Comparative Financial Analysis: Sainsbury's and Tesco (2018 & 2019)

VerifiedAdded on 2023/01/03

|14

|3768

|47

Report

AI Summary

This report presents a comprehensive financial analysis of Sainsbury's and Tesco, focusing on their performance in 2018 and 2019. It begins with the calculation of various financial ratios, including liquidity, profitability, efficiency, and gearing ratios, for both companies. The analysis then delves into a detailed comparison of their financial positions and performances, highlighting key trends and differences. The report evaluates the strengths and weaknesses of each company, and offers specific recommendations for Sainsbury's to improve its financial performance. Furthermore, it explores investment appraisal techniques, identifying the most beneficial projects and their limitations. The analysis also examines the limitations of using financial ratios in general. The report is based on publicly available financial data and provides insights into the financial health and strategic positioning of these two major retailers.

PORTFOLIO

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

PORTFOLIO 1.................................................................................................................................1

a) Calculating the financial ratios of both the companies for year 2018 & 2019. ......................1

b) Analysing the financial performance and position of two companies for year 2018 and

2019. ............................................................................................................................................4

c) Recommendations for improving performance of Sainsbury .................................................7

d) Limitations of financial ratios..................................................................................................7

PORTFOLIO 2.................................................................................................................................8

a) Using appropriate investment appraisal techniques choosing the most beneficial project. ....8

b) Limitations of using the different investment appraisal techniques......................................11

REFERENCES..............................................................................................................................13

PORTFOLIO 1.................................................................................................................................1

a) Calculating the financial ratios of both the companies for year 2018 & 2019. ......................1

b) Analysing the financial performance and position of two companies for year 2018 and

2019. ............................................................................................................................................4

c) Recommendations for improving performance of Sainsbury .................................................7

d) Limitations of financial ratios..................................................................................................7

PORTFOLIO 2.................................................................................................................................8

a) Using appropriate investment appraisal techniques choosing the most beneficial project. ....8

b) Limitations of using the different investment appraisal techniques......................................11

REFERENCES..............................................................................................................................13

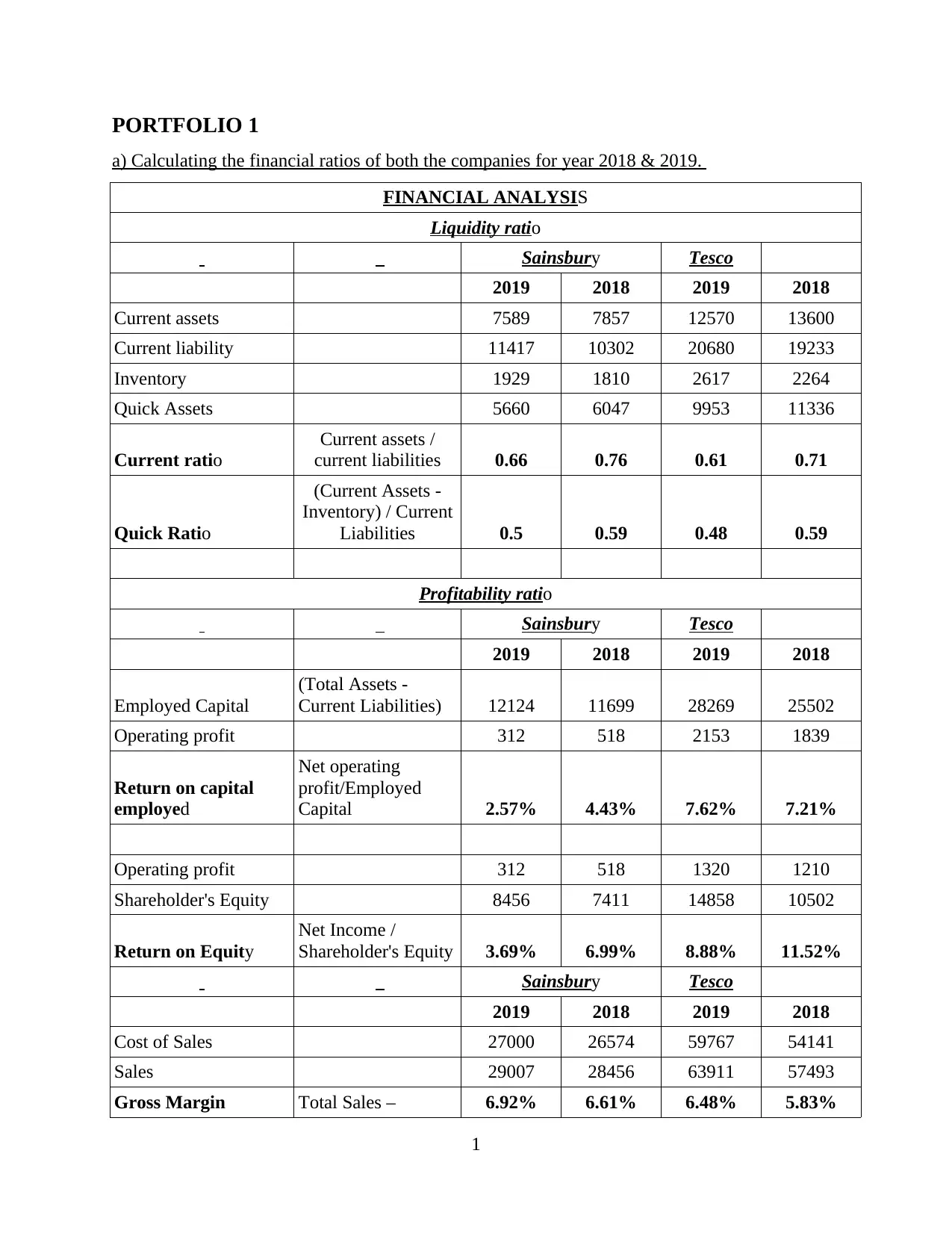

PORTFOLIO 1

a) Calculating the financial ratios of both the companies for year 2018 & 2019.

