Impact of International Financial Reporting Standards on Investors

VerifiedAdded on 2020/04/15

|25

|6005

|57

Report

AI Summary

This report delves into the significance of International Financial Reporting Standards (IFRS) and their implications for investors. It explores the advantages, such as increased comparability, transparency, and access to detailed financial information, which can lead to better-informed investment decisions and reduced capital costs. The report also addresses the disadvantages, including the high implementation costs, potential for manipulation due to the flexibility in applying standards, and the challenges of global acceptance. The study examines the impact of IFRS on various factors affecting investors, including the timeliness of loss recognition and the convergence of financial statements. It also highlights the importance of understanding IFRS for making informed investment choices, considering both the benefits and the potential drawbacks. The methodology includes a literature review, sample selection, and variable selection, to provide a comprehensive analysis of the topic.

Running head: IFRS PROS AND CONS FOR INVESTORS

IFRS pros and cons for investors

Name of the student

Name of the university

Author note

IFRS pros and cons for investors

Name of the student

Name of the university

Author note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2IFRS PROS AND CONS FOR INVESTORS

Table of Contents

1.0 Introduction..........................................................................................................................4

1.1 Importance of the Research..............................................................................................5

1.2 Research Questions..........................................................................................................5

2.0 Literature review..................................................................................................................6

2.1.1 Focus on the investors...................................................................................................7

2.1.2 Recognition of loss in timeliness..................................................................................8

2.1.3 Comparability................................................................................................................8

2.2.1 Requirement of high costs.............................................................................................9

2.2.2 Prone to manipulation...................................................................................................9

2.2.3 Not globally accepted..................................................................................................10

2.3 Conceptual Framework......................................................................................................10

2.4Summary.........................................................................................................................10

3.0 Research methodology:......................................................................................................12

3.1 Sample selection:...........................................................................................................12

3.2 Sample period:...............................................................................................................13

3.3 Model selection:.............................................................................................................13

3.4 Variable selection:..........................................................................................................14

4.0 Results and findings:..........................................................................................................15

5.0 Conclusion..........................................................................................................................18

5.1 Recommendation............................................................................................................19

Table of Contents

1.0 Introduction..........................................................................................................................4

1.1 Importance of the Research..............................................................................................5

1.2 Research Questions..........................................................................................................5

2.0 Literature review..................................................................................................................6

2.1.1 Focus on the investors...................................................................................................7

2.1.2 Recognition of loss in timeliness..................................................................................8

2.1.3 Comparability................................................................................................................8

2.2.1 Requirement of high costs.............................................................................................9

2.2.2 Prone to manipulation...................................................................................................9

2.2.3 Not globally accepted..................................................................................................10

2.3 Conceptual Framework......................................................................................................10

2.4Summary.........................................................................................................................10

3.0 Research methodology:......................................................................................................12

3.1 Sample selection:...........................................................................................................12

3.2 Sample period:...............................................................................................................13

3.3 Model selection:.............................................................................................................13

3.4 Variable selection:..........................................................................................................14

4.0 Results and findings:..........................................................................................................15

5.0 Conclusion..........................................................................................................................18

5.1 Recommendation............................................................................................................19

3IFRS PROS AND CONS FOR INVESTORS

Reference..................................................................................................................................20

Reference..................................................................................................................................20

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

4IFRS PROS AND CONS FOR INVESTORS

1.0 Introduction

There are various standards and processes that are used in the current world and these

processes are useful for proper maintenance and functioning of the organizations that

existent. This research study tries to elaborate the significance of IFRS (International

Financial Reporting Standard) and their pros and cons that are existent for an investor. IFRS

has been in the forefront in the current agenda as the organizations that are listed are required

to disclose their financial statements in accordance the standards of accounting put forth by

IFRS (Doukakis et al., 2017). The International Financial Reporting Standard provides

assisting standards for the developing countries that would be helpful in increasing the

economic revenues by disclosing the fair and true position of the economy. This research

paper comprises of the precise discussion of International Financial Reporting Standard and

the pros and cons that are associated for the investors. The financial reports that are

constructed by the companies are seen by the investors relying on IFRS but have not been

able to experience the full scale of the adjustments for a yearly basis that might be triggered

by the IFRS (Rhee et al., 2016). It is essential to explain the pros and cons that is available to

the investors so that the investors gain knowledge about the same and take extensive

measures that would be beneficial for the investors with respect to their investments.

