Hotel Finance and Revenue: A Financial Analysis Report

VerifiedAdded on 2023/06/12

|24

|5308

|409

AI Summary

This report conducts a financial analysis of British Airways, evaluating its profitability, efficiency, liquidity, capital structure, and investor ratios. The report provides insights into the company's financial performance and position.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running Head: Hotel Finance and revenue

1

Project Report: Hotel Finance and revenue

1

Project Report: Hotel Finance and revenue

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Hotel Finance and revenue

2

Contents

Introduction.......................................................................................................................3

Company overview...........................................................................................................3

Findings............................................................................................................................3

Profitability ratios.........................................................................................................4

Efficiency ratios............................................................................................................5

Liquidity ratios..............................................................................................................7

Capital structure ratios..................................................................................................9

Investor’s ratios..........................................................................................................10

Discussion.......................................................................................................................11

Conclusion and recommendation...................................................................................12

References.......................................................................................................................14

Appendix.........................................................................................................................16

2

Contents

Introduction.......................................................................................................................3

Company overview...........................................................................................................3

Findings............................................................................................................................3

Profitability ratios.........................................................................................................4

Efficiency ratios............................................................................................................5

Liquidity ratios..............................................................................................................7

Capital structure ratios..................................................................................................9

Investor’s ratios..........................................................................................................10

Discussion.......................................................................................................................11

Conclusion and recommendation...................................................................................12

References.......................................................................................................................14

Appendix.........................................................................................................................16

Hotel Finance and revenue

3

Introduction:

Financial evaluation and analysis is a process which is used by the companies and the

investors and financial analyse of the company to analyze the performance of the company in

context with the finance. This process evaluates the budgets, projects, financial related

entities etc of an organization to identify the suitability and the performance of the company.

Normally, financial analysis process is used by the related parties to identify that whether the

organization is stable, liquid, solvent and profitable enough to manage the performance and

the position in the industry. Financial analyst and the financial manager of a company

evaluate the financial statement and the financial transaction of a company to generate the

idea about the performance of the company.

There are various tools to evaluate the financial performance of the company. All the

tools are used by the companies to generate a basic idea about the different business

transactions and the decisions of the company. In the report, British airways has been taken

into the concern and the ratio analysis study has been conducted on the company to generate

an idea about the stable, liquid, solvent and profitable position of the company.

Company overview:

“British airways” is the largest airline on the basis of fleet size in United Kingdom.

The company has been founded in 1974. The head office of the company has based in

Waterside at London Heathrow Airport. The company has been merged with a company,

Iberia to diversify the market. The British airways are offering its services at many

destinations in Australia as well as at international level. Currently, company is serving into

183 destinations. Company is registered in London stock exchange by the name of Boeing

Company (Home, 2018). The financial evaluation explains that the last few decades was not

that much good for the company. Various up and down has been faced by the company in last

few decades.

Findings:

The financial statement of the company has been evaluated to identify the

performance of the company. The ratio analysis study has been conducted on the company to

generate an idea about the stable, liquid, solvent and profitable position of the company as

well as the changes into the financial statement of the company has also been evaluated on

3

Introduction:

Financial evaluation and analysis is a process which is used by the companies and the

investors and financial analyse of the company to analyze the performance of the company in

context with the finance. This process evaluates the budgets, projects, financial related

entities etc of an organization to identify the suitability and the performance of the company.

Normally, financial analysis process is used by the related parties to identify that whether the

organization is stable, liquid, solvent and profitable enough to manage the performance and

the position in the industry. Financial analyst and the financial manager of a company

evaluate the financial statement and the financial transaction of a company to generate the

idea about the performance of the company.

There are various tools to evaluate the financial performance of the company. All the

tools are used by the companies to generate a basic idea about the different business

transactions and the decisions of the company. In the report, British airways has been taken

into the concern and the ratio analysis study has been conducted on the company to generate

an idea about the stable, liquid, solvent and profitable position of the company.

Company overview:

“British airways” is the largest airline on the basis of fleet size in United Kingdom.

The company has been founded in 1974. The head office of the company has based in

Waterside at London Heathrow Airport. The company has been merged with a company,

Iberia to diversify the market. The British airways are offering its services at many

destinations in Australia as well as at international level. Currently, company is serving into

183 destinations. Company is registered in London stock exchange by the name of Boeing

Company (Home, 2018). The financial evaluation explains that the last few decades was not

that much good for the company. Various up and down has been faced by the company in last

few decades.

Findings:

The financial statement of the company has been evaluated to identify the

performance of the company. The ratio analysis study has been conducted on the company to

generate an idea about the stable, liquid, solvent and profitable position of the company as

well as the changes into the financial statement of the company has also been evaluated on

Hotel Finance and revenue

4

the basis of year 2013 to analyze that how much changes have occurred into the financial

performance of the company in last five years.

Ratio analysis is a quantitative analysis which evaluates information that is combined

in the financial statement of a company. Ratio analysis study is used by the companies to

evaluate the various financial aspect of an organization. It explains about the stable, liquid,

solvent and profitable position of the company. The ratio analysis study of the company is as

follows:

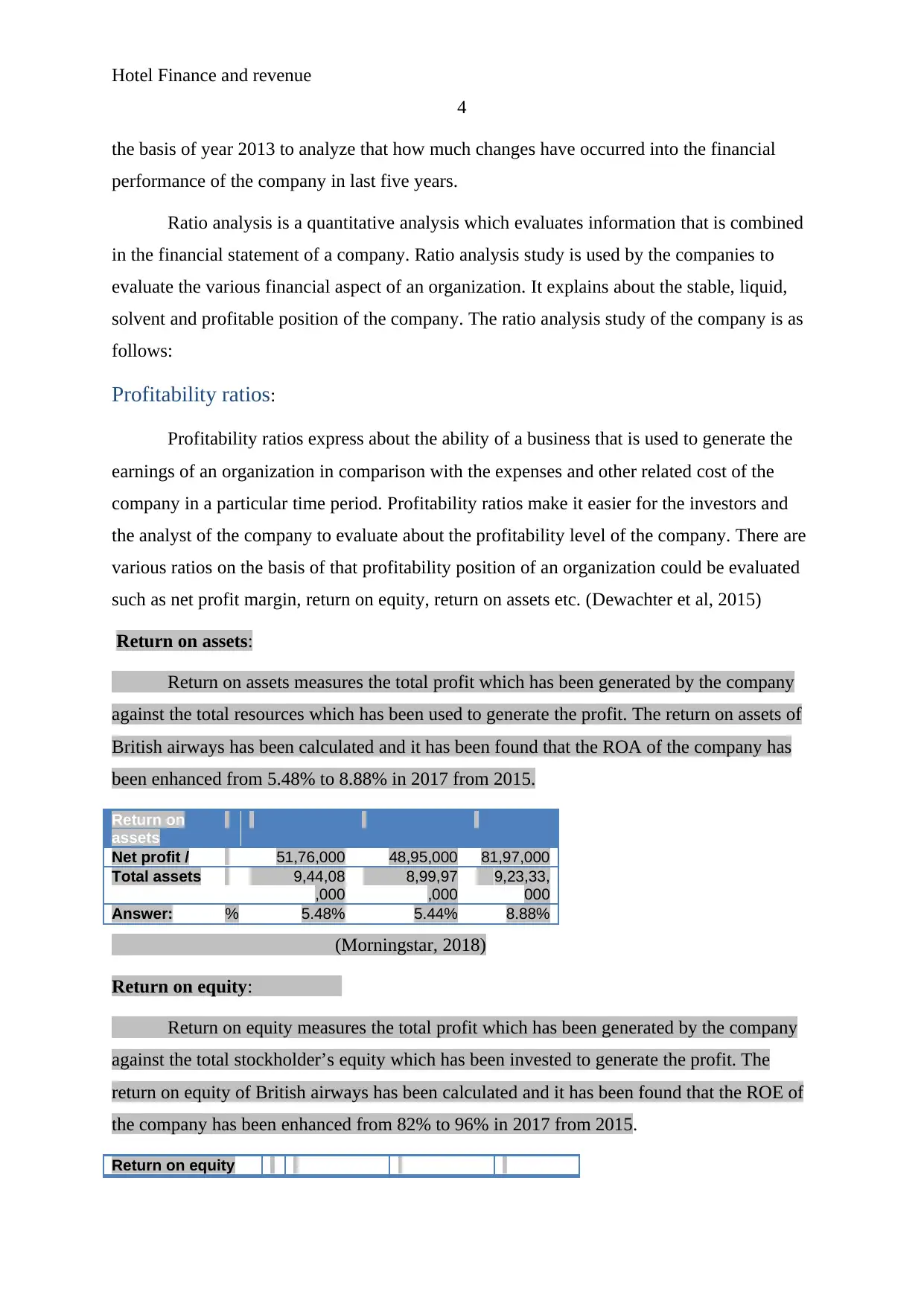

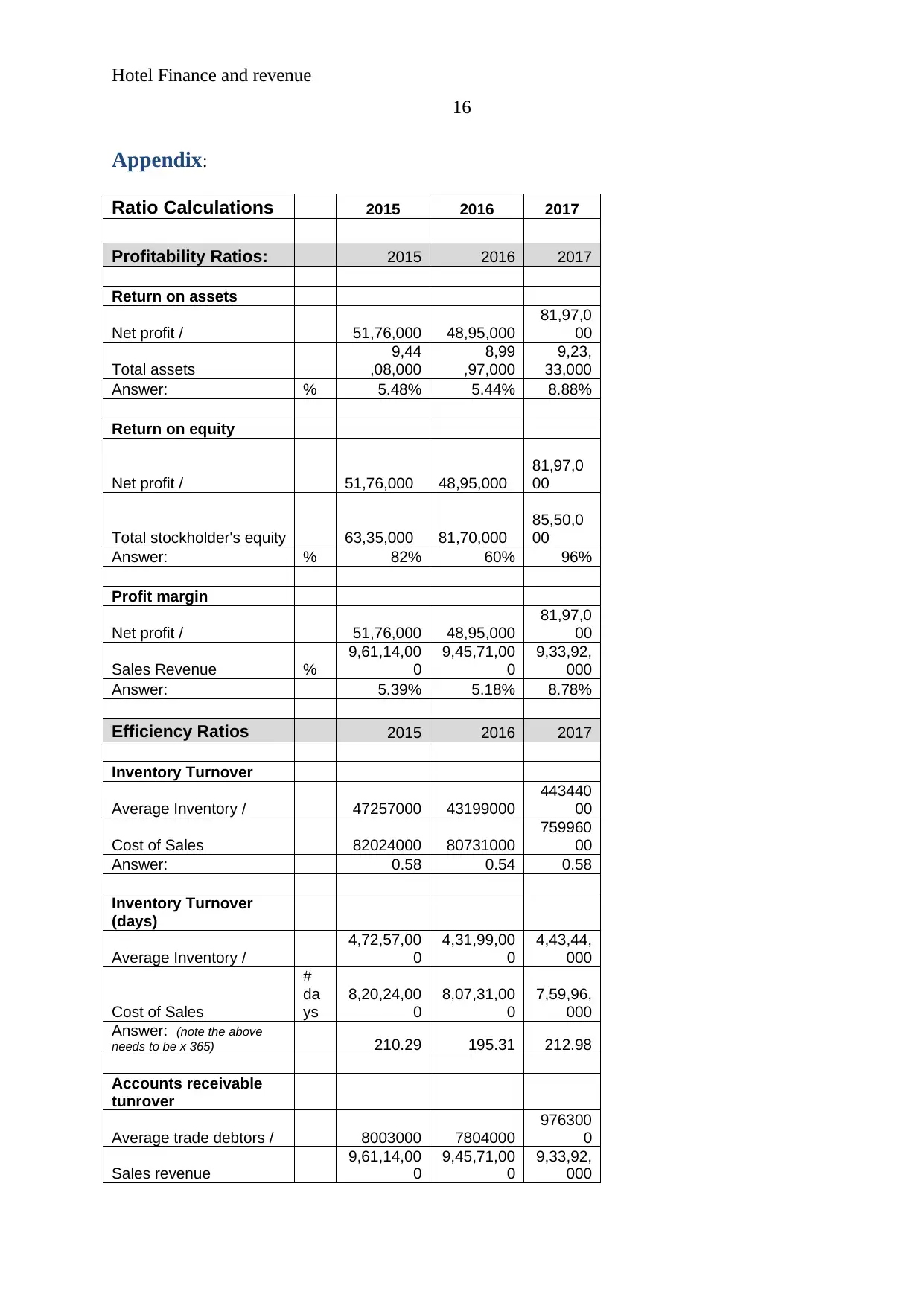

Profitability ratios:

Profitability ratios express about the ability of a business that is used to generate the

earnings of an organization in comparison with the expenses and other related cost of the

company in a particular time period. Profitability ratios make it easier for the investors and

the analyst of the company to evaluate about the profitability level of the company. There are

various ratios on the basis of that profitability position of an organization could be evaluated

such as net profit margin, return on equity, return on assets etc. (Dewachter et al, 2015)

Return on assets:

Return on assets measures the total profit which has been generated by the company

against the total resources which has been used to generate the profit. The return on assets of

British airways has been calculated and it has been found that the ROA of the company has

been enhanced from 5.48% to 8.88% in 2017 from 2015.

Return on

assets

Net profit / 51,76,000 48,95,000 81,97,000

Total assets 9,44,08

,000

8,99,97

,000

9,23,33,

000

Answer: % 5.48% 5.44% 8.88%

(Morningstar, 2018)

Return on equity:

Return on equity measures the total profit which has been generated by the company

against the total stockholder’s equity which has been invested to generate the profit. The

return on equity of British airways has been calculated and it has been found that the ROE of

the company has been enhanced from 82% to 96% in 2017 from 2015.

