Detailed Analysis of Impairment Loss in Corporate Accounting

VerifiedAdded on 2023/06/11

|11

|2560

|142

Report

AI Summary

This report provides a detailed analysis of impairment loss in corporate accounting, focusing on the application of AASB 136. It defines key terms such as carrying amount, cash generating unit (CGU), cost of disposal, and recoverable amount, explaining how to determine impairment loss and when to reverse it. The report outlines the indicators of impairment, both external and internal, and details the process for identifying CGUs and allocating impairment losses. It also includes practical examples with journal entries for impairment loss computation, excluding inventories. The document concludes by emphasizing the disclosure requirements for impairment loss in CGUs, offering a comprehensive understanding of the accounting standards and procedures involved. Desklib provides a platform to access this document along with numerous solved assignments and past papers.

Running head: CORPORATE ACCOUNTING

Corporate accounting

Name of the student

Name of the university

Student ID

Author note

Corporate accounting

Name of the student

Name of the university

Student ID

Author note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2CORPORATE ACCOUNTING

Part A

Impairment loss for cash generating unit excluding goodwill

The main objective of the standard that is AASB 136 on Impairment of the

assets depicts that the assets in the financial statement of the company shall not be

carried out at the amount which is greater than its recoverable amount. Any asset is

recorded at greater than its recoverable amount while the carrying amount of the

asset is more than recoverable amount through the sale or use of the asset

(Corgnati et al. 2013). In this case the asset will be regarded as impaired and it will

require the company to identify the amount of impairment loss. AASB 136 also states

the scenario under which the impairment loss reversal shall be carried out and

disclosed. However the standard is not applicable to inventories, deferred tax assets,

assets generated from the construction contracts, assets generated from the

employee benefits or the assets identified as held for the purpose of sale. The

reason is that the standard is applicable to the mentioned assets that contain the

requirement for measuring and recognising the assets (Robinson and Sensoy 2016).

The standard is applicable to the assets those are carried at the revalued amount

that is the fair value at the revaluation date reduced by the amount of depreciation

and impairment, if any (Aasb.gov.au 2018).

For the accounting standard the term carrying amount is defined as the

amount for which the asset is recorded after subtracting the accumulated

depreciation and accumulated impairment losses, if any. Further, the term cash

generating unit (CGU) is defined as the smallest group for identifiable asset that

create cash inflows. The cash inflows here are widely independent of cash flows

generated from various other assets or the group of asset. Cost of disposal is the

Part A

Impairment loss for cash generating unit excluding goodwill

The main objective of the standard that is AASB 136 on Impairment of the

assets depicts that the assets in the financial statement of the company shall not be

carried out at the amount which is greater than its recoverable amount. Any asset is

recorded at greater than its recoverable amount while the carrying amount of the

asset is more than recoverable amount through the sale or use of the asset

(Corgnati et al. 2013). In this case the asset will be regarded as impaired and it will

require the company to identify the amount of impairment loss. AASB 136 also states

the scenario under which the impairment loss reversal shall be carried out and

disclosed. However the standard is not applicable to inventories, deferred tax assets,

assets generated from the construction contracts, assets generated from the

employee benefits or the assets identified as held for the purpose of sale. The

reason is that the standard is applicable to the mentioned assets that contain the

requirement for measuring and recognising the assets (Robinson and Sensoy 2016).

The standard is applicable to the assets those are carried at the revalued amount

that is the fair value at the revaluation date reduced by the amount of depreciation

and impairment, if any (Aasb.gov.au 2018).

For the accounting standard the term carrying amount is defined as the

amount for which the asset is recorded after subtracting the accumulated

depreciation and accumulated impairment losses, if any. Further, the term cash

generating unit (CGU) is defined as the smallest group for identifiable asset that

create cash inflows. The cash inflows here are widely independent of cash flows

generated from various other assets or the group of asset. Cost of disposal is the

3CORPORATE ACCOUNTING

incremental cost that is directly attributable to disposal of the asset or the CGU while

the income tax expenses and finance costs are not taken into consideration.