The initial section of the paper tries to explain the principles of International Financial

Reporting Standard so that a brief idea about the standard can be attained. The next section of

the paper tries to assess the pros and cons for the investors with respect to IFRS when it is

implemented by various countries. The pros and cons are different and depend upon by the

various external factors that are existent in various countries. The various councils that looks

in to these standards, constructs the strategy for the compliance of these standards with the

1.0 Introduction

There are various standards and processes that are used in the current world and these

processes are useful for proper maintenance and functioning of the organizations that

existent. This research study tries to elaborate the significance of IFRS (International

Financial Reporting Standard) and their pros and cons that are existent for an investor. IFRS

has been in the forefront in the current agenda as the organizations that are listed are required

to disclose their financial statements in accordance the standards of accounting put forth by

IFRS (Doukakis et al., 2017). The International Financial Reporting Standard provides

assisting standards for the developing countries that would be helpful in increasing the

economic revenues by disclosing the fair and true position of the economy. This research

paper comprises of the precise discussion of International Financial Reporting Standard and

the pros and cons that are associated for the investors. The financial reports that are

constructed by the companies are seen by the investors relying on IFRS but have not been

able to experience the full scale of the adjustments for a yearly basis that might be triggered

by the IFRS (Rhee et al., 2016). It is essential to explain the pros and cons that is available to

the investors so that the investors gain knowledge about the same and take extensive

measures that would be beneficial for the investors with respect to their investments.

The initial section of the paper tries to explain the principles of International Financial

Reporting Standard so that a brief idea about the standard can be attained. The next section of

the paper tries to assess the pros and cons for the investors with respect to IFRS when it is

implemented by various countries. The pros and cons are different and depend upon by the

various external factors that are existent in various countries. The various councils that looks

in to these standards, constructs the strategy for the compliance of these standards with the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

5IFRS PROS AND CONS FOR INVESTORS

ones that existent to the regulations and laws and even assesses the standards when

incorporated (Santana et al., 2014).

There are various importance and benefits of IFRS that is inclusive of comparative

assessment of the true and fair statements, precise resource allocation, confidence of the

investors etc. These are certain pros that can assist the investors in understanding their

investments and in the same manner undertake investments in a precise manner (Barbu et al.,

2014). The paper even tries to explain the obstacles and the cons that the investors can face

and therefore specific assessments can be taken in order to understand the same about the

topic.

1.1 Importance of the Research

The answering of these issues is vital as it would be helpful in discovering the pros

and cons that are existent in IFRS for the investors and thereby helping the companies and the

investors to gain knowledge about the same and construct their strategies in an effective

manner.

1.2 Research Questions

The research questions have been constructed in order to have an idea about the

International Financial Reporting Standard and the companies that have been incorporating

the same. The research question is helpful in constructing the course and the path that would

be followed in order to complete the research in an effective manner. The research questions

consist of the issue that is needed to be answered by the paper. The research questions are

given as follows:

Q1. What are the various factors that can have an impact on IFRS and in that manner can

have an impact on the investors?

ones that existent to the regulations and laws and even assesses the standards when

incorporated (Santana et al., 2014).

There are various importance and benefits of IFRS that is inclusive of comparative

assessment of the true and fair statements, precise resource allocation, confidence of the

investors etc. These are certain pros that can assist the investors in understanding their

investments and in the same manner undertake investments in a precise manner (Barbu et al.,

2014). The paper even tries to explain the obstacles and the cons that the investors can face

and therefore specific assessments can be taken in order to understand the same about the

topic.

1.1 Importance of the Research

The answering of these issues is vital as it would be helpful in discovering the pros

and cons that are existent in IFRS for the investors and thereby helping the companies and the

investors to gain knowledge about the same and construct their strategies in an effective

manner.

1.2 Research Questions

The research questions have been constructed in order to have an idea about the

International Financial Reporting Standard and the companies that have been incorporating

the same. The research question is helpful in constructing the course and the path that would

be followed in order to complete the research in an effective manner. The research questions

consist of the issue that is needed to be answered by the paper. The research questions are

given as follows:

Q1. What are the various factors that can have an impact on IFRS and in that manner can

have an impact on the investors?

6IFRS PROS AND CONS FOR INVESTORS

Q2. What are the benefits and the hurdles that are associated with IFRS to the investors?

Q2. What are the benefits and the hurdles that are associated with IFRS to the investors?

