Accounting Report: Leadership, Cost, Budgeting, and Financial Analysis

VerifiedAdded on 2020/11/23

|13

|1892

|446

Report

AI Summary

This accounting report provides a comprehensive analysis of several key areas within the field. It begins with an examination of leadership in the modern business environment, discussing the impact of technological advancements, the importance of competent leadership, and the essential qualities for success. The report then delves into cost analysis, including the measurement of variable costs, contribution margins, and break-even analysis, alongside the construction of cost-volume-profit graphs. Budgeting is addressed through the creation of sales and purchase budgets. Further, the report assesses GST implications, journal entries, and balance sheets. Finally, it presents a general ledger and a bank reconciliation statement, offering a complete overview of the financial aspects of the business. The report also includes recommendations on supplier changes and the decision to import motors or buy them in Australia.

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

QUESTION 1...................................................................................................................................1

1. Game changers of businesses and consequences of less hierarchical business models.....1

2. Importance of competent leadership..................................................................................1

3. Core leadership and additional new qualities.....................................................................1

4. Alterations in leadership roles and skills via automation and artificial intelligence..........1

5. Overlap between soft and employability skills..................................................................2

6. Critical Leadership skills....................................................................................................2

7. Role of trust........................................................................................................................2

8. Expectation of modern professional accountants...............................................................2

9. Identification of soft and critical leadership skill...............................................................2

QUESTION 2...................................................................................................................................3

1. Measuring the variable cost................................................................................................3

2. Measuring the contribution margin per unit.......................................................................3

3.Profit equation in relation with terms of motor sold...........................................................3

4. Drafting a Cost volume profit graph..................................................................................4

5. Break even analysis............................................................................................................4

6. Analysing the current profit or loss....................................................................................5

7. Changing the suppliers.......................................................................................................5

8. Decision based on importing motors or buying in Australia..............................................5

QUESTION 3...................................................................................................................................6

A. Sales Budget......................................................................................................................6

B. Purchase Budget................................................................................................................6

QUESTION 4...................................................................................................................................7

1. GST analysis.......................................................................................................................7

2. General Journal Entry.........................................................................................................7

3. Balance sheet......................................................................................................................7

4. Modification of transactional entries..................................................................................8

QUESTION 5...................................................................................................................................8

1. General Ledger Cash..........................................................................................................8

2. Bank Reconciliation Statement..........................................................................................8

QUESTION 1...................................................................................................................................1

1. Game changers of businesses and consequences of less hierarchical business models.....1

2. Importance of competent leadership..................................................................................1

3. Core leadership and additional new qualities.....................................................................1

4. Alterations in leadership roles and skills via automation and artificial intelligence..........1

5. Overlap between soft and employability skills..................................................................2

6. Critical Leadership skills....................................................................................................2

7. Role of trust........................................................................................................................2

8. Expectation of modern professional accountants...............................................................2

9. Identification of soft and critical leadership skill...............................................................2

QUESTION 2...................................................................................................................................3

1. Measuring the variable cost................................................................................................3

2. Measuring the contribution margin per unit.......................................................................3

3.Profit equation in relation with terms of motor sold...........................................................3

4. Drafting a Cost volume profit graph..................................................................................4

5. Break even analysis............................................................................................................4

6. Analysing the current profit or loss....................................................................................5

7. Changing the suppliers.......................................................................................................5

8. Decision based on importing motors or buying in Australia..............................................5

QUESTION 3...................................................................................................................................6

A. Sales Budget......................................................................................................................6

B. Purchase Budget................................................................................................................6

QUESTION 4...................................................................................................................................7

1. GST analysis.......................................................................................................................7

2. General Journal Entry.........................................................................................................7

3. Balance sheet......................................................................................................................7

4. Modification of transactional entries..................................................................................8

QUESTION 5...................................................................................................................................8

1. General Ledger Cash..........................................................................................................8

2. Bank Reconciliation Statement..........................................................................................8

REFERENCES................................................................................................................................9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

QUESTION 1

1. Game changers of businesses and consequences of less hierarchical business models

The modern age is referred as game changer for business and leader perspective. The

combination of rapid technological development, globalisation and emergence of knowledge and

data is altering each and everything. In the same series, different external factors via

technological alteration for raising complexity in business and rush towards alterations in

auditors. The report of audit could be great opportunity for various changes to break its mould

and for demonstrating audit value.

The emergence of innovative business models and business entity are considered as less

hierarchical. Ideas and innovation could be emerged everywhere but concerned point is stated

with capability for encouraging development and for recognition of the best aspect.

2. Importance of competent leadership

Competent leadership is very important skill in digital age due to rapid evolution, risky,

messy, unpredictable time as it provides in-surety about technological development. In this

environment, leaders which are outstanding are referred as very important currency.

3. Core leadership and additional new qualities

Core leadership qualities: Motivational skills, emotional intelligence and team building

Additional new qualities: domain expertise, authority, decisiveness, short term task focus

In the present scenario, leaders should be capable for understanding impact of technology

with aspect of business. Technical expertise is second requirement but prior it must be capable

for forecasting both potential negative impact of technology and opportunity as well.

4. Alterations in leadership roles and skills via automation and artificial intelligence

The major driving force is refereed as impact of artificial intelligence, automation and

machine learning in workplace partly as machines are taking over elements which are according

to task with context of leadership. Automation provides wider implications for employees in

leadership as it provides increment about guidance and reassurance for business leaders with

context of workplace's future and their jobs. The organization with artificial intelligence holds

specific record for raising exercises of the fastest capital.

1

1. Game changers of businesses and consequences of less hierarchical business models

The modern age is referred as game changer for business and leader perspective. The

combination of rapid technological development, globalisation and emergence of knowledge and

data is altering each and everything. In the same series, different external factors via

technological alteration for raising complexity in business and rush towards alterations in

auditors. The report of audit could be great opportunity for various changes to break its mould

and for demonstrating audit value.

The emergence of innovative business models and business entity are considered as less

hierarchical. Ideas and innovation could be emerged everywhere but concerned point is stated

with capability for encouraging development and for recognition of the best aspect.