Recoverable amount of the assets or CGU is value and use and fair value reduced

by cost of disposal, whichever is higher. Finally the impairment loss is the amount of

loss by which the asset’s carrying amount or the CGU exceeds the recoverable

amount (Bond, Govendir and Wells 2016).

The entity shall assess the asset at the end of every reporting period to check

whether any signal is there for the impairment. If the signal for impairment exists the

entity shall immediately estimate the asset’s recoverable amount. However,

irrespective of the signal the company shall assess the intangible asset for

impairment that has recognisable useful asset and not yet available for the use

through comparing the carrying amount with the recoverable amount. The

impairment test shall be performed at any of the time during the year however; it

shall be carried on same time for each year. Various intangible assets shall be tested

for impairment at various times. However, the test shall be carried out before the

current annual period end (Accounting, Part and Plans 2015). The ability of the

intangible asset to create adequate economic benefits for recovering the carrying

amount is subject to the greater uncertainty when the asset is not available for use

as compared to the time when the asset is available for the use. Therefore, the

company shall test the impairment at least annually for computing the carrying

amount of the asset that is not yet available for use. While assessing the impairment

indication for any asset the company shall takes into consideration the specific

external sources as well as internal sources of information. The external sources are

– (i) the market value of the asset during the period has been significantly reduced

more than expectation owing to normal use (ii) considerable changes has been

incremental cost that is directly attributable to disposal of the asset or the CGU while

the income tax expenses and finance costs are not taken into consideration.

Recoverable amount of the assets or CGU is value and use and fair value reduced

by cost of disposal, whichever is higher. Finally the impairment loss is the amount of

loss by which the asset’s carrying amount or the CGU exceeds the recoverable

amount (Bond, Govendir and Wells 2016).

The entity shall assess the asset at the end of every reporting period to check

whether any signal is there for the impairment. If the signal for impairment exists the

entity shall immediately estimate the asset’s recoverable amount. However,

irrespective of the signal the company shall assess the intangible asset for

impairment that has recognisable useful asset and not yet available for the use

through comparing the carrying amount with the recoverable amount. The

impairment test shall be performed at any of the time during the year however; it

shall be carried on same time for each year. Various intangible assets shall be tested

for impairment at various times. However, the test shall be carried out before the

current annual period end (Accounting, Part and Plans 2015). The ability of the

intangible asset to create adequate economic benefits for recovering the carrying

amount is subject to the greater uncertainty when the asset is not available for use

as compared to the time when the asset is available for the use. Therefore, the

company shall test the impairment at least annually for computing the carrying

amount of the asset that is not yet available for use. While assessing the impairment

indication for any asset the company shall takes into consideration the specific

external sources as well as internal sources of information. The external sources are

– (i) the market value of the asset during the period has been significantly reduced

more than expectation owing to normal use (ii) considerable changes has been

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

4CORPORATE ACCOUNTING

taken place or will take place in future period with adverse impact on the company

during the period. The changes can be in the market, legal, technological or

economic environment under which the company operates or the market to which

the asset is contributed (iii) interest rate in the market or any other return rate of

market on the investment during the period increased. Further, the increases are

expected to have an impact on the rate of discount that is used for computing the

worth of the asset in use and the recoverable amount of asset is decreased

materially (iv) carrying amount of the company’s net asset is more as compared to

the market capitalization. On the other hand, the internal sources of indication are –

(i) it is evidential that asset is obsolete or physically damaged (ii) considerable

changes has been taken place or will take place in future period with adverse impact

on the company during the period. The change includes the plans of reorganization

or discontinuation of the operation; asset is idle, plans for disposing-off the asset

before the date of expectation. It further includes the reassessment of the asset’s

useful life as definite as against indefinite (iii) it is evidential from internal sources

that the economic performance of the asset is worse as compared to expectation.

