ACFI5020 Accounting: Analyzing Financial Ratios of Hotel Chocolat

VerifiedAdded on 2023/06/15

|11

|2607

|65

Report

AI Summary

This report provides a detailed financial analysis of Hotel Chocolat plc, utilizing accounting ratios to assess the company's liquidity, profitability, and efficiency. It examines the company's performance across several years, highlighting key trends and challenges, particularly the impact of the pandemic. The analysis includes calculations and interpretations of ratios such as current ratio, quick ratio, return on capital employed, gross profit margin, net margin, asset turnover, and debt-to-equity ratio. The report also discusses potential improvements for the company, such as enhancing inventory turnover, increasing return on investment, managing volatility, and improving profitability. Furthermore, it explores the influence of factors like supply disruptions, international vulnerability, and market expansion on the company's accounting ratios and overall financial health.

Accounting for

Managers ACFI5020

Managers ACFI5020

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

Contents...........................................................................................................................................2

INTRODUCTION...........................................................................................................................1

MAIN BODY..................................................................................................................................1

Task 1...........................................................................................................................................1

Task 2...........................................................................................................................................4

Task 3...........................................................................................................................................6

Task 4...........................................................................................................................................7

Task 5...........................................................................................................................................7

CONCLUSION................................................................................................................................8

REFERENCES................................................................................................................................9

Contents...........................................................................................................................................2

INTRODUCTION...........................................................................................................................1

MAIN BODY..................................................................................................................................1

Task 1...........................................................................................................................................1

Task 2...........................................................................................................................................4

Task 3...........................................................................................................................................6

Task 4...........................................................................................................................................7

Task 5...........................................................................................................................................7

CONCLUSION................................................................................................................................8

REFERENCES................................................................................................................................9

INTRODUCTION

Firm's monetary assessment can reveal data about a firm’s revenue, stability, operating

excellence, and viability (Alsharari and Abougamos, 2017). Hotel Chocolat plc is a British

chocolates and bean firm with over 100 stores across the country. The current study offers a

detailed analysis of the company's fiscal achievements. An overview of the officer’s

management is included in the latest presentation, and also information on possible threats which

could affect the proportion cost and schedule.

MAIN BODY

Task 1

Calculation of ratios

HOTEL CHOCOLAT

2019 2020 2021

Liquidity

ratio

Current assets 28029 51531 55554

Current

liability 21153 38271 52209

Inventory 12810 13916 32038

Quick Assets 15219 37615 23516

28029/21153 51531/38271 55554/52209

Current ratio

Current assets /

current liabilities 1.33:1 1.35:1 1.06:1

(28029-12810)/21153

(51531–

13916)/38271 (55554-32038)/55029

Quick Ratio

(Current Assets -

Inventory) / Current

Liabilities 0.72 0.98 0.45

Firm's monetary assessment can reveal data about a firm’s revenue, stability, operating

excellence, and viability (Alsharari and Abougamos, 2017). Hotel Chocolat plc is a British

chocolates and bean firm with over 100 stores across the country. The current study offers a

detailed analysis of the company's fiscal achievements. An overview of the officer’s

management is included in the latest presentation, and also information on possible threats which

could affect the proportion cost and schedule.

