Hotel Finance and Revenue Analysis: A Study of Qantas and Virgin Australia

VerifiedAdded on 2023/06/15

|14

|3703

|91

AI Summary

This report analyses the financial performance of Qantas and Virgin Australia using ratio analysis and revenue management techniques. It provides recommendations for increasing revenue targets.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: HOTEL FINANCE AND REVENUE

Hotel finance and revenue

Name of the student

Name of the university

Student ID

Author note

Hotel finance and revenue

Name of the student

Name of the university

Student ID

Author note

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1HOTEL FINANCE AND REVENUE

Table of Contents

Introduction................................................................................................................................2

Ratio analysis.............................................................................................................................2

Revenue management................................................................................................................9

Conclusion................................................................................................................................10

Reference..................................................................................................................................11

Table of Contents

Introduction................................................................................................................................2

Ratio analysis.............................................................................................................................2

Revenue management................................................................................................................9

Conclusion................................................................................................................................10

Reference..................................................................................................................................11

2HOTEL FINANCE AND REVENUE

Introduction

The main objective of the report is to analyse and interpret the financial performance

of two airlines from Australia that is Virgin Australia and Qantas Airlines. The analysis and

interpretation will be based on various ratio calculations like profitability ratio, liquidity ratio

and efficiency ratio. Finally, based on the analysis some recommendation will be provided

for increasing the revenue target.

Qantas Airline was established in the year 1920 in Queensland and became the largest

international and domestic airline in Australia. They are well known for excellence in

operational reliability, safety, maintenance, engineering and the service provided to the

customers. Main business of the company is to provide transportation service to the

customers through 2 complementary brands of airlines that is, Jetstar and Qantas. The

company also operate subsidiary business that includes other airlines and the businesses

under specialist markets like Q Catering (Flights | Qantas AU, 2018). It operates

international, domestic and regional services and employs more than 30,000 employees out of

which near about 93% are based in Australia. On the other hand, Virgin Australia entered

into the aviation market of Australia in the year 2000 and brought the real competition in the

market’s leisure sector. The main objective of the company is to revolutionise the air travel

through all the market segments. The objectives will be achieved through delivering seamless

experience all over the international and domestic market in addition to retaining same level

of excellent services (Virgin Australia | Home, 2018).