Return on equity

4

the basis of year 2013 to analyze that how much changes have occurred into the financial

performance of the company in last five years.

Ratio analysis is a quantitative analysis which evaluates information that is combined

in the financial statement of a company. Ratio analysis study is used by the companies to

evaluate the various financial aspect of an organization. It explains about the stable, liquid,

solvent and profitable position of the company. The ratio analysis study of the company is as

follows:

Profitability ratios:

Profitability ratios express about the ability of a business that is used to generate the

earnings of an organization in comparison with the expenses and other related cost of the

company in a particular time period. Profitability ratios make it easier for the investors and

the analyst of the company to evaluate about the profitability level of the company. There are

various ratios on the basis of that profitability position of an organization could be evaluated

such as net profit margin, return on equity, return on assets etc. (Dewachter et al, 2015)

Return on assets:

Return on assets measures the total profit which has been generated by the company

against the total resources which has been used to generate the profit. The return on assets of

British airways has been calculated and it has been found that the ROA of the company has

been enhanced from 5.48% to 8.88% in 2017 from 2015.

Return on

assets

Net profit / 51,76,000 48,95,000 81,97,000

Total assets 9,44,08

,000

8,99,97

,000

9,23,33,

000

Answer: % 5.48% 5.44% 8.88%

(Morningstar, 2018)

Return on equity:

Return on equity measures the total profit which has been generated by the company

against the total stockholder’s equity which has been invested to generate the profit. The

return on equity of British airways has been calculated and it has been found that the ROE of

the company has been enhanced from 82% to 96% in 2017 from 2015.

Return on equity

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Hotel Finance and revenue

5

Net profit /

51,76,000 48,95,000 81,97,00

0

Total stockholder's

equity 63,35,000 81,70,000 85,50,00

0

Answer: % 82% 60% 96%

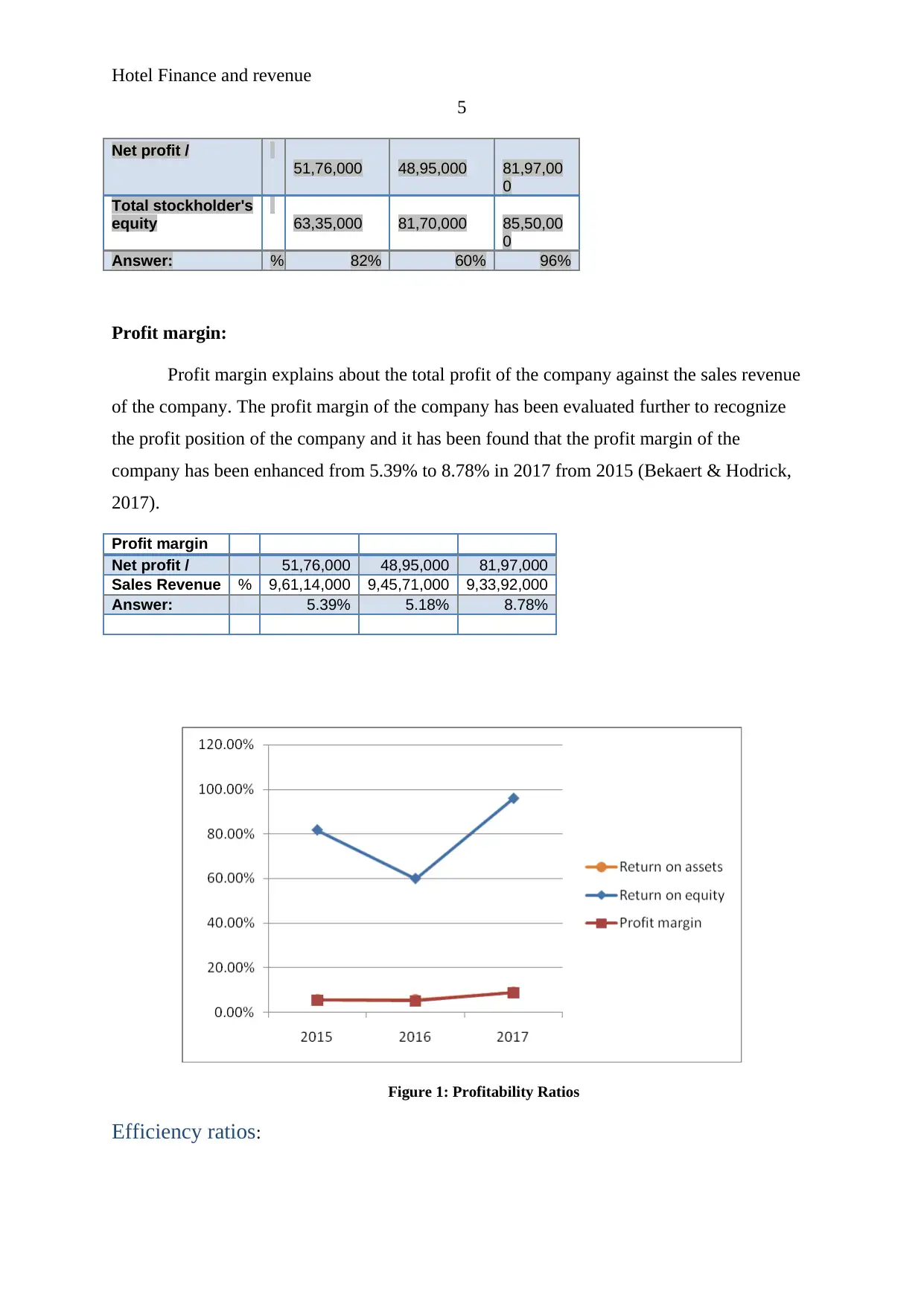

Profit margin:

Profit margin explains about the total profit of the company against the sales revenue

of the company. The profit margin of the company has been evaluated further to recognize

the profit position of the company and it has been found that the profit margin of the

company has been enhanced from 5.39% to 8.78% in 2017 from 2015 (Bekaert & Hodrick,

2017).

Profit margin

Net profit / 51,76,000 48,95,000 81,97,000

Sales Revenue % 9,61,14,000 9,45,71,000 9,33,92,000

Answer: 5.39% 5.18% 8.78%

Figure 1: Profitability Ratios

Efficiency ratios:

5

Net profit /

51,76,000 48,95,000 81,97,00

0

Total stockholder's

equity 63,35,000 81,70,000 85,50,00

0

Answer: % 82% 60% 96%

Profit margin:

Profit margin explains about the total profit of the company against the sales revenue

of the company. The profit margin of the company has been evaluated further to recognize

the profit position of the company and it has been found that the profit margin of the

company has been enhanced from 5.39% to 8.78% in 2017 from 2015 (Bekaert & Hodrick,

2017).

Profit margin

Net profit / 51,76,000 48,95,000 81,97,000

Sales Revenue % 9,61,14,000 9,45,71,000 9,33,92,000

Answer: 5.39% 5.18% 8.78%

Figure 1: Profitability Ratios

Efficiency ratios:

Hotel Finance and revenue

6

Asset efficiency ratios express about the combination of assets and liabilities of the

company and evaluates about the performance of the company. Efficiency ratios are used by

the companies and the financial analyst to evaluate the commercial performance of the

company. It measure the total time period in which the cash conversion cycle of an

organization competes. There are various ratios on the basis of that efficiency position of an

organization could be evaluated such as receivable turnover ratio, inventory turnover ratio,

payable turnover ratio etc.

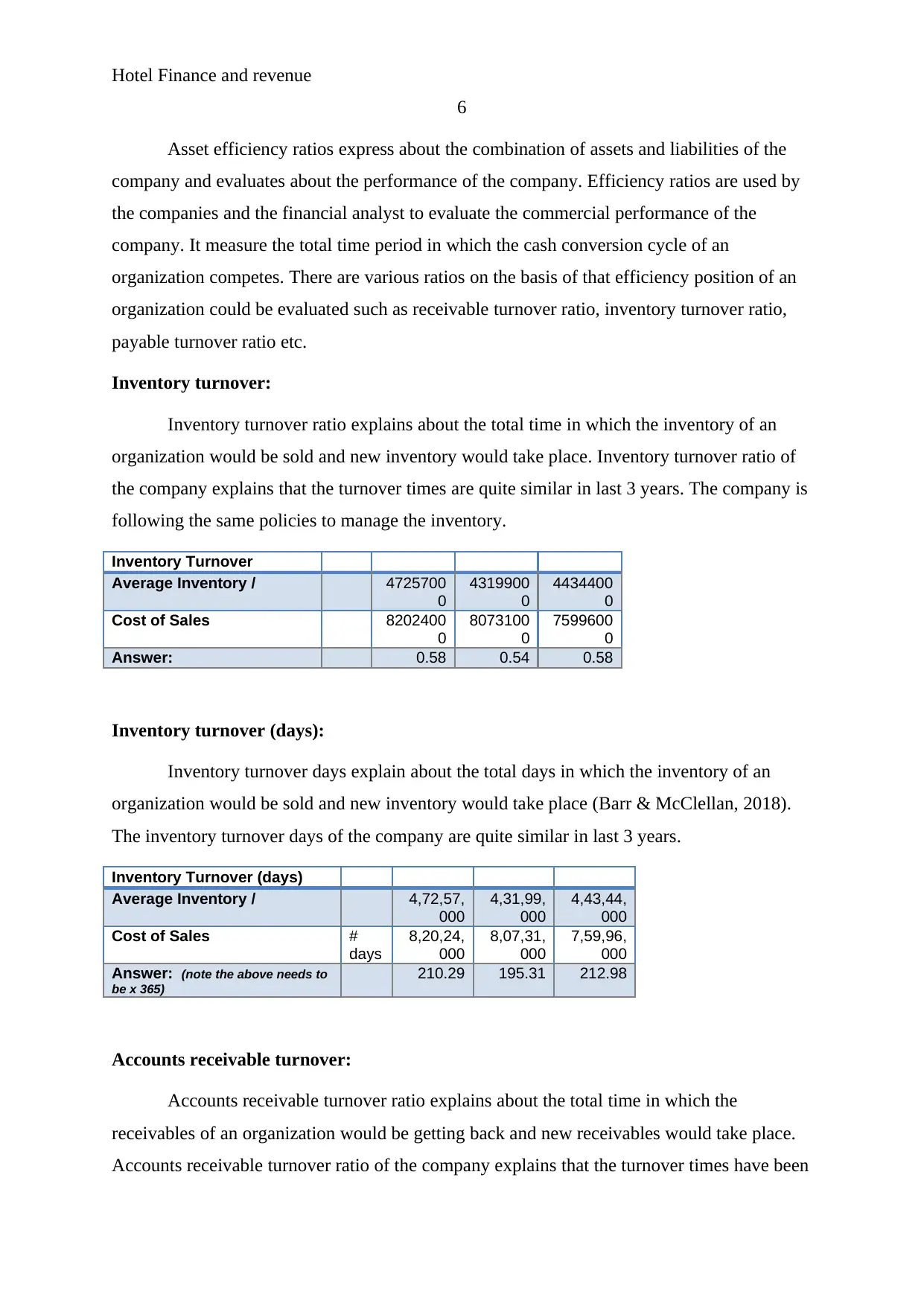

Inventory turnover:

Inventory turnover ratio explains about the total time in which the inventory of an

organization would be sold and new inventory would take place. Inventory turnover ratio of

the company explains that the turnover times are quite similar in last 3 years. The company is

following the same policies to manage the inventory.

Inventory Turnover

Average Inventory / 4725700

0

4319900

0

4434400

0

Cost of Sales 8202400

0

8073100

0

7599600

0

Answer: 0.58 0.54 0.58

Inventory turnover (days):

Inventory turnover days explain about the total days in which the inventory of an

organization would be sold and new inventory would take place (Barr & McClellan, 2018).

The inventory turnover days of the company are quite similar in last 3 years.