MAIN BODY

Task 1

Calculation of ratios

HOTEL CHOCOLAT

2019 2020 2021

Liquidity

ratio

Current assets 28029 51531 55554

Current

liability 21153 38271 52209

Inventory 12810 13916 32038

Quick Assets 15219 37615 23516

28029/21153 51531/38271 55554/52209

Current ratio

Current assets /

current liabilities 1.33:1 1.35:1 1.06:1

(28029-12810)/21153

(51531–

13916)/38271 (55554-32038)/55029

Quick Ratio

(Current Assets -

Inventory) / Current

Liabilities 0.72 0.98 0.45

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Profitability

ratio

Employed

Capital 53040 104267 113806

PBIT 10929 -7541 7824

(10929/53040)*100 (7457/104267)*100 (7824/113806)*100

Return on

capital

employed

PBIT/Employed

Capital 20.61% -7.23% 6.87%

Profit after tax 10929 -7457 5685

Shareholder's

Equity 49330 66990 71688

10929/49330 -7457/66990 5685/71688

Return on

Equity

Profit after tax /

Shareholder's Equity 22.15% -11.13% 7.93%

Cost of Sales 45140 53256 62877

Sales 132480 136290 164551

(132480-

45140)/132480*100

(136290-

53256/136290)*100

(164551-

62877/164551)*100

Gross

Margin COGS/Total Sales 65.93% 60.92% 61.79%

Net Operating

profit 14061 -7541 7824

Sales 132480 136290 164551

(14061/132480)*100 (-7541/136290)*100 (7824/164551)*100

Net

Operating

profit ratio

Operating Income/

Net Sales 10.61% -5.53% 4.75%

ratio

Employed

Capital 53040 104267 113806

PBIT 10929 -7541 7824

(10929/53040)*100 (7457/104267)*100 (7824/113806)*100

Return on

capital

employed

PBIT/Employed

Capital 20.61% -7.23% 6.87%

Profit after tax 10929 -7457 5685

Shareholder's

Equity 49330 66990 71688

10929/49330 -7457/66990 5685/71688

Return on

Equity

Profit after tax /

Shareholder's Equity 22.15% -11.13% 7.93%

Cost of Sales 45140 53256 62877

Sales 132480 136290 164551

(132480-

45140)/132480*100

(136290-

53256/136290)*100

(164551-

62877/164551)*100

Gross

Margin COGS/Total Sales 65.93% 60.92% 61.79%

Net Operating

profit 14061 -7541 7824

Sales 132480 136290 164551

(14061/132480)*100 (-7541/136290)*100 (7824/164551)*100

Net

Operating

profit ratio

Operating Income/