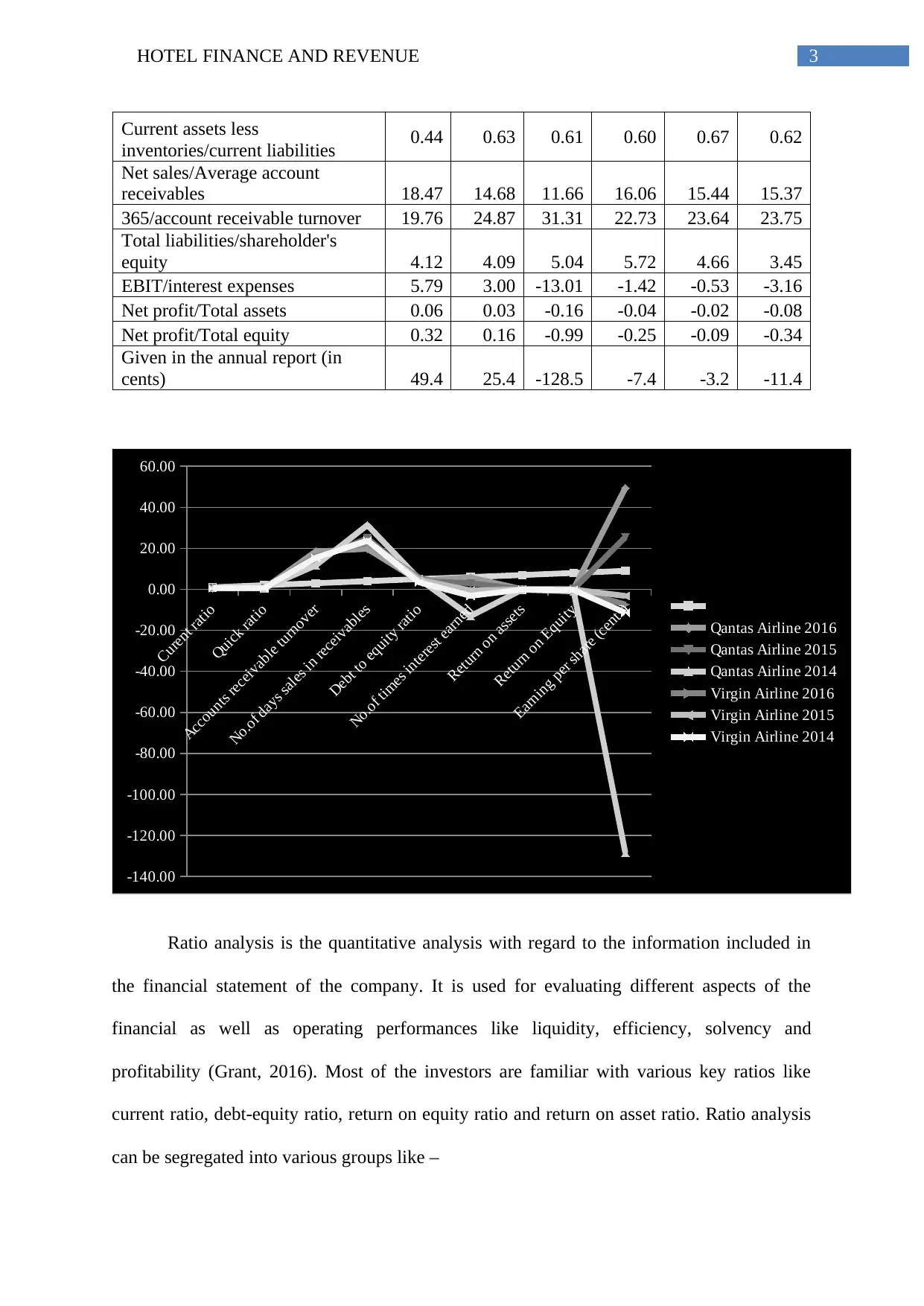

Ratio analysis

Formula Qantas Airline Virgin Airline

2016 2015 2014 2016 2015 2014

Current assets/Current liabilities 0.49 0.68 0.66 0.62 0.69 0.64

Introduction

The main objective of the report is to analyse and interpret the financial performance

of two airlines from Australia that is Virgin Australia and Qantas Airlines. The analysis and

interpretation will be based on various ratio calculations like profitability ratio, liquidity ratio

and efficiency ratio. Finally, based on the analysis some recommendation will be provided

for increasing the revenue target.

Qantas Airline was established in the year 1920 in Queensland and became the largest

international and domestic airline in Australia. They are well known for excellence in

operational reliability, safety, maintenance, engineering and the service provided to the

customers. Main business of the company is to provide transportation service to the

customers through 2 complementary brands of airlines that is, Jetstar and Qantas. The

company also operate subsidiary business that includes other airlines and the businesses

under specialist markets like Q Catering (Flights | Qantas AU, 2018). It operates

international, domestic and regional services and employs more than 30,000 employees out of

which near about 93% are based in Australia. On the other hand, Virgin Australia entered

into the aviation market of Australia in the year 2000 and brought the real competition in the

market’s leisure sector. The main objective of the company is to revolutionise the air travel

through all the market segments. The objectives will be achieved through delivering seamless

experience all over the international and domestic market in addition to retaining same level

of excellent services (Virgin Australia | Home, 2018).

Ratio analysis

Formula Qantas Airline Virgin Airline

2016 2015 2014 2016 2015 2014

Current assets/Current liabilities 0.49 0.68 0.66 0.62 0.69 0.64

3HOTEL FINANCE AND REVENUE

Current assets less

inventories/current liabilities 0.44 0.63 0.61 0.60 0.67 0.62

Net sales/Average account

receivables 18.47 14.68 11.66 16.06 15.44 15.37

365/account receivable turnover 19.76 24.87 31.31 22.73 23.64 23.75

Total liabilities/shareholder's

equity 4.12 4.09 5.04 5.72 4.66 3.45

EBIT/interest expenses 5.79 3.00 -13.01 -1.42 -0.53 -3.16

Net profit/Total assets 0.06 0.03 -0.16 -0.04 -0.02 -0.08

Net profit/Total equity 0.32 0.16 -0.99 -0.25 -0.09 -0.34

Given in the annual report (in

cents) 49.4 25.4 -128.5 -7.4 -3.2 -11.4

Curent ratio

Quick ratio

Accounts receivable turnover

No.of days sales in receivables

Debt to equity ratio

No.of times interest earned

Return on assets

Return on Equity

Earning per share (cents)

