Global Financial Crisis, UK Impact, FSA Failure, and New Regulations

VerifiedAdded on 2020/10/22

|21

|5975

|420

Report

AI Summary

This report provides a comprehensive analysis of the global financial crisis, with a specific focus on its impact on the United Kingdom. It begins with an overview of the crisis, detailing its origins, key events, and the five major phases since the Great Depression. The report then delves into the specific consequences of the crisis for the UK, including economic downturn, unemployment, and increased debt. A significant portion of the report examines the failures of the Financial Services Authority (FSA) in the UK, exploring the reasons behind its shortcomings and the calls for its replacement. The report concludes by discussing recent regulatory changes implemented in the UK financial system to address the crisis and prevent future occurrences. Throughout the report, various sources and diagrams are used to support the analysis and provide a clear understanding of the complex issues involved.

LAW QUESTION

1

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

INTRODUCTION...........................................................................................................................3

MAIN BODY...................................................................................................................................3

Global financial crisis.................................................................................................................3

Impact of global financial crisis on UK......................................................................................6

Failure of FSA.............................................................................................................................8

Recent regulations of UK financial system...............................................................................13

CONCLUSION..............................................................................................................................16

REFERENCES..............................................................................................................................17

2

MAIN BODY...................................................................................................................................3

Global financial crisis.................................................................................................................3

Impact of global financial crisis on UK......................................................................................6

Failure of FSA.............................................................................................................................8

Recent regulations of UK financial system...............................................................................13

CONCLUSION..............................................................................................................................16

REFERENCES..............................................................................................................................17

2

INTRODUCTION

Global financial crisis is a broad concept which shows the trauma of funds across the

globe due to fluctuation in several factors that affects international finance department. However,

financial crisis of 2007-2008 is known as global financial crisis and almost large number of

economists said that it was a worst crisis since the Great depression of 1930s 1. Therefore,

assignment is going to highlight the major financial crisis which affects the whole world and its

influence on entire global platform. In order to cope up with financial issue, various international

institutions are coming up with new policies or ideas to control this situation. Along with this,

regulatory frameworks and legitimate bodies of UK have taken major steps by coming up with

new legal acts for supporting the nation. Hence, two new regulators are mainly outlined in the

report which replaced the existing financial services authority for stabilizing the UK condition.

MAIN BODY

Global financial crisis

Global financial crisis highlight the time period where there was availability of extreme

stress in global financial markets and banking systems in almost mid of 2007 till early of 2009.

Basically, it was caused due to the deregulation in financial industry which allows the banks to

get involved in hedge fund trading with derivates. After that, bank demanded more mortgagees

for supporting the profitable sale of that derivates. As a result, entire scenario creates a breath

taking financial crisis which led to great recession. By the September, 2008 financial crisis

become more worsened as stock markets across the globe crashed as well as highly volatile. As a

result, confidence of customers also hit rock bottom due to which every individual tightened

their belts and lost their faith on marketplace 2.

From the sub-prime to downturn, five phases of most dangerous crisis almost hit the

entire globe economy since the Great depression which was found in these five dates such as; 9

august 2017, 15th September 2008, 2nd April 2009, 9th May 2010, 5th August, 2011. Initial

1 . Helleiner, E., 2011. Understanding the 2007–2008 global financial crisis: Lessons for

scholars of international political economy. Annual Review of Political Science, 14,

pp.67-87.

2 . Erkens, D.H., Hung, M. and Matos, P., 2012. Corporate governance in the 2007–2008

financial crisis: Evidence from financial institutions worldwide. Journal of Corporate

Finance, 18(2), pp.389-411.

3

Global financial crisis is a broad concept which shows the trauma of funds across the

globe due to fluctuation in several factors that affects international finance department. However,

financial crisis of 2007-2008 is known as global financial crisis and almost large number of

economists said that it was a worst crisis since the Great depression of 1930s 1. Therefore,

assignment is going to highlight the major financial crisis which affects the whole world and its

influence on entire global platform. In order to cope up with financial issue, various international

institutions are coming up with new policies or ideas to control this situation. Along with this,

regulatory frameworks and legitimate bodies of UK have taken major steps by coming up with

new legal acts for supporting the nation. Hence, two new regulators are mainly outlined in the

report which replaced the existing financial services authority for stabilizing the UK condition.

MAIN BODY

Global financial crisis

Global financial crisis highlight the time period where there was availability of extreme

stress in global financial markets and banking systems in almost mid of 2007 till early of 2009.

Basically, it was caused due to the deregulation in financial industry which allows the banks to

get involved in hedge fund trading with derivates. After that, bank demanded more mortgagees

for supporting the profitable sale of that derivates. As a result, entire scenario creates a breath

taking financial crisis which led to great recession. By the September, 2008 financial crisis

become more worsened as stock markets across the globe crashed as well as highly volatile. As a

result, confidence of customers also hit rock bottom due to which every individual tightened

their belts and lost their faith on marketplace 2.

From the sub-prime to downturn, five phases of most dangerous crisis almost hit the

entire globe economy since the Great depression which was found in these five dates such as; 9

august 2017, 15th September 2008, 2nd April 2009, 9th May 2010, 5th August, 2011. Initial

1 . Helleiner, E., 2011. Understanding the 2007–2008 global financial crisis: Lessons for

scholars of international political economy. Annual Review of Political Science, 14,

pp.67-87.

2 . Erkens, D.H., Hung, M. and Matos, P., 2012. Corporate governance in the 2007–2008

financial crisis: Evidence from financial institutions worldwide. Journal of Corporate

Finance, 18(2), pp.389-411.

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

phase is on 9th August 2007 started with the seizure in entire banking system when Merril Lynch

trader Strenfors got a call which change his life. It’s really a sparking issue which is a great

exposure for individual banks in which trust evaporated overnight because of this; all the banks

stopped doing business with each other.