2. Importance of competent leadership

Competent leadership is very important skill in digital age due to rapid evolution, risky,

messy, unpredictable time as it provides in-surety about technological development. In this

environment, leaders which are outstanding are referred as very important currency.

3. Core leadership and additional new qualities

Core leadership qualities: Motivational skills, emotional intelligence and team building

Additional new qualities: domain expertise, authority, decisiveness, short term task focus

In the present scenario, leaders should be capable for understanding impact of technology

with aspect of business. Technical expertise is second requirement but prior it must be capable

for forecasting both potential negative impact of technology and opportunity as well.

4. Alterations in leadership roles and skills via automation and artificial intelligence

The major driving force is refereed as impact of artificial intelligence, automation and

machine learning in workplace partly as machines are taking over elements which are according

to task with context of leadership. Automation provides wider implications for employees in

leadership as it provides increment about guidance and reassurance for business leaders with

context of workplace's future and their jobs. The organization with artificial intelligence holds

specific record for raising exercises of the fastest capital.

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

5. Overlap between soft and employability skills

Communication, problem solving, teamwork are major skills which are overlapped in

soft and employability skills. The major areas such as finance and research and development has

huge requirement.

6. Critical Leadership skills

The critical leadership skills are:

Adaptability: It is referred as openness to innovative ideas and presence of willingness for

altering mind during performance as it could threaten leader's ego as well.

Vision: It is considered as very important for business entity as it is very vital in this digital

world as business models are disrupted constantly and it has presence of high uncertainty

of short term.

Humility: It is referred as leader’s evolution about requirement of learning in context of

digital age, knowledge could be originated from anywhere.

7. Role of trust

Trust among customer and business entity has gained innovative level of importance. The

most important role of CEO is for building trust. Employer belongs to safe house in context of

global governance as major employer performs what is right for organization. Business entity

take particular actions for raising profit and to improve social and economic conditions.

8. Expectation of modern professional accountants

All the alterations must be capable for deep integration, relevant and broad technical

expertise along with professional and ethical skills provides forward thinking strategic

capabilities and advanced skill set must be shaped for future of global business (Accountancy

Futures, 2018).

9. Identification of soft and critical leadership skill

Strong skill: Communication and leadership

Weak skill: Problem Solving abilities

To improve problem solving capability to work with logic puzzles, reading idea journal

and to be updated with present scenarios. In the same series. Problem should be understood and

special focus must be laid. Things should be simplified and all possible solutions must be listed

and thinking process should be lateral

2

Communication, problem solving, teamwork are major skills which are overlapped in

soft and employability skills. The major areas such as finance and research and development has

huge requirement.

6. Critical Leadership skills

The critical leadership skills are:

Adaptability: It is referred as openness to innovative ideas and presence of willingness for

altering mind during performance as it could threaten leader's ego as well.

Vision: It is considered as very important for business entity as it is very vital in this digital

world as business models are disrupted constantly and it has presence of high uncertainty

of short term.

Humility: It is referred as leader’s evolution about requirement of learning in context of

digital age, knowledge could be originated from anywhere.

7. Role of trust

Trust among customer and business entity has gained innovative level of importance. The

most important role of CEO is for building trust. Employer belongs to safe house in context of

global governance as major employer performs what is right for organization. Business entity

take particular actions for raising profit and to improve social and economic conditions.

8. Expectation of modern professional accountants

All the alterations must be capable for deep integration, relevant and broad technical

expertise along with professional and ethical skills provides forward thinking strategic

capabilities and advanced skill set must be shaped for future of global business (Accountancy

Futures, 2018).

9. Identification of soft and critical leadership skill

Strong skill: Communication and leadership

Weak skill: Problem Solving abilities

To improve problem solving capability to work with logic puzzles, reading idea journal

and to be updated with present scenarios. In the same series. Problem should be understood and

special focus must be laid. Things should be simplified and all possible solutions must be listed