Inventory Turnover (days)

Average Inventory / 4,72,57,

000

4,31,99,

000

4,43,44,

000

Cost of Sales #

days

8,20,24,

000

8,07,31,

000

7,59,96,

000

Answer: (note the above needs to

be x 365)

210.29 195.31 212.98

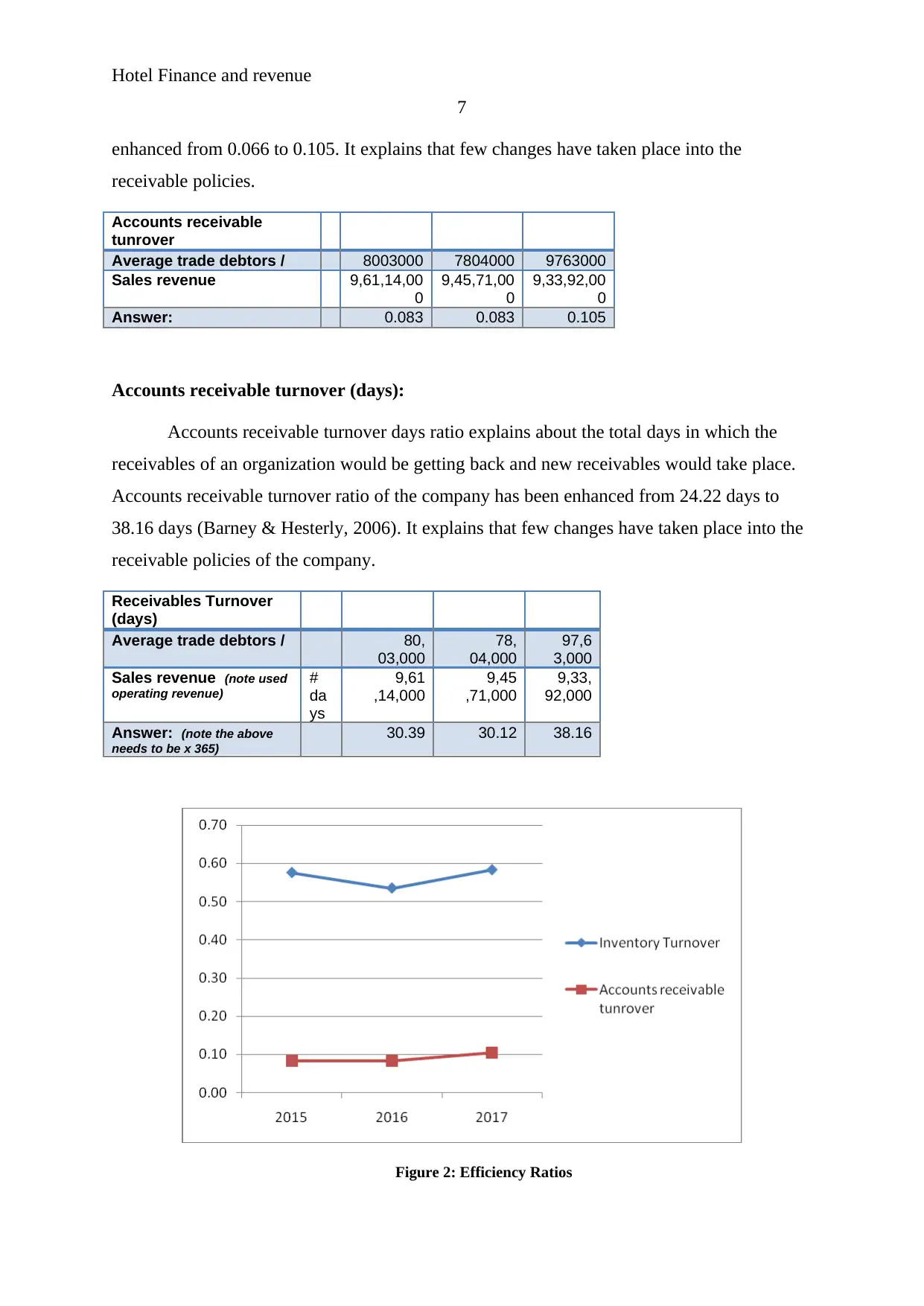

Accounts receivable turnover:

Accounts receivable turnover ratio explains about the total time in which the

receivables of an organization would be getting back and new receivables would take place.

Accounts receivable turnover ratio of the company explains that the turnover times have been

6

Asset efficiency ratios express about the combination of assets and liabilities of the

company and evaluates about the performance of the company. Efficiency ratios are used by

the companies and the financial analyst to evaluate the commercial performance of the

company. It measure the total time period in which the cash conversion cycle of an

organization competes. There are various ratios on the basis of that efficiency position of an

organization could be evaluated such as receivable turnover ratio, inventory turnover ratio,

payable turnover ratio etc.

Inventory turnover:

Inventory turnover ratio explains about the total time in which the inventory of an

organization would be sold and new inventory would take place. Inventory turnover ratio of

the company explains that the turnover times are quite similar in last 3 years. The company is

following the same policies to manage the inventory.

Inventory Turnover

Average Inventory / 4725700

0

4319900

0

4434400

0

Cost of Sales 8202400

0

8073100

0

7599600

0

Answer: 0.58 0.54 0.58

Inventory turnover (days):

Inventory turnover days explain about the total days in which the inventory of an

organization would be sold and new inventory would take place (Barr & McClellan, 2018).

The inventory turnover days of the company are quite similar in last 3 years.

Inventory Turnover (days)

Average Inventory / 4,72,57,

000

4,31,99,

000

4,43,44,

000

Cost of Sales #

days

8,20,24,

000

8,07,31,

000

7,59,96,

000

Answer: (note the above needs to

be x 365)

210.29 195.31 212.98

Accounts receivable turnover:

Accounts receivable turnover ratio explains about the total time in which the

receivables of an organization would be getting back and new receivables would take place.

Accounts receivable turnover ratio of the company explains that the turnover times have been

Hotel Finance and revenue

7

enhanced from 0.066 to 0.105. It explains that few changes have taken place into the

receivable policies.

Accounts receivable

tunrover

Average trade debtors / 8003000 7804000 9763000

Sales revenue 9,61,14,00

0

9,45,71,00

0

9,33,92,00

0

Answer: 0.083 0.083 0.105

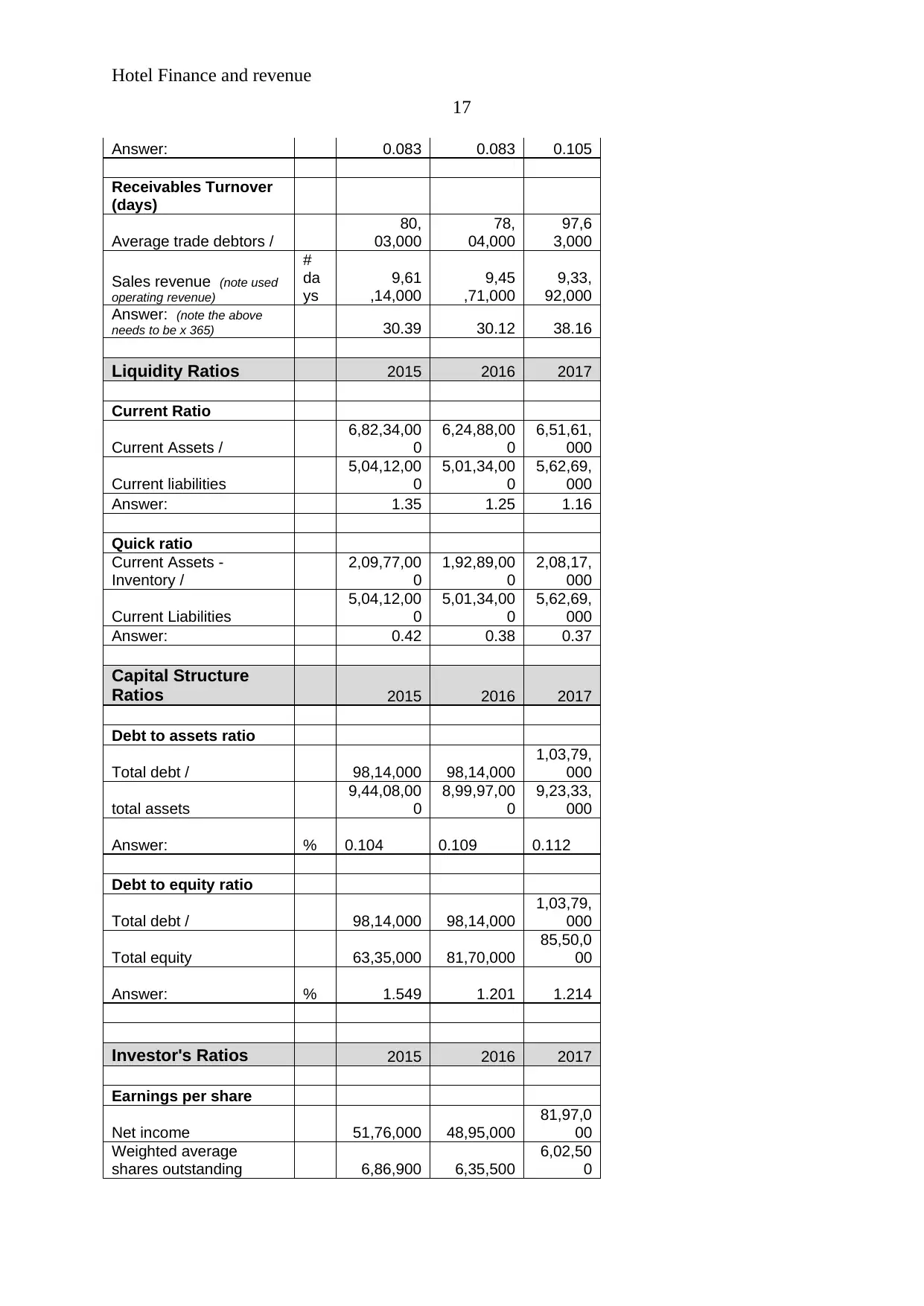

Accounts receivable turnover (days):

Accounts receivable turnover days ratio explains about the total days in which the

receivables of an organization would be getting back and new receivables would take place.

Accounts receivable turnover ratio of the company has been enhanced from 24.22 days to

38.16 days (Barney & Hesterly, 2006). It explains that few changes have taken place into the

receivable policies of the company.

Receivables Turnover

(days)

Average trade debtors / 80,

03,000

78,

04,000

97,6

3,000

Sales revenue (note used

operating revenue)

#

da

ys

9,61

,14,000

9,45

,71,000

9,33,

92,000

Answer: (note the above

needs to be x 365)

30.39 30.12 38.16

Figure 2: Efficiency Ratios

7

enhanced from 0.066 to 0.105. It explains that few changes have taken place into the

receivable policies.

Accounts receivable

tunrover

Average trade debtors / 8003000 7804000 9763000

Sales revenue 9,61,14,00

0

9,45,71,00

0

9,33,92,00

0

Answer: 0.083 0.083 0.105

Accounts receivable turnover (days):

Accounts receivable turnover days ratio explains about the total days in which the

receivables of an organization would be getting back and new receivables would take place.

Accounts receivable turnover ratio of the company has been enhanced from 24.22 days to

38.16 days (Barney & Hesterly, 2006). It explains that few changes have taken place into the

receivable policies of the company.

Receivables Turnover

(days)

Average trade debtors / 80,

03,000

78,

04,000

97,6

3,000

Sales revenue (note used

operating revenue)

#

da

ys

9,61

,14,000

9,45

,71,000

9,33,

92,000

Answer: (note the above

needs to be x 365)

30.39 30.12 38.16

Figure 2: Efficiency Ratios

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Hotel Finance and revenue

8

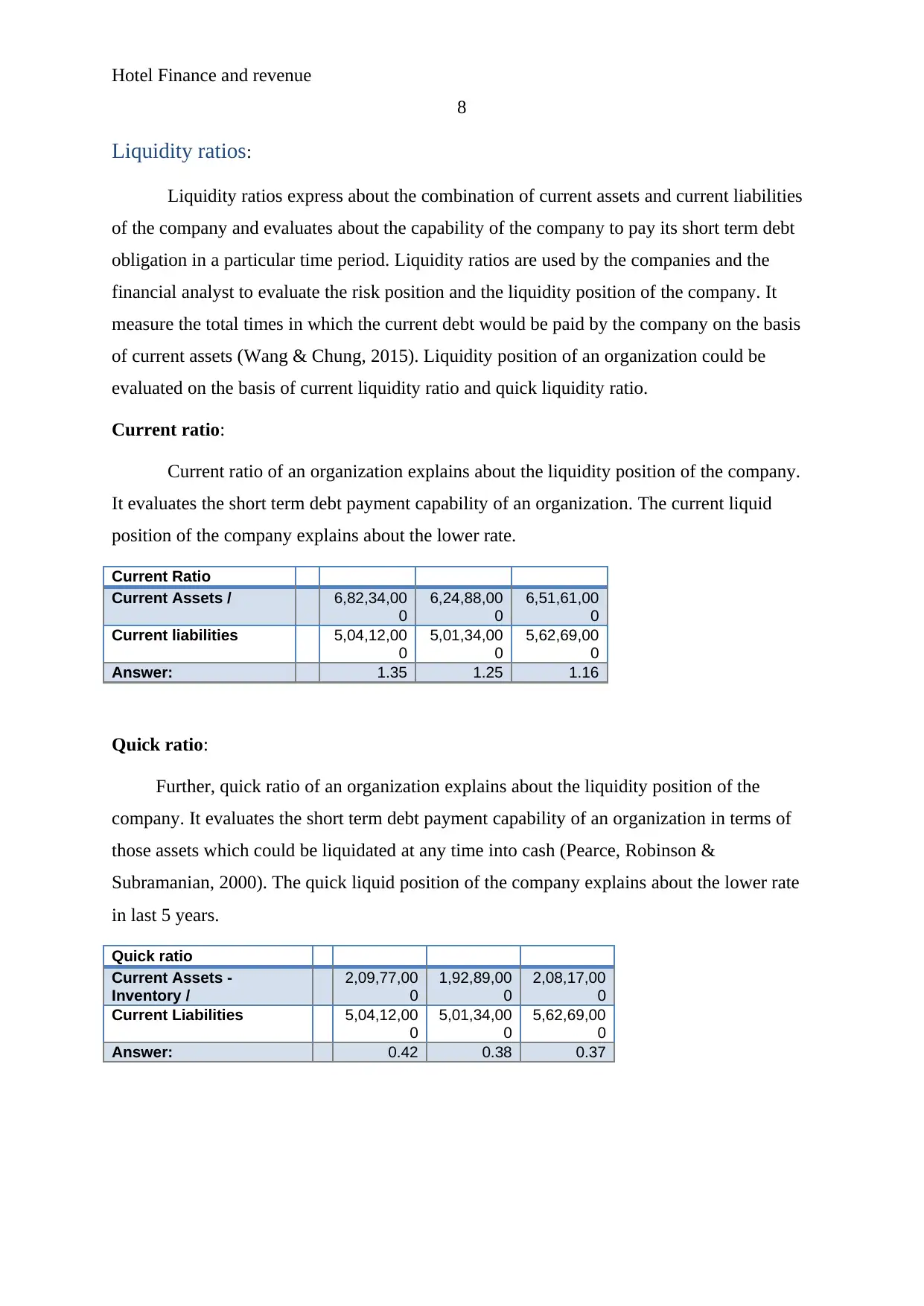

Liquidity ratios:

Liquidity ratios express about the combination of current assets and current liabilities

of the company and evaluates about the capability of the company to pay its short term debt

obligation in a particular time period. Liquidity ratios are used by the companies and the

financial analyst to evaluate the risk position and the liquidity position of the company. It

measure the total times in which the current debt would be paid by the company on the basis

of current assets (Wang & Chung, 2015). Liquidity position of an organization could be

evaluated on the basis of current liquidity ratio and quick liquidity ratio.

