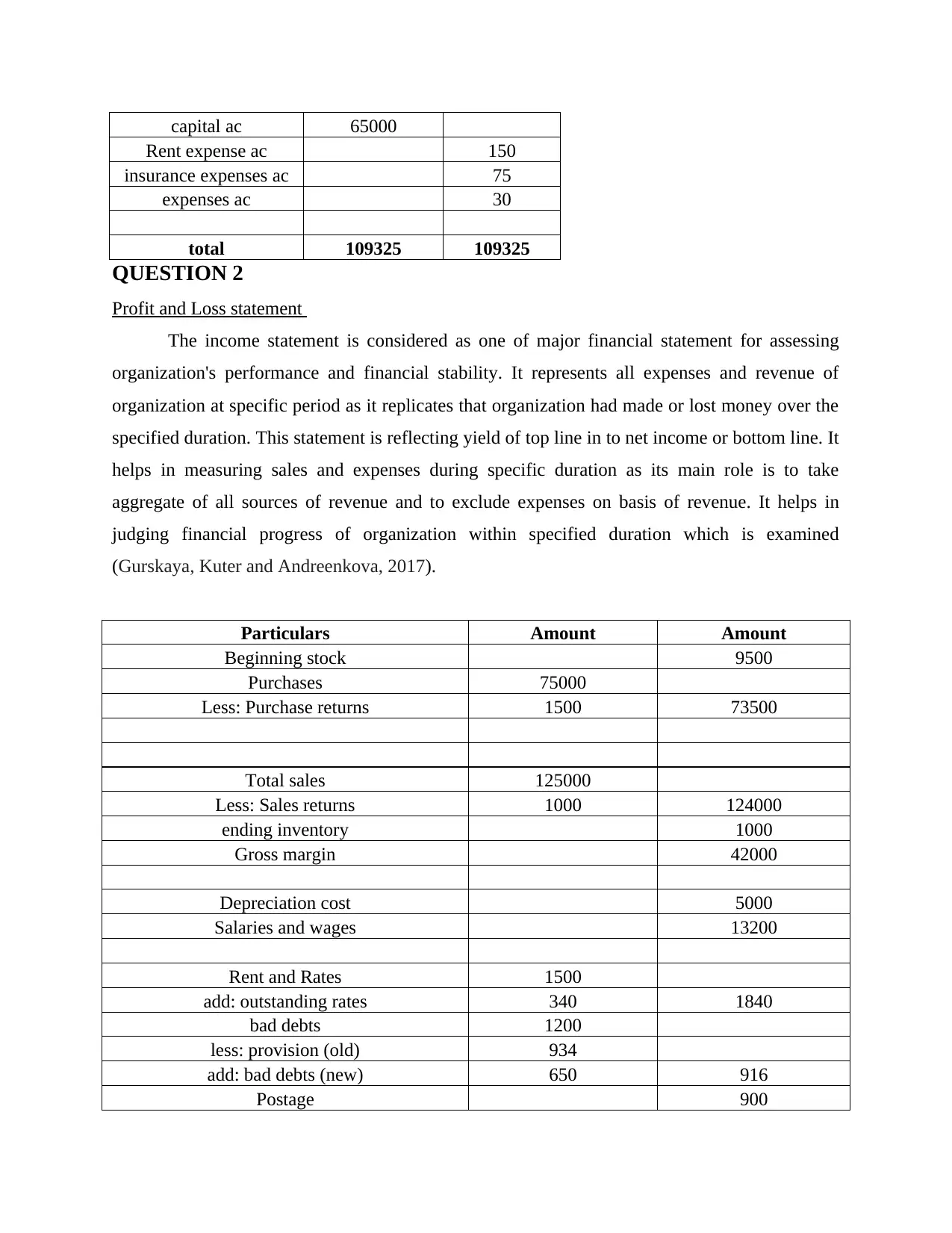

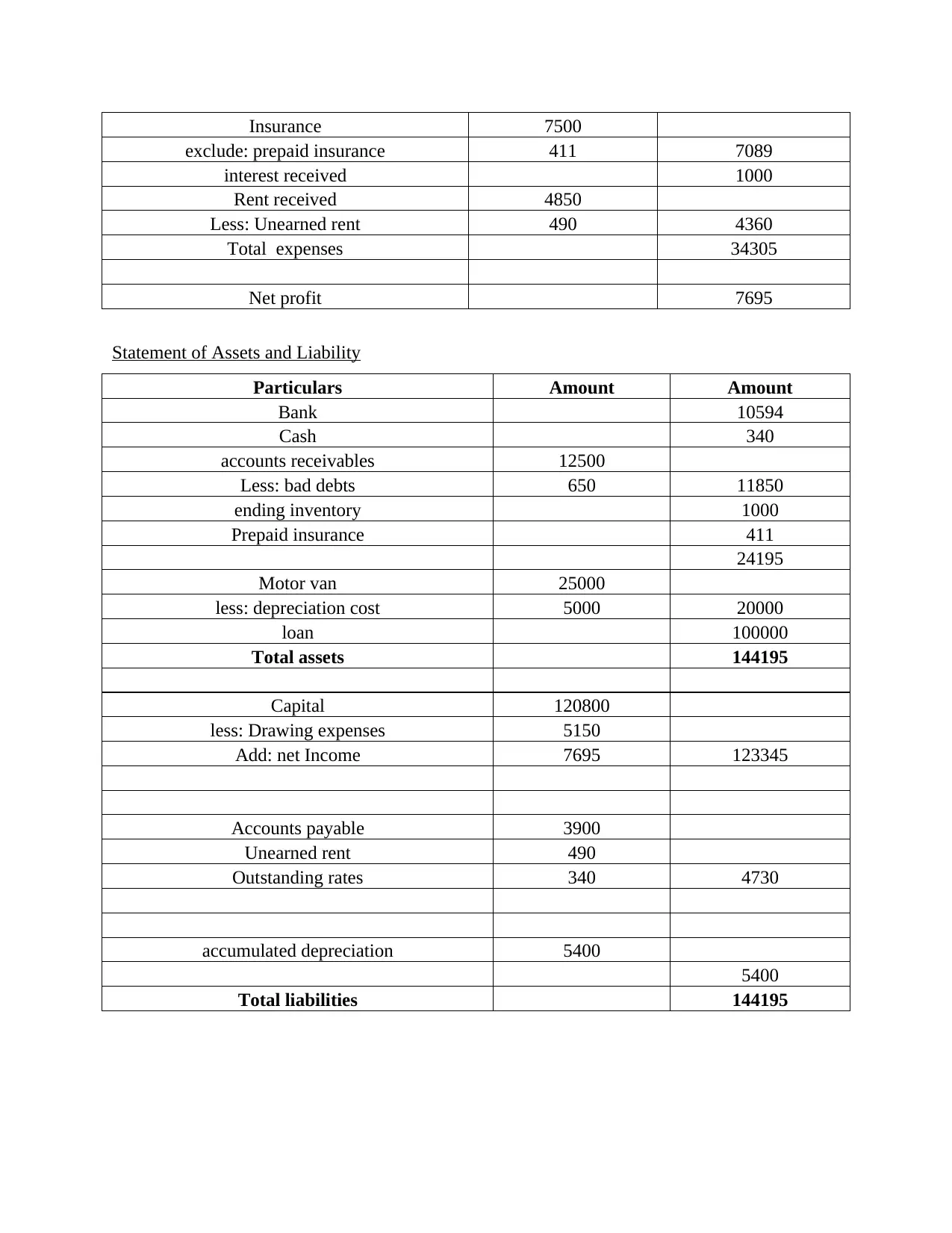

This financial accounting project report, prepared for HNBS 310, delves into key aspects of financial accounting. It begins with an introduction highlighting the importance of financial accounting in organizations and the use of double-entry bookkeeping. Project 1 focuses on financial accounting principles, including journal entries, ledger accounts, and trial balances. The report presents detailed journal entries for various business transactions, followed by the creation of ledger accounts and a trial balance to ensure the accuracy of financial data. The report also includes a profit and loss statement and a statement of assets and liabilities. Project 2 addresses bank reconciliation and rectification statements. The report concludes with references to relevant accounting literature. The report is a comprehensive overview of financial accounting principles and their application in practical scenarios.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.