BE130 Financial Reporting: Dynamics Co. Ltd Issues & Solutions

VerifiedAdded on 2023/06/13

|9

|2126

|189

Report

AI Summary

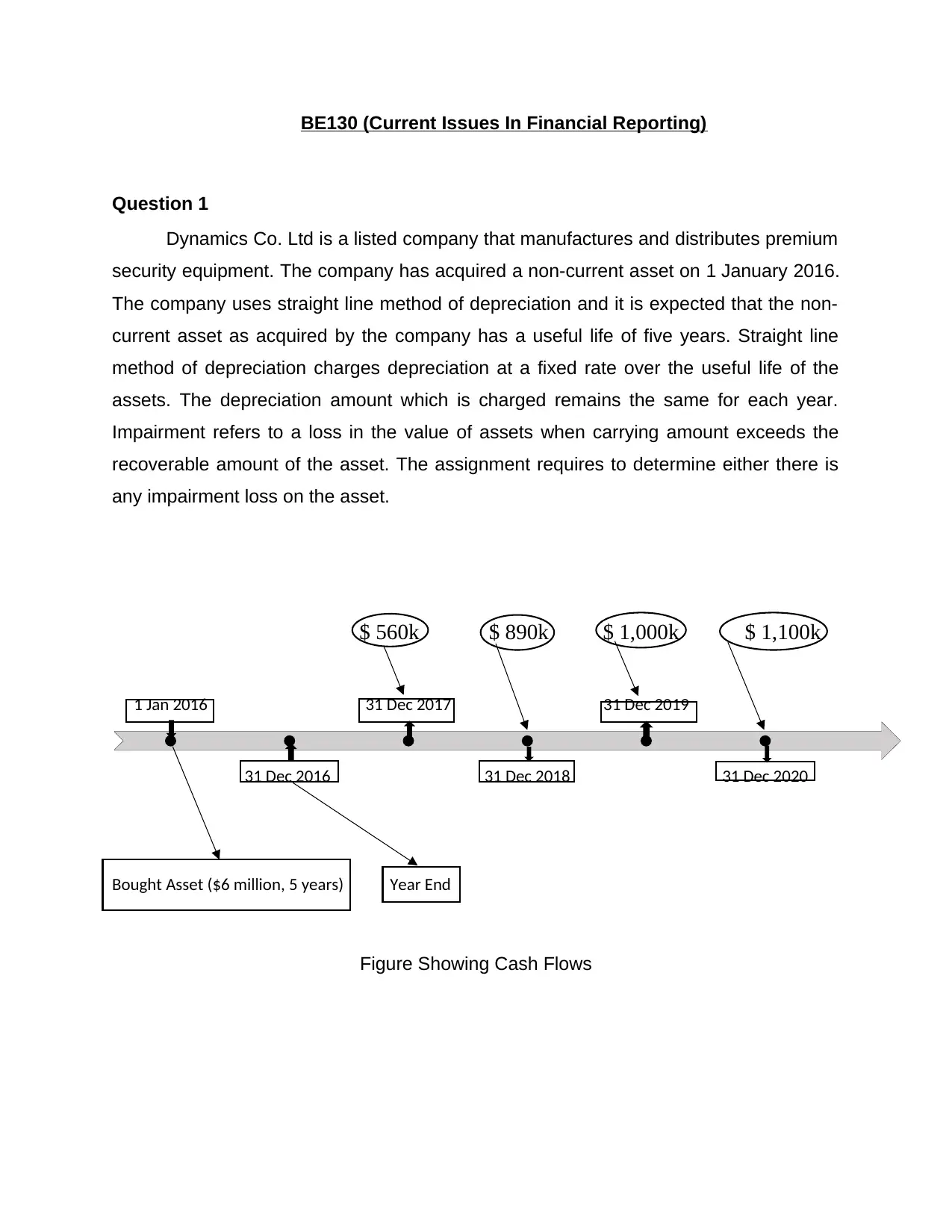

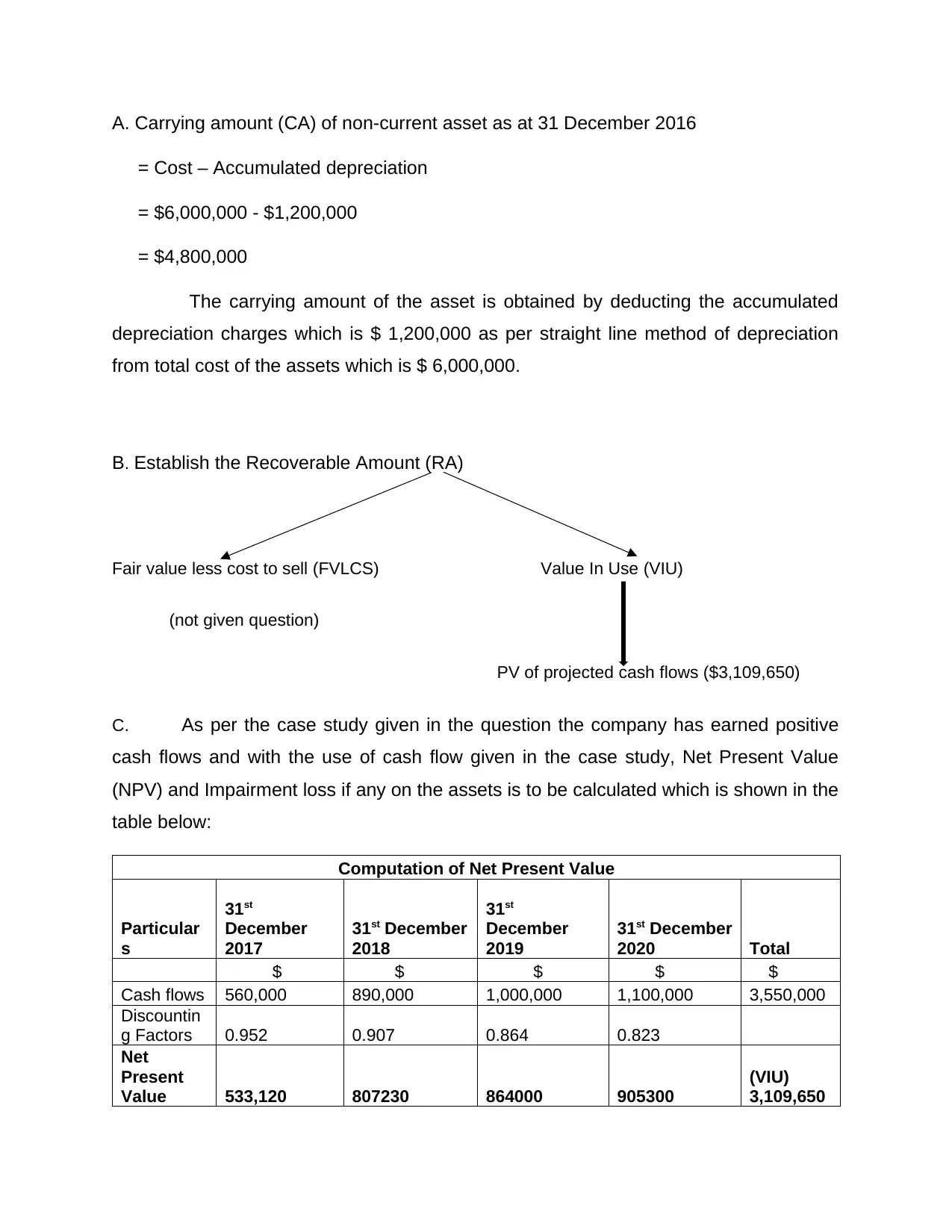

