The Impact of Dividend Policy on Shareholders' Wealth

VerifiedAdded on 2022/08/16

|13

|9630

|16

AI Summary

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

www.pbr.co.in

The Impact of Dividend Policy on Shareholders' Wealth:

Evidence from Consumer Cyclical Sector in India

Pacific Business Review International

Volume 9 Issue 7, Jan. 2017

91

Abstract

Dividend policy (DP) is the most important to shareholders because it

can affect the share price and shareholders’ wealth (SW) as well.

Generally, higher dividends increase the market price of the share and

vice versa. Besides higher future dividends may also increase the

market price of share and thereby end up with wealth maximization of

the shareholders. Hence, the objective of the paper is to analyze the

impact of DP on SW of Consumer Cyclical Sector in India. Out of

13firms listed on Bombay Stock Exchange (BSE), 10 firms that have

been paying dividend consecutively for the recent past ten years are

considered for analysis. Besides descriptive statistics, Augmented

Dickey Fuller Test (ADF), Levin, Lin & Chu (LLC) t test, Philip Perron

(PP) Fisher x2 test, Im- Pesaran-Shin W (IPS-W) and Breitung test are

used. To test whether the data are stationary and to satisfy one pre-

condition for co-integration, Johansen Co-integration test is used.

Regression and Chow test are also applied to differentiate the impact

between pre and post financial meltdown periods. The results of the co-

integration test proves that there exists a stationary, long-run co-

integration between DP and SW. Regression result proves that DP has

significant impact on SW and the Chow test result proves that the

impact of DP on SW of Consumer Cyclical Sector has been

significantly affected by the event viz., the financial meltdown in

respect of variable dividend yield (DY) and not for the other selected

variables viz., dividend per share (DPS) and dividend payout (DPO).

Keywords:Dividend policy, Shareholders’ wealth, Financial

meltdown

JEL Classification:G 35, L 25, L 62

Introduction

The principal financial objective of any business enterprise is to

maximize the shareholders’ wealth (SW). The corporate function of

maximizing the SW assumes that managers operate in the best interests

of the shareholders. Therefore, it takes place when the returns to the

shareholders’ on the investment are maximized. In addition, these

returns are made up of capital gains in the form of increase in the share

prices, as well as dividends, which are made possible when the firm

generates adequate distributable profits.

When facing uncertainty, it is not always possible for a firm to achieve

its objectives. Wealth creation in entrepreneurial and established

organizations is a complex and challenging task. Therefore, in an ever-

Sandanam Gejalakshmi

Ph.D Research Scholar

Kanchi Mamunivar Centre for PG Studies

Puducherry

Dr. Ramachandran Azhagaiah

Associate Professor of Commerce

Avvaiyar Govt. College for Women

Karaikal

The Impact of Dividend Policy on Shareholders' Wealth:

Evidence from Consumer Cyclical Sector in India

Pacific Business Review International

Volume 9 Issue 7, Jan. 2017

91

Abstract

Dividend policy (DP) is the most important to shareholders because it

can affect the share price and shareholders’ wealth (SW) as well.

Generally, higher dividends increase the market price of the share and

vice versa. Besides higher future dividends may also increase the

market price of share and thereby end up with wealth maximization of

the shareholders. Hence, the objective of the paper is to analyze the

impact of DP on SW of Consumer Cyclical Sector in India. Out of

13firms listed on Bombay Stock Exchange (BSE), 10 firms that have

been paying dividend consecutively for the recent past ten years are

considered for analysis. Besides descriptive statistics, Augmented

Dickey Fuller Test (ADF), Levin, Lin & Chu (LLC) t test, Philip Perron

(PP) Fisher x2 test, Im- Pesaran-Shin W (IPS-W) and Breitung test are

used. To test whether the data are stationary and to satisfy one pre-

condition for co-integration, Johansen Co-integration test is used.

Regression and Chow test are also applied to differentiate the impact

between pre and post financial meltdown periods. The results of the co-

integration test proves that there exists a stationary, long-run co-

integration between DP and SW. Regression result proves that DP has

significant impact on SW and the Chow test result proves that the

impact of DP on SW of Consumer Cyclical Sector has been

significantly affected by the event viz., the financial meltdown in

respect of variable dividend yield (DY) and not for the other selected

variables viz., dividend per share (DPS) and dividend payout (DPO).

Keywords:Dividend policy, Shareholders’ wealth, Financial

meltdown

JEL Classification:G 35, L 25, L 62

Introduction

The principal financial objective of any business enterprise is to

maximize the shareholders’ wealth (SW). The corporate function of

maximizing the SW assumes that managers operate in the best interests

of the shareholders. Therefore, it takes place when the returns to the

shareholders’ on the investment are maximized. In addition, these

returns are made up of capital gains in the form of increase in the share

prices, as well as dividends, which are made possible when the firm

generates adequate distributable profits.

When facing uncertainty, it is not always possible for a firm to achieve

its objectives. Wealth creation in entrepreneurial and established

organizations is a complex and challenging task. Therefore, in an ever-

Sandanam Gejalakshmi

Ph.D Research Scholar

Kanchi Mamunivar Centre for PG Studies

Puducherry

Dr. Ramachandran Azhagaiah

Associate Professor of Commerce

Avvaiyar Govt. College for Women

Karaikal

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

www.pbr.co.inwww.pbr.co.in

Pacific Business Review International

92

changing environment, any organization wishing to Profile of the Study Sector - Consumer Cyclical Sect

maintain a competitive position and to satisfy its India

shareholders’ expectation should be engaged in planning Consumer cyclical sector includes industries such as

carefully every time when there is a need for. automotive, housing, entertainment and retail. The sector

The SW (Azhagaiah and Sabaripriya, 2008) is represented can further be divided into durable and non-durable sectors.

by market price of the firm’s common stock, which in turn, is Durable includes physical goods such as hardware or

the function of the firm’s investment, financing and vehicles, while consumer non-durable represents sector viz.,

dividend decision. The modern approach of financial entertainment or hotel services.

management provides a conceptual and analytical The performance of consumer cyclical sector is highly

framework for decision making, which emphasizes the related to the state of the economy. It represents goods and

effective use of resources to create SW. The optimal services that are not considered necessities, but for luxurious

dividend policy (DP) is one that maximizes the firm’s stock purchases. During contractions or recessions, investors

price; this leads to maximization of SW and thereby ensures have less disposable income to spend on consumer cyclical.

rapid economic growth. When the economy is expanding or booming, the sale of

Therefore, the present study is aimed at to study the long-run these goods rise as retail and leisure spending increase.

co-integration between the DP and the SW, and the impact of Consumer cyclical sector comprises textiles, automobiles,

DP on SW before and after an event viz., the global financial tyres, hotel, tourism and others as shown in figure A.

meltdown.

Figure A

Industries of Consumer Cyclical Sector

Source:http://www.investopedia.com

Review of Literature Priya and Nimalathasan (2013) revealed that dividend

payout had a significant impact on SW. Further, earnings per

Researchers have propounded many theories about a firm’s share (EPS), price earnings ratio (P/E) and market price to

value as well as the SW. There has been a substantial book value (MP_BV) had significant correlation with return

literature on the relationship between the DP and the SW and on assets (ROA); the P/E ratio had significant correlation

the impact of DP on SW. Several studies were made in with return on equity (ROE); EPS and the MP_BV were

respect of determinants of DP as well asSW in the developed significantly correlated with ROE of the selected hotels and

as well as in the developing economics like India. restaurants in Sri Lanka.

Vijaya kumar (2011) revealed that the sales and profit after Kumaresan (2014) found that there was a positive

tax of automobile firms had strong relationship with SW. relationship between return on equity, dividend per share

Devaki and Kamalaveni (2012)revealed that there was a and DP and SW of the firms while there was a negative

positive association between lagged dividend, earnings, relationship between retention ratio and SW of the listed

debt-equity ratio, sales size, age of the firm and institutional firms in hotel and travel sectors of Sri Lanka.

shareholding of the Indian corporate hotels. Ganesh et al.

(2013) found that the economic value added, market value Iqbal et al. (2014)found that the DP, firm size and firm

added, cash flow, and market to book value ratio were growth had significant positive impact on SW of selected

healthier in Ashok Leyland than that of the Tata Motors. manufacturing industries from three sectors viz., textile,

sugar and chemical.

Pacific Business Review International

92

changing environment, any organization wishing to Profile of the Study Sector - Consumer Cyclical Sect

maintain a competitive position and to satisfy its India

shareholders’ expectation should be engaged in planning Consumer cyclical sector includes industries such as

carefully every time when there is a need for. automotive, housing, entertainment and retail. The sector

The SW (Azhagaiah and Sabaripriya, 2008) is represented can further be divided into durable and non-durable sectors.

by market price of the firm’s common stock, which in turn, is Durable includes physical goods such as hardware or

the function of the firm’s investment, financing and vehicles, while consumer non-durable represents sector viz.,

dividend decision. The modern approach of financial entertainment or hotel services.

management provides a conceptual and analytical The performance of consumer cyclical sector is highly

framework for decision making, which emphasizes the related to the state of the economy. It represents goods and

effective use of resources to create SW. The optimal services that are not considered necessities, but for luxurious

dividend policy (DP) is one that maximizes the firm’s stock purchases. During contractions or recessions, investors

price; this leads to maximization of SW and thereby ensures have less disposable income to spend on consumer cyclical.

rapid economic growth. When the economy is expanding or booming, the sale of

Therefore, the present study is aimed at to study the long-run these goods rise as retail and leisure spending increase.

co-integration between the DP and the SW, and the impact of Consumer cyclical sector comprises textiles, automobiles,

DP on SW before and after an event viz., the global financial tyres, hotel, tourism and others as shown in figure A.

meltdown.

Figure A

Industries of Consumer Cyclical Sector

Source:http://www.investopedia.com

Review of Literature Priya and Nimalathasan (2013) revealed that dividend

payout had a significant impact on SW. Further, earnings per

Researchers have propounded many theories about a firm’s share (EPS), price earnings ratio (P/E) and market price to

value as well as the SW. There has been a substantial book value (MP_BV) had significant correlation with return

literature on the relationship between the DP and the SW and on assets (ROA); the P/E ratio had significant correlation

the impact of DP on SW. Several studies were made in with return on equity (ROE); EPS and the MP_BV were

respect of determinants of DP as well asSW in the developed significantly correlated with ROE of the selected hotels and

as well as in the developing economics like India. restaurants in Sri Lanka.

Vijaya kumar (2011) revealed that the sales and profit after Kumaresan (2014) found that there was a positive

tax of automobile firms had strong relationship with SW. relationship between return on equity, dividend per share

Devaki and Kamalaveni (2012)revealed that there was a and DP and SW of the firms while there was a negative

positive association between lagged dividend, earnings, relationship between retention ratio and SW of the listed

debt-equity ratio, sales size, age of the firm and institutional firms in hotel and travel sectors of Sri Lanka.

shareholding of the Indian corporate hotels. Ganesh et al.

(2013) found that the economic value added, market value Iqbal et al. (2014)found that the DP, firm size and firm

added, cash flow, and market to book value ratio were growth had significant positive impact on SW of selected

healthier in Ashok Leyland than that of the Tata Motors. manufacturing industries from three sectors viz., textile,

sugar and chemical.

93www.pbr.co.in

Volume 9 Issue 7, Jan. 2017

Ashvin (2012) found that there was a linear relationship Specific Objectives

between dividend decision and market price of stock of the To study the long-run relationship between dividend per

firm of selected auto sector. Ajanthan (2013) showed that the share, dividend payout as well as dividend yield and

DP was a crucial factor affecting the firm’s performance of shareholders’ wealth of the Consumer Cyclical Sector in

the listed hotels and restaurants in Sri Lanka. India.

