HI6025 Accounting Theory: Effects of IFRS Adoption in Australia

VerifiedAdded on 2024/05/14

|11

|2446

|110

Report

AI Summary

This report provides an executive summary of the IFRS adoption by Australian companies in 2005, discussing the impacts on financial reporting and accounting quality. It highlights the positive and negative aspects of IFRS, comparing the conditions before and after adoption. The report analyzes the transformation from AASB to IFRS, covering aspects like goodwill capitalization, intangible assets, financial statement readability, and revenue-expense matching. It also discusses the decline in financial reporting costs, rise in management efficiency, and increased investor confidence. The conclusion emphasizes the improvement in comparability of financial statements and the benefits of globalization for Australian companies after IFRS adoption.

HI6025 Accounting Theory and Current

Issue

Issue

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Executive summary:

In this assessment, the brief discussion will be done for the IFRS that Australian companies have

adopted in 2005. The major considerations in this assessment are the IFRS impacts that

companies will face. Codes of IFRS are allotted for the regulation of financial reporting as well

as accounting. Also using the IFRS quality of accounting statement can be improved and

statements can be made more reliable. IFRS have both some positive aspects and some negative

aspects and the report will discuss both in brief. The comparative outlook will be given in this

report for both that is a condition before IFRS adoption and condition after IFRS adoption.

Further, the accounting statement of Australia will be enhanced by taking in account the different

factors like cost, quality and more for the better knowledge of the same. This assessment is done

for learning and understanding the IFRS effects on the Australian financial statement. Different

IFRS rules will be taken and analysed for making the accounting statement consistent so that,

account statements of different companies in different zones of the world could be easily

compared and investigate. AASB are the guidelines which were followed before the IFRS

adoption. As the IFRS got adopted a transformation took place the consistency gets enhanced

among the AASB and IFRS. In implementing IFRS many challenges needs to be faced by

Australian companies but the successful IFRS implementation has greater benefits for the

companies.

In this assessment, the brief discussion will be done for the IFRS that Australian companies have

adopted in 2005. The major considerations in this assessment are the IFRS impacts that

companies will face. Codes of IFRS are allotted for the regulation of financial reporting as well

as accounting. Also using the IFRS quality of accounting statement can be improved and

statements can be made more reliable. IFRS have both some positive aspects and some negative

aspects and the report will discuss both in brief. The comparative outlook will be given in this

report for both that is a condition before IFRS adoption and condition after IFRS adoption.

Further, the accounting statement of Australia will be enhanced by taking in account the different

factors like cost, quality and more for the better knowledge of the same. This assessment is done

for learning and understanding the IFRS effects on the Australian financial statement. Different

IFRS rules will be taken and analysed for making the accounting statement consistent so that,

account statements of different companies in different zones of the world could be easily

compared and investigate. AASB are the guidelines which were followed before the IFRS

adoption. As the IFRS got adopted a transformation took place the consistency gets enhanced

among the AASB and IFRS. In implementing IFRS many challenges needs to be faced by

Australian companies but the successful IFRS implementation has greater benefits for the

companies.

Implications of transformation into the (IFRS) from (AASB) in Australia -

After adoption of IFRS standards in place of AASB standards, there were changes in the

manner financial reporting is carried out –

capitalization of Goodwill impairment and self-generated intangibles –

The central debate regarding goodwill and other intangibles is that whether the company should

amortize these assets or it will be subject to impairment. This puts the company in a complex

situation and at times one method over the other distorts the profits of the company by making it

look more than it actually is. After the adoption of IFRS, those companies who recognized

identifiable intangible assets which are intangible will have to derecognize them. Along with this

revaluation of intangible will be required to be undone. Ji and Lu (2014) added with their

research in the field that after the adoption of IFRS relevance of intangible has seen a significant

decline. However, intangibles are seen to be more related in the firms where these are assumed to

be more trustworthy.

The rise in readability of the financial statements

Financial statements are meant to help the readers of the financial statements to understand the

information mentioned in it effortlessly. One of the basic features of financial statement is its

readability. Cheung and Lau (2016, p. 162) carried out reassert in the field and came up with the

following result. They came up with the following conclusions – after the adoption of the IFRS

system the financial statements that were prepared by the companies have become lengthier;

however, despite their length, their readability has risen significantly. They further added that

three accounting policies being used now that is report of significant accounting strategies,

financial implements, and intangible assets have lengthier disclosures, which contributed to the

length of the financial statements.

