Financial Analysis Report: Ratios, Budgets, Break-Even Analysis

VerifiedAdded on 2023/06/04

|18

|3824

|77

Report

AI Summary

This report provides a comprehensive financial analysis, beginning with ratio analysis to assess a company's financial health, including gross profit margin, asset usage, current ratio, and debt-to-equity ratio. It then moves on to cash budgeting, forecasting income and expenses over a six-month period, and identifying areas for cost control and revenue enhancement. The report also delves into break-even analysis, margin of safety calculations, and strategic recommendations for improving sales and profitability. Finally, it evaluates investment projects using payback period, net present value, and average rate of return, recommending the most effective project appraisal method and discussing capital budgeting techniques. The report concludes with a summary of findings and recommendations to improve financial performance and guide investment decisions.

Importance of Finance

1

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

Contents...........................................................................................................................................2

INTRODUCTION...........................................................................................................................3

Question 1........................................................................................................................................3

a) Calculate the financial ratio for the year ended as 31 march 2018-19....................................3

b)USERS OF FINANCIAL STATEMENTS-.............................................................................5

QUESTION 2..................................................................................................................................6

a) financial status's opening statement at the beginning of July 2015........................................6

b) Computation of forecast cash budget for next 6 months.........................................................6

c) Clarification of additional disbursements................................................................................7

QUESTION 3..................................................................................................................................7

a ) Calculation of Break even point (BEP)..................................................................................7

b) Margin of safety ( MOS ) for the year ended 2019 and 2020.................................................9

c) Evaluate the new strategies that can be made by Jessica.........................................................9

QUESTION 4..................................................................................................................................9

a) calculation of pay back period, Net present value and average rate of return.........................9

b) Determine the most effective method of project appraisal....................................................13

c)Capital budgeting methods and techniques that can used for investments decisions.............13

CONCLUSION..............................................................................................................................16

REFERENCES..............................................................................................................................18

2

Contents...........................................................................................................................................2

INTRODUCTION...........................................................................................................................3

Question 1........................................................................................................................................3

a) Calculate the financial ratio for the year ended as 31 march 2018-19....................................3

b)USERS OF FINANCIAL STATEMENTS-.............................................................................5

QUESTION 2..................................................................................................................................6

a) financial status's opening statement at the beginning of July 2015........................................6

b) Computation of forecast cash budget for next 6 months.........................................................6

c) Clarification of additional disbursements................................................................................7

QUESTION 3..................................................................................................................................7

a ) Calculation of Break even point (BEP)..................................................................................7

b) Margin of safety ( MOS ) for the year ended 2019 and 2020.................................................9

c) Evaluate the new strategies that can be made by Jessica.........................................................9

QUESTION 4..................................................................................................................................9

a) calculation of pay back period, Net present value and average rate of return.........................9

b) Determine the most effective method of project appraisal....................................................13

c)Capital budgeting methods and techniques that can used for investments decisions.............13

CONCLUSION..............................................................................................................................16

REFERENCES..............................................................................................................................18

2

INTRODUCTION

Finance plays an important role in an organisation stability, growth and expansion, it

basically the backbone of a business entity. There are various components indulge in managing

the finance, planning, organising, directing and controlling (Baker, Kumar and Pandey, 2020)

(Black and Stafford, 2018). In this report, ratio analysis has been used for finding out the

position of the company. In the second part cash budget have been prepared to forecast the

estimated expenses and income of specific period. In third question breakeven point, margin

safety concepts are used for determining the sales related decisions in order to develop a new

strategy to compete in the market. The other question asks for finding out the pay back, NPV and

ARR for finding out the most viable investment project.

Question 1

a) Calculate the financial ratio for the year ended as 31 march 2018-19.

