HNBS 310 Financial accounting

VerifiedAdded on 2023/01/06

|24

|4585

|47

AI Summary

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Financial Accounting

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Contents

INTRODUCTION.......................................................................................................................................3

SCENARIO 1..............................................................................................................................................3

Question 1...............................................................................................................................................3

Question 2...............................................................................................................................................5

Question 3.............................................................................................................................................11

Question 4.............................................................................................................................................13

Question 5.............................................................................................................................................13

SCENARIO 2............................................................................................................................................15

Question 1.............................................................................................................................................15

Question 2.............................................................................................................................................16

Question 3.............................................................................................................................................17

Question 4.............................................................................................................................................17

Question 5.............................................................................................................................................19

CONCLUSION.........................................................................................................................................21

INTRODUCTION.......................................................................................................................................3

SCENARIO 1..............................................................................................................................................3

Question 1...............................................................................................................................................3

Question 2...............................................................................................................................................5

Question 3.............................................................................................................................................11

Question 4.............................................................................................................................................13

Question 5.............................................................................................................................................13

SCENARIO 2............................................................................................................................................15

Question 1.............................................................................................................................................15

Question 2.............................................................................................................................................16

Question 3.............................................................................................................................................17

Question 4.............................................................................................................................................17

Question 5.............................................................................................................................................19

CONCLUSION.........................................................................................................................................21

INTRODUCTION

Financial accounting is the practice of documenting, analyzing and presenting financial

operations and events that are at least partially financial in nature and analyzing results in a

meaningful manner. Financial accounting is an accountant professional department that ways of

measuring of cash operation inside a company (Aifuwa, Embele and Saidu, 2018). The

expenditures are registered, summarized and income tax or financial statement, including a cash

flow statement or a balance sheet, using structured guidelines. This report is decided by the

multiple tasks of documenting business activities in forms of papers, report, trial balance and the

creation of annual report for business organizations. This study also involved a bank audit in

order to determine if financial records are right or not.

SCENARIO 1

Question 1

There are various forms of business activities that have been used to document in the

accounting records and then further define the sum with which it is based. These are as follows:

Sales transactions require the sale of the product to customers in return for cash or on

credit basis. Leading companies are a debit to money or accounts receivable and a credit

to the sales linked account in the sales reports.

Purchases are the transactions that a business uses to buy the products or resources

required to attain the organization’s goals. Buys of products purchased in money resulted

in a debit to the accounting system and a money loan. Unless items were bought on credit

terms then the transaction would be paid, the debit would still be placed into the

accounting period and the reimbursement would be deposited into the debit account.

Receivables are documents which occur within the organization paid for the receipt of

product to another company. The invoice exchange happens as a money debit and a credit

to the accruals in the seller's report (Appelbaum and et.al, 2017).

Payments are transactions that distribute funds for either a product or service to a

business that is receiving money. People are reported in the accounting journal of the

Financial accounting is the practice of documenting, analyzing and presenting financial

operations and events that are at least partially financial in nature and analyzing results in a

meaningful manner. Financial accounting is an accountant professional department that ways of

measuring of cash operation inside a company (Aifuwa, Embele and Saidu, 2018). The

expenditures are registered, summarized and income tax or financial statement, including a cash

flow statement or a balance sheet, using structured guidelines. This report is decided by the

multiple tasks of documenting business activities in forms of papers, report, trial balance and the

creation of annual report for business organizations. This study also involved a bank audit in

order to determine if financial records are right or not.

SCENARIO 1

Question 1

There are various forms of business activities that have been used to document in the

accounting records and then further define the sum with which it is based. These are as follows:

Sales transactions require the sale of the product to customers in return for cash or on

credit basis. Leading companies are a debit to money or accounts receivable and a credit

to the sales linked account in the sales reports.

Purchases are the transactions that a business uses to buy the products or resources

required to attain the organization’s goals. Buys of products purchased in money resulted

in a debit to the accounting system and a money loan. Unless items were bought on credit

terms then the transaction would be paid, the debit would still be placed into the

accounting period and the reimbursement would be deposited into the debit account.

Receivables are documents which occur within the organization paid for the receipt of

product to another company. The invoice exchange happens as a money debit and a credit

to the accruals in the seller's report (Appelbaum and et.al, 2017).

Payments are transactions that distribute funds for either a product or service to a

business that is receiving money. People are reported in the accounting journal of the

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

business which enables the payment to be given as an amount received and a deduction to

the accounts payable.

Single entry bookkeeping

Single-entry bookkeeping would possibly only operate for company unless the company is quite

compact and easy, with low operation amount. Usually it's close to having your own personal

cheque book. When using single-entry book keeping it maintains a history of information such as

money, tax-deductible expenditures and tax payable.

Double entry bookkeeping

Many firms, including the survival of new companies, have double-entry bookkeeping for their

financial requirements. Two features of bookkeeping with double entry are how each ledger has

two columns but that expenditure is in different sides. By each payment, two transactions are

recorded-one debit in one bank and one credit from another (Ayres, Huang and Myring, 2017).

Trial balance and its importance

The trial balance is a worksheet in which all ledgers' accounts are integrated into the debit

and credit part quantities, and the amount is balanced against one another. The firm used to

regularly start preparing trial balance, usually at the end of the financial period. The trial balance

importance’s are as follows:

Checking reliability: This means that perhaps the trial balance was being used to verify the

actual number accumulated on the correct side of the current ledger while moving data from

various documents including such purchase records, writing records, cash books, etc. Trial

Balance other than consideration in accounting system, the authenticity of single purpose

financial statements is often essential to understand.

Helps in preparing financial statements: At end of each fiscal accounting year the income

statement, the balance sheet and the working capital should be updated. The amount of all the

funds that used prepare the financial reports is also available in the trial report, allowing the

financial details simple to prepare and understand (Bishop, DeZoort and Hermanson, 2017).

the accounts payable.

Single entry bookkeeping

Single-entry bookkeeping would possibly only operate for company unless the company is quite

compact and easy, with low operation amount. Usually it's close to having your own personal

cheque book. When using single-entry book keeping it maintains a history of information such as

money, tax-deductible expenditures and tax payable.

Double entry bookkeeping

Many firms, including the survival of new companies, have double-entry bookkeeping for their

financial requirements. Two features of bookkeeping with double entry are how each ledger has

two columns but that expenditure is in different sides. By each payment, two transactions are

recorded-one debit in one bank and one credit from another (Ayres, Huang and Myring, 2017).

Trial balance and its importance

The trial balance is a worksheet in which all ledgers' accounts are integrated into the debit

and credit part quantities, and the amount is balanced against one another. The firm used to

regularly start preparing trial balance, usually at the end of the financial period. The trial balance

importance’s are as follows:

Checking reliability: This means that perhaps the trial balance was being used to verify the

actual number accumulated on the correct side of the current ledger while moving data from

various documents including such purchase records, writing records, cash books, etc. Trial

Balance other than consideration in accounting system, the authenticity of single purpose

financial statements is often essential to understand.

Helps in preparing financial statements: At end of each fiscal accounting year the income

statement, the balance sheet and the working capital should be updated. The amount of all the

funds that used prepare the financial reports is also available in the trial report, allowing the

financial details simple to prepare and understand (Bishop, DeZoort and Hermanson, 2017).

Rectifying errors: The cumulative debit of both balance sheet shall be equal to the trial

balance's aggregate credit. All this reviews booklet precision of the numerical. If that's not the

case, the accountant will notice the error and repair it. Additionally, professional accountants feel

satisfied when the debt balance total and the amount owed total are balanced.

Help in adjustments: Adjustment plans, such as payroll charges, retained bonds, closing needs

to share, etc., should be changed mostly during jury equilibrium development process. This

serves to create changes that are only significant in the existing year of financial reporting.

Businesses typically send the adjustment news stories at the close of the budget year. There is no

restriction to starting new changes transactions when people happen (Bolívar and et.al, 2018).