-140.00

-120.00

-100.00

-80.00

-60.00

-40.00

-20.00

0.00

20.00

40.00

60.00

Qantas Airline 2016

Qantas Airline 2015

Qantas Airline 2014

Virgin Airline 2016

Virgin Airline 2015

Virgin Airline 2014

Ratio analysis is the quantitative analysis with regard to the information included in

the financial statement of the company. It is used for evaluating different aspects of the

financial as well as operating performances like liquidity, efficiency, solvency and

profitability (Grant, 2016). Most of the investors are familiar with various key ratios like

current ratio, debt-equity ratio, return on equity ratio and return on asset ratio. Ratio analysis

can be segregated into various groups like –

Current assets less

inventories/current liabilities 0.44 0.63 0.61 0.60 0.67 0.62

Net sales/Average account

receivables 18.47 14.68 11.66 16.06 15.44 15.37

365/account receivable turnover 19.76 24.87 31.31 22.73 23.64 23.75

Total liabilities/shareholder's

equity 4.12 4.09 5.04 5.72 4.66 3.45

EBIT/interest expenses 5.79 3.00 -13.01 -1.42 -0.53 -3.16

Net profit/Total assets 0.06 0.03 -0.16 -0.04 -0.02 -0.08

Net profit/Total equity 0.32 0.16 -0.99 -0.25 -0.09 -0.34

Given in the annual report (in

cents) 49.4 25.4 -128.5 -7.4 -3.2 -11.4

Curent ratio

Quick ratio

Accounts receivable turnover

No.of days sales in receivables

Debt to equity ratio

No.of times interest earned

Return on assets

Return on Equity

Earning per share (cents)

-140.00

-120.00

-100.00

-80.00

-60.00

-40.00

-20.00

0.00

20.00

40.00

60.00

Qantas Airline 2016

Qantas Airline 2015

Qantas Airline 2014

Virgin Airline 2016

Virgin Airline 2015

Virgin Airline 2014

Ratio analysis is the quantitative analysis with regard to the information included in

the financial statement of the company. It is used for evaluating different aspects of the

financial as well as operating performances like liquidity, efficiency, solvency and

profitability (Grant, 2016). Most of the investors are familiar with various key ratios like

current ratio, debt-equity ratio, return on equity ratio and return on asset ratio. Ratio analysis

can be segregated into various groups like –

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

4HOTEL FINANCE AND REVENUE

Liquidity Ratio – it measures the ability of the company to pay off the short-term obligations

as they become due and are met through the quick assets or current assets. Various ratios

through which the liquidity of the company is measured are the current ratio and quick ratio.

Current ratio – it is the liquidity ratio that computes the ability of the company for

paying off the long term and short term obligations. To measure the ability current

ratio tales into consideration the total current assets of the company against the total

current liabilities (Heikal, Khaddafi & Ummah, 2014). It is calculated through

dividing the current assets by current liabilities. It is called current ratio as as it

incorporates all the current liabilities and current assets. Generally the ratio less than

1 represent that the current assets of the company are lower than its current

liabilities. Looking into the annual report of Qantas airline and Virgin Australia

airline and the calculation from the above table that the current ratio of Qantas

airline reduced from 0.66 to 0.49 and for Virgin Australia it is reduced from 0.64 to

0.62 over the years from 2014 to 2016. Therefore, it presents that the financial health

of both the companies are not good (Hevert, 2013). However, it does not mean that

the company will become bankrupt and various ways are there for the company to

access finance if it has realistic expectation regarding the future earnings to pay-off

the borrowings. Further, these ratios of below 1 will be acceptable to the investors if

the companies are able for negotiating long term credit periods with the suppliers

and at the same time offering lower credit terms to the customers. These companies

will be able to maintain the minimum levels of the inventory under the balance sheet

if the operations are carried out efficiently.

Quick ratio – the quick ratio that is also known as the acid-test ratio measure the

efficiency of the company to meet its short-term financial obligations. It is calculated

through dividing the current assets of the company reducing the inventories of the

Liquidity Ratio – it measures the ability of the company to pay off the short-term obligations

as they become due and are met through the quick assets or current assets. Various ratios

through which the liquidity of the company is measured are the current ratio and quick ratio.

Current ratio – it is the liquidity ratio that computes the ability of the company for

paying off the long term and short term obligations. To measure the ability current

ratio tales into consideration the total current assets of the company against the total

current liabilities (Heikal, Khaddafi & Ummah, 2014). It is calculated through

dividing the current assets by current liabilities. It is called current ratio as as it

incorporates all the current liabilities and current assets. Generally the ratio less than

1 represent that the current assets of the company are lower than its current

liabilities. Looking into the annual report of Qantas airline and Virgin Australia

airline and the calculation from the above table that the current ratio of Qantas

airline reduced from 0.66 to 0.49 and for Virgin Australia it is reduced from 0.64 to

0.62 over the years from 2014 to 2016. Therefore, it presents that the financial health

of both the companies are not good (Hevert, 2013). However, it does not mean that

the company will become bankrupt and various ways are there for the company to

access finance if it has realistic expectation regarding the future earnings to pay-off

the borrowings. Further, these ratios of below 1 will be acceptable to the investors if

the companies are able for negotiating long term credit periods with the suppliers

and at the same time offering lower credit terms to the customers. These companies

will be able to maintain the minimum levels of the inventory under the balance sheet

if the operations are carried out efficiently.