The above literature provides a review of impact of DP on To estimate the impact of dividend variables along with

SW. The previous studies, by and large, were attempted to finance variables on shareholders’ wealth of the

study the long-run and short-run co-integration between DP Consumer Cyclical Sectorin India.

and SW and the impact of DP on SW. In the present study, an To estimate the influence of finance factors on

attempt has been made to estimate the difference in the shareholders’ wealthof the Consumer Cyclical Sector in

impact of DP on SW between pre and post financial India.

meltdown periods. To study the difference in the impact of dividend policy

Statement of the Problem on shareholders’ wealth of Consumer Cyclical Sector

Previous researchers have propounded many theories on DP between pre and post financial meltdown periods.

as well as on SW. Thus, the researchers are puzzled by the Hypotheses Developed for the Study

question, “whether SW was affected by DP? for many years. H01:“There is no co-integration between dividend per share

In the literature, there are different views regarding whether and shareholders’ wealth”.

DP affects firm’s share price in the long-run. Some studies H02:“There is no co-integration between dividend payout

showed that the firm’s value was not influenced by DP while and shareholders’ wealth”.

some others showed that DP affected firm’s value (Toby, H03: “There is no co-integration between dividend yield and

2014; and Baker Collins et al.2007). So, the present study shareholders’ wealth”.

has made an attempt to study the difference in the impact of H04:“There is no significant impact of dividend policy on

DP on SW between pre and post financial meltdown periods shareholders’ wealth”.

of the selected firms of Consumer Cyclical Sector in India. H05: “There is no significant difference in the impact of

Research Questions dividend per share on shareholders’ wealth between pre and

The research proposes to seek answers to the following post financial meltdown periods”.

questions: H06: “There is no significant difference in the impact of

Whether long-run relationship exists between dividend dividend payout on shareholders’ wealth between pre and

policy and shareholders’ wealth of listed firms of post financial meltdown periods”.

Consumer Cyclical Sector during the study period. H07:“There is no significant difference in the impact of

How do the dividend variables along with financial dividend yield on shareholders’ wealth between pre and post

variables influence the shareholders’ wealth of financial meltdown periods”.

Consumer Cyclical Sector? Research Methodology

How do finance variables (after removing dividend Data Source and Period of the Study

variables) influence the shareholders’ wealth of the The study used secondary data, which are collected from the

Consumer Cyclical Sector in India? capital market data base called Centre for Monitoring Indian

How does dividend policy impact shareholders’ wealth Economy Private Limited (Prowess CMIE) for a period of

before and after financial meltdown of Consumer 10 years on year to year basis from 2003-04 to 2012-13.

Cyclical Sector in India? Sampling Procedure and Technique

Objectives of the Study The study used multi-stage non-random sampling technique

To study the difference in the impact of dividend policy on and the different stages involved in it are shown in figure B.

shareholders’ wealth between before and after financial

meltdown periods.

Source: Compiled and edited data collected from PROWESS database provided by CMIE

Volume 9 Issue 7, Jan. 2017

Ashvin (2012) found that there was a linear relationship Specific Objectives

between dividend decision and market price of stock of the To study the long-run relationship between dividend per

firm of selected auto sector. Ajanthan (2013) showed that the share, dividend payout as well as dividend yield and

DP was a crucial factor affecting the firm’s performance of shareholders’ wealth of the Consumer Cyclical Sector in

the listed hotels and restaurants in Sri Lanka. India.

The above literature provides a review of impact of DP on To estimate the impact of dividend variables along with

SW. The previous studies, by and large, were attempted to finance variables on shareholders’ wealth of the

study the long-run and short-run co-integration between DP Consumer Cyclical Sectorin India.

and SW and the impact of DP on SW. In the present study, an To estimate the influence of finance factors on

attempt has been made to estimate the difference in the shareholders’ wealthof the Consumer Cyclical Sector in

impact of DP on SW between pre and post financial India.

meltdown periods. To study the difference in the impact of dividend policy

Statement of the Problem on shareholders’ wealth of Consumer Cyclical Sector

Previous researchers have propounded many theories on DP between pre and post financial meltdown periods.

as well as on SW. Thus, the researchers are puzzled by the Hypotheses Developed for the Study

question, “whether SW was affected by DP? for many years. H01:“There is no co-integration between dividend per share

In the literature, there are different views regarding whether and shareholders’ wealth”.

DP affects firm’s share price in the long-run. Some studies H02:“There is no co-integration between dividend payout

showed that the firm’s value was not influenced by DP while and shareholders’ wealth”.

some others showed that DP affected firm’s value (Toby, H03: “There is no co-integration between dividend yield and

2014; and Baker Collins et al.2007). So, the present study shareholders’ wealth”.

has made an attempt to study the difference in the impact of H04:“There is no significant impact of dividend policy on

DP on SW between pre and post financial meltdown periods shareholders’ wealth”.

of the selected firms of Consumer Cyclical Sector in India. H05: “There is no significant difference in the impact of

Research Questions dividend per share on shareholders’ wealth between pre and

The research proposes to seek answers to the following post financial meltdown periods”.

questions: H06: “There is no significant difference in the impact of

Whether long-run relationship exists between dividend dividend payout on shareholders’ wealth between pre and

policy and shareholders’ wealth of listed firms of post financial meltdown periods”.

Consumer Cyclical Sector during the study period. H07:“There is no significant difference in the impact of

How do the dividend variables along with financial dividend yield on shareholders’ wealth between pre and post

variables influence the shareholders’ wealth of financial meltdown periods”.

Consumer Cyclical Sector? Research Methodology

How do finance variables (after removing dividend Data Source and Period of the Study

variables) influence the shareholders’ wealth of the The study used secondary data, which are collected from the

Consumer Cyclical Sector in India? capital market data base called Centre for Monitoring Indian

How does dividend policy impact shareholders’ wealth Economy Private Limited (Prowess CMIE) for a period of

before and after financial meltdown of Consumer 10 years on year to year basis from 2003-04 to 2012-13.

Cyclical Sector in India? Sampling Procedure and Technique

Objectives of the Study The study used multi-stage non-random sampling technique

To study the difference in the impact of dividend policy on and the different stages involved in it are shown in figure B.

shareholders’ wealth between before and after financial

meltdown periods.

Source: Compiled and edited data collected from PROWESS database provided by CMIE

www.pbr.co.in94

Pacific Business Review International

Table-1- List of Firms Selected for the Study (Based on listed firms in BSE 200) for

the Study Period 2003-04 – 2012-13

Total No.

of Firms

(1)

Dividendnon-paying firms

(2)

Adequate Data

not availablein

the data source

(3)

Totalnumber of firms not

considered for the study

(4)= (2+3)

Ultimate sample firms

selected for the study

(5) =(1) - (4)

13 2 1 3 10

Source: Compiled data collected from PROWESS database provided by CMIE

Table 1 shows the number of firms of Consumer Cyclical statistical methods viz., Augmented Dickey Fuller Test,

sector listed in Bombay stock exchange (13), out of which Johansen Co-integration, Ordinary Least Square method

dividend non-paying firms (2), and firms for which adequate and Chow test are applied for analysis of data using Eviews

data were not in the data source (1) are eliminated, hence the 7 Econometrics software package.

ultimate number of sample firms considered for the study is Ratios used for Analysis

10 only.

The study used two important ratios viz., dividend related

Research Methods ratios and shareholders' wealth related ratios and details of

Besides various dividend variables and finance factors, the ratios used for analysis are shown in table2.

Table2- Dividend Variables (DPS, DPO and DY) used to Estimate the Impact of DP on SW (M

Sl.

No.

Classification of

DividendRatios Variables Description Inference

I Dividend related

ratios

1. Dividend per

share (DPS)

Dividend / Number

of equity shares

outstanding

The DPS reveals how well

earnings support the dividend

payout.

2. Dividend

payout ratio

(DPO)

Dividend per share /

Earnings per share

The DPO provides an idea as to

how well earnings support the

dividend payment. Mature firms

tend to have a higher payout ratio,

while low dividend payout ratio

enables the firm to keep a large

portion of its earnings for its

future growth.

3. Dividend

yield (DY)

Dividend per share /

Market price per

share

The DY shows how much a firm

pays out as dividend each year

relative to its share price. Higher

dividend yield has been

considered to be desirable for

most investors. A high share price

will lead to low dividend yield and

vice versa.

II

Shareholders'

wealth (SW)

related ratio

1. Market price

per share

(MPS)

Market capitalization

/ Number of equity

shares outstanding

High market price reflects that the

firms are in very good position

and low market price reflects

reverse.

Source: www.scibd.com/essays/finance.php; www.ukessays.com/essays/finance/current -assets-current-

liability.php

Table2 shows the variables used to study the co-integration Besides, the study also used finance variables viz., return on

between DP and SW and to analyze the impact of DP on SW capital employed (R_CE), return on net worth (R_NW),

before and after financial meltdown periods. Market price return on assets (ROA), return on long-term fund (R_LF),

per share (MPS) is considered as proxy response variable for return on equity (ROE), total debt to equity (TD_EQ), total

shareholders’ wealth (SW), while dividend per share (DPS), debt to total assets (TD_TA), total debt to fixed assets

dividend payout (DPO), and dividend yield (DY) are (TD_FA), equity multiplier (EM), proprietary ratio (PR),

considered as predictor dividend variables. total liabilities to net worth (TL_NW), current ratio (CR),

Pacific Business Review International

Table-1- List of Firms Selected for the Study (Based on listed firms in BSE 200) for

the Study Period 2003-04 – 2012-13

Total No.

of Firms

(1)

Dividendnon-paying firms

(2)

Adequate Data

not availablein

the data source

(3)

Totalnumber of firms not

considered for the study

(4)= (2+3)

Ultimate sample firms

selected for the study

(5) =(1) - (4)

13 2 1 3 10

Source: Compiled data collected from PROWESS database provided by CMIE

Table 1 shows the number of firms of Consumer Cyclical statistical methods viz., Augmented Dickey Fuller Test,

sector listed in Bombay stock exchange (13), out of which Johansen Co-integration, Ordinary Least Square method

dividend non-paying firms (2), and firms for which adequate and Chow test are applied for analysis of data using Eviews

data were not in the data source (1) are eliminated, hence the 7 Econometrics software package.

ultimate number of sample firms considered for the study is Ratios used for Analysis

10 only.

The study used two important ratios viz., dividend related

Research Methods ratios and shareholders' wealth related ratios and details of

Besides various dividend variables and finance factors, the ratios used for analysis are shown in table2.

Table2- Dividend Variables (DPS, DPO and DY) used to Estimate the Impact of DP on SW (M

Sl.

No.

Classification of

DividendRatios Variables Description Inference

I Dividend related

ratios

1. Dividend per

share (DPS)

Dividend / Number

of equity shares

outstanding

The DPS reveals how well

earnings support the dividend

payout.

2. Dividend

payout ratio

(DPO)

Dividend per share /

Earnings per share

The DPO provides an idea as to

how well earnings support the

dividend payment. Mature firms

tend to have a higher payout ratio,

while low dividend payout ratio

enables the firm to keep a large

portion of its earnings for its

future growth.

3. Dividend

yield (DY)

Dividend per share /

Market price per

share

The DY shows how much a firm

pays out as dividend each year

relative to its share price. Higher

dividend yield has been

considered to be desirable for

most investors. A high share price

will lead to low dividend yield and

vice versa.

II

Shareholders'

wealth (SW)

related ratio

1. Market price

per share

(MPS)

Market capitalization

/ Number of equity

shares outstanding

High market price reflects that the

firms are in very good position

and low market price reflects

reverse.

