ACCT20075 Auditing: A Financial Analysis of Harvey Norman Limited

VerifiedAdded on 2022/12/23

|10

|2441

|1

Report

AI Summary

This report presents a financial analysis of Harvey Norman Limited, focusing on the company's audit assessment. It covers materiality quantification using gross profit, equity levels, total assets, and net profits, along with a review of the company’s disclosures and draft notes from the annual financial reports. The analysis includes a review of the firm’s financial ratios and their trends over the past four years, alongside considerations of audit assertions and procedures. Specific attention is given to the balance sheets and profit & loss statements, highlighting key accounts that require further scrutiny. The report also discusses the company's cash flows, including operating, investing, and financing activities, and reviews the audit report provided by Ernst & Young, emphasizing adherence to accounting standards and key audit matters such as the recoverability of receivables and investment property valuation. The analysis concludes with an overall assessment of Harvey Norman’s financial performance, noting improvements in profitability and solvency while suggesting areas for further enhancement.

Running Head: HVN AUDIT ANALYSIS 1

Harvey Norman Limited Company Audit Assessment

Name

Institution

Harvey Norman Limited Company Audit Assessment

Name

Institution

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

HVN Audit Analysis 2

Background

Actually, this financial, analysis report is intended for the Harvey Norman Company which is

a reputable company in Australia. It’s a multi-national retail entity that provides furniture,

computers, and customer products linked to electrical gadgets and many more. The main

objectivity of the reports creation if assisting the company’s audit and evaluation of the

company’s materiality, which will be effective for auditors in assessing vital financial

accounts utilizing precise quantifiable materiality approximation techniques. Moreover, other

detailed data on the company’s disclosures highlighted in the annual financial reports have

been critically assessed taking into account the major issues based on the auditing

perspectives (ACCC. 2011). Consequently, there will be a concise review of the firm’s ratios

and its trend in variance where data from the last 4 years were computed. Hence,

consideration of accurate audit assertions and the audit procedures have also been included in

the report. Lastly, the report will specifically highlight on the balance sheets, and profit &

loss account statements, pointing out if there is an acute account which must be pointed out

(CARTWRIGHT, 2012).

Discussion and Analysis

Thus the company in our topic discussion is Harvey Norman limited operating in Australia.

Moreover, the company operates HVN including other branded stores within the Australian,

Singapore, New Zealand, Slovenia, Singapore, Ireland, and Croatia. Thus section

incorporated revenue acquired through the company’s franchise business. The company is

currently the largest retailer in provision of computer hardware, furniture and other products.

Consequently, the company takes hold of portfolio assets investments that entice rental

income based from the third parties and the franchise business. Additionally, HVN comprises

of 5420 employees and ranked as number 124 amid 2000 firms in Australia. Most of the

company’s income comes from the store-based retail business.

Background

Actually, this financial, analysis report is intended for the Harvey Norman Company which is

a reputable company in Australia. It’s a multi-national retail entity that provides furniture,

computers, and customer products linked to electrical gadgets and many more. The main

objectivity of the reports creation if assisting the company’s audit and evaluation of the

company’s materiality, which will be effective for auditors in assessing vital financial

accounts utilizing precise quantifiable materiality approximation techniques. Moreover, other

detailed data on the company’s disclosures highlighted in the annual financial reports have

been critically assessed taking into account the major issues based on the auditing

perspectives (ACCC. 2011). Consequently, there will be a concise review of the firm’s ratios

and its trend in variance where data from the last 4 years were computed. Hence,

consideration of accurate audit assertions and the audit procedures have also been included in

the report. Lastly, the report will specifically highlight on the balance sheets, and profit &

loss account statements, pointing out if there is an acute account which must be pointed out

(CARTWRIGHT, 2012).

Discussion and Analysis

Thus the company in our topic discussion is Harvey Norman limited operating in Australia.

Moreover, the company operates HVN including other branded stores within the Australian,

Singapore, New Zealand, Slovenia, Singapore, Ireland, and Croatia. Thus section

incorporated revenue acquired through the company’s franchise business. The company is

currently the largest retailer in provision of computer hardware, furniture and other products.

Consequently, the company takes hold of portfolio assets investments that entice rental

income based from the third parties and the franchise business. Additionally, HVN comprises

of 5420 employees and ranked as number 124 amid 2000 firms in Australia. Most of the

company’s income comes from the store-based retail business.