Quick ratio – the quick ratio that is also known as the acid-test ratio measure the

efficiency of the company to meet its short-term financial obligations. It is calculated

through dividing the current assets of the company reducing the inventories of the

5HOTEL FINANCE AND REVENUE

company by the current liabilities. Through the quick ratio of the company is similar

to the current ratio, the quick ratio provides more precise analysis of the ability of

company for paying off the current obligations (Jones & Kulish, 2013). Looking into

the quick ratio of both the companies it is identified that the quick ratio of Qantas

airline are reduced from 0.61 to 0.44 and for Virgin Australia it is reduced from 0.62

to 0.60 over the years from 2014 to 2016.

Therefore, taking into consideration both the liquidity ratios, it is observed that the

liquidity position of Virgin Australia airline is better as compared to Qantas airline. However,

the liquidity ratios assumed that the company will liquidate the current assets for paying the

current liabilities that is not realistic always taking into consideration the thing that the

company is required to maintain the same level of working capital for the operation

management.

Solvency ratios – it is also called as he financial leverage ratio and it compares the debt levels

of the company with the earnings, equity and assets for evaluating whether the company can

sustain in the market for long-term period through paying off its long term borrowings and

interests on that (Sunder, 2016). Various solvency ratios include interest coverage ratio or

number of times interest earned and debt to equity ratio.

Number of times interest earned – it is used for determining the efficiency of the

company to pay off their interest expenses on the outstanding borrowings. It is

calculated through dividing the operating profit of the company by the interest

expenses for the period (Brooks, 2015). The lower ratio represents that the company

is burdened with debt expenses. While the interest coverage ratio of the company is 2

or lower than that the ability of the company to meet the interest expenses can be

questionable. It measures the times that the company can pay the outstanding

company by the current liabilities. Through the quick ratio of the company is similar

to the current ratio, the quick ratio provides more precise analysis of the ability of

company for paying off the current obligations (Jones & Kulish, 2013). Looking into

the quick ratio of both the companies it is identified that the quick ratio of Qantas

airline are reduced from 0.61 to 0.44 and for Virgin Australia it is reduced from 0.62

to 0.60 over the years from 2014 to 2016.

Therefore, taking into consideration both the liquidity ratios, it is observed that the

liquidity position of Virgin Australia airline is better as compared to Qantas airline. However,

the liquidity ratios assumed that the company will liquidate the current assets for paying the

current liabilities that is not realistic always taking into consideration the thing that the

company is required to maintain the same level of working capital for the operation

management.

Solvency ratios – it is also called as he financial leverage ratio and it compares the debt levels

of the company with the earnings, equity and assets for evaluating whether the company can

sustain in the market for long-term period through paying off its long term borrowings and

interests on that (Sunder, 2016). Various solvency ratios include interest coverage ratio or

number of times interest earned and debt to equity ratio.

Number of times interest earned – it is used for determining the efficiency of the

company to pay off their interest expenses on the outstanding borrowings. It is

calculated through dividing the operating profit of the company by the interest

expenses for the period (Brooks, 2015). The lower ratio represents that the company

is burdened with debt expenses. While the interest coverage ratio of the company is 2

or lower than that the ability of the company to meet the interest expenses can be

questionable. It measures the times that the company can pay the outstanding

6HOTEL FINANCE AND REVENUE

borrowings using the earnings of the company. It is considered as the margin of

safety for the creditors of the company that can run into the financial difficulty for the

company. The ability of paying off the debt obligations is major factor for

determining the solvency of the company and it is a crucial statistic for the

shareholders and potential investors (Drehmann & Nikolaou, 2013). Looking into the

calculation table it is found that the Interest coverage ratio of Virgin airline for all the

three years are in negative as the company was not able to earn any positive operating

income throughout all 3 years. On the other hand, the interest coverage ratio for

Qantas airline improved in 2016 as compared to the year 2014 and 2015.

Debt to equity ratio – the debt to equity ratio is calculated through dividing the total

liabilities of the company by the shareholder’s equity. It is used for measuring the

financial leverage of the company. This ratio indicates the amount of debt used by the

company to finance the assets as compared to the amount of equity. If the company

use higher amount of debts for increasing finance for its operations the company can

generate higher level of earnings as compared to the amount that would have been

earned if it did not opt for outside finance (Nobes, 2014). It can be identified from the

annual report and calculation table that the debt to equity ratio of both companies is

quite high. It represents that the total liabilities of both the companies are

significantly high as compared to the total equities of the company. However, the

debt to equity ratio of Qantas airline is better as compared to Virgin Australia as its

debt to equity ratio is slightly lower than Virgin Australia.

