ACCG923 - Wesfarmers Limited: Assessment of AASB 136 Compliance

VerifiedAdded on 2023/06/12

|14

|2488

|359

Report

AI Summary

This report provides a detailed analysis of impairment write-downs in the Australian corporate sector, focusing on Wesfarmers Limited and its compliance with AASB 136. It identifies the major assets tested for impairment, including property, plant, and equipment, trade receivables, goodwill, and int...

Running head: ACCOUNTING STANDARDS AND PRACTICE

Financial Reporting Disclosures in the Australian Corporate Sector

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Financial Reporting Disclosures in the Australian Corporate Sector

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1ACCOUNTING STANDARDS AND PRACTICE

Executive Summary:

In this report, emphasis would be placed on the impairment write-downs in the Australian

corporate sector. For simplification of the report, Wesfarmers Limited is selected as the

organisation, which is the leading retailer of Australia in terms of revenue, size and market share

(Wesfarmers.com.au 2018). The significant issues related to impairment testing include cash

generating units and segments, difference between value-in-use and fair value along with use of

the discount rates. It has been evaluated that Wesfarmers Limited has met all the necessary

disclosures laid out in the objective of general purpose financial reporting and AASB 136.

However, some recommendations have been provided so that the quality of disclosures could be

improved further in future.

Executive Summary:

In this report, emphasis would be placed on the impairment write-downs in the Australian

corporate sector. For simplification of the report, Wesfarmers Limited is selected as the

organisation, which is the leading retailer of Australia in terms of revenue, size and market share

(Wesfarmers.com.au 2018). The significant issues related to impairment testing include cash

generating units and segments, difference between value-in-use and fair value along with use of

the discount rates. It has been evaluated that Wesfarmers Limited has met all the necessary

disclosures laid out in the objective of general purpose financial reporting and AASB 136.

However, some recommendations have been provided so that the quality of disclosures could be

improved further in future.

2ACCOUNTING STANDARDS AND PRACTICE

Table of Contents

Introduction:....................................................................................................................................3

a. Detailed explanation of the impairment write-downs made by Wesfarmers in the year ended

30 June 2017:...................................................................................................................................3

b. Critical analysis of some of the complexities and key issues involved in impairment testing:...4

c. Extent to which the annual report of Wesfarmers meets the disclosure requirements for

impairment as per AASB 136:.........................................................................................................5

d. Alignment of the disclosures on impairment of Wesfarmers with the objective of general

purpose financial reporting and recommended actions for improvement:......................................9

Conclusion:....................................................................................................................................10

References:....................................................................................................................................12

Table of Contents

Introduction:....................................................................................................................................3

a. Detailed explanation of the impairment write-downs made by Wesfarmers in the year ended

30 June 2017:...................................................................................................................................3

b. Critical analysis of some of the complexities and key issues involved in impairment testing:...4

c. Extent to which the annual report of Wesfarmers meets the disclosure requirements for

impairment as per AASB 136:.........................................................................................................5

d. Alignment of the disclosures on impairment of Wesfarmers with the objective of general

purpose financial reporting and recommended actions for improvement:......................................9

Conclusion:....................................................................................................................................10

References:....................................................................................................................................12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3ACCOUNTING STANDARDS AND PRACTICE

Introduction:

In the current era, the quality of financial information that the business organisations

provide to their users of financial statements is of utmost importance for aiding in the decision-

making process of the users. In this report, emphasis would be placed on the impairment write-

downs in the Australian corporate sector. For simplification of the report, Wesfarmers Limited is

selected as the organisation, which is the leading retailer of Australia in terms of revenue, size

and market share (Wesfarmers.com.au 2018). The different assets that the company tests for

impairment are identified and analysed from the critical perspective. The second section would

elaborate on highlighting the significant problems encountered while conducting impairment

testing. The third segment would identify the extent to which the annual report of the

organisation fulfils the impairment disclosure requirements in accordance with AASB 136.

Finally, the report would shed light on aligning such impairment disclosures with the objectives

laid out in general purpose financial reporting.

a. Detailed explanation of the impairment write-downs made by Wesfarmers in the year

ended 30 June 2017:

According to the annual report of Wesfarmers in 2017, it has been identified that the

major assets tested for impairment include property, plant and equipment, trade receivables,

freehold property, goodwill and other intangible assets along with non-financial assets

(Wesfarmers.com.au 2018). For property, plant and equipment, the measurement is carried out at

cost less accumulated depreciation and impairment. In case of trade receivables, impairment is

recognised in the income statement, when evidence is obtained that the organisation would not

be able to recover the debts (Beekes, Brown and Zhang 2015).

