University Finance Report: Hypothesis Testing and Portfolio Analysis

VerifiedAdded on 2023/03/23

|21

|3495

|39

Report

AI Summary

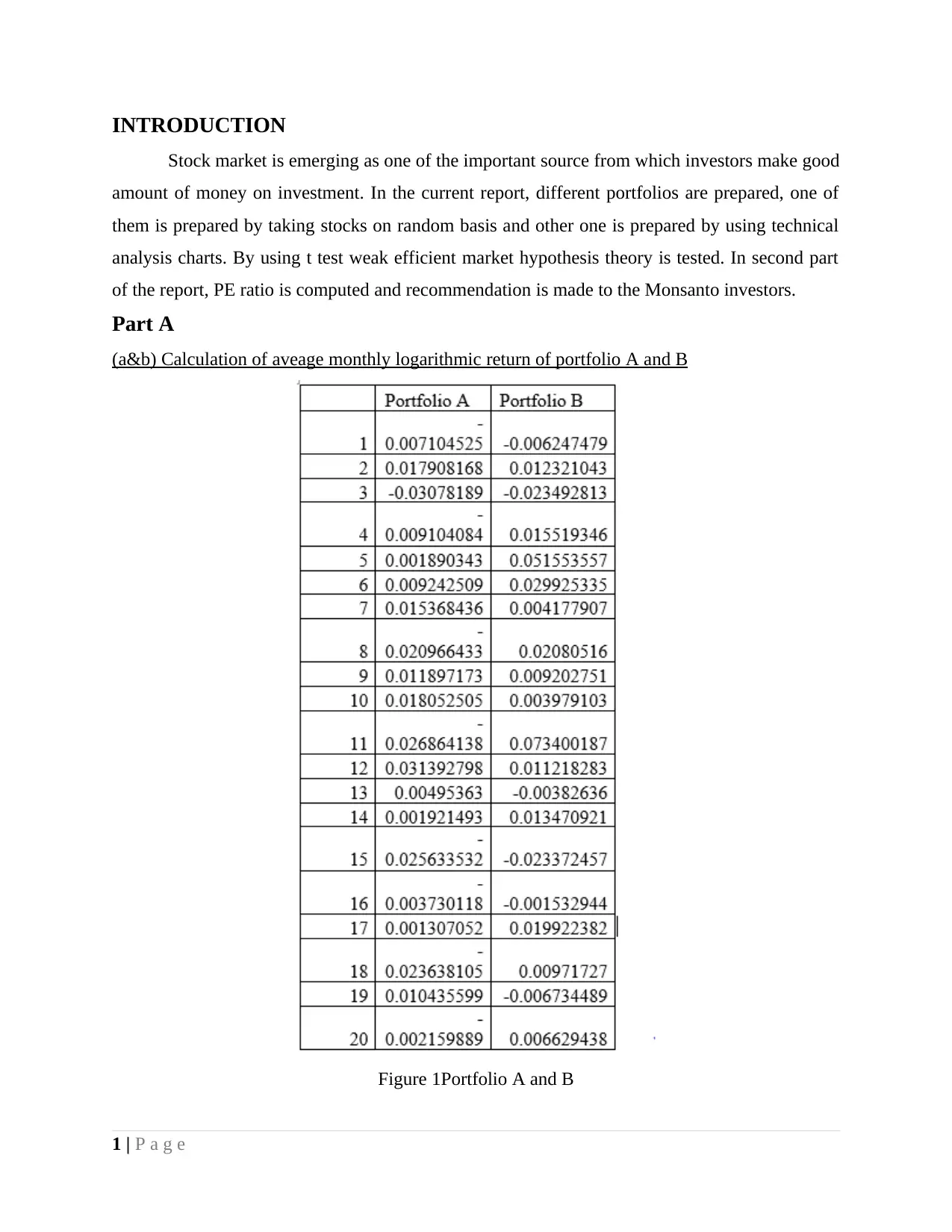

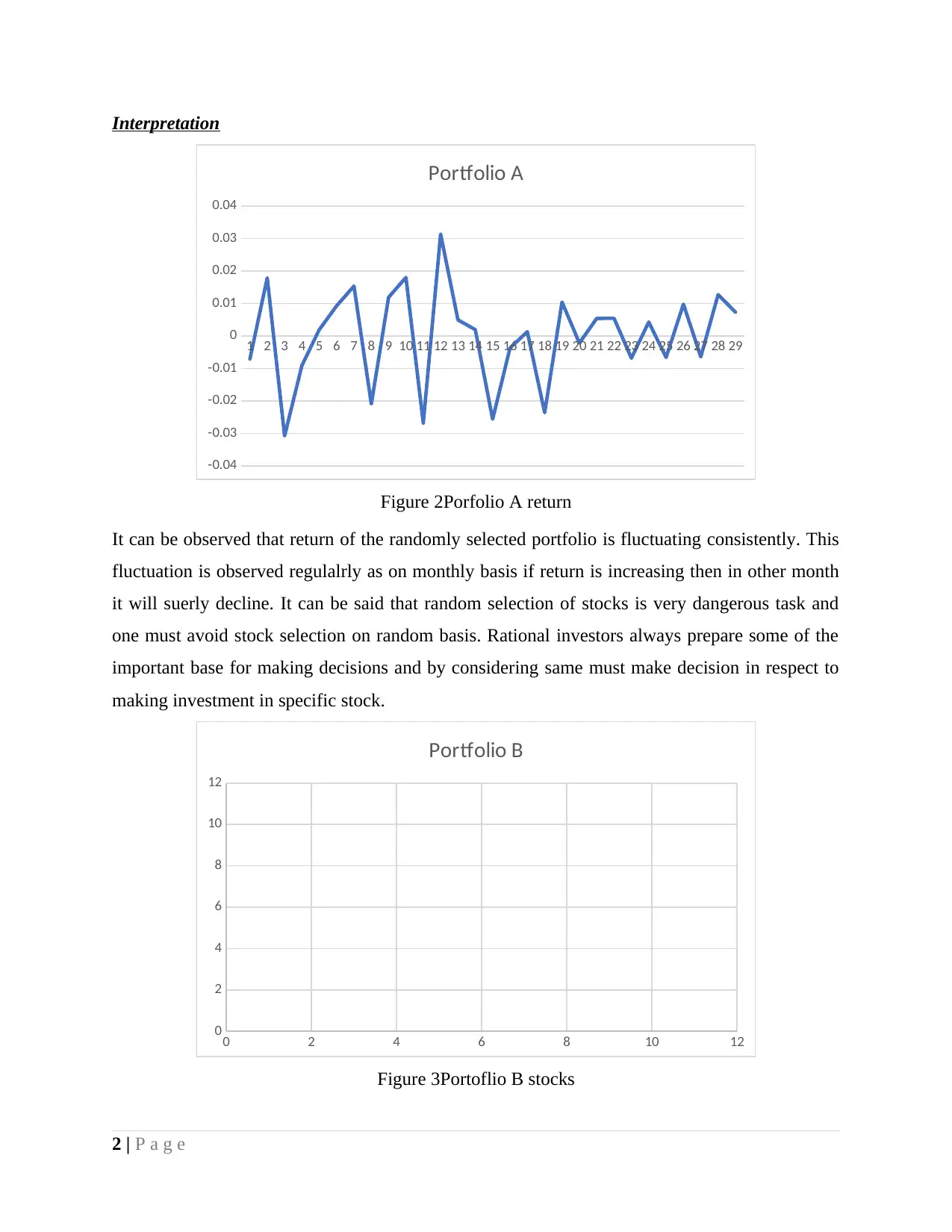

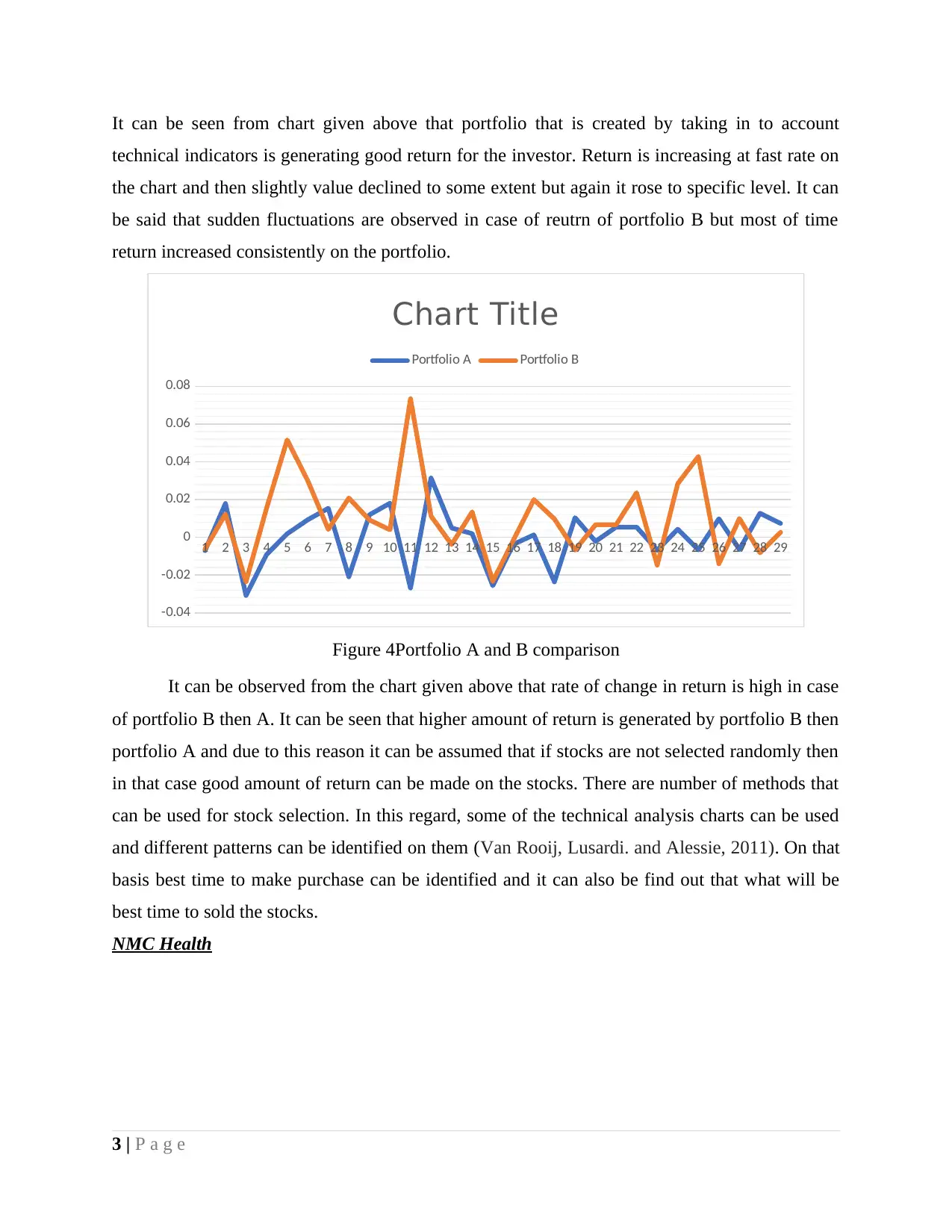