Profitability ratio – it measures the company’s ability to ear the profit and create return for its

shareholders. While the solvency ratios and liquidity ratios states the company’s financial

position the profitability ratio and efficiency ratio states the financial performance of the

borrowings using the earnings of the company. It is considered as the margin of

safety for the creditors of the company that can run into the financial difficulty for the

company. The ability of paying off the debt obligations is major factor for

determining the solvency of the company and it is a crucial statistic for the

shareholders and potential investors (Drehmann & Nikolaou, 2013). Looking into the

calculation table it is found that the Interest coverage ratio of Virgin airline for all the

three years are in negative as the company was not able to earn any positive operating

income throughout all 3 years. On the other hand, the interest coverage ratio for

Qantas airline improved in 2016 as compared to the year 2014 and 2015.

Debt to equity ratio – the debt to equity ratio is calculated through dividing the total

liabilities of the company by the shareholder’s equity. It is used for measuring the

financial leverage of the company. This ratio indicates the amount of debt used by the

company to finance the assets as compared to the amount of equity. If the company

use higher amount of debts for increasing finance for its operations the company can

generate higher level of earnings as compared to the amount that would have been

earned if it did not opt for outside finance (Nobes, 2014). It can be identified from the

annual report and calculation table that the debt to equity ratio of both companies is

quite high. It represents that the total liabilities of both the companies are

significantly high as compared to the total equities of the company. However, the

debt to equity ratio of Qantas airline is better as compared to Virgin Australia as its

debt to equity ratio is slightly lower than Virgin Australia.

Profitability ratio – it measures the company’s ability to ear the profit and create return for its

shareholders. While the solvency ratios and liquidity ratios states the company’s financial

position the profitability ratio and efficiency ratio states the financial performance of the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7HOTEL FINANCE AND REVENUE

company. Major profitability ratios are the return on assets, return on equity and earnings per

share.

Return on assets – this ratio is the calculation of net income as compared to the total

assets of the business during the financial year. It is used to measure the efficiency of

business through using the assets for generating net income. It indicates the cents

earned with each dollar of the asset. Therefore, the higher return indicates that the

business is more profitable. However, this ratio shall be used to compare the

companies under same industry. Increasing of ROA indicates that profitability for the

company is improving (Luez & Wysocki, 2016). Looking into the ROA of both the

companies it is found that the ROA for Qantas airline for the year 2014 was in

negative as the net income of the company was negative. However, for 2015 and 2016

the ROA of the company is in positive. However, the ratio is significantly low for

Qantas airline. On the other hand, for Virgin Australia ROA, for all the three years are

in negative as the net income of the company for all the 3 years are in negative.

Return on equity - this ratio is the calculation of net income as compared to the total

shareholder’s equity of the business during the financial year. It is used to measure the

profitability on shareholder’s investment. It is the important measure for the

company’s profitability. Higher ratio represent that the company is efficient for

creating income on the shareholder’s investment. When the capital is raised through

debt for reducing the share capital the ROE will increase even if the income is

constant (Kettunen, 2017). Looking into the ROE of both the companies it is observed

that ROE of Qantas airline for the year 2014 was in negative as the net income of the

company was negative. However, for 2015 and 2016 the ROE of the company is in

positive. On the other hand, for Virgin Australia, ROA for all the three years are in

negative as the net income of the company for all the 3 years are in negative.

company. Major profitability ratios are the return on assets, return on equity and earnings per

share.

Return on assets – this ratio is the calculation of net income as compared to the total

assets of the business during the financial year. It is used to measure the efficiency of

business through using the assets for generating net income. It indicates the cents

earned with each dollar of the asset. Therefore, the higher return indicates that the

business is more profitable. However, this ratio shall be used to compare the

companies under same industry. Increasing of ROA indicates that profitability for the

company is improving (Luez & Wysocki, 2016). Looking into the ROA of both the

companies it is found that the ROA for Qantas airline for the year 2014 was in

negative as the net income of the company was negative. However, for 2015 and 2016

the ROA of the company is in positive. However, the ratio is significantly low for

Qantas airline. On the other hand, for Virgin Australia ROA, for all the three years are

in negative as the net income of the company for all the 3 years are in negative.

Return on equity - this ratio is the calculation of net income as compared to the total

shareholder’s equity of the business during the financial year. It is used to measure the

profitability on shareholder’s investment. It is the important measure for the

company’s profitability. Higher ratio represent that the company is efficient for

creating income on the shareholder’s investment. When the capital is raised through

debt for reducing the share capital the ROE will increase even if the income is

constant (Kettunen, 2017). Looking into the ROE of both the companies it is observed

that ROE of Qantas airline for the year 2014 was in negative as the net income of the

company was negative. However, for 2015 and 2016 the ROE of the company is in

positive. On the other hand, for Virgin Australia, ROA for all the three years are in

negative as the net income of the company for all the 3 years are in negative.