Goodwill, which is obtained in a business combination, is gauged initially at cost. After

the initial recognition, the measurement of goodwill is carried out at cost less any losses related

to accumulated impairment. In case of intangible assets, they are obtained separately and their

measurement is made on initial realisation at cost (Bepari, Rahman and Mollik 2014). The cost

of intangible assets, which are obtained in a business combination, is their fair value when they

Introduction:

In the current era, the quality of financial information that the business organisations

provide to their users of financial statements is of utmost importance for aiding in the decision-

making process of the users. In this report, emphasis would be placed on the impairment write-

downs in the Australian corporate sector. For simplification of the report, Wesfarmers Limited is

selected as the organisation, which is the leading retailer of Australia in terms of revenue, size

and market share (Wesfarmers.com.au 2018). The different assets that the company tests for

impairment are identified and analysed from the critical perspective. The second section would

elaborate on highlighting the significant problems encountered while conducting impairment

testing. The third segment would identify the extent to which the annual report of the

organisation fulfils the impairment disclosure requirements in accordance with AASB 136.

Finally, the report would shed light on aligning such impairment disclosures with the objectives

laid out in general purpose financial reporting.

a. Detailed explanation of the impairment write-downs made by Wesfarmers in the year

ended 30 June 2017:

According to the annual report of Wesfarmers in 2017, it has been identified that the

major assets tested for impairment include property, plant and equipment, trade receivables,

freehold property, goodwill and other intangible assets along with non-financial assets

(Wesfarmers.com.au 2018). For property, plant and equipment, the measurement is carried out at

cost less accumulated depreciation and impairment. In case of trade receivables, impairment is

recognised in the income statement, when evidence is obtained that the organisation would not

be able to recover the debts (Beekes, Brown and Zhang 2015).

Goodwill, which is obtained in a business combination, is gauged initially at cost. After

the initial recognition, the measurement of goodwill is carried out at cost less any losses related

to accumulated impairment. In case of intangible assets, they are obtained separately and their

measurement is made on initial realisation at cost (Bepari, Rahman and Mollik 2014). The cost

of intangible assets, which are obtained in a business combination, is their fair value when they

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4ACCOUNTING STANDARDS AND PRACTICE

are acquired. After the initial realisation, the measurement of intangible assets is made at cost

less amortisation and any losses of impairment.

It is necessary for all the business organisations operating in the Australian market to

review their assets for ascertaining whether there are indicators of impairment at the end of every

accounting year and there is no exception to this rule for Wesfarmers Limited as well. The

organisation is involved in impairing its property, plant and equipment and intangible assets due

to the changes in technology or plan of liquidating any particular business operation. In addition,

it is due to the decrease in usefulness of a particular asset and the value of the estimated

economic benefits associated with the intangible assets or property, plant and equipment as well