Current ratio:

Current ratio of an organization explains about the liquidity position of the company.

It evaluates the short term debt payment capability of an organization. The current liquid

position of the company explains about the lower rate.

Current Ratio

Current Assets / 6,82,34,00

0

6,24,88,00

0

6,51,61,00

0

Current liabilities 5,04,12,00

0

5,01,34,00

0

5,62,69,00

0

Answer: 1.35 1.25 1.16

Quick ratio:

Further, quick ratio of an organization explains about the liquidity position of the

company. It evaluates the short term debt payment capability of an organization in terms of

those assets which could be liquidated at any time into cash (Pearce, Robinson &

Subramanian, 2000). The quick liquid position of the company explains about the lower rate

in last 5 years.

Quick ratio

Current Assets -

Inventory /

2,09,77,00

0

1,92,89,00

0

2,08,17,00

0

Current Liabilities 5,04,12,00

0

5,01,34,00

0

5,62,69,00

0

Answer: 0.42 0.38 0.37

8

Liquidity ratios:

Liquidity ratios express about the combination of current assets and current liabilities

of the company and evaluates about the capability of the company to pay its short term debt

obligation in a particular time period. Liquidity ratios are used by the companies and the

financial analyst to evaluate the risk position and the liquidity position of the company. It

measure the total times in which the current debt would be paid by the company on the basis

of current assets (Wang & Chung, 2015). Liquidity position of an organization could be

evaluated on the basis of current liquidity ratio and quick liquidity ratio.

Current ratio:

Current ratio of an organization explains about the liquidity position of the company.

It evaluates the short term debt payment capability of an organization. The current liquid

position of the company explains about the lower rate.

Current Ratio

Current Assets / 6,82,34,00

0

6,24,88,00

0

6,51,61,00

0

Current liabilities 5,04,12,00

0

5,01,34,00

0

5,62,69,00

0

Answer: 1.35 1.25 1.16

Quick ratio:

Further, quick ratio of an organization explains about the liquidity position of the

company. It evaluates the short term debt payment capability of an organization in terms of

those assets which could be liquidated at any time into cash (Pearce, Robinson &

Subramanian, 2000). The quick liquid position of the company explains about the lower rate

in last 5 years.

Quick ratio

Current Assets -

Inventory /

2,09,77,00

0

1,92,89,00

0

2,08,17,00

0

Current Liabilities 5,04,12,00

0

5,01,34,00

0

5,62,69,00

0

Answer: 0.42 0.38 0.37

Hotel Finance and revenue

9

Figure 3: Liquidity ratio

Capital structure ratios:

Capital structure ratios evaluate the debt level, asset kevel and equity level of an

organization. It measures the overall operations and the growth of the company by using the

different sources through which the company has raised the funds. Capital structure position

of an organization could be evaluated on the basis of debt, assets and equity level of the

company (Lau, 2016). Capital structure ratios of the company are as follows:

Debt to asset ratio:

Debt to asset ratio explains about the level of debts of an organization in terms of

assets of the company. It measures the level of both the sources to identify the risk and return

position of the company. Debt to assets ratio of the British airways is 0.112 in current year

which has been enhanced from 0.104 in 2015.

Debt to assets

ratio

Total debt / 98,14,000 98,14,000 1,03,79,0

00

total assets 9,44,08,000 8,99,97,000 9,23,33,0

00

Answer: %

0.104 0.109 0.112

(Titman, Keown & Martin, 2017)

Debt to equity ratio:

9

Figure 3: Liquidity ratio

Capital structure ratios:

Capital structure ratios evaluate the debt level, asset kevel and equity level of an

organization. It measures the overall operations and the growth of the company by using the

different sources through which the company has raised the funds. Capital structure position

of an organization could be evaluated on the basis of debt, assets and equity level of the

company (Lau, 2016). Capital structure ratios of the company are as follows:

Debt to asset ratio:

Debt to asset ratio explains about the level of debts of an organization in terms of

assets of the company. It measures the level of both the sources to identify the risk and return

position of the company. Debt to assets ratio of the British airways is 0.112 in current year

which has been enhanced from 0.104 in 2015.

Debt to assets

ratio

Total debt / 98,14,000 98,14,000 1,03,79,0

00

total assets 9,44,08,000 8,99,97,000 9,23,33,0

00

Answer: %

0.104 0.109 0.112

(Titman, Keown & Martin, 2017)

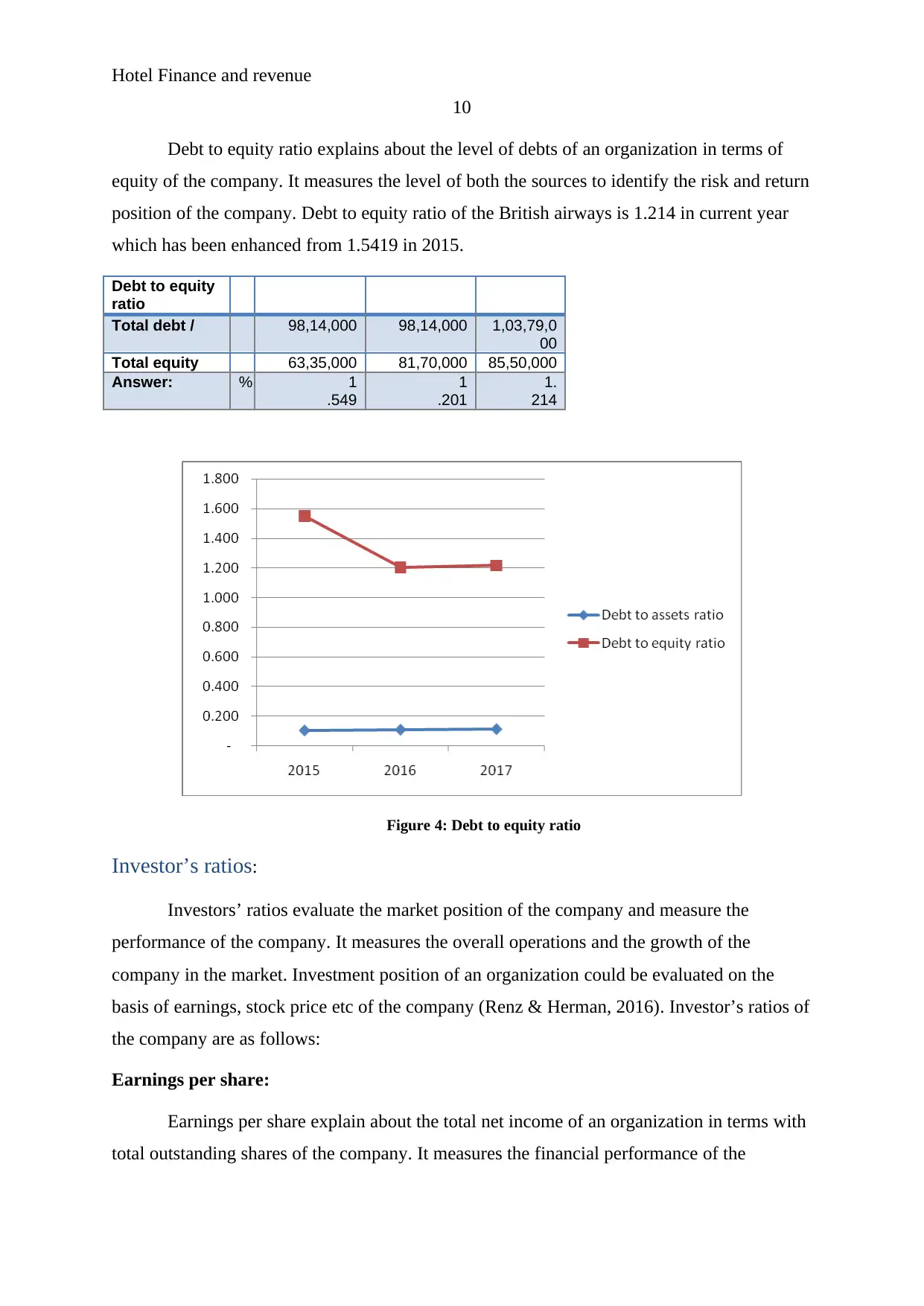

Debt to equity ratio:

Hotel Finance and revenue

10

Debt to equity ratio explains about the level of debts of an organization in terms of

equity of the company. It measures the level of both the sources to identify the risk and return

position of the company. Debt to equity ratio of the British airways is 1.214 in current year

which has been enhanced from 1.5419 in 2015.

Debt to equity

ratio

Total debt / 98,14,000 98,14,000 1,03,79,0

00

Total equity 63,35,000 81,70,000 85,50,000

Answer: % 1

.549

1

.201

1.

214

Figure 4: Debt to equity ratio

Investor’s ratios:

Investors’ ratios evaluate the market position of the company and measure the

performance of the company. It measures the overall operations and the growth of the

company in the market. Investment position of an organization could be evaluated on the

basis of earnings, stock price etc of the company (Renz & Herman, 2016). Investor’s ratios of

the company are as follows:

Earnings per share:

Earnings per share explain about the total net income of an organization in terms with

total outstanding shares of the company. It measures the financial performance of the

10

Debt to equity ratio explains about the level of debts of an organization in terms of

equity of the company. It measures the level of both the sources to identify the risk and return

position of the company. Debt to equity ratio of the British airways is 1.214 in current year

which has been enhanced from 1.5419 in 2015.

Debt to equity

ratio

Total debt / 98,14,000 98,14,000 1,03,79,0

00

Total equity 63,35,000 81,70,000 85,50,000

Answer: % 1

.549

1

.201

1.

214

Figure 4: Debt to equity ratio

Investor’s ratios:

Investors’ ratios evaluate the market position of the company and measure the

performance of the company. It measures the overall operations and the growth of the

company in the market. Investment position of an organization could be evaluated on the

basis of earnings, stock price etc of the company (Renz & Herman, 2016). Investor’s ratios of

the company are as follows:

Earnings per share:

Earnings per share explain about the total net income of an organization in terms with

total outstanding shares of the company. It measures the financial performance of the

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Hotel Finance and revenue

11

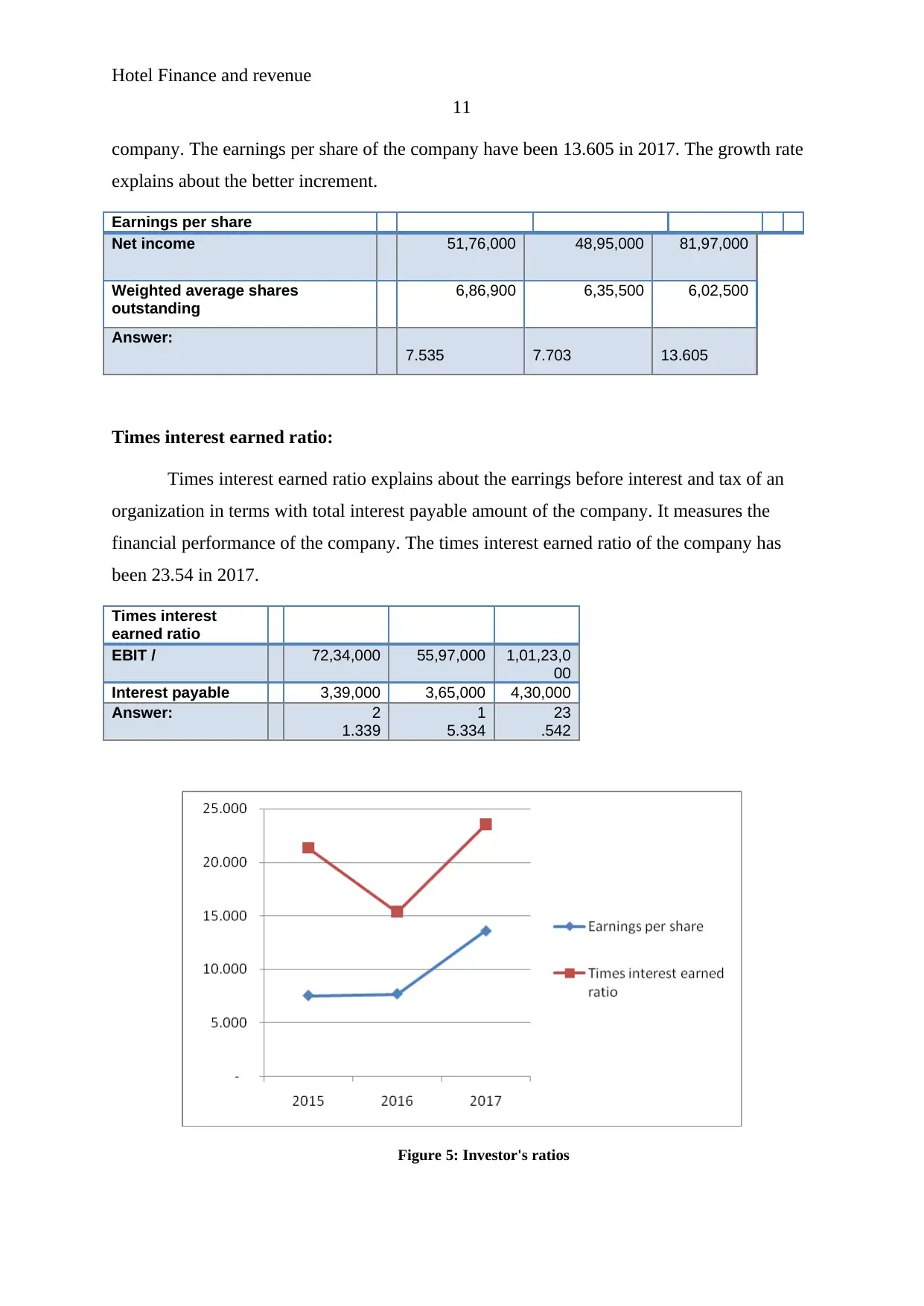

company. The earnings per share of the company have been 13.605 in 2017. The growth rate

explains about the better increment.