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

7IFRS PROS AND CONS FOR INVESTORS

2.0 Literature review

IFRS (International Financial Reporting Standards) is set of the standards that are

created by IASB. Earlier the standards were known as the IAS (International Accounting

Standards) and were in use between the years 1973 and 2001. However, later it came to

known as IASB and in that way the new system created. On the basis of IFRS, the complete

financial statement shall include the income statement, balance sheet and the cash flow

statement of the company. It shall further include the changes in equity if the company

(Ahmed, Chalmers & Khlif, 2013). Data related to these are crucial in the process of decision

making of the investors as well as the management. Financial statement is key component for

the potential investors for taking the decisions regarding whether the company is feasible to

make investment or not. However, the policies of the entity also play crucial role in taking

any decisions regarding the accounting statement.

The accounting standard is shaped by the political and economic forces and it follows

the worldwide integration of the politics and markets that is generally driven by the reduction

in the costs associated with information processing and communications. It makes the

integration of financial reporting practice and standards nearly inevitable (Barth et al., 2012).

However, most of the political and market forces may remain local for foreseeable future,

therefore, it is not clear that how much convergence with regard to the practice in the actual

financial reporting will take place. Moreover, very little evidence or theory is there based on

which the assessment of disadvantages and advantages of the rules associated with the

uniform accounting within the country or internationally. Therefore the pros or cons of IFS

for the investors are hypothetical in some context. Adoption of IFRS at international level, in

the present years is frequently discussed and analyzed under the accounting field which in

2.0 Literature review

IFRS (International Financial Reporting Standards) is set of the standards that are

created by IASB. Earlier the standards were known as the IAS (International Accounting

Standards) and were in use between the years 1973 and 2001. However, later it came to

known as IASB and in that way the new system created. On the basis of IFRS, the complete

financial statement shall include the income statement, balance sheet and the cash flow

statement of the company. It shall further include the changes in equity if the company

(Ahmed, Chalmers & Khlif, 2013). Data related to these are crucial in the process of decision

making of the investors as well as the management. Financial statement is key component for

the potential investors for taking the decisions regarding whether the company is feasible to

make investment or not. However, the policies of the entity also play crucial role in taking

any decisions regarding the accounting statement.

The accounting standard is shaped by the political and economic forces and it follows

the worldwide integration of the politics and markets that is generally driven by the reduction

in the costs associated with information processing and communications. It makes the

integration of financial reporting practice and standards nearly inevitable (Barth et al., 2012).

However, most of the political and market forces may remain local for foreseeable future,

therefore, it is not clear that how much convergence with regard to the practice in the actual

financial reporting will take place. Moreover, very little evidence or theory is there based on

which the assessment of disadvantages and advantages of the rules associated with the

uniform accounting within the country or internationally. Therefore the pros or cons of IFS

for the investors are hypothetical in some context. Adoption of IFRS at international level, in

the present years is frequently discussed and analyzed under the accounting field which in

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

8IFRS PROS AND CONS FOR INVESTORS

turn generates the interests among the scholars, professionals, investors and the other users of

the financial information (Škoda & Bilka, 2012).

If the pros of adopting the IFRS are considered with regard to the investors, it can be

said that the IFRS delivers the information with more details as compared to the GAAP.

Further, it is easy and simple to use and it delivers the reporting with more detailed approach.

IFRS is flexible and it allows choosing the course of conduct and also offers for giving the

fair view with regard to the financial position of the company. Further, the IFRS allows any

company to adapt the changes with regard to the business environment in better way as they

do not have many guidelines. This approach influences usages of the professional judgements

which in turn enable the financial statements to be more transparent with flexible

interpreting; straightforward thinking and the standards of the reporting are produced as per

the expectation. Based on the judgement of IFRS supporters, business decisions are generally

relied on the professional judgements and not rely on the rules. Therefore, if any company

fails on disclosing the professional judgements with regard to the financial statements, it can

be misleading to the investors.

2.1.1 Focus on the investors

The single set of the accounting standards will definitely provide comparability and

will enable the companies for different countries for applying same standards. It will improve

the transparency and allow cross-border investment along with lower capital cost and greater

liquidity. Further, it will cut down costs and time for preparing the financial statements as per

various standards, regulations and will result into great savings with regard to long-term

capital. Using the uniform standards of accounting and and adopting the IFRS will eliminate

the expected different outcome of accounting from the application of various standards if US

does not move toward or adopt IFRS. Further, maintenance of multiple standards for

reporting purpose will increase the auditing and accounting costs and will deliver no value to

turn generates the interests among the scholars, professionals, investors and the other users of

the financial information (Škoda & Bilka, 2012).