8HOTEL FINANCE AND REVENUE

Earnings per share – EPS are defined as the attributable net income to each of the

company’s common stock. It is the profitability ratio that indicates the income earned

per share by the company in specific period. It is calculated through dividing the net

income of the company by weighted average number of outstanding shares. While

analysing the company’s profitability the net income amount alone is not much useful

as it is dependent on the size of business (Hill, Jones & Schilling, 2014). Looking into

the EPS of both the companies it is observed that EPS of Qantas airline for the year

2014 was in negative as the net income of the company was negative. However, for

2015 and 2016 the EPS of the company is in positive. On the other hand, for Virgin

Australia, EPS for all the three years are in negative as the net income of the company

for all the 3 years are in negative (Prasetyorini, 2013).

Therefore, taking into consideration all the above mentioned profitability and

efficiency ratios it is recognized that the profitability position of Qantas airline is

considerable better as compared to Virgin Australia as Virgin Australia was not able to earn

positive earning for all the three years under consideration.

Activity ratios – These ratios assesses the operational efficiency of the business. It attempts to

find out the efficiency of the business to convert the inventories in sales and the sales into

cash. In other words, it is the efficiency in using the working capital and fixed assets. Key

activity ratios taken into consideration for the analysis of Qantas airline and Virgin Australia

are account receivable turnover ratio and number of days the sales in receivables.

Account receivable turnover – it is the ratio of net credit sales of business to the

average accounts receivables during the particular period, generally the accounting

year (Ch, Patel & White, 2015). It measures the efficiency of business in collecting

the credit sales. High ratio represents the favourable condition and lower figure

Earnings per share – EPS are defined as the attributable net income to each of the

company’s common stock. It is the profitability ratio that indicates the income earned

per share by the company in specific period. It is calculated through dividing the net

income of the company by weighted average number of outstanding shares. While

analysing the company’s profitability the net income amount alone is not much useful

as it is dependent on the size of business (Hill, Jones & Schilling, 2014). Looking into

the EPS of both the companies it is observed that EPS of Qantas airline for the year

2014 was in negative as the net income of the company was negative. However, for

2015 and 2016 the EPS of the company is in positive. On the other hand, for Virgin

Australia, EPS for all the three years are in negative as the net income of the company

for all the 3 years are in negative (Prasetyorini, 2013).

Therefore, taking into consideration all the above mentioned profitability and

efficiency ratios it is recognized that the profitability position of Qantas airline is

considerable better as compared to Virgin Australia as Virgin Australia was not able to earn

positive earning for all the three years under consideration.

Activity ratios – These ratios assesses the operational efficiency of the business. It attempts to

find out the efficiency of the business to convert the inventories in sales and the sales into

cash. In other words, it is the efficiency in using the working capital and fixed assets. Key

activity ratios taken into consideration for the analysis of Qantas airline and Virgin Australia

are account receivable turnover ratio and number of days the sales in receivables.

Account receivable turnover – it is the ratio of net credit sales of business to the

average accounts receivables during the particular period, generally the accounting

year (Ch, Patel & White, 2015). It measures the efficiency of business in collecting

the credit sales. High ratio represents the favourable condition and lower figure

9HOTEL FINANCE AND REVENUE

represent the inefficiency. It can be identified from the calculation that for 2014 and

2015 the receivable ratio of Virgin Australia is better as compared to Qantas.

However, for the year 2016 the receivable position of Qantas airline is better.

No. of days sales in receivables – it is used for measuring average number of days the

business takes for collecting the trade receivables after the sales made (Acito, Hogan

& Imdieke, 2015). As it is the time taken to convert the sales into cash, lower days

represent as favourable and the higher days are represented as unfavourable. It can be

identified from the calculation that for 2014 and 2015 the days outstanding of Virgin

Australia is better as compared to Qantas. However, for the year 2016 the receivable

position of Qantas airline is better Čermák, 2015).

Revenue management

As the nature of the airline business is of challenging type and requires continuous

investment for updated and new technologies, the particular area for focussing is the revenue

management (RM). The RM systems are used for determining optimum price for selling the

seat at any given point of the time (Graf & Kimms, 2013). The required information will be

able to make the decision based on various factors. For increasing the revenue –

The company shall adapt to the conditions of changing market in the real time for the

improves procedure

Leverage the demand of customers across the revenue streams for increasing the

revenue.

Improve the forecast accuracy and analyst productivity through enhancing the

decision making procedures (Board & Skrzypacz, 2016).

Enable the integration of unmatched business planning for enhancing the decision

making.

represent the inefficiency. It can be identified from the calculation that for 2014 and

2015 the receivable ratio of Virgin Australia is better as compared to Qantas.