Net Sales 10.61% -5.53% 4.75%

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Net Profit

Margin Net Profit/Sales (10929/132480)*100 (-7457/136290)*100 (5685/164551)*100

8.24% -5.47% 3.45%

Efficiency

Ratios

Inventory 12810 13916 32038

Trade

Receivables 9360 7492 12421

Net Assets 49330 66990 71688

Cost of Sales 45140 53256 62877

Sales 132480 136290 164551

ATO 132480/53040 136290/104267 164551/113806

Asset

turnover

ratio

Sales / Capital

employed 2.49 2.03 2.30

45140/12810 53256/13916 62877/32038

Inventory

turnover

ratio Sales / Inventory 3.52 3.83 1.96

(3710/132480)*365 (7492/136290)*365 (12421/164551)*365

Account

receivable

turnover

ratio

(Accounts Receivable

/

Sales)*365 14.15 18.19 13.25

(12810/45140)*365 (13916/53256)*365 (32038/62877)*365

Stock Days

Average

(Stock/COGS)*365 104 95 186

Margin Net Profit/Sales (10929/132480)*100 (-7457/136290)*100 (5685/164551)*100

8.24% -5.47% 3.45%

Efficiency

Ratios

Inventory 12810 13916 32038

Trade

Receivables 9360 7492 12421

Net Assets 49330 66990 71688

Cost of Sales 45140 53256 62877

Sales 132480 136290 164551

ATO 132480/53040 136290/104267 164551/113806

Asset

turnover

ratio

Sales / Capital

employed 2.49 2.03 2.30

45140/12810 53256/13916 62877/32038

Inventory

turnover

ratio Sales / Inventory 3.52 3.83 1.96

(3710/132480)*365 (7492/136290)*365 (12421/164551)*365

Account

receivable

turnover

ratio

(Accounts Receivable

/

Sales)*365 14.15 18.19 13.25

(12810/45140)*365 (13916/53256)*365 (32038/62877)*365

Stock Days

Average

(Stock/COGS)*365 104 95 186

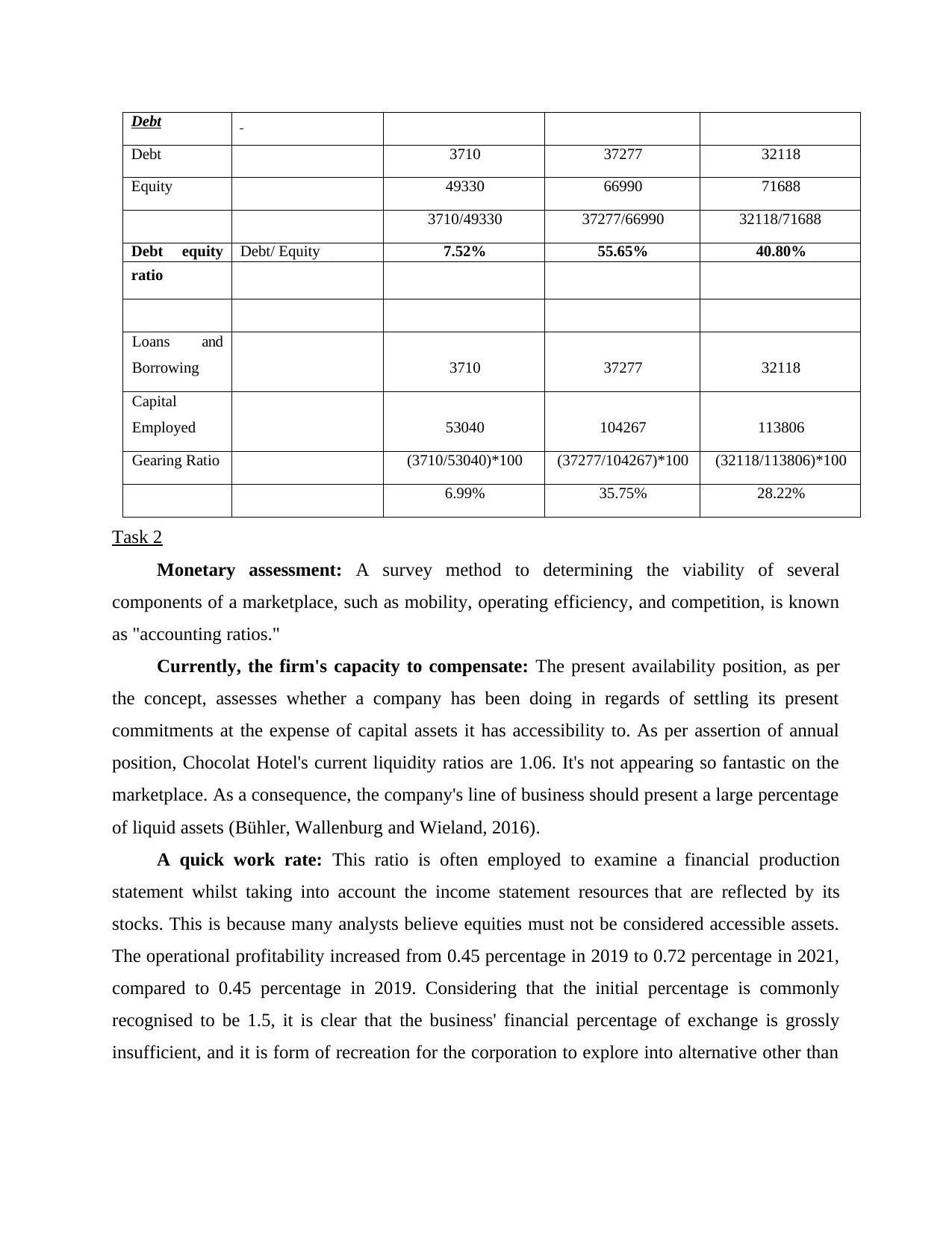

Debt

Debt 3710 37277 32118

Equity 49330 66990 71688

3710/49330 37277/66990 32118/71688

Debt equity Debt/ Equity 7.52% 55.65% 40.80%

ratio

Loans and

Borrowing 3710 37277 32118

Capital

Employed 53040 104267 113806

Gearing Ratio (3710/53040)*100 (37277/104267)*100 (32118/113806)*100

6.99% 35.75% 28.22%

Task 2

Monetary assessment: A survey method to determining the viability of several

components of a marketplace, such as mobility, operating efficiency, and competition, is known

as "accounting ratios."