HVN Audit Analysis 3

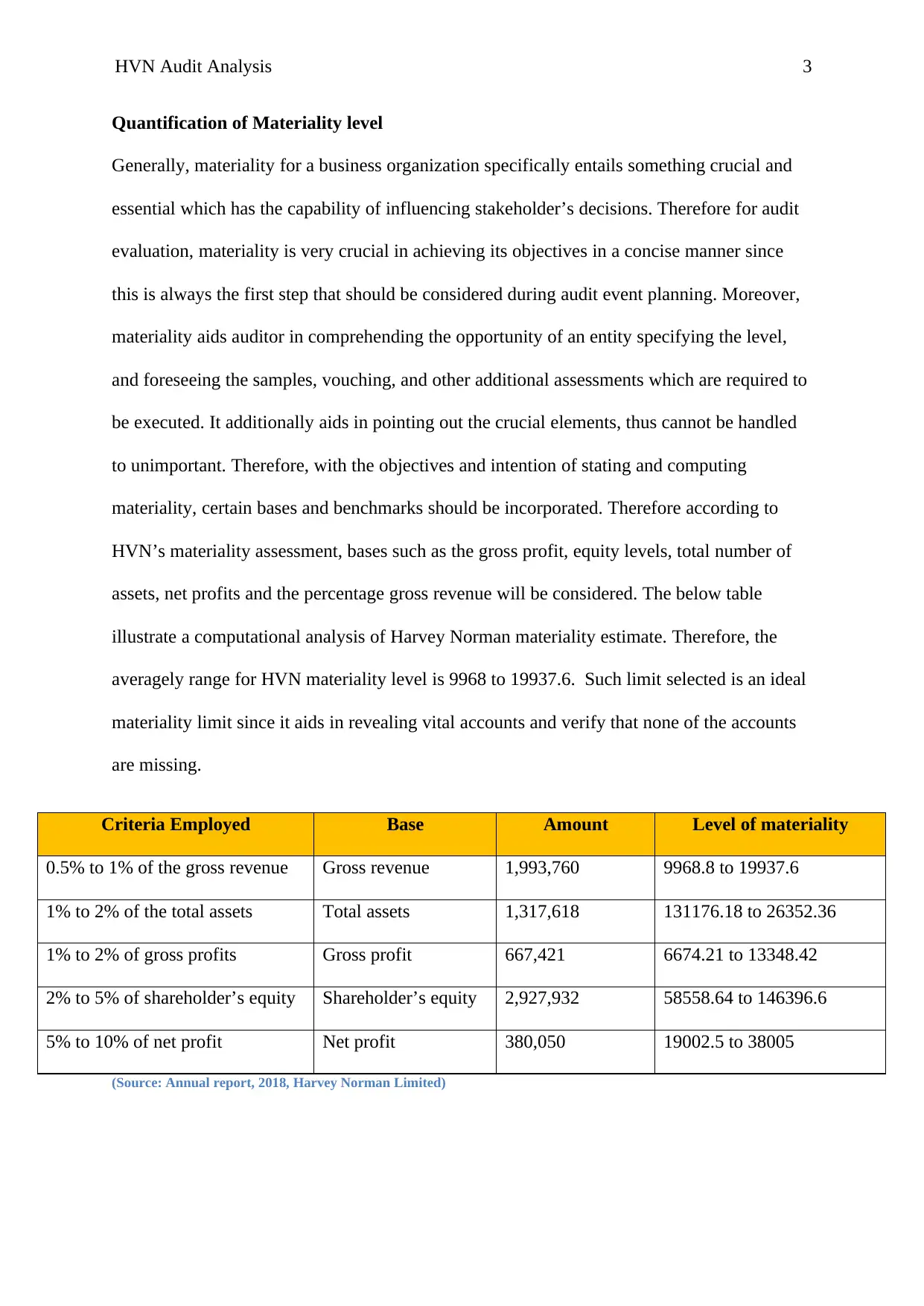

Quantification of Materiality level

Generally, materiality for a business organization specifically entails something crucial and

essential which has the capability of influencing stakeholder’s decisions. Therefore for audit

evaluation, materiality is very crucial in achieving its objectives in a concise manner since

this is always the first step that should be considered during audit event planning. Moreover,

materiality aids auditor in comprehending the opportunity of an entity specifying the level,

and foreseeing the samples, vouching, and other additional assessments which are required to

be executed. It additionally aids in pointing out the crucial elements, thus cannot be handled

to unimportant. Therefore, with the objectives and intention of stating and computing

materiality, certain bases and benchmarks should be incorporated. Therefore according to

HVN’s materiality assessment, bases such as the gross profit, equity levels, total number of

assets, net profits and the percentage gross revenue will be considered. The below table

illustrate a computational analysis of Harvey Norman materiality estimate. Therefore, the

averagely range for HVN materiality level is 9968 to 19937.6. Such limit selected is an ideal

materiality limit since it aids in revealing vital accounts and verify that none of the accounts

are missing.

Criteria Employed Base Amount Level of materiality

0.5% to 1% of the gross revenue Gross revenue 1,993,760 9968.8 to 19937.6

1% to 2% of the total assets Total assets 1,317,618 131176.18 to 26352.36

1% to 2% of gross profits Gross profit 667,421 6674.21 to 13348.42

2% to 5% of shareholder’s equity Shareholder’s equity 2,927,932 58558.64 to 146396.6

5% to 10% of net profit Net profit 380,050 19002.5 to 38005

(Source: Annual report, 2018, Harvey Norman Limited)