Earnings per share

Net income 51,76,000 48,95,000 81,97,000

Weighted average shares

outstanding

6,86,900 6,35,500 6,02,500

Answer:

7.535 7.703 13.605

Times interest earned ratio:

Times interest earned ratio explains about the earrings before interest and tax of an

organization in terms with total interest payable amount of the company. It measures the

financial performance of the company. The times interest earned ratio of the company has

been 23.54 in 2017.

Times interest

earned ratio

EBIT / 72,34,000 55,97,000 1,01,23,0

00

Interest payable 3,39,000 3,65,000 4,30,000

Answer: 2

1.339

1

5.334

23

.542

Figure 5: Investor's ratios

11

company. The earnings per share of the company have been 13.605 in 2017. The growth rate

explains about the better increment.

Earnings per share

Net income 51,76,000 48,95,000 81,97,000

Weighted average shares

outstanding

6,86,900 6,35,500 6,02,500

Answer:

7.535 7.703 13.605

Times interest earned ratio:

Times interest earned ratio explains about the earrings before interest and tax of an

organization in terms with total interest payable amount of the company. It measures the

financial performance of the company. The times interest earned ratio of the company has

been 23.54 in 2017.

Times interest

earned ratio

EBIT / 72,34,000 55,97,000 1,01,23,0

00

Interest payable 3,39,000 3,65,000 4,30,000

Answer: 2

1.339

1

5.334

23

.542

Figure 5: Investor's ratios

Hotel Finance and revenue

12

Discussion:

On the basis of the above calculation and evaluation, it has been found that various

changes have occurred into the financial performance and position of the company in last 5

years. The profitability level of the company has been studied firstly and it has been found

that the enough profits are generated by the company. The level of the profits has also been

enhanced from last years in the current financial year of the company. Though, it has been

found that the company should focus on the operating expenses of the company which is

quite higher (Finkler et al, 2016). These changes would help the company to earn more. The

return on equity and return on asset ratio of the comapny explains that the equity level of the

company is quite lower and thus the return on equity of the company is quite higher than the

return on assets of the company.

Further, the efficiency ratios of the company have been evaluated which explains

about the efficient operations and position of the company. On the basis of calculations, it has

been found that the inventory turnover ratio of the company is quite higher which explains

about more working capital involvement of the company. So, the company should make few

changes into inventory policies so that the working capital involvement could be lower and

capital requirement could also be lower (Bekaert & Hodrick, 2017). In addition, the accounts

receivable turnover days of the company are quite competitive and it explains about

competitive position of the company.

In addition, the liquidity ratios of the company have been evaluated which explains

about the liquid position of the company. On the basis of calculations, it has been found that

the current liquidity ratio and quick ratios of the company has been lower form 2015 in 2017.

These changes are quite competitive and explain about the better position of the company.

Currently, the debt payment capability of the company is quite better in terms of industry.

Capital structure ratios have been discussed further. The capitals structure ratio of the

company has been evaluated which explains about the risk and return of the company. On the

basis of calculations, it has been found that the debt to equity level of the company is quite

higher which explains that the level of debt is more than equity level. These changes are quite

risky for the company. Though, the debt to asset level of the company is quite better and

explains about the competitive position (Vogel, 2014).

12

Discussion:

On the basis of the above calculation and evaluation, it has been found that various

changes have occurred into the financial performance and position of the company in last 5

years. The profitability level of the company has been studied firstly and it has been found

that the enough profits are generated by the company. The level of the profits has also been

enhanced from last years in the current financial year of the company. Though, it has been

found that the company should focus on the operating expenses of the company which is

quite higher (Finkler et al, 2016). These changes would help the company to earn more. The

return on equity and return on asset ratio of the comapny explains that the equity level of the

company is quite lower and thus the return on equity of the company is quite higher than the

return on assets of the company.

Further, the efficiency ratios of the company have been evaluated which explains

about the efficient operations and position of the company. On the basis of calculations, it has

been found that the inventory turnover ratio of the company is quite higher which explains

about more working capital involvement of the company. So, the company should make few

changes into inventory policies so that the working capital involvement could be lower and

capital requirement could also be lower (Bekaert & Hodrick, 2017). In addition, the accounts

receivable turnover days of the company are quite competitive and it explains about

competitive position of the company.

In addition, the liquidity ratios of the company have been evaluated which explains

about the liquid position of the company. On the basis of calculations, it has been found that

the current liquidity ratio and quick ratios of the company has been lower form 2015 in 2017.

These changes are quite competitive and explain about the better position of the company.

Currently, the debt payment capability of the company is quite better in terms of industry.

Capital structure ratios have been discussed further. The capitals structure ratio of the

company has been evaluated which explains about the risk and return of the company. On the

basis of calculations, it has been found that the debt to equity level of the company is quite

higher which explains that the level of debt is more than equity level. These changes are quite

risky for the company. Though, the debt to asset level of the company is quite better and

explains about the competitive position (Vogel, 2014).

Hotel Finance and revenue

13

Lastly, the investor ratios have been discussed further. The investor ratio of the

company has been evaluated which explains about market position of the company. On the

basis of calculations, it has been found that the market position of the company is quite better

which explains that the investment opportunity of the company is quite attractive. The

company is offering good returns to its stockholders.

Conclusion and recommendation:

On the basis of the above findings and discussion, it has been found that the few

changes rare required to be done in the organization for the better performance of the

company. The company should maintain the performance and the position according to the

industry. Company is required t make the changes into its quite level. The equity level should

be improved by the company for the better position of the company. On the other hand,

inventory management policies are also required to be change to manage the working capital

of the company.

To conclude, the current financial performance of the company is quite competitive,

various positive changes have taken place into the performance of the company in last 5 years

which has made the position of the company more attractive. The investors are recommended

to make investment into the company for the great returns.

13

Lastly, the investor ratios have been discussed further. The investor ratio of the

company has been evaluated which explains about market position of the company. On the

basis of calculations, it has been found that the market position of the company is quite better

which explains that the investment opportunity of the company is quite attractive. The

company is offering good returns to its stockholders.

Conclusion and recommendation:

On the basis of the above findings and discussion, it has been found that the few

changes rare required to be done in the organization for the better performance of the

company. The company should maintain the performance and the position according to the

industry. Company is required t make the changes into its quite level. The equity level should

be improved by the company for the better position of the company. On the other hand,

inventory management policies are also required to be change to manage the working capital

of the company.

To conclude, the current financial performance of the company is quite competitive,

various positive changes have taken place into the performance of the company in last 5 years

which has made the position of the company more attractive. The investors are recommended

to make investment into the company for the great returns.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Hotel Finance and revenue

14

References:

Barney, J. B., &Hesterly, W. S. (2006). Strategic management and competitive advantage.

Upper Saddle River, NJ: Pearson Prentice Hall.

Barr, M. J., & McClellan, G. S. (2018). Budgets and financial management in higher

education. John Wiley & Sons.

Bekaert, G., & Hodrick, R. (2017). International financial management. Cambridge

University Press.

Bekaert, G., & Hodrick, R. (2017). International financial management. Cambridge

University Press.

Dewachter, H., Iania, L., Lyrio, M., & de Sola Perea, M. (2015). A macro-financial analysis

of the euro area sovereign bond market. Journal of Banking & Finance, 50, 308-325.

Finkler, S. A., Smith, D. L., Calabrese, T. D., & Purtell, R. M. (2016). Financial management

for public, health, and not-for-profit organizations. CQ Press.

Home. (2018). British Airways limited. (online). Reterived as on 27th April 2018 from

https://www.britishairways.com/travel/home/public/en_us

Inventors. (2018). Boeing co. (online). Reterived as on 27th April 2018 from

http://investors.boeing.com/investors/financial-reports/default.aspx.

Lau, C. (2016). Financial Management. Pearson.

Morningstar. (2018). Boeing co. (online). Reterived as on 27th April 2018 from

http://financials.morningstar.com/ratios/r.html?t=BA

Pearce, J. A., Robinson, R. B., & Subramanian, R. (2000). Strategic management:

Formulation, implementation, and control. Columbus, OH: Irwin/McGraw-Hill.

Renz, D. O., & Herman, R. D. 2016). The Jossey-Bass handbook of nonprofit leadership and

management. John Wiley & Sons.

14

References:

Barney, J. B., &Hesterly, W. S. (2006). Strategic management and competitive advantage.

Upper Saddle River, NJ: Pearson Prentice Hall.

Barr, M. J., & McClellan, G. S. (2018). Budgets and financial management in higher

education. John Wiley & Sons.

Bekaert, G., & Hodrick, R. (2017). International financial management. Cambridge

University Press.

Bekaert, G., & Hodrick, R. (2017). International financial management. Cambridge

University Press.

Dewachter, H., Iania, L., Lyrio, M., & de Sola Perea, M. (2015). A macro-financial analysis

of the euro area sovereign bond market. Journal of Banking & Finance, 50, 308-325.

Finkler, S. A., Smith, D. L., Calabrese, T. D., & Purtell, R. M. (2016). Financial management

for public, health, and not-for-profit organizations. CQ Press.

Home. (2018). British Airways limited. (online). Reterived as on 27th April 2018 from

https://www.britishairways.com/travel/home/public/en_us

Inventors. (2018). Boeing co. (online). Reterived as on 27th April 2018 from

http://investors.boeing.com/investors/financial-reports/default.aspx.

Lau, C. (2016). Financial Management. Pearson.

Morningstar. (2018). Boeing co. (online). Reterived as on 27th April 2018 from

http://financials.morningstar.com/ratios/r.html?t=BA

Pearce, J. A., Robinson, R. B., & Subramanian, R. (2000). Strategic management:

Formulation, implementation, and control. Columbus, OH: Irwin/McGraw-Hill.

Renz, D. O., & Herman, R. D. 2016). The Jossey-Bass handbook of nonprofit leadership and

management. John Wiley & Sons.

Hotel Finance and revenue

15

Titman, S., Keown, A. J., & Martin, J. D. (2017). Financial management: Principles and

applications. Pearson.

Vogel, H. L. (2014). Entertainment industry economics: A guide for financial analysis.

Cambridge University Press.

Wang. Y, & Chung, Y. (2015). Hotel brand portfolio strategy. International Journal of

Contemporary Hospitality Management. 27(4). 561 – 584.

Yahoo finance. (2018). Boeing co. (online). Reterived as on 27th April 2018 from

https://finance.yahoo.com/quote/BA/

15

Titman, S., Keown, A. J., & Martin, J. D. (2017). Financial management: Principles and

applications. Pearson.

Vogel, H. L. (2014). Entertainment industry economics: A guide for financial analysis.

Cambridge University Press.

Wang. Y, & Chung, Y. (2015). Hotel brand portfolio strategy. International Journal of

Contemporary Hospitality Management. 27(4). 561 – 584.