FINANCIAL ANALYSIS

Liquidity ratio

Sainsbury Tesco

2019 2018 2019 2018

Current assets 7589 7857 12570 13600

Current liability 11417 10302 20680 19233

Inventory 1929 1810 2617 2264

Quick Assets 5660 6047 9953 11336

Current ratio

Current assets /

current liabilities 0.66 0.76 0.61 0.71

Quick Ratio

(Current Assets -

Inventory) / Current

Liabilities 0.5 0.59 0.48 0.59

Profitability ratio

Sainsbury Tesco

2019 2018 2019 2018

Employed Capital

(Total Assets -

Current Liabilities) 12124 11699 28269 25502

Operating profit 312 518 2153 1839

Return on capital

employed

Net operating

profit/Employed

Capital 2.57% 4.43% 7.62% 7.21%

Operating profit 312 518 1320 1210

Shareholder's Equity 8456 7411 14858 10502

Return on Equity

Net Income /

Shareholder's Equity 3.69% 6.99% 8.88% 11.52%

Sainsbury Tesco

2019 2018 2019 2018

Cost of Sales 27000 26574 59767 54141

Sales 29007 28456 63911 57493

Gross Margin Total Sales – 6.92% 6.61% 6.48% 5.83%

1

a) Calculating the financial ratios of both the companies for year 2018 & 2019.