If the pros of adopting the IFRS are considered with regard to the investors, it can be

said that the IFRS delivers the information with more details as compared to the GAAP.

Further, it is easy and simple to use and it delivers the reporting with more detailed approach.

IFRS is flexible and it allows choosing the course of conduct and also offers for giving the

fair view with regard to the financial position of the company. Further, the IFRS allows any

company to adapt the changes with regard to the business environment in better way as they

do not have many guidelines. This approach influences usages of the professional judgements

which in turn enable the financial statements to be more transparent with flexible

interpreting; straightforward thinking and the standards of the reporting are produced as per

the expectation. Based on the judgement of IFRS supporters, business decisions are generally

relied on the professional judgements and not rely on the rules. Therefore, if any company

fails on disclosing the professional judgements with regard to the financial statements, it can

be misleading to the investors.

2.1.1 Focus on the investors

The single set of the accounting standards will definitely provide comparability and

will enable the companies for different countries for applying same standards. It will improve

the transparency and allow cross-border investment along with lower capital cost and greater

liquidity. Further, it will cut down costs and time for preparing the financial statements as per

various standards, regulations and will result into great savings with regard to long-term

capital. Using the uniform standards of accounting and and adopting the IFRS will eliminate

the expected different outcome of accounting from the application of various standards if US

does not move toward or adopt IFRS. Further, maintenance of multiple standards for

reporting purpose will increase the auditing and accounting costs and will deliver no value to

9IFRS PROS AND CONS FOR INVESTORS

any nation. More than 100 nations have already adopted or under the process for adopting the

IFRS. Delays for adoption of IFRS by US will force the multi-national organizations to

prepare their primary reports applying IFRS that will result into parallel reports in the US

GAAP. It is estimated that there will requirement of huge investment for the transition to the

IFRS, however, the expenses will be one time investment as the financial reports will be

reduced from 3 to 1 which in turn will save money in the long term period (Christensen,

2012).

2.1.2 Recognition of loss in timeliness

Recognition of the loss immediately is the crucial factor of the IFRS as it is beneficial

to the investors as well as to the stakeholders and lenders of the company. Further, the

improvements in transparency and the recognition of loss for IFRS, generally enhances the

efficiency with regard to the contracts among the organizations and management which in

turn also improves corporate governance (Cherry & Schwartz, 2013). With the improvements

in the transparency, the lenders also become beneficial as it make the recognition of the loss

immediately as compulsory. Further, the recognition of timelier loss in IFRS identifies the

issues associated with the economic losses and that will be known to the shareholders and

other potential investors. The recognition of timelier loss will also enable the company to

review the book values of the equities, earnings, liabilities and assets.

2.1.3 Comparability

Convergence to the IFRS will improve comparability of the financial statement for the

companies all over the world. If all the organizations prepare and report their consolidated

financial statements under the one standard for reporting, it will improve comparability for

the investors as well as the shareholders who generally use the financial statements for

making various decisions. Owing to strong national identity of the IFRS reports, the IFRS

mainly have an impact on the how the companies identify, disclose and measure the items.

any nation. More than 100 nations have already adopted or under the process for adopting the

IFRS. Delays for adoption of IFRS by US will force the multi-national organizations to

prepare their primary reports applying IFRS that will result into parallel reports in the US

GAAP. It is estimated that there will requirement of huge investment for the transition to the

IFRS, however, the expenses will be one time investment as the financial reports will be

reduced from 3 to 1 which in turn will save money in the long term period (Christensen,

2012).

2.1.2 Recognition of loss in timeliness

Recognition of the loss immediately is the crucial factor of the IFRS as it is beneficial

to the investors as well as to the stakeholders and lenders of the company. Further, the

improvements in transparency and the recognition of loss for IFRS, generally enhances the

efficiency with regard to the contracts among the organizations and management which in

turn also improves corporate governance (Cherry & Schwartz, 2013). With the improvements

in the transparency, the lenders also become beneficial as it make the recognition of the loss

immediately as compulsory. Further, the recognition of timelier loss in IFRS identifies the

issues associated with the economic losses and that will be known to the shareholders and

other potential investors. The recognition of timelier loss will also enable the company to

review the book values of the equities, earnings, liabilities and assets.

