Assessment of IASB Conceptual Framework Revision on Liabilities

VerifiedAdded on 2022/11/18

|11

|591

|260

Presentation

AI Summary

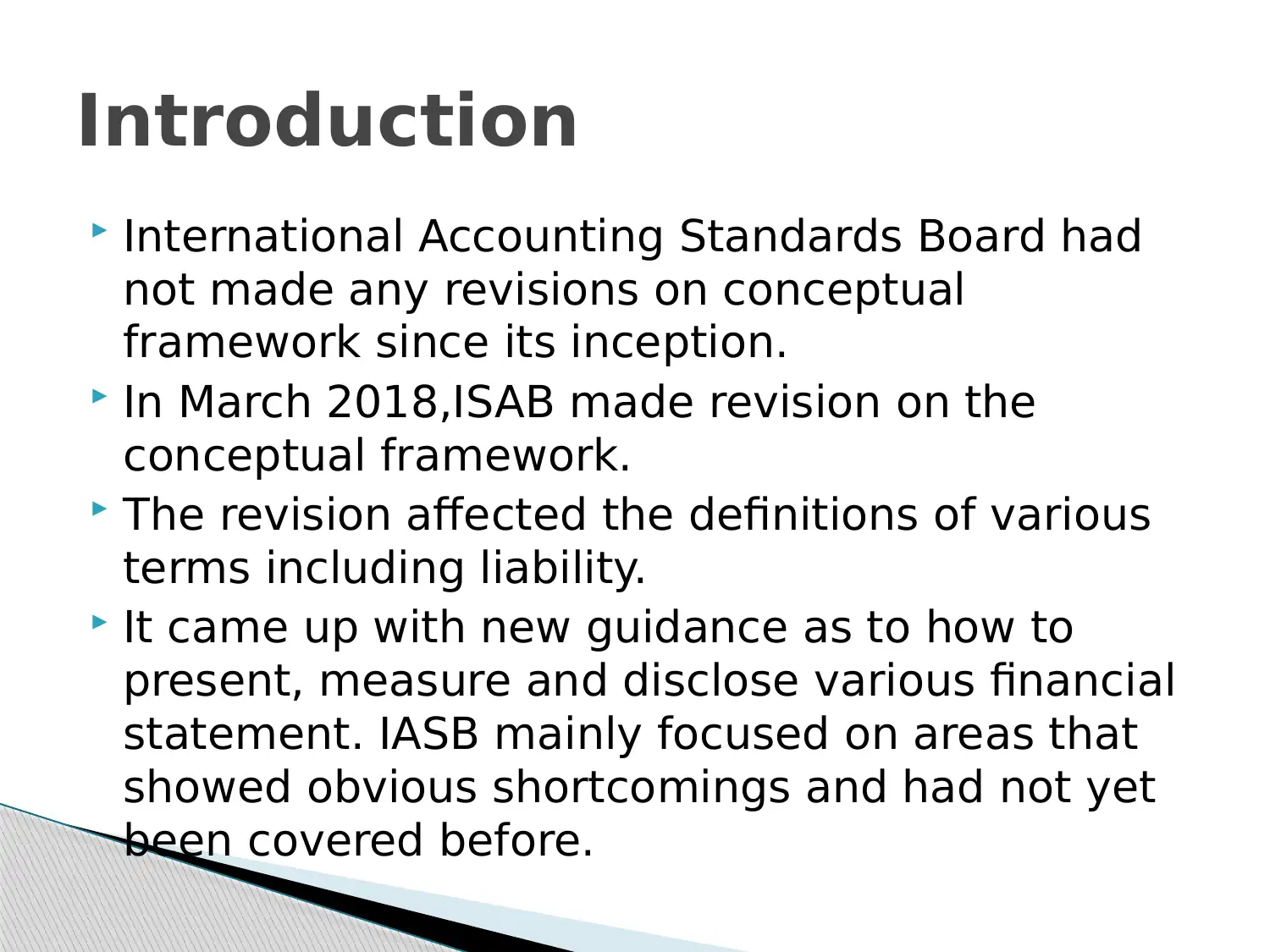

