Case Study: Financial Planning Analysis for Megan and Kevin Lee, 2001

VerifiedAdded on 2021/06/17

|8

|1305

|50

Homework Assignment

AI Summary

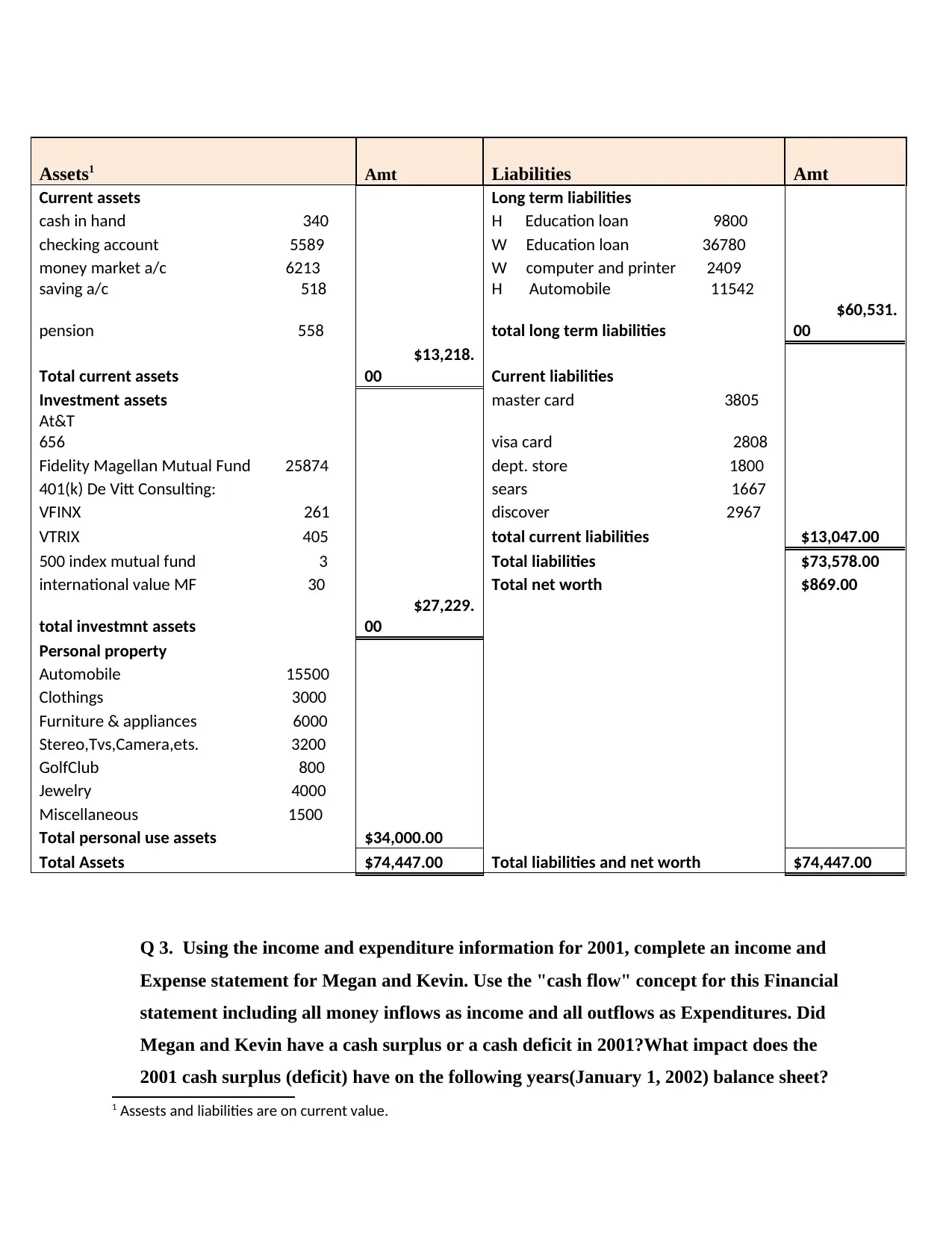

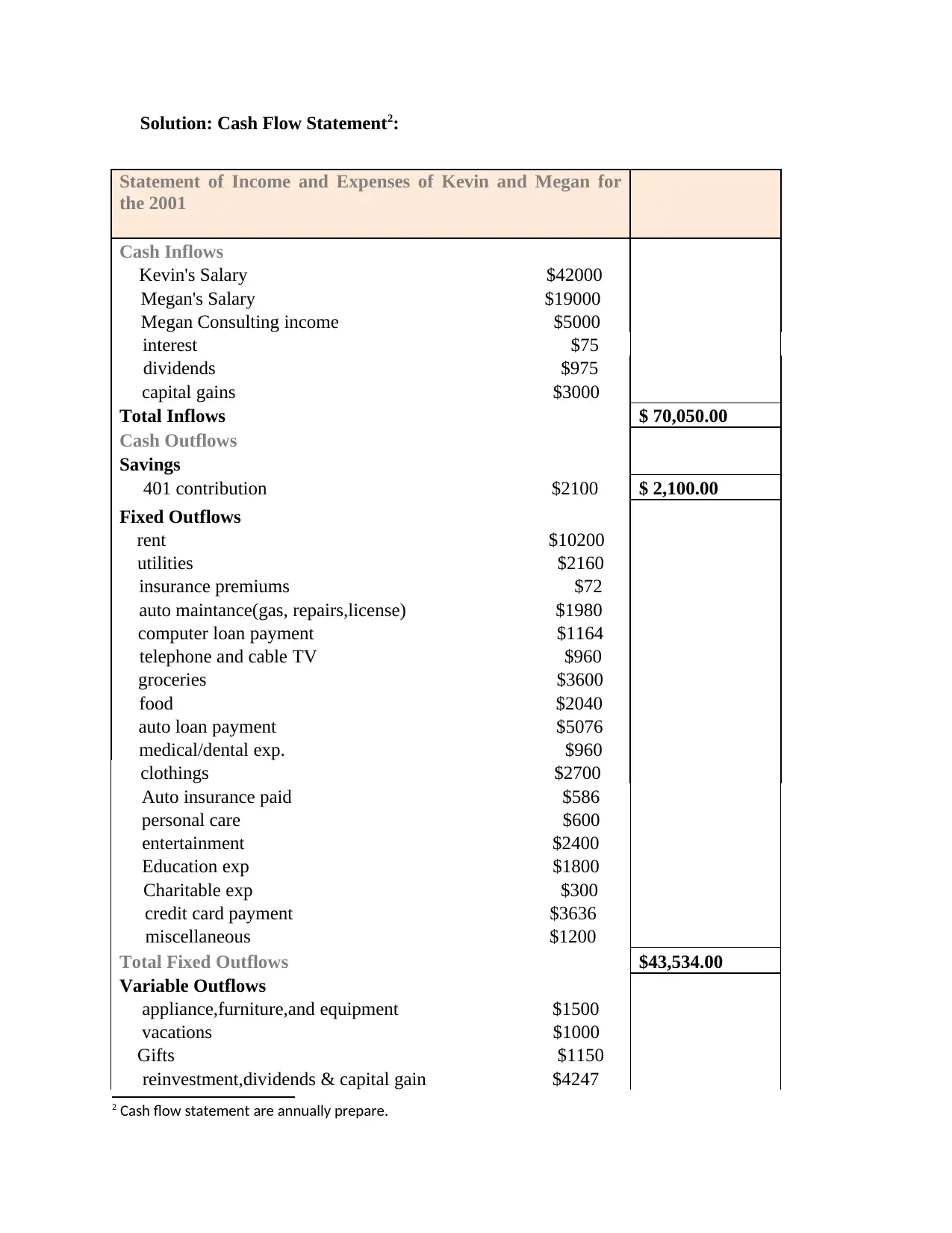

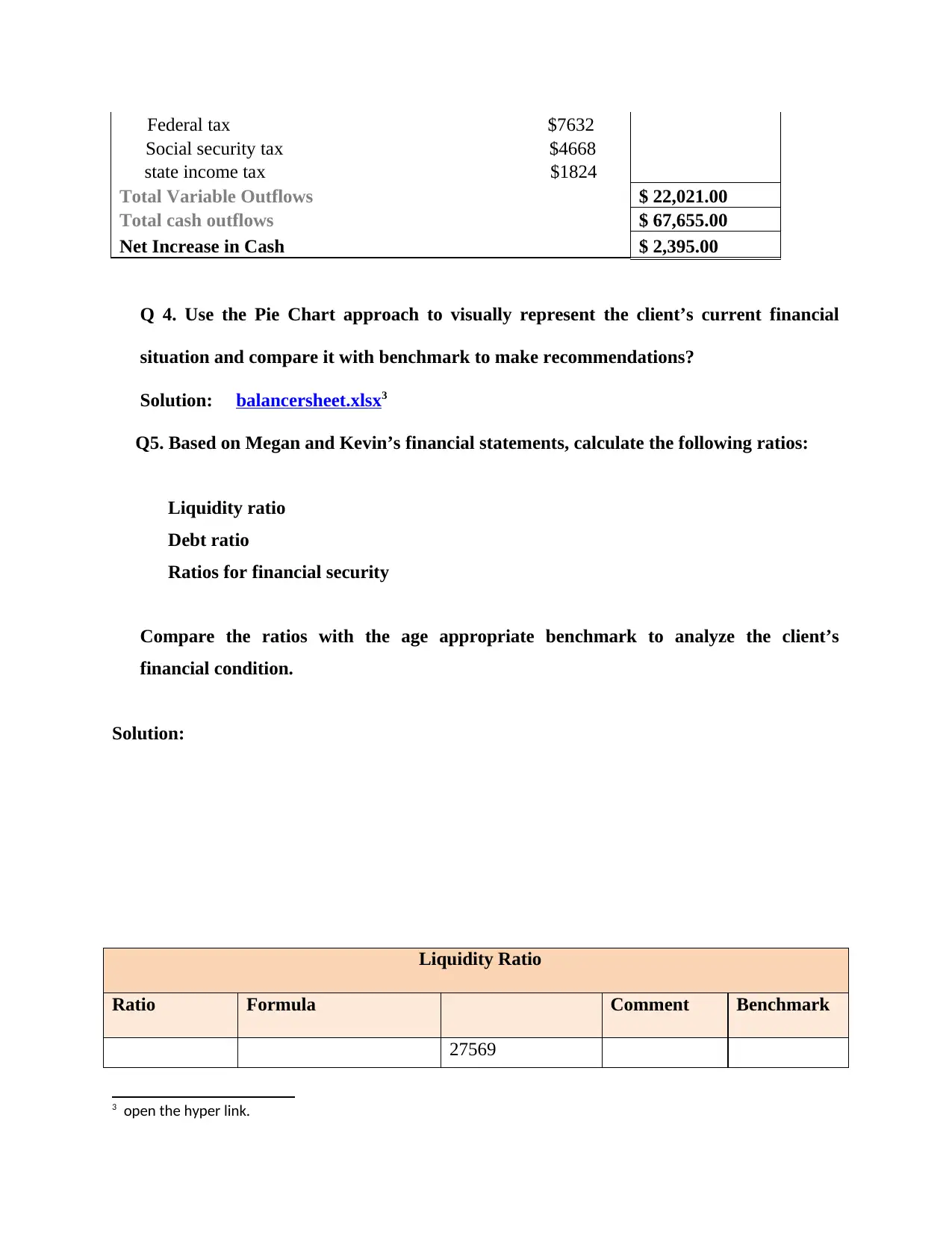

This assignment presents a financial planning analysis case study focusing on Megan and Kevin Lee, a married couple in 2001. The analysis begins with an introduction to financial planning, followed by questions addressing their life cycle phase, development of a balance sheet, and creation of an income and expense statement. The assignment requires calculating and interpreting various financial ratios like liquidity and debt ratios, comparing them with benchmarks to assess their financial condition. It also involves using a two-step/three-panel approach to analyze their financial independence and risk profile, offering recommendations for risk management, debt management, and savings and investment strategies. The solution includes detailed calculations, ratio analysis, and recommendations for improving their financial well-being, including suggestions for life insurance, health insurance, disability insurance, and retirement planning. The analysis incorporates a cash flow statement and pie chart representation to visually depict their financial situation and compare it with benchmarks. Finally, the assignment emphasizes the importance of savings, investment, and overall financial security, referencing various financial planning approaches and benchmarks.

1 out of 8

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.