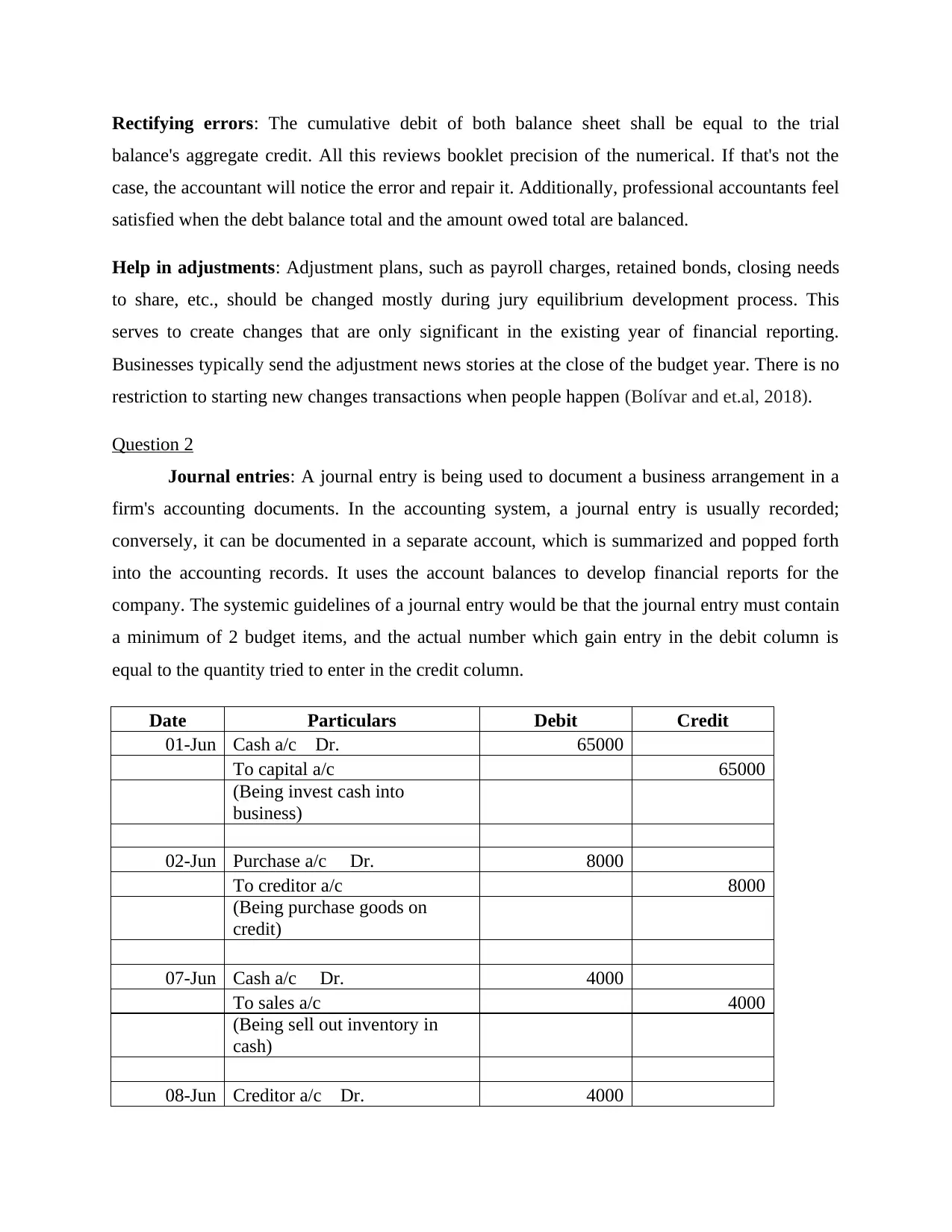

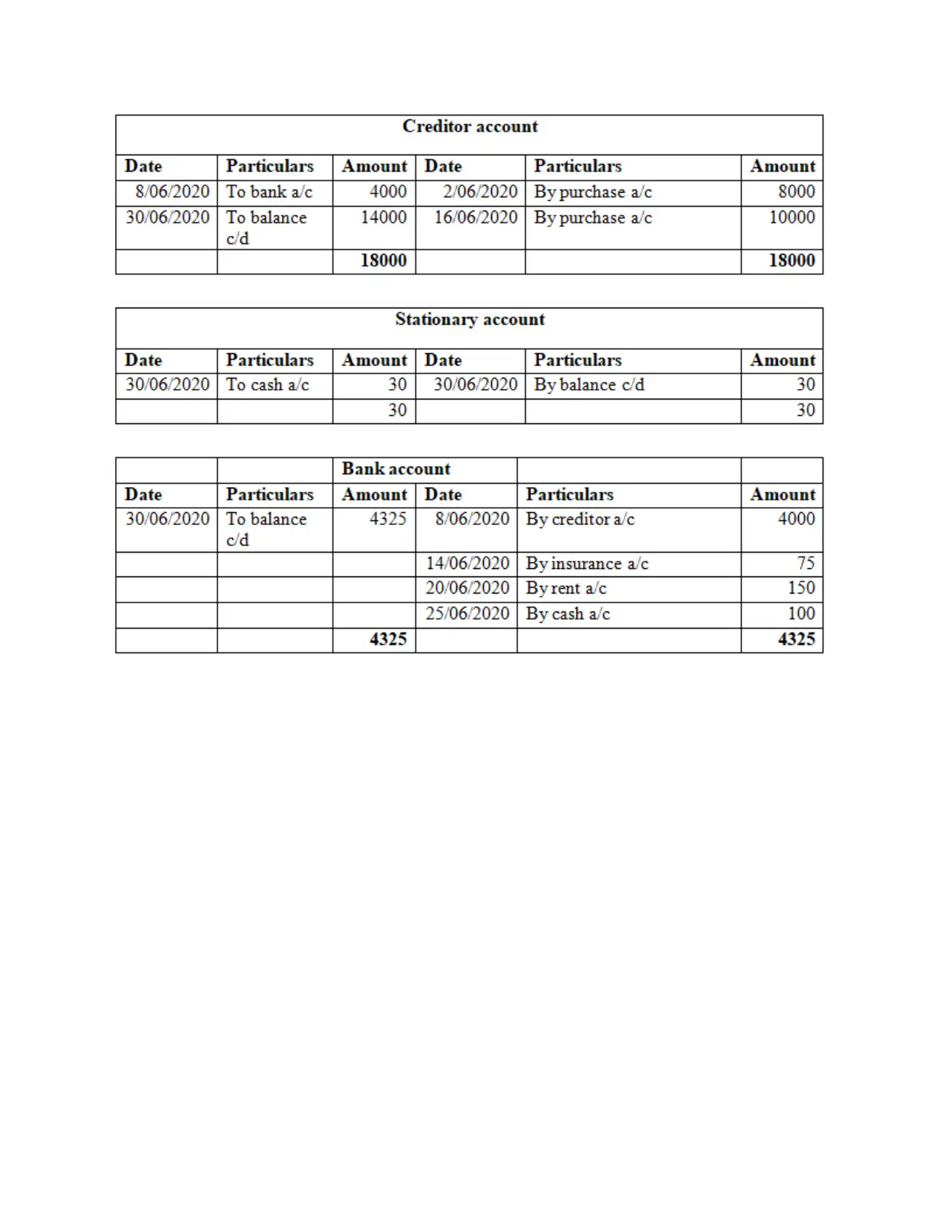

Question 2

Journal entries: A journal entry is being used to document a business arrangement in a

firm's accounting documents. In the accounting system, a journal entry is usually recorded;

conversely, it can be documented in a separate account, which is summarized and popped forth

into the accounting records. It uses the account balances to develop financial reports for the

company. The systemic guidelines of a journal entry would be that the journal entry must contain

a minimum of 2 budget items, and the actual number which gain entry in the debit column is

equal to the quantity tried to enter in the credit column.

Date Particulars Debit Credit

01-Jun Cash a/c Dr. 65000

To capital a/c 65000

(Being invest cash into

business)

02-Jun Purchase a/c Dr. 8000

To creditor a/c 8000

(Being purchase goods on

credit)

07-Jun Cash a/c Dr. 4000

To sales a/c 4000

(Being sell out inventory in

cash)

08-Jun Creditor a/c Dr. 4000

balance's aggregate credit. All this reviews booklet precision of the numerical. If that's not the

case, the accountant will notice the error and repair it. Additionally, professional accountants feel

satisfied when the debt balance total and the amount owed total are balanced.

Help in adjustments: Adjustment plans, such as payroll charges, retained bonds, closing needs

to share, etc., should be changed mostly during jury equilibrium development process. This

serves to create changes that are only significant in the existing year of financial reporting.

Businesses typically send the adjustment news stories at the close of the budget year. There is no

restriction to starting new changes transactions when people happen (Bolívar and et.al, 2018).

Question 2

Journal entries: A journal entry is being used to document a business arrangement in a

firm's accounting documents. In the accounting system, a journal entry is usually recorded;

conversely, it can be documented in a separate account, which is summarized and popped forth

into the accounting records. It uses the account balances to develop financial reports for the

company. The systemic guidelines of a journal entry would be that the journal entry must contain

a minimum of 2 budget items, and the actual number which gain entry in the debit column is

equal to the quantity tried to enter in the credit column.

Date Particulars Debit Credit

01-Jun Cash a/c Dr. 65000

To capital a/c 65000

(Being invest cash into

business)

02-Jun Purchase a/c Dr. 8000

To creditor a/c 8000

(Being purchase goods on

credit)

07-Jun Cash a/c Dr. 4000

To sales a/c 4000

(Being sell out inventory in

cash)