The rise in matching between expenses and revenues

Many researches are conducted to investigate the matching between revenues and expenses for

top 200 listed Australian non – financial firms between 1993 and 2011. After this, it further

became reinforced, the importance of matching principle in the traditional accounting system

(Jin et al. 2015). The research concluded that during the period 2001 – 2003 the extent of

After adoption of IFRS standards in place of AASB standards, there were changes in the

manner financial reporting is carried out –

capitalization of Goodwill impairment and self-generated intangibles –

The central debate regarding goodwill and other intangibles is that whether the company should

amortize these assets or it will be subject to impairment. This puts the company in a complex

situation and at times one method over the other distorts the profits of the company by making it

look more than it actually is. After the adoption of IFRS, those companies who recognized

identifiable intangible assets which are intangible will have to derecognize them. Along with this

revaluation of intangible will be required to be undone. Ji and Lu (2014) added with their

research in the field that after the adoption of IFRS relevance of intangible has seen a significant

decline. However, intangibles are seen to be more related in the firms where these are assumed to

be more trustworthy.

The rise in readability of the financial statements

Financial statements are meant to help the readers of the financial statements to understand the

information mentioned in it effortlessly. One of the basic features of financial statement is its

readability. Cheung and Lau (2016, p. 162) carried out reassert in the field and came up with the

following result. They came up with the following conclusions – after the adoption of the IFRS

system the financial statements that were prepared by the companies have become lengthier;

however, despite their length, their readability has risen significantly. They further added that

three accounting policies being used now that is report of significant accounting strategies,

financial implements, and intangible assets have lengthier disclosures, which contributed to the

length of the financial statements.

The rise in matching between expenses and revenues

Many researches are conducted to investigate the matching between revenues and expenses for

top 200 listed Australian non – financial firms between 1993 and 2011. After this, it further

became reinforced, the importance of matching principle in the traditional accounting system

(Jin et al. 2015). The research concluded that during the period 2001 – 2003 the extent of

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

matching between revenues and expenses declined but after the mandatory adoption of the IFRS

system in Australia the matching between revenues and expenses rose. This was attributable to

operating and other expenses which were responsible for increasing coefficient of contemporary

expenses. This shows that after replacing Australian standards with the IFRS standards there was

a rise in the matching of expenses and revenue and this also added to the reliability of the

financial reporting by the company.

The decline in the costs of financial reporting and rise in management efficiency and

investor confidence

After the adoption of IFRS standards in 2005 the Australian companies which were producing a

number of financial statements because of their global operations but now they can just make on

the statement that is a statement based on IFRS standards. This has resulted in significant decline

in the financial reporting costs of the firm and also reduced unnecessary bookkeeping work.

Previously, the companies were preparing multiple financial reports for different countries in

which the companies were carrying out its operation. Now as the IFRS standards are global and

most countries allow their companies to use these standards it has reduced the financial reporting

workload. As the management previously had to read financial records made with different

standards it made their work challenging but after the adoption of the new system they can carry

out management activities with just one single statement. By relying on one statement for

undertaking investment decisions, investors can now make more informed decisions and

previously those investors who were not able to invest in the company because that required

understanding of Australian standards now they will be able to carry out that investment.

After adoption of IFRS standards in place of AASB standards in Australia as seen above there

has been a decline in the impairment brought in the books particularly of the intangibles

(including goodwill) but reliable companies have still maintained it at former levels, legibility of

the financial statement has risen, there has been a rise in matching between revenues and

expenses and decline in cost of financial reporting and rise in managerial efficiency. After the

system was adopted according to the research carried out by AASB the transformation was

smooth and the companies who adopted the new system benefited from a decline in cost and rise

in competitiveness. This helps the companies to undertake expansion across continents without

worrying about the standards of financial reporting in those countries. The adoption of IFRS has

system in Australia the matching between revenues and expenses rose. This was attributable to

operating and other expenses which were responsible for increasing coefficient of contemporary

expenses. This shows that after replacing Australian standards with the IFRS standards there was

a rise in the matching of expenses and revenue and this also added to the reliability of the

financial reporting by the company.