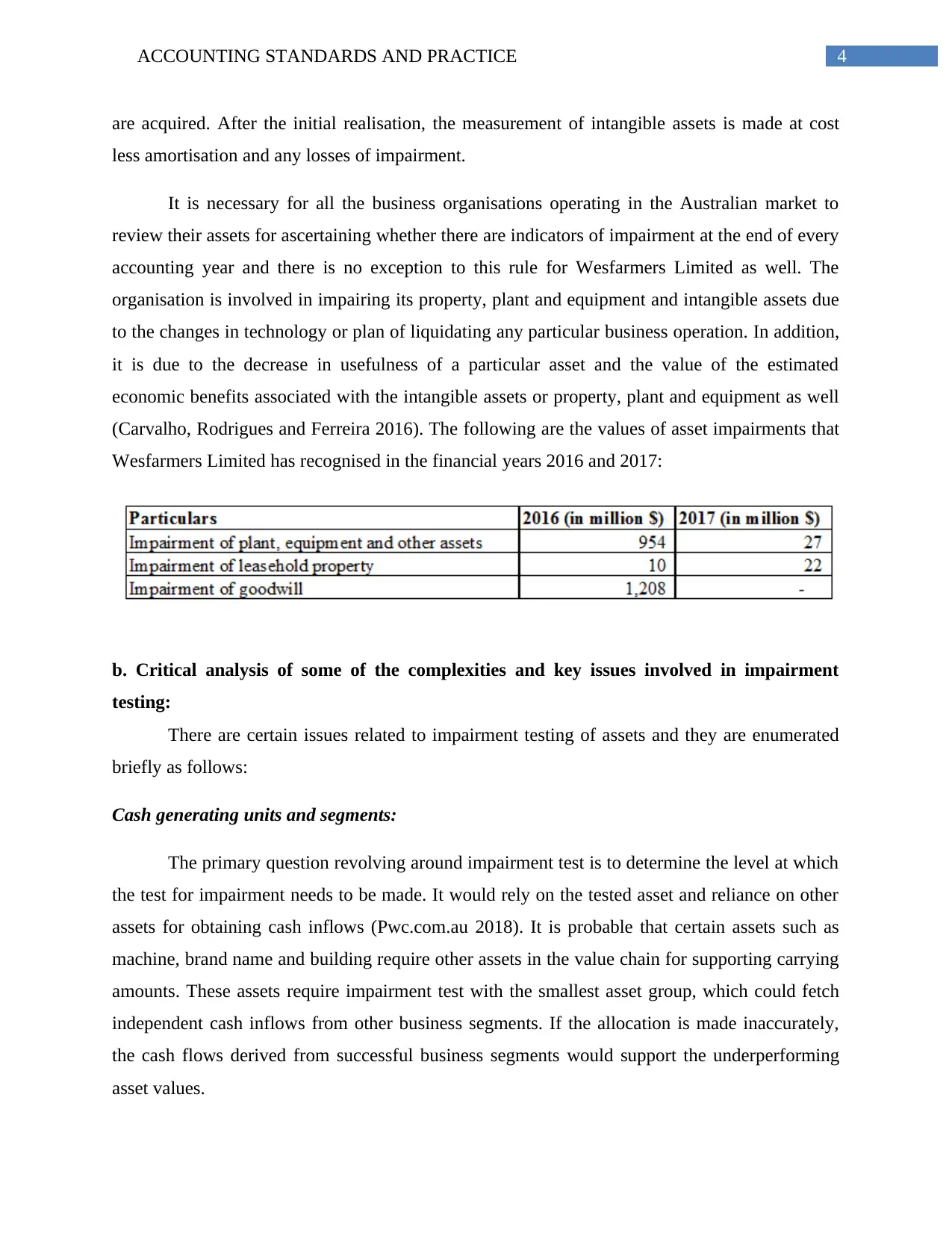

(Carvalho, Rodrigues and Ferreira 2016). The following are the values of asset impairments that

Wesfarmers Limited has recognised in the financial years 2016 and 2017:

b. Critical analysis of some of the complexities and key issues involved in impairment

testing:

There are certain issues related to impairment testing of assets and they are enumerated

briefly as follows:

Cash generating units and segments:

The primary question revolving around impairment test is to determine the level at which

the test for impairment needs to be made. It would rely on the tested asset and reliance on other

assets for obtaining cash inflows (Pwc.com.au 2018). It is probable that certain assets such as

machine, brand name and building require other assets in the value chain for supporting carrying

amounts. These assets require impairment test with the smallest asset group, which could fetch

independent cash inflows from other business segments. If the allocation is made inaccurately,

the cash flows derived from successful business segments would support the underperforming

asset values.

are acquired. After the initial realisation, the measurement of intangible assets is made at cost

less amortisation and any losses of impairment.

It is necessary for all the business organisations operating in the Australian market to

review their assets for ascertaining whether there are indicators of impairment at the end of every

accounting year and there is no exception to this rule for Wesfarmers Limited as well. The

organisation is involved in impairing its property, plant and equipment and intangible assets due

to the changes in technology or plan of liquidating any particular business operation. In addition,

it is due to the decrease in usefulness of a particular asset and the value of the estimated

economic benefits associated with the intangible assets or property, plant and equipment as well

(Carvalho, Rodrigues and Ferreira 2016). The following are the values of asset impairments that

Wesfarmers Limited has recognised in the financial years 2016 and 2017:

b. Critical analysis of some of the complexities and key issues involved in impairment

testing:

There are certain issues related to impairment testing of assets and they are enumerated

briefly as follows:

Cash generating units and segments:

The primary question revolving around impairment test is to determine the level at which

the test for impairment needs to be made. It would rely on the tested asset and reliance on other

assets for obtaining cash inflows (Pwc.com.au 2018). It is probable that certain assets such as

machine, brand name and building require other assets in the value chain for supporting carrying

amounts. These assets require impairment test with the smallest asset group, which could fetch

independent cash inflows from other business segments. If the allocation is made inaccurately,

the cash flows derived from successful business segments would support the underperforming

asset values.

5ACCOUNTING STANDARDS AND PRACTICE

Difference between value-in-use and fair value:

With the help of far value, it is possible to know the amount that an independent investor

would incur for an asset, while value-in-use signifies the internal generating ability of the asset

for the business organisation. Such difference is depicted in the assumptions accepted under each

model (D’Arcy and Tarca 2016). For instance, fair value could take into account the risks, costs

and benefits related to restructuring or asset improvements, which are not included in the balance

sheet statement. On the other hand, value-in-use could comprise of synergies and economies of

scale, which would be specific to the organisation and this would not be transferred at the time of

external sale of the asset. However, this is not the case for fair value.

Using the appropriate discount rate:

It has been observed that various organisations use weighted average cost of capital

(WACC) and CAPM in order to ascertain their rates of discount for the value-in-use purposes

related to impairment testing (Steele 2015). This is validated only; in case, the risks related to

any particular cash generating unit do not vary from the overall business. However, in practice,

varied discount rates are needed for various cash generating units. This is because of the

variations in currency risk, industry risk, product risk, country risk and the market maturity

where the units operate.

c. Extent to which the annual report of Wesfarmers meets the disclosure requirements for

impairment as per AASB 136:

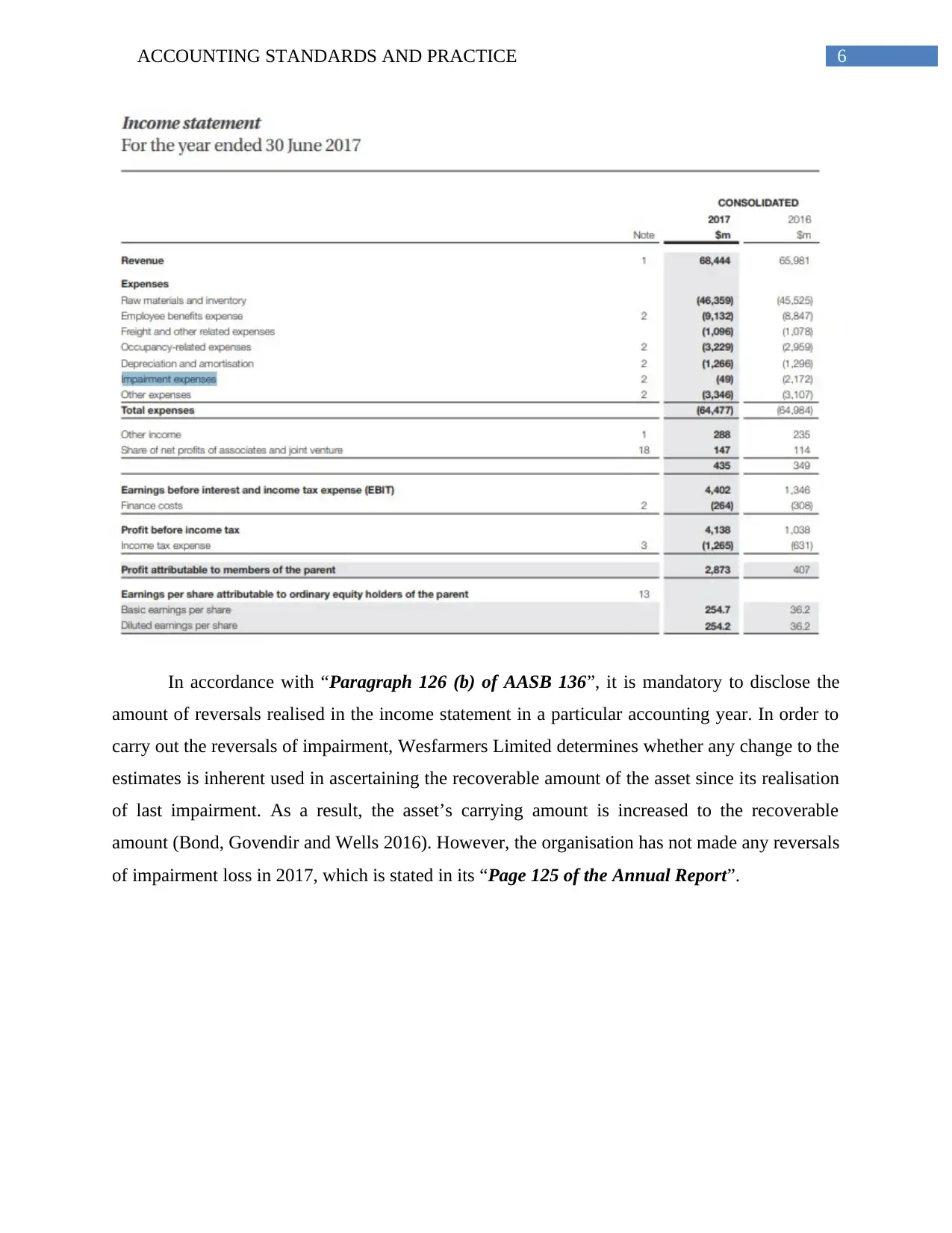

According to “Paragraph 126 (a) of AASB 136”, it is necessary for the business

organisations to realise impairment loss in the income statement (Aasb.gov.au 2018). In case of

Wesfarmers Limited, it could be observed that it has disclosed its amount of impairment loss in

the income statement laid out in “Page 94 of the Annual Report”.

Difference between value-in-use and fair value:

With the help of far value, it is possible to know the amount that an independent investor

would incur for an asset, while value-in-use signifies the internal generating ability of the asset

for the business organisation. Such difference is depicted in the assumptions accepted under each

model (D’Arcy and Tarca 2016). For instance, fair value could take into account the risks, costs

and benefits related to restructuring or asset improvements, which are not included in the balance

sheet statement. On the other hand, value-in-use could comprise of synergies and economies of

scale, which would be specific to the organisation and this would not be transferred at the time of

external sale of the asset. However, this is not the case for fair value.