Paragraph 66 – 108 stated the requirements to identify the CGU to which the

asset is included and determines the carrying value and identify the amount of

impairment loss for the CGU. If signal is there that the asset can be impaired then

the recoverable amount must be projected for the individual asset. If determination of

recoverable amount for individual asset is not possible the company must determine

the CGU’s recoverable amount under which the asset is included (Abbott and Tan‐

Kantor 2017). Further, the individual asset’s recoverable amount is not possible to

determine if any cash inflows cannot be generated from the asset that is widely

independent from the other assets. Individual asset’s recoverable amount is also not

taken place or will take place in future period with adverse impact on the company

during the period. The changes can be in the market, legal, technological or

economic environment under which the company operates or the market to which

the asset is contributed (iii) interest rate in the market or any other return rate of

market on the investment during the period increased. Further, the increases are

expected to have an impact on the rate of discount that is used for computing the

worth of the asset in use and the recoverable amount of asset is decreased

materially (iv) carrying amount of the company’s net asset is more as compared to

the market capitalization. On the other hand, the internal sources of indication are –

(i) it is evidential that asset is obsolete or physically damaged (ii) considerable

changes has been taken place or will take place in future period with adverse impact

on the company during the period. The change includes the plans of reorganization

or discontinuation of the operation; asset is idle, plans for disposing-off the asset

before the date of expectation. It further includes the reassessment of the asset’s

useful life as definite as against indefinite (iii) it is evidential from internal sources

that the economic performance of the asset is worse as compared to expectation.

Paragraph 66 – 108 stated the requirements to identify the CGU to which the

asset is included and determines the carrying value and identify the amount of

impairment loss for the CGU. If signal is there that the asset can be impaired then

the recoverable amount must be projected for the individual asset. If determination of

recoverable amount for individual asset is not possible the company must determine

the CGU’s recoverable amount under which the asset is included (Abbott and Tan‐

Kantor 2017). Further, the individual asset’s recoverable amount is not possible to

determine if any cash inflows cannot be generated from the asset that is widely

independent from the other assets. Individual asset’s recoverable amount is also not

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

5CORPORATE ACCOUNTING

possible if the value in use of the asset is not possible to project to near its fair value

reduced by selling cost. If there is an active market for the output generated by the

group of asset or the individual asset the group of asset or the individual asset shall

be recognized as the CGU even if all the output or some of the output is internally

used. Further, if cash inflows created by any individual asset or CGU are impacted

by the internal transfer pricing the company shall use the best estimate by the

management for future prices that can be obtained under arm length transaction

(Hull and White 2014). It is applied while estimating the future outflows of cash that is

used for determining the value in use of CGU or any other individual asset that may

be impacted by the internal transfer pricing. The CGU shall be recognized

consistently for same asset or for same kind of asset from period to period unless

any changes have been recognized.

Recoverable amount of the CGU is greater among the value in use and fair

value less selling cost. The carrying value of CGU must be determined on the basis

that is consistent with the method in which the CGU’s recoverable amount is

determined. While the assets are combined as a group for assessing the

recoverability it is suggested to include all the assets under the CGU those are used

to generate relevant cash inflows (Kabir, Rahman and Su 2017). On the contrary, the

CGU are considered as fully recoverable if the impairment loss takes place. While

testing the CGU for impairment the company shall recognize all corporate assets

that are associated to the CGU under consideration. The corporate asset includes

the individual asset or the group of the asset like headquarter building, research

centre or EDP equipment. If part of the carrying value of corporate asset can be

assigned to the unit on consistent and reasonable basis the company shall compare

the unit’s carrying amount inclusive of the part of corporate asset’s carrying amount

possible if the value in use of the asset is not possible to project to near its fair value

reduced by selling cost. If there is an active market for the output generated by the

group of asset or the individual asset the group of asset or the individual asset shall

be recognized as the CGU even if all the output or some of the output is internally

used. Further, if cash inflows created by any individual asset or CGU are impacted

by the internal transfer pricing the company shall use the best estimate by the

management for future prices that can be obtained under arm length transaction

(Hull and White 2014). It is applied while estimating the future outflows of cash that is

used for determining the value in use of CGU or any other individual asset that may

be impacted by the internal transfer pricing. The CGU shall be recognized

consistently for same asset or for same kind of asset from period to period unless

any changes have been recognized.

