Corporate Accounting and Reporting 1 Assignment: Impairment

VerifiedAdded on 2023/06/07

|7

|1417

|176

Homework Assignment

AI Summary

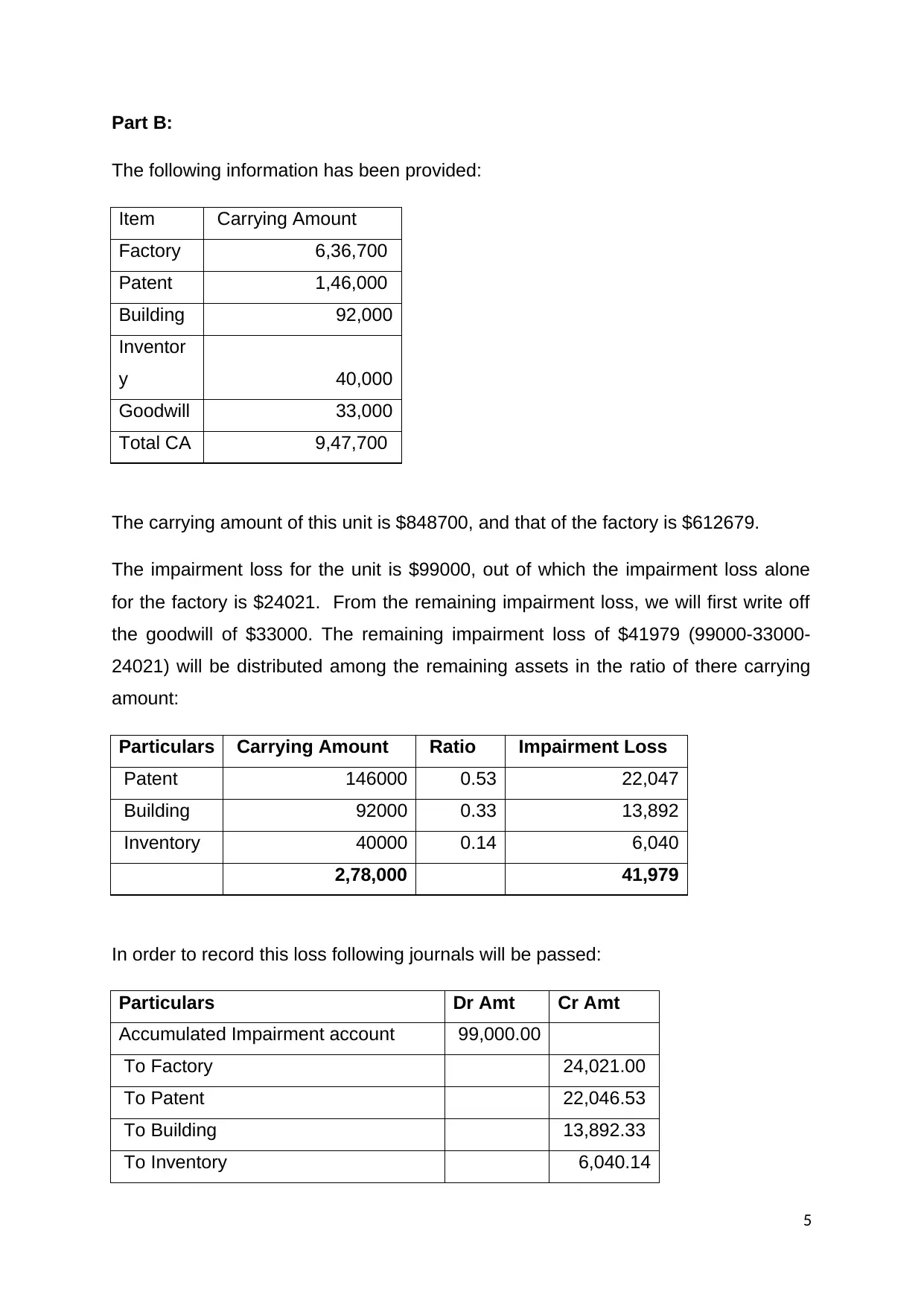

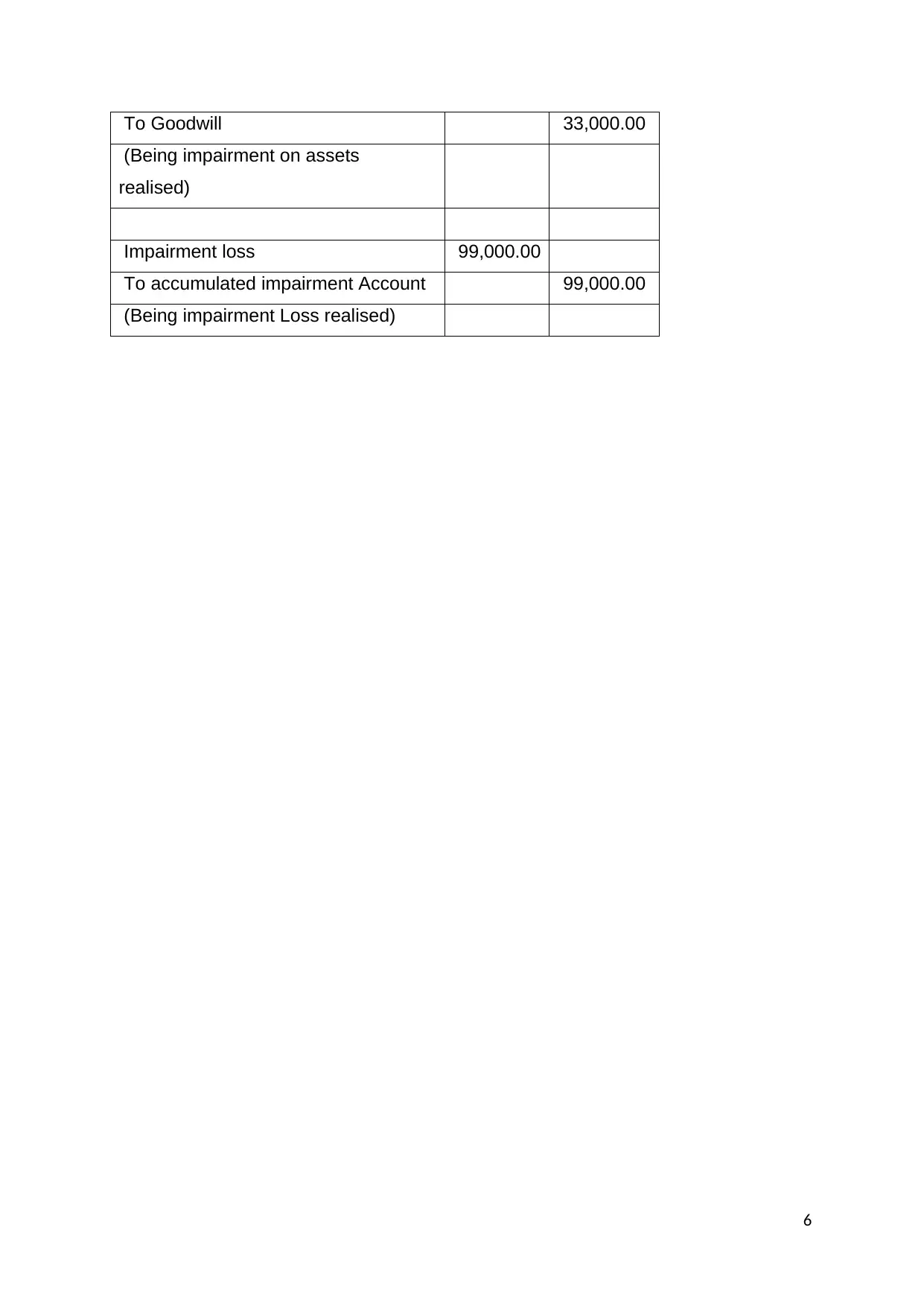

This assignment solution addresses a corporate accounting assignment focusing on asset impairment. Part A provides a detailed explanation of impairment testing, emphasizing the calculation of recoverable amount, fair value less cost of disposal, and value in use. It explains the conditions under which impairment occurs and the accounting treatments required. Part B presents a practical application of the theory, including a case study of Gali Ltd's fine china division, treated as a cash-generating unit (CGU). It includes all the required calculations, such as the determination of the impairment loss for each asset, and the subsequent journal entries to record the impairment loss for the factory, patent, building, inventory and goodwill. The solution references several accounting standards and academic sources to support its analysis.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.