2.1.3 Comparability

Convergence to the IFRS will improve comparability of the financial statement for the

companies all over the world. If all the organizations prepare and report their consolidated

financial statements under the one standard for reporting, it will improve comparability for

the investors as well as the shareholders who generally use the financial statements for

making various decisions. Owing to strong national identity of the IFRS reports, the IFRS

mainly have an impact on the how the companies identify, disclose and measure the items.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

10IFRS PROS AND CONS FOR INVESTORS

Further, as most of the companies already adopted the IFRS, it will minimize the alterations

from the earlier national standards which in turn will increase the ability of comparing the

financial statements all over the industries in the same sector (Marulkar, 2013).

If the cons of adopting IFRS with regard to the investors are considered, it is

recognized that the most crucial disadvantage of convergence to IFRS is the involvement of

cost that is associated with the application of IFRS by the multinational entities that includes

altering of internal systems for making it more compatible with new standards for reporting

and the costs associated with training. Further the issues associated with regulation of IFRS

in all the countries will not be possible owing to various reasons that is beyond the control of

IASC or IASB as they are not able to enforce IFRS application for all the countries all over

the world.

2.2.1 Requirement of high costs

Irrespective of the size, all the businesses feel that it will greatly impact them if they

adopt the IFRS. However, the small entities will not have enough resources for implementing

the changes associated with IFRS and will require trained staff or consultants or accountants

for assistance (Dvořáková, 2013). Therefore, they will have to bear more burdens in financial

terms as compared to the big companies.

2.2.2 Prone to manipulation

As any business can use only that method they wish to, it will lead to revealing the

desired results in the financial statements which in turn will lead to manipulation of profit. As

the new set of the standards needs the changes with regard to the ways in which the rules are

supposed to be applied to make it justifiable, chances are there that the businesses will come

up with various reasons for adopting the changes (Jiao et al., 2012). That is to say those more

Further, as most of the companies already adopted the IFRS, it will minimize the alterations

from the earlier national standards which in turn will increase the ability of comparing the

financial statements all over the industries in the same sector (Marulkar, 2013).

If the cons of adopting IFRS with regard to the investors are considered, it is

recognized that the most crucial disadvantage of convergence to IFRS is the involvement of

cost that is associated with the application of IFRS by the multinational entities that includes

altering of internal systems for making it more compatible with new standards for reporting

and the costs associated with training. Further the issues associated with regulation of IFRS

in all the countries will not be possible owing to various reasons that is beyond the control of

IASC or IASB as they are not able to enforce IFRS application for all the countries all over

the world.

2.2.1 Requirement of high costs

Irrespective of the size, all the businesses feel that it will greatly impact them if they

adopt the IFRS. However, the small entities will not have enough resources for implementing

the changes associated with IFRS and will require trained staff or consultants or accountants

for assistance (Dvořáková, 2013). Therefore, they will have to bear more burdens in financial

terms as compared to the big companies.

2.2.2 Prone to manipulation

As any business can use only that method they wish to, it will lead to revealing the

desired results in the financial statements which in turn will lead to manipulation of profit. As

the new set of the standards needs the changes with regard to the ways in which the rules are

supposed to be applied to make it justifiable, chances are there that the businesses will come

up with various reasons for adopting the changes (Jiao et al., 2012). That is to say those more

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

11IFRS PROS AND CONS FOR INVESTORS

strict rules will be implemented for assuring that all the companies will value the statements

in similar manner.

2.2.3 Not globally accepted

As US has not yet adopted IFRS, various other countries in the same way is chosen to

continue with the old standards. This means to say that the accounting system by foreign

companies dealing in these countries that have not adopted IFRS will have to face difficulties

as they have to prepare the financial statement using both the systems.