FINANCIAL ANALYSIS

Liquidity ratio

Sainsbury Tesco

2019 2018 2019 2018

Current assets 7589 7857 12570 13600

Current liability 11417 10302 20680 19233

Inventory 1929 1810 2617 2264

Quick Assets 5660 6047 9953 11336

Current ratio

Current assets /

current liabilities 0.66 0.76 0.61 0.71

Quick Ratio

(Current Assets -

Inventory) / Current

Liabilities 0.5 0.59 0.48 0.59

Profitability ratio

Sainsbury Tesco

2019 2018 2019 2018

Employed Capital

(Total Assets -

Current Liabilities) 12124 11699 28269 25502

Operating profit 312 518 2153 1839

Return on capital

employed

Net operating

profit/Employed

Capital 2.57% 4.43% 7.62% 7.21%

Operating profit 312 518 1320 1210

Shareholder's Equity 8456 7411 14858 10502

Return on Equity

Net Income /

Shareholder's Equity 3.69% 6.99% 8.88% 11.52%

Sainsbury Tesco

2019 2018 2019 2018

Cost of Sales 27000 26574 59767 54141

Sales 29007 28456 63911 57493

Gross Margin Total Sales – 6.92% 6.61% 6.48% 5.83%

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

COGS/Total Sales

Net profit 312 518 1320 1210

Sales 29007 28456 63911 57493

Net profit ratio

Operating Income/

Net Sales 1.08% 1.82% 2.07% 2.10%

Efficiency Ratios

Sainsbury Tesco

2019 2018 2019 2018

Trade Payables 4444 4322 9354 8994

Trade Receivables 661 744 1640 1504

Inventory 1929 1810 2617 2264

Net Assets 8456 7411 14858 10502

Cost of Sales 27000 26574 59767 54141

Sales 29007 28456 63911 57493

Inventory turnover

period

(Inventory/ Cost of

Sales)*365 26 25 16 15

Accounts Payable

Days

Accounts payable

/Cost of Sales *365 60 59 57 61

Account receivable

days

Accounts Receivable

/Cost of Sales * 365 9 10 10 10

Gearing Ratios

Sainsbury Tesco

2019 2018 2019 2018

Total Debt 15085 14590 34213 34404

Shareholder's Equity 8456 7411 14858 10502

Gearing ratio Total Debt/ Equity 1.78 1.97 2.30 3.28

Investor Ratios

Sainsbury Tesco

2

Net profit 312 518 1320 1210

Sales 29007 28456 63911 57493

Net profit ratio

Operating Income/

Net Sales 1.08% 1.82% 2.07% 2.10%

Efficiency Ratios

Sainsbury Tesco

2019 2018 2019 2018

Trade Payables 4444 4322 9354 8994

Trade Receivables 661 744 1640 1504

Inventory 1929 1810 2617 2264

Net Assets 8456 7411 14858 10502

Cost of Sales 27000 26574 59767 54141

Sales 29007 28456 63911 57493

Inventory turnover

period

(Inventory/ Cost of

Sales)*365 26 25 16 15

Accounts Payable

Days

Accounts payable

/Cost of Sales *365 60 59 57 61

Account receivable

days

Accounts Receivable

/Cost of Sales * 365 9 10 10 10

Gearing Ratios

Sainsbury Tesco

2019 2018 2019 2018

Total Debt 15085 14590 34213 34404

Shareholder's Equity 8456 7411 14858 10502

Gearing ratio Total Debt/ Equity 1.78 1.97 2.30 3.28

Investor Ratios

Sainsbury Tesco

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

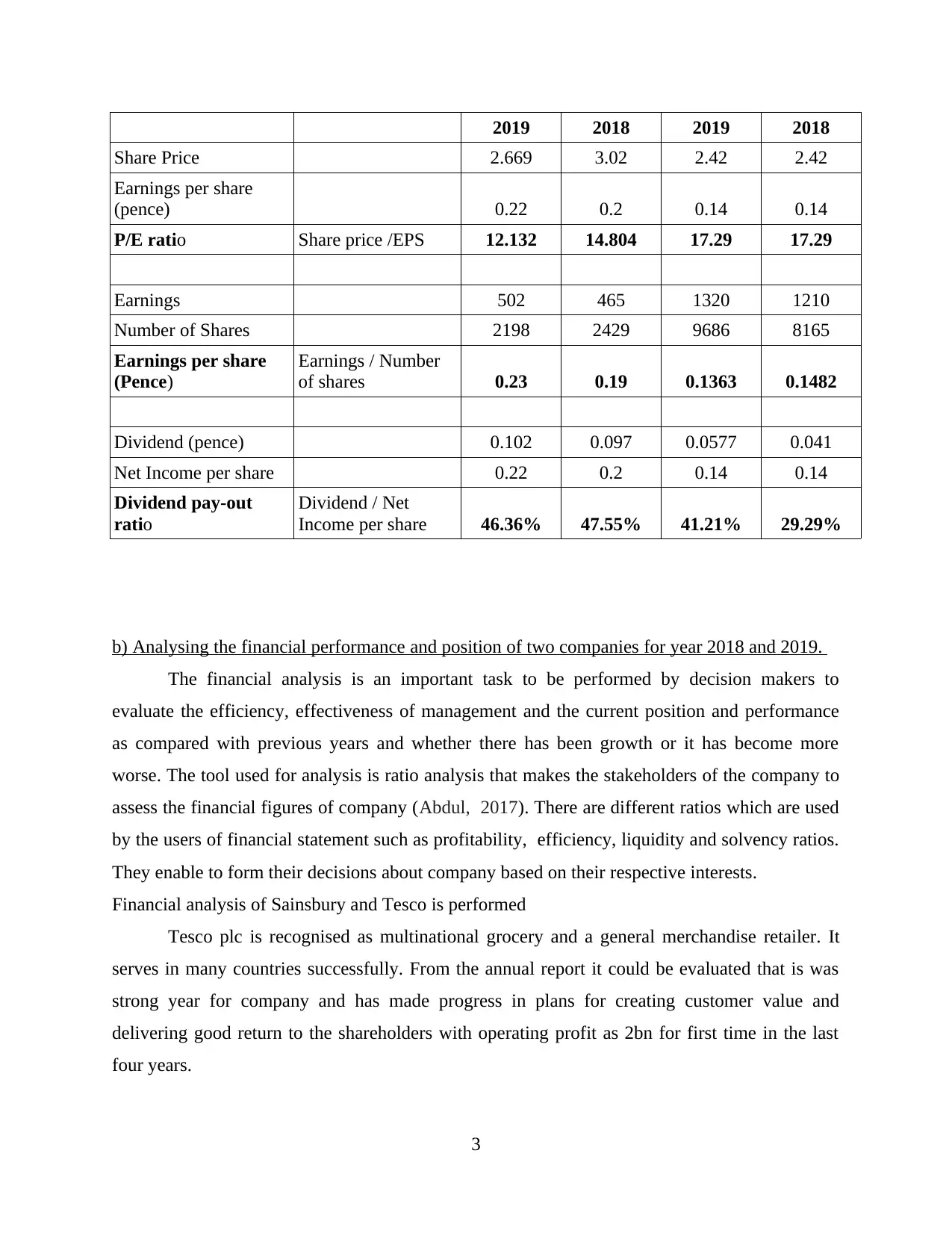

2019 2018 2019 2018

Share Price 2.669 3.02 2.42 2.42

Earnings per share

(pence) 0.22 0.2 0.14 0.14

P/E ratio Share price /EPS 12.132 14.804 17.29 17.29

Earnings 502 465 1320 1210

Number of Shares 2198 2429 9686 8165

Earnings per share

(Pence)

Earnings / Number

of shares 0.23 0.19 0.1363 0.1482

Dividend (pence) 0.102 0.097 0.0577 0.041

Net Income per share 0.22 0.2 0.14 0.14

Dividend pay-out

ratio

Dividend / Net

Income per share 46.36% 47.55% 41.21% 29.29%

b) Analysing the financial performance and position of two companies for year 2018 and 2019.

The financial analysis is an important task to be performed by decision makers to

evaluate the efficiency, effectiveness of management and the current position and performance

as compared with previous years and whether there has been growth or it has become more

worse. The tool used for analysis is ratio analysis that makes the stakeholders of the company to

assess the financial figures of company (Abdul, 2017). There are different ratios which are used

by the users of financial statement such as profitability, efficiency, liquidity and solvency ratios.

They enable to form their decisions about company based on their respective interests.

Financial analysis of Sainsbury and Tesco is performed

Tesco plc is recognised as multinational grocery and a general merchandise retailer. It

serves in many countries successfully. From the annual report it could be evaluated that is was

strong year for company and has made progress in plans for creating customer value and

delivering good return to the shareholders with operating profit as 2bn for first time in the last

four years.

3

Share Price 2.669 3.02 2.42 2.42

Earnings per share

(pence) 0.22 0.2 0.14 0.14

P/E ratio Share price /EPS 12.132 14.804 17.29 17.29

Earnings 502 465 1320 1210

Number of Shares 2198 2429 9686 8165

Earnings per share

(Pence)

Earnings / Number

of shares 0.23 0.19 0.1363 0.1482

Dividend (pence) 0.102 0.097 0.0577 0.041

Net Income per share 0.22 0.2 0.14 0.14

Dividend pay-out

ratio

Dividend / Net

Income per share 46.36% 47.55% 41.21% 29.29%

b) Analysing the financial performance and position of two companies for year 2018 and 2019.

The financial analysis is an important task to be performed by decision makers to

evaluate the efficiency, effectiveness of management and the current position and performance

as compared with previous years and whether there has been growth or it has become more

worse. The tool used for analysis is ratio analysis that makes the stakeholders of the company to

assess the financial figures of company (Abdul, 2017). There are different ratios which are used

by the users of financial statement such as profitability, efficiency, liquidity and solvency ratios.

They enable to form their decisions about company based on their respective interests.

Financial analysis of Sainsbury and Tesco is performed

Tesco plc is recognised as multinational grocery and a general merchandise retailer. It

serves in many countries successfully. From the annual report it could be evaluated that is was

strong year for company and has made progress in plans for creating customer value and

delivering good return to the shareholders with operating profit as 2bn for first time in the last

four years.

3

Sainsbury on the other is 2nd largest supermarket chain in UK. Company had performance

history with revenues of 29.007 billion and net income of 219 million. The company has been

committed to delivering values to the customers with adequate returns to the shareholders. The

company has seen growth of 7.8% in underlying PBT. It has also seen reducing in the carbon

emissions and achieved target for 2020.

Current Ratios

It is calculated for evaluating the financial liquidity of company. It tells about ability of

company in making payments for the short term liabilities with the available current assets. A

company is supposed to have standard current assets twice of current liabilities. IT is considered

as strong and good liquidity position. Current ratio of Sainsbury in 2018 was 0.76 and 0.66 in

2019. There has been downward movement in current ratio. While Teso had 0.71 in 2018 and

0.61 in 2018. It has also shown decline from last year. The decreasing liquidity ratio is a serious

concern as both company are already having very liquidity position. They are not having enough

current assets to meet the liabilities or short term obligations (Chiaramonte and Casu, 2017). The

consequences of this could result in suppliers reducing their supplies and requiring quick

clearance of payments. It would create extra burden on companies causing them to take more

funds to make payments increasing their financial costs. The cash operating cycle of both the

firms is not adequate. Management is required to take active actions to improve the liquidity

position as it may impact the business. It has to control its increasing short term obligations by

raising funds through long term modes and also by improving the collection systems of

organisation.