Quantification of Materiality level

Generally, materiality for a business organization specifically entails something crucial and

essential which has the capability of influencing stakeholder’s decisions. Therefore for audit

evaluation, materiality is very crucial in achieving its objectives in a concise manner since

this is always the first step that should be considered during audit event planning. Moreover,

materiality aids auditor in comprehending the opportunity of an entity specifying the level,

and foreseeing the samples, vouching, and other additional assessments which are required to

be executed. It additionally aids in pointing out the crucial elements, thus cannot be handled

to unimportant. Therefore, with the objectives and intention of stating and computing

materiality, certain bases and benchmarks should be incorporated. Therefore according to

HVN’s materiality assessment, bases such as the gross profit, equity levels, total number of

assets, net profits and the percentage gross revenue will be considered. The below table

illustrate a computational analysis of Harvey Norman materiality estimate. Therefore, the

averagely range for HVN materiality level is 9968 to 19937.6. Such limit selected is an ideal

materiality limit since it aids in revealing vital accounts and verify that none of the accounts

are missing.

Criteria Employed Base Amount Level of materiality

0.5% to 1% of the gross revenue Gross revenue 1,993,760 9968.8 to 19937.6

1% to 2% of the total assets Total assets 1,317,618 131176.18 to 26352.36

1% to 2% of gross profits Gross profit 667,421 6674.21 to 13348.42

2% to 5% of shareholder’s equity Shareholder’s equity 2,927,932 58558.64 to 146396.6

5% to 10% of net profit Net profit 380,050 19002.5 to 38005

(Source: Annual report, 2018, Harvey Norman Limited)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

HVN Audit Analysis 4

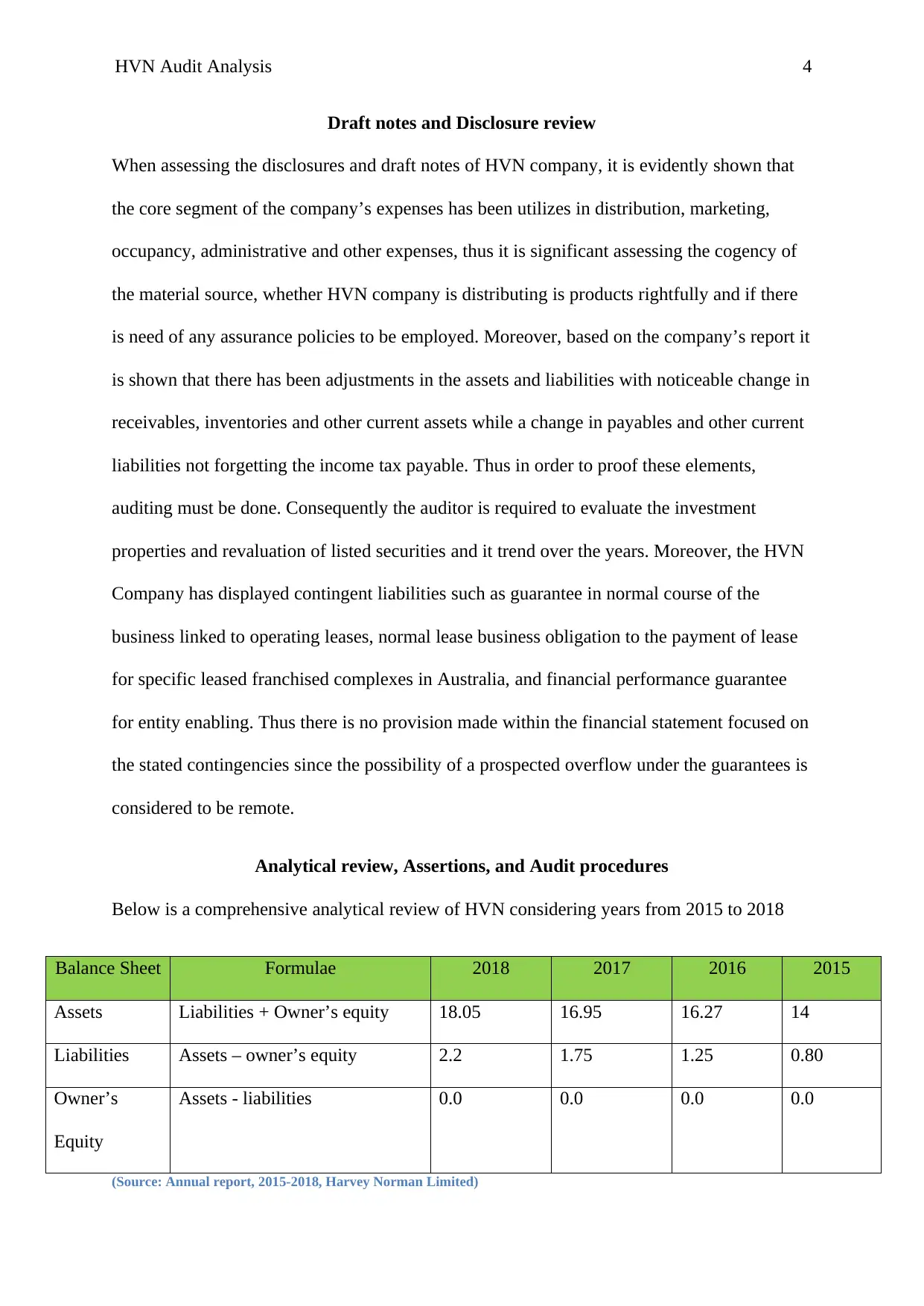

Draft notes and Disclosure review

When assessing the disclosures and draft notes of HVN company, it is evidently shown that