Recoverable amount of the CGU is greater among the value in use and fair

value less selling cost. The carrying value of CGU must be determined on the basis

that is consistent with the method in which the CGU’s recoverable amount is

determined. While the assets are combined as a group for assessing the

recoverability it is suggested to include all the assets under the CGU those are used

to generate relevant cash inflows (Kabir, Rahman and Su 2017). On the contrary, the

CGU are considered as fully recoverable if the impairment loss takes place. While

testing the CGU for impairment the company shall recognize all corporate assets

that are associated to the CGU under consideration. The corporate asset includes

the individual asset or the group of the asset like headquarter building, research

centre or EDP equipment. If part of the carrying value of corporate asset can be

assigned to the unit on consistent and reasonable basis the company shall compare

the unit’s carrying amount inclusive of the part of corporate asset’s carrying amount

6CORPORATE ACCOUNTING

that is assigned to the unit with the recoverable amount (Singleton-Green 2014).

However, if the part of corporate asset’s carrying amount cannot be assigned to the

unit on consistent and reasonable basis the company shall – (i) compare the unit’s

carrying amount not taking into consideration corporate asset with the recoverable

amount and shall identify the impairment loss, if any (ii) compare the group’s carrying

amount of the CGU taking into consideration the corporate asset that is assigned to

the group of units along with the group’s recoverable amount (Johnson 2014). Here

in this case, the impairment loss must be recognised, if any (iii) the smallest group of

the CGU shall be identified that is inclusive of CGU under review and under which

part of the carrying amount of corporate asset can be assigned on consistent and

reasonable basis (Vanza, Wells and Wright 2018).

Impairment loss for the CGU (the smallest group of CGU) shall be identified if

the recoverable value of the unit is less as compared to the carrying value of the unit.

The amount of impairment loss shall be assigned to reduce carrying amount of

assets in the following manner – (i) in the 1st step, the carrying amount of goodwill

that is assigned to CGU shall be reduced (ii) thereafter the amount shall be assigned

to other assets of the CGU on pro rata basis on carrying value for each of the asset

(Rennekamp, Rupar and Seybert 2014). The reduction for the carrying amount shall

be recognized and recorded as impairment looses on the individual asset. While the

impairment loss in assigned the company shall not reduce carrying amount of the

asset at the higher values among – (i) the fair value reduced by the selling cost (ii)

value in use and (iii) zero.

Reversal of the impairment loss for the CGU shall be assigned to the assets

of the CGU excluding the goodwill. The allocation shall be made on pro rata basis

based on carrying value of the asset. The increase of the carrying value owing to the

that is assigned to the unit with the recoverable amount (Singleton-Green 2014).

However, if the part of corporate asset’s carrying amount cannot be assigned to the

unit on consistent and reasonable basis the company shall – (i) compare the unit’s

carrying amount not taking into consideration corporate asset with the recoverable

amount and shall identify the impairment loss, if any (ii) compare the group’s carrying

amount of the CGU taking into consideration the corporate asset that is assigned to

the group of units along with the group’s recoverable amount (Johnson 2014). Here

in this case, the impairment loss must be recognised, if any (iii) the smallest group of

the CGU shall be identified that is inclusive of CGU under review and under which

part of the carrying amount of corporate asset can be assigned on consistent and

reasonable basis (Vanza, Wells and Wright 2018).

Impairment loss for the CGU (the smallest group of CGU) shall be identified if

the recoverable value of the unit is less as compared to the carrying value of the unit.