Currently, the firm's capacity to compensate: The present availability position, as per

the concept, assesses whether a company has been doing in regards of settling its present

commitments at the expense of capital assets it has accessibility to. As per assertion of annual

position, Chocolat Hotel's current liquidity ratios are 1.06. It's not appearing so fantastic on the

marketplace. As a consequence, the company's line of business should present a large percentage

of liquid assets (Bühler, Wallenburg and Wieland, 2016).

A quick work rate: This ratio is often employed to examine a financial production

statement whilst taking into account the income statement resources that are reflected by its

stocks. This is because many analysts believe equities must not be considered accessible assets.

The operational profitability increased from 0.45 percentage in 2019 to 0.72 percentage in 2021,

compared to 0.45 percentage in 2019. Considering that the initial percentage is commonly

recognised to be 1.5, it is clear that the business' financial percentage of exchange is grossly

insufficient, and it is form of recreation for the corporation to explore into alternative other than

Debt 3710 37277 32118

Equity 49330 66990 71688

3710/49330 37277/66990 32118/71688

Debt equity Debt/ Equity 7.52% 55.65% 40.80%

ratio

Loans and

Borrowing 3710 37277 32118

Capital

Employed 53040 104267 113806

Gearing Ratio (3710/53040)*100 (37277/104267)*100 (32118/113806)*100

6.99% 35.75% 28.22%

Task 2

Monetary assessment: A survey method to determining the viability of several

components of a marketplace, such as mobility, operating efficiency, and competition, is known

as "accounting ratios."

Currently, the firm's capacity to compensate: The present availability position, as per

the concept, assesses whether a company has been doing in regards of settling its present

commitments at the expense of capital assets it has accessibility to. As per assertion of annual

position, Chocolat Hotel's current liquidity ratios are 1.06. It's not appearing so fantastic on the

marketplace. As a consequence, the company's line of business should present a large percentage

of liquid assets (Bühler, Wallenburg and Wieland, 2016).

A quick work rate: This ratio is often employed to examine a financial production

statement whilst taking into account the income statement resources that are reflected by its

stocks. This is because many analysts believe equities must not be considered accessible assets.

The operational profitability increased from 0.45 percentage in 2019 to 0.72 percentage in 2021,

compared to 0.45 percentage in 2019. Considering that the initial percentage is commonly

recognised to be 1.5, it is clear that the business' financial percentage of exchange is grossly

insufficient, and it is form of recreation for the corporation to explore into alternative other than

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

the planned capital magnitude relation. Somebody who gains income by participating in

companies is referred to as an operator.

Return on capital: This proportion is commonly utilized to evaluate an owner's

performance in regards of effectively employing goods. As per the business's ROCE analysis,

this percentage would drop to 20.61 percentage in 2019, but would increase to 5.48 percentage in

2021. Reducing clients and deflationary economy earnings were cited as among the main reasons

for the drop in ROCE (Eisenberg, 2016).

Proportion of Productivity

Gross Profit margin: It is determined using various resources in the firm to evaluate the

company's performance and development. So when yield on equities for two years is examined,

the yield on capital in 2020 is -11.13 percentage, while the yield on capital in 2021 is 7.93

percentage. Such improvements show that the company has acknowledged previous issues and

changed its operational practises. It also helped the group achieve great results.

Profitable

Proportion of gross margin: Once all of the corporation's owners for the output have

indeed been covered, this percentage decides how much amount of net income left in the

business. The operating income for the sector is predicted to grow to 60.92 percentage in 2020

and 61.79 percentage in 2021, noted a large improvement in GP. As a consequence, the company

could be said to be particularly good in managing operating costs.