Source: www.scibd.com/essays/finance.php; www.ukessays.com/essays/finance/current -assets-current-

liability.php

Table2 shows the variables used to study the co-integration Besides, the study also used finance variables viz., return on

between DP and SW and to analyze the impact of DP on SW capital employed (R_CE), return on net worth (R_NW),

before and after financial meltdown periods. Market price return on assets (ROA), return on long-term fund (R_LF),

per share (MPS) is considered as proxy response variable for return on equity (ROE), total debt to equity (TD_EQ), total

shareholders’ wealth (SW), while dividend per share (DPS), debt to total assets (TD_TA), total debt to fixed assets

dividend payout (DPO), and dividend yield (DY) are (TD_FA), equity multiplier (EM), proprietary ratio (PR),

considered as predictor dividend variables. total liabilities to net worth (TL_NW), current ratio (CR),

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

95www.pbr.co.in

Volume 9 Issue 7, Jan. 2017

quick ratio (QR), earnings per share (EPS), price earnings 1990 and Osterwald-Lenum, 1992)

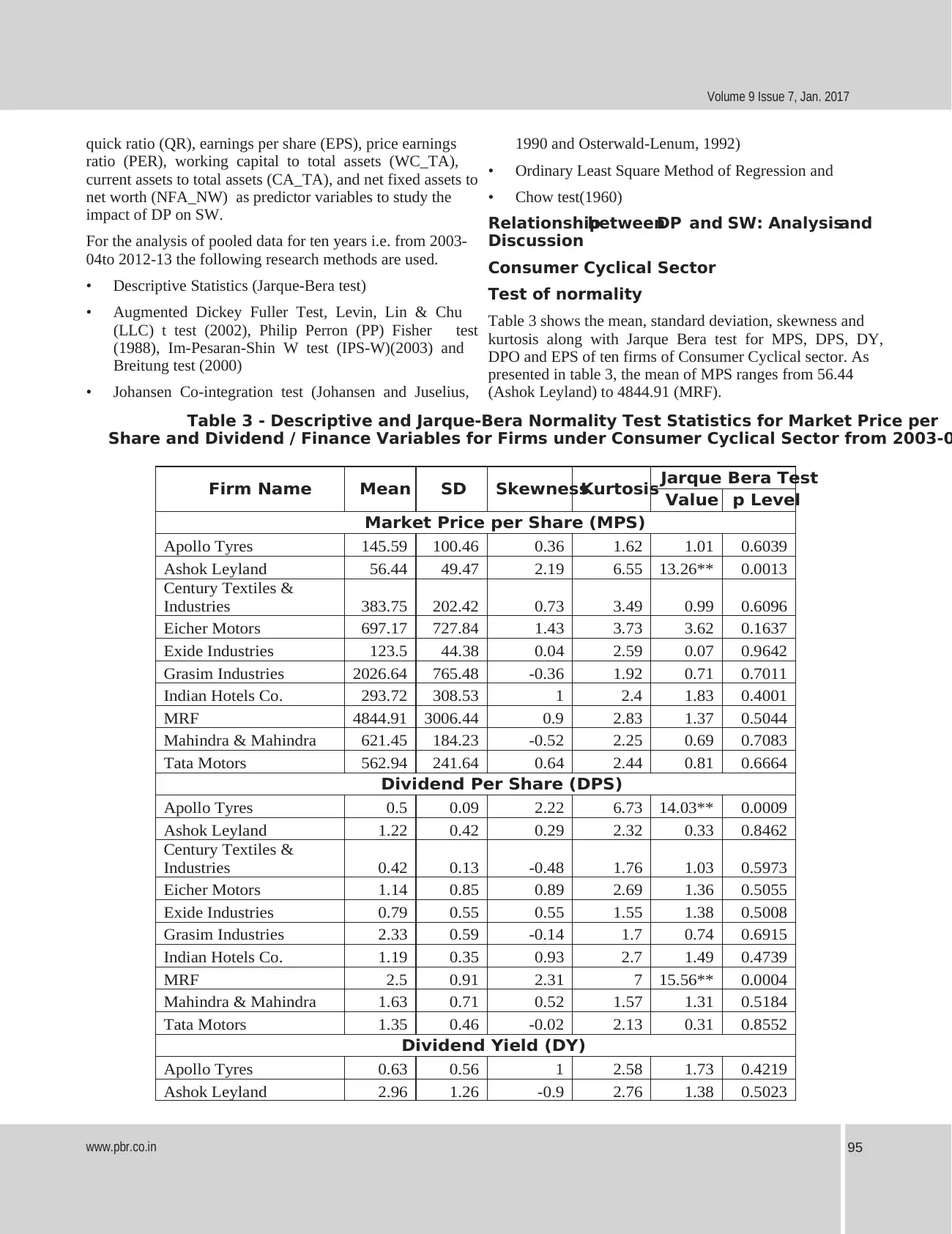

ratio (PER), working capital to total assets (WC_TA), • Ordinary Least Square Method of Regression and

current assets to total assets (CA_TA), and net fixed assets to

• Chow test(1960)net worth (NFA_NW) as predictor variables to study the

impact of DP on SW. RelationshipbetweenDP and SW: Analysisand

DiscussionFor the analysis of pooled data for ten years i.e. from 2003-

04to 2012-13 the following research methods are used. Consumer Cyclical Sector

• Descriptive Statistics (Jarque-Bera test) Test of normality

• Augmented Dickey Fuller Test, Levin, Lin & Chu Table 3 shows the mean, standard deviation, skewness and

(LLC) t test (2002), Philip Perron (PP) Fisher test kurtosis along with Jarque Bera test for MPS, DPS, DY,

(1988), Im-Pesaran-Shin W test (IPS-W)(2003) and DPO and EPS of ten firms of Consumer Cyclical sector. As

Breitung test (2000) presented in table 3, the mean of MPS ranges from 56.44

(Ashok Leyland) to 4844.91 (MRF).• Johansen Co-integration test (Johansen and Juselius,

Table 3 - Descriptive and Jarque-Bera Normality Test Statistics for Market Price per

Share and Dividend / Finance Variables for Firms under Consumer Cyclical Sector from 2003-0

Firm Name Mean SD SkewnessKurtosisJarque Bera Test

Value p Level

Market Price per Share (MPS)

Apollo Tyres 145.59 100.46 0.36 1.62 1.01 0.6039

Ashok Leyland 56.44 49.47 2.19 6.55 13.26** 0.0013

Century Textiles &

Industries 383.75 202.42 0.73 3.49 0.99 0.6096

Eicher Motors 697.17 727.84 1.43 3.73 3.62 0.1637

Exide Industries 123.5 44.38 0.04 2.59 0.07 0.9642

Grasim Industries 2026.64 765.48 -0.36 1.92 0.71 0.7011

Indian Hotels Co. 293.72 308.53 1 2.4 1.83 0.4001

MRF 4844.91 3006.44 0.9 2.83 1.37 0.5044

Mahindra & Mahindra 621.45 184.23 -0.52 2.25 0.69 0.7083

Tata Motors 562.94 241.64 0.64 2.44 0.81 0.6664

Dividend Per Share (DPS)

Apollo Tyres 0.5 0.09 2.22 6.73 14.03** 0.0009

Ashok Leyland 1.22 0.42 0.29 2.32 0.33 0.8462

Century Textiles &

Industries 0.42 0.13 -0.48 1.76 1.03 0.5973

Eicher Motors 1.14 0.85 0.89 2.69 1.36 0.5055

Exide Industries 0.79 0.55 0.55 1.55 1.38 0.5008

Grasim Industries 2.33 0.59 -0.14 1.7 0.74 0.6915

Indian Hotels Co. 1.19 0.35 0.93 2.7 1.49 0.4739

MRF 2.5 0.91 2.31 7 15.56** 0.0004

Mahindra & Mahindra 1.63 0.71 0.52 1.57 1.31 0.5184

Tata Motors 1.35 0.46 -0.02 2.13 0.31 0.8552

Dividend Yield (DY)

Apollo Tyres 0.63 0.56 1 2.58 1.73 0.4219

Ashok Leyland 2.96 1.26 -0.9 2.76 1.38 0.5023

Volume 9 Issue 7, Jan. 2017

quick ratio (QR), earnings per share (EPS), price earnings 1990 and Osterwald-Lenum, 1992)

ratio (PER), working capital to total assets (WC_TA), • Ordinary Least Square Method of Regression and

current assets to total assets (CA_TA), and net fixed assets to

• Chow test(1960)net worth (NFA_NW) as predictor variables to study the

impact of DP on SW. RelationshipbetweenDP and SW: Analysisand

DiscussionFor the analysis of pooled data for ten years i.e. from 2003-

04to 2012-13 the following research methods are used. Consumer Cyclical Sector

• Descriptive Statistics (Jarque-Bera test) Test of normality

• Augmented Dickey Fuller Test, Levin, Lin & Chu Table 3 shows the mean, standard deviation, skewness and

(LLC) t test (2002), Philip Perron (PP) Fisher test kurtosis along with Jarque Bera test for MPS, DPS, DY,

(1988), Im-Pesaran-Shin W test (IPS-W)(2003) and DPO and EPS of ten firms of Consumer Cyclical sector. As

Breitung test (2000) presented in table 3, the mean of MPS ranges from 56.44

(Ashok Leyland) to 4844.91 (MRF).• Johansen Co-integration test (Johansen and Juselius,

Table 3 - Descriptive and Jarque-Bera Normality Test Statistics for Market Price per

Share and Dividend / Finance Variables for Firms under Consumer Cyclical Sector from 2003-0

Firm Name Mean SD SkewnessKurtosisJarque Bera Test

Value p Level

Market Price per Share (MPS)

Apollo Tyres 145.59 100.46 0.36 1.62 1.01 0.6039

Ashok Leyland 56.44 49.47 2.19 6.55 13.26** 0.0013

Century Textiles &

Industries 383.75 202.42 0.73 3.49 0.99 0.6096

Eicher Motors 697.17 727.84 1.43 3.73 3.62 0.1637

Exide Industries 123.5 44.38 0.04 2.59 0.07 0.9642

Grasim Industries 2026.64 765.48 -0.36 1.92 0.71 0.7011

Indian Hotels Co. 293.72 308.53 1 2.4 1.83 0.4001

MRF 4844.91 3006.44 0.9 2.83 1.37 0.5044

Mahindra & Mahindra 621.45 184.23 -0.52 2.25 0.69 0.7083

Tata Motors 562.94 241.64 0.64 2.44 0.81 0.6664

Dividend Per Share (DPS)

Apollo Tyres 0.5 0.09 2.22 6.73 14.03** 0.0009

Ashok Leyland 1.22 0.42 0.29 2.32 0.33 0.8462

Century Textiles &

Industries 0.42 0.13 -0.48 1.76 1.03 0.5973

Eicher Motors 1.14 0.85 0.89 2.69 1.36 0.5055

Exide Industries 0.79 0.55 0.55 1.55 1.38 0.5008

Grasim Industries 2.33 0.59 -0.14 1.7 0.74 0.6915

Indian Hotels Co. 1.19 0.35 0.93 2.7 1.49 0.4739

MRF 2.5 0.91 2.31 7 15.56** 0.0004

Mahindra & Mahindra 1.63 0.71 0.52 1.57 1.31 0.5184

Tata Motors 1.35 0.46 -0.02 2.13 0.31 0.8552

Dividend Yield (DY)