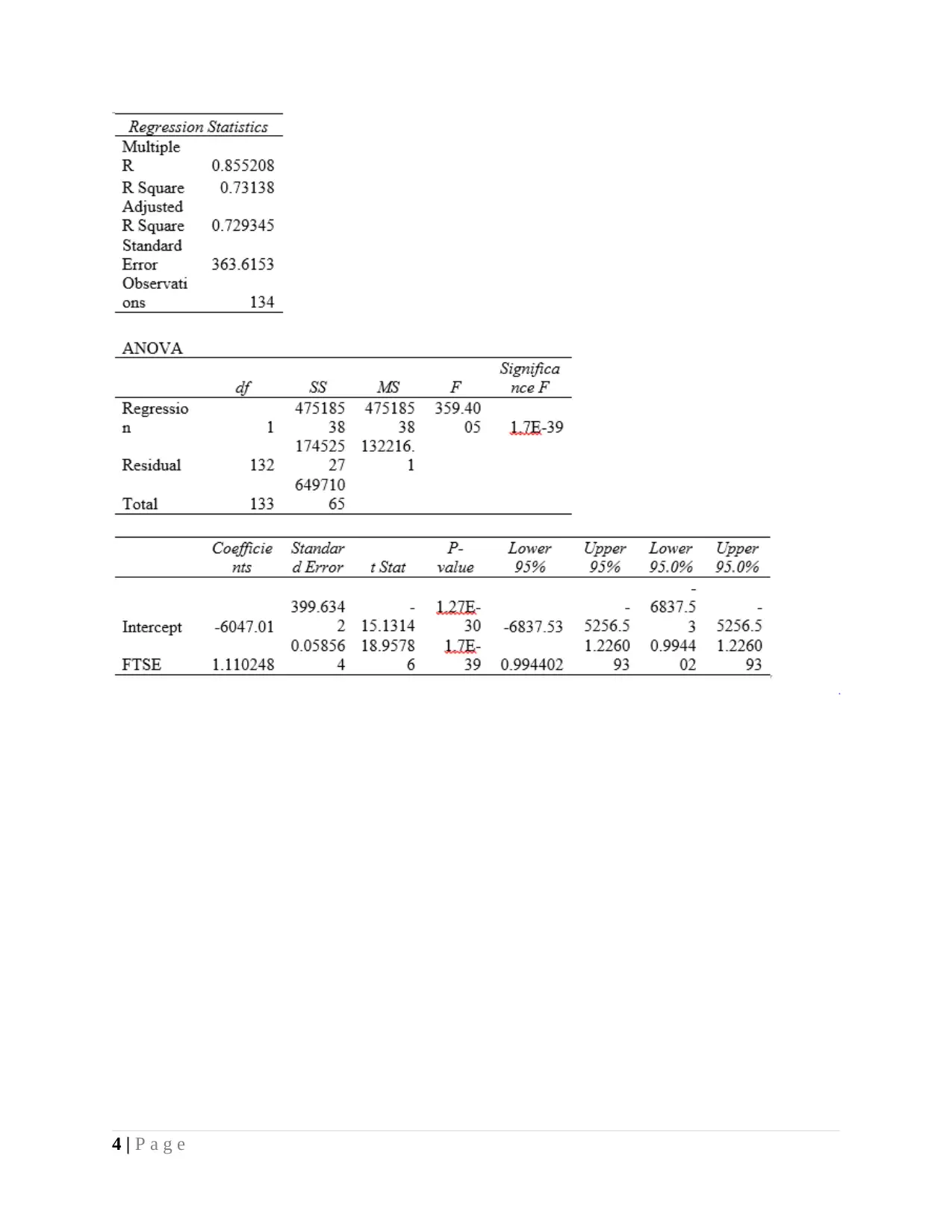

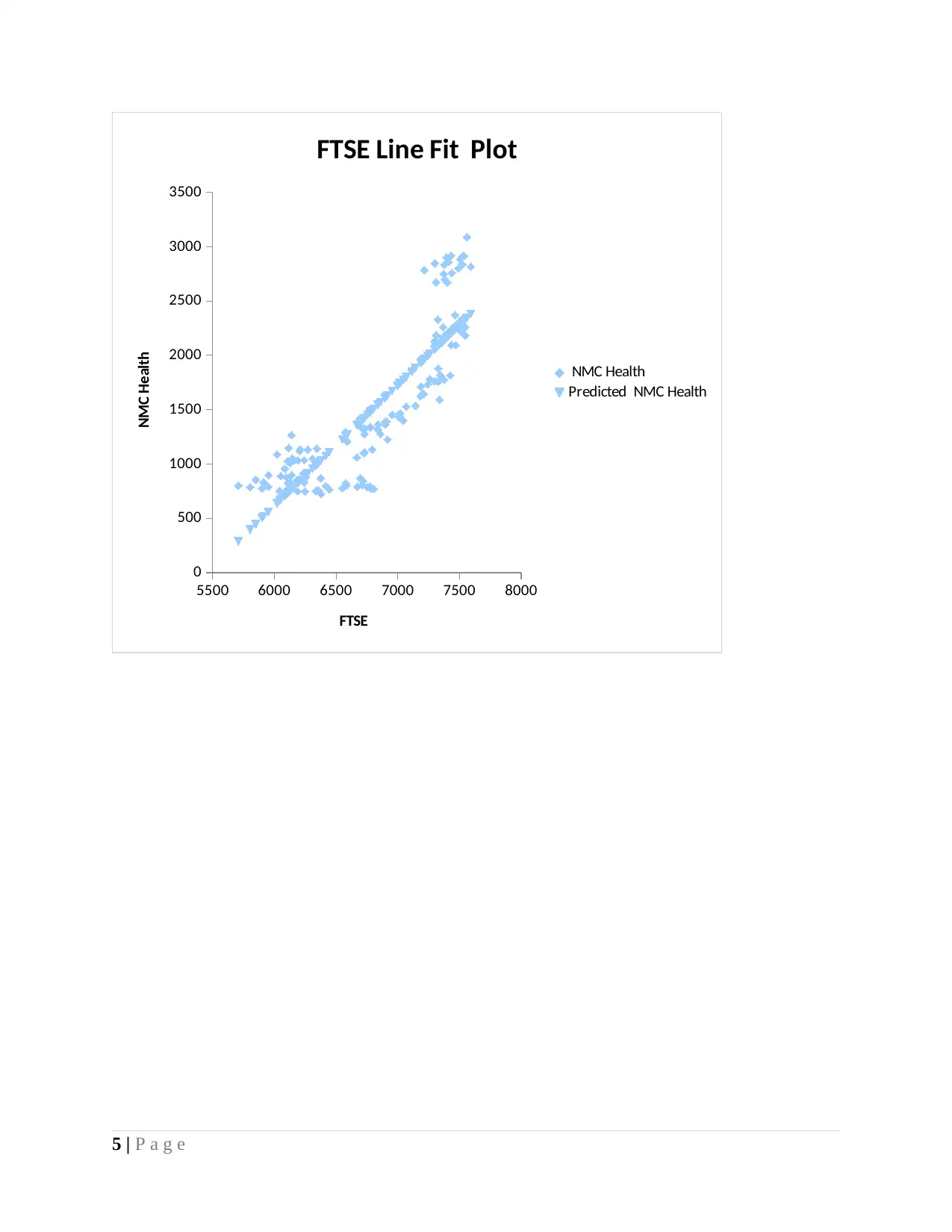

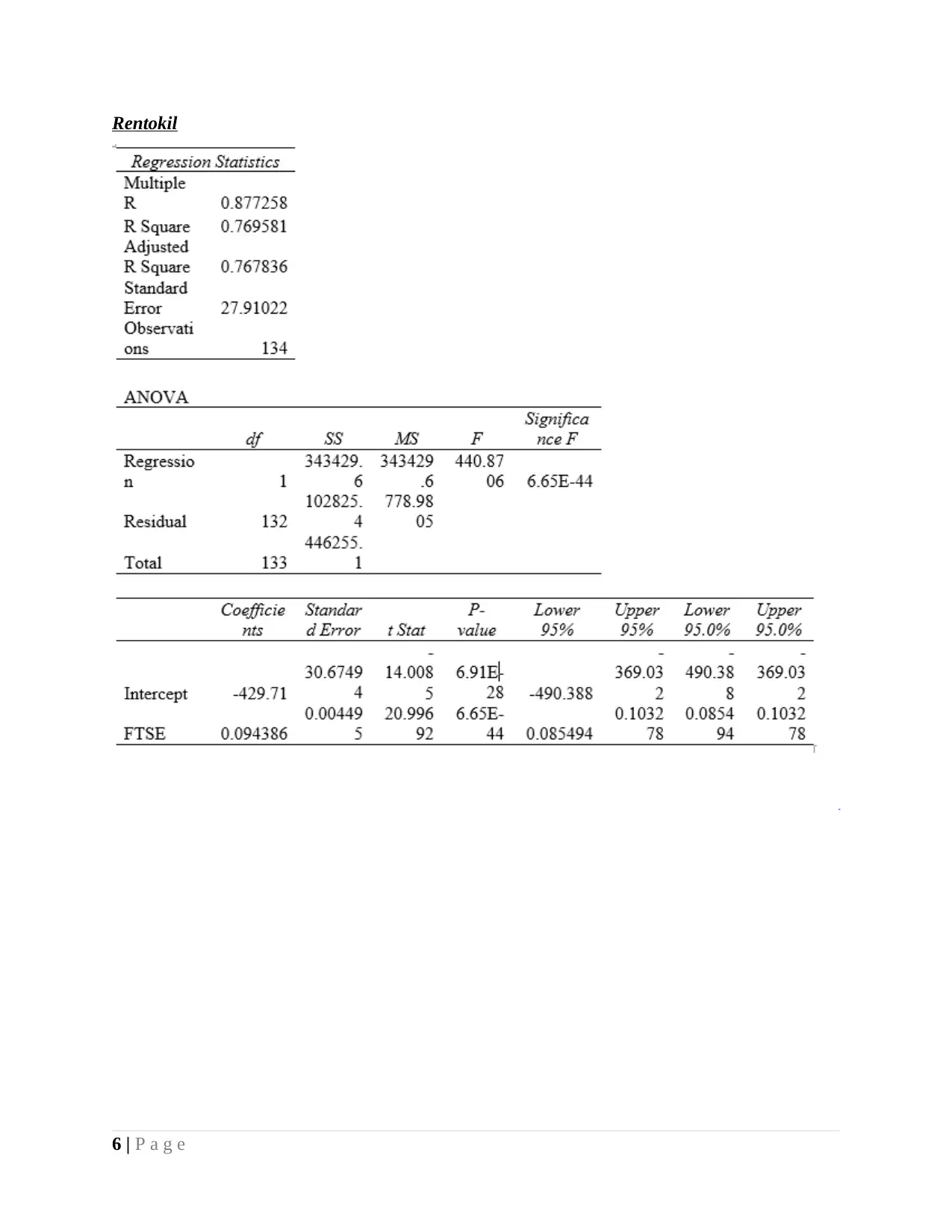

This report analyzes the performance of two investment portfolios, one constructed randomly and the other using technical analysis. The study tests the weak-form efficient market hypothesis using a t-test to compare the returns of the portfolios. The analysis reveals significant differences in returns, indicating that the technical analysis-based portfolio outperformed the randomly selected one, suggesting that market information impacts stock returns. The report also explores valuation methods, specifically the price-earnings (PE) ratio and PEG ratio, to assess the fair value of equity, and provides a comparative analysis of Bayer's PE ratio. The findings are compared to previous research on the efficient market hypothesis, highlighting the limitations of the theory and the potential for outperforming the market through informed investment strategies. The report concludes with a discussion on the implications of these findings for investors and the importance of considering market information in investment decisions.

1 out of 21

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.