Net margin: While looking at this profitability ratio, it is clear that the outbreak had no

impact, hence it is critical to examine the company's revenue income. The company's net income

margins increased, but only slightly. Firm should keep on trying a range of approaches in order

to maintain their current degree of improvement. In form of proportion, 5.47 percentage in 2019

and 3.45 percentage in 2020 were reached (Glushchenko, Yarkova and Kucherova, 2017).

The Productivity Ratio: It is a metric for determining how effectively a procedure is

performed through. Operating margin is critical in the organizational processes. The company's

turnover ratio has dropped from 2.69 in 2018 to 2.30 in 2019. This shows that the company has

been incapable to make full utilization of its assets. It was clear that the firm used its capital

more effectively last year than it would this year. In the corporate sector, stocks are changed onto

a constant schedule; turnover ratio is described as leadership's ability to update merchandise in a

short amount of duration. Stock turnover fell to 1.96 in 2019, down from 3.83 the year before.

companies is referred to as an operator.

Return on capital: This proportion is commonly utilized to evaluate an owner's

performance in regards of effectively employing goods. As per the business's ROCE analysis,

this percentage would drop to 20.61 percentage in 2019, but would increase to 5.48 percentage in

2021. Reducing clients and deflationary economy earnings were cited as among the main reasons

for the drop in ROCE (Eisenberg, 2016).

Proportion of Productivity

Gross Profit margin: It is determined using various resources in the firm to evaluate the

company's performance and development. So when yield on equities for two years is examined,

the yield on capital in 2020 is -11.13 percentage, while the yield on capital in 2021 is 7.93

percentage. Such improvements show that the company has acknowledged previous issues and

changed its operational practises. It also helped the group achieve great results.

Profitable

Proportion of gross margin: Once all of the corporation's owners for the output have

indeed been covered, this percentage decides how much amount of net income left in the

business. The operating income for the sector is predicted to grow to 60.92 percentage in 2020

and 61.79 percentage in 2021, noted a large improvement in GP. As a consequence, the company

could be said to be particularly good in managing operating costs.

Net margin: While looking at this profitability ratio, it is clear that the outbreak had no

impact, hence it is critical to examine the company's revenue income. The company's net income

margins increased, but only slightly. Firm should keep on trying a range of approaches in order

to maintain their current degree of improvement. In form of proportion, 5.47 percentage in 2019

and 3.45 percentage in 2020 were reached (Glushchenko, Yarkova and Kucherova, 2017).

The Productivity Ratio: It is a metric for determining how effectively a procedure is

performed through. Operating margin is critical in the organizational processes. The company's

turnover ratio has dropped from 2.69 in 2018 to 2.30 in 2019. This shows that the company has

been incapable to make full utilization of its assets. It was clear that the firm used its capital

more effectively last year than it would this year. In the corporate sector, stocks are changed onto

a constant schedule; turnover ratio is described as leadership's ability to update merchandise in a

short amount of duration. Stock turnover fell to 1.96 in 2019, down from 3.83 the year before.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Accounts receivables turnover proportion: Whenever a corporation's this proportion is

significant, it shows how much energy it spends on the marketplace seeking to collect loans from

its borrowers. To improve the very same liquidity ratios, a variety of measures should be taken.

Borrowing-to-GDP Ratios: The debt-to-equity proportion is a finance metric which can

be used to assess a firm's fiscal stability and also the level of volatility associated with its

activities. The payout percentage is utilized to show that the debt-to-income percentage is

declining, with a goal of 55.65% in 2020 and 44.80% currently (Kuurila, 2016).

Task 3

Advancement: As a consequence of reviewing all of the various proportions, the company

required to undertake a lot of modifications. Some of the required changes are as follows:

Efficiency Possibility: According to the research, a company's inventory turnover isn't

quite as good as it appears and disappears. The marketing plan of a corporation might be

strengthened to improve annualized rates.