and thinking process should be lateral

2

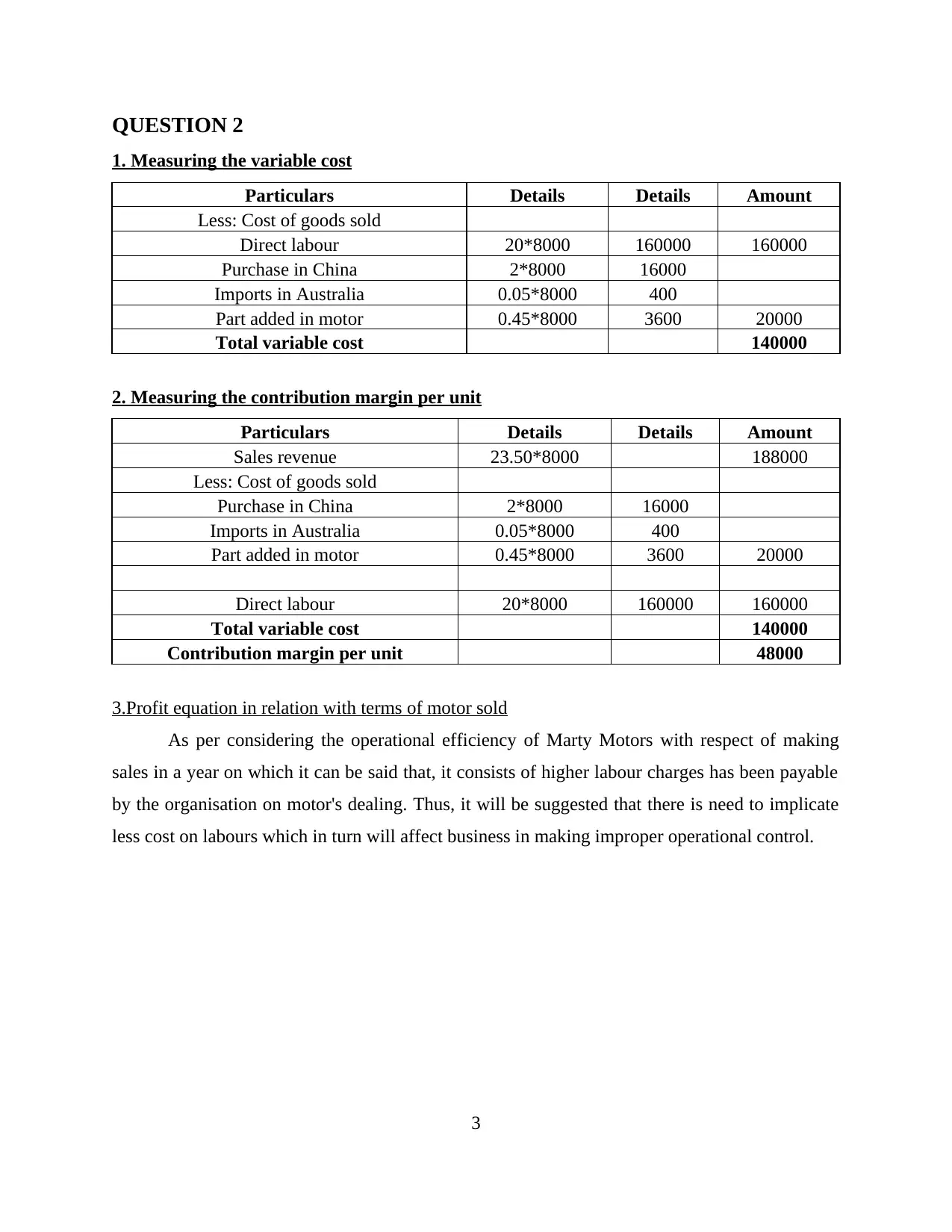

QUESTION 2

1. Measuring the variable cost

Particulars Details Details Amount

Less: Cost of goods sold

Direct labour 20*8000 160000 160000

Purchase in China 2*8000 16000

Imports in Australia 0.05*8000 400

Part added in motor 0.45*8000 3600 20000

Total variable cost 140000

2. Measuring the contribution margin per unit

Particulars Details Details Amount

Sales revenue 23.50*8000 188000

Less: Cost of goods sold

Purchase in China 2*8000 16000

Imports in Australia 0.05*8000 400

Part added in motor 0.45*8000 3600 20000

Direct labour 20*8000 160000 160000

Total variable cost 140000

Contribution margin per unit 48000

3.Profit equation in relation with terms of motor sold

As per considering the operational efficiency of Marty Motors with respect of making

sales in a year on which it can be said that, it consists of higher labour charges has been payable

by the organisation on motor's dealing. Thus, it will be suggested that there is need to implicate

less cost on labours which in turn will affect business in making improper operational control.

3

1. Measuring the variable cost

Particulars Details Details Amount

Less: Cost of goods sold

Direct labour 20*8000 160000 160000

Purchase in China 2*8000 16000

Imports in Australia 0.05*8000 400

Part added in motor 0.45*8000 3600 20000

Total variable cost 140000

2. Measuring the contribution margin per unit

Particulars Details Details Amount

Sales revenue 23.50*8000 188000

Less: Cost of goods sold

Purchase in China 2*8000 16000

Imports in Australia 0.05*8000 400

Part added in motor 0.45*8000 3600 20000

Direct labour 20*8000 160000 160000

Total variable cost 140000

Contribution margin per unit 48000

3.Profit equation in relation with terms of motor sold

As per considering the operational efficiency of Marty Motors with respect of making

sales in a year on which it can be said that, it consists of higher labour charges has been payable

by the organisation on motor's dealing. Thus, it will be suggested that there is need to implicate

less cost on labours which in turn will affect business in making improper operational control.