the core segment of the company’s expenses has been utilizes in distribution, marketing,

occupancy, administrative and other expenses, thus it is significant assessing the cogency of

the material source, whether HVN company is distributing is products rightfully and if there

is need of any assurance policies to be employed. Moreover, based on the company’s report it

is shown that there has been adjustments in the assets and liabilities with noticeable change in

receivables, inventories and other current assets while a change in payables and other current

liabilities not forgetting the income tax payable. Thus in order to proof these elements,

auditing must be done. Consequently the auditor is required to evaluate the investment

properties and revaluation of listed securities and it trend over the years. Moreover, the HVN

Company has displayed contingent liabilities such as guarantee in normal course of the

business linked to operating leases, normal lease business obligation to the payment of lease

for specific leased franchised complexes in Australia, and financial performance guarantee

for entity enabling. Thus there is no provision made within the financial statement focused on

the stated contingencies since the possibility of a prospected overflow under the guarantees is

considered to be remote.

Analytical review, Assertions, and Audit procedures

Below is a comprehensive analytical review of HVN considering years from 2015 to 2018

Balance Sheet Formulae 2018 2017 2016 2015

Assets Liabilities + Owner’s equity 18.05 16.95 16.27 14

Liabilities Assets – owner’s equity 2.2 1.75 1.25 0.80

Owner’s

Equity

Assets - liabilities 0.0 0.0 0.0 0.0

(Source: Annual report, 2015-2018, Harvey Norman Limited)

Draft notes and Disclosure review

When assessing the disclosures and draft notes of HVN company, it is evidently shown that

the core segment of the company’s expenses has been utilizes in distribution, marketing,

occupancy, administrative and other expenses, thus it is significant assessing the cogency of

the material source, whether HVN company is distributing is products rightfully and if there

is need of any assurance policies to be employed. Moreover, based on the company’s report it

is shown that there has been adjustments in the assets and liabilities with noticeable change in

receivables, inventories and other current assets while a change in payables and other current

liabilities not forgetting the income tax payable. Thus in order to proof these elements,

auditing must be done. Consequently the auditor is required to evaluate the investment

properties and revaluation of listed securities and it trend over the years. Moreover, the HVN

Company has displayed contingent liabilities such as guarantee in normal course of the

business linked to operating leases, normal lease business obligation to the payment of lease

for specific leased franchised complexes in Australia, and financial performance guarantee

for entity enabling. Thus there is no provision made within the financial statement focused on

the stated contingencies since the possibility of a prospected overflow under the guarantees is

considered to be remote.

Analytical review, Assertions, and Audit procedures

Below is a comprehensive analytical review of HVN considering years from 2015 to 2018

Balance Sheet Formulae 2018 2017 2016 2015

Assets Liabilities + Owner’s equity 18.05 16.95 16.27 14

Liabilities Assets – owner’s equity 2.2 1.75 1.25 0.80

Owner’s

Equity

Assets - liabilities 0.0 0.0 0.0 0.0

(Source: Annual report, 2015-2018, Harvey Norman Limited)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