The amount of impairment loss shall be assigned to reduce carrying amount of

assets in the following manner – (i) in the 1st step, the carrying amount of goodwill

that is assigned to CGU shall be reduced (ii) thereafter the amount shall be assigned

to other assets of the CGU on pro rata basis on carrying value for each of the asset

(Rennekamp, Rupar and Seybert 2014). The reduction for the carrying amount shall

be recognized and recorded as impairment looses on the individual asset. While the

impairment loss in assigned the company shall not reduce carrying amount of the

asset at the higher values among – (i) the fair value reduced by the selling cost (ii)

value in use and (iii) zero.

Reversal of the impairment loss for the CGU shall be assigned to the assets

of the CGU excluding the goodwill. The allocation shall be made on pro rata basis

based on carrying value of the asset. The increase of the carrying value owing to the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

7CORPORATE ACCOUNTING

reversal of impairment shall be recognised and recorded as reversal of impairment

losses for the individual asset. While assigning the impairment loss reversal value for

the CGU the carrying value of the asset to which the amount is allocated shall not be

increased above – (i) the recoverable value if it can be assessed and (ii) the carrying

amount of the asset that would have assessed after deducting the depreciation and

amortisation, if any, whichever is lower (Christensen and Nikolaev 2013).

For disclosing the impairment loss for CGU the following shall be disclosed –

(i) description of CGU like plant, product line, geographical area, business operation

or the reportable segment (ii) amount recognized for impairment loss or reversal for

the asset class if the company reports the segment information (iii) if the aggregate

amount of asset for the CGU has altered from previous projection of CGU’ s

recoverable amount the description of previous and present method of aggregating

the assets and changes in the recognition of CGU (Zhuang 2016).

reversal of impairment shall be recognised and recorded as reversal of impairment

losses for the individual asset. While assigning the impairment loss reversal value for

the CGU the carrying value of the asset to which the amount is allocated shall not be

increased above – (i) the recoverable value if it can be assessed and (ii) the carrying

amount of the asset that would have assessed after deducting the depreciation and

amortisation, if any, whichever is lower (Christensen and Nikolaev 2013).

For disclosing the impairment loss for CGU the following shall be disclosed –

(i) description of CGU like plant, product line, geographical area, business operation

or the reportable segment (ii) amount recognized for impairment loss or reversal for

the asset class if the company reports the segment information (iii) if the aggregate

amount of asset for the CGU has altered from previous projection of CGU’ s

recoverable amount the description of previous and present method of aggregating

the assets and changes in the recognition of CGU (Zhuang 2016).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