Apollo Tyres 0.63 0.56 1 2.58 1.73 0.4219

Ashok Leyland 2.96 1.26 -0.9 2.76 1.38 0.5023

www.pbr.co.in96

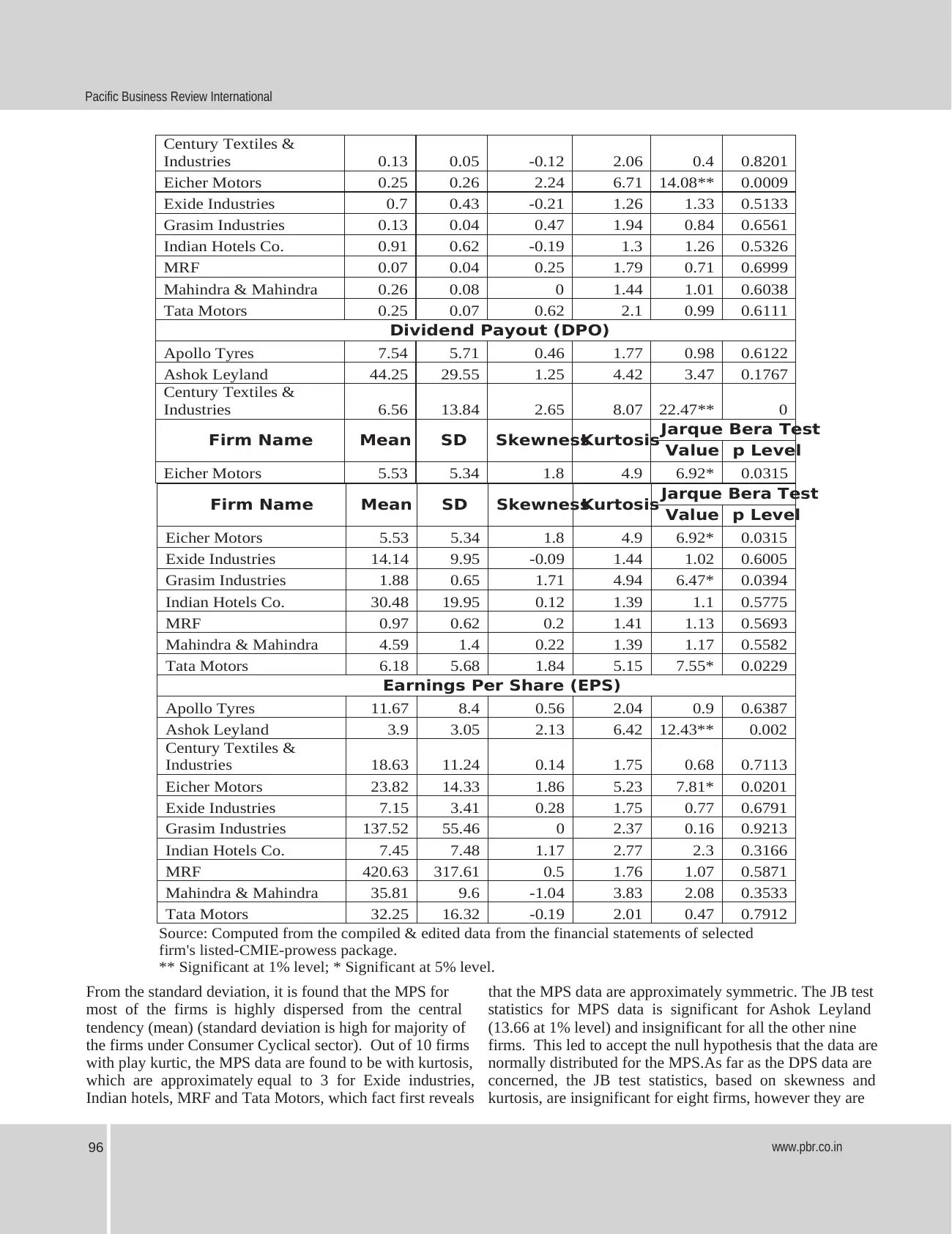

Pacific Business Review International

Century Textiles &

Industries 0.13 0.05 -0.12 2.06 0.4 0.8201

Eicher Motors 0.25 0.26 2.24 6.71 14.08** 0.0009

Exide Industries 0.7 0.43 -0.21 1.26 1.33 0.5133

Grasim Industries 0.13 0.04 0.47 1.94 0.84 0.6561

Indian Hotels Co. 0.91 0.62 -0.19 1.3 1.26 0.5326

MRF 0.07 0.04 0.25 1.79 0.71 0.6999

Mahindra & Mahindra 0.26 0.08 0 1.44 1.01 0.6038

Tata Motors 0.25 0.07 0.62 2.1 0.99 0.6111

Dividend Payout (DPO)

Apollo Tyres 7.54 5.71 0.46 1.77 0.98 0.6122

Ashok Leyland 44.25 29.55 1.25 4.42 3.47 0.1767

Century Textiles &

Industries 6.56 13.84 2.65 8.07 22.47** 0

Firm Name Mean SD SkewnessKurtosisJarque Bera Test

Value p Level

Eicher Motors 5.53 5.34 1.8 4.9 6.92* 0.0315

Firm Name Mean SD SkewnessKurtosisJarque Bera Test

Value p Level

Eicher Motors 5.53 5.34 1.8 4.9 6.92* 0.0315

Exide Industries 14.14 9.95 -0.09 1.44 1.02 0.6005

Grasim Industries 1.88 0.65 1.71 4.94 6.47* 0.0394

Indian Hotels Co. 30.48 19.95 0.12 1.39 1.1 0.5775

MRF 0.97 0.62 0.2 1.41 1.13 0.5693

Mahindra & Mahindra 4.59 1.4 0.22 1.39 1.17 0.5582

Tata Motors 6.18 5.68 1.84 5.15 7.55* 0.0229

Earnings Per Share (EPS)

Apollo Tyres 11.67 8.4 0.56 2.04 0.9 0.6387

Ashok Leyland 3.9 3.05 2.13 6.42 12.43** 0.002

Century Textiles &

Industries 18.63 11.24 0.14 1.75 0.68 0.7113

Eicher Motors 23.82 14.33 1.86 5.23 7.81* 0.0201

Exide Industries 7.15 3.41 0.28 1.75 0.77 0.6791

Grasim Industries 137.52 55.46 0 2.37 0.16 0.9213

Indian Hotels Co. 7.45 7.48 1.17 2.77 2.3 0.3166

MRF 420.63 317.61 0.5 1.76 1.07 0.5871

Mahindra & Mahindra 35.81 9.6 -1.04 3.83 2.08 0.3533

Tata Motors 32.25 16.32 -0.19 2.01 0.47 0.7912

Source: Computed from the compiled & edited data from the financial statements of selected

firm's listed-CMIE-prowess package.

** Significant at 1% level; * Significant at 5% level.

From the standard deviation, it is found that the MPS for that the MPS data are approximately symmetric. The JB test

most of the firms is highly dispersed from the central statistics for MPS data is significant for Ashok Leyland

tendency (mean) (standard deviation is high for majority of (13.66 at 1% level) and insignificant for all the other nine

the firms under Consumer Cyclical sector). Out of 10 firms firms. This led to accept the null hypothesis that the data are

with play kurtic, the MPS data are found to be with kurtosis, normally distributed for the MPS.As far as the DPS data are

which are approximately equal to 3 for Exide industries, concerned, the JB test statistics, based on skewness and

Indian hotels, MRF and Tata Motors, which fact first reveals kurtosis, are insignificant for eight firms, however they are

Pacific Business Review International

Century Textiles &

Industries 0.13 0.05 -0.12 2.06 0.4 0.8201

Eicher Motors 0.25 0.26 2.24 6.71 14.08** 0.0009

Exide Industries 0.7 0.43 -0.21 1.26 1.33 0.5133

Grasim Industries 0.13 0.04 0.47 1.94 0.84 0.6561

Indian Hotels Co. 0.91 0.62 -0.19 1.3 1.26 0.5326

MRF 0.07 0.04 0.25 1.79 0.71 0.6999

Mahindra & Mahindra 0.26 0.08 0 1.44 1.01 0.6038

Tata Motors 0.25 0.07 0.62 2.1 0.99 0.6111

Dividend Payout (DPO)

Apollo Tyres 7.54 5.71 0.46 1.77 0.98 0.6122

Ashok Leyland 44.25 29.55 1.25 4.42 3.47 0.1767

Century Textiles &

Industries 6.56 13.84 2.65 8.07 22.47** 0

Firm Name Mean SD SkewnessKurtosisJarque Bera Test

Value p Level

Eicher Motors 5.53 5.34 1.8 4.9 6.92* 0.0315

Firm Name Mean SD SkewnessKurtosisJarque Bera Test

Value p Level

Eicher Motors 5.53 5.34 1.8 4.9 6.92* 0.0315

Exide Industries 14.14 9.95 -0.09 1.44 1.02 0.6005

Grasim Industries 1.88 0.65 1.71 4.94 6.47* 0.0394

Indian Hotels Co. 30.48 19.95 0.12 1.39 1.1 0.5775

MRF 0.97 0.62 0.2 1.41 1.13 0.5693

Mahindra & Mahindra 4.59 1.4 0.22 1.39 1.17 0.5582

Tata Motors 6.18 5.68 1.84 5.15 7.55* 0.0229

Earnings Per Share (EPS)

Apollo Tyres 11.67 8.4 0.56 2.04 0.9 0.6387

Ashok Leyland 3.9 3.05 2.13 6.42 12.43** 0.002

Century Textiles &

Industries 18.63 11.24 0.14 1.75 0.68 0.7113

Eicher Motors 23.82 14.33 1.86 5.23 7.81* 0.0201

Exide Industries 7.15 3.41 0.28 1.75 0.77 0.6791

Grasim Industries 137.52 55.46 0 2.37 0.16 0.9213

Indian Hotels Co. 7.45 7.48 1.17 2.77 2.3 0.3166

MRF 420.63 317.61 0.5 1.76 1.07 0.5871

Mahindra & Mahindra 35.81 9.6 -1.04 3.83 2.08 0.3533

Tata Motors 32.25 16.32 -0.19 2.01 0.47 0.7912

Source: Computed from the compiled & edited data from the financial statements of selected

firm's listed-CMIE-prowess package.

** Significant at 1% level; * Significant at 5% level.

From the standard deviation, it is found that the MPS for that the MPS data are approximately symmetric. The JB test

most of the firms is highly dispersed from the central statistics for MPS data is significant for Ashok Leyland

tendency (mean) (standard deviation is high for majority of (13.66 at 1% level) and insignificant for all the other nine

the firms under Consumer Cyclical sector). Out of 10 firms firms. This led to accept the null hypothesis that the data are

with play kurtic, the MPS data are found to be with kurtosis, normally distributed for the MPS.As far as the DPS data are

which are approximately equal to 3 for Exide industries, concerned, the JB test statistics, based on skewness and

Indian hotels, MRF and Tata Motors, which fact first reveals kurtosis, are insignificant for eight firms, however they are

97www.pbr.co.in

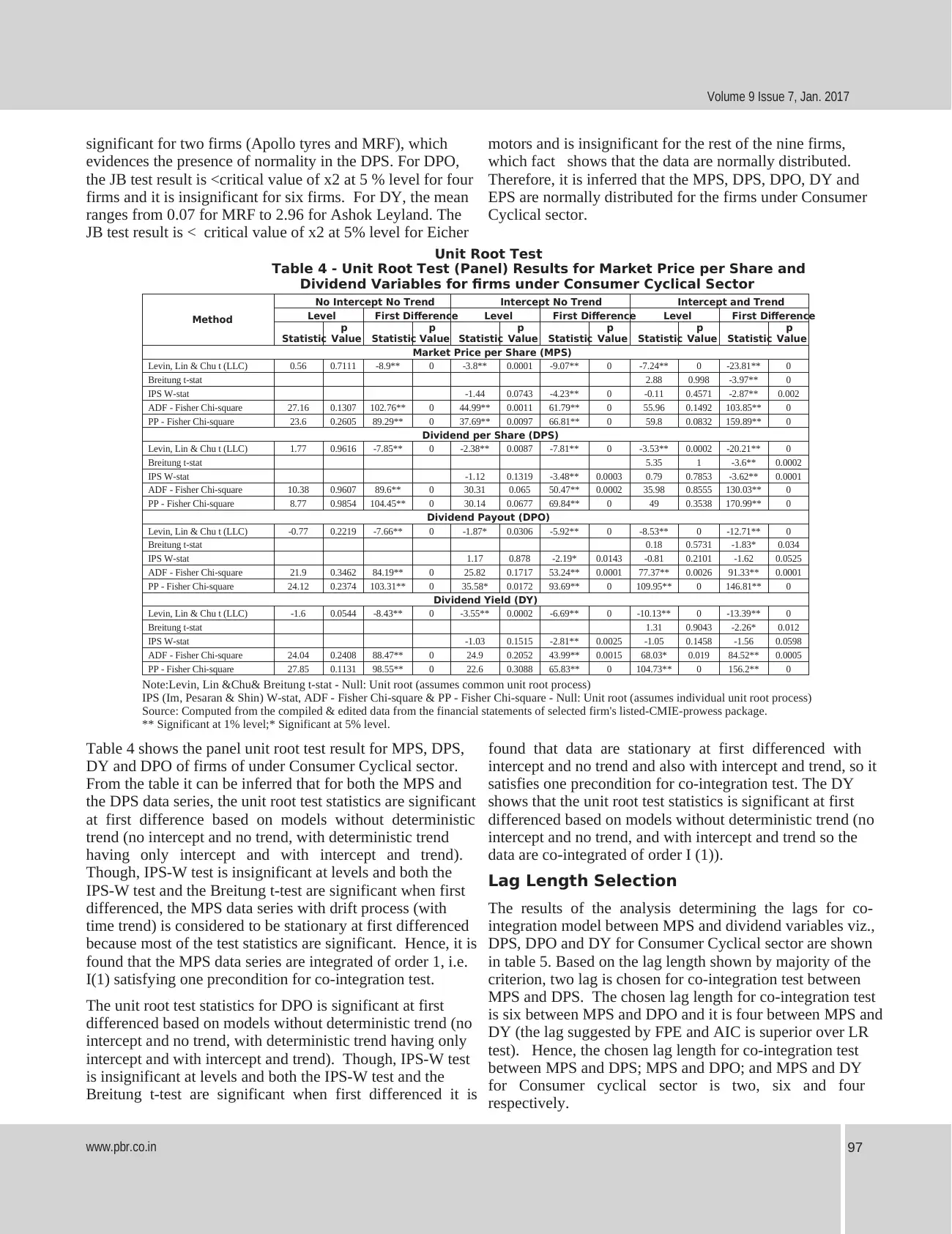

Volume 9 Issue 7, Jan. 2017

significant for two firms (Apollo tyres and MRF), which motors and is insignificant for the rest of the nine firms,

evidences the presence of normality in the DPS. For DPO, which fact shows that the data are normally distributed.

the JB test result is <critical value of x2 at 5 % level for four Therefore, it is inferred that the MPS, DPS, DPO, DY and

firms and it is insignificant for six firms. For DY, the mean EPS are normally distributed for the firms under Consumer

ranges from 0.07 for MRF to 2.96 for Ashok Leyland. The Cyclical sector.