HVN Audit Analysis 5

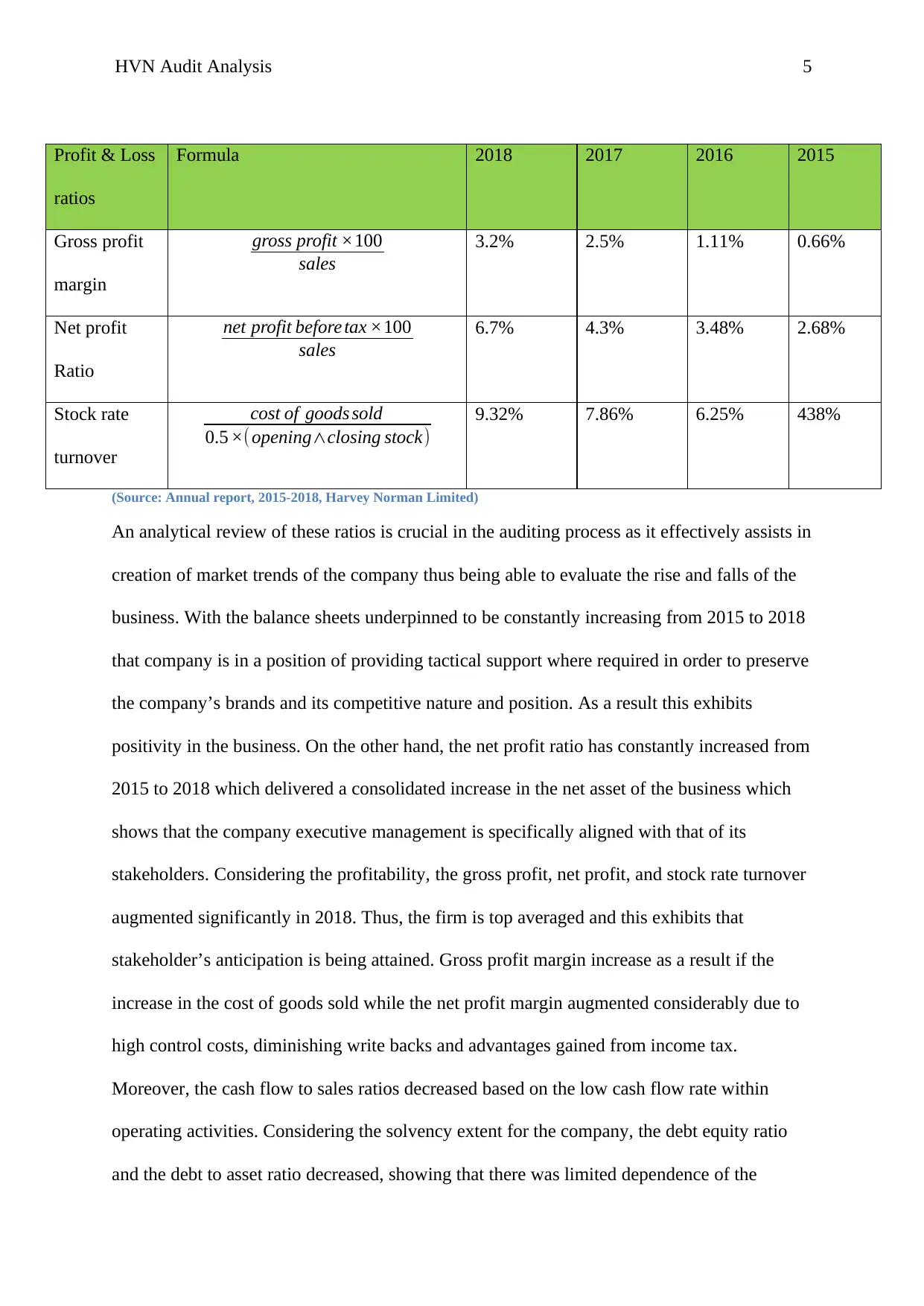

Profit & Loss

ratios

Formula 2018 2017 2016 2015

Gross profit

margin

gross profit ×100

sales

3.2% 2.5% 1.11% 0.66%

Net profit

Ratio

net profit before tax ×100

sales

6.7% 4.3% 3.48% 2.68%

Stock rate

turnover

cost of goods sold

0.5 ×( opening∧closing stock)

9.32% 7.86% 6.25% 438%

(Source: Annual report, 2015-2018, Harvey Norman Limited)

An analytical review of these ratios is crucial in the auditing process as it effectively assists in

creation of market trends of the company thus being able to evaluate the rise and falls of the

business. With the balance sheets underpinned to be constantly increasing from 2015 to 2018

that company is in a position of providing tactical support where required in order to preserve

the company’s brands and its competitive nature and position. As a result this exhibits

positivity in the business. On the other hand, the net profit ratio has constantly increased from

2015 to 2018 which delivered a consolidated increase in the net asset of the business which

shows that the company executive management is specifically aligned with that of its

stakeholders. Considering the profitability, the gross profit, net profit, and stock rate turnover

augmented significantly in 2018. Thus, the firm is top averaged and this exhibits that

stakeholder’s anticipation is being attained. Gross profit margin increase as a result if the

increase in the cost of goods sold while the net profit margin augmented considerably due to

high control costs, diminishing write backs and advantages gained from income tax.

Moreover, the cash flow to sales ratios decreased based on the low cash flow rate within

operating activities. Considering the solvency extent for the company, the debt equity ratio

and the debt to asset ratio decreased, showing that there was limited dependence of the

Profit & Loss

ratios

Formula 2018 2017 2016 2015

Gross profit

margin

gross profit ×100

sales

3.2% 2.5% 1.11% 0.66%

Net profit

Ratio

net profit before tax ×100

sales

6.7% 4.3% 3.48% 2.68%

Stock rate

turnover

cost of goods sold

0.5 ×( opening∧closing stock)

9.32% 7.86% 6.25% 438%

(Source: Annual report, 2015-2018, Harvey Norman Limited)

An analytical review of these ratios is crucial in the auditing process as it effectively assists in

creation of market trends of the company thus being able to evaluate the rise and falls of the

business. With the balance sheets underpinned to be constantly increasing from 2015 to 2018

that company is in a position of providing tactical support where required in order to preserve

the company’s brands and its competitive nature and position. As a result this exhibits

positivity in the business. On the other hand, the net profit ratio has constantly increased from

2015 to 2018 which delivered a consolidated increase in the net asset of the business which

shows that the company executive management is specifically aligned with that of its

stakeholders. Considering the profitability, the gross profit, net profit, and stock rate turnover

augmented significantly in 2018. Thus, the firm is top averaged and this exhibits that

stakeholder’s anticipation is being attained. Gross profit margin increase as a result if the

increase in the cost of goods sold while the net profit margin augmented considerably due to

high control costs, diminishing write backs and advantages gained from income tax.