Yahoo finance. (2018). Boeing co. (online). Reterived as on 27th April 2018 from

https://finance.yahoo.com/quote/BA/

Hotel Finance and revenue

16

Appendix:

Ratio Calculations 2015 2016 2017

Profitability Ratios: 2015 2016 2017

Return on assets

Net profit / 51,76,000 48,95,000

81,97,0

00

Total assets

9,44

,08,000

8,99

,97,000

9,23,

33,000

Answer: % 5.48% 5.44% 8.88%

Return on equity

Net profit / 51,76,000 48,95,000

81,97,0

00

Total stockholder's equity 63,35,000 81,70,000

85,50,0

00

Answer: % 82% 60% 96%

Profit margin

Net profit / 51,76,000 48,95,000

81,97,0

00

Sales Revenue %

9,61,14,00

0

9,45,71,00

0

9,33,92,

000

Answer: 5.39% 5.18% 8.78%

Efficiency Ratios 2015 2016 2017

Inventory Turnover

Average Inventory / 47257000 43199000

443440

00

Cost of Sales 82024000 80731000

759960

00

Answer: 0.58 0.54 0.58

Inventory Turnover

(days)

Average Inventory /

4,72,57,00

0

4,31,99,00

0

4,43,44,

000

Cost of Sales

#

da

ys

8,20,24,00

0

8,07,31,00

0

7,59,96,

000

Answer: (note the above

needs to be x 365) 210.29 195.31 212.98

Accounts receivable

tunrover

Average trade debtors / 8003000 7804000

976300

0

Sales revenue

9,61,14,00

0

9,45,71,00

0

9,33,92,

000

16

Appendix:

Ratio Calculations 2015 2016 2017

Profitability Ratios: 2015 2016 2017

Return on assets

Net profit / 51,76,000 48,95,000

81,97,0

00

Total assets

9,44

,08,000

8,99

,97,000

9,23,

33,000

Answer: % 5.48% 5.44% 8.88%

Return on equity

Net profit / 51,76,000 48,95,000

81,97,0

00

Total stockholder's equity 63,35,000 81,70,000

85,50,0

00

Answer: % 82% 60% 96%

Profit margin

Net profit / 51,76,000 48,95,000

81,97,0

00

Sales Revenue %

9,61,14,00

0

9,45,71,00

0

9,33,92,

000

Answer: 5.39% 5.18% 8.78%

Efficiency Ratios 2015 2016 2017

Inventory Turnover

Average Inventory / 47257000 43199000

443440

00

Cost of Sales 82024000 80731000

759960

00

Answer: 0.58 0.54 0.58

Inventory Turnover

(days)

Average Inventory /

4,72,57,00

0

4,31,99,00

0

4,43,44,

000

Cost of Sales

#

da

ys

8,20,24,00

0

8,07,31,00

0

7,59,96,

000

Answer: (note the above

needs to be x 365) 210.29 195.31 212.98

Accounts receivable

tunrover

Average trade debtors / 8003000 7804000

976300

0

Sales revenue

9,61,14,00

0

9,45,71,00

0

9,33,92,

000

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Hotel Finance and revenue

17

Answer: 0.083 0.083 0.105

Receivables Turnover

(days)

Average trade debtors /

80,

03,000

78,

04,000

97,6

3,000

Sales revenue (note used

operating revenue)

#

da

ys

9,61

,14,000

9,45

,71,000

9,33,

92,000

Answer: (note the above

needs to be x 365) 30.39 30.12 38.16

Liquidity Ratios 2015 2016 2017

Current Ratio

Current Assets /

6,82,34,00

0

6,24,88,00

0

6,51,61,

000

Current liabilities

5,04,12,00

0

5,01,34,00

0

5,62,69,

000

Answer: 1.35 1.25 1.16

Quick ratio

Current Assets -

Inventory /

2,09,77,00

0

1,92,89,00

0

2,08,17,

000

Current Liabilities

5,04,12,00

0

5,01,34,00

0

5,62,69,

000

Answer: 0.42 0.38 0.37

Capital Structure

Ratios 2015 2016 2017

Debt to assets ratio

Total debt / 98,14,000 98,14,000

1,03,79,

000

total assets

9,44,08,00

0

8,99,97,00

0

9,23,33,

000

Answer: % 0.104 0.109 0.112

Debt to equity ratio

Total debt / 98,14,000 98,14,000

1,03,79,

000

Total equity 63,35,000 81,70,000

85,50,0

00

Answer: % 1.549 1.201 1.214

Investor's Ratios 2015 2016 2017

Earnings per share

Net income 51,76,000 48,95,000

81,97,0

00

Weighted average

shares outstanding 6,86,900 6,35,500

6,02,50

0

17

Answer: 0.083 0.083 0.105

Receivables Turnover

(days)

Average trade debtors /

80,

03,000

78,

04,000

97,6

3,000

Sales revenue (note used

operating revenue)

#

da

ys

9,61

,14,000

9,45

,71,000

9,33,

92,000

Answer: (note the above

needs to be x 365) 30.39 30.12 38.16

Liquidity Ratios 2015 2016 2017

Current Ratio

Current Assets /

6,82,34,00

0

6,24,88,00

0

6,51,61,

000

Current liabilities

5,04,12,00

0

5,01,34,00

0

5,62,69,

000

Answer: 1.35 1.25 1.16

Quick ratio

Current Assets -

Inventory /

2,09,77,00

0

1,92,89,00

0

2,08,17,

000

Current Liabilities

5,04,12,00

0

5,01,34,00

0

5,62,69,

000

Answer: 0.42 0.38 0.37

Capital Structure

Ratios 2015 2016 2017

Debt to assets ratio

Total debt / 98,14,000 98,14,000

1,03,79,

000

total assets

9,44,08,00

0

8,99,97,00

0

9,23,33,

000

Answer: % 0.104 0.109 0.112

Debt to equity ratio

Total debt / 98,14,000 98,14,000

1,03,79,

000

Total equity 63,35,000 81,70,000

85,50,0

00

Answer: % 1.549 1.201 1.214

Investor's Ratios 2015 2016 2017

Earnings per share

Net income 51,76,000 48,95,000

81,97,0

00

Weighted average

shares outstanding 6,86,900 6,35,500

6,02,50

0

Hotel Finance and revenue

18

Answer: 7.535 7.703 13.605

Times interest earned

ratio

EBIT / 72,34,000 55,97,000

1,01,23,

000

Interest payable 3,39,000 3,65,000

4,30,00

0

Answer: 21.339 15.334

2

3.542

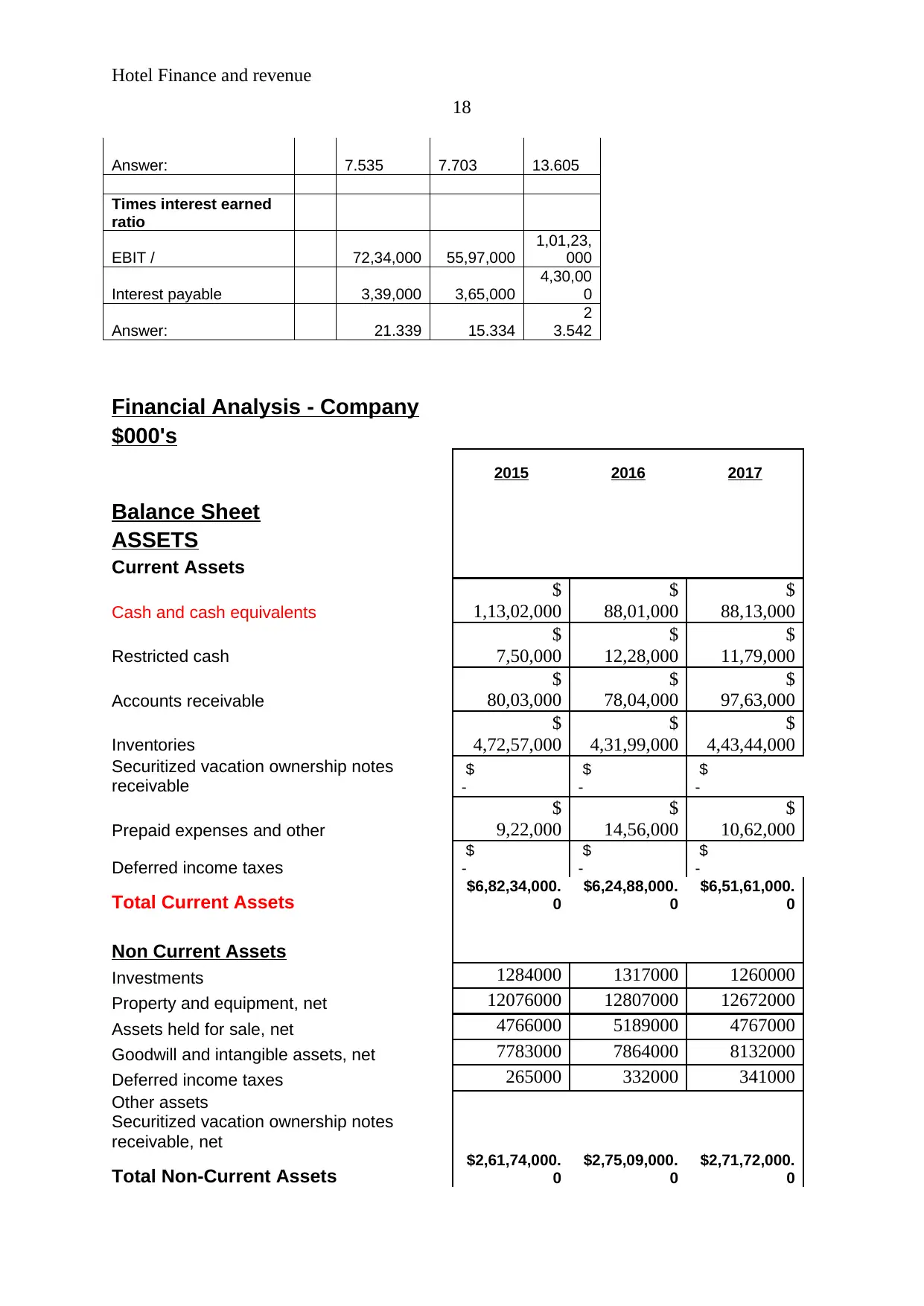

Financial Analysis - Company

$000's

2015 2016 2017

Balance Sheet

ASSETS

Current Assets

Cash and cash equivalents

$

1,13,02,000

$

88,01,000

$

88,13,000

Restricted cash

$

7,50,000

$

12,28,000

$

11,79,000

Accounts receivable

$

80,03,000

$

78,04,000

$

97,63,000

Inventories

$

4,72,57,000

$

4,31,99,000

$

4,43,44,000

Securitized vacation ownership notes

receivable

$

-

$

-

$

-

Prepaid expenses and other

$

9,22,000

$

14,56,000

$

10,62,000

Deferred income taxes

$

-

$

-

$

-

Total Current Assets $6,82,34,000.

0

$6,24,88,000.

0

$6,51,61,000.

0

Non Current Assets

Investments 1284000 1317000 1260000

Property and equipment, net 12076000 12807000 12672000

Assets held for sale, net 4766000 5189000 4767000

Goodwill and intangible assets, net 7783000 7864000 8132000

Deferred income taxes 265000 332000 341000

Other assets

Securitized vacation ownership notes

receivable, net

Total Non-Current Assets $2,61,74,000.

0

$2,75,09,000.

0

$2,71,72,000.

0

18

Answer: 7.535 7.703 13.605

Times interest earned

ratio

EBIT / 72,34,000 55,97,000

1,01,23,

000

Interest payable 3,39,000 3,65,000

4,30,00

0

Answer: 21.339 15.334

2

3.542

Financial Analysis - Company

$000's

2015 2016 2017

Balance Sheet

ASSETS

Current Assets

Cash and cash equivalents

$

1,13,02,000

$

88,01,000

$

88,13,000

Restricted cash

$

7,50,000

$

12,28,000

$

11,79,000

Accounts receivable

$

80,03,000

$

78,04,000

$

97,63,000

Inventories

$

4,72,57,000

$

4,31,99,000

$

4,43,44,000

Securitized vacation ownership notes

receivable

$

-

$

-

$

-

Prepaid expenses and other

$

9,22,000

$

14,56,000

$

10,62,000

Deferred income taxes

$

-

$

-

$

-

Total Current Assets $6,82,34,000.

0

$6,24,88,000.

0

$6,51,61,000.

0

Non Current Assets

Investments 1284000 1317000 1260000

Property and equipment, net 12076000 12807000 12672000

Assets held for sale, net 4766000 5189000 4767000

Goodwill and intangible assets, net 7783000 7864000 8132000

Deferred income taxes 265000 332000 341000

Other assets

Securitized vacation ownership notes

receivable, net

Total Non-Current Assets $2,61,74,000.

0

$2,75,09,000.

0

$2,71,72,000.

0

Hotel Finance and revenue

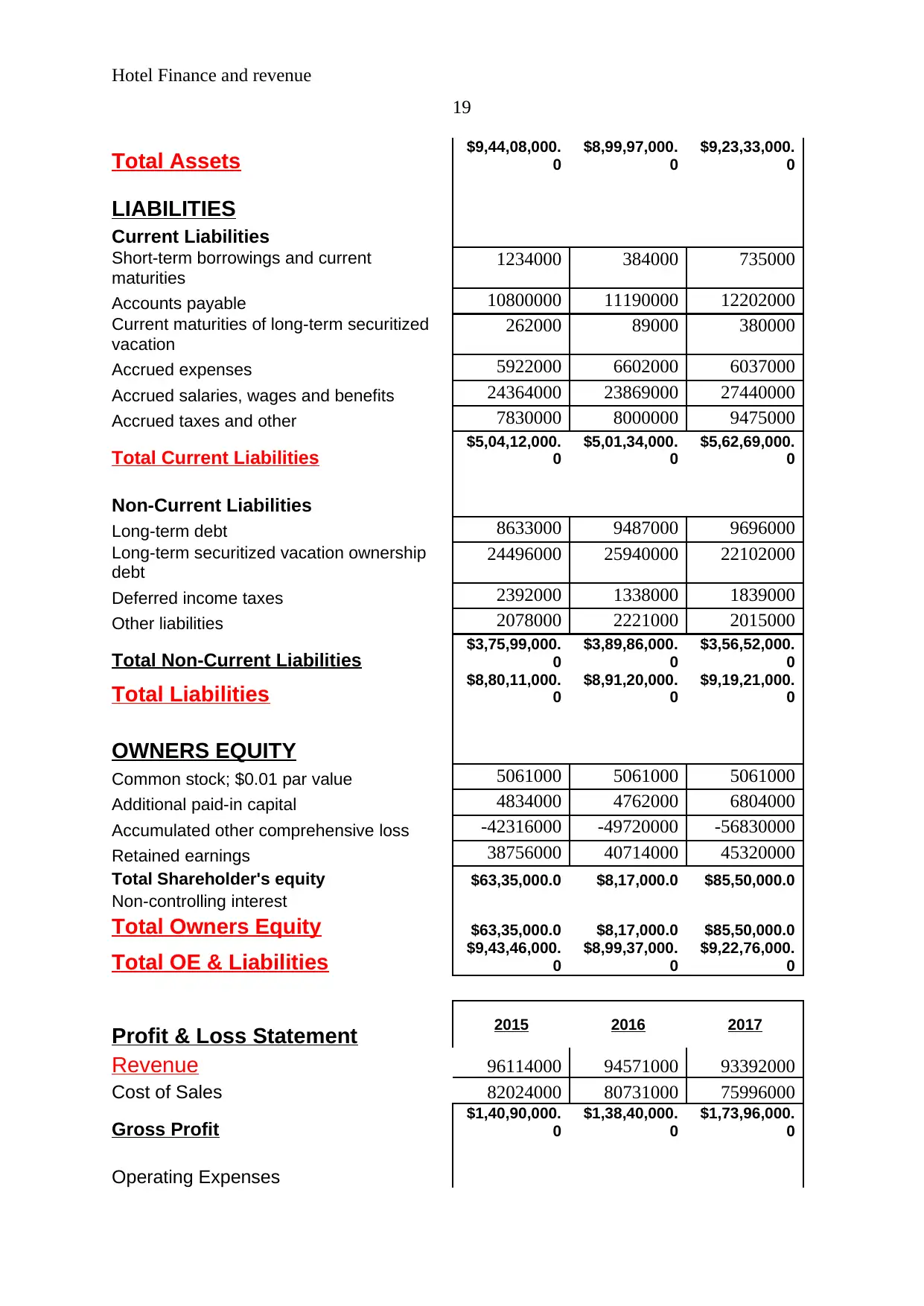

19

Total Assets $9,44,08,000.