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

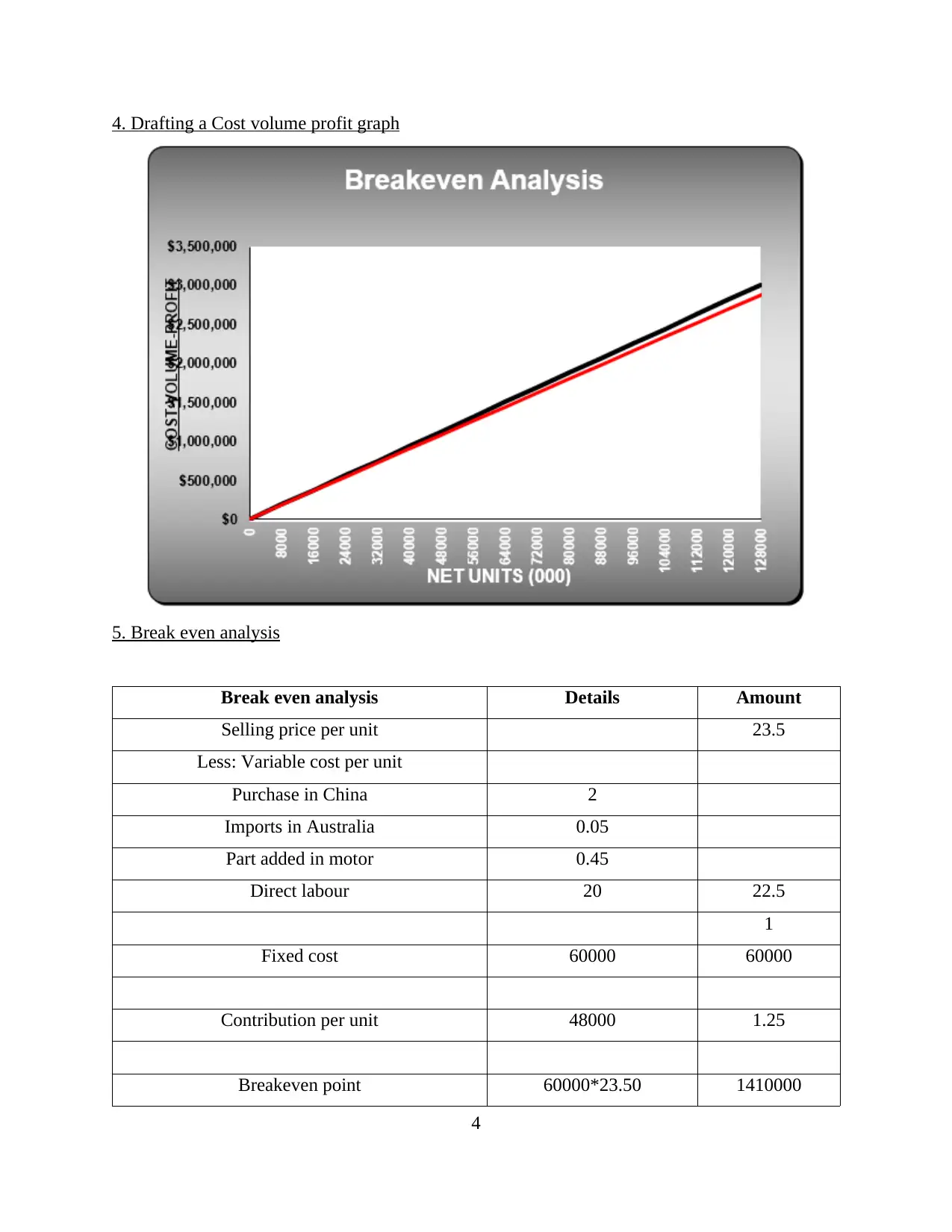

4. Drafting a Cost volume profit graph

5. Break even analysis

Break even analysis Details Amount

Selling price per unit 23.5

Less: Variable cost per unit

Purchase in China 2

Imports in Australia 0.05

Part added in motor 0.45

Direct labour 20 22.5

1

Fixed cost 60000 60000

Contribution per unit 48000 1.25

Breakeven point 60000*23.50 1410000

4

5. Break even analysis

Break even analysis Details Amount

Selling price per unit 23.5

Less: Variable cost per unit

Purchase in China 2

Imports in Australia 0.05

Part added in motor 0.45

Direct labour 20 22.5

1

Fixed cost 60000 60000

Contribution per unit 48000 1.25

Breakeven point 60000*23.50 1410000

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

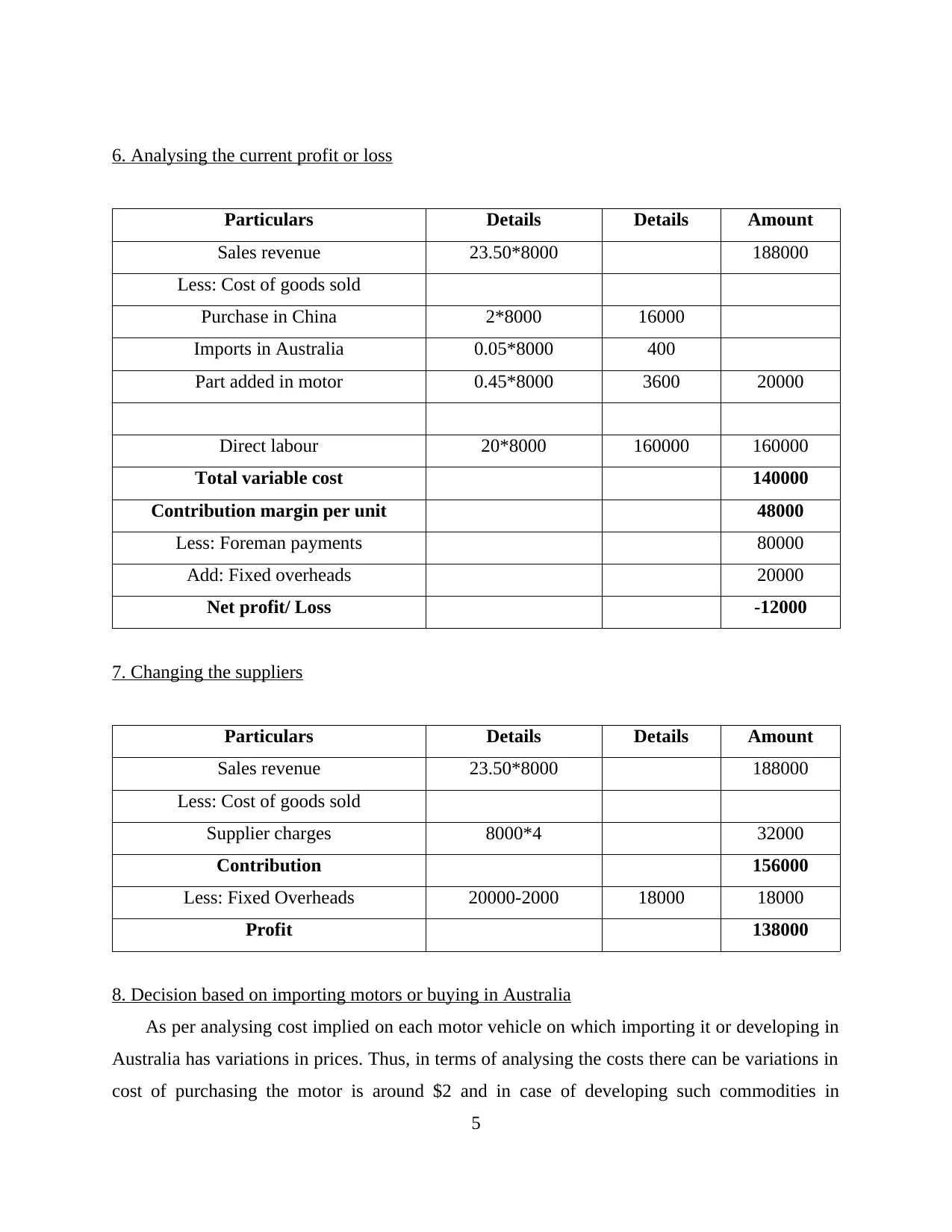

6. Analysing the current profit or loss

Particulars Details Details Amount

Sales revenue 23.50*8000 188000

Less: Cost of goods sold

Purchase in China 2*8000 16000

Imports in Australia 0.05*8000 400

Part added in motor 0.45*8000 3600 20000

Direct labour 20*8000 160000 160000

Total variable cost 140000

Contribution margin per unit 48000

Less: Foreman payments 80000

Add: Fixed overheads 20000

Net profit/ Loss -12000

7. Changing the suppliers

Particulars Details Details Amount

Sales revenue 23.50*8000 188000

Less: Cost of goods sold

Supplier charges 8000*4 32000

Contribution 156000

Less: Fixed Overheads 20000-2000 18000 18000

Profit 138000

8. Decision based on importing motors or buying in Australia

As per analysing cost implied on each motor vehicle on which importing it or developing in