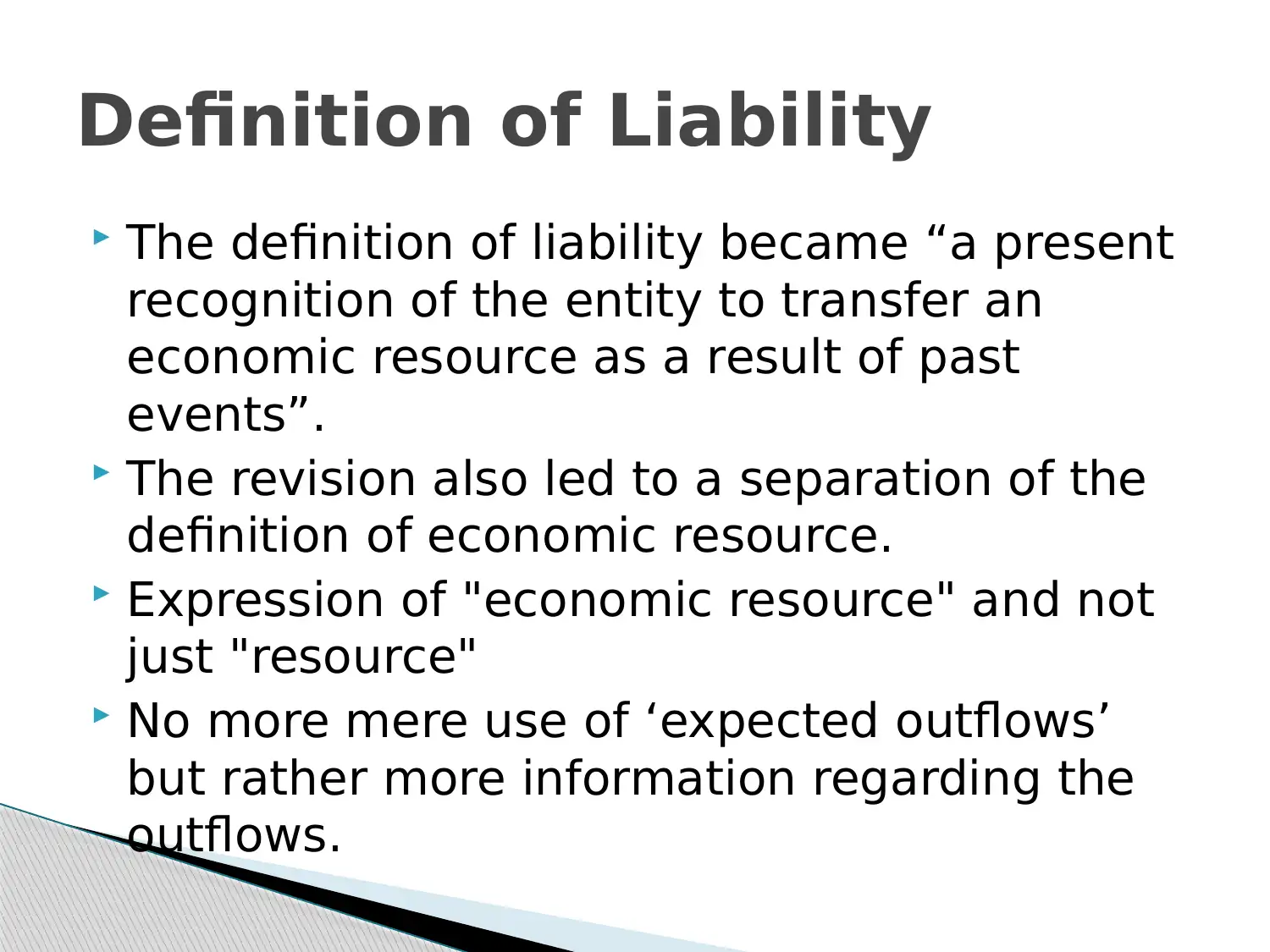

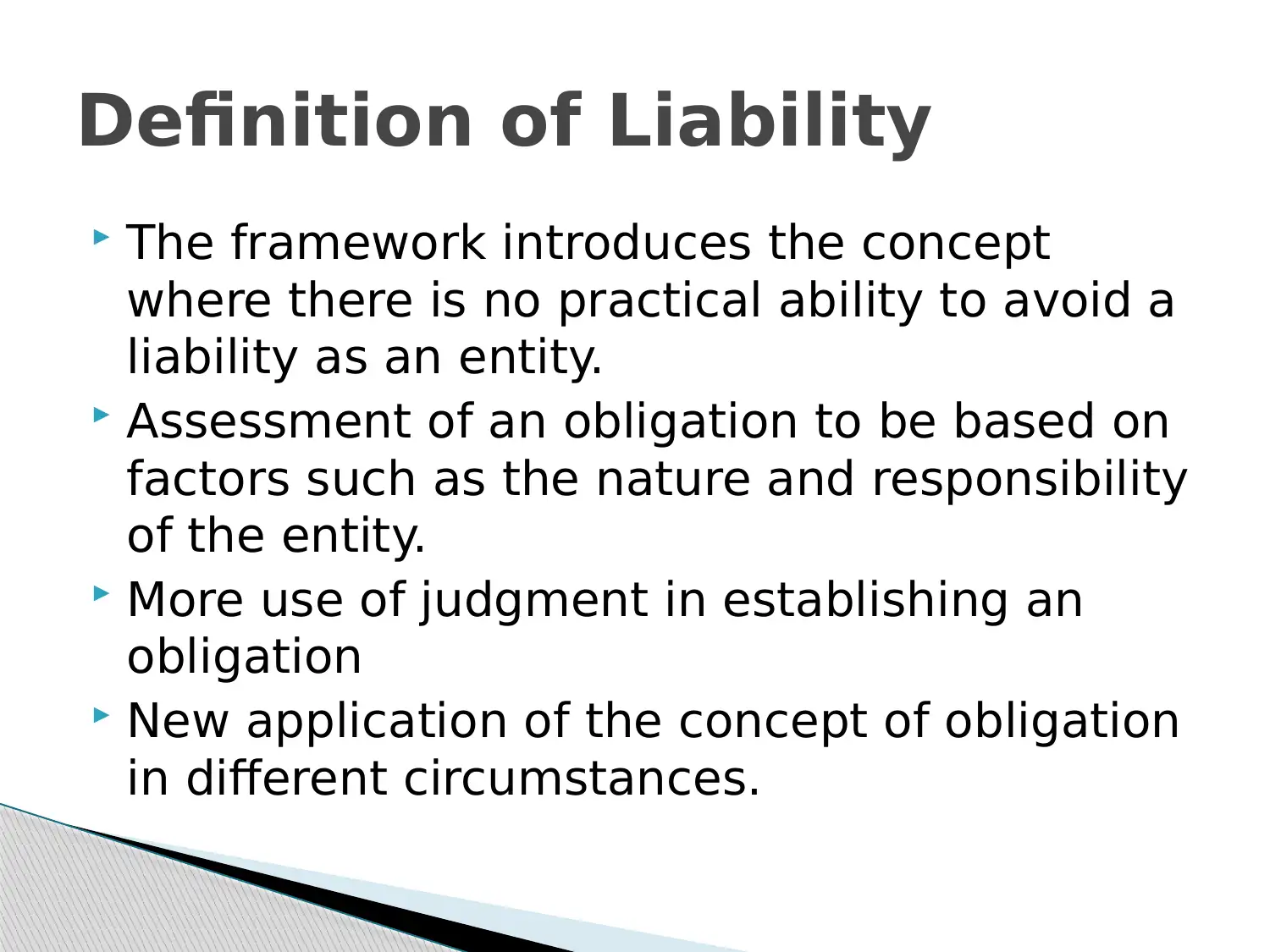

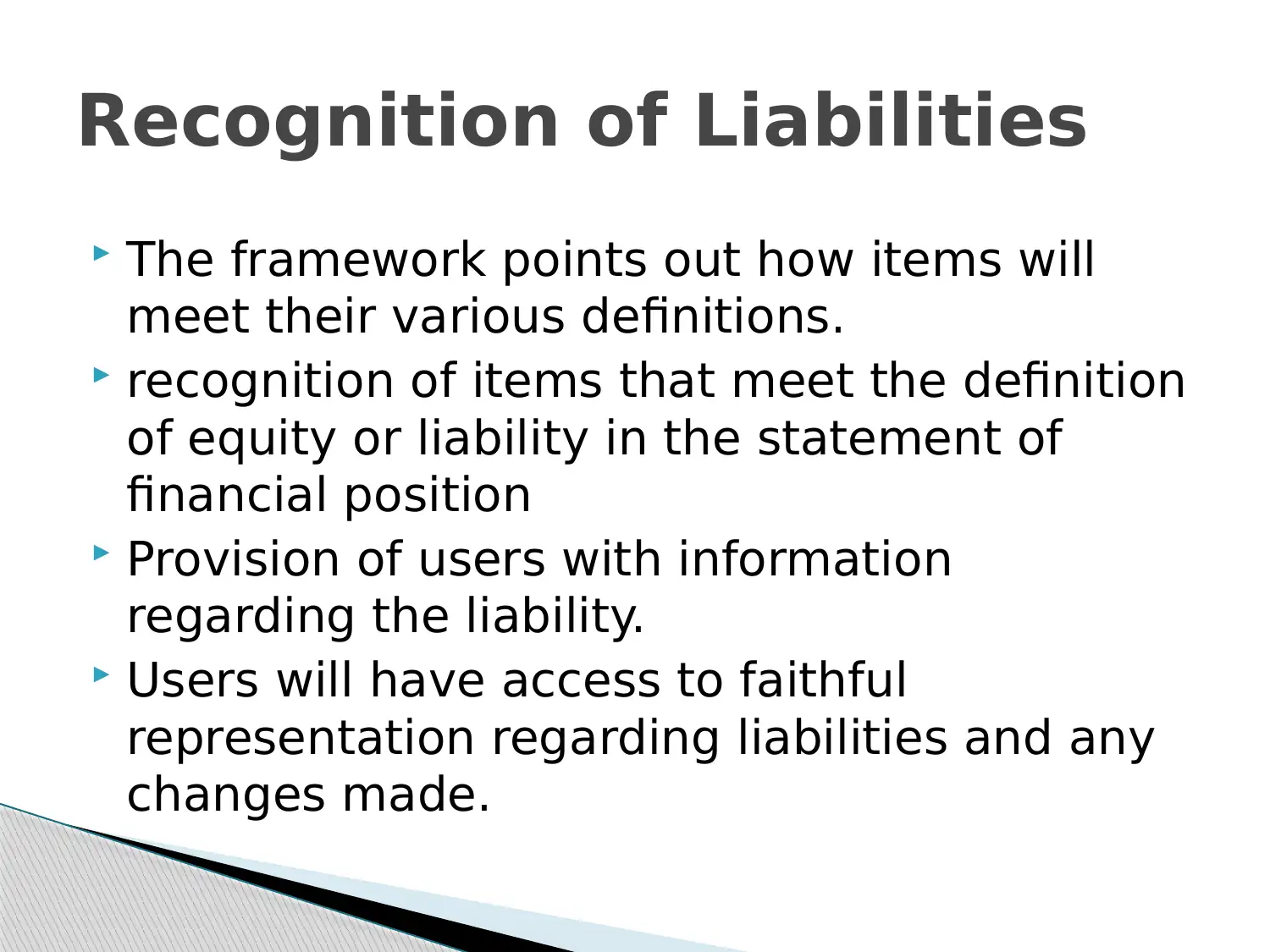

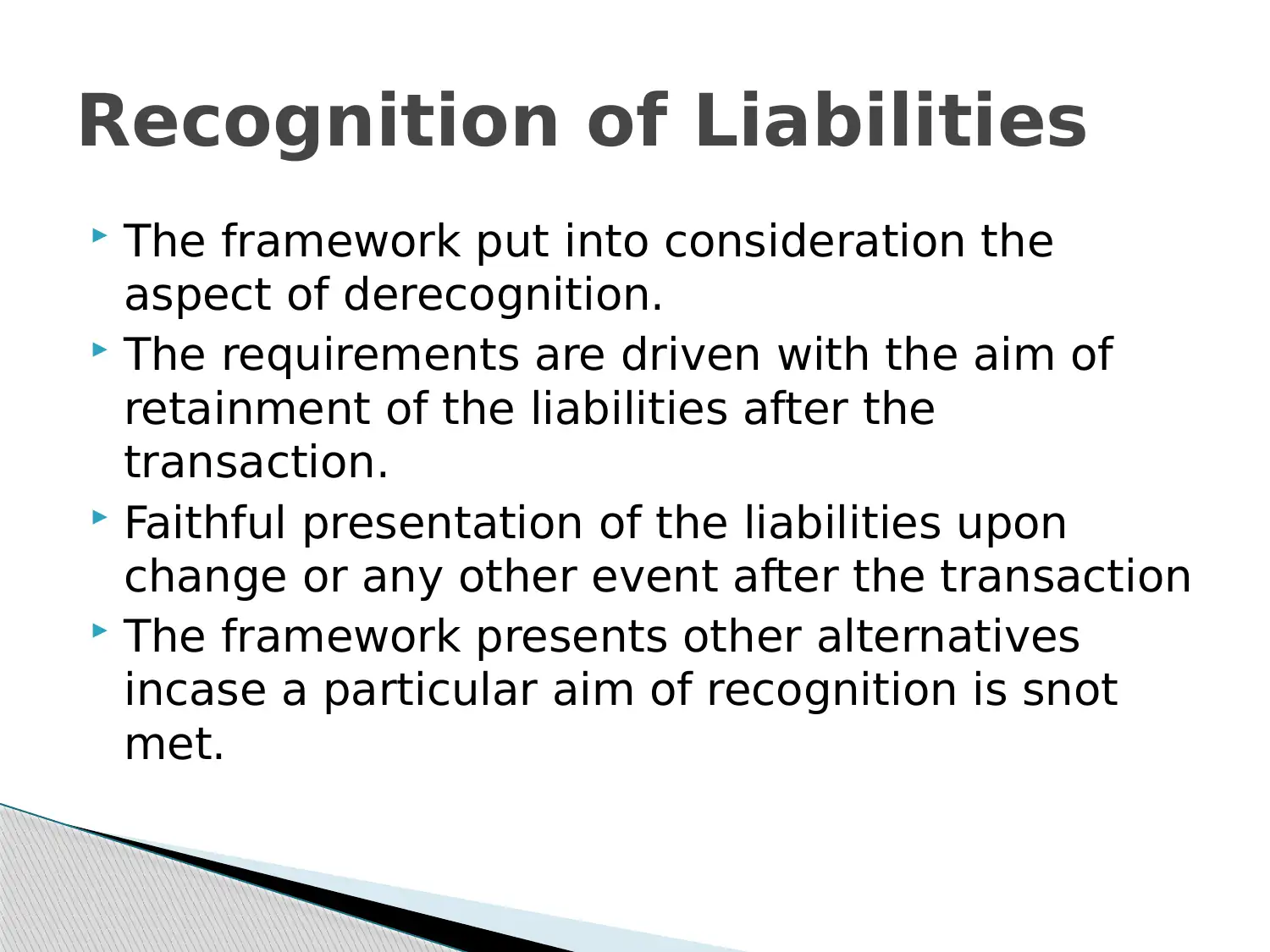

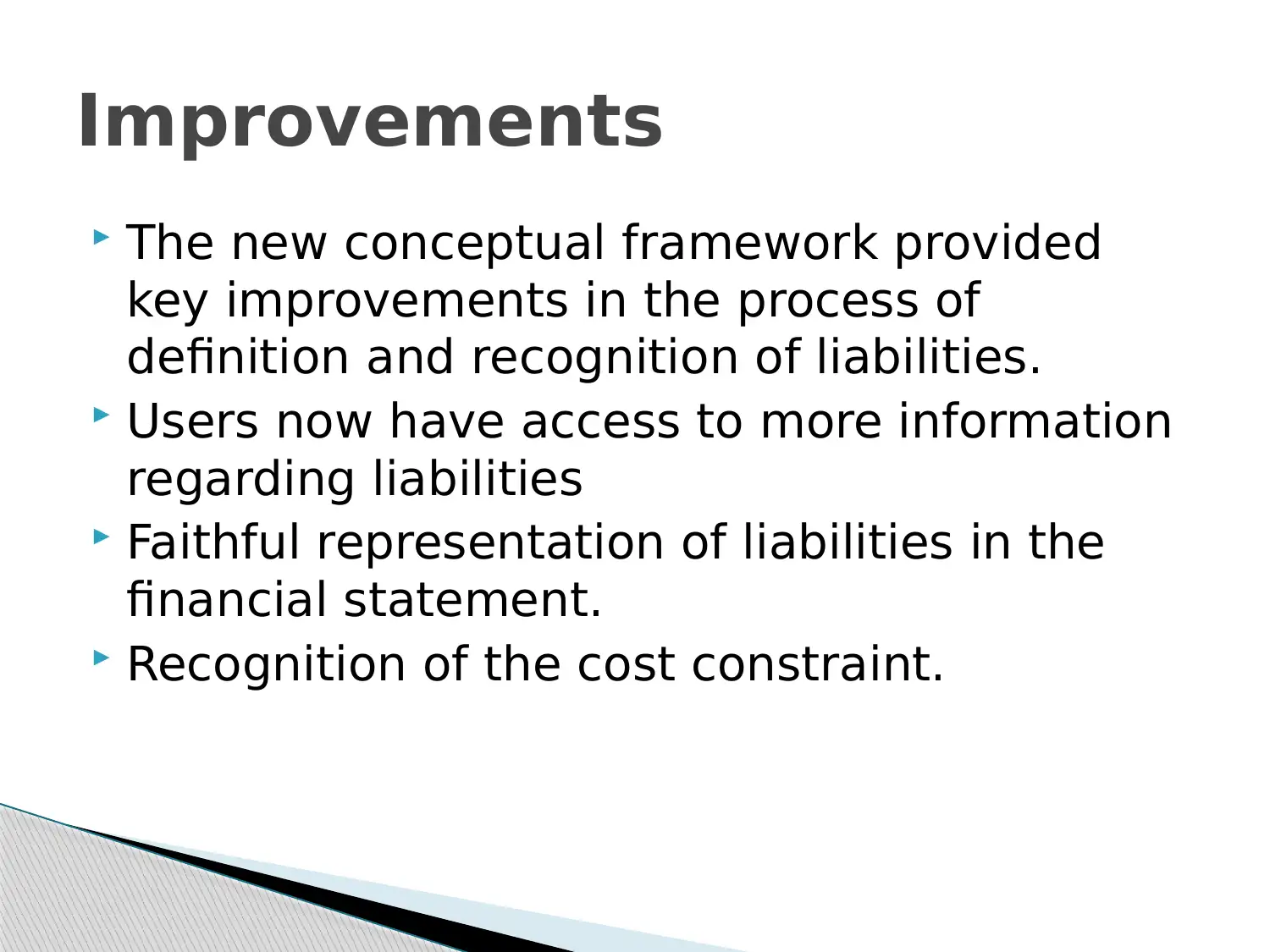

