Accounting Report: IFRS Adoption and Analysis for TOTAL S.A Company

VerifiedAdded on 2023/06/10

|8

|1602

|265

Report

AI Summary

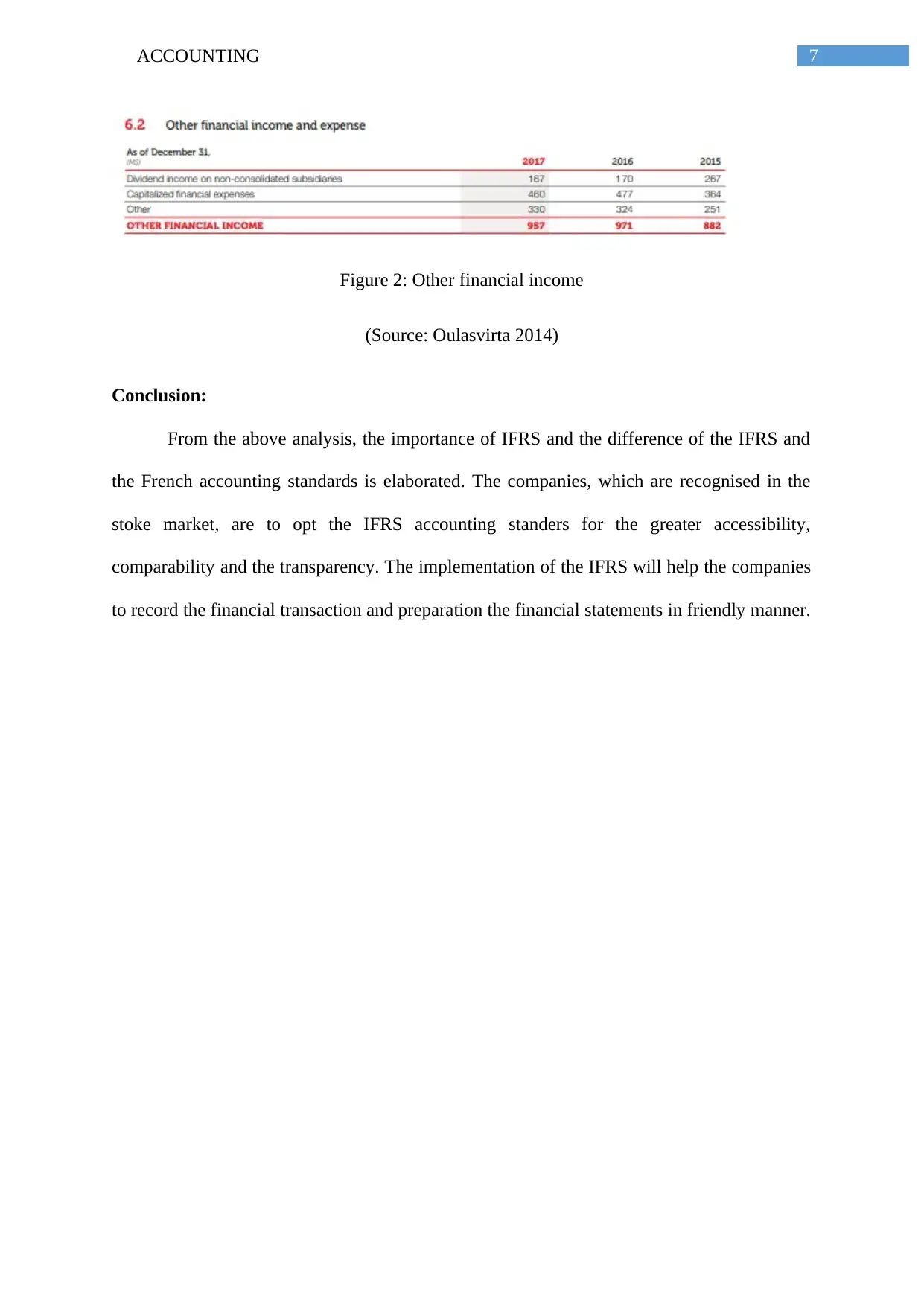

This report provides a detailed analysis of the implementation of International Financial Reporting Standards (IFRS) by TOTAL S.A, a major oil and gas company. The report examines the company's adoption of IFRS, highlighting the benefits of transparency and comparability with other international companies. It conducts a critical analysis of the differences between IFRS and the French Generally Accepted Accounting Principles (GAAP), focusing on areas such as employee benefits and revenue recognition. The report explains how IFRS affects the treatment of employee benefits, including share-based payments and the valuation process, contrasting it with French accounting practices. It also explores the impact of IFRS on the closing period and net income recognition, specifically how revenue and expenses are recognized. The analysis includes figures illustrating employee shareholding and other financial income. The report concludes by emphasizing the importance of IFRS for companies listed in the stock market, promoting greater accessibility, comparability, and transparency in financial reporting.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

© 2024 | Zucol Services PVT LTD | All rights reserved.