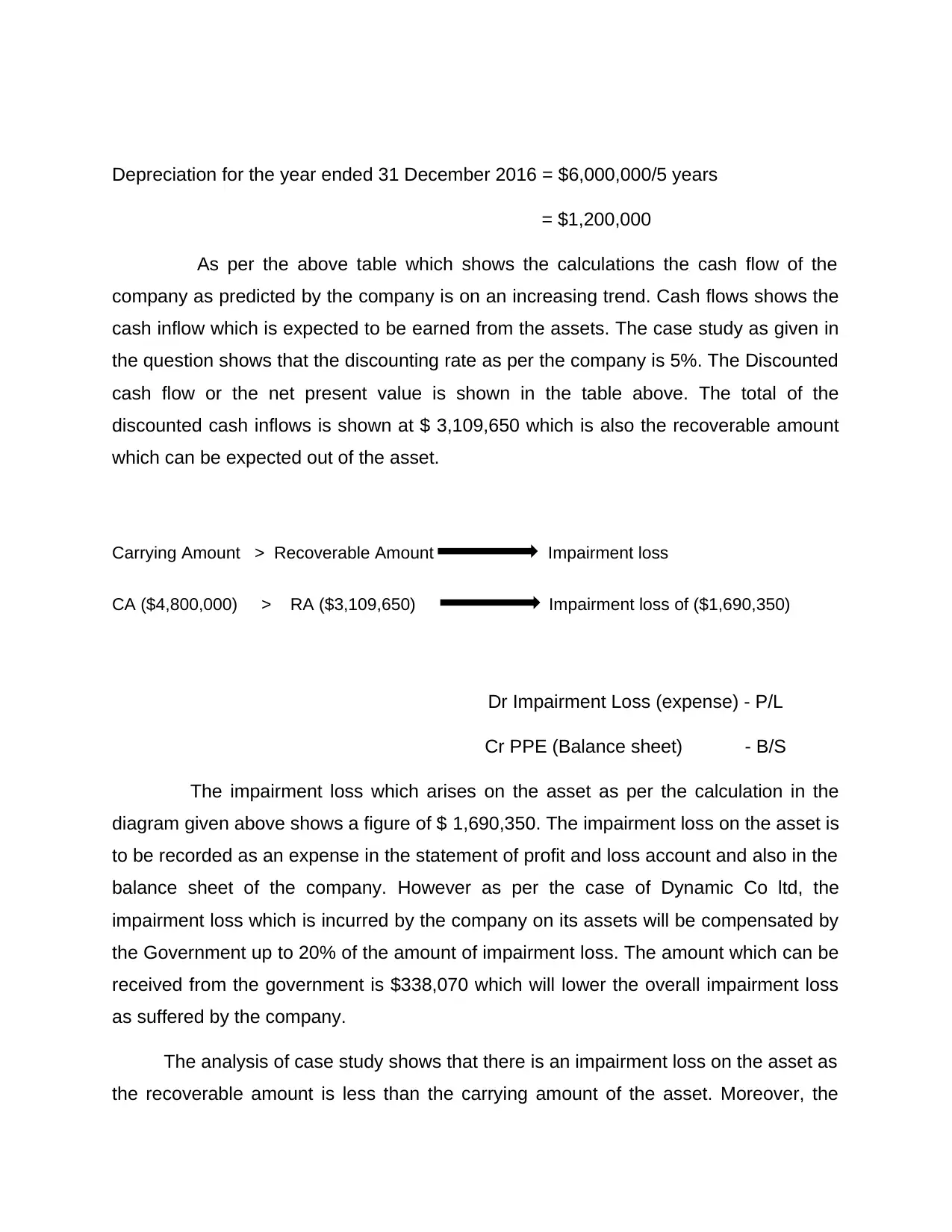

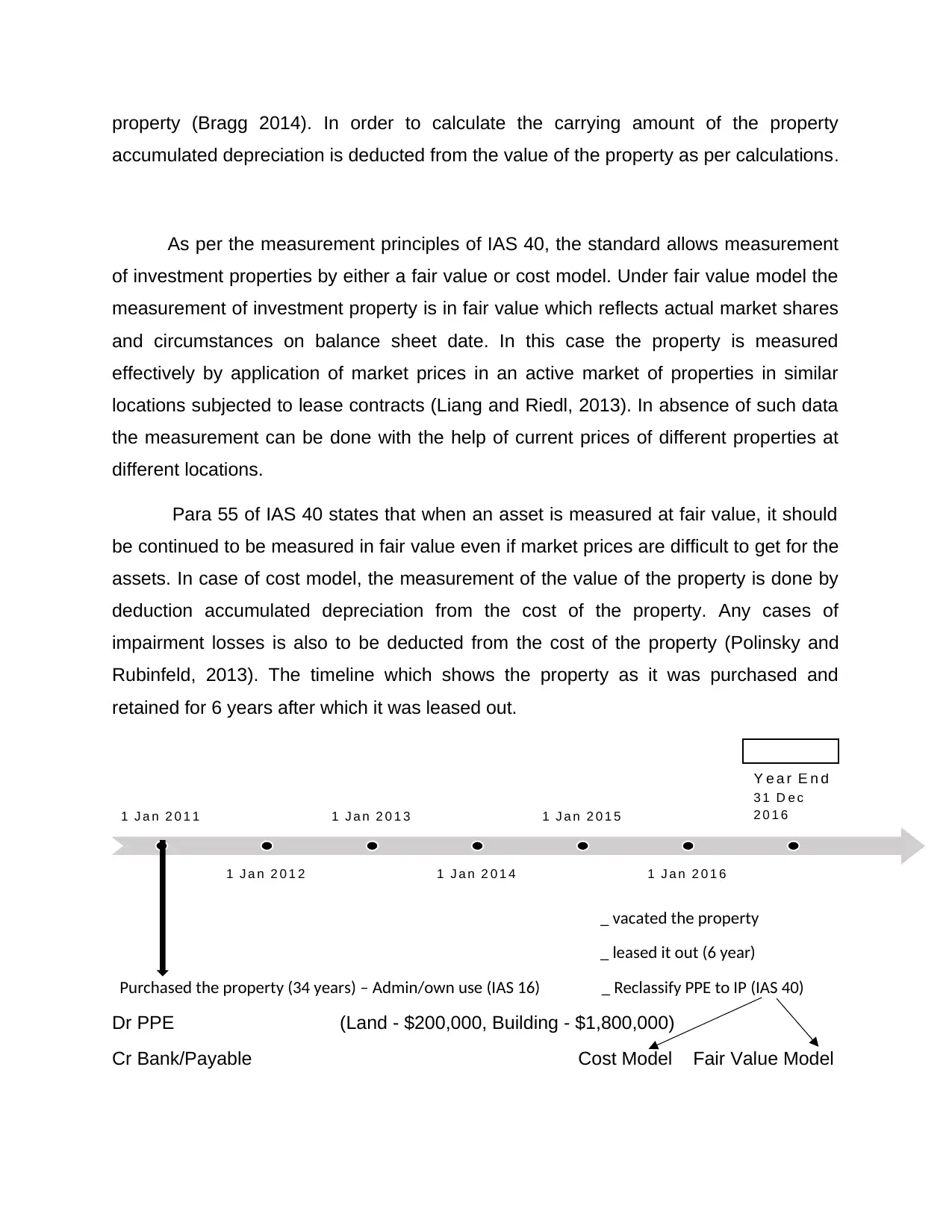

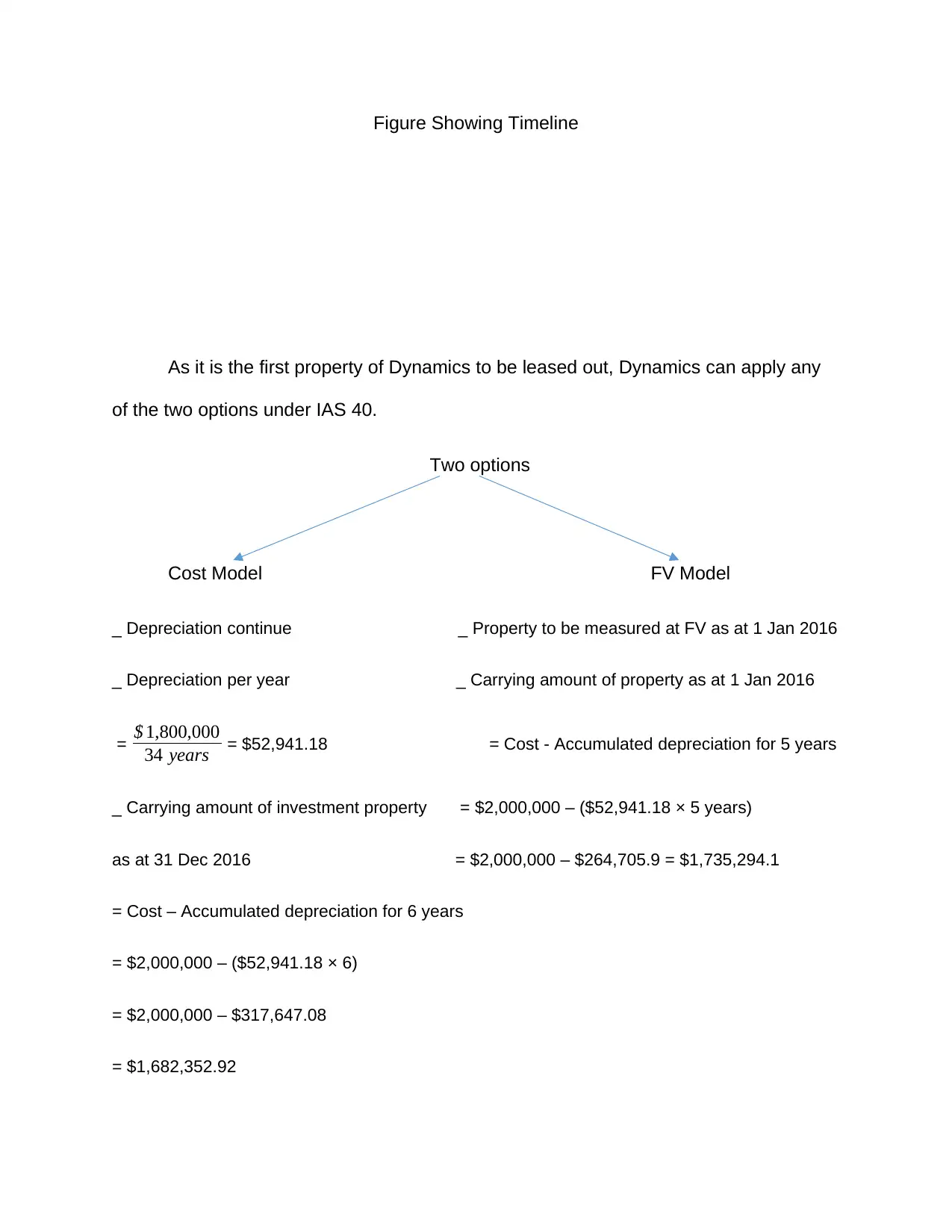

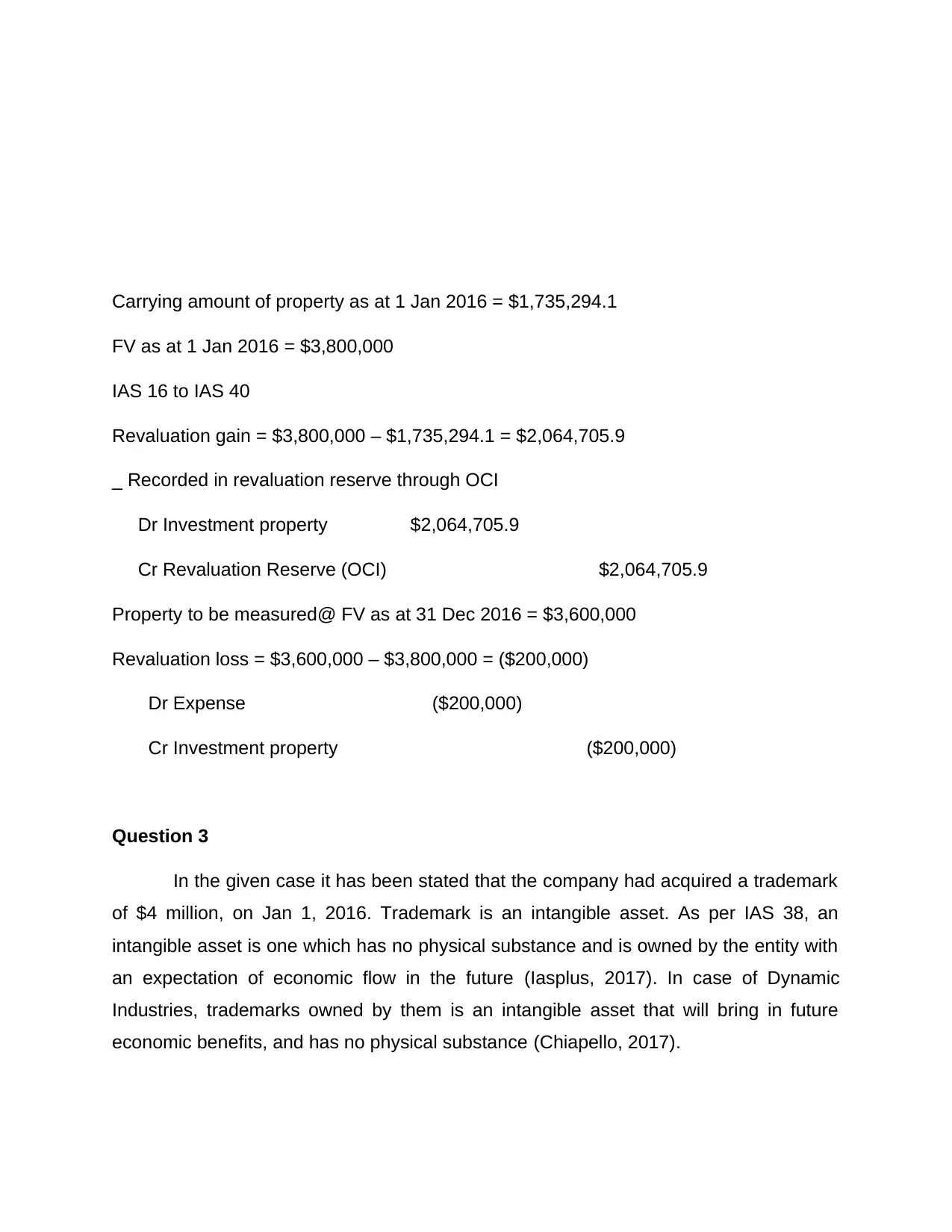

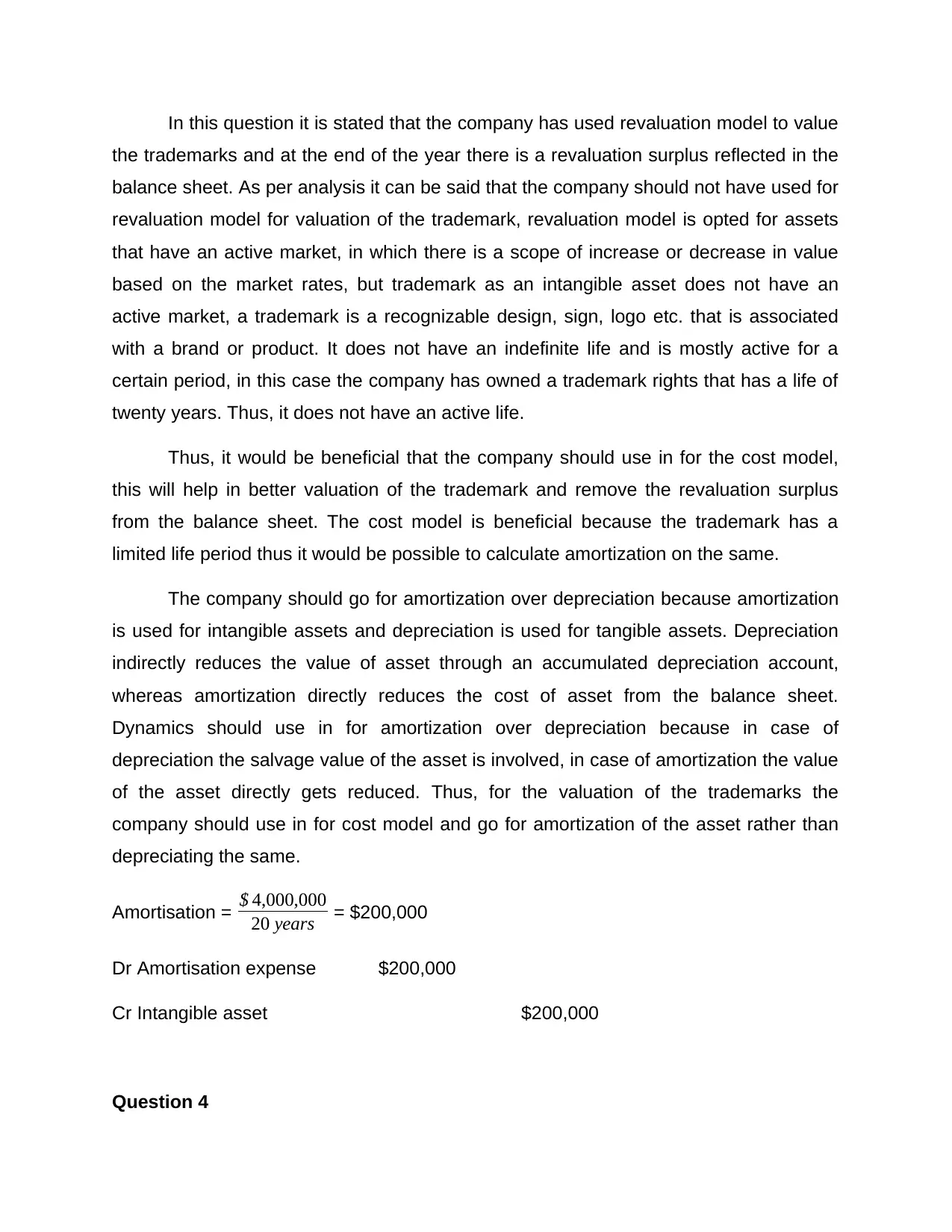

This assignment provides a detailed analysis of Dynamics Co. Ltd's financial reporting practices, covering key issues such as impairment loss calculation, lease accounting treatment, and intangible asset valuation. The first question focuses on determining the impairment loss on a non-current asset, considering cash flows and government compensation. The second question discusses the accounting treatment for a property leased out by Dynamics Limited, evaluating the application of IAS 16 and IAS 40 using both fair value and cost models. The third question addresses the valuation of a trademark, an intangible asset, and suggests using the cost model with amortization instead of the revaluation model. The assignment utilizes calculations and timelines to illustrate the accounting procedures and provides recommendations for improved financial reporting practices. Desklib offers this and other solved assignments to aid students in their studies.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.