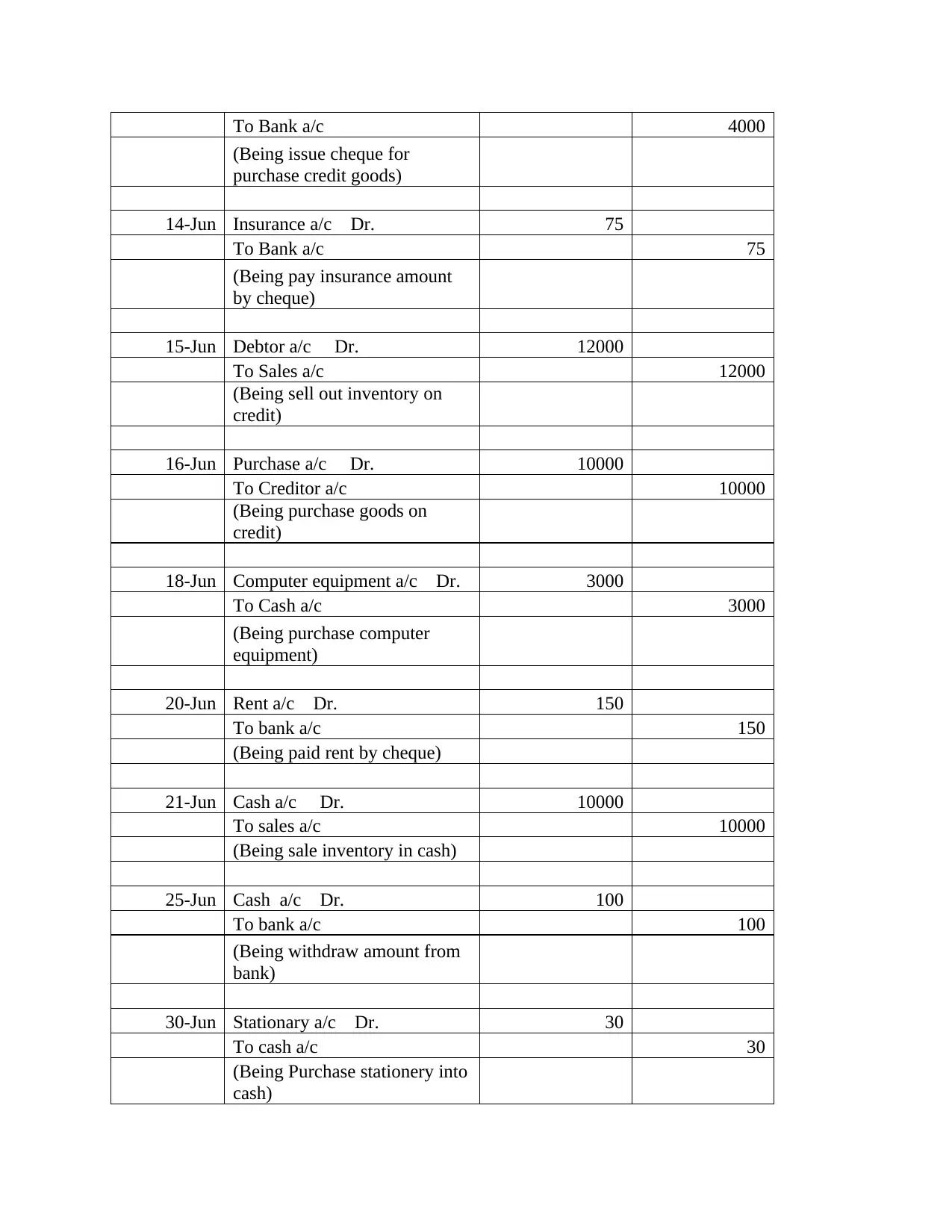

08-Jun Creditor a/c Dr. 4000

To Bank a/c 4000

(Being issue cheque for

purchase credit goods)

14-Jun Insurance a/c Dr. 75

To Bank a/c 75

(Being pay insurance amount

by cheque)

15-Jun Debtor a/c Dr. 12000

To Sales a/c 12000

(Being sell out inventory on

credit)

16-Jun Purchase a/c Dr. 10000

To Creditor a/c 10000

(Being purchase goods on

credit)

18-Jun Computer equipment a/c Dr. 3000

To Cash a/c 3000

(Being purchase computer

equipment)

20-Jun Rent a/c Dr. 150

To bank a/c 150

(Being paid rent by cheque)

21-Jun Cash a/c Dr. 10000

To sales a/c 10000

(Being sale inventory in cash)

25-Jun Cash a/c Dr. 100

To bank a/c 100

(Being withdraw amount from

bank)

30-Jun Stationary a/c Dr. 30

To cash a/c 30

(Being Purchase stationery into

cash)

(Being issue cheque for

purchase credit goods)

14-Jun Insurance a/c Dr. 75

To Bank a/c 75

(Being pay insurance amount

by cheque)

15-Jun Debtor a/c Dr. 12000

To Sales a/c 12000

(Being sell out inventory on

credit)

16-Jun Purchase a/c Dr. 10000

To Creditor a/c 10000

(Being purchase goods on

credit)

18-Jun Computer equipment a/c Dr. 3000

To Cash a/c 3000

(Being purchase computer

equipment)

20-Jun Rent a/c Dr. 150

To bank a/c 150

(Being paid rent by cheque)

21-Jun Cash a/c Dr. 10000

To sales a/c 10000

(Being sale inventory in cash)

25-Jun Cash a/c Dr. 100

To bank a/c 100

(Being withdraw amount from

bank)