Moreover, the cash flow to sales ratios decreased based on the low cash flow rate within

operating activities. Considering the solvency extent for the company, the debt equity ratio

and the debt to asset ratio decreased, showing that there was limited dependence of the

HVN Audit Analysis 6

company on the debt capital thus a positive implication for the company’s success. Moreover

the company capital management is assessed through the debt to equity ratio

(borrowings/total equity). Thus the targeted consolidated entity’s debt to equity ratio is

effectively tolerated up to 50%. Based on the company’s efficiency, the inventories, payables,

and receivables, increased or decreased with limited changes done. Hence, HVN Company

should work on the inventories and supply chain management so that the efficiency of each

franchise within the supply chain in line with the clients service standards entirely within

three years.

Assertions and Audit procedures

Important assertions made by the company managerial team that are exhibited in the report

were majorly focused on the cut-off dates stating the transaction carried out. This is so as the

company is engaged in franchise business operations. Therefore, the auditor should employ

effective auditing tests in order to assess the validity of the stated claims. Moreover, valuation

as an assertion is significant as all assets, liabilities, and the equity balances should be

recorded using an effective valuation which avoids inconveniences. There is equal

duplication of disclosure assertions and presentation. This is essential in auditing as a sole

assertion can significantly alter the quality of the report and thus this should be prioritized by

an auditor utilizing vast analytical tools.

Analysis of Cash flows

Pleasingly, the company’s cash flows increased which included cash and cash equivalent

increased by $90.32M which was majorly contributed by the operating activities and net

cash flows and the primarily increase in the net receipts. On the other hand, the cash outflows

basically came from the net cash financing activities which constantly diminished due to

consecutive borrowing of syndicated facilities in funding various acquisitions and

refurbishment of investment properties, and equipment assets. On the other hand, the

company on the debt capital thus a positive implication for the company’s success. Moreover

the company capital management is assessed through the debt to equity ratio

(borrowings/total equity). Thus the targeted consolidated entity’s debt to equity ratio is

effectively tolerated up to 50%. Based on the company’s efficiency, the inventories, payables,

and receivables, increased or decreased with limited changes done. Hence, HVN Company

should work on the inventories and supply chain management so that the efficiency of each

franchise within the supply chain in line with the clients service standards entirely within

three years.

Assertions and Audit procedures

Important assertions made by the company managerial team that are exhibited in the report

were majorly focused on the cut-off dates stating the transaction carried out. This is so as the

company is engaged in franchise business operations. Therefore, the auditor should employ

effective auditing tests in order to assess the validity of the stated claims. Moreover, valuation

as an assertion is significant as all assets, liabilities, and the equity balances should be

recorded using an effective valuation which avoids inconveniences. There is equal

duplication of disclosure assertions and presentation. This is essential in auditing as a sole

assertion can significantly alter the quality of the report and thus this should be prioritized by

an auditor utilizing vast analytical tools.

Analysis of Cash flows

Pleasingly, the company’s cash flows increased which included cash and cash equivalent

increased by $90.32M which was majorly contributed by the operating activities and net

cash flows and the primarily increase in the net receipts. On the other hand, the cash outflows

basically came from the net cash financing activities which constantly diminished due to

consecutive borrowing of syndicated facilities in funding various acquisitions and

refurbishment of investment properties, and equipment assets. On the other hand, the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

HVN Audit Analysis 7

principal cradle for the cash receipt was from franchises which in turn have decreased due to

mobility of aggregate amount of financial accommodation issued by the franchise business

(HVN. 2012c). This decrease was accompanied by the decrease in inventory reserves held by

the franchise business. Thus the major cash line products relating to investment and financial

activities were included property plant and equipment, payment of purchase of units in unit’s

trusts, and payment to purchase of equity accounted investments. The evidence of impairment

may include indicators in which the debtor or rather a group of debtors has been encountering

financial challenge, default, or delinquency of interest or core payment that they will be

insolvent (COMMONWEALTH, 2010). Operating activity cash flow shows that supplier and

employee payment has been enhanced unlike the customer receipt. Due to the fact that

operating activities is on the rise it is prospected that the company is on a going concern

which shows that the company is on the right track.