Returns on Investing: While ROCE have improved, the company does still have work

to do to improve its ROI. Businesses should utilize all of its assets to the greatest degree

feasible as a preliminary step for development. Furthermore, lowering the firm's non-

productive resources may help to improve this proportion (Roberts and Gnan, 2017).

The Volatility Factor: By judging by the present stability proportion, it's simple to

understand why the company's business working capital is not at all strong and also too

insufficient in the marketplace. When a firm's revenue circulation statement is poor, it's

more difficult to fulfil monthly repayments that undermine the professional image with

vendors. Increased flexibility over the transfer of cash is essential to improve the image

of the identical company.

Profitable Proportion: The overall income proportion could only be enhanced by

employing a variety of cost-effective strategies that would ultimately result in reduced

manufacturing expenses and a higher overall income proportion. By verifying that a

company's expenses are handled in a way which adds to the company's corporation

financial performance, the competitiveness proportion percentage can be enhanced.

Liquidity management proportion: To decrease a firm's financial leverage, resources

or financial money should be utilised to pay down the mortgage. In the big scheme of

things, a lower debt-to-equity proportion would support the business.

significant, it shows how much energy it spends on the marketplace seeking to collect loans from

its borrowers. To improve the very same liquidity ratios, a variety of measures should be taken.

Borrowing-to-GDP Ratios: The debt-to-equity proportion is a finance metric which can

be used to assess a firm's fiscal stability and also the level of volatility associated with its

activities. The payout percentage is utilized to show that the debt-to-income percentage is

declining, with a goal of 55.65% in 2020 and 44.80% currently (Kuurila, 2016).

Task 3

Advancement: As a consequence of reviewing all of the various proportions, the company

required to undertake a lot of modifications. Some of the required changes are as follows:

Efficiency Possibility: According to the research, a company's inventory turnover isn't

quite as good as it appears and disappears. The marketing plan of a corporation might be

strengthened to improve annualized rates.

Returns on Investing: While ROCE have improved, the company does still have work

to do to improve its ROI. Businesses should utilize all of its assets to the greatest degree

feasible as a preliminary step for development. Furthermore, lowering the firm's non-

productive resources may help to improve this proportion (Roberts and Gnan, 2017).

The Volatility Factor: By judging by the present stability proportion, it's simple to

understand why the company's business working capital is not at all strong and also too

insufficient in the marketplace. When a firm's revenue circulation statement is poor, it's

more difficult to fulfil monthly repayments that undermine the professional image with

vendors. Increased flexibility over the transfer of cash is essential to improve the image

of the identical company.

Profitable Proportion: The overall income proportion could only be enhanced by

employing a variety of cost-effective strategies that would ultimately result in reduced

manufacturing expenses and a higher overall income proportion. By verifying that a

company's expenses are handled in a way which adds to the company's corporation

financial performance, the competitiveness proportion percentage can be enhanced.

Liquidity management proportion: To decrease a firm's financial leverage, resources

or financial money should be utilised to pay down the mortgage. In the big scheme of

things, a lower debt-to-equity proportion would support the business.

Task 4

An examination of the operations assessment:

Promotion of other businesses: The company is alleged to have lent cash to one of its

collaborative relationships in Tokyo. They wanted to help effect current company internal

funds that are raised by any money lent as acquisitions. With this in mind, Hotel Chocolat may

probably achieve its working capital increase while focusing on the beneficial impact on

accounting ratios.

Capability Advancement: If the facility is enlarged to 160,000 square meters, revenues

would increase to $500 million. As a consequence, shareholders' earnings would soar, and

additional territories would start opening. Hotel Chocolat can take use of this chance to expand

its marketplace and improve overall fiscal analyses. As a result, this component would aid in

determining the company's anticipated impact on accounting ratios.