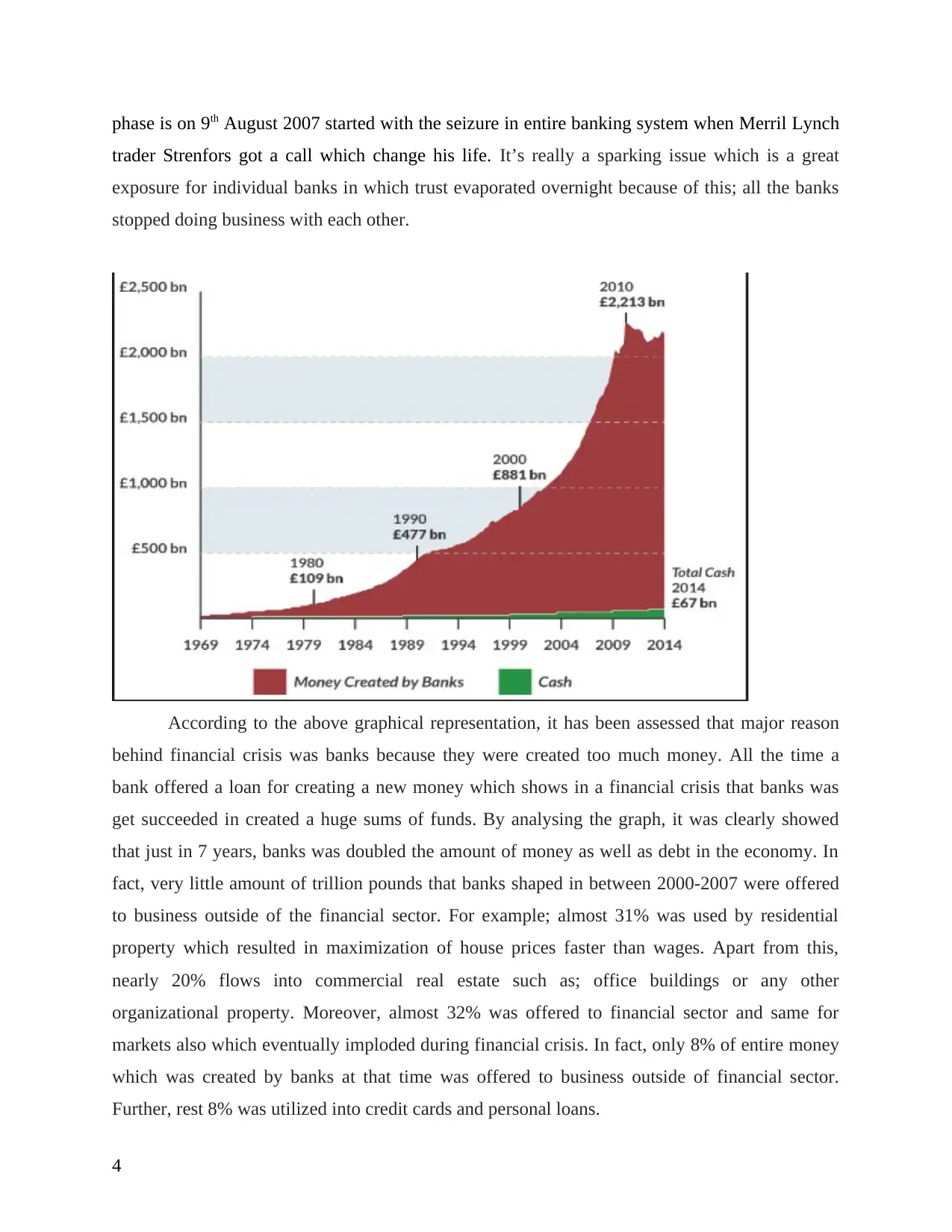

According to the above graphical representation, it has been assessed that major reason

behind financial crisis was banks because they were created too much money. All the time a

bank offered a loan for creating a new money which shows in a financial crisis that banks was

get succeeded in created a huge sums of funds. By analysing the graph, it was clearly showed

that just in 7 years, banks was doubled the amount of money as well as debt in the economy. In

fact, very little amount of trillion pounds that banks shaped in between 2000-2007 were offered

to business outside of the financial sector. For example; almost 31% was used by residential

property which resulted in maximization of house prices faster than wages. Apart from this,

nearly 20% flows into commercial real estate such as; office buildings or any other

organizational property. Moreover, almost 32% was offered to financial sector and same for

markets also which eventually imploded during financial crisis. In fact, only 8% of entire money

which was created by banks at that time was offered to business outside of financial sector.

Further, rest 8% was utilized into credit cards and personal loans.

4

trader Strenfors got a call which change his life. It’s really a sparking issue which is a great

exposure for individual banks in which trust evaporated overnight because of this; all the banks

stopped doing business with each other.

According to the above graphical representation, it has been assessed that major reason

behind financial crisis was banks because they were created too much money. All the time a

bank offered a loan for creating a new money which shows in a financial crisis that banks was

get succeeded in created a huge sums of funds. By analysing the graph, it was clearly showed

that just in 7 years, banks was doubled the amount of money as well as debt in the economy. In

fact, very little amount of trillion pounds that banks shaped in between 2000-2007 were offered

to business outside of the financial sector. For example; almost 31% was used by residential

property which resulted in maximization of house prices faster than wages. Apart from this,

nearly 20% flows into commercial real estate such as; office buildings or any other

organizational property. Moreover, almost 32% was offered to financial sector and same for

markets also which eventually imploded during financial crisis. In fact, only 8% of entire money

which was created by banks at that time was offered to business outside of financial sector.

Further, rest 8% was utilized into credit cards and personal loans.

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

On 15th September 2008, one of the major announcement shaken the entire world that is;

bankruptcy of Lehman brothers at midnight of Monday. Thus, it shows that financial crisis was

now entered into an acute phase marked by failures of major American and European banks. As

a result, governing bodies of Americans and European Union tries to rescue distressed financial

institutions. For example; emerging passage of Emergency Economic stabilization Act of 2008

whereas infusion of funds into major banks in European countries.