30-Jun Stationary a/c Dr. 30

To cash a/c 30

(Being Purchase stationery into

cash)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

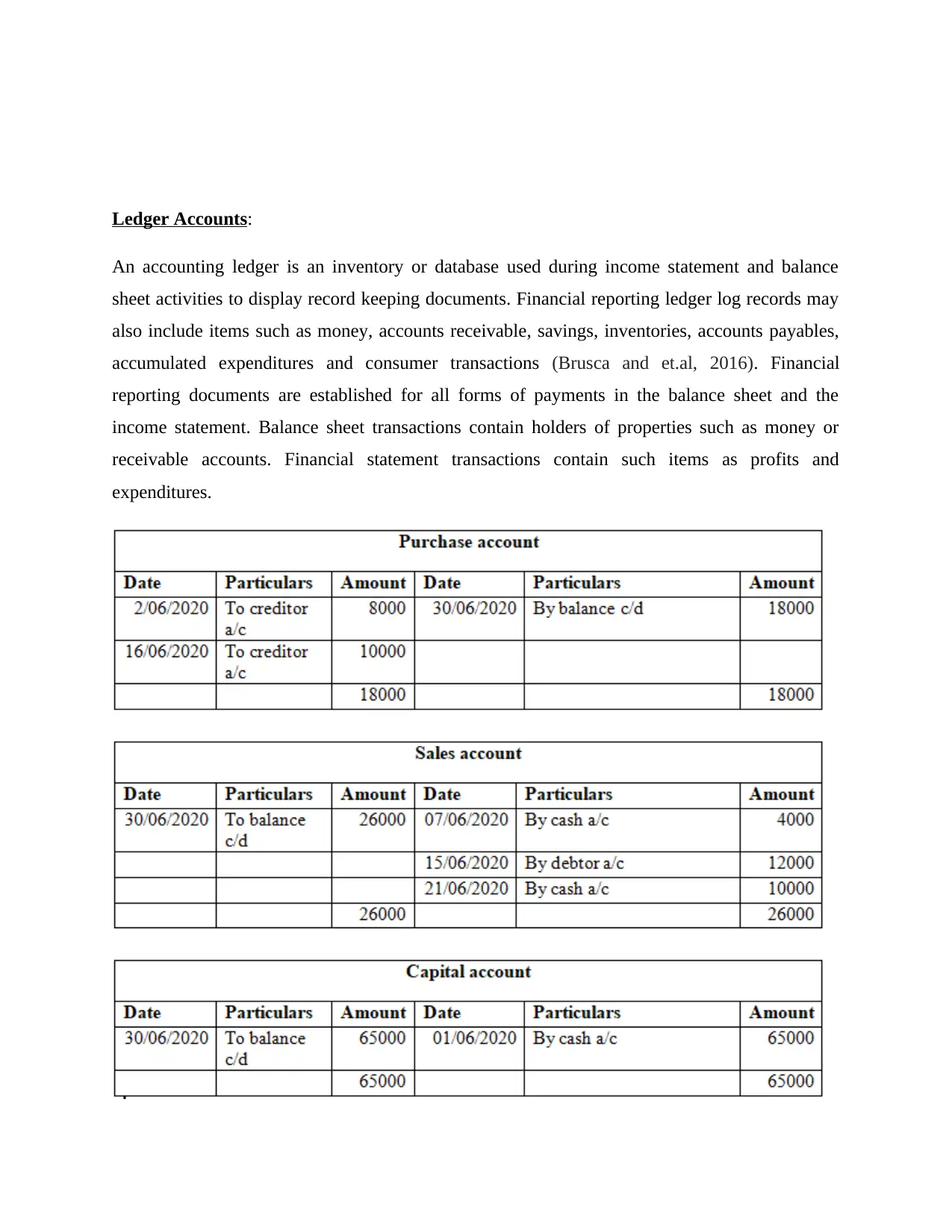

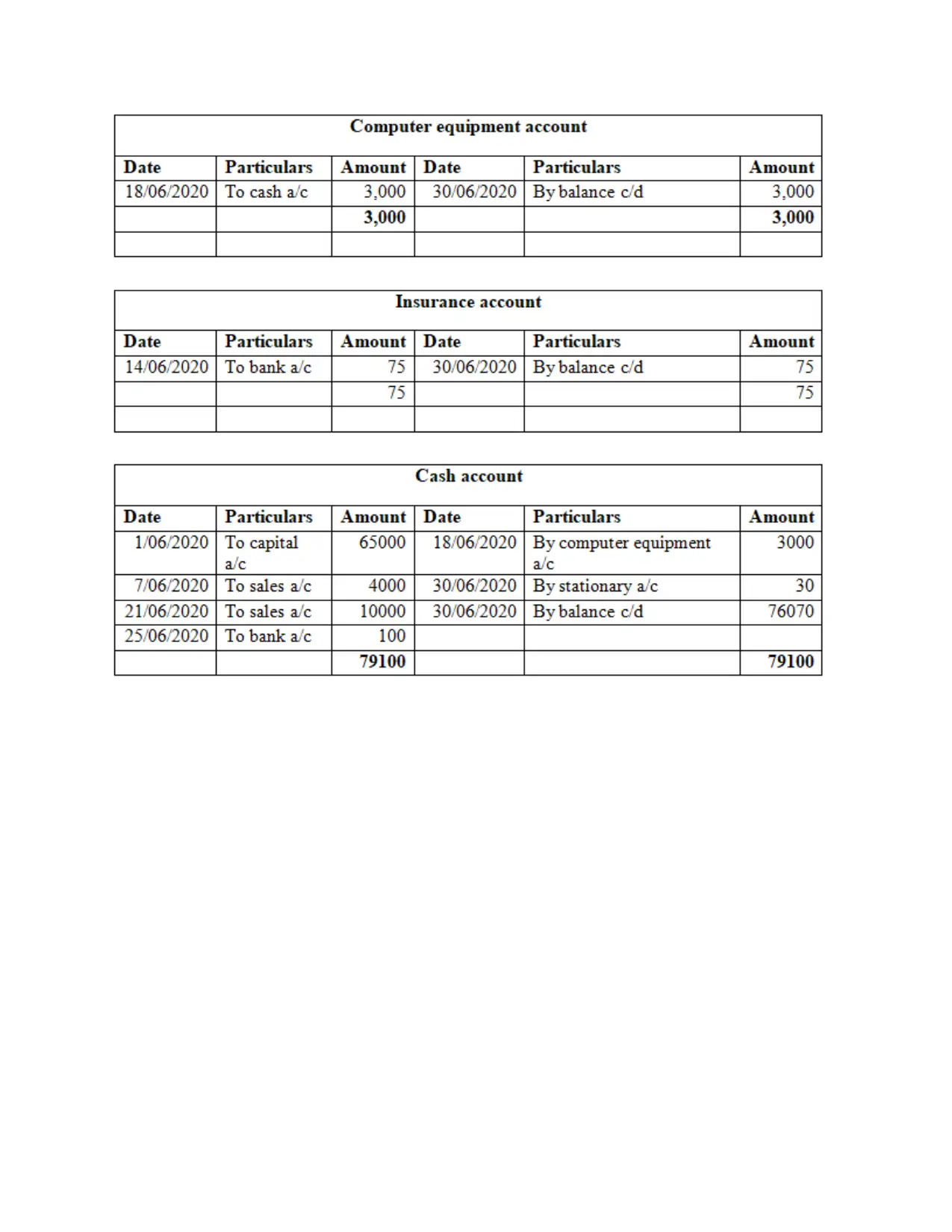

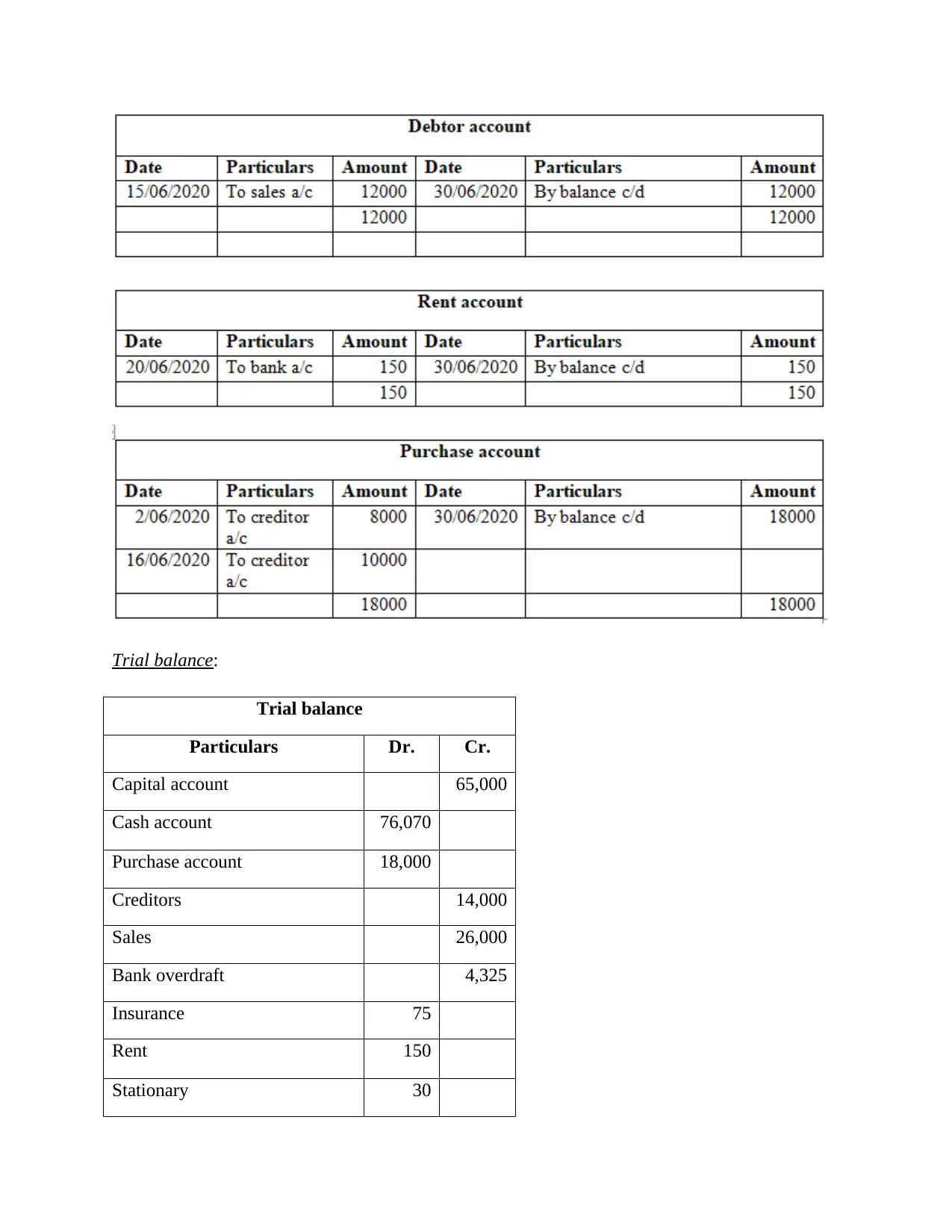

Ledger Accounts:

An accounting ledger is an inventory or database used during income statement and balance

sheet activities to display record keeping documents. Financial reporting ledger log records may

also include items such as money, accounts receivable, savings, inventories, accounts payables,

accumulated expenditures and consumer transactions (Brusca and et.al, 2016). Financial

reporting documents are established for all forms of payments in the balance sheet and the

income statement. Balance sheet transactions contain holders of properties such as money or

receivable accounts. Financial statement transactions contain such items as profits and

expenditures.

An accounting ledger is an inventory or database used during income statement and balance

sheet activities to display record keeping documents. Financial reporting ledger log records may

also include items such as money, accounts receivable, savings, inventories, accounts payables,

accumulated expenditures and consumer transactions (Brusca and et.al, 2016). Financial

reporting documents are established for all forms of payments in the balance sheet and the

income statement. Balance sheet transactions contain holders of properties such as money or

receivable accounts. Financial statement transactions contain such items as profits and

expenditures.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Trial balance:

Trial balance

Particulars Dr. Cr.

Capital account 65,000

Cash account 76,070

Purchase account 18,000

Creditors 14,000

Sales 26,000

Bank overdraft 4,325

Insurance 75

Rent 150

Stationary 30

Trial balance

Particulars Dr. Cr.

Capital account 65,000

Cash account 76,070

Purchase account 18,000

Creditors 14,000

Sales 26,000

Bank overdraft 4,325

Insurance 75

Rent 150

Stationary 30

Debtor 12,000

Computer equipment 3,000

109,32

5

109,32

5

Question 3

Financial reporting is a process of primary interface staff with information in order to

make effective decisions and the income report is the result of the financial reports. That is the

main distinction between financial reporting and accounts. Financial statements have been

prepared over a specific accounting period, usually for one year. This accounting period is linked

to as a 'financial year' and is different from a schedule period, because the financial statement

may vary depending on the situation of the organisation or business (Gotti, 2016). Financial

Statements are meant to even provide data on business situation, working capital and operating

performance. This process helped those statements' viewers make planning and decision. These

reports seek to identify commodity use, cash flow, corporate reputation and the company's

financial wellbeing. This allows traders and individuals make better decisions as to how the

company should be managed.

The concepts "financial report" and "financial statement" are considered synonymous, not

even in the same way. "Financial report" is a paragliding concept that underlies so many kinds of

reporting. This one study which comes under the umbrella of the financial report is the income

reports. In many other sentences, all annual reports are accounting standards, but the income

accounts may not all be.

Requirement of financial reports and its users:

According to the GAAPs, organizations are paying for trying to report on their retained

earnings, profit-making operational efficiency economic policies. The preceding 3 major

financial statements must be prepared underneath the GAAP, including such statement of

comprehensive income, balance sheet and statement of working capital. Even without heavy

price of updating their GL or ERP, financial reporting system can be combined with the current

general ledger, offering solid and current incorporated analyses. When the firm has built the right

Computer equipment 3,000

109,32

5

109,32

5

Question 3

Financial reporting is a process of primary interface staff with information in order to

make effective decisions and the income report is the result of the financial reports. That is the

main distinction between financial reporting and accounts. Financial statements have been

prepared over a specific accounting period, usually for one year. This accounting period is linked

to as a 'financial year' and is different from a schedule period, because the financial statement

may vary depending on the situation of the organisation or business (Gotti, 2016). Financial

Statements are meant to even provide data on business situation, working capital and operating

performance. This process helped those statements' viewers make planning and decision. These

reports seek to identify commodity use, cash flow, corporate reputation and the company's

financial wellbeing. This allows traders and individuals make better decisions as to how the

company should be managed.

The concepts "financial report" and "financial statement" are considered synonymous, not

even in the same way. "Financial report" is a paragliding concept that underlies so many kinds of

reporting. This one study which comes under the umbrella of the financial report is the income

reports. In many other sentences, all annual reports are accounting standards, but the income

accounts may not all be.

