Financial Reporting: Impairment Loss on Cash Generating Units-AASB 136

VerifiedAdded on 2023/04/03

|5

|1599

|86

Report

AI Summary

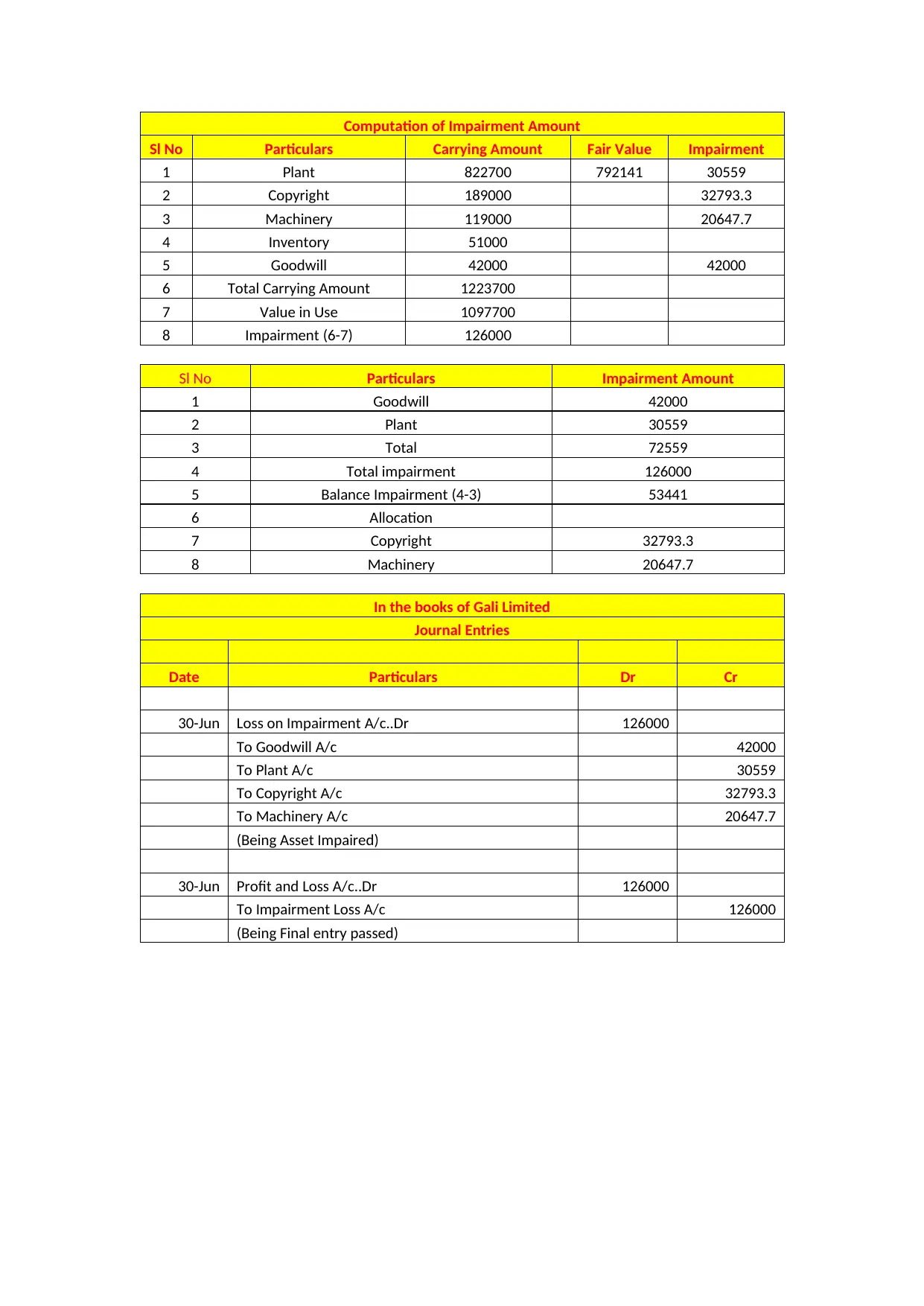

This report provides an analysis of impairment loss for cash-generating units (CGUs) as defined under AASB 136, the Australian accounting standard for impairment of assets. It explains the key concepts, recognition, and measurement of impairment loss, focusing on how to identify CGUs and determine their recoverable amounts. The report discusses scenarios where the recoverable amount of individual assets cannot be determined and emphasizes the importance of arm's length transactions in internal transfers. It includes a detailed example with journal entries, illustrating the computation and allocation of impairment loss among various assets within a CGU, such as goodwill, plant, copyright, and machinery, in accordance with AASB guidelines. The document also references relevant sections of the Corporations Act 2001 and accounting news from BDO Australia Ltd. to provide a comprehensive understanding of the topic.

1 out of 5

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.