Australia has variations in prices. Thus, in terms of analysing the costs there can be variations in

cost of purchasing the motor is around $2 and in case of developing such commodities in

5

Particulars Details Details Amount

Sales revenue 23.50*8000 188000

Less: Cost of goods sold

Purchase in China 2*8000 16000

Imports in Australia 0.05*8000 400

Part added in motor 0.45*8000 3600 20000

Direct labour 20*8000 160000 160000

Total variable cost 140000

Contribution margin per unit 48000

Less: Foreman payments 80000

Add: Fixed overheads 20000

Net profit/ Loss -12000

7. Changing the suppliers

Particulars Details Details Amount

Sales revenue 23.50*8000 188000

Less: Cost of goods sold

Supplier charges 8000*4 32000

Contribution 156000

Less: Fixed Overheads 20000-2000 18000 18000

Profit 138000

8. Decision based on importing motors or buying in Australia

As per analysing cost implied on each motor vehicle on which importing it or developing in

Australia has variations in prices. Thus, in terms of analysing the costs there can be variations in

cost of purchasing the motor is around $2 and in case of developing such commodities in

5

Australia which is of $0.05. Thus, in this case manufacturing the Motor vehicle in Australia will

be helpful in reducing the costs implied in each activity.

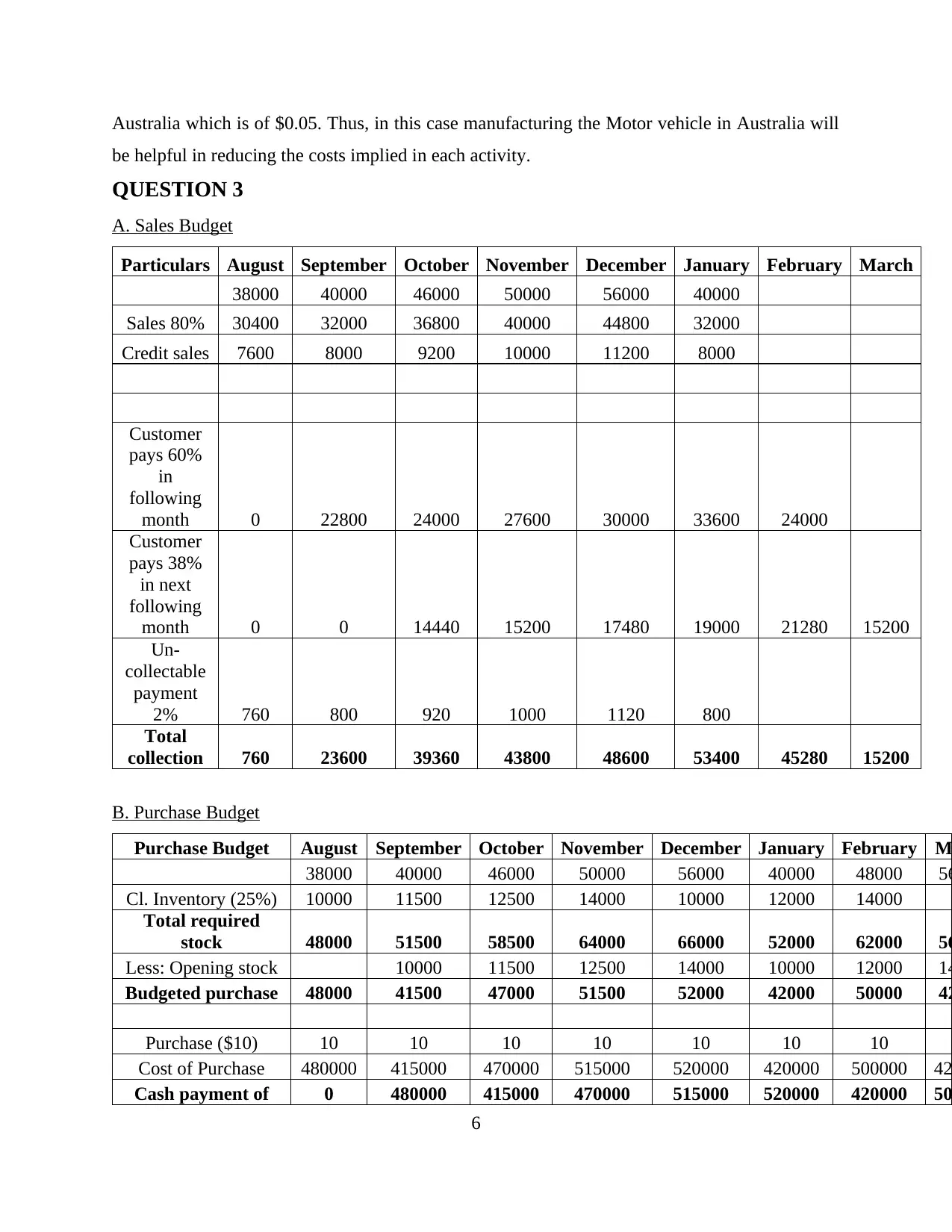

QUESTION 3

A. Sales Budget

Particulars August September October November December January February March

38000 40000 46000 50000 56000 40000

Sales 80% 30400 32000 36800 40000 44800 32000

Credit sales 7600 8000 9200 10000 11200 8000

Customer

pays 60%

in

following

month 0 22800 24000 27600 30000 33600 24000

Customer

pays 38%

in next

following

month 0 0 14440 15200 17480 19000 21280 15200

Un-

collectable

payment

2% 760 800 920 1000 1120 800

Total

collection 760 23600 39360 43800 48600 53400 45280 15200

B. Purchase Budget

Purchase Budget August September October November December January February M

38000 40000 46000 50000 56000 40000 48000 56

Cl. Inventory (25%) 10000 11500 12500 14000 10000 12000 14000

Total required

stock 48000 51500 58500 64000 66000 52000 62000 56

Less: Opening stock 10000 11500 12500 14000 10000 12000 14

Budgeted purchase 48000 41500 47000 51500 52000 42000 50000 42

Purchase ($10) 10 10 10 10 10 10 10

Cost of Purchase 480000 415000 470000 515000 520000 420000 500000 42

Cash payment of 0 480000 415000 470000 515000 520000 420000 50

6

be helpful in reducing the costs implied in each activity.