Quick Ratios

The ratio is also liquidity ratio used for identifying ability to repay the short term

financial obligations from existing current assets. The difference is that this ratio does not

consider inventor as current asset it could not be sold quickly in the market. QR of Sainsbury

was 0.59 in 2018 and 0.5 it has also decreased. Tesco had QR of 0.59 in 2019 and 0.48 in 2018.

It could be seen there has been decline in ratio showing that it is required to be improved

(Madushanka and Jathurika, 2018). It requires that financial obligations has to be decreased.

Quick ratio has to be improved by restructuring the existing processes for cash cycle and funding

sources that will help in maintaining adequate capital structure.

Net Profit Margin

4

history with revenues of 29.007 billion and net income of 219 million. The company has been

committed to delivering values to the customers with adequate returns to the shareholders. The

company has seen growth of 7.8% in underlying PBT. It has also seen reducing in the carbon

emissions and achieved target for 2020.

Current Ratios

It is calculated for evaluating the financial liquidity of company. It tells about ability of

company in making payments for the short term liabilities with the available current assets. A

company is supposed to have standard current assets twice of current liabilities. IT is considered

as strong and good liquidity position. Current ratio of Sainsbury in 2018 was 0.76 and 0.66 in

2019. There has been downward movement in current ratio. While Teso had 0.71 in 2018 and

0.61 in 2018. It has also shown decline from last year. The decreasing liquidity ratio is a serious

concern as both company are already having very liquidity position. They are not having enough

current assets to meet the liabilities or short term obligations (Chiaramonte and Casu, 2017). The

consequences of this could result in suppliers reducing their supplies and requiring quick

clearance of payments. It would create extra burden on companies causing them to take more

funds to make payments increasing their financial costs. The cash operating cycle of both the

firms is not adequate. Management is required to take active actions to improve the liquidity

position as it may impact the business. It has to control its increasing short term obligations by

raising funds through long term modes and also by improving the collection systems of

organisation.

Quick Ratios

The ratio is also liquidity ratio used for identifying ability to repay the short term

financial obligations from existing current assets. The difference is that this ratio does not

consider inventor as current asset it could not be sold quickly in the market. QR of Sainsbury

was 0.59 in 2018 and 0.5 it has also decreased. Tesco had QR of 0.59 in 2019 and 0.48 in 2018.

It could be seen there has been decline in ratio showing that it is required to be improved

(Madushanka and Jathurika, 2018). It requires that financial obligations has to be decreased.

Quick ratio has to be improved by restructuring the existing processes for cash cycle and funding

sources that will help in maintaining adequate capital structure.

Net Profit Margin

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

It could be considered as most important ratio that is assessed by every stakeholder. This

reflects the ability of company to manage all activities and operation to earn adequate profits. It

is the final outcome of carrying out every business. NP of Sainsbury is 1.08% in 2019 and 1.82%

in 2018. It has decreased this year also. On the other Tesco is having NP of 2.07% and was

2.10% in 2018. The profits have shown decline (Bayrakdaroglu, Mirgen and Kuyu, 2017). Both

the companies have faced decline but it could be seen that NP of Sainsbury is more lower than

Tesco and the decrease is also higher from Tesco in current year. It shows that the business

performance of company is constantly declining which requires management to undertake steps

that would improve the profitability of both firm.

Gross Profit Margin

It is also a profitability ratio used to assess the trading effectiveness of the company. It

evaluated whether it had been successful in controlling the costs and generate adequate profits.

GP of Sainsbury was 6.61%in 2018 and 6.92% in 2018 which shows improvement as compared

with previous year. Tesco was having GP at 5.83% in 2018 and 6.48% in 2019. It could be

evaluated that the GP of both the firm is improved from last year but NP has been decreased

(Laitinen, 2017). The revenues of companies has increased from last year due to effective

marketing strategies and new collaborations. The growth of Tesco is higher than Sainsbury in GP

which shows strategies of Tesco are working effectively and it is required to implement effective

governance to monitor the policies for improvements and growth. Both the companies are

required to adopt technology that is more cost efficient and productive for them. It will help in

reducing their costs of production and increasing the profits.

Gearing Ratio

It is the ratio used for determining the risks associated with the company. It provides

whether there is adequate capital structure or not of the firm. As capital structure determines the

costs of capital of company. Sainsbury is having gearing ratio of 1.78 in 2019 and it was 1.97

last year. It has declined. On other Tesco is having GR of 2.30 in 2019 that was 3.28 last year.

Ratio has moved downward. The ratios of both companies have declined but Tesco has shown

major fall than Sainsbury. Downward movement shows that debts have been repaid and the

existing financial structure has been improved. Financial risk associated with business has

decreased.

P/E Ratio

5

reflects the ability of company to manage all activities and operation to earn adequate profits. It

is the final outcome of carrying out every business. NP of Sainsbury is 1.08% in 2019 and 1.82%

in 2018. It has decreased this year also. On the other Tesco is having NP of 2.07% and was

2.10% in 2018. The profits have shown decline (Bayrakdaroglu, Mirgen and Kuyu, 2017). Both

the companies have faced decline but it could be seen that NP of Sainsbury is more lower than

Tesco and the decrease is also higher from Tesco in current year. It shows that the business

performance of company is constantly declining which requires management to undertake steps

that would improve the profitability of both firm.

Gross Profit Margin

It is also a profitability ratio used to assess the trading effectiveness of the company. It

evaluated whether it had been successful in controlling the costs and generate adequate profits.

GP of Sainsbury was 6.61%in 2018 and 6.92% in 2018 which shows improvement as compared

with previous year. Tesco was having GP at 5.83% in 2018 and 6.48% in 2019. It could be

evaluated that the GP of both the firm is improved from last year but NP has been decreased

(Laitinen, 2017). The revenues of companies has increased from last year due to effective

marketing strategies and new collaborations. The growth of Tesco is higher than Sainsbury in GP

which shows strategies of Tesco are working effectively and it is required to implement effective

governance to monitor the policies for improvements and growth. Both the companies are

required to adopt technology that is more cost efficient and productive for them. It will help in

reducing their costs of production and increasing the profits.

Gearing Ratio

It is the ratio used for determining the risks associated with the company. It provides

whether there is adequate capital structure or not of the firm. As capital structure determines the

costs of capital of company. Sainsbury is having gearing ratio of 1.78 in 2019 and it was 1.97

last year. It has declined. On other Tesco is having GR of 2.30 in 2019 that was 3.28 last year.