JB test result is < critical value of x2 at 5% level for Eicher

Unit Root Test

Table 4 - Unit Root Test (Panel) Results for Market Price per Share and

Dividend Variables for firms under Consumer Cyclical Sector

Method

No Intercept No Trend Intercept No Trend Intercept and Trend

Level First Difference Level First Difference Level First Difference

Statistic

p

Value Statistic

p

Value Statistic

p

Value Statistic

p

Value Statistic

p

Value Statistic

p

Value

Market Price per Share (MPS)

Levin, Lin & Chu t (LLC) 0.56 0.7111 -8.9** 0 -3.8** 0.0001 -9.07** 0 -7.24** 0 -23.81** 0

Breitung t-stat 2.88 0.998 -3.97** 0

IPS W-stat -1.44 0.0743 -4.23** 0 -0.11 0.4571 -2.87** 0.002

ADF - Fisher Chi-square 27.16 0.1307 102.76** 0 44.99** 0.0011 61.79** 0 55.96 0.1492 103.85** 0

PP - Fisher Chi-square 23.6 0.2605 89.29** 0 37.69** 0.0097 66.81** 0 59.8 0.0832 159.89** 0

Dividend per Share (DPS)

Levin, Lin & Chu t (LLC) 1.77 0.9616 -7.85** 0 -2.38** 0.0087 -7.81** 0 -3.53** 0.0002 -20.21** 0

Breitung t-stat 5.35 1 -3.6** 0.0002

IPS W-stat -1.12 0.1319 -3.48** 0.0003 0.79 0.7853 -3.62** 0.0001

ADF - Fisher Chi-square 10.38 0.9607 89.6** 0 30.31 0.065 50.47** 0.0002 35.98 0.8555 130.03** 0

PP - Fisher Chi-square 8.77 0.9854 104.45** 0 30.14 0.0677 69.84** 0 49 0.3538 170.99** 0

Dividend Payout (DPO)

Levin, Lin & Chu t (LLC) -0.77 0.2219 -7.66** 0 -1.87* 0.0306 -5.92** 0 -8.53** 0 -12.71** 0

Breitung t-stat 0.18 0.5731 -1.83* 0.034

IPS W-stat 1.17 0.878 -2.19* 0.0143 -0.81 0.2101 -1.62 0.0525

ADF - Fisher Chi-square 21.9 0.3462 84.19** 0 25.82 0.1717 53.24** 0.0001 77.37** 0.0026 91.33** 0.0001

PP - Fisher Chi-square 24.12 0.2374 103.31** 0 35.58* 0.0172 93.69** 0 109.95** 0 146.81** 0

Dividend Yield (DY)

Levin, Lin & Chu t (LLC) -1.6 0.0544 -8.43** 0 -3.55** 0.0002 -6.69** 0 -10.13** 0 -13.39** 0

Breitung t-stat 1.31 0.9043 -2.26* 0.012

IPS W-stat -1.03 0.1515 -2.81** 0.0025 -1.05 0.1458 -1.56 0.0598

ADF - Fisher Chi-square 24.04 0.2408 88.47** 0 24.9 0.2052 43.99** 0.0015 68.03* 0.019 84.52** 0.0005

PP - Fisher Chi-square 27.85 0.1131 98.55** 0 22.6 0.3088 65.83** 0 104.73** 0 156.2** 0

Note:Levin, Lin &Chu& Breitung t-stat - Null: Unit root (assumes common unit root process)

IPS (Im, Pesaran & Shin) W-stat, ADF - Fisher Chi-square & PP - Fisher Chi-square - Null: Unit root (assumes individual unit root process)

Source: Computed from the compiled & edited data from the financial statements of selected firm's listed-CMIE-prowess package.

** Significant at 1% level;* Significant at 5% level.

Table 4 shows the panel unit root test result for MPS, DPS, found that data are stationary at first differenced with

DY and DPO of firms of under Consumer Cyclical sector. intercept and no trend and also with intercept and trend, so it

From the table it can be inferred that for both the MPS and satisfies one precondition for co-integration test. The DY

the DPS data series, the unit root test statistics are significant shows that the unit root test statistics is significant at first

at first difference based on models without deterministic differenced based on models without deterministic trend (no

trend (no intercept and no trend, with deterministic trend intercept and no trend, and with intercept and trend so the

having only intercept and with intercept and trend). data are co-integrated of order I (1)).

Though, IPS-W test is insignificant at levels and both the Lag Length Selection

IPS-W test and the Breitung t-test are significant when first

The results of the analysis determining the lags for co-differenced, the MPS data series with drift process (with

integration model between MPS and dividend variables viz.,time trend) is considered to be stationary at first differenced

DPS, DPO and DY for Consumer Cyclical sector are shownbecause most of the test statistics are significant. Hence, it is

in table 5. Based on the lag length shown by majority of thefound that the MPS data series are integrated of order 1, i.e.

criterion, two lag is chosen for co-integration test betweenI(1) satisfying one precondition for co-integration test.

MPS and DPS. The chosen lag length for co-integration test

The unit root test statistics for DPO is significant at first is six between MPS and DPO and it is four between MPS and

differenced based on models without deterministic trend (no DY (the lag suggested by FPE and AIC is superior over LR

intercept and no trend, with deterministic trend having only test). Hence, the chosen lag length for co-integration test

intercept and with intercept and trend). Though, IPS-W test between MPS and DPS; MPS and DPO; and MPS and DY

is insignificant at levels and both the IPS-W test and the for Consumer cyclical sector is two, six and four

Breitung t-test are significant when first differenced it is respectively.

Volume 9 Issue 7, Jan. 2017

significant for two firms (Apollo tyres and MRF), which motors and is insignificant for the rest of the nine firms,

evidences the presence of normality in the DPS. For DPO, which fact shows that the data are normally distributed.

the JB test result is <critical value of x2 at 5 % level for four Therefore, it is inferred that the MPS, DPS, DPO, DY and

firms and it is insignificant for six firms. For DY, the mean EPS are normally distributed for the firms under Consumer

ranges from 0.07 for MRF to 2.96 for Ashok Leyland. The Cyclical sector.

JB test result is < critical value of x2 at 5% level for Eicher

Unit Root Test

Table 4 - Unit Root Test (Panel) Results for Market Price per Share and

Dividend Variables for firms under Consumer Cyclical Sector

Method

No Intercept No Trend Intercept No Trend Intercept and Trend

Level First Difference Level First Difference Level First Difference

Statistic

p

Value Statistic

p

Value Statistic

p

Value Statistic

p

Value Statistic

p

Value Statistic

p

Value

Market Price per Share (MPS)

Levin, Lin & Chu t (LLC) 0.56 0.7111 -8.9** 0 -3.8** 0.0001 -9.07** 0 -7.24** 0 -23.81** 0

Breitung t-stat 2.88 0.998 -3.97** 0

IPS W-stat -1.44 0.0743 -4.23** 0 -0.11 0.4571 -2.87** 0.002

ADF - Fisher Chi-square 27.16 0.1307 102.76** 0 44.99** 0.0011 61.79** 0 55.96 0.1492 103.85** 0

PP - Fisher Chi-square 23.6 0.2605 89.29** 0 37.69** 0.0097 66.81** 0 59.8 0.0832 159.89** 0

Dividend per Share (DPS)

Levin, Lin & Chu t (LLC) 1.77 0.9616 -7.85** 0 -2.38** 0.0087 -7.81** 0 -3.53** 0.0002 -20.21** 0

Breitung t-stat 5.35 1 -3.6** 0.0002

IPS W-stat -1.12 0.1319 -3.48** 0.0003 0.79 0.7853 -3.62** 0.0001

ADF - Fisher Chi-square 10.38 0.9607 89.6** 0 30.31 0.065 50.47** 0.0002 35.98 0.8555 130.03** 0

PP - Fisher Chi-square 8.77 0.9854 104.45** 0 30.14 0.0677 69.84** 0 49 0.3538 170.99** 0

Dividend Payout (DPO)

Levin, Lin & Chu t (LLC) -0.77 0.2219 -7.66** 0 -1.87* 0.0306 -5.92** 0 -8.53** 0 -12.71** 0

Breitung t-stat 0.18 0.5731 -1.83* 0.034

IPS W-stat 1.17 0.878 -2.19* 0.0143 -0.81 0.2101 -1.62 0.0525

ADF - Fisher Chi-square 21.9 0.3462 84.19** 0 25.82 0.1717 53.24** 0.0001 77.37** 0.0026 91.33** 0.0001

PP - Fisher Chi-square 24.12 0.2374 103.31** 0 35.58* 0.0172 93.69** 0 109.95** 0 146.81** 0

Dividend Yield (DY)

Levin, Lin & Chu t (LLC) -1.6 0.0544 -8.43** 0 -3.55** 0.0002 -6.69** 0 -10.13** 0 -13.39** 0

Breitung t-stat 1.31 0.9043 -2.26* 0.012

IPS W-stat -1.03 0.1515 -2.81** 0.0025 -1.05 0.1458 -1.56 0.0598

ADF - Fisher Chi-square 24.04 0.2408 88.47** 0 24.9 0.2052 43.99** 0.0015 68.03* 0.019 84.52** 0.0005

PP - Fisher Chi-square 27.85 0.1131 98.55** 0 22.6 0.3088 65.83** 0 104.73** 0 156.2** 0

Note:Levin, Lin &Chu& Breitung t-stat - Null: Unit root (assumes common unit root process)

IPS (Im, Pesaran & Shin) W-stat, ADF - Fisher Chi-square & PP - Fisher Chi-square - Null: Unit root (assumes individual unit root process)

Source: Computed from the compiled & edited data from the financial statements of selected firm's listed-CMIE-prowess package.

** Significant at 1% level;* Significant at 5% level.

Table 4 shows the panel unit root test result for MPS, DPS, found that data are stationary at first differenced with

DY and DPO of firms of under Consumer Cyclical sector. intercept and no trend and also with intercept and trend, so it

From the table it can be inferred that for both the MPS and satisfies one precondition for co-integration test. The DY

the DPS data series, the unit root test statistics are significant shows that the unit root test statistics is significant at first

at first difference based on models without deterministic differenced based on models without deterministic trend (no

trend (no intercept and no trend, with deterministic trend intercept and no trend, and with intercept and trend so the

having only intercept and with intercept and trend). data are co-integrated of order I (1)).

Though, IPS-W test is insignificant at levels and both the Lag Length Selection

IPS-W test and the Breitung t-test are significant when first

The results of the analysis determining the lags for co-differenced, the MPS data series with drift process (with

integration model between MPS and dividend variables viz.,time trend) is considered to be stationary at first differenced

DPS, DPO and DY for Consumer Cyclical sector are shownbecause most of the test statistics are significant. Hence, it is

in table 5. Based on the lag length shown by majority of thefound that the MPS data series are integrated of order 1, i.e.

criterion, two lag is chosen for co-integration test betweenI(1) satisfying one precondition for co-integration test.