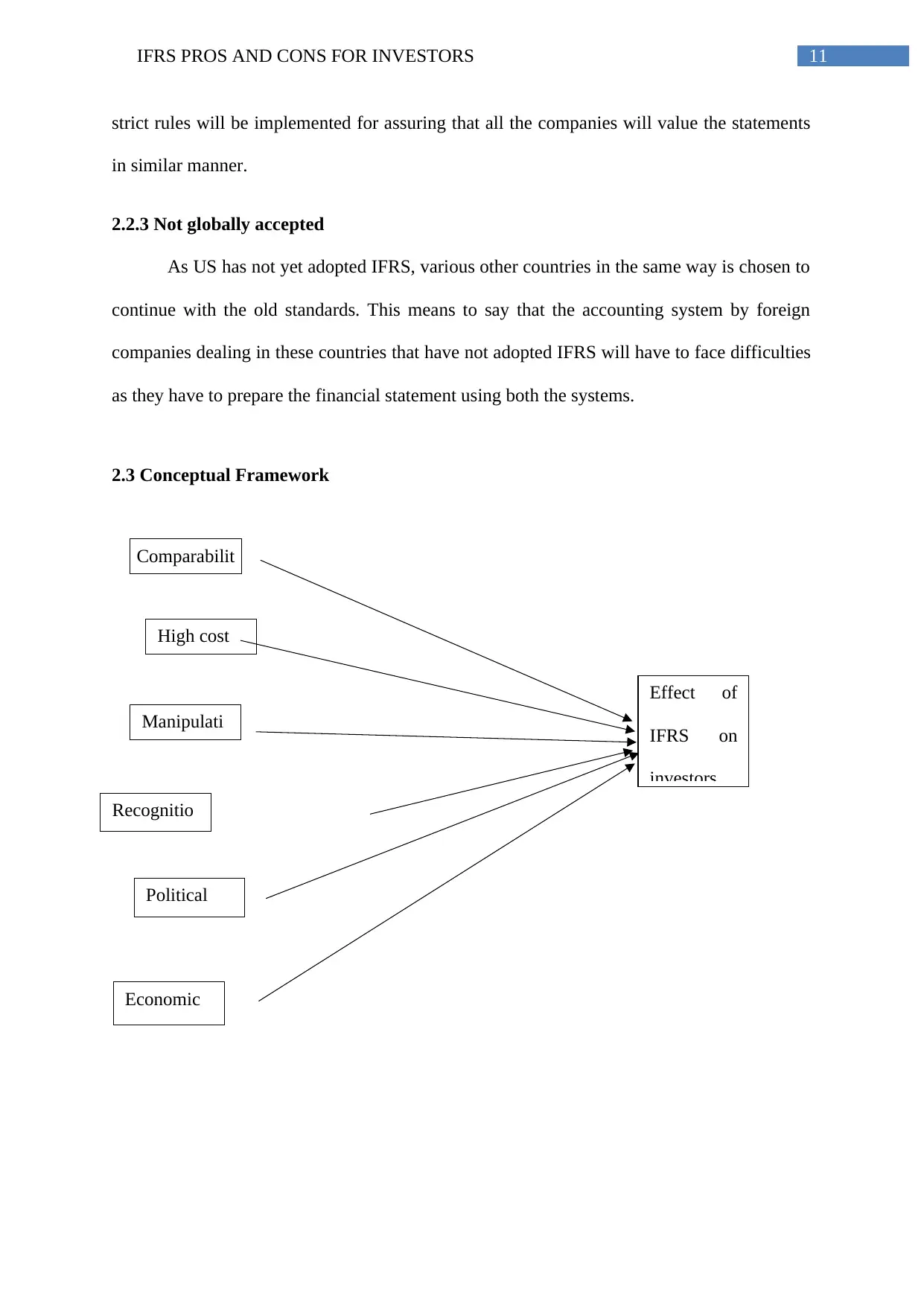

2.3 Conceptual Framework

Comparabilit

y

High cost

Manipulati

on

Recognitio

n of loss in

Political

effect

Economic

effect

Effect of

IFRS on

investors

strict rules will be implemented for assuring that all the companies will value the statements

in similar manner.

2.2.3 Not globally accepted

As US has not yet adopted IFRS, various other countries in the same way is chosen to

continue with the old standards. This means to say that the accounting system by foreign

companies dealing in these countries that have not adopted IFRS will have to face difficulties

as they have to prepare the financial statement using both the systems.

2.3 Conceptual Framework

Comparabilit

y

High cost

Manipulati

on

Recognitio

n of loss in

Political

effect

Economic

effect

Effect of

IFRS on

investors

12IFRS PROS AND CONS FOR INVESTORS

2.4 Summary

It is concluded from the above discussion that the application of IFRS helps the small

or new investors through making the standards of reporting better and simpler as it puts the

new and small investor in same position along with other professional investors in same

position. However, it is disadvantageous to the investors as IFRS is still not accepted globally

and the financial statements are prone to manipulation by the management.

2.4 Summary

It is concluded from the above discussion that the application of IFRS helps the small

or new investors through making the standards of reporting better and simpler as it puts the

new and small investor in same position along with other professional investors in same

position. However, it is disadvantageous to the investors as IFRS is still not accepted globally

and the financial statements are prone to manipulation by the management.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 25

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.