Requirement of financial reports and its users:

According to the GAAPs, organizations are paying for trying to report on their retained

earnings, profit-making operational efficiency economic policies. The preceding 3 major

financial statements must be prepared underneath the GAAP, including such statement of

comprehensive income, balance sheet and statement of working capital. Even without heavy

price of updating their GL or ERP, financial reporting system can be combined with the current

general ledger, offering solid and current incorporated analyses. When the firm has built the right

lasting partnership, holders expect efficiency growth (Honggowati and et.al, 2017).

Development, packaging, and distribution assessments can be conducted with reliability and

consistency while consolidating sources of data, places, and currency exchange. The reporting

software ensures reports are ideally designed to meet the needs of both the subcommittee and the

SEC.

The statement of income together with the affiliated operating expenses shall address the

revenues received by the firm from over fiscal quarter. It encompasses activities and non-

operating profits, allowing creditors and debtors to decide profit margins. It's often alluded to as

financial statements and loss statements. Likewise, in balance sheet, the value of the property

and obligations listed in the financial statement and the resulting working capital represents. This

knowledge is being used by employees of the organization who have a particular effect on the

financial results of the business. All are listed below:

Management: The top management wishes to recognize the organization’s performance,

flexibility and working capital regularly so it can undertake further product-related accounting

and strategic assessments.

Creditors: These are going to warrant the evaluation of financial statements since they're the

corporation's owners and would like to acknowledge their cash's growth (Khoja, Chipulu and

Jayasekera, 2019).

Competitors: Organizations bargaining with a business can expect to have access to their bank

documents to determine their financial position. Expert knowledge they gain could alter their

commanding advantage.

Customers: When determining that producer to use for a large contract, the buyer first needs to

re - examine his financial report to decide the company's available funds to remain in business

sufficient enough to have the services or goods that the contract requires.

Employees: A company can opt to start presenting its financial reports to its staff members,

along with a comprehensive explanation of what the procedures are in place. It could be used to

raise the level of employee engagement in the business and its comprehension.

Development, packaging, and distribution assessments can be conducted with reliability and

consistency while consolidating sources of data, places, and currency exchange. The reporting

software ensures reports are ideally designed to meet the needs of both the subcommittee and the

SEC.

The statement of income together with the affiliated operating expenses shall address the

revenues received by the firm from over fiscal quarter. It encompasses activities and non-

operating profits, allowing creditors and debtors to decide profit margins. It's often alluded to as

financial statements and loss statements. Likewise, in balance sheet, the value of the property

and obligations listed in the financial statement and the resulting working capital represents. This

knowledge is being used by employees of the organization who have a particular effect on the

financial results of the business. All are listed below:

Management: The top management wishes to recognize the organization’s performance,

flexibility and working capital regularly so it can undertake further product-related accounting

and strategic assessments.

Creditors: These are going to warrant the evaluation of financial statements since they're the

corporation's owners and would like to acknowledge their cash's growth (Khoja, Chipulu and

Jayasekera, 2019).

Competitors: Organizations bargaining with a business can expect to have access to their bank

documents to determine their financial position. Expert knowledge they gain could alter their

commanding advantage.

Customers: When determining that producer to use for a large contract, the buyer first needs to

re - examine his financial report to decide the company's available funds to remain in business

sufficient enough to have the services or goods that the contract requires.

Employees: A company can opt to start presenting its financial reports to its staff members,

along with a comprehensive explanation of what the procedures are in place. It could be used to

raise the level of employee engagement in the business and its comprehension.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Question 4

There are many accounting standards which even the organisation adopts when

measuring its business activities and preparing account balances. Those are dealt below with:

Accrual principle: It is the concept of documenting bank documents in the accounting statement

and once they take place, instead of in the intervals so if cash flows integrate with each other.

This would be the basis of the accounting revenue statement. What really occurred mostly during

accounting cycle is critical for the growth of the firm’s financial performance, rather than being

unnatural method postponed or accelerated by the associated retained earnings (Kumar and et.al,

2018).

Conservatism Principle: this is also the concept that allows the study to document

commitments as rapidly as feasible, but still only document profit growth whether they are sure

that they will occur. This concept tends to advance refer to the relevant soon instead of

afterwards. When an organisation insistently mischaracterizes the results to be better than would

be probably the case, this principle may be driven far enough.

Full disclosure principle: This is the idea that business should disclose any details and may

have an impact on the recipient's interpretation of those reports in or as well as the business

performance statements. By identifying a vast number of social identities, the accounting

standards significantly strengthened this definition.

Going concern principle: The theory of going concern is the presumption that a company can

stay in operation for the coming years. In comparison, this ensures that the company will not be

compelled to suspend activities and repossess its properties at what could be very small fire-sale

rates in the near term. Through making this statement, the auditor is rational in postponing the

identification of such expenditures for a later date when the company is likely to stay in

operation and use its resources as quickly and efficiently as possible (Legenzova, 2016).

Question 5

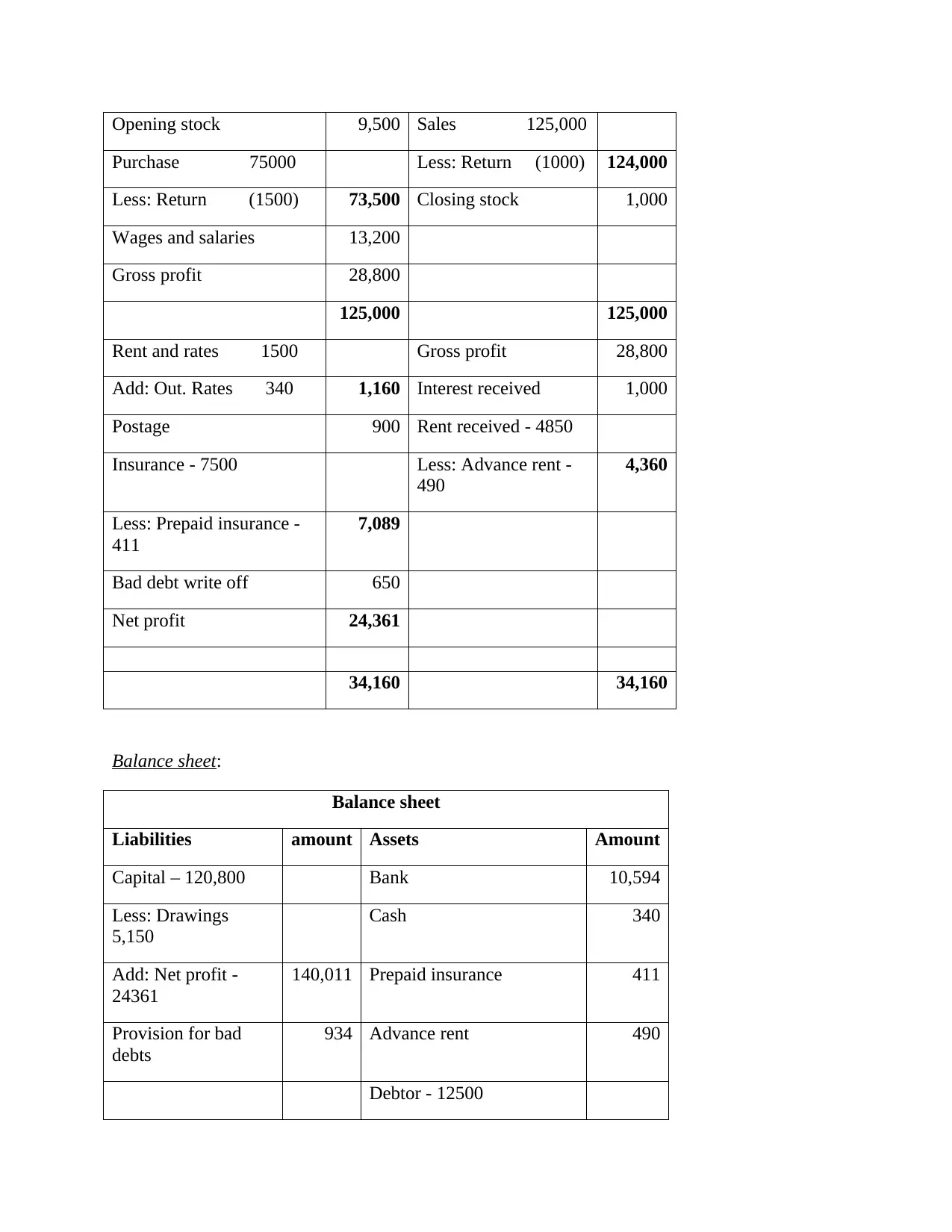

Profit and loss account for the year ended 31st December 2017:

Profit and loss account

Particulars Amount Particulars amount

There are many accounting standards which even the organisation adopts when

measuring its business activities and preparing account balances. Those are dealt below with:

Accrual principle: It is the concept of documenting bank documents in the accounting statement

and once they take place, instead of in the intervals so if cash flows integrate with each other.

This would be the basis of the accounting revenue statement. What really occurred mostly during

accounting cycle is critical for the growth of the firm’s financial performance, rather than being

unnatural method postponed or accelerated by the associated retained earnings (Kumar and et.al,

2018).

Conservatism Principle: this is also the concept that allows the study to document

commitments as rapidly as feasible, but still only document profit growth whether they are sure

that they will occur. This concept tends to advance refer to the relevant soon instead of

afterwards. When an organisation insistently mischaracterizes the results to be better than would

be probably the case, this principle may be driven far enough.

Full disclosure principle: This is the idea that business should disclose any details and may

have an impact on the recipient's interpretation of those reports in or as well as the business

performance statements. By identifying a vast number of social identities, the accounting

standards significantly strengthened this definition.