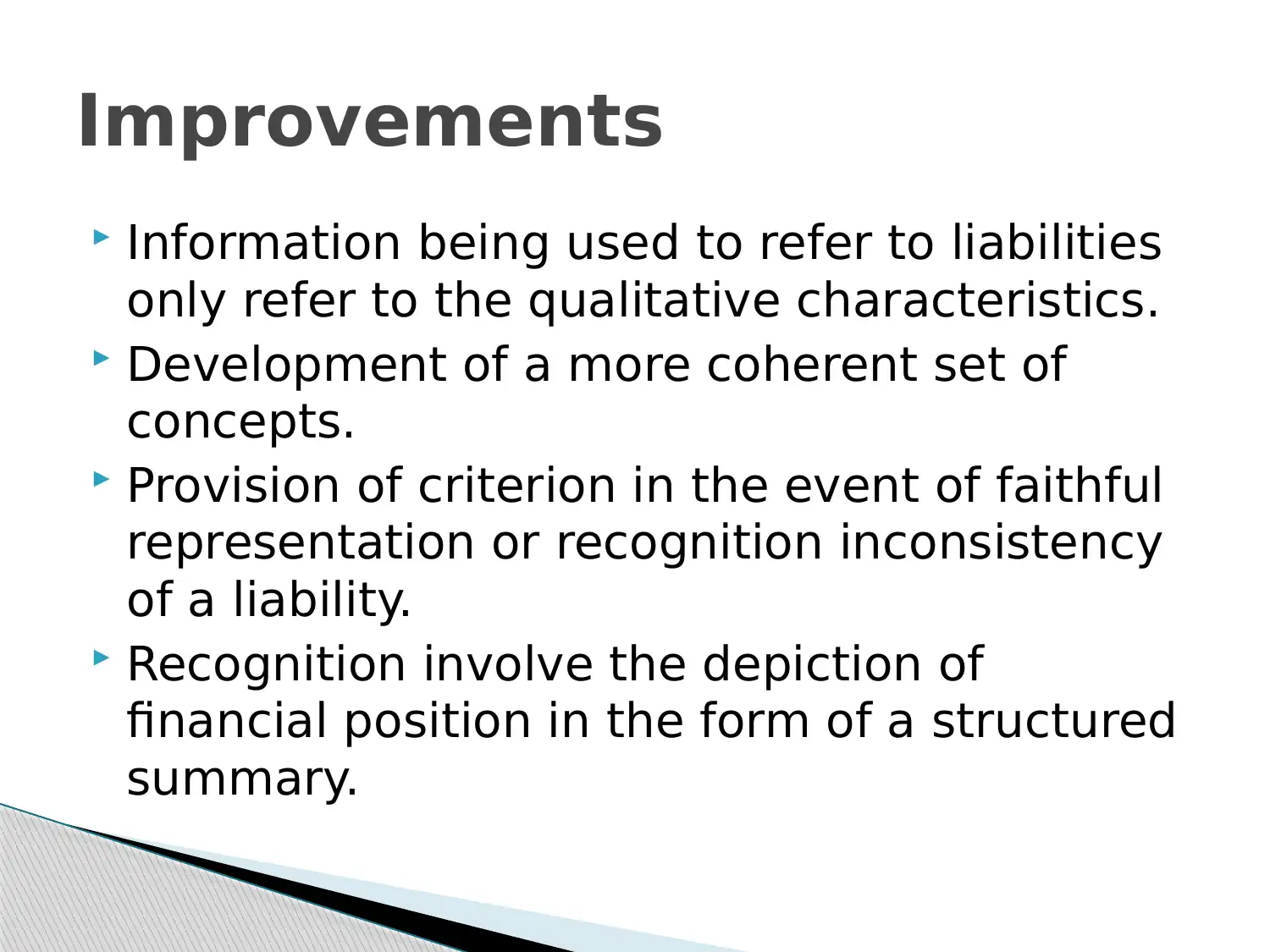

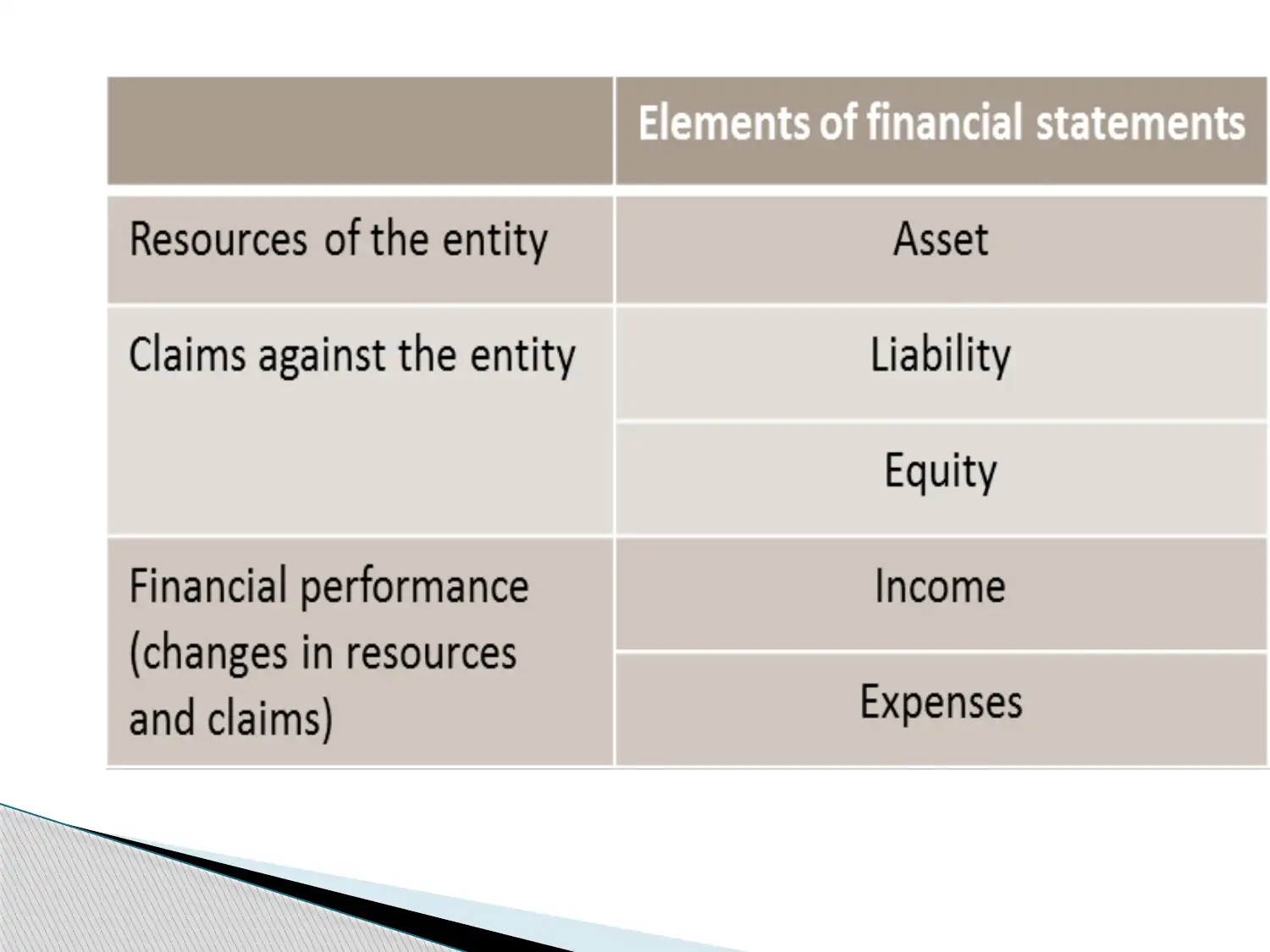

This presentation examines the March 2018 revision of the IASB Conceptual Framework, specifically focusing on the definition and recognition of liabilities. It explores the changes made to the definition of a liability, emphasizing the shift towards recognizing a present obligation to transfer an economic resource due to past events. The presentation highlights improvements in the framework, such as the increased availability of information regarding liabilities, the faithful representation of liabilities in financial statements, and the inclusion of the cost constraint. It also discusses the framework's influence on derecognition, the presentation of financial position, and the provision of criteria for faithful representation. The presentation concludes by summarizing the key enhancements in the revised framework and its impact on financial reporting, providing a deeper understanding of the changes for improved financial statement analysis.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.