Funding: Investment in technology which assists in the introduction of unique concepts

is an option for businesses. According to the inspectors, new technology or hiring new staff

could have a substantial impact on the company's existing obligations whilst still improving its

business results (Tan, 2016).

Industrial Growth in the Great Britain: To increase manufacturing capability,

corporations must build facilities to accommodate more than 80,000 employees. This would be

ideal for their needs. It enables Hotel Chocolat to extend their company and concentrate on

exterior initiatives, allowing them to assess the value of their assets. It would have a favourable

impact on accounting ratios.

Task 5

The influence of volatility on accounting ratios:

Supplying disruptions: If a firm or organisation is ineffective, it is difficult to provide

things and activities on schedule that has an influence on revenues and, by implication, other

areas of its activities, such as accounts receivable. This component could have both a direct and

indirect effect on accounting ratios.

International vulnerability: Any international vulnerability would have an impact on a

corporation's economic situation and profit generation. It must have been admitted that this

vulnerability had influenced the cash flow in some way. It aids the company's emphasis on

An examination of the operations assessment:

Promotion of other businesses: The company is alleged to have lent cash to one of its

collaborative relationships in Tokyo. They wanted to help effect current company internal

funds that are raised by any money lent as acquisitions. With this in mind, Hotel Chocolat may

probably achieve its working capital increase while focusing on the beneficial impact on

accounting ratios.

Capability Advancement: If the facility is enlarged to 160,000 square meters, revenues

would increase to $500 million. As a consequence, shareholders' earnings would soar, and

additional territories would start opening. Hotel Chocolat can take use of this chance to expand

its marketplace and improve overall fiscal analyses. As a result, this component would aid in

determining the company's anticipated impact on accounting ratios.

Funding: Investment in technology which assists in the introduction of unique concepts

is an option for businesses. According to the inspectors, new technology or hiring new staff

could have a substantial impact on the company's existing obligations whilst still improving its

business results (Tan, 2016).

Industrial Growth in the Great Britain: To increase manufacturing capability,

corporations must build facilities to accommodate more than 80,000 employees. This would be

ideal for their needs. It enables Hotel Chocolat to extend their company and concentrate on

exterior initiatives, allowing them to assess the value of their assets. It would have a favourable

impact on accounting ratios.

Task 5

The influence of volatility on accounting ratios:

Supplying disruptions: If a firm or organisation is ineffective, it is difficult to provide

things and activities on schedule that has an influence on revenues and, by implication, other

areas of its activities, such as accounts receivable. This component could have both a direct and

indirect effect on accounting ratios.

International vulnerability: Any international vulnerability would have an impact on a

corporation's economic situation and profit generation. It must have been admitted that this

vulnerability had influenced the cash flow in some way. It aids the company's emphasis on

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

worldwide strategic planning, allowing them to quickly achieve their objectives and assure

profitability ratios.

Development into new markets: As a consequence of global growth, the expense of

establishing new sections increases. As a result, the danger of internationalization strategy rises,

which could have a detrimental effect on the company’s, accounting ratios (Velte, 2019).

Positive appearance: Furthermore, the impression that a corporation has a terrible publicity

might have an adverse effect on corporate productivity. There is a clear link among terrible

photos and a drop in income because they induce customers to depart for an extended amount of

time, resulting in a drop in income. It may result in a reduction of marketing strategy, forcing

Hotel Chocolat to deal with societal failings. It may have a detrimental effect on their accounting

ratios.

CONCLUSION

Based on a comprehensive review of the aforesaid information, it was decided that Hotel

Chocolat is having a particularly tough cost as a consequence of the epidemic, because the

corporation's economic records clearly show that 2020 will be a particularly challenging year for

Hotel Chocolat. Positive reputation, as a result of continuous work, has an impact on the product

repertoire, and the company has had to cope with some undesirable elements as a result.

Businesses have a bad fiscal state that can be improved by incorporating different strategies

within the company.

profitability ratios.