MPS and DPS. The chosen lag length for co-integration test

The unit root test statistics for DPO is significant at first is six between MPS and DPO and it is four between MPS and

differenced based on models without deterministic trend (no DY (the lag suggested by FPE and AIC is superior over LR

intercept and no trend, with deterministic trend having only test). Hence, the chosen lag length for co-integration test

intercept and with intercept and trend). Though, IPS-W test between MPS and DPS; MPS and DPO; and MPS and DY

is insignificant at levels and both the IPS-W test and the for Consumer cyclical sector is two, six and four

Breitung t-test are significant when first differenced it is respectively.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

www.pbr.co.in98

Pacific Business Review International

Table 5 - Lag Length Selection Criteria for Co-integration Test for

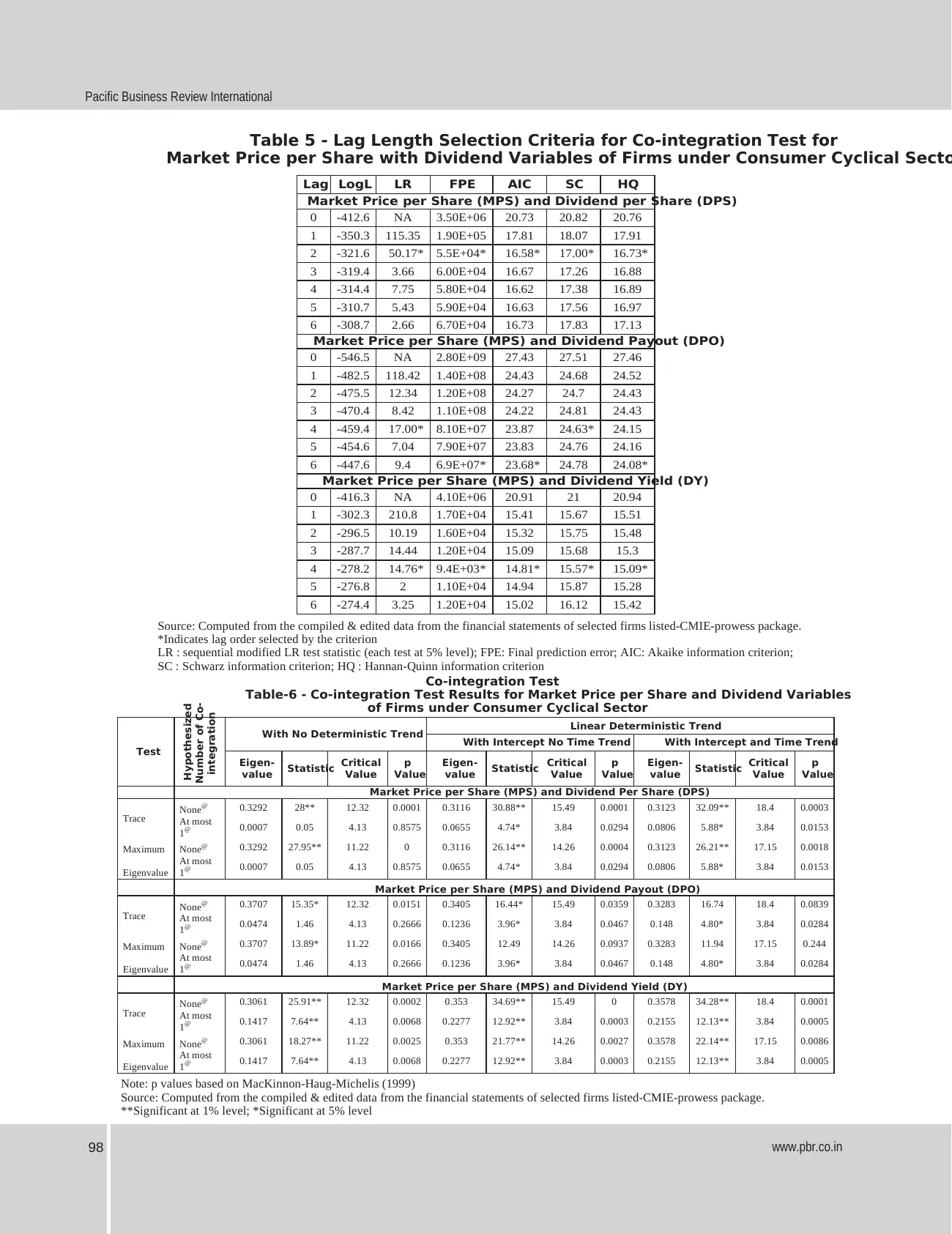

Market Price per Share with Dividend Variables of Firms under Consumer Cyclical Secto

Lag LogL LR FPE AIC SC HQ

Market Price per Share (MPS) and Dividend per Share (DPS)

0 -412.6 NA 3.50E+06 20.73 20.82 20.76

1 -350.3 115.35 1.90E+05 17.81 18.07 17.91

2 -321.6 50.17* 5.5E+04* 16.58* 17.00* 16.73*

3 -319.4 3.66 6.00E+04 16.67 17.26 16.88

4 -314.4 7.75 5.80E+04 16.62 17.38 16.89

5 -310.7 5.43 5.90E+04 16.63 17.56 16.97

6 -308.7 2.66 6.70E+04 16.73 17.83 17.13

Market Price per Share (MPS) and Dividend Payout (DPO)

0 -546.5 NA 2.80E+09 27.43 27.51 27.46

1 -482.5 118.42 1.40E+08 24.43 24.68 24.52

2 -475.5 12.34 1.20E+08 24.27 24.7 24.43

3 -470.4 8.42 1.10E+08 24.22 24.81 24.43

4 -459.4 17.00* 8.10E+07 23.87 24.63* 24.15

5 -454.6 7.04 7.90E+07 23.83 24.76 24.16

6 -447.6 9.4 6.9E+07* 23.68* 24.78 24.08*

Market Price per Share (MPS) and Dividend Yield (DY)

0 -416.3 NA 4.10E+06 20.91 21 20.94

1 -302.3 210.8 1.70E+04 15.41 15.67 15.51

2 -296.5 10.19 1.60E+04 15.32 15.75 15.48

3 -287.7 14.44 1.20E+04 15.09 15.68 15.3

4 -278.2 14.76* 9.4E+03* 14.81* 15.57* 15.09*

5 -276.8 2 1.10E+04 14.94 15.87 15.28

6 -274.4 3.25 1.20E+04 15.02 16.12 15.42

Source: Computed from the compiled & edited data from the financial statements of selected firms listed-CMIE-prowess package.

*Indicates lag order selected by the criterion

LR : sequential modified LR test statistic (each test at 5% level); FPE: Final prediction error; AIC: Akaike information criterion;

SC : Schwarz information criterion; HQ : Hannan-Quinn information criterion

Co-integration Test

Table-6 - Co-integration Test Results for Market Price per Share and Dividend Variables

of Firms under Consumer Cyclical Sector

Test

Hypothesized

Number of Co-

integration

With No Deterministic Trend Linear Deterministic Trend

With Intercept No Time Trend With Intercept and Time Trend

Eigen-

value Statistic Critical

Value

p

Value

Eigen-

value Statistic Critical

Value

p

Value

Eigen-

value Statistic Critical

Value

p

Value

Market Price per Share (MPS) and Dividend Per Share (DPS)

Trace None@ 0.3292 28** 12.32 0.0001 0.3116 30.88** 15.49 0.0001 0.3123 32.09** 18.4 0.0003

At most

1@ 0.0007 0.05 4.13 0.8575 0.0655 4.74* 3.84 0.0294 0.0806 5.88* 3.84 0.0153

Maximum None@ 0.3292 27.95** 11.22 0 0.3116 26.14** 14.26 0.0004 0.3123 26.21** 17.15 0.0018

Eigenvalue

At most

1@ 0.0007 0.05 4.13 0.8575 0.0655 4.74* 3.84 0.0294 0.0806 5.88* 3.84 0.0153

Market Price per Share (MPS) and Dividend Payout (DPO)

Trace None@ 0.3707 15.35* 12.32 0.0151 0.3405 16.44* 15.49 0.0359 0.3283 16.74 18.4 0.0839

At most

1@ 0.0474 1.46 4.13 0.2666 0.1236 3.96* 3.84 0.0467 0.148 4.80* 3.84 0.0284

Maximum None@ 0.3707 13.89* 11.22 0.0166 0.3405 12.49 14.26 0.0937 0.3283 11.94 17.15 0.244

Eigenvalue

At most

1@ 0.0474 1.46 4.13 0.2666 0.1236 3.96* 3.84 0.0467 0.148 4.80* 3.84 0.0284

Market Price per Share (MPS) and Dividend Yield (DY)

Trace None@ 0.3061 25.91** 12.32 0.0002 0.353 34.69** 15.49 0 0.3578 34.28** 18.4 0.0001

At most

1@ 0.1417 7.64** 4.13 0.0068 0.2277 12.92** 3.84 0.0003 0.2155 12.13** 3.84 0.0005

Maximum None@ 0.3061 18.27** 11.22 0.0025 0.353 21.77** 14.26 0.0027 0.3578 22.14** 17.15 0.0086

Eigenvalue

At most

1@ 0.1417 7.64** 4.13 0.0068 0.2277 12.92** 3.84 0.0003 0.2155 12.13** 3.84 0.0005

Note: p values based on MacKinnon-Haug-Michelis (1999)

Source: Computed from the compiled & edited data from the financial statements of selected firms listed-CMIE-prowess package.

**Significant at 1% level; *Significant at 5% level

Pacific Business Review International

Table 5 - Lag Length Selection Criteria for Co-integration Test for

Market Price per Share with Dividend Variables of Firms under Consumer Cyclical Secto

Lag LogL LR FPE AIC SC HQ

Market Price per Share (MPS) and Dividend per Share (DPS)

0 -412.6 NA 3.50E+06 20.73 20.82 20.76

1 -350.3 115.35 1.90E+05 17.81 18.07 17.91

2 -321.6 50.17* 5.5E+04* 16.58* 17.00* 16.73*

3 -319.4 3.66 6.00E+04 16.67 17.26 16.88

4 -314.4 7.75 5.80E+04 16.62 17.38 16.89

5 -310.7 5.43 5.90E+04 16.63 17.56 16.97

6 -308.7 2.66 6.70E+04 16.73 17.83 17.13

Market Price per Share (MPS) and Dividend Payout (DPO)

0 -546.5 NA 2.80E+09 27.43 27.51 27.46

1 -482.5 118.42 1.40E+08 24.43 24.68 24.52

2 -475.5 12.34 1.20E+08 24.27 24.7 24.43

3 -470.4 8.42 1.10E+08 24.22 24.81 24.43

4 -459.4 17.00* 8.10E+07 23.87 24.63* 24.15

5 -454.6 7.04 7.90E+07 23.83 24.76 24.16

6 -447.6 9.4 6.9E+07* 23.68* 24.78 24.08*

Market Price per Share (MPS) and Dividend Yield (DY)

0 -416.3 NA 4.10E+06 20.91 21 20.94

1 -302.3 210.8 1.70E+04 15.41 15.67 15.51

2 -296.5 10.19 1.60E+04 15.32 15.75 15.48

3 -287.7 14.44 1.20E+04 15.09 15.68 15.3

4 -278.2 14.76* 9.4E+03* 14.81* 15.57* 15.09*

5 -276.8 2 1.10E+04 14.94 15.87 15.28

6 -274.4 3.25 1.20E+04 15.02 16.12 15.42

Source: Computed from the compiled & edited data from the financial statements of selected firms listed-CMIE-prowess package.