Going concern principle: The theory of going concern is the presumption that a company can

stay in operation for the coming years. In comparison, this ensures that the company will not be

compelled to suspend activities and repossess its properties at what could be very small fire-sale

rates in the near term. Through making this statement, the auditor is rational in postponing the

identification of such expenditures for a later date when the company is likely to stay in

operation and use its resources as quickly and efficiently as possible (Legenzova, 2016).

Question 5

Profit and loss account for the year ended 31st December 2017:

Profit and loss account

Particulars Amount Particulars amount

Opening stock 9,500 Sales 125,000

Purchase 75000 Less: Return (1000) 124,000

Less: Return (1500) 73,500 Closing stock 1,000

Wages and salaries 13,200

Gross profit 28,800

125,000 125,000

Rent and rates 1500 Gross profit 28,800

Add: Out. Rates 340 1,160 Interest received 1,000

Postage 900 Rent received - 4850

Insurance - 7500 Less: Advance rent -

490

4,360

Less: Prepaid insurance -

411

7,089

Bad debt write off 650

Net profit 24,361

34,160 34,160

Balance sheet:

Balance sheet

Liabilities amount Assets Amount

Capital – 120,800 Bank 10,594

Less: Drawings

5,150

Cash 340

Add: Net profit -

24361

140,011 Prepaid insurance 411

Provision for bad

debts

934 Advance rent 490

Debtor - 12500

Purchase 75000 Less: Return (1000) 124,000

Less: Return (1500) 73,500 Closing stock 1,000

Wages and salaries 13,200

Gross profit 28,800

125,000 125,000

Rent and rates 1500 Gross profit 28,800

Add: Out. Rates 340 1,160 Interest received 1,000

Postage 900 Rent received - 4850

Insurance - 7500 Less: Advance rent -

490

4,360

Less: Prepaid insurance -

411

7,089

Bad debt write off 650

Net profit 24,361

34,160 34,160

Balance sheet:

Balance sheet

Liabilities amount Assets Amount

Capital – 120,800 Bank 10,594

Less: Drawings

5,150

Cash 340

Add: Net profit -

24361

140,011 Prepaid insurance 411

Provision for bad

debts

934 Advance rent 490

Debtor - 12500

Creditor 3,900 Less: Bad debt write off -

934

11,850

Outstanding rates 340 Motor van at WDV - 19600

Less: Dep - 5000 14,600

Loan 100,000

Closing stock 1,000

145,185 145,185

SCENARIO 2

Question 1

It is a presumption that persons are able to recognize, clarify and accept any differences

in the difference between the bank statement and the balance as per the financial statements. Any

agreement between the issuer and the bank is agreed by all party representatives to enter

separately in their papers. For just a multitude of reasons which show various balances, these

documentation may be dissatisfied. The purpose of providing financial report is to identify and

clarify the reasons of this difference in checking account (Liang and Zhang, 2019).

Why bank reconciliation is required and how to achieve it:

Bank reconciliation procedures are conducted immediately to verify the bank records of

the company individually. The fundamental accounting demonstrates the variation between the

'Cash at Bank' value and the true value on the credit card. Business and bank hold financial

documents of the very same quantity of funds involved in the financial with bank. Some

differences relate to the fact that cash transactions recorded but at the other hand are sometimes

uneducated about record player. Money also obtained commercial transactions that may have

been reported and have not yet been documented in financial records or loan amount paid by the

loan from the corporation's bank account but has not notified by the corporation.

Another reason for allowing bank reconciliation is to accept the amount of capital

efficiently in the employment of the employees. The amount of funds mentioned on the bank

934

11,850

Outstanding rates 340 Motor van at WDV - 19600

Less: Dep - 5000 14,600

Loan 100,000

Closing stock 1,000

145,185 145,185

SCENARIO 2

Question 1

It is a presumption that persons are able to recognize, clarify and accept any differences

in the difference between the bank statement and the balance as per the financial statements. Any

agreement between the issuer and the bank is agreed by all party representatives to enter

separately in their papers. For just a multitude of reasons which show various balances, these

documentation may be dissatisfied. The purpose of providing financial report is to identify and

clarify the reasons of this difference in checking account (Liang and Zhang, 2019).

Why bank reconciliation is required and how to achieve it:

Bank reconciliation procedures are conducted immediately to verify the bank records of

the company individually. The fundamental accounting demonstrates the variation between the

'Cash at Bank' value and the true value on the credit card. Business and bank hold financial

documents of the very same quantity of funds involved in the financial with bank. Some

differences relate to the fact that cash transactions recorded but at the other hand are sometimes

uneducated about record player. Money also obtained commercial transactions that may have

been reported and have not yet been documented in financial records or loan amount paid by the

loan from the corporation's bank account but has not notified by the corporation.

Another reason for allowing bank reconciliation is to accept the amount of capital

efficiently in the employment of the employees. The amount of funds mentioned on the bank

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

statement does not necessarily represent the quantity of funds the business has interested to pay.

This can be due to the fact that perhaps the banking does not recognize the authentication that

were charged but have not yet been explained to the customer. Bank reconciliation is done by a

study of their very own financial reports that must be checked with their regular bank statement

to clear their balance sheets (Richard, 2015). Check each payment separately, please ensure the

sum matches perfectly and take into account any inconsistencies that require more analysis. The

procedure may be as structured or casual as they want, and certain firms can give notice of bank

reconciliation to show the accounts that are periodically reconciled. If the company is unable to

accomplish the task on a routine basis, this can be achieved on a frequent basis, on an annual or

any other form it wants. Defining and checking the optimum, and deciding if it is the very same

not, is significant. When individuals see a difference, or suggest a reason for that too, they must

have a justification.

Question 2

Explain control accounts:

In a general ledger account, the control account is often known as a management account and

describes and integrates all related financial information of a particular sort. In other terms, it is a

season accounts comparable to the full hierarchical accounts used to simplify the balance sheet

which handles it (Saud, Chen and Haseeb, 2020).

Role of control accounts in financial management:

Control accounts serve a variety of financial management functions that are of immediate benefit

to the business and listed elsewhere here:

• Sets up a system for original fault and fraud redress.

• Delete the unorganized General Ledger records.

• Large corporations shall make different statutory employment for particular locations.

• Projections of the trial balance include a rundown of the averages rather than the individual

accounts.

This can be due to the fact that perhaps the banking does not recognize the authentication that

were charged but have not yet been explained to the customer. Bank reconciliation is done by a

study of their very own financial reports that must be checked with their regular bank statement

to clear their balance sheets (Richard, 2015). Check each payment separately, please ensure the

sum matches perfectly and take into account any inconsistencies that require more analysis. The

procedure may be as structured or casual as they want, and certain firms can give notice of bank

reconciliation to show the accounts that are periodically reconciled. If the company is unable to

accomplish the task on a routine basis, this can be achieved on a frequent basis, on an annual or

any other form it wants. Defining and checking the optimum, and deciding if it is the very same

not, is significant. When individuals see a difference, or suggest a reason for that too, they must

have a justification.

Question 2

Explain control accounts:

In a general ledger account, the control account is often known as a management account and

describes and integrates all related financial information of a particular sort. In other terms, it is a

season accounts comparable to the full hierarchical accounts used to simplify the balance sheet

which handles it (Saud, Chen and Haseeb, 2020).

Role of control accounts in financial management:

Control accounts serve a variety of financial management functions that are of immediate benefit

to the business and listed elsewhere here:

• Sets up a system for original fault and fraud redress.

• Delete the unorganized General Ledger records.

• Large corporations shall make different statutory employment for particular locations.

• Projections of the trial balance include a rundown of the averages rather than the individual

accounts.

• Eliminates the possibility of fraud, particularly although this payment processing documents

and the primary report are handled separately by different personnel.

Question 3

Explain suspense account:

Suspense account is defined as a general ledger account wherein the company keeps

documenting its ambiguous entries and may need additional study to decide each person's

marketing funnel or position. Suspense account is a form in which the investor restaurants their

capital for an amount of time before being used through to public expenditure (Tahat and

Alhadab, 2017).

Reasons of drafting suspense account:

This account may also be formulated wherein the appropriate reimbursement at the time the

transactions were initially approved could not be recorded or quantified. A few instances of this

will be when such a recipient provides a limited bill, even if they're uncertain that bill people

pay. Whenever the payment volatility is resolved with the consumer, the equilibrium attributable

will be relocated from the consideration of expectation to the account linked.

Unless the trial balance of the company continues to be so out of reach, the imbalance will stay

in the expectation fund until the other difference is fixed. The assumption payment will be shown

on the trial balance under the moving "Other counterparty assets." unless the company has

realized and corrected the justification for the disparity, the assumption equilibrium will be

connected; although the trial balance would no matter how much experience be involved.