QUESTION 3

A. Sales Budget

Particulars August September October November December January February March

38000 40000 46000 50000 56000 40000

Sales 80% 30400 32000 36800 40000 44800 32000

Credit sales 7600 8000 9200 10000 11200 8000

Customer

pays 60%

in

following

month 0 22800 24000 27600 30000 33600 24000

Customer

pays 38%

in next

following

month 0 0 14440 15200 17480 19000 21280 15200

Un-

collectable

payment

2% 760 800 920 1000 1120 800

Total

collection 760 23600 39360 43800 48600 53400 45280 15200

B. Purchase Budget

Purchase Budget August September October November December January February M

38000 40000 46000 50000 56000 40000 48000 56

Cl. Inventory (25%) 10000 11500 12500 14000 10000 12000 14000

Total required

stock 48000 51500 58500 64000 66000 52000 62000 56

Less: Opening stock 10000 11500 12500 14000 10000 12000 14

Budgeted purchase 48000 41500 47000 51500 52000 42000 50000 42

Purchase ($10) 10 10 10 10 10 10 10

Cost of Purchase 480000 415000 470000 515000 520000 420000 500000 42

Cash payment of 0 480000 415000 470000 515000 520000 420000 50

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Purchase

QUESTION 4

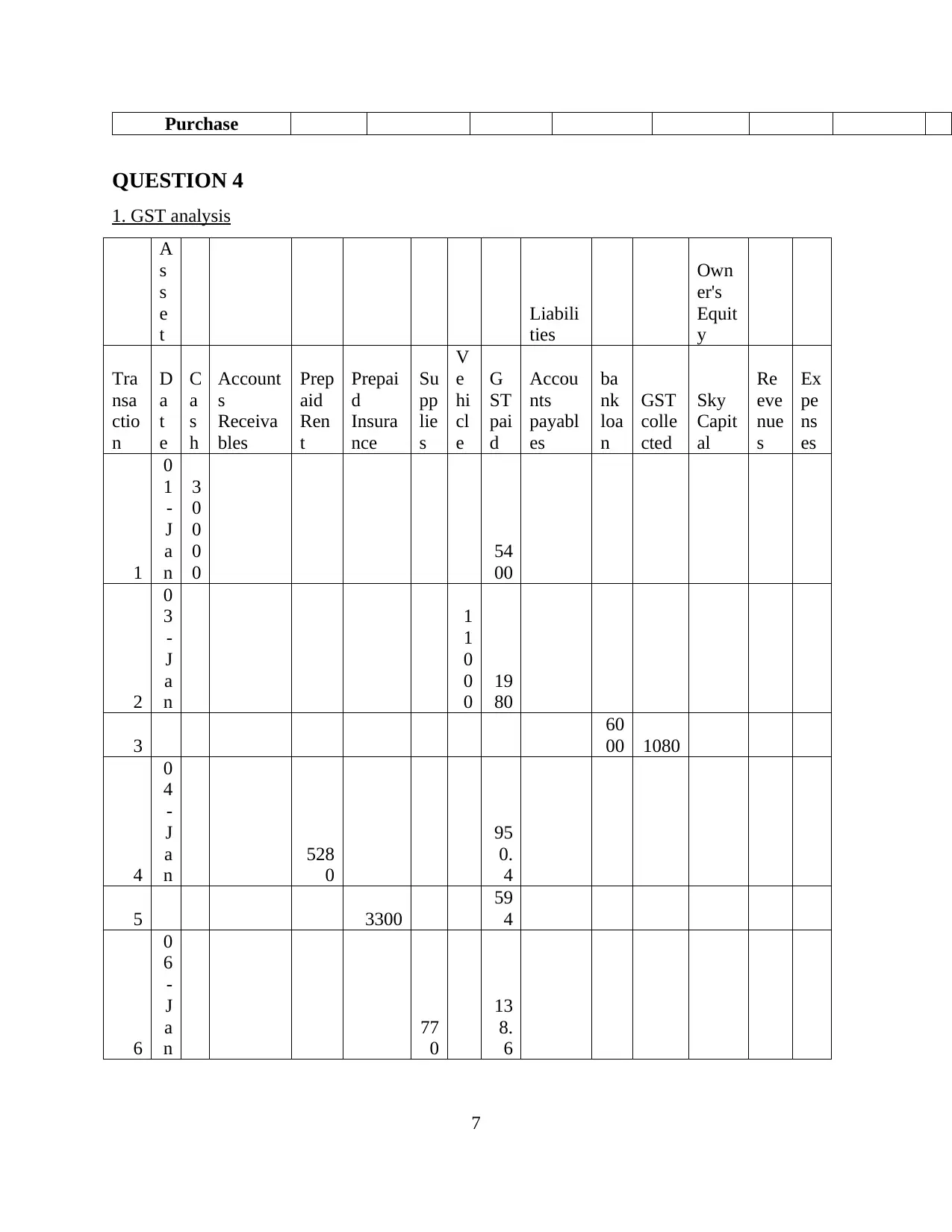

1. GST analysis

A

s

s

e

t

Liabili

ties

Own

er's

Equit

y

Tra

nsa

ctio

n

D

a

t

e

C

a

s

h

Account

s

Receiva

bles

Prep

aid

Ren

t

Prepai

d

Insura

nce

Su

pp

lie

s

V

e

hi

cl

e

G

ST

pai

d

Accou

nts

payabl

es

ba

nk

loa

n

GST

colle

cted

Sky

Capit

al

Re

eve

nue

s

Ex

pe

ns

es

1

0

1

-

J

a

n

3

0

0

0

0

54

00

2

0

3

-

J

a

n

1

1

0

0

0

19

80

3

60

00 1080

4

0

4

-

J

a

n

528

0

95

0.

4

5 3300

59

4

6

0

6

-

J

a

n

77

0

13

8.