8CORPORATE ACCOUNTING

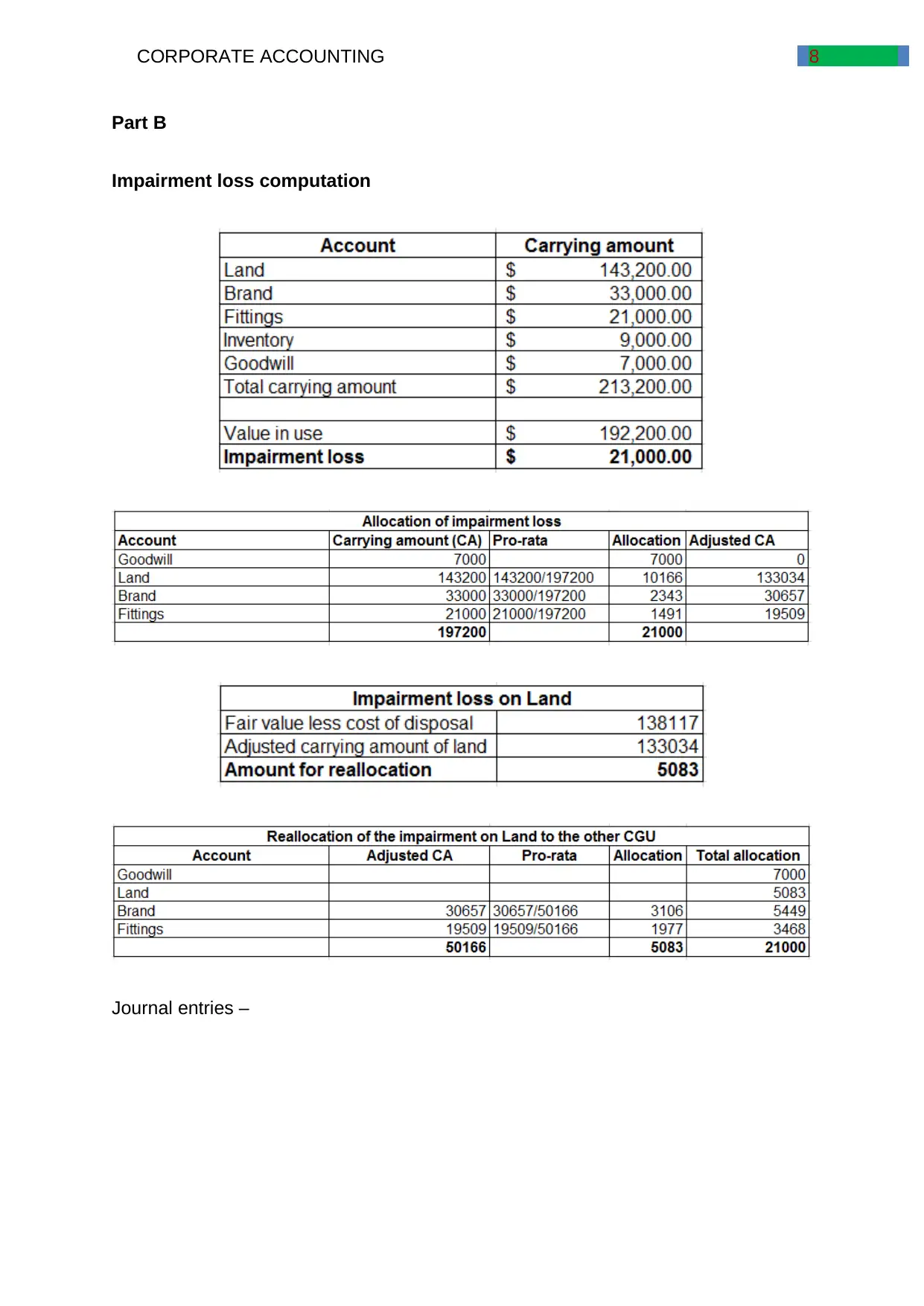

Part B

Impairment loss computation

Journal entries –

Part B

Impairment loss computation

Journal entries –

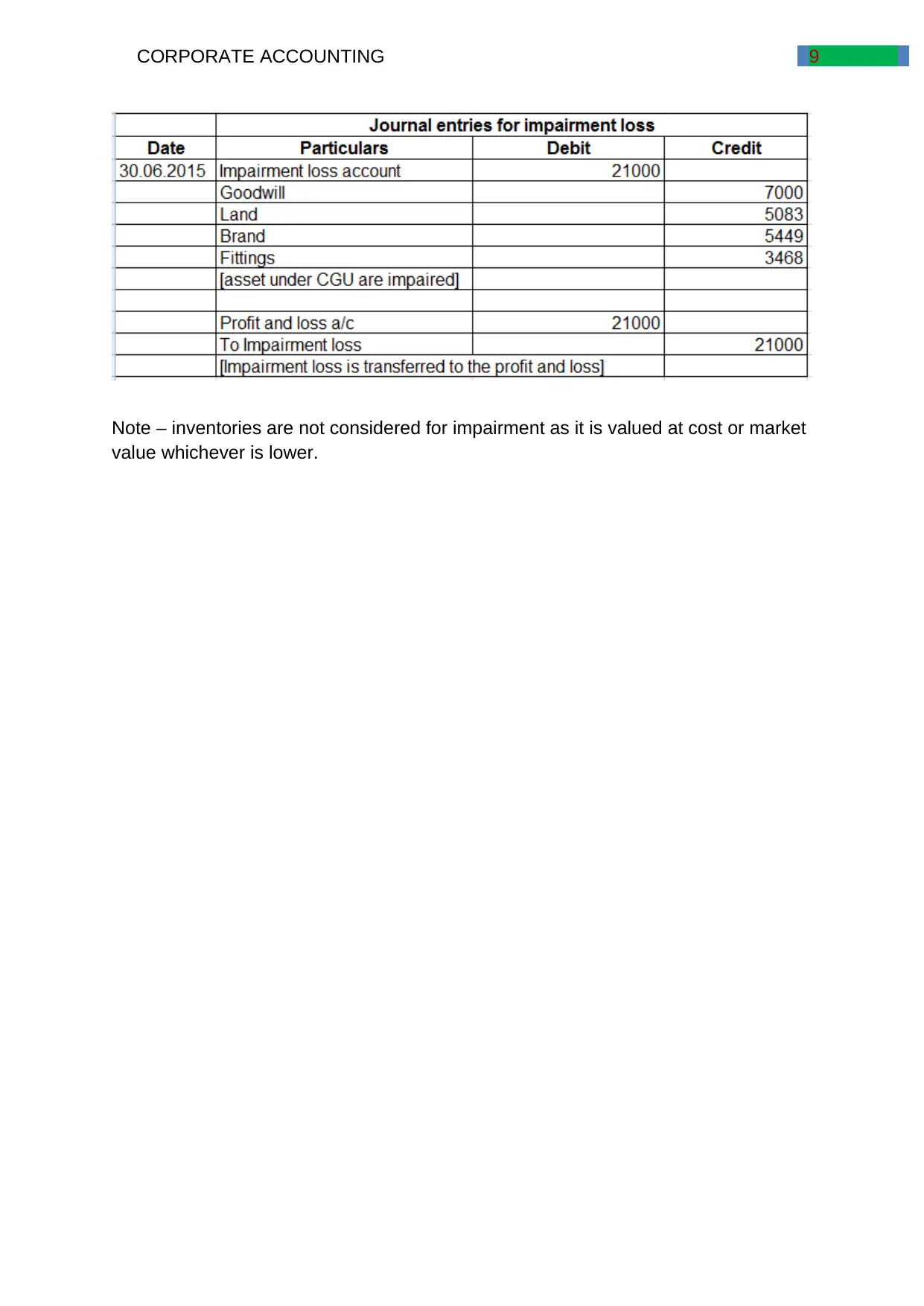

9CORPORATE ACCOUNTING

Note – inventories are not considered for impairment as it is valued at cost or market

value whichever is lower.

Note – inventories are not considered for impairment as it is valued at cost or market

value whichever is lower.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

10CORPORATE ACCOUNTING

Reference

Aasb.gov.au., 2018. [online] Available at:

http://www.aasb.gov.au/admin/file/content105/c9/AASB136_07-04_COMPjun09_01-

10.pdf [Accessed 15 Jun. 2018].

Abbott, M. and Tan‐Kantor, A., 2017. Fair Value Measurement and Mandated

Accounting Changes: The Case of the Victorian Rail Track Corporation. Australian

Accounting Review.

Accounting, H., Part, B. and Plans, D.B., 2015. Notes to the financial statements.

Bond, D., Govendir, B. and Wells, P., 2016. An evaluation of asset impairments by

Australian firms and whether they were impacted by AASB 136. Accounting &

Finance, 56(1), pp.259-288.

Christensen, H.B. and Nikolaev, V.V., 2013. Does fair value accounting for non-

financial assets pass the market test?. Review of Accounting Studies, 18(3), pp.734-

775.

Corgnati, S.P., Fabrizio, E., Filippi, M. and Monetti, V., 2013. Reference buildings for

cost optimal analysis: Method of definition and application. Applied energy, 102,

pp.983-993.

Hull, J. and White, A., 2014. Valuing derivatives: Funding value adjustments and fair

value. Financial Analysts Journal, 70(3), pp.46-56.