The decline in the costs of financial reporting and rise in management efficiency and

investor confidence

After the adoption of IFRS standards in 2005 the Australian companies which were producing a

number of financial statements because of their global operations but now they can just make on

the statement that is a statement based on IFRS standards. This has resulted in significant decline

in the financial reporting costs of the firm and also reduced unnecessary bookkeeping work.

Previously, the companies were preparing multiple financial reports for different countries in

which the companies were carrying out its operation. Now as the IFRS standards are global and

most countries allow their companies to use these standards it has reduced the financial reporting

workload. As the management previously had to read financial records made with different

standards it made their work challenging but after the adoption of the new system they can carry

out management activities with just one single statement. By relying on one statement for

undertaking investment decisions, investors can now make more informed decisions and

previously those investors who were not able to invest in the company because that required

understanding of Australian standards now they will be able to carry out that investment.

After adoption of IFRS standards in place of AASB standards in Australia as seen above there

has been a decline in the impairment brought in the books particularly of the intangibles

(including goodwill) but reliable companies have still maintained it at former levels, legibility of

the financial statement has risen, there has been a rise in matching between revenues and

expenses and decline in cost of financial reporting and rise in managerial efficiency. After the

system was adopted according to the research carried out by AASB the transformation was

smooth and the companies who adopted the new system benefited from a decline in cost and rise

in competitiveness. This helps the companies to undertake expansion across continents without

worrying about the standards of financial reporting in those countries. The adoption of IFRS has

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

added to the competitiveness of the Australian firms and has helped them to raise finances on a

global level, which will increase their expansion capabilities.

global level, which will increase their expansion capabilities.