*Indicates lag order selected by the criterion

LR : sequential modified LR test statistic (each test at 5% level); FPE: Final prediction error; AIC: Akaike information criterion;

SC : Schwarz information criterion; HQ : Hannan-Quinn information criterion

Co-integration Test

Table-6 - Co-integration Test Results for Market Price per Share and Dividend Variables

of Firms under Consumer Cyclical Sector

Test

Hypothesized

Number of Co-

integration

With No Deterministic Trend Linear Deterministic Trend

With Intercept No Time Trend With Intercept and Time Trend

Eigen-

value Statistic Critical

Value

p

Value

Eigen-

value Statistic Critical

Value

p

Value

Eigen-

value Statistic Critical

Value

p

Value

Market Price per Share (MPS) and Dividend Per Share (DPS)

Trace None@ 0.3292 28** 12.32 0.0001 0.3116 30.88** 15.49 0.0001 0.3123 32.09** 18.4 0.0003

At most

1@ 0.0007 0.05 4.13 0.8575 0.0655 4.74* 3.84 0.0294 0.0806 5.88* 3.84 0.0153

Maximum None@ 0.3292 27.95** 11.22 0 0.3116 26.14** 14.26 0.0004 0.3123 26.21** 17.15 0.0018

Eigenvalue

At most

1@ 0.0007 0.05 4.13 0.8575 0.0655 4.74* 3.84 0.0294 0.0806 5.88* 3.84 0.0153

Market Price per Share (MPS) and Dividend Payout (DPO)

Trace None@ 0.3707 15.35* 12.32 0.0151 0.3405 16.44* 15.49 0.0359 0.3283 16.74 18.4 0.0839

At most

1@ 0.0474 1.46 4.13 0.2666 0.1236 3.96* 3.84 0.0467 0.148 4.80* 3.84 0.0284

Maximum None@ 0.3707 13.89* 11.22 0.0166 0.3405 12.49 14.26 0.0937 0.3283 11.94 17.15 0.244

Eigenvalue

At most

1@ 0.0474 1.46 4.13 0.2666 0.1236 3.96* 3.84 0.0467 0.148 4.80* 3.84 0.0284

Market Price per Share (MPS) and Dividend Yield (DY)

Trace None@ 0.3061 25.91** 12.32 0.0002 0.353 34.69** 15.49 0 0.3578 34.28** 18.4 0.0001

At most

1@ 0.1417 7.64** 4.13 0.0068 0.2277 12.92** 3.84 0.0003 0.2155 12.13** 3.84 0.0005

Maximum None@ 0.3061 18.27** 11.22 0.0025 0.353 21.77** 14.26 0.0027 0.3578 22.14** 17.15 0.0086

Eigenvalue

At most

1@ 0.1417 7.64** 4.13 0.0068 0.2277 12.92** 3.84 0.0003 0.2155 12.13** 3.84 0.0005

Note: p values based on MacKinnon-Haug-Michelis (1999)

Source: Computed from the compiled & edited data from the financial statements of selected firms listed-CMIE-prowess package.

**Significant at 1% level; *Significant at 5% level

99www.pbr.co.in

Volume 9 Issue 7, Jan. 2017

The results of co-integration analysis of Consumer Cyclical The DY and the MPS have long-run relationship proved by

sector are shown in table 6.The table reveals that both the trace rank test and maximum eigen value test without

trace and the maximum eigen value test statistics are deterministic trend, with intercept without time trend as well

significant for CE with intercept but without time trend as as with intercept and time trend. The results of trace test and

well as CE with intercept and time trend hypothesized as maximum eigen value without deterministic trend for DY

‘none’. This shows that the DPS and the MPS are co- and MPS show the critical values as 12.32 and 11.22,

integrated when the variables in the model are allowed for statistical values as 25.91and 18.27 respectively; that of for

linear deterministic trend. This has further proved the with intercept and without time trend the critical

existence of long-run relationship with time trend between valuesas15.49 and 14.26,statistical values as34.69and 21.77

DPS and MPS. respectively; and that of for with intercept and time trend the

critical values as 18.40 and 17.15,statistical values as34.28

The results further show that the data series is co-integrated and 22.14 respectively, which are highly significant at 1%

as both the trace test and the maximum eigen-value test level.

reject the null hypothesis of no co-integration, and suggests

that there are two significant co-integrating vectors in the The statistical values of the trace test and maximum eigen

model, which implies that there are two common stochastic value test are >critical values for three situations i.e. without

trends indicating a degree of market integration. The DPS deterministic trend, with intercept without time trend as well

and the MPS have long-run relationship, which and is as with intercept and time trend, hence the null

proved by trace rank test and maximum eigen value test hypothesisH03: “there is no co-integration between

without deterministic trend, with intercept without time dividend yield (DY) and shareholders’ wealth (SW)” is

trend as well as with intercept and time trend. rejected at 1% level. Therefore, the co-integration results

prove that there exists a stationary, long-run relationship

The results of trace test and maximum eigen value test between DY and MPS.

without deterministic trend for DPS and MPS show the

critical value as 12.32 and 11.22, statistical value as Both the trace test and the maximum eigen value test

28.00and 27.95 respectively; that of for with intercept and statistics for the CEs without and with deterministic trend

without time trend the critical value as15.49 and for MPS with DPS, DPO and DY are hypothesized as ‘none’

14.26,statistical value as30.88and 26.14 respectively; and at level shows the presence of a long-run relationship

that of for with intercept and time trend the critical value as between DP and SW(MPS and DPS; MPS and DPO; and

18.40 and 17.15,statistical value as32.09 and 26.21 MPS and DY).

respectively, which are highly significant at 1% level. Results and Discussion of Impact of DP on SW

The statistical values of the trace test and maximum eigen Table 7 is reported with the results of regression for eliciting

value test are >critical values for three situations i.e. without the impact of DP on SW. There are two regressions; first one

deterministic trend, with intercept without time trend as well with dividend variables (DPS, DPO and DY) besides the

as with intercept and time trend hence the null financial factors (P, LEV, OF, LQ, EPS, WF, AQ) and the

hypothesisH01: “there is no co-integration between second one is with financial factors (P, LEV, OF, LQ, EPS,

dividend per share (DPS) and shareholders’ wealth (SW)” is WF, AQ) only.

rejected at 1% level. Therefore, the co-integration results

The significance of the explanatory power of DP on SW,prove that there exists a stationary, long-run relationship

when all the financial factors are held constant, is foundbetween DPS and MPS.

based on F value obtained from comparing R2 values of the

The results of trace test and maximum eigen value test two models using the following formula:

without deterministic trend for DPO and MPS show the

critical value as 12.32 and 11.22, statistical value as

15.35and 13.89 respectively; that of for with intercept and

without time trend the critical value as15.49 and

Where,14.26,statistical value as16.44and 3.96 respectively; and

that of for with intercept and time trend the critical value as R2L = R2 from the larger model (full model)

18.40 and 17.15,statistical value as4.80 each respectively,

R2S = R2 from the smaller model (subset model afterwhich are highly significant at 5% level. The statistical

removing certain predictors)values of the trace test and maximum eigen value are

>critical values for three situations i.e. without deterministic dfL = Row degrees of freedom (or number of predictors)

trend, with intercept without time trend as well as with in the larger model

intercept and time trend hence the null hypothesisH02:

dfS = Row degrees of freedom in the smaller model“there is no co-integration between dividend payout (DPO)

and shareholders’ wealth (SW)” is rejected at 5% level. N =Number of observations

Volume 9 Issue 7, Jan. 2017

The results of co-integration analysis of Consumer Cyclical The DY and the MPS have long-run relationship proved by

sector are shown in table 6.The table reveals that both the trace rank test and maximum eigen value test without

trace and the maximum eigen value test statistics are deterministic trend, with intercept without time trend as well

significant for CE with intercept but without time trend as as with intercept and time trend. The results of trace test and

well as CE with intercept and time trend hypothesized as maximum eigen value without deterministic trend for DY

‘none’. This shows that the DPS and the MPS are co- and MPS show the critical values as 12.32 and 11.22,

integrated when the variables in the model are allowed for statistical values as 25.91and 18.27 respectively; that of for

linear deterministic trend. This has further proved the with intercept and without time trend the critical

existence of long-run relationship with time trend between valuesas15.49 and 14.26,statistical values as34.69and 21.77

DPS and MPS. respectively; and that of for with intercept and time trend the

critical values as 18.40 and 17.15,statistical values as34.28

The results further show that the data series is co-integrated and 22.14 respectively, which are highly significant at 1%

as both the trace test and the maximum eigen-value test level.

reject the null hypothesis of no co-integration, and suggests

that there are two significant co-integrating vectors in the The statistical values of the trace test and maximum eigen

model, which implies that there are two common stochastic value test are >critical values for three situations i.e. without

trends indicating a degree of market integration. The DPS deterministic trend, with intercept without time trend as well

and the MPS have long-run relationship, which and is as with intercept and time trend, hence the null

proved by trace rank test and maximum eigen value test hypothesisH03: “there is no co-integration between

without deterministic trend, with intercept without time dividend yield (DY) and shareholders’ wealth (SW)” is

trend as well as with intercept and time trend. rejected at 1% level. Therefore, the co-integration results

prove that there exists a stationary, long-run relationship

The results of trace test and maximum eigen value test between DY and MPS.

without deterministic trend for DPS and MPS show the

critical value as 12.32 and 11.22, statistical value as Both the trace test and the maximum eigen value test

28.00and 27.95 respectively; that of for with intercept and statistics for the CEs without and with deterministic trend

without time trend the critical value as15.49 and for MPS with DPS, DPO and DY are hypothesized as ‘none’

14.26,statistical value as30.88and 26.14 respectively; and at level shows the presence of a long-run relationship

that of for with intercept and time trend the critical value as between DP and SW(MPS and DPS; MPS and DPO; and

18.40 and 17.15,statistical value as32.09 and 26.21 MPS and DY).

respectively, which are highly significant at 1% level. Results and Discussion of Impact of DP on SW

The statistical values of the trace test and maximum eigen Table 7 is reported with the results of regression for eliciting

value test are >critical values for three situations i.e. without the impact of DP on SW. There are two regressions; first one

deterministic trend, with intercept without time trend as well with dividend variables (DPS, DPO and DY) besides the

as with intercept and time trend hence the null financial factors (P, LEV, OF, LQ, EPS, WF, AQ) and the

hypothesisH01: “there is no co-integration between second one is with financial factors (P, LEV, OF, LQ, EPS,

dividend per share (DPS) and shareholders’ wealth (SW)” is WF, AQ) only.

rejected at 1% level. Therefore, the co-integration results

The significance of the explanatory power of DP on SW,prove that there exists a stationary, long-run relationship

when all the financial factors are held constant, is foundbetween DPS and MPS.

based on F value obtained from comparing R2 values of the

The results of trace test and maximum eigen value test two models using the following formula:

without deterministic trend for DPO and MPS show the

critical value as 12.32 and 11.22, statistical value as

15.35and 13.89 respectively; that of for with intercept and

without time trend the critical value as15.49 and

Where,14.26,statistical value as16.44and 3.96 respectively; and

that of for with intercept and time trend the critical value as R2L = R2 from the larger model (full model)