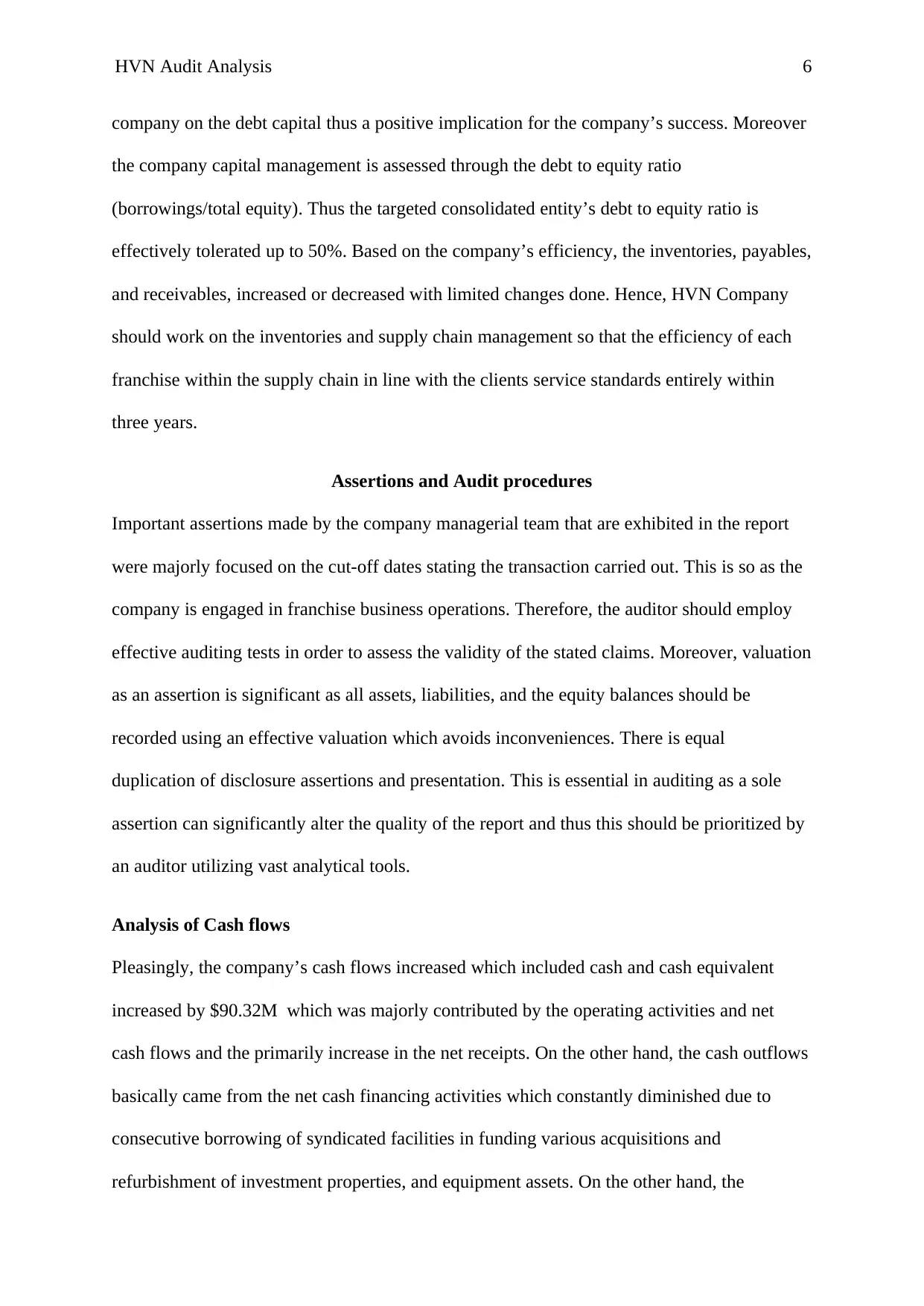

Review of HVN Company Audit Report

The auditor of the HVN’s Company audit report is Ernst & Young, as they provide

consolidated data of the financial position of the company. Moreover, they have highlighted

the trends in equity and cash flows for the year ended 30 June 2018. Important accounting

rules and policies have been highlighted and the director’s declaration. Thus the entire audit

report is in adherence with the corporation’s act of 2001 which include:

Providing precise and equitable outline of consolidated financial position of a group

for the year ended 30 June 2018 and alongside its financial performance

Adhering to the Australian Accounting Standards (AAS) and the Corporation

regulations 2001

principal cradle for the cash receipt was from franchises which in turn have decreased due to

mobility of aggregate amount of financial accommodation issued by the franchise business

(HVN. 2012c). This decrease was accompanied by the decrease in inventory reserves held by

the franchise business. Thus the major cash line products relating to investment and financial

activities were included property plant and equipment, payment of purchase of units in unit’s

trusts, and payment to purchase of equity accounted investments. The evidence of impairment

may include indicators in which the debtor or rather a group of debtors has been encountering

financial challenge, default, or delinquency of interest or core payment that they will be

insolvent (COMMONWEALTH, 2010). Operating activity cash flow shows that supplier and

employee payment has been enhanced unlike the customer receipt. Due to the fact that

operating activities is on the rise it is prospected that the company is on a going concern

which shows that the company is on the right track.