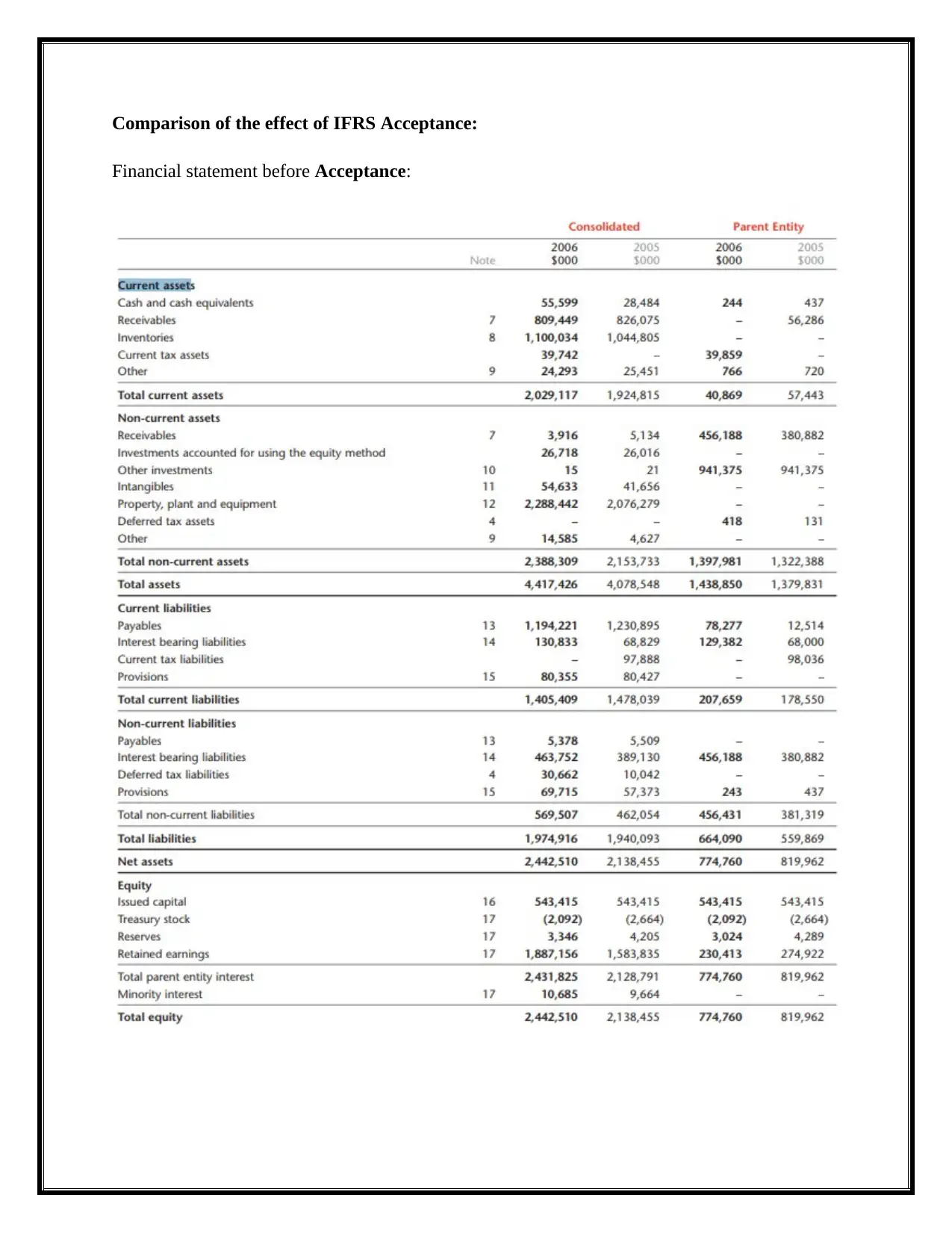

Comparison of the effect of IFRS Acceptance:

Financial statement before Acceptance:

Financial statement before Acceptance:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

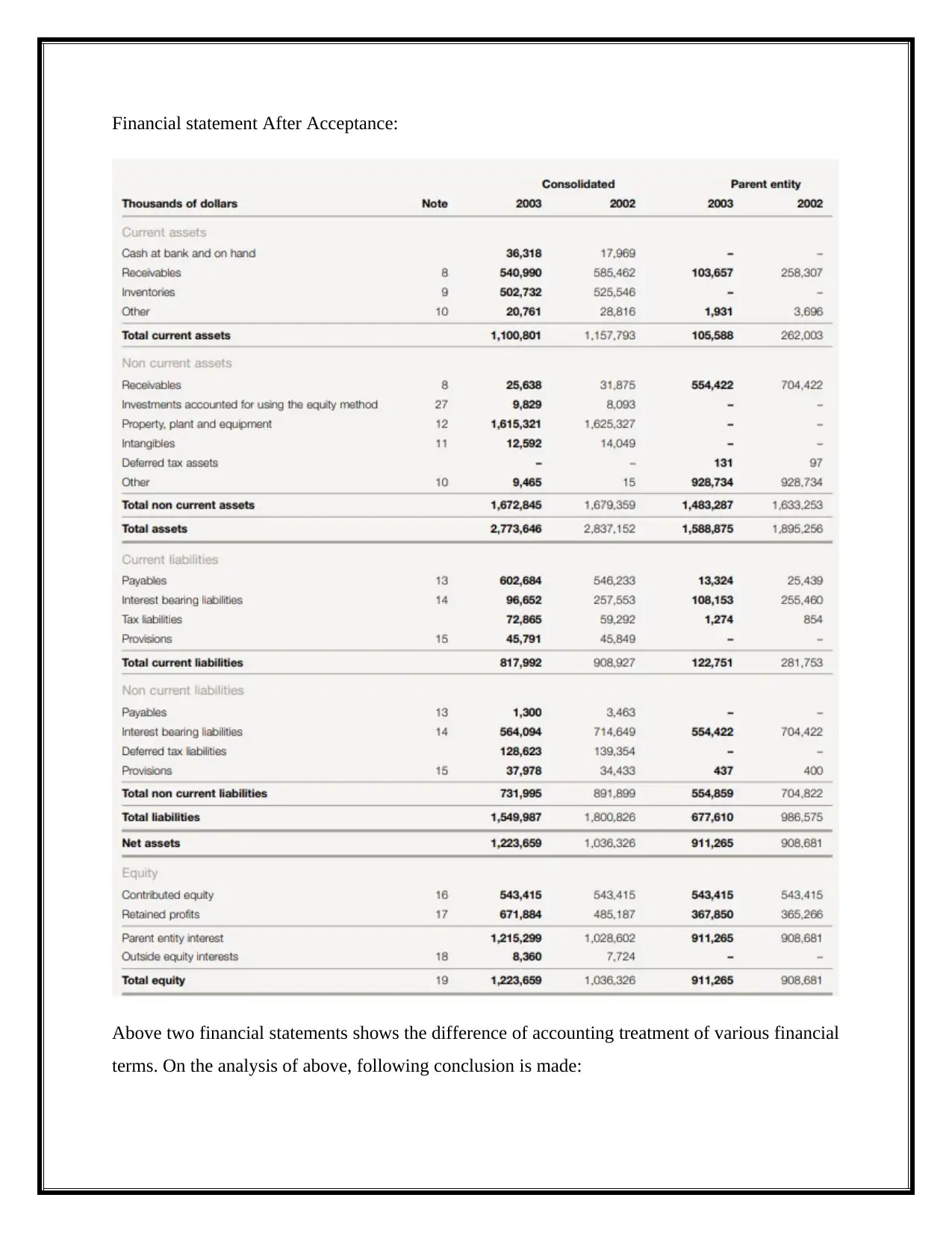

Financial statement After Acceptance:

Above two financial statements shows the difference of accounting treatment of various financial

terms. On the analysis of above, following conclusion is made:

Above two financial statements shows the difference of accounting treatment of various financial

terms. On the analysis of above, following conclusion is made:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Impact on the quality of Accounting

Maximum researches on IFRS impact conclude that Adoption of IFRS has a optimistic impact on

the quality of accounting. It improves the faith and reliability of user on financial statements and

provides a way to make accounting reporting more comparable (Chua, et.al, 2012). After the

acceptance of IFRS, Financial Statements of Australian companies become more understandable

for the global user which is also a proof of increased accounting quality.

Inventory valuation and depreciation:

After the adoption of IFRS rules, use of LIFO method for inventory valuation is banned due to

practicalness of this system. In some cases, depreciation calculation for the associated parts of

machinery made separately.

Impact on Income Recognition system:

IFRS portrays income as a gross inflow of monetary benefits perspective understanding an

extension in esteem debts; aside from prepare esteem duties made with the aid of owners. This

prompts differentiates in how arrangements, gain and surrendered pay are seen and uncovered

( Bryce, et.al, 2015). The qualifications in income affirmation can influence internet pay and a

large assortment of coins associated extents, inciting a long way accomplishing adjustments in an

affiliation's execution measures when changing to IFRS.

Treatment of business combination transaction:

According to the AASB rules, the business combination transactions like business acquisition

and business purchase conducted before the January 2004 was not included in the financial

statements but after the Acceptance Goodwill is communicated at introduced much less any

gathered impairment losses (Loyeung, et.al, 2016). Goodwill is distributed to coins making

gadgets and is attempted every 12 months for a deterrent. In respect of tremendous worth

accounted investees, the passing on a measure of selflessness is fused into the passing on a

measure of the passion for the partner. Negative liberality developing on an acquisition is seen

direct inside the repayment enunciation.

Treatment of Good and service Tax

Maximum researches on IFRS impact conclude that Adoption of IFRS has a optimistic impact on

the quality of accounting. It improves the faith and reliability of user on financial statements and

provides a way to make accounting reporting more comparable (Chua, et.al, 2012). After the

acceptance of IFRS, Financial Statements of Australian companies become more understandable

for the global user which is also a proof of increased accounting quality.

Inventory valuation and depreciation:

After the adoption of IFRS rules, use of LIFO method for inventory valuation is banned due to

practicalness of this system. In some cases, depreciation calculation for the associated parts of

machinery made separately.

Impact on Income Recognition system:

IFRS portrays income as a gross inflow of monetary benefits perspective understanding an

extension in esteem debts; aside from prepare esteem duties made with the aid of owners. This

prompts differentiates in how arrangements, gain and surrendered pay are seen and uncovered

( Bryce, et.al, 2015). The qualifications in income affirmation can influence internet pay and a

large assortment of coins associated extents, inciting a long way accomplishing adjustments in an

affiliation's execution measures when changing to IFRS.

Treatment of business combination transaction:

According to the AASB rules, the business combination transactions like business acquisition

and business purchase conducted before the January 2004 was not included in the financial

statements but after the Acceptance Goodwill is communicated at introduced much less any

gathered impairment losses (Loyeung, et.al, 2016). Goodwill is distributed to coins making

gadgets and is attempted every 12 months for a deterrent. In respect of tremendous worth

accounted investees, the passing on a measure of selflessness is fused into the passing on a

measure of the passion for the partner. Negative liberality developing on an acquisition is seen

direct inside the repayment enunciation.