18.40 and 17.15,statistical value as4.80 each respectively,

R2S = R2 from the smaller model (subset model afterwhich are highly significant at 5% level. The statistical

removing certain predictors)values of the trace test and maximum eigen value are

>critical values for three situations i.e. without deterministic dfL = Row degrees of freedom (or number of predictors)

trend, with intercept without time trend as well as with in the larger model

intercept and time trend hence the null hypothesisH02:

dfS = Row degrees of freedom in the smaller model“there is no co-integration between dividend payout (DPO)

and shareholders’ wealth (SW)” is rejected at 5% level. N =Number of observations

www.pbr.co.in100

Pacific Business Review International

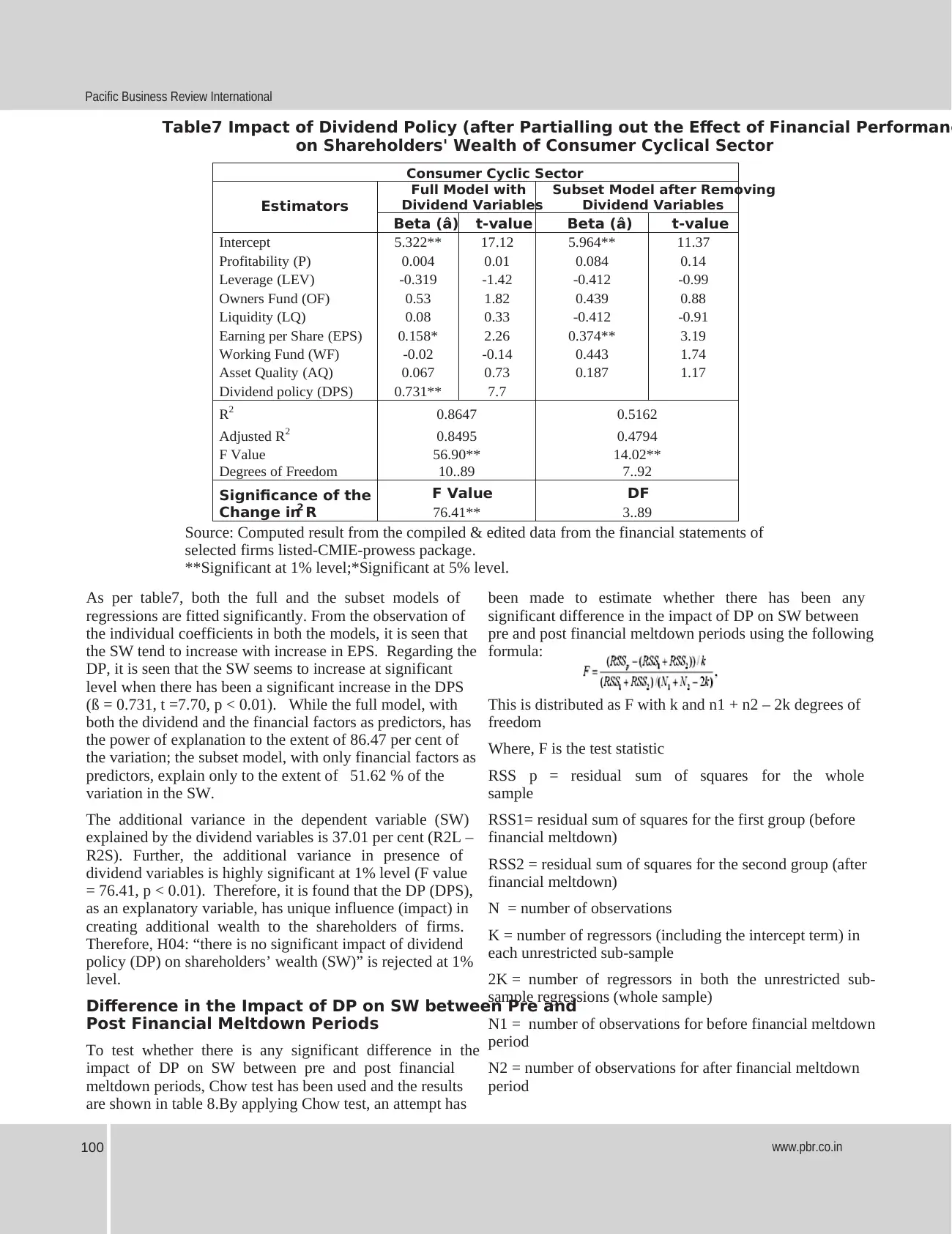

Table7 Impact of Dividend Policy (after Partialling out the Effect of Financial Performanc

on Shareholders' Wealth of Consumer Cyclical Sector

Consumer Cyclic Sector

Estimators

Full Model with

Dividend Variables

Subset Model after Removing

Dividend Variables

Beta (â) t-value Beta (â) t-value

Intercept 5.322** 17.12 5.964** 11.37

Profitability (P) 0.004 0.01 0.084 0.14

Leverage (LEV) -0.319 -1.42 -0.412 -0.99

Owners Fund (OF) 0.53 1.82 0.439 0.88

Liquidity (LQ) 0.08 0.33 -0.412 -0.91

Earning per Share (EPS) 0.158* 2.26 0.374** 3.19

Working Fund (WF) -0.02 -0.14 0.443 1.74

Asset Quality (AQ) 0.067 0.73 0.187 1.17

Dividend policy (DPS) 0.731** 7.7

R 2 0.8647 0.5162

Adjusted R 2 0.8495 0.4794

F Value 56.90** 14.02**

Degrees of Freedom 10..89 7..92

Significance of the

Change in R2

F Value DF

76.41** 3..89

Source: Computed result from the compiled & edited data from the financial statements of

selected firms listed-CMIE-prowess package.

**Significant at 1% level;*Significant at 5% level.

As per table7, both the full and the subset models of been made to estimate whether there has been any

regressions are fitted significantly. From the observation of significant difference in the impact of DP on SW between

the individual coefficients in both the models, it is seen that pre and post financial meltdown periods using the following

the SW tend to increase with increase in EPS. Regarding the formula:

DP, it is seen that the SW seems to increase at significant

level when there has been a significant increase in the DPS

This is distributed as F with k and n1 + n2 – 2k degrees of(ß = 0.731, t =7.70, p < 0.01). While the full model, with

freedomboth the dividend and the financial factors as predictors, has

the power of explanation to the extent of 86.47 per cent of Where, F is the test statistic

the variation; the subset model, with only financial factors as

RSS p = residual sum of squares for the wholepredictors, explain only to the extent of 51.62 % of the

samplevariation in the SW.

RSS1= residual sum of squares for the first group (beforeThe additional variance in the dependent variable (SW)

financial meltdown)explained by the dividend variables is 37.01 per cent (R2L –

R2S). Further, the additional variance in presence of RSS2 = residual sum of squares for the second group (after

dividend variables is highly significant at 1% level (F value financial meltdown)

= 76.41, p < 0.01). Therefore, it is found that the DP (DPS),

N = number of observationsas an explanatory variable, has unique influence (impact) in

creating additional wealth to the shareholders of firms. K = number of regressors (including the intercept term) in

Therefore, H04: “there is no significant impact of dividend each unrestricted sub-sample

policy (DP) on shareholders’ wealth (SW)” is rejected at 1%

2K = number of regressors in both the unrestricted sub-level.

sample regressions (whole sample)

Difference in the Impact of DP on SW between Pre and

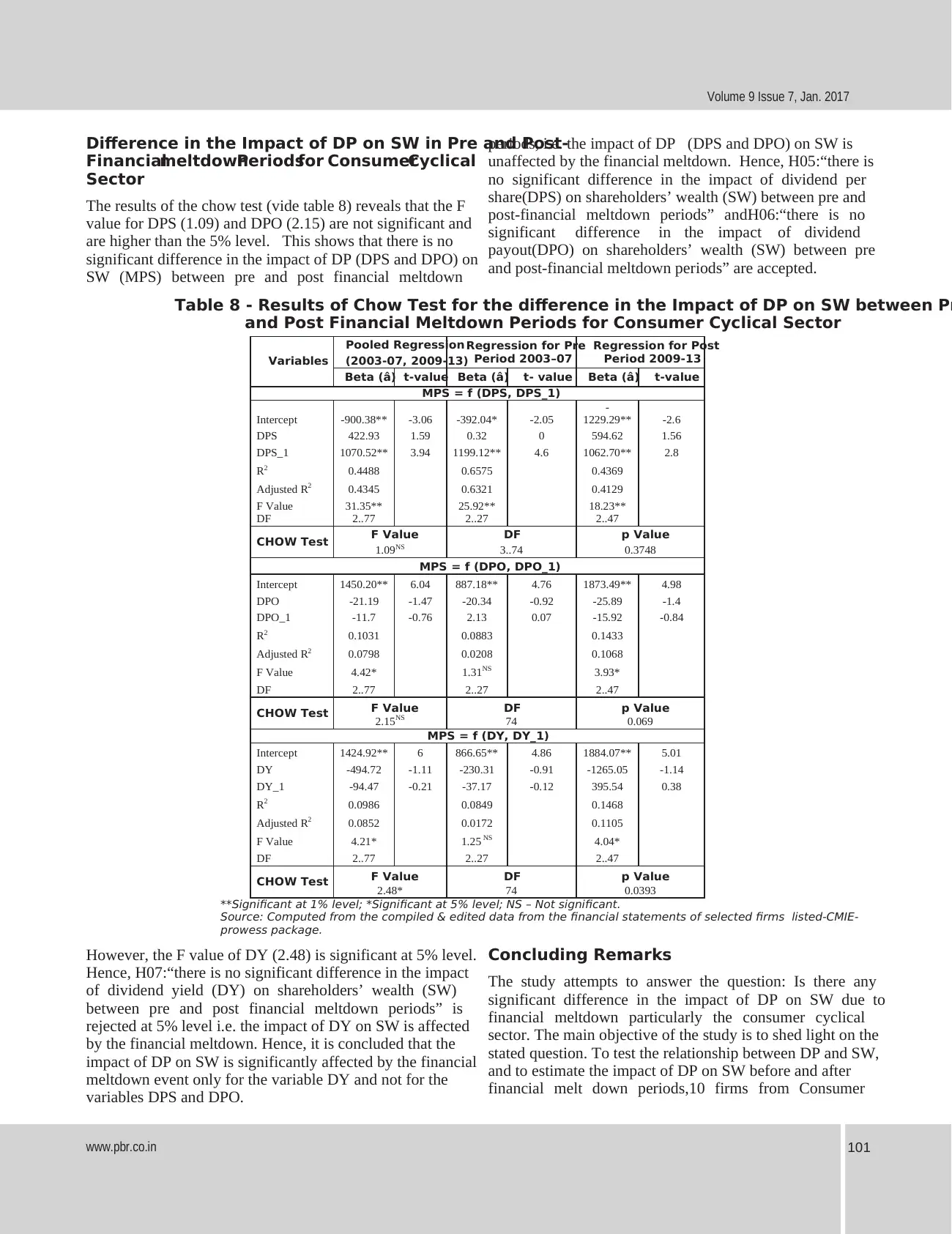

Post Financial Meltdown Periods N1 = number of observations for before financial meltdown

period

To test whether there is any significant difference in the

N2 = number of observations for after financial meltdownimpact of DP on SW between pre and post financial

periodmeltdown periods, Chow test has been used and the results

are shown in table 8.By applying Chow test, an attempt has

Pacific Business Review International

Table7 Impact of Dividend Policy (after Partialling out the Effect of Financial Performanc

on Shareholders' Wealth of Consumer Cyclical Sector

Consumer Cyclic Sector

Estimators

Full Model with

Dividend Variables

Subset Model after Removing

Dividend Variables

Beta (â) t-value Beta (â) t-value

Intercept 5.322** 17.12 5.964** 11.37

Profitability (P) 0.004 0.01 0.084 0.14

Leverage (LEV) -0.319 -1.42 -0.412 -0.99

Owners Fund (OF) 0.53 1.82 0.439 0.88

Liquidity (LQ) 0.08 0.33 -0.412 -0.91

Earning per Share (EPS) 0.158* 2.26 0.374** 3.19

Working Fund (WF) -0.02 -0.14 0.443 1.74

Asset Quality (AQ) 0.067 0.73 0.187 1.17

Dividend policy (DPS) 0.731** 7.7

R 2 0.8647 0.5162

Adjusted R 2 0.8495 0.4794

F Value 56.90** 14.02**

Degrees of Freedom 10..89 7..92

Significance of the

Change in R2

F Value DF

76.41** 3..89

Source: Computed result from the compiled & edited data from the financial statements of

selected firms listed-CMIE-prowess package.

**Significant at 1% level;*Significant at 5% level.

As per table7, both the full and the subset models of been made to estimate whether there has been any

regressions are fitted significantly. From the observation of significant difference in the impact of DP on SW between

the individual coefficients in both the models, it is seen that pre and post financial meltdown periods using the following

the SW tend to increase with increase in EPS. Regarding the formula:

DP, it is seen that the SW seems to increase at significant

level when there has been a significant increase in the DPS

This is distributed as F with k and n1 + n2 – 2k degrees of(ß = 0.731, t =7.70, p < 0.01). While the full model, with

freedomboth the dividend and the financial factors as predictors, has

the power of explanation to the extent of 86.47 per cent of Where, F is the test statistic

the variation; the subset model, with only financial factors as