For various Americans, financial crisis becoming more worst in 2009 such as; in March

plummeted of market more as well as panicking to those investors who was thinking that

worsened situation was over. It means, in April 2007 trust from financial system are breaking

down which was caused subprime Mortgage crisis. In the winter of 2008-09, G20 group which

was recently formed engaged in coordinating with others for developing the nations and trying to

defend recession 3. For example; cutting of interest rates, announce fiscal stimulus packages of

distinct sizes as well as creation of electronic money with the use of quantitative easing. On 2nd

April 2009 in London G20 submitted that leaders of world committed to themselves to around

this much of “$5tn (£3tn)” fiscal expansion as well as extra almost $1.1tn of resources for

supporting International Monetary fund’s (Larry Elliott, 2011 ). As , their main motive is to

facilitate global institutions for boosting the jobs, growth and to modify the banks.

9th may 2010 is a day when concerned was switched from private sector to public sector.

At that time, IMF and European Union announced that they are going to offer financial support

to Greece. Another day of financial crisis was on 5th august 2011 was remembered as most

memorable day when US hegemony was lost. Although, it was really terrible news for Barack

Obama as he was not delivered economic recovery. As a result, US were drowning in a negative

equity and foreclosed houses.

Impact of global financial crisis on UK

Whole world is getting influenced by this major fluctuation of finance market. From

which UK was also affected very badly and major fall in the national economy. For example;

economic downturn, unemployment, maximization of debt henceforth. In fact, number of authors

and specialist has expressed their opinions towards impact of financial crisis on UK. As per the

major article of Financial Express, it was clearly stated that crisis of 2007-2008 was the great

3 . Ivashina, V. and Scharfstein, D., 2010. Bank lending during the financial crisis of

2008. Journal of Financial economics, 97(3), pp.319-338.

5

bankruptcy of Lehman brothers at midnight of Monday. Thus, it shows that financial crisis was

now entered into an acute phase marked by failures of major American and European banks. As

a result, governing bodies of Americans and European Union tries to rescue distressed financial

institutions. For example; emerging passage of Emergency Economic stabilization Act of 2008

whereas infusion of funds into major banks in European countries.

For various Americans, financial crisis becoming more worst in 2009 such as; in March

plummeted of market more as well as panicking to those investors who was thinking that

worsened situation was over. It means, in April 2007 trust from financial system are breaking

down which was caused subprime Mortgage crisis. In the winter of 2008-09, G20 group which

was recently formed engaged in coordinating with others for developing the nations and trying to

defend recession 3. For example; cutting of interest rates, announce fiscal stimulus packages of

distinct sizes as well as creation of electronic money with the use of quantitative easing. On 2nd

April 2009 in London G20 submitted that leaders of world committed to themselves to around

this much of “$5tn (£3tn)” fiscal expansion as well as extra almost $1.1tn of resources for

supporting International Monetary fund’s (Larry Elliott, 2011 ). As , their main motive is to

facilitate global institutions for boosting the jobs, growth and to modify the banks.

9th may 2010 is a day when concerned was switched from private sector to public sector.

At that time, IMF and European Union announced that they are going to offer financial support

to Greece. Another day of financial crisis was on 5th august 2011 was remembered as most

memorable day when US hegemony was lost. Although, it was really terrible news for Barack

Obama as he was not delivered economic recovery. As a result, US were drowning in a negative

equity and foreclosed houses.

Impact of global financial crisis on UK

Whole world is getting influenced by this major fluctuation of finance market. From

which UK was also affected very badly and major fall in the national economy. For example;

economic downturn, unemployment, maximization of debt henceforth. In fact, number of authors

and specialist has expressed their opinions towards impact of financial crisis on UK. As per the

major article of Financial Express, it was clearly stated that crisis of 2007-2008 was the great

3 . Ivashina, V. and Scharfstein, D., 2010. Bank lending during the financial crisis of

2008. Journal of Financial economics, 97(3), pp.319-338.

5

blunder after the great depression of 1930s because it was rendered almost 8.8 million people of

United states unemployed alone. Main target of this crisis are advanced countries such as; United

states, Germany, United Kingdom and Hong Kong 4.