Using the appropriate discount rate:

It has been observed that various organisations use weighted average cost of capital

(WACC) and CAPM in order to ascertain their rates of discount for the value-in-use purposes

related to impairment testing (Steele 2015). This is validated only; in case, the risks related to

any particular cash generating unit do not vary from the overall business. However, in practice,

varied discount rates are needed for various cash generating units. This is because of the

variations in currency risk, industry risk, product risk, country risk and the market maturity

where the units operate.

c. Extent to which the annual report of Wesfarmers meets the disclosure requirements for

impairment as per AASB 136:

According to “Paragraph 126 (a) of AASB 136”, it is necessary for the business

organisations to realise impairment loss in the income statement (Aasb.gov.au 2018). In case of

Wesfarmers Limited, it could be observed that it has disclosed its amount of impairment loss in

the income statement laid out in “Page 94 of the Annual Report”.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6ACCOUNTING STANDARDS AND PRACTICE

In accordance with “Paragraph 126 (b) of AASB 136”, it is mandatory to disclose the

amount of reversals realised in the income statement in a particular accounting year. In order to

carry out the reversals of impairment, Wesfarmers Limited determines whether any change to the

estimates is inherent used in ascertaining the recoverable amount of the asset since its realisation

of last impairment. As a result, the asset’s carrying amount is increased to the recoverable

amount (Bond, Govendir and Wells 2016). However, the organisation has not made any reversals

of impairment loss in 2017, which is stated in its “Page 125 of the Annual Report”.

In accordance with “Paragraph 126 (b) of AASB 136”, it is mandatory to disclose the

amount of reversals realised in the income statement in a particular accounting year. In order to

carry out the reversals of impairment, Wesfarmers Limited determines whether any change to the

estimates is inherent used in ascertaining the recoverable amount of the asset since its realisation

of last impairment. As a result, the asset’s carrying amount is increased to the recoverable

amount (Bond, Govendir and Wells 2016). However, the organisation has not made any reversals

of impairment loss in 2017, which is stated in its “Page 125 of the Annual Report”.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7ACCOUNTING STANDARDS AND PRACTICE

In addition, according to “Paragraph 130 (g) of AASB 136”, if the recoverable amount

of any CGU is found in the form of value-in-use, the discount rates are used in the current

estimate and past estimate, if any, related to value-in-use. In case of Wesfarmers Limited, key

assumptions are made for determining the recoverable amounts of the different CGUs of the

organisation, which could be observed from “Page 126 of the Annual Report”.

In addition, according to “Paragraph 130 (g) of AASB 136”, if the recoverable amount

of any CGU is found in the form of value-in-use, the discount rates are used in the current

estimate and past estimate, if any, related to value-in-use. In case of Wesfarmers Limited, key

assumptions are made for determining the recoverable amounts of the different CGUs of the

organisation, which could be observed from “Page 126 of the Annual Report”.