Ratio has moved downward. The ratios of both companies have declined but Tesco has shown

major fall than Sainsbury. Downward movement shows that debts have been repaid and the

existing financial structure has been improved. Financial risk associated with business has

decreased.

P/E Ratio

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

This ratio is used for valuing company which measures the current share prices relative to

earnings per share. PE is also known as earnings multiple. These are used by the experts to

determine relative value of the shares in apple to apple comparison. It provided the share price

represents projected EPS accurately (Jitmaneeroj, 2017). P/E of Sainsbury is 12 in current year

where of Tesco it is 17. The P/E of Sainsbury has declined where Tesco has not major change. It

could be evaluated from the analysis that share prices are correctly priced. The declining

performance of Sainsbury has declined the PE and share prices too which is not good for

company.

Earning Per share

It represents earnings per share available to the shareholders of company. EPS of

Sainsbury is 0.23 and 0.13 of Tesco. The EPS of Tesco is lower as the number of shareholders

are very high as compared with Sainsbury. It could also be evaluated that EPS of Sainsbury has

increased from last year and declined of Tesco. Increase is seen due to decrease in shareholders

and increase in profits. It shows that Sainsbury is making efforts to increase earnings to the

shareholders.

Return on capital employed

The ratio is used to analyse the effectiveness of management in generating returns over

the existing resources of company. It is an important ratio that provides the investors whether

company will be able to utilise the resources appropriately or not. Sainsbury has seen fall in

ROCE from 4.43% in 2018 to 2.57% in 2019. While Tesco had ROCE of 7.62% 2019 and it was

7.21%. There has been no significant fluctuations in ROCE of Tesco but the ratio of Sainsbury

has fallen to half from last year (Pivac, Barać and Tadić, 2017). Sainsbury is required to improve

the ROCE as it shows the existing management strategies are not working effectively to generate

adequate returns for the business. It has to assess existing methods and do restructuring or

implement new practices for making optimum utilisation to generate better returns.

Average inventory turnover period

It tells about the time within which management is making the inventory to convert in

cash. It comes under efficiency ratio as it management efficiency in rotating the inventory. The

ITP of Sainsbury is 26 days which was 25 in last year. Tesco is having ITP of 16 days in 2019

and 15 days in 2018. Turnover period of Tesco is short which shows that the management is

more efficient than Sainsbury. Lower period means inventory is converted into cash quickly.

6

earnings per share. PE is also known as earnings multiple. These are used by the experts to

determine relative value of the shares in apple to apple comparison. It provided the share price

represents projected EPS accurately (Jitmaneeroj, 2017). P/E of Sainsbury is 12 in current year

where of Tesco it is 17. The P/E of Sainsbury has declined where Tesco has not major change. It

could be evaluated from the analysis that share prices are correctly priced. The declining

performance of Sainsbury has declined the PE and share prices too which is not good for

company.

Earning Per share

It represents earnings per share available to the shareholders of company. EPS of

Sainsbury is 0.23 and 0.13 of Tesco. The EPS of Tesco is lower as the number of shareholders

are very high as compared with Sainsbury. It could also be evaluated that EPS of Sainsbury has

increased from last year and declined of Tesco. Increase is seen due to decrease in shareholders

and increase in profits. It shows that Sainsbury is making efforts to increase earnings to the

shareholders.

Return on capital employed

The ratio is used to analyse the effectiveness of management in generating returns over

the existing resources of company. It is an important ratio that provides the investors whether

company will be able to utilise the resources appropriately or not. Sainsbury has seen fall in

ROCE from 4.43% in 2018 to 2.57% in 2019. While Tesco had ROCE of 7.62% 2019 and it was

7.21%. There has been no significant fluctuations in ROCE of Tesco but the ratio of Sainsbury

has fallen to half from last year (Pivac, Barać and Tadić, 2017). Sainsbury is required to improve

the ROCE as it shows the existing management strategies are not working effectively to generate

adequate returns for the business. It has to assess existing methods and do restructuring or

implement new practices for making optimum utilisation to generate better returns.

Average inventory turnover period

It tells about the time within which management is making the inventory to convert in

cash. It comes under efficiency ratio as it management efficiency in rotating the inventory. The

ITP of Sainsbury is 26 days which was 25 in last year. Tesco is having ITP of 16 days in 2019

and 15 days in 2018. Turnover period of Tesco is short which shows that the management is

more efficient than Sainsbury. Lower period means inventory is converted into cash quickly.