Johnson, P.F., 2014. Purchasing and supply management. McGraw-Hill Higher

Education.

Reference

Aasb.gov.au., 2018. [online] Available at:

http://www.aasb.gov.au/admin/file/content105/c9/AASB136_07-04_COMPjun09_01-

10.pdf [Accessed 15 Jun. 2018].

Abbott, M. and Tan‐Kantor, A., 2017. Fair Value Measurement and Mandated

Accounting Changes: The Case of the Victorian Rail Track Corporation. Australian

Accounting Review.

Accounting, H., Part, B. and Plans, D.B., 2015. Notes to the financial statements.

Bond, D., Govendir, B. and Wells, P., 2016. An evaluation of asset impairments by

Australian firms and whether they were impacted by AASB 136. Accounting &

Finance, 56(1), pp.259-288.

Christensen, H.B. and Nikolaev, V.V., 2013. Does fair value accounting for non-

financial assets pass the market test?. Review of Accounting Studies, 18(3), pp.734-

775.

Corgnati, S.P., Fabrizio, E., Filippi, M. and Monetti, V., 2013. Reference buildings for

cost optimal analysis: Method of definition and application. Applied energy, 102,

pp.983-993.

Hull, J. and White, A., 2014. Valuing derivatives: Funding value adjustments and fair

value. Financial Analysts Journal, 70(3), pp.46-56.

Johnson, P.F., 2014. Purchasing and supply management. McGraw-Hill Higher

Education.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

11CORPORATE ACCOUNTING

Kabir, H., Rahman, A.R. and Su, L., 2017. The Association between Goodwill

Impairment Loss and Goodwill Impairment Test-Related Disclosures in Australia.

Rennekamp, K., Rupar, K.K. and Seybert, N., 2014. Impaired judgment: The effects

of asset impairment reversibility and cognitive dissonance on future investment. The

Accounting Review, 90(2), pp.739-759.

Robinson, D.T. and Sensoy, B.A., 2016. Cyclicality, performance measurement, and

cash flow liquidity in private equity. Journal of Financial Economics, 122(3), pp.521-

543.

Singleton-Green, B., 2014. Should financial reporting reflect firms’ business models?

What accounting can learn from the economic theory of the firm. Journal of

Management & Governance, 18(3), pp.697-706.

Vanza, S., Wells, P. and Wright, A., 2018. Do asset impairments and the associated

disclosures resolve uncertainty about future returns and reduce information

asymmetry?. Journal of Contemporary Accounting & Economics, 14(1), pp.22-40.

Zhuang, Z., 2016. Discussion of ‘An evaluation of asset impairments by Australian

firms and whether they were impacted by AASB 136’. Accounting & Finance, 56(1),

pp.289-294.

Kabir, H., Rahman, A.R. and Su, L., 2017. The Association between Goodwill

Impairment Loss and Goodwill Impairment Test-Related Disclosures in Australia.

Rennekamp, K., Rupar, K.K. and Seybert, N., 2014. Impaired judgment: The effects

of asset impairment reversibility and cognitive dissonance on future investment. The

Accounting Review, 90(2), pp.739-759.

Robinson, D.T. and Sensoy, B.A., 2016. Cyclicality, performance measurement, and

cash flow liquidity in private equity. Journal of Financial Economics, 122(3), pp.521-

543.

Singleton-Green, B., 2014. Should financial reporting reflect firms’ business models?

What accounting can learn from the economic theory of the firm. Journal of

Management & Governance, 18(3), pp.697-706.

Vanza, S., Wells, P. and Wright, A., 2018. Do asset impairments and the associated

disclosures resolve uncertainty about future returns and reduce information

asymmetry?. Journal of Contemporary Accounting & Economics, 14(1), pp.22-40.

Zhuang, Z., 2016. Discussion of ‘An evaluation of asset impairments by Australian

firms and whether they were impacted by AASB 136’. Accounting & Finance, 56(1),

pp.289-294.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.