8ACCOUNTING STANDARDS AND PRACTICE

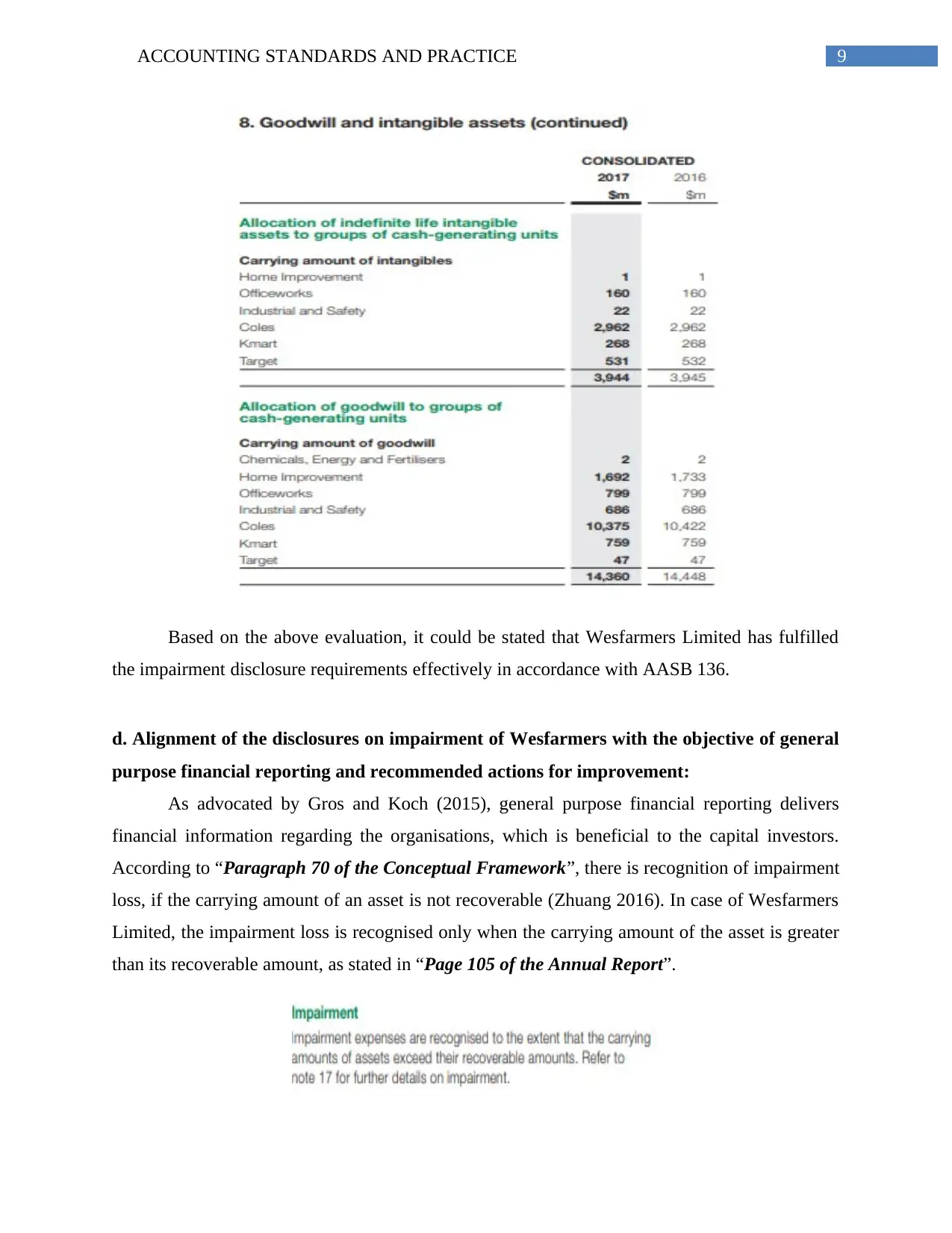

Finally, “Paragraph 80 of AASB 136” cites that goodwill needs to be allocated to a class

of cash generating units estimated to benefit from the combination synergies (Detzen, Stork

Genannt Wersborg and Zülch 2016). Wesfarmers Limited has allocated goodwill to groups of

cash generating units for the same purpose, which could be identified from “Page 111 of the

Annual Report”.

Finally, “Paragraph 80 of AASB 136” cites that goodwill needs to be allocated to a class

of cash generating units estimated to benefit from the combination synergies (Detzen, Stork

Genannt Wersborg and Zülch 2016). Wesfarmers Limited has allocated goodwill to groups of

cash generating units for the same purpose, which could be identified from “Page 111 of the

Annual Report”.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9ACCOUNTING STANDARDS AND PRACTICE

Based on the above evaluation, it could be stated that Wesfarmers Limited has fulfilled

the impairment disclosure requirements effectively in accordance with AASB 136.

d. Alignment of the disclosures on impairment of Wesfarmers with the objective of general

purpose financial reporting and recommended actions for improvement:

As advocated by Gros and Koch (2015), general purpose financial reporting delivers

financial information regarding the organisations, which is beneficial to the capital investors.

According to “Paragraph 70 of the Conceptual Framework”, there is recognition of impairment

loss, if the carrying amount of an asset is not recoverable (Zhuang 2016). In case of Wesfarmers

Limited, the impairment loss is recognised only when the carrying amount of the asset is greater

than its recoverable amount, as stated in “Page 105 of the Annual Report”.

Based on the above evaluation, it could be stated that Wesfarmers Limited has fulfilled

the impairment disclosure requirements effectively in accordance with AASB 136.

d. Alignment of the disclosures on impairment of Wesfarmers with the objective of general

purpose financial reporting and recommended actions for improvement:

As advocated by Gros and Koch (2015), general purpose financial reporting delivers

financial information regarding the organisations, which is beneficial to the capital investors.

According to “Paragraph 70 of the Conceptual Framework”, there is recognition of impairment

loss, if the carrying amount of an asset is not recoverable (Zhuang 2016). In case of Wesfarmers

Limited, the impairment loss is recognised only when the carrying amount of the asset is greater

than its recoverable amount, as stated in “Page 105 of the Annual Report”.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10ACCOUNTING STANDARDS AND PRACTICE