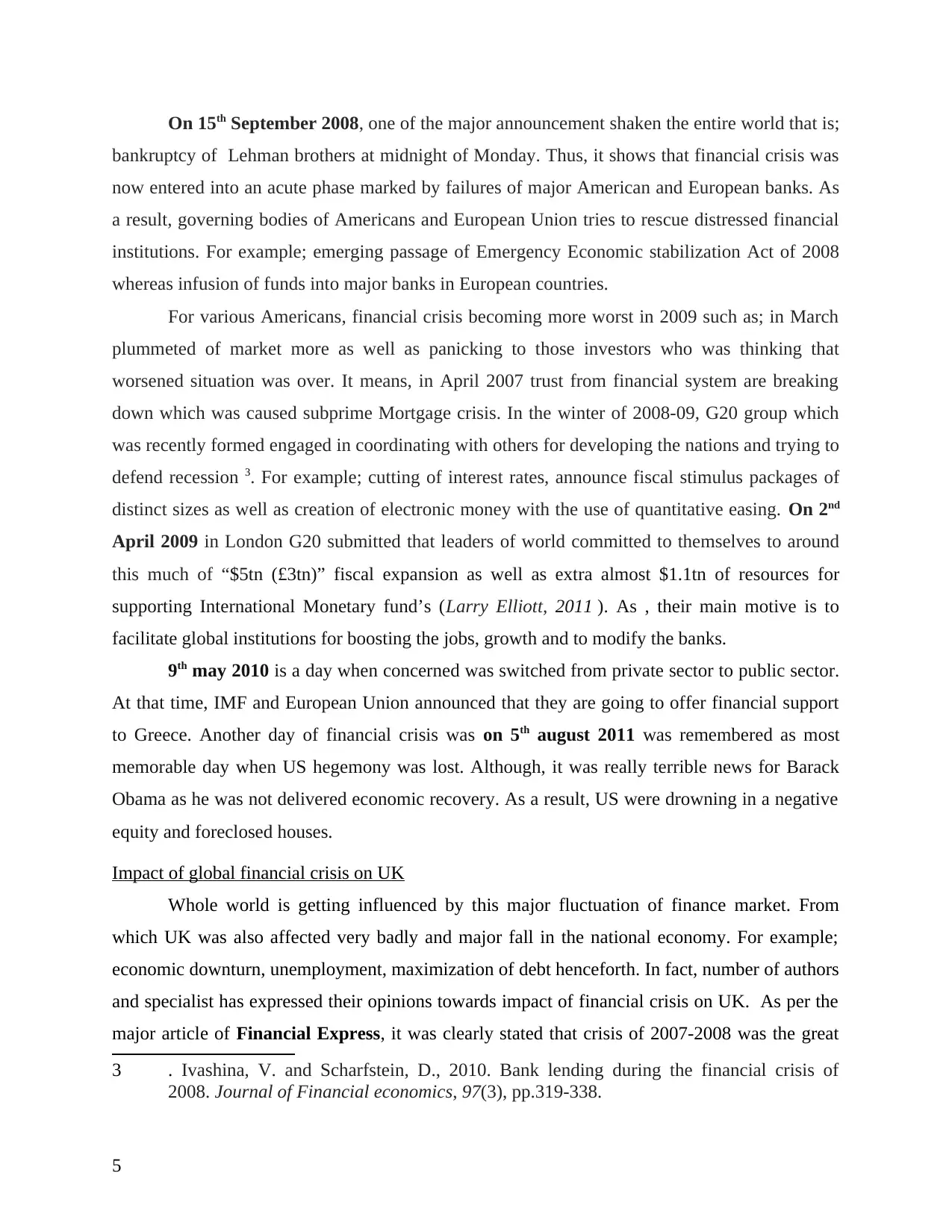

From the above diagrammatic representation, it has been determined that advanced

countries are circulated around major trauma and encountered several ups or downs in between

2005 to 2012. For example; UK is also effecting by the crisis in various manner as common

people of the nation are suffering from distinct day to day problems.

As per the viewpoint of Gordon Rayner, 2008 “UK was encountered worst financial

crisis in decades” because of America latest corporate meltdown. However, one of the biggest

mortgage lender of Britain’s is Halifax Bank of Scotland because it lost around 13% of its value

and scared that profit of the bank is directly influenced by global credit crunch. Moreover,

Barclays and Royal Bank of Scotland wiped off their share price by 9%. Thus, Bank of England

has filled approximately £5 billion into money markets in order to restoring the confidence in

banking system. Although, this solution is not much enough to defend the economy for

becoming worse because predicators are saying that worst is yet to come. Bear steams which is

the night biggest investment bank across the globe was in the situation of getting collapsed due

4 . How badly 2008 financial crisis hurt US, UK, Germany, 2018. [Online]. Available

through<hhttps://www.financialexpress.com/economy/how-badly-2008-financial-crisis-

hurt-us-uk-germany-this-1-chart-shows-it-all/1146819/ >.

6

United states unemployed alone. Main target of this crisis are advanced countries such as; United

states, Germany, United Kingdom and Hong Kong 4.

From the above diagrammatic representation, it has been determined that advanced

countries are circulated around major trauma and encountered several ups or downs in between

2005 to 2012. For example; UK is also effecting by the crisis in various manner as common

people of the nation are suffering from distinct day to day problems.

As per the viewpoint of Gordon Rayner, 2008 “UK was encountered worst financial

crisis in decades” because of America latest corporate meltdown. However, one of the biggest

mortgage lender of Britain’s is Halifax Bank of Scotland because it lost around 13% of its value

and scared that profit of the bank is directly influenced by global credit crunch. Moreover,

Barclays and Royal Bank of Scotland wiped off their share price by 9%. Thus, Bank of England

has filled approximately £5 billion into money markets in order to restoring the confidence in

banking system. Although, this solution is not much enough to defend the economy for

becoming worse because predicators are saying that worst is yet to come. Bear steams which is

the night biggest investment bank across the globe was in the situation of getting collapsed due

4 . How badly 2008 financial crisis hurt US, UK, Germany, 2018. [Online]. Available

through<hhttps://www.financialexpress.com/economy/how-badly-2008-financial-crisis-

hurt-us-uk-germany-this-1-chart-shows-it-all/1146819/ >.

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

to heavy losses because of sub-prime mortgage crisis. As a result, other banking giants are

fearing and in a major trouble 5.

On the other hand, Prime Minister Gordon Brown is promising to initiate whatever action

is required for maintaining the stability of economy. Whereas, Terry Smith who was a chief

executive of Tullett Prebon and a expertise broker in the city states that “I was working in

finance in current city as well as across the globe for nearly 34 years but I haven’t seen anything

like this”. On contrary to this, David Buick of spread betting firm Cantor Index states that “None

of the individual who is living in current phase have ever face this kind of banking trauma. In

fact I was working from last 46 years but out looked has never seen as bleak”. Mainly, this

turmoil is immediately knocking and affecting for homeowners because of which families of

Britain are already suffering from credit crunch. Since last summer of year 2008 bills of

household are steadily increased 6.

Apart from this, average houses of UK was also lost almost 20% of its value in 16

months to February, 2009 and transaction levels was an averaged nearly 1.65 million in a year in

a last decade, plummeted to almost 730, 000 in next 12 months till June, 2016. On the other

hand, there was one report from property advisor Savills who states that influence of crisis

pushed UK into deepest post-war recession. In fact, it was still felt in housing market of UK as

new homeowners mainly reliant on “the Bank of Mum and Dad”, current house owners are

struggling to trade up the market 7.

Failure of FSA

Financial bodies of UK systems tried their best for maintaining stability at EU

marketplace. Financial Conduct Authority is a framework which considered as a financial

regulatory body in UK. Basically, it operates independently on the behalf of UK financial

institutions and acquired funds by charging fees from various members of financial services

industry. FSA was established by financial services and markets act 2000 to work as an

5 . Shiller, R.J., 2012. The subprime solution: how today's global financial crisis happened,

and what to do about it. Princeton University Press.

6 . UK facing worst financial crisis 'in decades', 2008. [Online]. Available

throughhttps://www.telegraph.co.uk/finance/markets/2786497/UK-facing-worst-

financial-crisis-in-decades.html

7 . Thomas Colson, 2017. [Online]. Available through<

https://www.businessinsider.com/how-2007-financial-crisis-transformed-uk-housing-market-

2017-7?IR=T>.