6

7

QUESTION 4

1. GST analysis

A

s

s

e

t

Liabili

ties

Own

er's

Equit

y

Tra

nsa

ctio

n

D

a

t

e

C

a

s

h

Account

s

Receiva

bles

Prep

aid

Ren

t

Prepai

d

Insura

nce

Su

pp

lie

s

V

e

hi

cl

e

G

ST

pai

d

Accou

nts

payabl

es

ba

nk

loa

n

GST

colle

cted

Sky

Capit

al

Re

eve

nue

s

Ex

pe

ns

es

1

0

1

-

J

a

n

3

0

0

0

0

54

00

2

0

3

-

J

a

n

1

1

0

0

0

19

80

3

60

00 1080

4

0

4

-

J

a

n

528

0

95

0.

4

5 3300

59

4

6

0

6

-

J

a

n

77

0

13

8.

6

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

1

4

-

J

a

n

8

8

0

0

88

00

8

1

8

-

J

a

n

22

0

9

2

0

-

J

a

n

11

0

19

.8

10

2

5

-

J

a

n

4

9

5

0

49

50

11

2

8

-

J

a

n

66

0

12

T

o

t

a

l

4

3

7

5

0 0

528

0 3300

88

0

1

1

0

0

0

90

82

.8 0

60

00 1080 0

13

75

0

88

0

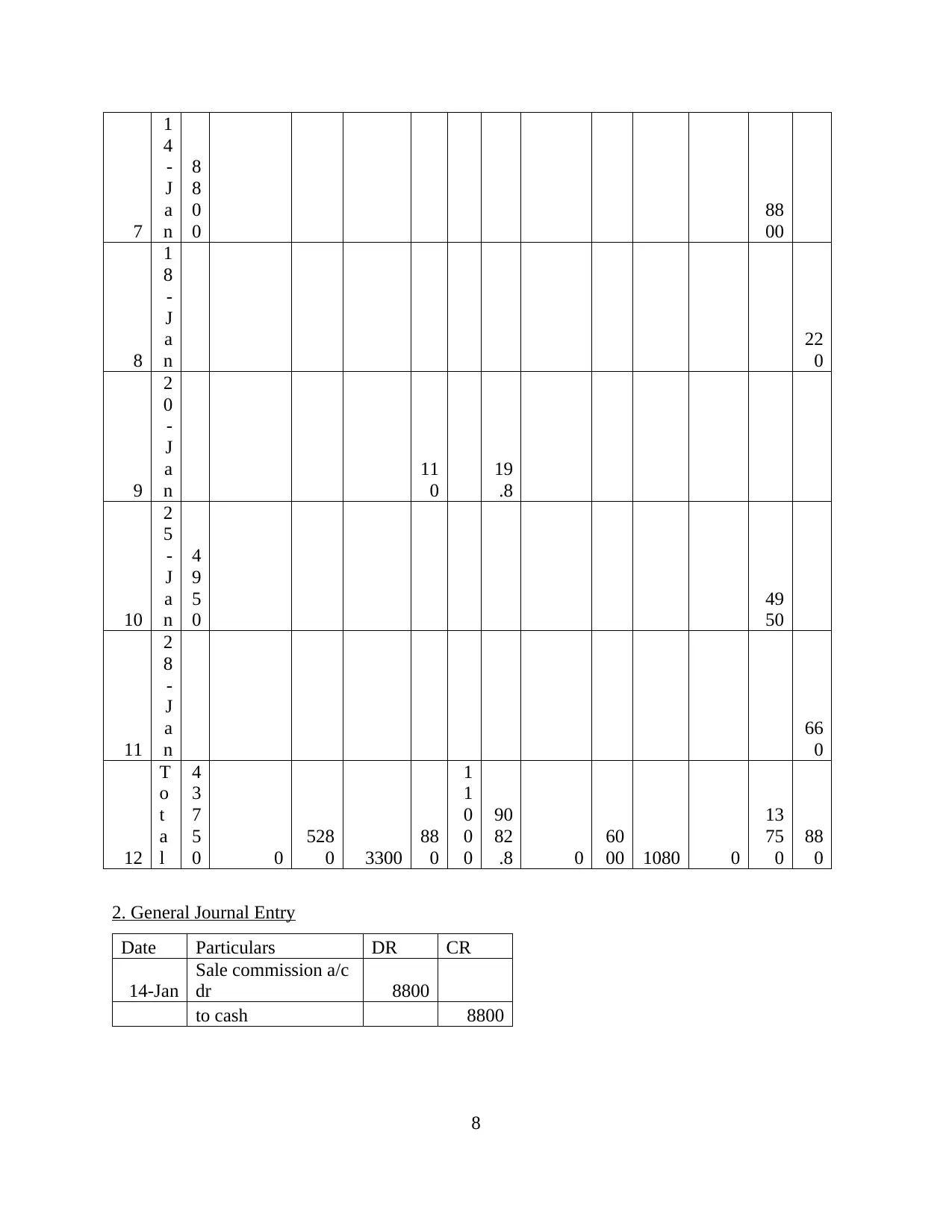

2. General Journal Entry

Date Particulars DR CR

14-Jan

Sale commission a/c

dr 8800

to cash 8800

8

1

4

-

J

a

n

8

8

0

0

88

00

8

1

8

-

J

a

n

22

0

9

2

0

-

J

a

n

11

0

19

.8

10

2

5

-

J

a

n

4

9

5

0

49

50

11

2

8

-

J

a

n

66

0

12

T

o

t

a

l

4

3

7

5

0 0

528

0 3300

88

0

1

1

0

0

0

90

82

.8 0

60

00 1080 0

13

75

0

88

0

2. General Journal Entry

Date Particulars DR CR

14-Jan

Sale commission a/c

dr 8800

to cash 8800

8

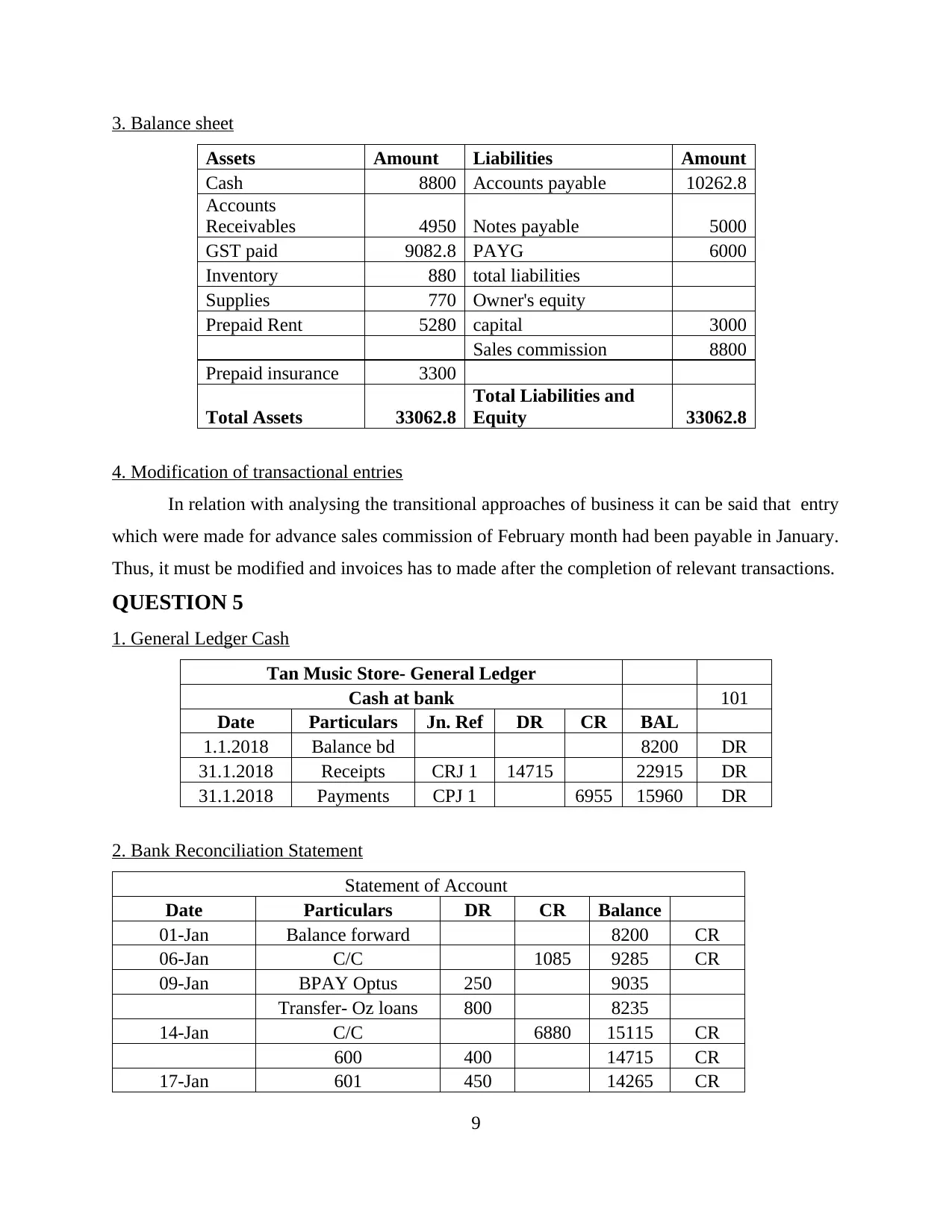

3. Balance sheet

Assets Amount Liabilities Amount

Cash 8800 Accounts payable 10262.8

Accounts

Receivables 4950 Notes payable 5000

GST paid 9082.8 PAYG 6000

Inventory 880 total liabilities

Supplies 770 Owner's equity

Prepaid Rent 5280 capital 3000

Sales commission 8800

Prepaid insurance 3300

Total Assets 33062.8

Total Liabilities and

Equity 33062.8

4. Modification of transactional entries

In relation with analysing the transitional approaches of business it can be said that entry