6

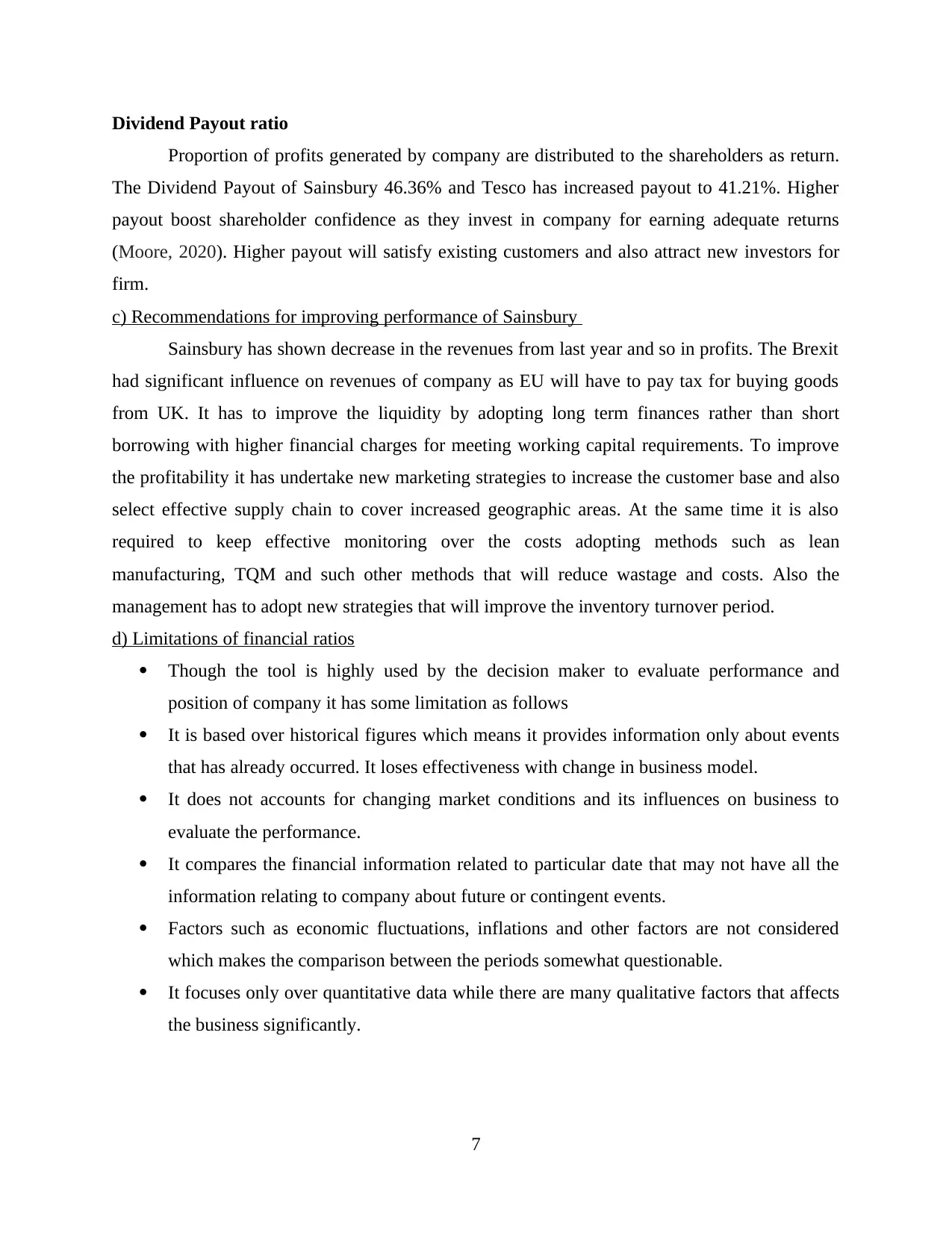

Dividend Payout ratio

Proportion of profits generated by company are distributed to the shareholders as return.

The Dividend Payout of Sainsbury 46.36% and Tesco has increased payout to 41.21%. Higher

payout boost shareholder confidence as they invest in company for earning adequate returns

(Moore, 2020). Higher payout will satisfy existing customers and also attract new investors for

firm.

c) Recommendations for improving performance of Sainsbury

Sainsbury has shown decrease in the revenues from last year and so in profits. The Brexit

had significant influence on revenues of company as EU will have to pay tax for buying goods

from UK. It has to improve the liquidity by adopting long term finances rather than short

borrowing with higher financial charges for meeting working capital requirements. To improve

the profitability it has undertake new marketing strategies to increase the customer base and also

select effective supply chain to cover increased geographic areas. At the same time it is also

required to keep effective monitoring over the costs adopting methods such as lean

manufacturing, TQM and such other methods that will reduce wastage and costs. Also the

management has to adopt new strategies that will improve the inventory turnover period.

d) Limitations of financial ratios

Though the tool is highly used by the decision maker to evaluate performance and

position of company it has some limitation as follows

It is based over historical figures which means it provides information only about events

that has already occurred. It loses effectiveness with change in business model.

It does not accounts for changing market conditions and its influences on business to

evaluate the performance.

It compares the financial information related to particular date that may not have all the

information relating to company about future or contingent events.

Factors such as economic fluctuations, inflations and other factors are not considered

which makes the comparison between the periods somewhat questionable.

It focuses only over quantitative data while there are many qualitative factors that affects

the business significantly.

7

Proportion of profits generated by company are distributed to the shareholders as return.

The Dividend Payout of Sainsbury 46.36% and Tesco has increased payout to 41.21%. Higher

payout boost shareholder confidence as they invest in company for earning adequate returns

(Moore, 2020). Higher payout will satisfy existing customers and also attract new investors for

firm.

c) Recommendations for improving performance of Sainsbury

Sainsbury has shown decrease in the revenues from last year and so in profits. The Brexit

had significant influence on revenues of company as EU will have to pay tax for buying goods

from UK. It has to improve the liquidity by adopting long term finances rather than short

borrowing with higher financial charges for meeting working capital requirements. To improve

the profitability it has undertake new marketing strategies to increase the customer base and also

select effective supply chain to cover increased geographic areas. At the same time it is also

required to keep effective monitoring over the costs adopting methods such as lean

manufacturing, TQM and such other methods that will reduce wastage and costs. Also the

management has to adopt new strategies that will improve the inventory turnover period.

d) Limitations of financial ratios

Though the tool is highly used by the decision maker to evaluate performance and

position of company it has some limitation as follows

It is based over historical figures which means it provides information only about events

that has already occurred. It loses effectiveness with change in business model.

It does not accounts for changing market conditions and its influences on business to

evaluate the performance.

It compares the financial information related to particular date that may not have all the

information relating to company about future or contingent events.

Factors such as economic fluctuations, inflations and other factors are not considered

which makes the comparison between the periods somewhat questionable.

It focuses only over quantitative data while there are many qualitative factors that affects

the business significantly.