7

fearing and in a major trouble 5.

On the other hand, Prime Minister Gordon Brown is promising to initiate whatever action

is required for maintaining the stability of economy. Whereas, Terry Smith who was a chief

executive of Tullett Prebon and a expertise broker in the city states that “I was working in

finance in current city as well as across the globe for nearly 34 years but I haven’t seen anything

like this”. On contrary to this, David Buick of spread betting firm Cantor Index states that “None

of the individual who is living in current phase have ever face this kind of banking trauma. In

fact I was working from last 46 years but out looked has never seen as bleak”. Mainly, this

turmoil is immediately knocking and affecting for homeowners because of which families of

Britain are already suffering from credit crunch. Since last summer of year 2008 bills of

household are steadily increased 6.

Apart from this, average houses of UK was also lost almost 20% of its value in 16

months to February, 2009 and transaction levels was an averaged nearly 1.65 million in a year in

a last decade, plummeted to almost 730, 000 in next 12 months till June, 2016. On the other

hand, there was one report from property advisor Savills who states that influence of crisis

pushed UK into deepest post-war recession. In fact, it was still felt in housing market of UK as

new homeowners mainly reliant on “the Bank of Mum and Dad”, current house owners are

struggling to trade up the market 7.

Failure of FSA

Financial bodies of UK systems tried their best for maintaining stability at EU

marketplace. Financial Conduct Authority is a framework which considered as a financial

regulatory body in UK. Basically, it operates independently on the behalf of UK financial

institutions and acquired funds by charging fees from various members of financial services

industry. FSA was established by financial services and markets act 2000 to work as an

5 . Shiller, R.J., 2012. The subprime solution: how today's global financial crisis happened,

and what to do about it. Princeton University Press.

6 . UK facing worst financial crisis 'in decades', 2008. [Online]. Available

throughhttps://www.telegraph.co.uk/finance/markets/2786497/UK-facing-worst-

financial-crisis-in-decades.html

7 . Thomas Colson, 2017. [Online]. Available through<

https://www.businessinsider.com/how-2007-financial-crisis-transformed-uk-housing-market-

2017-7?IR=T>.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

independent non-governmental body in order to act as a statutory regulator of UK’s financial

service sector. Thus, failing of this association was come out after collapsed of Royal Bank of

Scotland. As a result, FSA produced an investigation report which was less than 300 words. On

the other hand, the Icelandic Truth Commission designed a report which was of almost over

2200 pages in length. However, major content that is highlighted in the whole report is that; FSA

get failed in defending banking meltdown. By thoroughgoing with all the relevant information

about FSA and its downturn, various members argued and demanded the replacement of this

financial institution. In fact, number of lawyers and jury members are raising their voice against

this major crisis as it influence the whole UK and created a financial overhauled in EU.

However, FSA was ruled for almost 15 years by the support of press, politicians, advisors, jury

and various other members. Basically, number of advisors argues that the FSA needs to be seen

in two ways. For example; first one is management of broad economy which includes regulations

of several banks and second one is implementation of new rules and regulations for financial

services community.

Peter Cooper, director of Cooper Johnston Associates, states that regulations of FSA for

the banks was a “complete/ abject failure”. Along with this, he said that banking crisis of

2007/2008 in which almost collapse of Royal bank of Scotland and HBOS was partly mistake of

regulators due to the use of “light touch approach”.

On the other hand, Allan Maxwell director of Corporate Benefits Consulting is very

liberal in his assessment for FSA. He said that, although FSA was failed in few areas but it was

not solely responsible for the banking crisis as well as difficulties that was incurred at financial

markets. In fact, he believes that “off course things was going wrong at large extent between

FSA, the Bank of England and the government. But it’s not right to blame only one institution

as number of people are took their eyes of the ball on FSA”. He again said that; “We are fully

aware about the IFAs which are not performing a better job but these few people are still

practicing.”.

On contrary to this, Alan Dick partner at Forty Two Wealth Management was an adviser

who always understands the significance of good regulations but still contradict that FSA was

very big and too much costly. He believes that, Yes there was few good people are present in this

organization but the association is enormous and capital of funding it was very much expensive.

Another thing which he added in his statement is that; FSA was trying their best to perform

8

service sector. Thus, failing of this association was come out after collapsed of Royal Bank of

Scotland. As a result, FSA produced an investigation report which was less than 300 words. On

the other hand, the Icelandic Truth Commission designed a report which was of almost over

2200 pages in length. However, major content that is highlighted in the whole report is that; FSA

get failed in defending banking meltdown. By thoroughgoing with all the relevant information

about FSA and its downturn, various members argued and demanded the replacement of this

financial institution. In fact, number of lawyers and jury members are raising their voice against

this major crisis as it influence the whole UK and created a financial overhauled in EU.

However, FSA was ruled for almost 15 years by the support of press, politicians, advisors, jury

and various other members. Basically, number of advisors argues that the FSA needs to be seen

in two ways. For example; first one is management of broad economy which includes regulations

of several banks and second one is implementation of new rules and regulations for financial

services community.

Peter Cooper, director of Cooper Johnston Associates, states that regulations of FSA for

the banks was a “complete/ abject failure”. Along with this, he said that banking crisis of

2007/2008 in which almost collapse of Royal bank of Scotland and HBOS was partly mistake of

regulators due to the use of “light touch approach”.

On the other hand, Allan Maxwell director of Corporate Benefits Consulting is very

liberal in his assessment for FSA. He said that, although FSA was failed in few areas but it was

not solely responsible for the banking crisis as well as difficulties that was incurred at financial

markets. In fact, he believes that “off course things was going wrong at large extent between

FSA, the Bank of England and the government. But it’s not right to blame only one institution

as number of people are took their eyes of the ball on FSA”. He again said that; “We are fully

aware about the IFAs which are not performing a better job but these few people are still

practicing.”.

On contrary to this, Alan Dick partner at Forty Two Wealth Management was an adviser

who always understands the significance of good regulations but still contradict that FSA was

very big and too much costly. He believes that, Yes there was few good people are present in this

organization but the association is enormous and capital of funding it was very much expensive.