Treatment of Good and service Tax

IFRS acceptance also gives an appropriate method to identify the GST expenses. Fees, assets and

wages are seen internet of the measure of GST, besides for wherein the measure of GST finished

is not recoverable from the government (ATO). In these situations, the GST is seen as a portion

of the price of obtaining the benefit or as a detail of the component of cost. Debtors and creditors

are communicated with the measure of GST protected. The net degree of GST receivable from,

or outstanding to, the government (ATO) is joined as a gift asset or threat to be resolved sheet

(Firth, and Gounopoulos, 2017).

Treatment of Operating Leases:

After the approval of IFRS by AASB board, a more appropriate way to identify the contingent

rent is provided by the IFRS rules. As per the IFRS, Operating leases are visible as a price in the

duration wherein they may be gained (Young, et.al, 2015). Lease inspirations got are visible in

the compensation explanation as an essential little bit of the overall lease cost on a straight-line

method basis over lease time.

Treatment of Research and development expenses:

Expenses related with investigation and development activities, whereby investigate disclosures

are related to a plan or layout for the age of new or basically upgraded things and systems, is

superior if the thing or procedure is truth be informed and modern possible, destiny money

related points of interest are probable and the Group has sufficient funds for entire development

work (Kabir, and Rahman, 2016). The expenditure related to development involves material

cost; the cost of labour and an inexpensive degree of overheads. Another expenditure related to

development is visible inside the profit statement as a cost as executed. Advanced change usage

is communicated as incurred huge harm much less amassed amortization and incapacitation

mishaps.

wages are seen internet of the measure of GST, besides for wherein the measure of GST finished

is not recoverable from the government (ATO). In these situations, the GST is seen as a portion

of the price of obtaining the benefit or as a detail of the component of cost. Debtors and creditors

are communicated with the measure of GST protected. The net degree of GST receivable from,

or outstanding to, the government (ATO) is joined as a gift asset or threat to be resolved sheet

(Firth, and Gounopoulos, 2017).

Treatment of Operating Leases:

After the approval of IFRS by AASB board, a more appropriate way to identify the contingent

rent is provided by the IFRS rules. As per the IFRS, Operating leases are visible as a price in the

duration wherein they may be gained (Young, et.al, 2015). Lease inspirations got are visible in

the compensation explanation as an essential little bit of the overall lease cost on a straight-line

method basis over lease time.

Treatment of Research and development expenses:

Expenses related with investigation and development activities, whereby investigate disclosures

are related to a plan or layout for the age of new or basically upgraded things and systems, is

superior if the thing or procedure is truth be informed and modern possible, destiny money

related points of interest are probable and the Group has sufficient funds for entire development

work (Kabir, and Rahman, 2016). The expenditure related to development involves material

cost; the cost of labour and an inexpensive degree of overheads. Another expenditure related to

development is visible inside the profit statement as a cost as executed. Advanced change usage

is communicated as incurred huge harm much less amassed amortization and incapacitation

mishaps.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Conclusion:

IFRS was adopted to provide strength to the accounting system of Australia so that Australian

companies can make internationally comparable financial statements. Previously financial

statements were made according to the AASB standard guidelines when IFRS rules were not

accepted in Australia and these rules were accepted to establish consistency in financial

statements. A depth discussion on the effects of IFRS adoption is made in above assignment

report and report concludes that the step of acceptance of IFRS was a game-changing action and

it has a significant impact on the financial reporting quality. A view of previous (before IFRS

acceptance) accounting system through the description of various accounting terms is also given

in above report which proves that the accounting system of Australia was good before the

adoption and the adoption is made to make a uniformity among global and Australian accounting

principles. The report also determines that the Application of IFRS was improved the

comparability of financial statements with global companies and aid to get the advantage of

globalisation. Capital is a big issue for every business and report proves the acceptance of IFRS

in 2005 was improved the capital availability for Australian companies and reduced the cost of

capital by availing the capital of global investors.