0

$8,99,97,000.

0

$9,23,33,000.

0

LIABILITIES

Current Liabilities

Short-term borrowings and current

maturities

1234000 384000 735000

Accounts payable 10800000 11190000 12202000

Current maturities of long-term securitized

vacation

262000 89000 380000

Accrued expenses 5922000 6602000 6037000

Accrued salaries, wages and benefits 24364000 23869000 27440000

Accrued taxes and other 7830000 8000000 9475000

Total Current Liabilities $5,04,12,000.

0

$5,01,34,000.

0

$5,62,69,000.

0

Non-Current Liabilities

Long-term debt 8633000 9487000 9696000

Long-term securitized vacation ownership

debt

24496000 25940000 22102000

Deferred income taxes 2392000 1338000 1839000

Other liabilities 2078000 2221000 2015000

Total Non-Current Liabilities $3,75,99,000.

0

$3,89,86,000.

0

$3,56,52,000.

0

Total Liabilities $8,80,11,000.

0

$8,91,20,000.

0

$9,19,21,000.

0

OWNERS EQUITY

Common stock; $0.01 par value 5061000 5061000 5061000

Additional paid-in capital 4834000 4762000 6804000

Accumulated other comprehensive loss -42316000 -49720000 -56830000

Retained earnings 38756000 40714000 45320000

Total Shareholder's equity $63,35,000.0 $8,17,000.0 $85,50,000.0

Non-controlling interest

Total Owners Equity $63,35,000.0 $8,17,000.0 $85,50,000.0

Total OE & Liabilities $9,43,46,000.

0

$8,99,37,000.

0

$9,22,76,000.

0

2015 2016 2017

Profit & Loss Statement

Revenue 96114000 94571000 93392000

Cost of Sales 82024000 80731000 75996000

Gross Profit $1,40,90,000.

0

$1,38,40,000.

0

$1,73,96,000.

0

Operating Expenses

19

Total Assets $9,44,08,000.

0

$8,99,97,000.

0

$9,23,33,000.

0

LIABILITIES

Current Liabilities

Short-term borrowings and current

maturities

1234000 384000 735000

Accounts payable 10800000 11190000 12202000

Current maturities of long-term securitized

vacation

262000 89000 380000

Accrued expenses 5922000 6602000 6037000

Accrued salaries, wages and benefits 24364000 23869000 27440000

Accrued taxes and other 7830000 8000000 9475000

Total Current Liabilities $5,04,12,000.

0

$5,01,34,000.

0

$5,62,69,000.

0

Non-Current Liabilities

Long-term debt 8633000 9487000 9696000

Long-term securitized vacation ownership

debt

24496000 25940000 22102000

Deferred income taxes 2392000 1338000 1839000

Other liabilities 2078000 2221000 2015000

Total Non-Current Liabilities $3,75,99,000.

0

$3,89,86,000.

0

$3,56,52,000.

0

Total Liabilities $8,80,11,000.

0

$8,91,20,000.

0

$9,19,21,000.

0

OWNERS EQUITY

Common stock; $0.01 par value 5061000 5061000 5061000

Additional paid-in capital 4834000 4762000 6804000

Accumulated other comprehensive loss -42316000 -49720000 -56830000

Retained earnings 38756000 40714000 45320000

Total Shareholder's equity $63,35,000.0 $8,17,000.0 $85,50,000.0

Non-controlling interest

Total Owners Equity $63,35,000.0 $8,17,000.0 $85,50,000.0

Total OE & Liabilities $9,43,46,000.

0

$8,99,37,000.

0

$9,22,76,000.

0

2015 2016 2017

Profit & Loss Statement

Revenue 96114000 94571000 93392000

Cost of Sales 82024000 80731000 75996000

Gross Profit $1,40,90,000.

0

$1,38,40,000.

0

$1,73,96,000.

0

Operating Expenses

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Hotel Finance and revenue

20

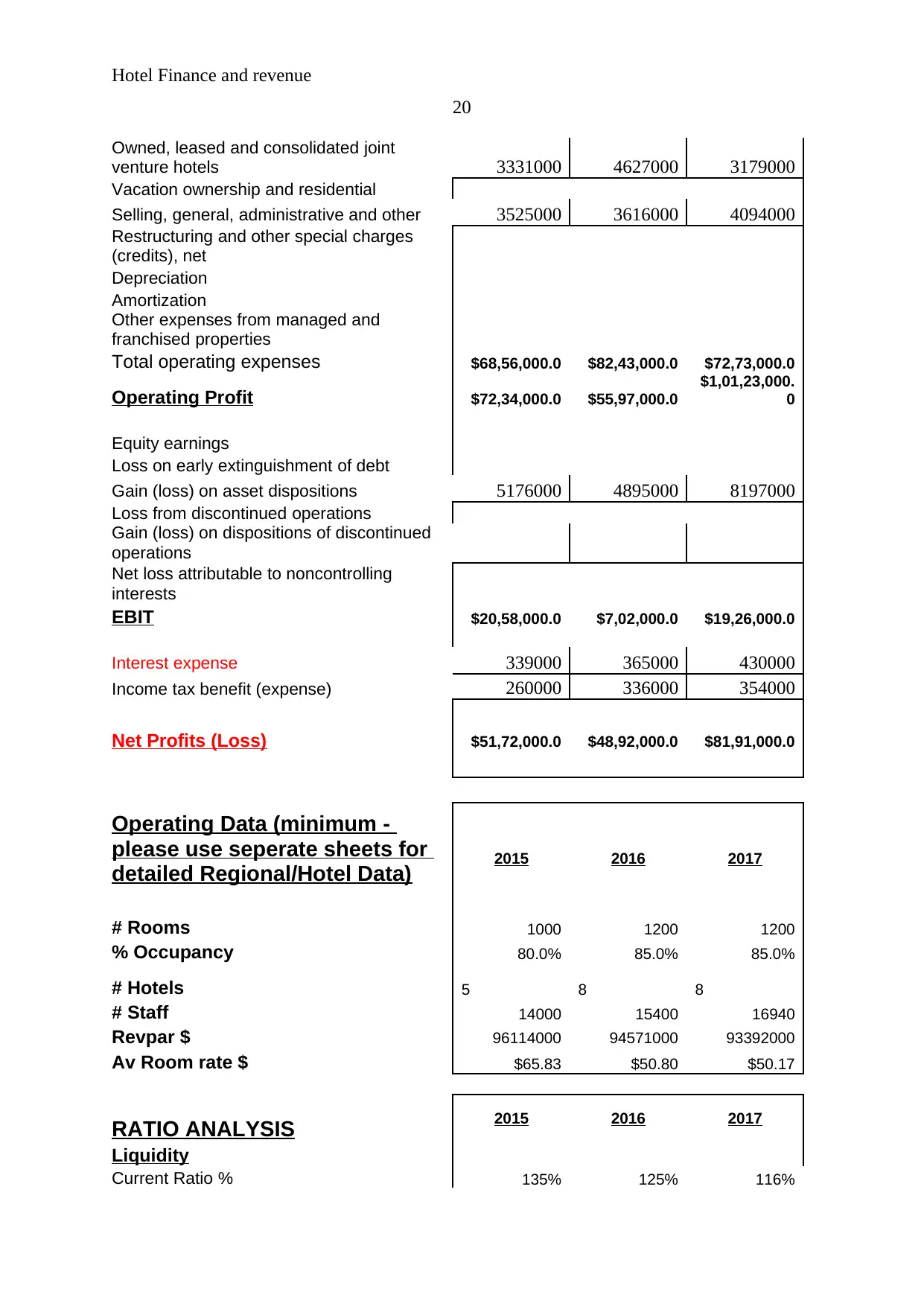

Owned, leased and consolidated joint

venture hotels 3331000 4627000 3179000

Vacation ownership and residential

Selling, general, administrative and other 3525000 3616000 4094000

Restructuring and other special charges

(credits), net

Depreciation

Amortization

Other expenses from managed and

franchised properties

Total operating expenses $68,56,000.0 $82,43,000.0 $72,73,000.0

Operating Profit $72,34,000.0 $55,97,000.0

$1,01,23,000.

0

Equity earnings

Loss on early extinguishment of debt

Gain (loss) on asset dispositions 5176000 4895000 8197000

Loss from discontinued operations

Gain (loss) on dispositions of discontinued

operations

Net loss attributable to noncontrolling

interests

EBIT $20,58,000.0 $7,02,000.0 $19,26,000.0

Interest expense 339000 365000 430000

Income tax benefit (expense) 260000 336000 354000

Net Profits (Loss) $51,72,000.0 $48,92,000.0 $81,91,000.0

Operating Data (minimum -

please use seperate sheets for

detailed Regional/Hotel Data) 2015 2016 2017

# Rooms 1000 1200 1200

% Occupancy 80.0% 85.0% 85.0%

# Hotels 5 8 8

# Staff 14000 15400 16940

Revpar $ 96114000 94571000 93392000

Av Room rate $ $65.83 $50.80 $50.17

2015 2016 2017

RATIO ANALYSIS

Liquidity

Current Ratio % 135% 125% 116%

20

Owned, leased and consolidated joint

venture hotels 3331000 4627000 3179000

Vacation ownership and residential

Selling, general, administrative and other 3525000 3616000 4094000

Restructuring and other special charges

(credits), net

Depreciation

Amortization

Other expenses from managed and

franchised properties

Total operating expenses $68,56,000.0 $82,43,000.0 $72,73,000.0

Operating Profit $72,34,000.0 $55,97,000.0

$1,01,23,000.