Another thing which he added in his statement is that; FSA was trying their best to perform

8

much better such as; produced a couple of very beneficial papers. As this paper is based on risk

profiling which make sure that advisers have the authority to ask question around capacity of

loss and behaviour towards risk.

In order respond towards all these argument, Chairman of FSA Lord Turner gave a

statement at Mansion house in which he says that “economic crisis occurred due to number of

failures in policy and practice”. Along with this, he apologised also for the failure of

organization as in April, On the other hand, he also said that, crisis was not a bolt from blue as it

was raised due to improper or worst supervision, negative rules or structures, dangerous cultures

as well as mistakes made by economist, regulators, central bankers, policy designers as well as

bankers themselves.

Hence, because of perceived regulatory failure of banks while financial crisis of 2007-

2008, UK governing bodies decided for restructuring of this finance regulation and abolish FSA

with effect from 1st April, 2013. At that time, financial services authority was totally criticised by

most of commentators as this body is unfit for financial purpose. Hence, Chancellor of

Exchequer, George Osborne announced his strategy for abolishing the Financial Regulatory

Body and replaced it 8. As governing bodies claimed that current regime requisite to reform

because this association “gets failed when tested during crisis”. In fact, FSA continuously failed

to fulfils its promises such as; enabled in maintaining marketing confidence, failed in defending

both stability of UK financial system as well as consumer interests 9. Most importantly, not able

to fight with financial crime which was occurred during 2007-2008.

8 . Reinhart, C.M. and Rogoff, K.S., 2011. From financial crash to debt crisis. American

Economic Review, 101(5), pp.1676-1706.

9 . Shiller, R.J., 2012. The subprime solution: how today's global financial crisis happened,

and what to do about it. Princeton University Press.

9

profiling which make sure that advisers have the authority to ask question around capacity of

loss and behaviour towards risk.

In order respond towards all these argument, Chairman of FSA Lord Turner gave a

statement at Mansion house in which he says that “economic crisis occurred due to number of

failures in policy and practice”. Along with this, he apologised also for the failure of

organization as in April, On the other hand, he also said that, crisis was not a bolt from blue as it

was raised due to improper or worst supervision, negative rules or structures, dangerous cultures

as well as mistakes made by economist, regulators, central bankers, policy designers as well as

bankers themselves.

Hence, because of perceived regulatory failure of banks while financial crisis of 2007-

2008, UK governing bodies decided for restructuring of this finance regulation and abolish FSA

with effect from 1st April, 2013. At that time, financial services authority was totally criticised by

most of commentators as this body is unfit for financial purpose. Hence, Chancellor of

Exchequer, George Osborne announced his strategy for abolishing the Financial Regulatory

Body and replaced it 8. As governing bodies claimed that current regime requisite to reform

because this association “gets failed when tested during crisis”. In fact, FSA continuously failed

to fulfils its promises such as; enabled in maintaining marketing confidence, failed in defending

both stability of UK financial system as well as consumer interests 9. Most importantly, not able

to fight with financial crime which was occurred during 2007-2008.

8 . Reinhart, C.M. and Rogoff, K.S., 2011. From financial crash to debt crisis. American

Economic Review, 101(5), pp.1676-1706.

9 . Shiller, R.J., 2012. The subprime solution: how today's global financial crisis happened,

and what to do about it. Princeton University Press.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