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

PORTFOLIO 2

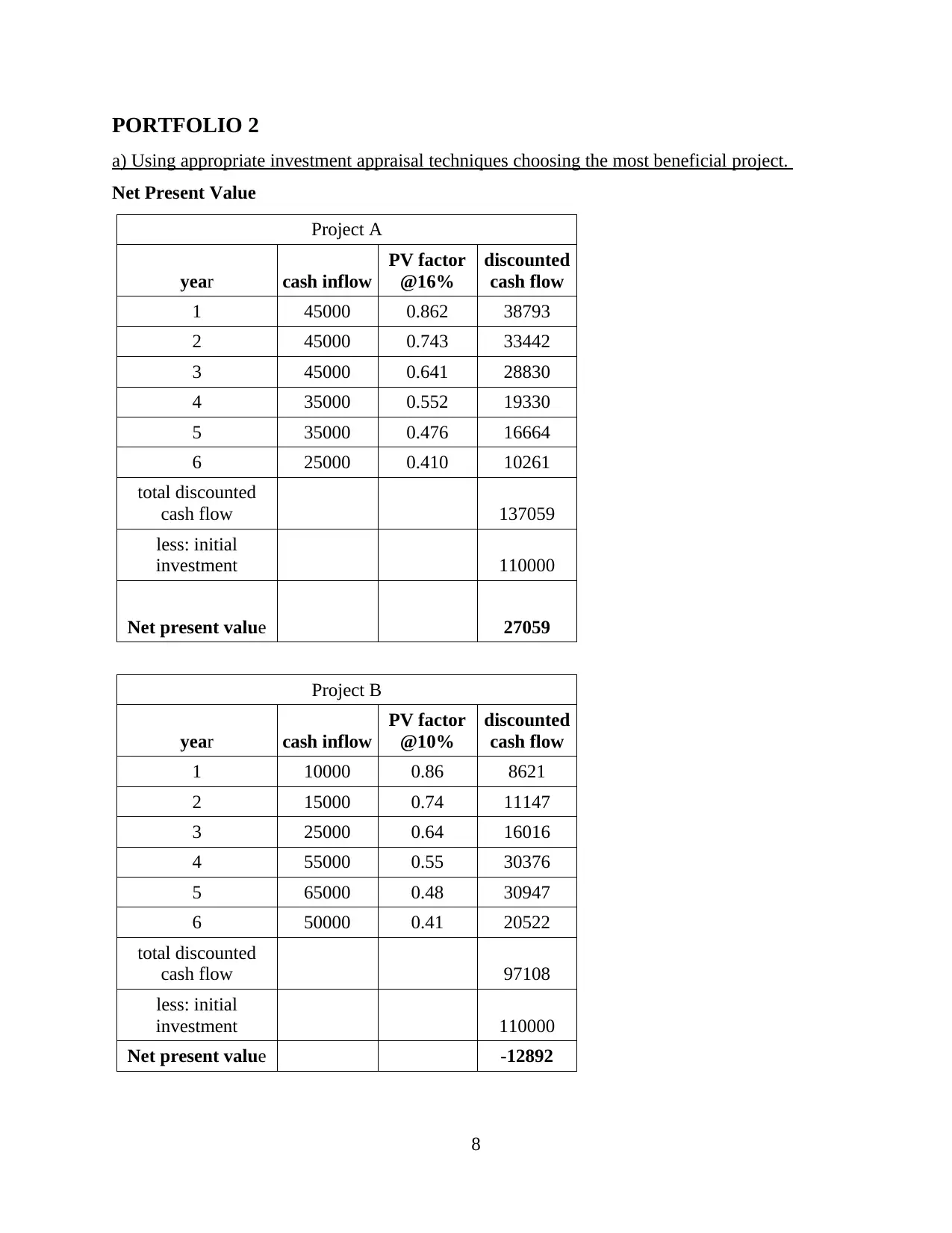

a) Using appropriate investment appraisal techniques choosing the most beneficial project.

Net Present Value

Project A

year cash inflow

PV factor

@16%

discounted

cash flow

1 45000 0.862 38793

2 45000 0.743 33442

3 45000 0.641 28830

4 35000 0.552 19330

5 35000 0.476 16664

6 25000 0.410 10261

total discounted

cash flow 137059

less: initial

investment 110000

Net present value 27059

Project B

year cash inflow

PV factor

@10%

discounted

cash flow

1 10000 0.86 8621

2 15000 0.74 11147

3 25000 0.64 16016

4 55000 0.55 30376

5 65000 0.48 30947

6 50000 0.41 20522

total discounted

cash flow 97108

less: initial

investment 110000

Net present value -12892

8

a) Using appropriate investment appraisal techniques choosing the most beneficial project.