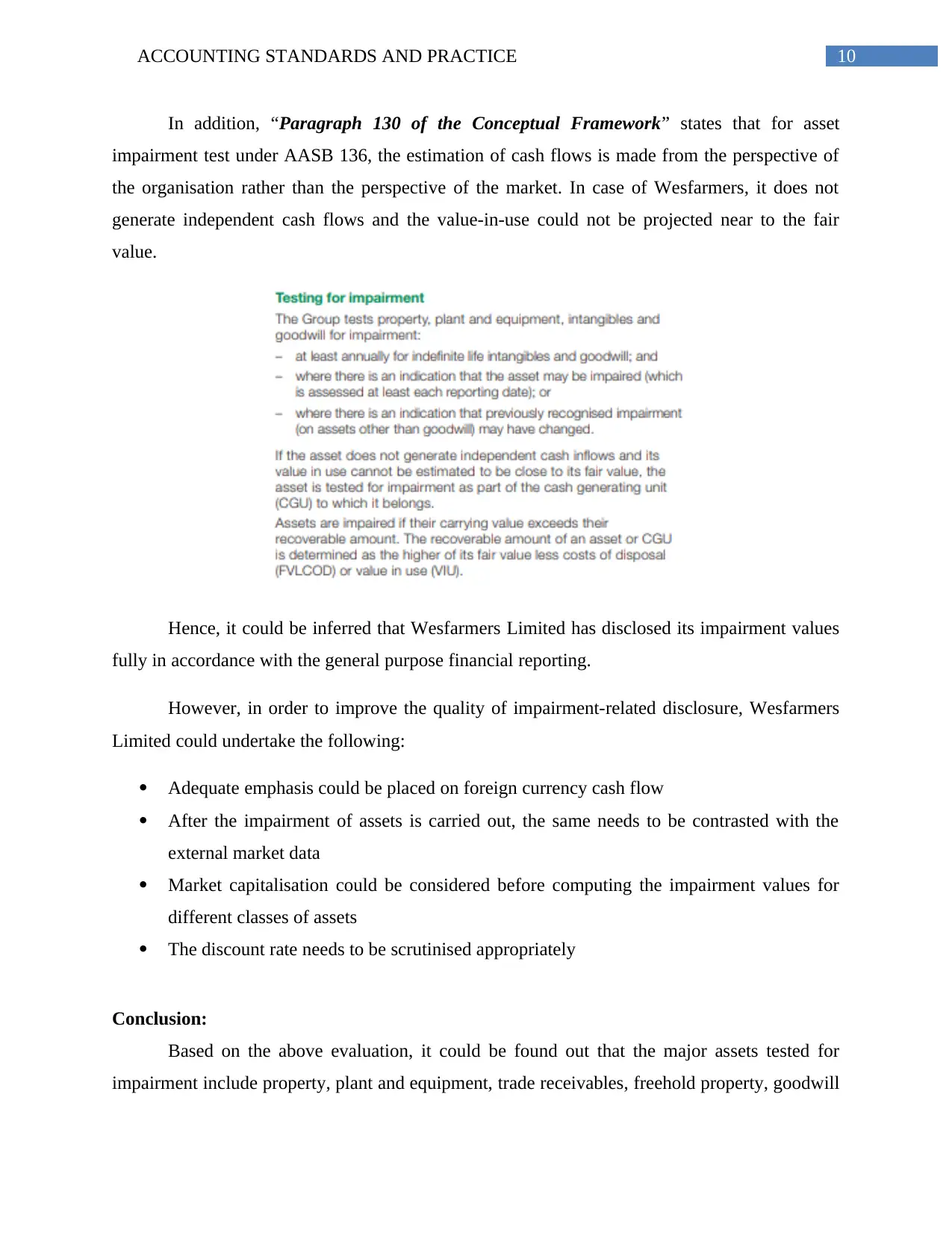

In addition, “Paragraph 130 of the Conceptual Framework” states that for asset

impairment test under AASB 136, the estimation of cash flows is made from the perspective of

the organisation rather than the perspective of the market. In case of Wesfarmers, it does not

generate independent cash flows and the value-in-use could not be projected near to the fair

value.

Hence, it could be inferred that Wesfarmers Limited has disclosed its impairment values

fully in accordance with the general purpose financial reporting.

However, in order to improve the quality of impairment-related disclosure, Wesfarmers

Limited could undertake the following:

Adequate emphasis could be placed on foreign currency cash flow

After the impairment of assets is carried out, the same needs to be contrasted with the

external market data

Market capitalisation could be considered before computing the impairment values for

different classes of assets

The discount rate needs to be scrutinised appropriately

Conclusion:

Based on the above evaluation, it could be found out that the major assets tested for

impairment include property, plant and equipment, trade receivables, freehold property, goodwill

In addition, “Paragraph 130 of the Conceptual Framework” states that for asset

impairment test under AASB 136, the estimation of cash flows is made from the perspective of

the organisation rather than the perspective of the market. In case of Wesfarmers, it does not

generate independent cash flows and the value-in-use could not be projected near to the fair

value.

Hence, it could be inferred that Wesfarmers Limited has disclosed its impairment values

fully in accordance with the general purpose financial reporting.

However, in order to improve the quality of impairment-related disclosure, Wesfarmers

Limited could undertake the following:

Adequate emphasis could be placed on foreign currency cash flow

After the impairment of assets is carried out, the same needs to be contrasted with the

external market data

Market capitalisation could be considered before computing the impairment values for

different classes of assets

The discount rate needs to be scrutinised appropriately

Conclusion:

Based on the above evaluation, it could be found out that the major assets tested for

impairment include property, plant and equipment, trade receivables, freehold property, goodwill

11ACCOUNTING STANDARDS AND PRACTICE

and other intangible assets along with non-financial assets. The issues associated with

impairment testing have been described in this paper as well. Finally, it has been evaluated that

Wesfarmers Limited has met all the necessary disclosures laid out in the objective of general

purpose financial reporting and AASB 136. However, some recommendations have been

provided so that the quality of disclosures could be improved further in future.

and other intangible assets along with non-financial assets. The issues associated with

impairment testing have been described in this paper as well. Finally, it has been evaluated that

Wesfarmers Limited has met all the necessary disclosures laid out in the objective of general

purpose financial reporting and AASB 136. However, some recommendations have been

provided so that the quality of disclosures could be improved further in future.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

12ACCOUNTING STANDARDS AND PRACTICE

References:

Aasb.gov.au., 2018. [online] Available at:

http://www.aasb.gov.au/admin/file/content102/c3/AASB136_07-04_ERDRjun10_07-09.pdf

[Accessed 23 Apr. 2018].