which were made for advance sales commission of February month had been payable in January.

Thus, it must be modified and invoices has to made after the completion of relevant transactions.

QUESTION 5

1. General Ledger Cash

Tan Music Store- General Ledger

Cash at bank 101

Date Particulars Jn. Ref DR CR BAL

1.1.2018 Balance bd 8200 DR

31.1.2018 Receipts CRJ 1 14715 22915 DR

31.1.2018 Payments CPJ 1 6955 15960 DR

2. Bank Reconciliation Statement

Statement of Account

Date Particulars DR CR Balance

01-Jan Balance forward 8200 CR

06-Jan C/C 1085 9285 CR

09-Jan BPAY Optus 250 9035

Transfer- Oz loans 800 8235

14-Jan C/C 6880 15115 CR

600 400 14715 CR

17-Jan 601 450 14265 CR

9

Assets Amount Liabilities Amount

Cash 8800 Accounts payable 10262.8

Accounts

Receivables 4950 Notes payable 5000

GST paid 9082.8 PAYG 6000

Inventory 880 total liabilities

Supplies 770 Owner's equity

Prepaid Rent 5280 capital 3000

Sales commission 8800

Prepaid insurance 3300

Total Assets 33062.8

Total Liabilities and

Equity 33062.8

4. Modification of transactional entries

In relation with analysing the transitional approaches of business it can be said that entry

which were made for advance sales commission of February month had been payable in January.

Thus, it must be modified and invoices has to made after the completion of relevant transactions.

QUESTION 5

1. General Ledger Cash

Tan Music Store- General Ledger

Cash at bank 101

Date Particulars Jn. Ref DR CR BAL

1.1.2018 Balance bd 8200 DR

31.1.2018 Receipts CRJ 1 14715 22915 DR

31.1.2018 Payments CPJ 1 6955 15960 DR

2. Bank Reconciliation Statement

Statement of Account

Date Particulars DR CR Balance

01-Jan Balance forward 8200 CR

06-Jan C/C 1085 9285 CR

09-Jan BPAY Optus 250 9035

Transfer- Oz loans 800 8235

14-Jan C/C 6880 15115 CR

600 400 14715 CR

17-Jan 601 450 14265 CR

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.