Review of HVN Company Audit Report

The auditor of the HVN’s Company audit report is Ernst & Young, as they provide

consolidated data of the financial position of the company. Moreover, they have highlighted

the trends in equity and cash flows for the year ended 30 June 2018. Important accounting

rules and policies have been highlighted and the director’s declaration. Thus the entire audit

report is in adherence with the corporation’s act of 2001 which include:

Providing precise and equitable outline of consolidated financial position of a group

for the year ended 30 June 2018 and alongside its financial performance

Adhering to the Australian Accounting Standards (AAS) and the Corporation

regulations 2001

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

HVN Audit Analysis 8

(Source: Annual report, 2018, Harvey Norman Limited)

Therefore the major opinion reflected in this audit is that key financial rules and regulations

have been adhered to thus making it logical and investors can take hold of that. Moreover, as

stated in the report that the company is an independent group, they follow ethical procedures;

it is efficient as it increases the company’s repute. Subsequently, various crucial segments

whereby the auditors used additional steps in explaining the rationale are shown below. They

are also included in the key audit issues, they include:

(Source: Annual report, 2018, Harvey Norman Limited)

Therefore the major opinion reflected in this audit is that key financial rules and regulations

have been adhered to thus making it logical and investors can take hold of that. Moreover, as

stated in the report that the company is an independent group, they follow ethical procedures;

it is efficient as it increases the company’s repute. Subsequently, various crucial segments

whereby the auditors used additional steps in explaining the rationale are shown below. They

are also included in the key audit issues, they include:

HVN Audit Analysis 9

Recoverability of receivables from franchises – recoverable are essential to the group, this

was a key audit matter provided the value of the matter and the prospected judgement

implemented by the group.

Investment property valuation and owner occupied assets – various asset samples were

collected which was subject to internal valuation during the period. Moreover, the use of

director’s nature was effective. Moreover there was consideration of different disclosures

which included note 1, note 14 and note 15 of the financial report.

Conclusion

In this paper, extensive analytical review has been executed focusing on Harvey Norman

Company, and thus it is prospected that the company’s performance is top notch. This was

accomplished by careful consideration of materiality, cash flows, balance sheets, and profit

and loss statements. Generally, the company enhanced ominously in the aspect of

profitability and solvency although there should be improvements on the profit and loss

ratios. Also the cash receipt and the audit report was also assessed in the paper.

Recoverability of receivables from franchises – recoverable are essential to the group, this

was a key audit matter provided the value of the matter and the prospected judgement

implemented by the group.

Investment property valuation and owner occupied assets – various asset samples were

collected which was subject to internal valuation during the period. Moreover, the use of

director’s nature was effective. Moreover there was consideration of different disclosures

which included note 1, note 14 and note 15 of the financial report.

Conclusion

In this paper, extensive analytical review has been executed focusing on Harvey Norman

Company, and thus it is prospected that the company’s performance is top notch. This was

accomplished by careful consideration of materiality, cash flows, balance sheets, and profit

and loss statements. Generally, the company enhanced ominously in the aspect of

profitability and solvency although there should be improvements on the profit and loss

ratios. Also the cash receipt and the audit report was also assessed in the paper.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

HVN Audit Analysis

10

Reference

ACCC. 2011. Harvey Norman holdings ltd penalized $1.25 million for misleading

advertising [Online]. Available: http://www.accc.gov.au/media-release/harvey-norman-

holdings-ltd-penalised-125-million-for-misleading-advertising [Accessed 22 April

2013].

Annual Report, 2015, Harvey Norman Company Limited

Annual Report, 2016, Harvey Norman Company Limited

Annual Report, 2017, Harvey Norman Company Limited

Annual Report, 2018, Harvey Norman Company Limited

CARTWRIGHT, M. 2012. CHOICE research exposes price discrimination [Online].

Available: http://www.choice.com.au/media-and-news/consumer-news/news/choice-

lodges-submission-on-it-price-discrimination.aspx [Accessed 1 May 2013].

COMMONWEALTH. 2010. Competition and Consumer Act 2010 [Online]. Available:

http://www.comlaw.gov.au/Details/C2011C00003 [Accessed 20 April 2013].

HVN. 2012c. 2012 HVN Annual Report [Online]. Available:

http://www.harveynormanholdings.com.au/pdf_files/2012_Annual_Report_Final.pdf

[Accessed 3 May 2013].

10

Reference

ACCC. 2011. Harvey Norman holdings ltd penalized $1.25 million for misleading

advertising [Online]. Available: http://www.accc.gov.au/media-release/harvey-norman-

holdings-ltd-penalised-125-million-for-misleading-advertising [Accessed 22 April

2013].

Annual Report, 2015, Harvey Norman Company Limited

Annual Report, 2016, Harvey Norman Company Limited

Annual Report, 2017, Harvey Norman Company Limited

Annual Report, 2018, Harvey Norman Company Limited

CARTWRIGHT, M. 2012. CHOICE research exposes price discrimination [Online].

Available: http://www.choice.com.au/media-and-news/consumer-news/news/choice-

lodges-submission-on-it-price-discrimination.aspx [Accessed 1 May 2013].

COMMONWEALTH. 2010. Competition and Consumer Act 2010 [Online]. Available:

http://www.comlaw.gov.au/Details/C2011C00003 [Accessed 20 April 2013].

HVN. 2012c. 2012 HVN Annual Report [Online]. Available:

http://www.harveynormanholdings.com.au/pdf_files/2012_Annual_Report_Final.pdf

[Accessed 3 May 2013].

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.