Net Present Value

Project A

year cash inflow

PV factor

@16%

discounted

cash flow

1 45000 0.862 38793

2 45000 0.743 33442

3 45000 0.641 28830

4 35000 0.552 19330

5 35000 0.476 16664

6 25000 0.410 10261

total discounted

cash flow 137059

less: initial

investment 110000

Net present value 27059

Project B

year cash inflow

PV factor

@10%

discounted

cash flow

1 10000 0.86 8621

2 15000 0.74 11147

3 25000 0.64 16016

4 55000 0.55 30376

5 65000 0.48 30947

6 50000 0.41 20522

total discounted

cash flow 97108

less: initial

investment 110000

Net present value -12892

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Internal Rate of Return

Project A Project B

Year Cash flow Year Cash flow

0 -110000 0 -110000

1 45000 1 10000

2 45000 2 15000

3 45000 3 25000

4 35000 4 55000

5 35000 5 65000

6 25000 6 50000

Internal

rate of

return 27.00%

Internal rate

of return 12.00%

Accounting Rate of Return

Project A Project B

Year Cash flow Year Cash flow

1 45000 1 10000

2 45000 2 15000

3 45000 3 25000

4 35000 4 55000

5 35000 5 65000

6 25000 6 50000

Average

profit 38333.33

Average

profit 36666.67

Average

investment 55000

Average

investment 59000

Average

rate of

return 70.00%

Average rate

of return 62.00%

Payback Period

Project A Project B

9

Project A Project B

Year Cash flow Year Cash flow

0 -110000 0 -110000

1 45000 1 10000

2 45000 2 15000

3 45000 3 25000

4 35000 4 55000

5 35000 5 65000

6 25000 6 50000

Internal

rate of

return 27.00%

Internal rate

of return 12.00%

Accounting Rate of Return

Project A Project B

Year Cash flow Year Cash flow

1 45000 1 10000

2 45000 2 15000

3 45000 3 25000

4 35000 4 55000

5 35000 5 65000

6 25000 6 50000

Average

profit 38333.33

Average

profit 36666.67

Average

investment 55000

Average

investment 59000

Average

rate of

return 70.00%

Average rate

of return 62.00%

Payback Period

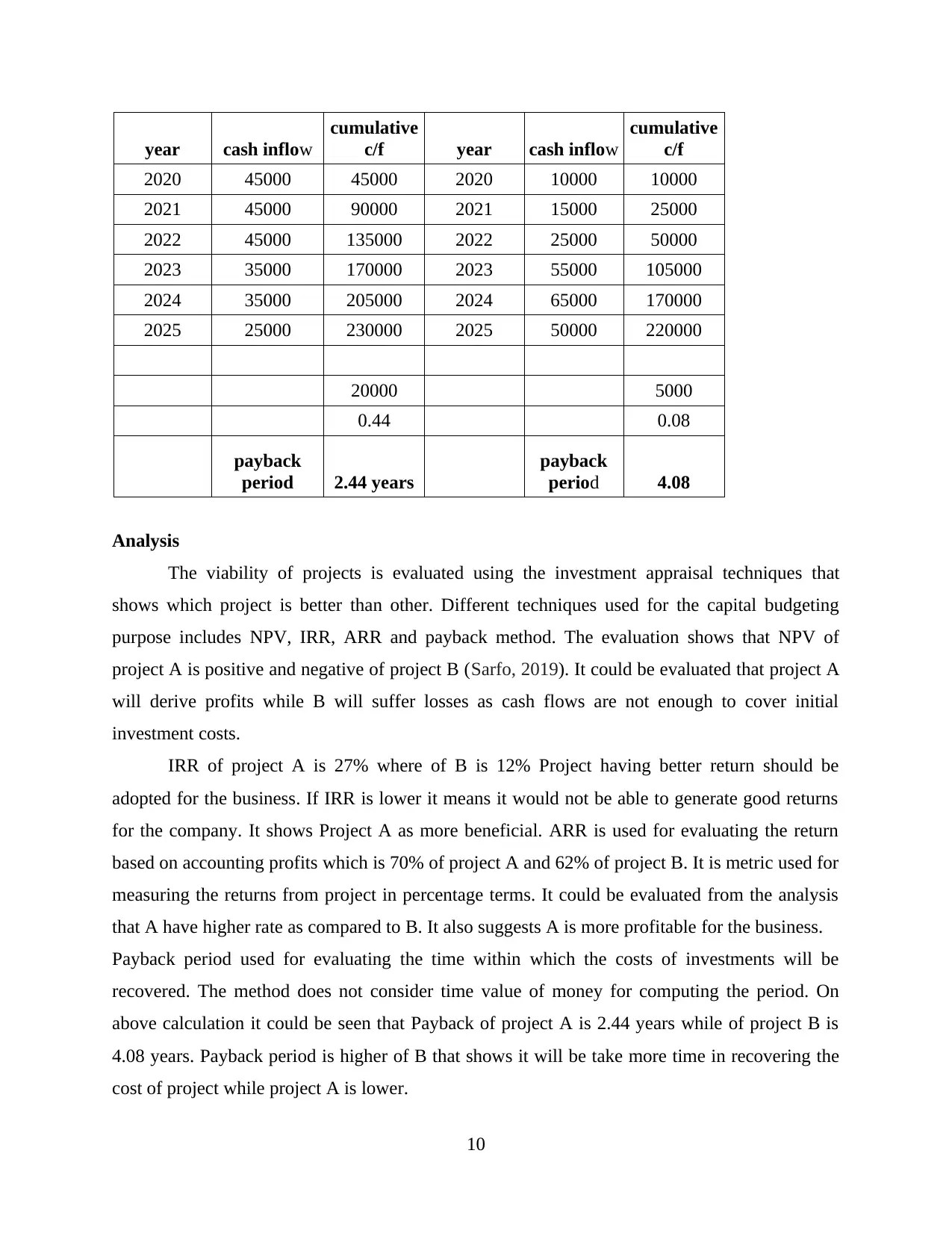

Project A Project B

9

year cash inflow

cumulative

c/f year cash inflow

cumulative

c/f

2020 45000 45000 2020 10000 10000

2021 45000 90000 2021 15000 25000

2022 45000 135000 2022 25000 50000

2023 35000 170000 2023 55000 105000

2024 35000 205000 2024 65000 170000

2025 25000 230000 2025 50000 220000

20000 5000

0.44 0.08

payback

period 2.44 years

payback

period 4.08

Analysis

The viability of projects is evaluated using the investment appraisal techniques that

shows which project is better than other. Different techniques used for the capital budgeting

purpose includes NPV, IRR, ARR and payback method. The evaluation shows that NPV of

project A is positive and negative of project B (Sarfo, 2019). It could be evaluated that project A

will derive profits while B will suffer losses as cash flows are not enough to cover initial

investment costs.

IRR of project A is 27% where of B is 12% Project having better return should be

adopted for the business. If IRR is lower it means it would not be able to generate good returns

for the company. It shows Project A as more beneficial. ARR is used for evaluating the return

based on accounting profits which is 70% of project A and 62% of project B. It is metric used for

measuring the returns from project in percentage terms. It could be evaluated from the analysis

that A have higher rate as compared to B. It also suggests A is more profitable for the business.

Payback period used for evaluating the time within which the costs of investments will be

recovered. The method does not consider time value of money for computing the period. On

above calculation it could be seen that Payback of project A is 2.44 years while of project B is

4.08 years. Payback period is higher of B that shows it will be take more time in recovering the

cost of project while project A is lower.

10

cumulative

c/f year cash inflow

cumulative

c/f

2020 45000 45000 2020 10000 10000

2021 45000 90000 2021 15000 25000

2022 45000 135000 2022 25000 50000

2023 35000 170000 2023 55000 105000

2024 35000 205000 2024 65000 170000

2025 25000 230000 2025 50000 220000

20000 5000

0.44 0.08

payback

period 2.44 years

payback

period 4.08

Analysis

The viability of projects is evaluated using the investment appraisal techniques that

shows which project is better than other. Different techniques used for the capital budgeting

purpose includes NPV, IRR, ARR and payback method. The evaluation shows that NPV of

project A is positive and negative of project B (Sarfo, 2019). It could be evaluated that project A

will derive profits while B will suffer losses as cash flows are not enough to cover initial

investment costs.

IRR of project A is 27% where of B is 12% Project having better return should be

adopted for the business. If IRR is lower it means it would not be able to generate good returns

for the company. It shows Project A as more beneficial. ARR is used for evaluating the return

based on accounting profits which is 70% of project A and 62% of project B. It is metric used for

measuring the returns from project in percentage terms. It could be evaluated from the analysis

that A have higher rate as compared to B. It also suggests A is more profitable for the business.

Payback period used for evaluating the time within which the costs of investments will be

recovered. The method does not consider time value of money for computing the period. On

above calculation it could be seen that Payback of project A is 2.44 years while of project B is

4.08 years. Payback period is higher of B that shows it will be take more time in recovering the

cost of project while project A is lower.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.