0

Equity earnings

Loss on early extinguishment of debt

Gain (loss) on asset dispositions 5176000 4895000 8197000

Loss from discontinued operations

Gain (loss) on dispositions of discontinued

operations

Net loss attributable to noncontrolling

interests

EBIT $20,58,000.0 $7,02,000.0 $19,26,000.0

Interest expense 339000 365000 430000

Income tax benefit (expense) 260000 336000 354000

Net Profits (Loss) $51,72,000.0 $48,92,000.0 $81,91,000.0

Operating Data (minimum -

please use seperate sheets for

detailed Regional/Hotel Data) 2015 2016 2017

# Rooms 1000 1200 1200

% Occupancy 80.0% 85.0% 85.0%

# Hotels 5 8 8

# Staff 14000 15400 16940

Revpar $ 96114000 94571000 93392000

Av Room rate $ $65.83 $50.80 $50.17

2015 2016 2017

RATIO ANALYSIS

Liquidity

Current Ratio % 135% 125% 116%

Hotel Finance and revenue

21

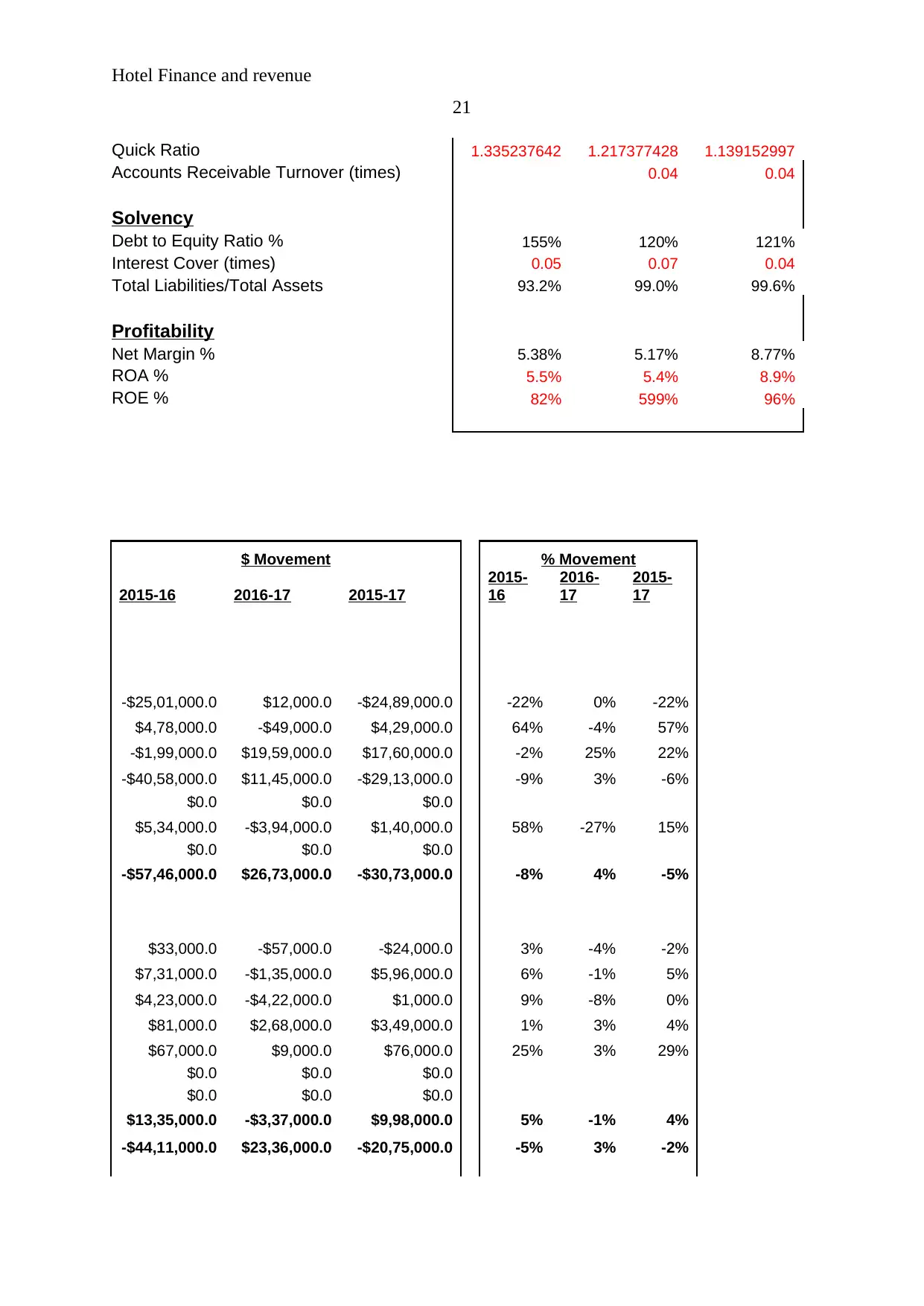

Quick Ratio 1.335237642 1.217377428 1.139152997

Accounts Receivable Turnover (times) 0.04 0.04

Solvency

Debt to Equity Ratio % 155% 120% 121%

Interest Cover (times) 0.05 0.07 0.04

Total Liabilities/Total Assets 93.2% 99.0% 99.6%

Profitability

Net Margin % 5.38% 5.17% 8.77%

ROA % 5.5% 5.4% 8.9%

ROE % 82% 599% 96%

$ Movement % Movement

2015-16 2016-17 2015-17

2015-

16

2016-

17

2015-

17

-$25,01,000.0 $12,000.0 -$24,89,000.0 -22% 0% -22%

$4,78,000.0 -$49,000.0 $4,29,000.0 64% -4% 57%

-$1,99,000.0 $19,59,000.0 $17,60,000.0 -2% 25% 22%

-$40,58,000.0 $11,45,000.0 -$29,13,000.0 -9% 3% -6%

$0.0 $0.0 $0.0

$5,34,000.0 -$3,94,000.0 $1,40,000.0 58% -27% 15%

$0.0 $0.0 $0.0

-$57,46,000.0 $26,73,000.0 -$30,73,000.0 -8% 4% -5%

$33,000.0 -$57,000.0 -$24,000.0 3% -4% -2%

$7,31,000.0 -$1,35,000.0 $5,96,000.0 6% -1% 5%

$4,23,000.0 -$4,22,000.0 $1,000.0 9% -8% 0%

$81,000.0 $2,68,000.0 $3,49,000.0 1% 3% 4%

$67,000.0 $9,000.0 $76,000.0 25% 3% 29%

$0.0 $0.0 $0.0

$0.0 $0.0 $0.0

$13,35,000.0 -$3,37,000.0 $9,98,000.0 5% -1% 4%

-$44,11,000.0 $23,36,000.0 -$20,75,000.0 -5% 3% -2%

21

Quick Ratio 1.335237642 1.217377428 1.139152997

Accounts Receivable Turnover (times) 0.04 0.04

Solvency

Debt to Equity Ratio % 155% 120% 121%

Interest Cover (times) 0.05 0.07 0.04

Total Liabilities/Total Assets 93.2% 99.0% 99.6%

Profitability

Net Margin % 5.38% 5.17% 8.77%

ROA % 5.5% 5.4% 8.9%

ROE % 82% 599% 96%

$ Movement % Movement

2015-16 2016-17 2015-17

2015-

16

2016-

17

2015-

17

-$25,01,000.0 $12,000.0 -$24,89,000.0 -22% 0% -22%

$4,78,000.0 -$49,000.0 $4,29,000.0 64% -4% 57%

-$1,99,000.0 $19,59,000.0 $17,60,000.0 -2% 25% 22%

-$40,58,000.0 $11,45,000.0 -$29,13,000.0 -9% 3% -6%

$0.0 $0.0 $0.0

$5,34,000.0 -$3,94,000.0 $1,40,000.0 58% -27% 15%

$0.0 $0.0 $0.0

-$57,46,000.0 $26,73,000.0 -$30,73,000.0 -8% 4% -5%

$33,000.0 -$57,000.0 -$24,000.0 3% -4% -2%

$7,31,000.0 -$1,35,000.0 $5,96,000.0 6% -1% 5%

$4,23,000.0 -$4,22,000.0 $1,000.0 9% -8% 0%

$81,000.0 $2,68,000.0 $3,49,000.0 1% 3% 4%

$67,000.0 $9,000.0 $76,000.0 25% 3% 29%

$0.0 $0.0 $0.0

$0.0 $0.0 $0.0

$13,35,000.0 -$3,37,000.0 $9,98,000.0 5% -1% 4%

-$44,11,000.0 $23,36,000.0 -$20,75,000.0 -5% 3% -2%

Hotel Finance and revenue

22

-$8,50,000.0 $3,51,000.0 -$4,99,000.0 -69% 91% -40%

$3,90,000.0 $10,12,000.0 $14,02,000.0 4% 9% 13%

-$1,73,000.0 $2,91,000.0 $1,18,000.0 -66% 327% 45%

$6,80,000.0 -$5,65,000.0 $1,15,000.0 11% -9% 2%

-$4,95,000.0 $35,71,000.0 $30,76,000.0 -2% 15% 13%

$1,70,000.0 $14,75,000.0 $16,45,000.0 2% 18% 21%

-$2,78,000.0 $61,35,000.0 $58,57,000.0 -1% 12% 12%

$8,54,000.0 $2,09,000.0 $10,63,000.0 10% 2% 12%

$14,44,000.0 -$38,38,000.0 -$23,94,000.0 6% -15% -10%

-$10,54,000.0 $5,01,000.0 -$5,53,000.0 -44% 37% -23%

$1,43,000.0 -$2,06,000.0 -$63,000.0 7% -9% -3%

$13,87,000.0 -$33,34,000.0 -$19,47,000.0 4% -9% -5%

$11,09,000.0 $28,01,000.0 $39,10,000.0 1% 3% 4%

$0.0 $0.0 $0.0 0% 0% 0%

-$72,000.0 $20,42,000.0 $19,70,000.0 -1% 43% 41%

-$74,04,000.0 -$71,10,000.0

-

$1,45,14,000.0 17% 14% 34%

$19,58,000.0 $46,06,000.0 $65,64,000.0 5% 11% 17%

-$55,18,000.0 $77,33,000.0 $22,15,000.0 -87% 947% 35%

$0.0 $0.0 $0.0

-$55,18,000.0 $77,33,000.0 $22,15,000.0 -87% 947% 35%

-$44,09,000.0 $23,39,000.0 -$20,70,000.0 -5% 3% -2%

$ Movement % Movement

2015-16 2016-17 2015-17

2015-

16

2016-

17

2015-

17

-$15,43,000.0 -$11,79,000.0 -$27,22,000.0 -2% -1% -3%

-$12,93,000.0 -$47,35,000.0 -$60,28,000.0 -2% -6% -7%

-$2,50,000.0 $35,56,000.0 $33,06,000.0 -2% 26% 23%

$12,96,000.0 -$14,48,000.0 -$1,52,000.0 39% -31% -5%

$0.0 $0.0 $0.0

$91,000.0 $4,78,000.0 $5,69,000.0 3% 13% 16%

$0.0 $0.0 $0.0

$0.0 $0.0 $0.0

$0.0 $0.0 $0.0

22

-$8,50,000.0 $3,51,000.0 -$4,99,000.0 -69% 91% -40%

$3,90,000.0 $10,12,000.0 $14,02,000.0 4% 9% 13%

-$1,73,000.0 $2,91,000.0 $1,18,000.0 -66% 327% 45%

$6,80,000.0 -$5,65,000.0 $1,15,000.0 11% -9% 2%

-$4,95,000.0 $35,71,000.0 $30,76,000.0 -2% 15% 13%

$1,70,000.0 $14,75,000.0 $16,45,000.0 2% 18% 21%

-$2,78,000.0 $61,35,000.0 $58,57,000.0 -1% 12% 12%

$8,54,000.0 $2,09,000.0 $10,63,000.0 10% 2% 12%

$14,44,000.0 -$38,38,000.0 -$23,94,000.0 6% -15% -10%

-$10,54,000.0 $5,01,000.0 -$5,53,000.0 -44% 37% -23%

$1,43,000.0 -$2,06,000.0 -$63,000.0 7% -9% -3%

$13,87,000.0 -$33,34,000.0 -$19,47,000.0 4% -9% -5%

$11,09,000.0 $28,01,000.0 $39,10,000.0 1% 3% 4%

$0.0 $0.0 $0.0 0% 0% 0%

-$72,000.0 $20,42,000.0 $19,70,000.0 -1% 43% 41%

-$74,04,000.0 -$71,10,000.0

-

$1,45,14,000.0 17% 14% 34%

$19,58,000.0 $46,06,000.0 $65,64,000.0 5% 11% 17%

-$55,18,000.0 $77,33,000.0 $22,15,000.0 -87% 947% 35%

$0.0 $0.0 $0.0

-$55,18,000.0 $77,33,000.0 $22,15,000.0 -87% 947% 35%

-$44,09,000.0 $23,39,000.0 -$20,70,000.0 -5% 3% -2%

$ Movement % Movement

2015-16 2016-17 2015-17

2015-

16

2016-

17

2015-

17

-$15,43,000.0 -$11,79,000.0 -$27,22,000.0 -2% -1% -3%

-$12,93,000.0 -$47,35,000.0 -$60,28,000.0 -2% -6% -7%

-$2,50,000.0 $35,56,000.0 $33,06,000.0 -2% 26% 23%

$12,96,000.0 -$14,48,000.0 -$1,52,000.0 39% -31% -5%

$0.0 $0.0 $0.0

$91,000.0 $4,78,000.0 $5,69,000.0 3% 13% 16%

$0.0 $0.0 $0.0

$0.0 $0.0 $0.0

$0.0 $0.0 $0.0

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Hotel Finance and revenue

23

$0.0 $0.0 $0.0

$13,87,000.0 -$9,70,000.0 $4,17,000.0 20% -12% 6%

-$16,37,000.0 $45,26,000.0 $28,89,000.0 -23% 81% 40%

$0.0 $0.0 $0.0

$0.0 $0.0 $0.0

-$2,81,000.0 $33,02,000.0 $30,21,000.0 -5% 67% 58%

$0.0 $0.0 $0.0

$0.0 $0.0 $0.0

$0.0 $0.0 $0.0

-$13,56,000.0 $12,24,000.0 -$1,32,000.0 -66% 174% -6%

$26,000.0 $65,000.0 $91,000.0 8% 18% 27%

$76,000.0 $18,000.0 $94,000.0 29% 5% 36%

-$2,80,000.0 $32,99,000.0 $30,19,000.0 -5% 67% 58%

Movement % Movement

2015-16 2016-17 2015-17

2015-

16

2016-

17

2015-

17

200 0 200 20.0% 0.0% 20.0%

0.05 0 0.05 6.2% 0.0% 6.2%

3 0 3 60.0% 0.0% 60.0%

1400 1540 2940 10.0% 10.0% 21.0%

-15.02785388 -0.633360193 -15.66121407 -22.8% -1.2% -23.8%

0 0 0

23

$0.0 $0.0 $0.0

$13,87,000.0 -$9,70,000.0 $4,17,000.0 20% -12% 6%

-$16,37,000.0 $45,26,000.0 $28,89,000.0 -23% 81% 40%

$0.0 $0.0 $0.0

$0.0 $0.0 $0.0

-$2,81,000.0 $33,02,000.0 $30,21,000.0 -5% 67% 58%

$0.0 $0.0 $0.0

$0.0 $0.0 $0.0

$0.0 $0.0 $0.0

-$13,56,000.0 $12,24,000.0 -$1,32,000.0 -66% 174% -6%

$26,000.0 $65,000.0 $91,000.0 8% 18% 27%

$76,000.0 $18,000.0 $94,000.0 29% 5% 36%

-$2,80,000.0 $32,99,000.0 $30,19,000.0 -5% 67% 58%

Movement % Movement

2015-16 2016-17 2015-17

2015-

16

2016-

17

2015-

17

200 0 200 20.0% 0.0% 20.0%

0.05 0 0.05 6.2% 0.0% 6.2%

3 0 3 60.0% 0.0% 60.0%

1400 1540 2940 10.0% 10.0% 21.0%

-15.02785388 -0.633360193 -15.66121407 -22.8% -1.2% -23.8%

0 0 0

Hotel Finance and revenue

24

24

1 out of 24

Related Documents

![[FINANCIAL ANALYSIS] Ratio Analysis of AA, BA, and CA Companies](/_next/image/?url=https%3A%2F%2Fdesklib.com%2Fmedia%2Fimages%2Fme%2F7ec77c9779a64d0faedda6aed8107017.jpg&w=256&q=75)

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.