However, for the year 2016 the receivable position of Qantas airline is better.

No. of days sales in receivables – it is used for measuring average number of days the

business takes for collecting the trade receivables after the sales made (Acito, Hogan

& Imdieke, 2015). As it is the time taken to convert the sales into cash, lower days

represent as favourable and the higher days are represented as unfavourable. It can be

identified from the calculation that for 2014 and 2015 the days outstanding of Virgin

Australia is better as compared to Qantas. However, for the year 2016 the receivable

position of Qantas airline is better Čermák, 2015).

Revenue management

As the nature of the airline business is of challenging type and requires continuous

investment for updated and new technologies, the particular area for focussing is the revenue

management (RM). The RM systems are used for determining optimum price for selling the

seat at any given point of the time (Graf & Kimms, 2013). The required information will be

able to make the decision based on various factors. For increasing the revenue –

The company shall adapt to the conditions of changing market in the real time for the

improves procedure

Leverage the demand of customers across the revenue streams for increasing the

revenue.

Improve the forecast accuracy and analyst productivity through enhancing the

decision making procedures (Board & Skrzypacz, 2016).

Enable the integration of unmatched business planning for enhancing the decision

making.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

10HOTEL FINANCE AND REVENUE

Conclusion

It is concluded from the above discussion that if the financial position and financial

performance of Qantas airline and Virgin Australia airline is taken into consideration it can

be identified that Qantas is better investment as compared to Virgin Australia. The reason

behind this is that Virgin Australia was not able to earn positive income for all the three years

under consideration. Further, if the solvency ratios and activity ratios are considered, it is

identified that Interest coverage ratio of Virgin airline for all the three years are in negative as

the company was not able to earn any positive operating income throughout all 3 years. On

the other hand, the interest coverage ratio for Qantas airline improved in 2016 as compared to

the year 2014 and 2015. The debt to equity ratio of Qantas airline is better as compared to

Virgin Australia as its debt to equity ratio is slightly lower than Virgin Australia. All the

profitability ratios of Qantas airline are better as compared to Virgin Australia. Therefore,

Qantas airline is better investment.

Conclusion

It is concluded from the above discussion that if the financial position and financial

performance of Qantas airline and Virgin Australia airline is taken into consideration it can

be identified that Qantas is better investment as compared to Virgin Australia. The reason

behind this is that Virgin Australia was not able to earn positive income for all the three years

under consideration. Further, if the solvency ratios and activity ratios are considered, it is

identified that Interest coverage ratio of Virgin airline for all the three years are in negative as

the company was not able to earn any positive operating income throughout all 3 years. On

the other hand, the interest coverage ratio for Qantas airline improved in 2016 as compared to

the year 2014 and 2015. The debt to equity ratio of Qantas airline is better as compared to

Virgin Australia as its debt to equity ratio is slightly lower than Virgin Australia. All the

profitability ratios of Qantas airline are better as compared to Virgin Australia. Therefore,

Qantas airline is better investment.

11HOTEL FINANCE AND REVENUE

Reference

Acito, A., Hogan, C., &Imdieke, A. (2015). Integrated Auditing St&ards & Financial

Reporting Quality. Working paper, Michigan State University.

Board, S., & Skrzypacz, A. (2016). Revenue management with forward-looking

buyers. Journal of Political Economy, 124(4), 1046-1087.

Brooks, R. (2015). Financial management: core concepts. Pearson

Čermák, P. (2015). Customer profitability analysis & customer life time value models:

Portfolio analysis. Procedia Economics & Finance, 25, 14-25.

Ch&, P., Patel, A. & White, M., (2015). Adopting international financial reporting st&ards

for small & medium‐sized enterprises. Australian Accounting Review, 25(2), pp.139-

154.

Drehmann, M., & Nikolaou, K. (2013). Funding liquidity risk: definition &

measurement. Journal of Banking & Finance, 37(7), 2173-2182.

Flights | Qantas AU. (2018). Qantas.com. Retrieved 13 February 2018, from

https://www.qantas.com/au/en/book-a-trip/flights.html

Graf, M., & Kimms, A. (2013). Transfer price optimization for option-based airline alliance

revenue management. International Journal of Production Economics, 145(1), 281-

293.

Grant, R.M., (2016). Contemporary strategy analysis: Text & cases edition. John Wiley &

Sons.

Reference

Acito, A., Hogan, C., &Imdieke, A. (2015). Integrated Auditing St&ards & Financial

Reporting Quality. Working paper, Michigan State University.

Board, S., & Skrzypacz, A. (2016). Revenue management with forward-looking

buyers. Journal of Political Economy, 124(4), 1046-1087.

Brooks, R. (2015). Financial management: core concepts. Pearson

Čermák, P. (2015). Customer profitability analysis & customer life time value models:

Portfolio analysis. Procedia Economics & Finance, 25, 14-25.