Beekes, W., Brown, P. and Zhang, Q., 2015. Corporate governance and the informativeness of

disclosures in Australia: A re‐examination. Accounting & Finance, 55(4), pp.931-963.

Bepari, M.K., Rahman, S.F. and Mollik, A.T., 2014. Firms' compliance with the disclosure

requirements of IFRS for goodwill impairment testing: Effect of the global financial crisis and

other firm characteristics. Journal of Accounting and Organizational Change, 10(1), pp.116-149.

Bond, D., Govendir, B. and Wells, P., 2016. An evaluation of asset impairments by Australian

firms and whether they were impacted by AASB 136. Accounting & Finance, 56(1), pp.259-288.

Carvalho, C., Rodrigues, A.M. and Ferreira, C., 2016. Goodwill and Mandatory Disclosure

Compliance: A Critical Review of the Literature. Australian Accounting Review, 26(4), pp.376-

389.

D’Arcy, A. and Tarca, A., 2016. Reviewing goodwill accounting research: What do we really

know about IFRS 3 and IAS 36 implementation effects. Working paper.

Detzen, D., Stork Genannt Wersborg, T. and Zülch, H., 2016. Impairment of Goodwill and

Deferred Taxes Under IFRS. Australian Accounting Review, 26(3), pp.301-311.

Gros, M. and Koch, S., 2015. Goodwill Impairment Test Disclosures Under IAS 36: Disclosure

Quality and its Determinants in Europe.

Pwc.com.au., 2018. [online] Available at:

https://www.pwc.com.au/assurance/ifrs/assets/ifrsinbrief-se-15may13.pdf [Accessed 23 Apr.

2018].

Steele, N., 2015. Accounting: Get the numbers right. Company Director, 31(5), p.41.

References:

Aasb.gov.au., 2018. [online] Available at:

http://www.aasb.gov.au/admin/file/content102/c3/AASB136_07-04_ERDRjun10_07-09.pdf

[Accessed 23 Apr. 2018].

Beekes, W., Brown, P. and Zhang, Q., 2015. Corporate governance and the informativeness of

disclosures in Australia: A re‐examination. Accounting & Finance, 55(4), pp.931-963.

Bepari, M.K., Rahman, S.F. and Mollik, A.T., 2014. Firms' compliance with the disclosure

requirements of IFRS for goodwill impairment testing: Effect of the global financial crisis and

other firm characteristics. Journal of Accounting and Organizational Change, 10(1), pp.116-149.

Bond, D., Govendir, B. and Wells, P., 2016. An evaluation of asset impairments by Australian

firms and whether they were impacted by AASB 136. Accounting & Finance, 56(1), pp.259-288.

Carvalho, C., Rodrigues, A.M. and Ferreira, C., 2016. Goodwill and Mandatory Disclosure

Compliance: A Critical Review of the Literature. Australian Accounting Review, 26(4), pp.376-

389.

D’Arcy, A. and Tarca, A., 2016. Reviewing goodwill accounting research: What do we really

know about IFRS 3 and IAS 36 implementation effects. Working paper.

Detzen, D., Stork Genannt Wersborg, T. and Zülch, H., 2016. Impairment of Goodwill and

Deferred Taxes Under IFRS. Australian Accounting Review, 26(3), pp.301-311.

Gros, M. and Koch, S., 2015. Goodwill Impairment Test Disclosures Under IAS 36: Disclosure

Quality and its Determinants in Europe.

Pwc.com.au., 2018. [online] Available at:

https://www.pwc.com.au/assurance/ifrs/assets/ifrsinbrief-se-15may13.pdf [Accessed 23 Apr.

2018].

Steele, N., 2015. Accounting: Get the numbers right. Company Director, 31(5), p.41.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

13ACCOUNTING STANDARDS AND PRACTICE

Wesfarmers.com.au., 2018. [online] Available at: https://www.wesfarmers.com.au/docs/default-

source/default-document-library/2017-annual-report.pdf?sfvrsn=0 [Accessed 23 Apr. 2018].

Zhuang, Z., 2016. Discussion of ‘An evaluation of asset impairments by Australian firms and

whether they were impacted by AASB 136’. Accounting & Finance, 56(1), pp.289-294.

Wesfarmers.com.au., 2018. [online] Available at: https://www.wesfarmers.com.au/docs/default-

source/default-document-library/2017-annual-report.pdf?sfvrsn=0 [Accessed 23 Apr. 2018].

Zhuang, Z., 2016. Discussion of ‘An evaluation of asset impairments by Australian firms and

whether they were impacted by AASB 136’. Accounting & Finance, 56(1), pp.289-294.

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.