IFRS was adopted to provide strength to the accounting system of Australia so that Australian

companies can make internationally comparable financial statements. Previously financial

statements were made according to the AASB standard guidelines when IFRS rules were not

accepted in Australia and these rules were accepted to establish consistency in financial

statements. A depth discussion on the effects of IFRS adoption is made in above assignment

report and report concludes that the step of acceptance of IFRS was a game-changing action and

it has a significant impact on the financial reporting quality. A view of previous (before IFRS

acceptance) accounting system through the description of various accounting terms is also given

in above report which proves that the accounting system of Australia was good before the

adoption and the adoption is made to make a uniformity among global and Australian accounting

principles. The report also determines that the Application of IFRS was improved the

comparability of financial statements with global companies and aid to get the advantage of

globalisation. Capital is a big issue for every business and report proves the acceptance of IFRS

in 2005 was improved the capital availability for Australian companies and reduced the cost of

capital by availing the capital of global investors.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

References

Cheung, E. and J. Lau (2016). “Readability of Notes to the Financial Statements and the

Adoption of IFRS.” Australian Accounting Review 26(2): 162-176

Jin, K., Y. Shan and S. Taylor (2015). “Matching between revenues and expenses and the

adoption of International Financial Reporting Standards.” Pacific-Basin Finance Journal

35(Part A): 90-107.

Ji, X. and L. Wei. (2014). “The value relevance and reliability of intangible assets:

Evidence from Australia before and after adopting IFRS.” Asian Review of

Accounting22(3): 182-216.

Iasplus.com. (2018). AASB research report concludes that IFRS adoption has benefited

the Australian economy. [online] Available at:

https://www.iasplus.com/en/news/2016/10/aasb [Accessed 25 May 2018].

Chua, Y.L., Cheong, C.S. and Gould, G., 2012. The impact of mandatory IFRS adoption

on accounting quality: Evidence from Australia. Journal of International Accounting

Research, 11(1), pp.119-146.

Bryce, M., Ali, M.J. and Mather, P.R., 2015. Accounting quality in the pre-/post-IFRS

adoption periods and the impact on audit committee effectiveness—Evidence from

Australia. Pacific-Basin Finance Journal, 35, pp.163-181.

Loyeung, A., Matolcsy, Z., Weber, J. and Wells, P., 2016. The cost of implementing new

accounting standards: The case of IFRS adoption in Australia. Australian Journal of

Management, 41(4), pp.611-632.

Kabir, H. and Rahman, A., 2016. The role of corporate governance in accounting

discretion under IFRS: Goodwill impairment in Australia. Journal of Contemporary

Accounting & Economics, 12(3), pp.290-308.

Ntoung Agbor Tabot, L., Fernandez, I.P. and Cibran, P.F., 2015. Operating Cash Flow

and Earnings Under IFRS/GAAP: Evidence from Australia, France & UK.

Firth, M. and Gounopoulos, D., 2017. IFRS adoption and management earnings forecasts

of Australian IPOs.

Cheung, E. and J. Lau (2016). “Readability of Notes to the Financial Statements and the

Adoption of IFRS.” Australian Accounting Review 26(2): 162-176

Jin, K., Y. Shan and S. Taylor (2015). “Matching between revenues and expenses and the

adoption of International Financial Reporting Standards.” Pacific-Basin Finance Journal

35(Part A): 90-107.

Ji, X. and L. Wei. (2014). “The value relevance and reliability of intangible assets:

Evidence from Australia before and after adopting IFRS.” Asian Review of

Accounting22(3): 182-216.

Iasplus.com. (2018). AASB research report concludes that IFRS adoption has benefited

the Australian economy. [online] Available at:

https://www.iasplus.com/en/news/2016/10/aasb [Accessed 25 May 2018].

Chua, Y.L., Cheong, C.S. and Gould, G., 2012. The impact of mandatory IFRS adoption

on accounting quality: Evidence from Australia. Journal of International Accounting

Research, 11(1), pp.119-146.

Bryce, M., Ali, M.J. and Mather, P.R., 2015. Accounting quality in the pre-/post-IFRS

adoption periods and the impact on audit committee effectiveness—Evidence from

Australia. Pacific-Basin Finance Journal, 35, pp.163-181.

Loyeung, A., Matolcsy, Z., Weber, J. and Wells, P., 2016. The cost of implementing new

accounting standards: The case of IFRS adoption in Australia. Australian Journal of

Management, 41(4), pp.611-632.

Kabir, H. and Rahman, A., 2016. The role of corporate governance in accounting

discretion under IFRS: Goodwill impairment in Australia. Journal of Contemporary

Accounting & Economics, 12(3), pp.290-308.

Ntoung Agbor Tabot, L., Fernandez, I.P. and Cibran, P.F., 2015. Operating Cash Flow

and Earnings Under IFRS/GAAP: Evidence from Australia, France & UK.

Firth, M. and Gounopoulos, D., 2017. IFRS adoption and management earnings forecasts

of Australian IPOs.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.