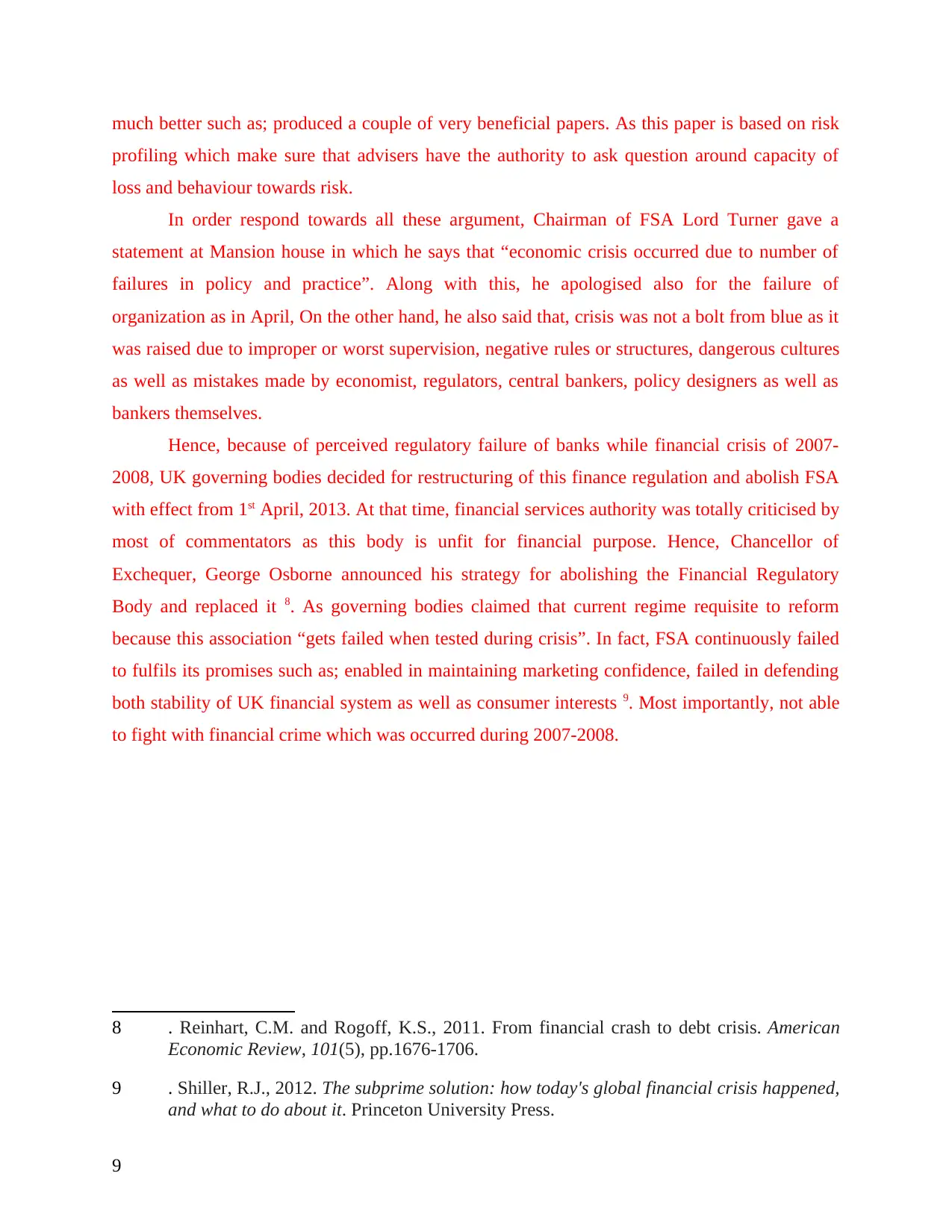

By assessing this above graph, it has been understood that there was a great fall in GDP

of the UK economy in between 2008-2009. Along with this, diagram is clearly highlighting that

UK recovery was seen as most slowest as compared to other. It means, FSA is totally failed in

managing this major turmoil which is almost destroying the markets and economy of a nation. In

fact, future of Britain was in a great dark and people are getting more scared with this

unpredictable situation 10.

It means all the above things and disturbances was enforced financial authorities of UK to

replace the FSA in order to control negative impact of financial crisis from EU.

10 . Tejvan Pettinger, 2017. [Online]. Available through<

https://www.economicshelp.org/blog/7501/economics/the-great-recession/>.

10

of the UK economy in between 2008-2009. Along with this, diagram is clearly highlighting that

UK recovery was seen as most slowest as compared to other. It means, FSA is totally failed in

managing this major turmoil which is almost destroying the markets and economy of a nation. In

fact, future of Britain was in a great dark and people are getting more scared with this

unpredictable situation 10.

It means all the above things and disturbances was enforced financial authorities of UK to

replace the FSA in order to control negative impact of financial crisis from EU.

10 . Tejvan Pettinger, 2017. [Online]. Available through<

https://www.economicshelp.org/blog/7501/economics/the-great-recession/>.

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

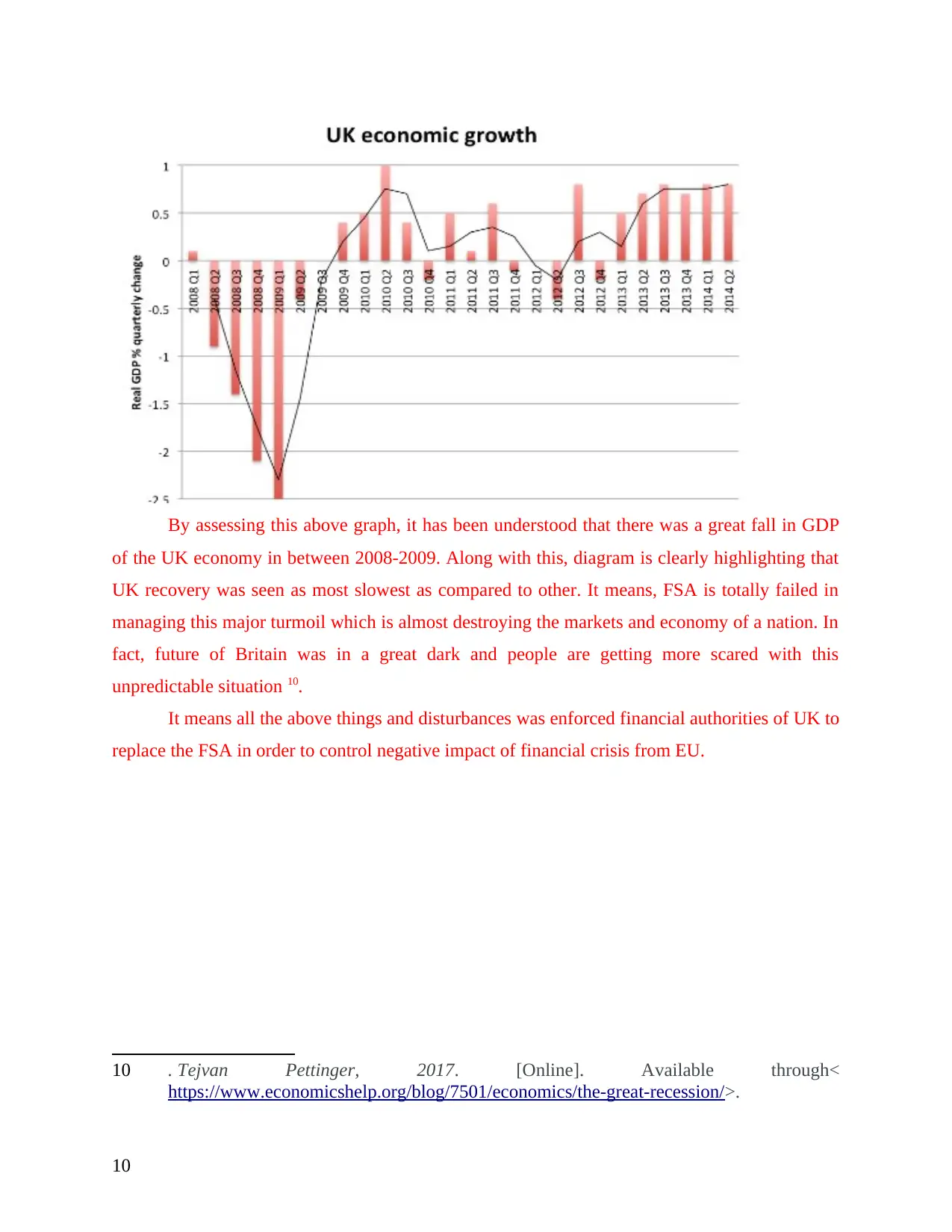

From the diagrammatic representation, it has been identified that governing bodies of UK

are really spending in the development of nation by enhancing labours. Along with this, trying

to come up with various ideas for managing drastic change which affects the lives of whole

nation 11.