Development into new markets: As a consequence of global growth, the expense of

establishing new sections increases. As a result, the danger of internationalization strategy rises,

which could have a detrimental effect on the company’s, accounting ratios (Velte, 2019).

Positive appearance: Furthermore, the impression that a corporation has a terrible publicity

might have an adverse effect on corporate productivity. There is a clear link among terrible

photos and a drop in income because they induce customers to depart for an extended amount of

time, resulting in a drop in income. It may result in a reduction of marketing strategy, forcing

Hotel Chocolat to deal with societal failings. It may have a detrimental effect on their accounting

ratios.

CONCLUSION

Based on a comprehensive review of the aforesaid information, it was decided that Hotel

Chocolat is having a particularly tough cost as a consequence of the epidemic, because the

corporation's economic records clearly show that 2020 will be a particularly challenging year for

Hotel Chocolat. Positive reputation, as a result of continuous work, has an impact on the product

repertoire, and the company has had to cope with some undesirable elements as a result.

Businesses have a bad fiscal state that can be improved by incorporating different strategies

within the company.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and journals

Alsharari, N. M. and Abougamos, H., 2017. The processes of accounting changes as emerging

from public and fiscal reforms. Asian Review of Accounting.

Bühler, A., Wallenburg, C. M. and Wieland, A., 2016. Accounting for external turbulence of

logistics organizations via performance measurement systems. Supply Chain

Management: An International Journal.

Eisenberg, P., 2016. The Balanced Scorecard and Beyond–Applying Theories of Performance

Measurement, Employment and Rewards in Management Accounting Education.

International Research Journal of Management Sciences. 4(7). pp.483-491.

Glushchenko, A. V., Yarkova, I. V. and Kucherova, Y. P., 2017, December. The Role of the

Ecologically-Oriented Accounting Systems from the Perspective of Minimizing the

Strategic Risks in Terms of Ecologizing the Production. In Perspectives on the use of

New Information and Communication Technology (ICT) in the Modern Economy (pp.

741-747). Springer, Cham.

Kuurila, J., 2016. The role of big data in Finnish companies and the implications of big data on

management accounting.

Roberts, H. and Gnan, L., 2017. Welcoming family business into the accounting family: an

introduction to the special issue. Qualitative Research in Accounting & Management.

Tan, B. S., 2016. Accounting research for the management accounting profession. Journal of

Applied Management Accounting Research. 14(1). pp.69-77.

Velte, P., 2019. What do we know about meta-analyses in accounting, auditing, and corporate

governance?. Meditari Accountancy Research.

Books and journals

Alsharari, N. M. and Abougamos, H., 2017. The processes of accounting changes as emerging

from public and fiscal reforms. Asian Review of Accounting.

Bühler, A., Wallenburg, C. M. and Wieland, A., 2016. Accounting for external turbulence of

logistics organizations via performance measurement systems. Supply Chain

Management: An International Journal.

Eisenberg, P., 2016. The Balanced Scorecard and Beyond–Applying Theories of Performance

Measurement, Employment and Rewards in Management Accounting Education.

International Research Journal of Management Sciences. 4(7). pp.483-491.

Glushchenko, A. V., Yarkova, I. V. and Kucherova, Y. P., 2017, December. The Role of the

Ecologically-Oriented Accounting Systems from the Perspective of Minimizing the

Strategic Risks in Terms of Ecologizing the Production. In Perspectives on the use of

New Information and Communication Technology (ICT) in the Modern Economy (pp.

741-747). Springer, Cham.

Kuurila, J., 2016. The role of big data in Finnish companies and the implications of big data on

management accounting.

Roberts, H. and Gnan, L., 2017. Welcoming family business into the accounting family: an

introduction to the special issue. Qualitative Research in Accounting & Management.

Tan, B. S., 2016. Accounting research for the management accounting profession. Journal of

Applied Management Accounting Research. 14(1). pp.69-77.

Velte, P., 2019. What do we know about meta-analyses in accounting, auditing, and corporate

governance?. Meditari Accountancy Research.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.