Question 4

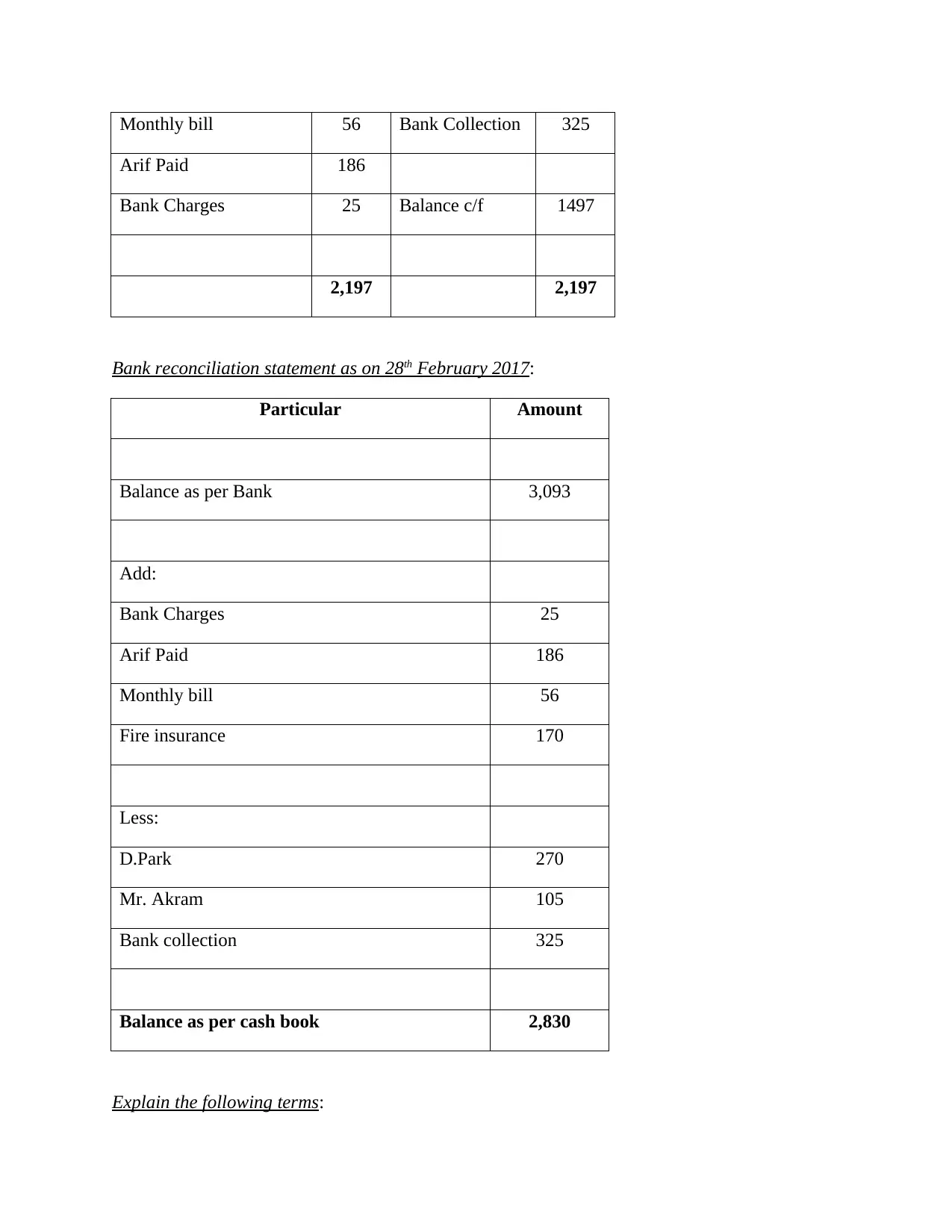

Updated cash book as at 28th February 2017:

Revised cash Book

Particulars Dr. Particular Cr.

Balance b/d 1,760 D.Park 270

Insurance against fire 170 Mr. Akram 105

and the primary report are handled separately by different personnel.

Question 3

Explain suspense account:

Suspense account is defined as a general ledger account wherein the company keeps

documenting its ambiguous entries and may need additional study to decide each person's

marketing funnel or position. Suspense account is a form in which the investor restaurants their

capital for an amount of time before being used through to public expenditure (Tahat and

Alhadab, 2017).

Reasons of drafting suspense account:

This account may also be formulated wherein the appropriate reimbursement at the time the

transactions were initially approved could not be recorded or quantified. A few instances of this

will be when such a recipient provides a limited bill, even if they're uncertain that bill people

pay. Whenever the payment volatility is resolved with the consumer, the equilibrium attributable

will be relocated from the consideration of expectation to the account linked.

Unless the trial balance of the company continues to be so out of reach, the imbalance will stay

in the expectation fund until the other difference is fixed. The assumption payment will be shown

on the trial balance under the moving "Other counterparty assets." unless the company has

realized and corrected the justification for the disparity, the assumption equilibrium will be

connected; although the trial balance would no matter how much experience be involved.

Question 4

Updated cash book as at 28th February 2017:

Revised cash Book

Particulars Dr. Particular Cr.

Balance b/d 1,760 D.Park 270

Insurance against fire 170 Mr. Akram 105

Monthly bill 56 Bank Collection 325

Arif Paid 186

Bank Charges 25 Balance c/f 1497

2,197 2,197

Bank reconciliation statement as on 28th February 2017:

Particular Amount

Balance as per Bank 3,093

Add:

Bank Charges 25

Arif Paid 186

Monthly bill 56

Fire insurance 170

Less:

D.Park 270

Mr. Akram 105

Bank collection 325

Balance as per cash book 2,830

Explain the following terms:

Arif Paid 186

Bank Charges 25 Balance c/f 1497

2,197 2,197

Bank reconciliation statement as on 28th February 2017:

Particular Amount

Balance as per Bank 3,093

Add:

Bank Charges 25

Arif Paid 186

Monthly bill 56

Fire insurance 170

Less:

D.Park 270

Mr. Akram 105

Bank collection 325

Balance as per cash book 2,830

Explain the following terms:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Direct debit: It is the quickest, least expensive and perhaps most efficient method of making

routine or periodic disbursements; which is why it is shown in goods such as local taxes and

consumes a lot. Direct Debit allows someone to pay it back from the transactions till they are

attributable. Many who offer the approval by submitting a direct debit requirement template; this

may be a document type or a web browser submitting it internet.

Standing order: A contract of employment that impacts its staff members may identify the

direct debit in any company as the serving sizes of the cloud storage. A union member aimed at

attaining uniformity in the work pressure as set down by the statutes legislature and the

corresponding jurisdiction has numerous reasons.

Bank charges: This covers all costs and fees paid from its clients by the bank. In commonly

used words; fees are commonly referred to for specific direct debits or approved transactions and

are paid on a periodic basis.

Dishonored cheque: companies offer the public purse the number, it's said the payment was

produced. Unless the bank refuses to pay the payment method the amount, the act is considered

to have been dishonored. In several other terms, search dishonor is a situation in which the bank

has stopped paying the payer the checking number (Werner, 2017).

Question 5

Journal entries:

S. No Particulars Dr. Cr.

1 Goods purchase account 2000

To suspense 2000

2 Bank Account 670

To suspense 670

3 Sales 650

routine or periodic disbursements; which is why it is shown in goods such as local taxes and

consumes a lot. Direct Debit allows someone to pay it back from the transactions till they are

attributable. Many who offer the approval by submitting a direct debit requirement template; this

may be a document type or a web browser submitting it internet.

Standing order: A contract of employment that impacts its staff members may identify the

direct debit in any company as the serving sizes of the cloud storage. A union member aimed at

attaining uniformity in the work pressure as set down by the statutes legislature and the

corresponding jurisdiction has numerous reasons.

Bank charges: This covers all costs and fees paid from its clients by the bank. In commonly

used words; fees are commonly referred to for specific direct debits or approved transactions and

are paid on a periodic basis.

Dishonored cheque: companies offer the public purse the number, it's said the payment was

produced. Unless the bank refuses to pay the payment method the amount, the act is considered

to have been dishonored. In several other terms, search dishonor is a situation in which the bank

has stopped paying the payer the checking number (Werner, 2017).

Question 5

Journal entries:

S. No Particulars Dr. Cr.

1 Goods purchase account 2000

To suspense 2000

2 Bank Account 670

To suspense 670

3 Sales 650

To G. Tahir 650

4 Electricity Bill 790

To Cash account 790

5 Expense account 500

To Motor vehicle 500

6 Sales accounts 270

To sales day book 270

7 L Samantha 190

To Discount receivable 190

Discount allowed 190

To L Samantha 190

8 D. Jones 384

To account receivable 384

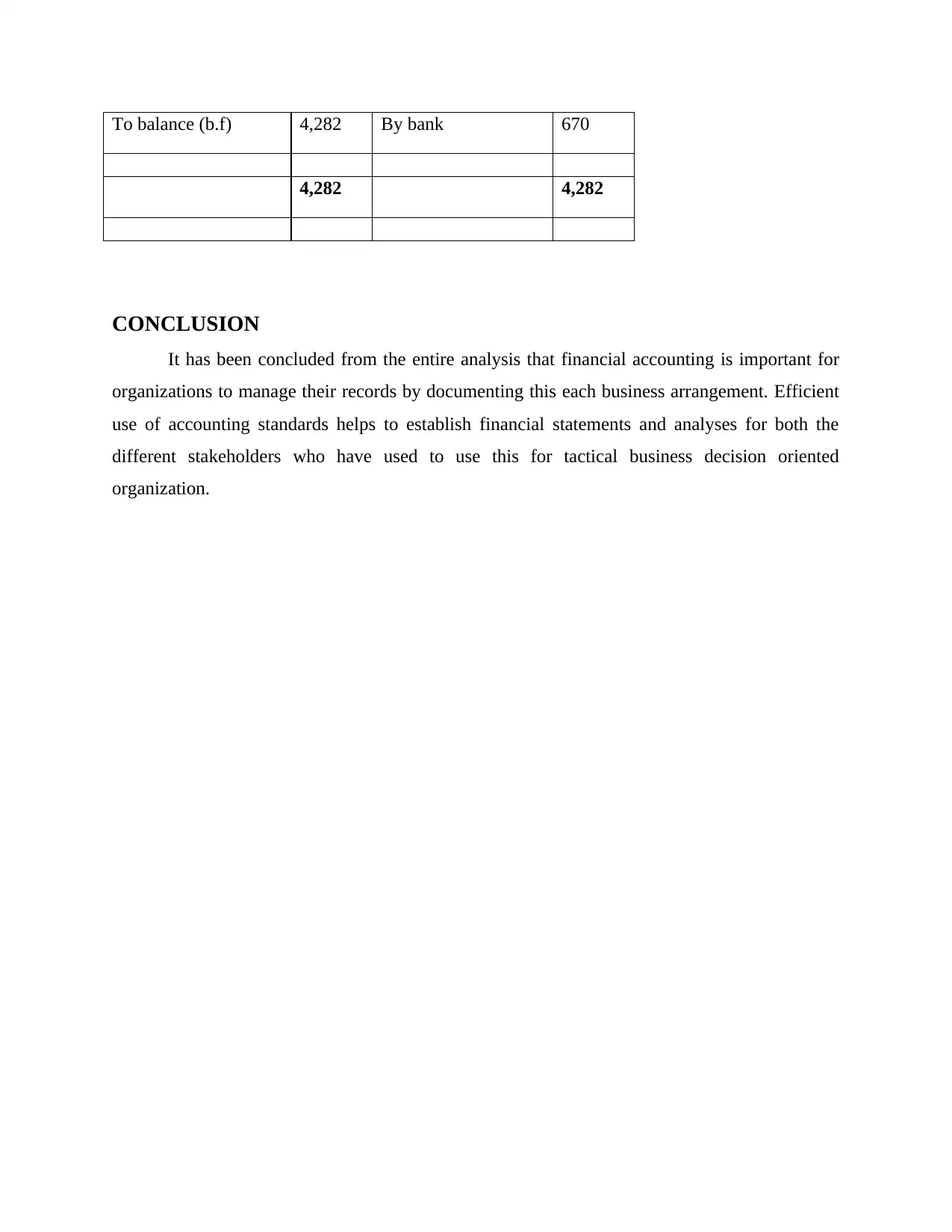

Suspense account:

Suspense account

Particulars Amoun

t

Particulars Amoun

t

By balance 1,612

By goods purchase 2,000

4 Electricity Bill 790

To Cash account 790

5 Expense account 500

To Motor vehicle 500

6 Sales accounts 270

To sales day book 270

7 L Samantha 190

To Discount receivable 190

Discount allowed 190

To L Samantha 190

8 D. Jones 384

To account receivable 384

Suspense account:

Suspense account

Particulars Amoun

t

Particulars Amoun

t

By balance 1,612

By goods purchase 2,000

To balance (b.f) 4,282 By bank 670

4,282 4,282

CONCLUSION

It has been concluded from the entire analysis that financial accounting is important for

organizations to manage their records by documenting this each business arrangement. Efficient

use of accounting standards helps to establish financial statements and analyses for both the

different stakeholders who have used to use this for tactical business decision oriented

organization.

4,282 4,282

CONCLUSION

It has been concluded from the entire analysis that financial accounting is important for

organizations to manage their records by documenting this each business arrangement. Efficient

use of accounting standards helps to establish financial statements and analyses for both the

different stakeholders who have used to use this for tactical business decision oriented

organization.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

REFERENCES

Books and Journal

Aifuwa, H. O., Embele, K. and Saidu, M., 2018. Ethical accounting practices and financial

reporting quality. EPRA Journal of Multidisciplinary Research. 4(12). pp.31-44.

Appelbaum, D. and et.al, 2017. Impact of business analytics and enterprise systems on

managerial accounting. International Journal of Accounting Information Systems. 25.

pp.29-44.

Ayres, D., Huang, X. S. and Myring, M., 2017. Fair value accounting and analyst forecast

accuracy. Advances in accounting. 37. pp.58-70.

Bishop, C. C., DeZoort, F. T. and Hermanson, D. R., 2017. The effect of CEO social influence

pressure and CFO accounting experience on CFO financial reporting decisions. Auditing:

A Journal of Practice & Theory. 36(1). pp.21-41.

Bolívar, M. P. R. and et.al, 2018. Analysing the accounting measurement of financial

sustainability in local governments through political factors. Accounting, Auditing &

Accountability Journal.

Brusca, I. and et.al, 2016. Public sector accounting and auditing in Europe: The challenge of

harmonization. Springer.

González, R. M. D., Julve, V. M. and Bargues, J. M. V., 2018. Towards convergence of

government financial statistics and accounting in Europe at central and local

levels. Revista de Contabilidad-Spanish Accounting Review. 21(2). pp.140-149.

Gotti, G., 2016. Discussion of Segment Disclosure Quantity and Quality under IFRS 8:

Determinants and the Effect of Financial Analysts' Earnings Forecast Errors. The

International Journal of Accounting. 51(4). pp.462-463.

Honggowati, S. and et.al, 2017. Corporate governance and strategic management accounting

disclosure. Indonesian Journal of Sustainability Accounting and Management. 1(1).

pp.23-30.

Khoja, L., Chipulu, M. and Jayasekera, R., 2019. Analysis of financial distress cross countries:

Using macroeconomic, industrial indicators and accounting data. International Review of

Financial Analysis, 66, p.101379.

Kumar, R. R. and et.al, 2018. The effect of remittances on economic growth in Kyrgyzstan and

Macedonia: accounting for financial development. International Migration. 56(1). pp.95-

126.

Legenzova, R., 2016. A concept of accounting quality from accounting harmonisation

perspective. Economics and Business. 28(1). pp.33-37.

Books and Journal

Aifuwa, H. O., Embele, K. and Saidu, M., 2018. Ethical accounting practices and financial

reporting quality. EPRA Journal of Multidisciplinary Research. 4(12). pp.31-44.

Appelbaum, D. and et.al, 2017. Impact of business analytics and enterprise systems on

managerial accounting. International Journal of Accounting Information Systems. 25.

pp.29-44.

Ayres, D., Huang, X. S. and Myring, M., 2017. Fair value accounting and analyst forecast

accuracy. Advances in accounting. 37. pp.58-70.

Bishop, C. C., DeZoort, F. T. and Hermanson, D. R., 2017. The effect of CEO social influence

pressure and CFO accounting experience on CFO financial reporting decisions. Auditing:

A Journal of Practice & Theory. 36(1). pp.21-41.

Bolívar, M. P. R. and et.al, 2018. Analysing the accounting measurement of financial

sustainability in local governments through political factors. Accounting, Auditing &

Accountability Journal.

Brusca, I. and et.al, 2016. Public sector accounting and auditing in Europe: The challenge of

harmonization. Springer.

González, R. M. D., Julve, V. M. and Bargues, J. M. V., 2018. Towards convergence of

government financial statistics and accounting in Europe at central and local

levels. Revista de Contabilidad-Spanish Accounting Review. 21(2). pp.140-149.

Gotti, G., 2016. Discussion of Segment Disclosure Quantity and Quality under IFRS 8:

Determinants and the Effect of Financial Analysts' Earnings Forecast Errors. The

International Journal of Accounting. 51(4). pp.462-463.

Honggowati, S. and et.al, 2017. Corporate governance and strategic management accounting

disclosure. Indonesian Journal of Sustainability Accounting and Management. 1(1).

pp.23-30.

Khoja, L., Chipulu, M. and Jayasekera, R., 2019. Analysis of financial distress cross countries:

Using macroeconomic, industrial indicators and accounting data. International Review of

Financial Analysis, 66, p.101379.

Kumar, R. R. and et.al, 2018. The effect of remittances on economic growth in Kyrgyzstan and

Macedonia: accounting for financial development. International Migration. 56(1). pp.95-

126.

Legenzova, R., 2016. A concept of accounting quality from accounting harmonisation

perspective. Economics and Business. 28(1). pp.33-37.

Liang, P. J. and Zhang, G., 2019. On the social value of accounting objectivity in financial

stability. The Accounting Review. 94(1). pp.229-248.

Richard, J., 2015. The dangerous dynamics of modern capitalism (from static to IFRS’futuristic

accounting). Critical Perspectives on Accounting. 30. pp.9-34.

Saud, S., Chen, S. and Haseeb, A., 2020. The role of financial development and globalization in

the environment: Accounting ecological footprint indicators for selected one-belt-one-

road initiative countries. Journal of Cleaner Production. 250. p.119518.

Tahat, Y. A. and Alhadab, M., 2017. Have accounting numbers lost their value relevance during

the recent financial credit crisis?. The Quarterly Review of Economics and Finance. 66.

pp.182-191.

Werner, M., 2017. Financial process mining-Accounting data structure dependent control flow

inference. International Journal of Accounting Information Systems. 25. pp.57-80.

stability. The Accounting Review. 94(1). pp.229-248.

Richard, J., 2015. The dangerous dynamics of modern capitalism (from static to IFRS’futuristic

accounting). Critical Perspectives on Accounting. 30. pp.9-34.

Saud, S., Chen, S. and Haseeb, A., 2020. The role of financial development and globalization in

the environment: Accounting ecological footprint indicators for selected one-belt-one-

road initiative countries. Journal of Cleaner Production. 250. p.119518.

Tahat, Y. A. and Alhadab, M., 2017. Have accounting numbers lost their value relevance during

the recent financial credit crisis?. The Quarterly Review of Economics and Finance. 66.

pp.182-191.

Werner, M., 2017. Financial process mining-Accounting data structure dependent control flow

inference. International Journal of Accounting Information Systems. 25. pp.57-80.

1 out of 24

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.