Ch&, P., Patel, A. & White, M., (2015). Adopting international financial reporting st&ards

for small & medium‐sized enterprises. Australian Accounting Review, 25(2), pp.139-

154.

Drehmann, M., & Nikolaou, K. (2013). Funding liquidity risk: definition &

measurement. Journal of Banking & Finance, 37(7), 2173-2182.

Flights | Qantas AU. (2018). Qantas.com. Retrieved 13 February 2018, from

https://www.qantas.com/au/en/book-a-trip/flights.html

Graf, M., & Kimms, A. (2013). Transfer price optimization for option-based airline alliance

revenue management. International Journal of Production Economics, 145(1), 281-

293.

Grant, R.M., (2016). Contemporary strategy analysis: Text & cases edition. John Wiley &

Sons.

12HOTEL FINANCE AND REVENUE

Heikal, M., Khaddafi, M., & Ummah, A. (2014). Influence analysis of return on assets

(ROA), return on equity (ROE), net profit margin (NPM), debt to equity ratio (DER),

& current ratio (CR), against corporate profit growth in automotive in Indonesia Stock

Exchange. International Journal of Academic Research in Business & Social

Sciences, 4(12), 101.

Hevert, S. R. B. (2013). Return on Equity.

Hill, C.W., Jones, G.R. & Schilling, M.A., (2014). Strategic management: theory: an

integrated approach. Cengage Learning.

Jones, C., & Kulish, M. (2013). Long-term interest rates, risk premia & unconventional

monetary policy. Journal of Economic Dynamics & Control, 37(12), 2547-2561.

Kettunen, J., (2017). Interlingual translation of the International Financial Reporting St&ards

as institutional work. Accounting, Organizations & Society, 56, pp.38-54.

Luez, C. & Wysocki, P., (2016). Economic Consequences of Financial Reporting &

Disclosure Regulation: A Review & Suggestions for Future Research. J. Acct. &

Econ., 50, p.525.

Nobes, C., (2014). International Classification of Financial Reporting 3e. Routledge.

Prasetyorini, B. F. (2013). Pengaruh ukuran perusahaan, leverage, price earning ratio dan

profitabilitas terhadap nilai perusahaan. Jurnal Ilmu Manajemen, 1(1), 183-196.

Scott, W.R., (2015). Financial accounting theory (Vol. 2, No. 0, p. 0). Prentice Hall.

Sunder, S., (2016). Rethinking financial reporting: st&ards, norms &

institutions. Foundations & Trends® in Accounting, 11(1–2), pp.1-118.

Heikal, M., Khaddafi, M., & Ummah, A. (2014). Influence analysis of return on assets

(ROA), return on equity (ROE), net profit margin (NPM), debt to equity ratio (DER),

& current ratio (CR), against corporate profit growth in automotive in Indonesia Stock

Exchange. International Journal of Academic Research in Business & Social

Sciences, 4(12), 101.

Hevert, S. R. B. (2013). Return on Equity.

Hill, C.W., Jones, G.R. & Schilling, M.A., (2014). Strategic management: theory: an

integrated approach. Cengage Learning.

Jones, C., & Kulish, M. (2013). Long-term interest rates, risk premia & unconventional

monetary policy. Journal of Economic Dynamics & Control, 37(12), 2547-2561.

Kettunen, J., (2017). Interlingual translation of the International Financial Reporting St&ards

as institutional work. Accounting, Organizations & Society, 56, pp.38-54.

Luez, C. & Wysocki, P., (2016). Economic Consequences of Financial Reporting &

Disclosure Regulation: A Review & Suggestions for Future Research. J. Acct. &

Econ., 50, p.525.

Nobes, C., (2014). International Classification of Financial Reporting 3e. Routledge.

Prasetyorini, B. F. (2013). Pengaruh ukuran perusahaan, leverage, price earning ratio dan

profitabilitas terhadap nilai perusahaan. Jurnal Ilmu Manajemen, 1(1), 183-196.

Scott, W.R., (2015). Financial accounting theory (Vol. 2, No. 0, p. 0). Prentice Hall.

Sunder, S., (2016). Rethinking financial reporting: st&ards, norms &

institutions. Foundations & Trends® in Accounting, 11(1–2), pp.1-118.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

13HOTEL FINANCE AND REVENUE

Virgin Australia | Home. (2018). Mobile.virginaustralia.com. Retrieved 13 February 2018,

from https://mobile.virginaustralia.com/virginaustralia/index.html

Virgin Australia | Home. (2018). Mobile.virginaustralia.com. Retrieved 13 February 2018,

from https://mobile.virginaustralia.com/virginaustralia/index.html

1 out of 14

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.