Hence, FSA was replaced by the “Twin Peaks” named as “Financial Conduct

Authority” and “Prudential Regulation Authority”. These two frameworks was official came

into force in almost 1st April, 2013 and promises number of things to the UK financial service

sector. However, foremost responsibility of FCA is to controlled financial organizations who is

offering services to the consumers and tries to maintain the integrity of UK’s financial markets

12. Some of the examples are; major focus on customers, problems related with misconduct like

Libor scandal, abusing of market as well as competitiveness. On the other hand, PRA was

formed as a part of The Bank of England and works along with FCA in “twin peaks”.

Additionally, liable for regulating almost 1700 banks across the UK, building communities and

societies as well as managing investment firms.

11 . Tejvan Pettinger, 2017. [Online]. Available through<

https://www.economicshelp.org/blog/7501/economics/the-great-recession/>.

12 . Reinhart, C.M. and Rogoff, K.S., 2011. From financial crash to debt crisis. American

Economic Review, 101(5), pp.1676-1706.

11

are really spending in the development of nation by enhancing labours. Along with this, trying

to come up with various ideas for managing drastic change which affects the lives of whole

nation 11.

Hence, FSA was replaced by the “Twin Peaks” named as “Financial Conduct

Authority” and “Prudential Regulation Authority”. These two frameworks was official came

into force in almost 1st April, 2013 and promises number of things to the UK financial service

sector. However, foremost responsibility of FCA is to controlled financial organizations who is

offering services to the consumers and tries to maintain the integrity of UK’s financial markets

12. Some of the examples are; major focus on customers, problems related with misconduct like

Libor scandal, abusing of market as well as competitiveness. On the other hand, PRA was

formed as a part of The Bank of England and works along with FCA in “twin peaks”.

Additionally, liable for regulating almost 1700 banks across the UK, building communities and

societies as well as managing investment firms.

11 . Tejvan Pettinger, 2017. [Online]. Available through<

https://www.economicshelp.org/blog/7501/economics/the-great-recession/>.

12 . Reinhart, C.M. and Rogoff, K.S., 2011. From financial crash to debt crisis. American

Economic Review, 101(5), pp.1676-1706.

11

FCA is considered as regulator of almost 56,000 financial services firms as well as

financial markets at UK marketplace. On the other hand, prudential regulator is offer around

24,000 of those organizations. Basically, these two were established on 1st APRIL, 2013 for

managing financial trauma of UK as well as in order to act on the behalf of Financial Services

Authority. Basically, their main objective is to make sure that all the related markets work well.

For making more advanced to strategic objectives there are almost three main targets such as;

Protect consumers- in order to secure an effective degree of prevention for customers 13.

Defend financial markets- for defending and enhancing the integrity of UK financial system.

Promote competition- encouraging healthy competition in the interests of consumers.

Hence, major reason behind establishing these two twin peaks is to make that UK have an

effective, creative and trusted financial service sector in order to meet the requirements of users.

Although, initially FCA was handling around 26000 firms and in 2014, took over nearly 50000

client credit firms from which few of them was already regulated for some other activity. After

that authorisation was took place by 31st march, 2016 in order to carrying regulation on credit

activities. Mainly, these two firms are famous for their major aim that is “identify and respond

instantly and effectively towards emerging issues before it will convert into major trauma”. As a

result, financial system of UK plays a major role for stabilizing the UK conditions after financial

crisis of 2007-2008 by replacing “FSA” with “twin peaks” 14.

(Prudential regulatory Authority (PRA)

Regulates This institution is regulates for various banks, enhancing societies, credit unions,

insurers and several investment organizations.

Structure Act as a subsidiary of Bank of England

Coordinate with FCA; Memorandum of understanding frames the

relationship; CEO of both the associations are sit on both Boards.

13 . Laeven, L. and Valencia, F., 2012. Resolution of banking crises. In Handbook of

Safeguarding Global Financial Stability(pp. 231-258).

14

Geels, F.W., 2013. The impact of the financial–economic crisis on sustainability transitions:

Financial investment, governance and public discourse. Environmental Innovation and

Societal Transitions, 6, pp.67-95.

12

financial markets at UK marketplace. On the other hand, prudential regulator is offer around

24,000 of those organizations. Basically, these two were established on 1st APRIL, 2013 for

managing financial trauma of UK as well as in order to act on the behalf of Financial Services

Authority. Basically, their main objective is to make sure that all the related markets work well.

For making more advanced to strategic objectives there are almost three main targets such as;

Protect consumers- in order to secure an effective degree of prevention for customers 13.

Defend financial markets- for defending and enhancing the integrity of UK financial system.

Promote competition- encouraging healthy competition in the interests of consumers.

Hence, major reason behind establishing these two twin peaks is to make that UK have an

effective, creative and trusted financial service sector in order to meet the requirements of users.

Although, initially FCA was handling around 26000 firms and in 2014, took over nearly 50000

client credit firms from which few of them was already regulated for some other activity. After

that authorisation was took place by 31st march, 2016 in order to carrying regulation on credit

activities. Mainly, these two firms are famous for their major aim that is “identify and respond

instantly and effectively towards emerging issues before it will convert into major trauma”. As a

result, financial system of UK plays a major role for stabilizing the UK conditions after financial

crisis of 2007-2008 by replacing “FSA” with “twin peaks” 14.

(Prudential regulatory Authority (PRA)

Regulates This institution is regulates for various banks, enhancing societies, credit unions,

insurers and several investment organizations.

Structure Act as a subsidiary of Bank of England

Coordinate with FCA; Memorandum of understanding frames the

relationship; CEO of both the associations are sit on both Boards.

13 . Laeven, L. and Valencia, F., 2012. Resolution of banking crises. In Handbook of

Safeguarding Global Financial Stability(pp. 231-258).

14

Geels, F.W., 2013. The impact of the financial–economic crisis on sustainability transitions:

Financial investment, governance and public discourse. Environmental Innovation and

Societal Transitions, 6, pp.67-95.

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 21

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.