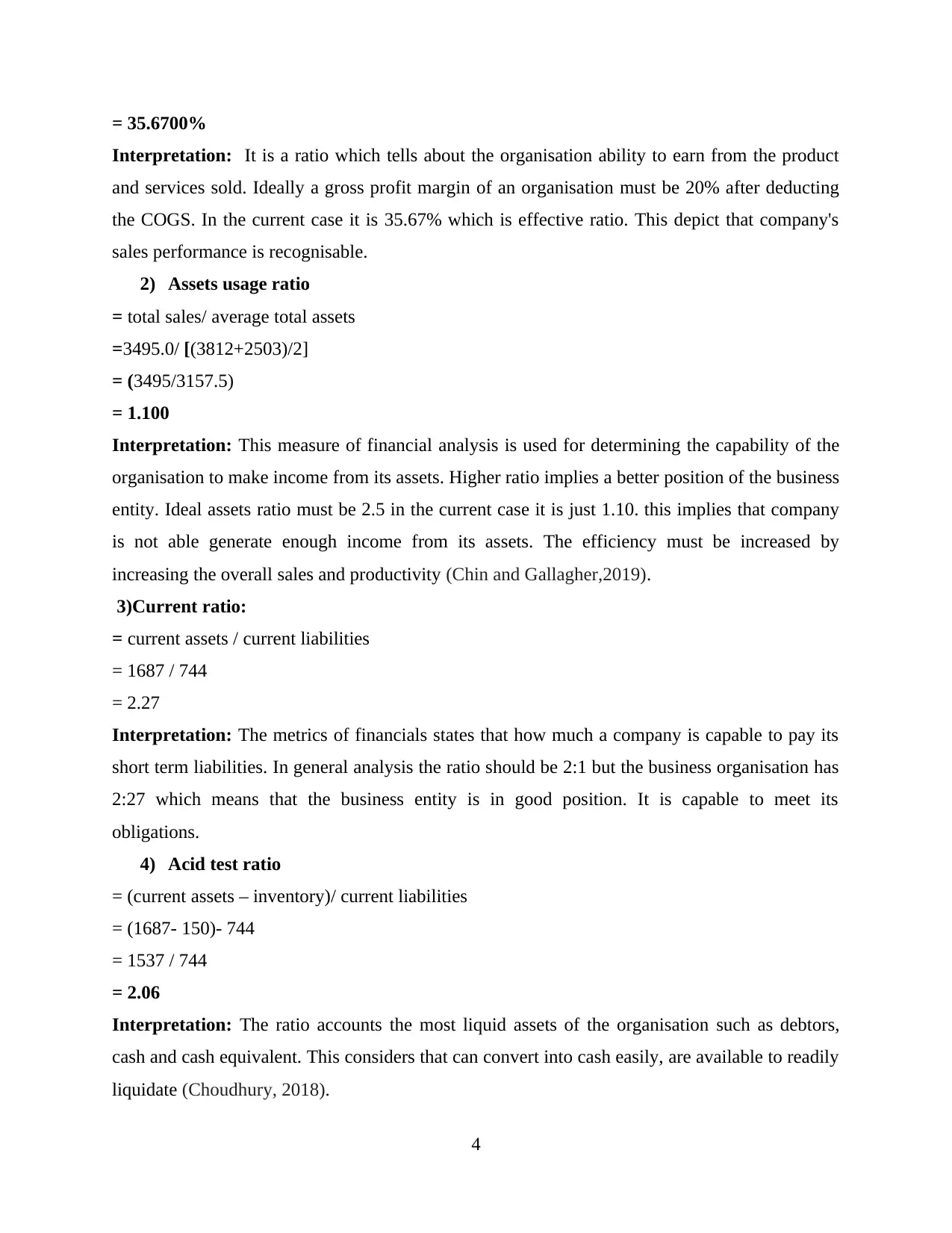

1) Gross profit margin

= (sales revenue – Cost of goods sold) * 100/ Revenue

= (3495.00-2182) *100 / 3495

= (1313/3495.00) *100

3

Finance plays an important role in an organisation stability, growth and expansion, it

basically the backbone of a business entity. There are various components indulge in managing

the finance, planning, organising, directing and controlling (Baker, Kumar and Pandey, 2020)

(Black and Stafford, 2018). In this report, ratio analysis has been used for finding out the

position of the company. In the second part cash budget have been prepared to forecast the

estimated expenses and income of specific period. In third question breakeven point, margin

safety concepts are used for determining the sales related decisions in order to develop a new

strategy to compete in the market. The other question asks for finding out the pay back, NPV and

ARR for finding out the most viable investment project.

Question 1

a) Calculate the financial ratio for the year ended as 31 march 2018-19.

1) Gross profit margin

= (sales revenue – Cost of goods sold) * 100/ Revenue

= (3495.00-2182) *100 / 3495

= (1313/3495.00) *100

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

= 35.6700%

Interpretation: It is a ratio which tells about the organisation ability to earn from the product

and services sold. Ideally a gross profit margin of an organisation must be 20% after deducting

the COGS. In the current case it is 35.67% which is effective ratio. This depict that company's

sales performance is recognisable.

2) Assets usage ratio

= total sales/ average total assets

=3495.0/ [(3812+2503)/2]

= (3495/3157.5)

= 1.100

Interpretation: This measure of financial analysis is used for determining the capability of the

organisation to make income from its assets. Higher ratio implies a better position of the business

entity. Ideal assets ratio must be 2.5 in the current case it is just 1.10. this implies that company

is not able generate enough income from its assets. The efficiency must be increased by

increasing the overall sales and productivity (Chin and Gallagher,2019).

3)Current ratio:

= current assets / current liabilities

= 1687 / 744

= 2.27

Interpretation: The metrics of financials states that how much a company is capable to pay its

short term liabilities. In general analysis the ratio should be 2:1 but the business organisation has

2:27 which means that the business entity is in good position. It is capable to meet its

obligations.

4) Acid test ratio

= (current assets – inventory)/ current liabilities

= (1687- 150)- 744

= 1537 / 744

= 2.06

Interpretation: The ratio accounts the most liquid assets of the organisation such as debtors,

cash and cash equivalent. This considers that can convert into cash easily, are available to readily

liquidate (Choudhury, 2018).

4

Interpretation: It is a ratio which tells about the organisation ability to earn from the product

and services sold. Ideally a gross profit margin of an organisation must be 20% after deducting

the COGS. In the current case it is 35.67% which is effective ratio. This depict that company's

sales performance is recognisable.

2) Assets usage ratio

= total sales/ average total assets

=3495.0/ [(3812+2503)/2]

= (3495/3157.5)

= 1.100

Interpretation: This measure of financial analysis is used for determining the capability of the

organisation to make income from its assets. Higher ratio implies a better position of the business

entity. Ideal assets ratio must be 2.5 in the current case it is just 1.10. this implies that company

is not able generate enough income from its assets. The efficiency must be increased by

increasing the overall sales and productivity (Chin and Gallagher,2019).

3)Current ratio:

= current assets / current liabilities

= 1687 / 744

= 2.27

Interpretation: The metrics of financials states that how much a company is capable to pay its

short term liabilities. In general analysis the ratio should be 2:1 but the business organisation has

2:27 which means that the business entity is in good position. It is capable to meet its

obligations.

4) Acid test ratio

= (current assets – inventory)/ current liabilities

= (1687- 150)- 744

= 1537 / 744

= 2.06

Interpretation: The ratio accounts the most liquid assets of the organisation such as debtors,

cash and cash equivalent. This considers that can convert into cash easily, are available to readily

liquidate (Choudhury, 2018).

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

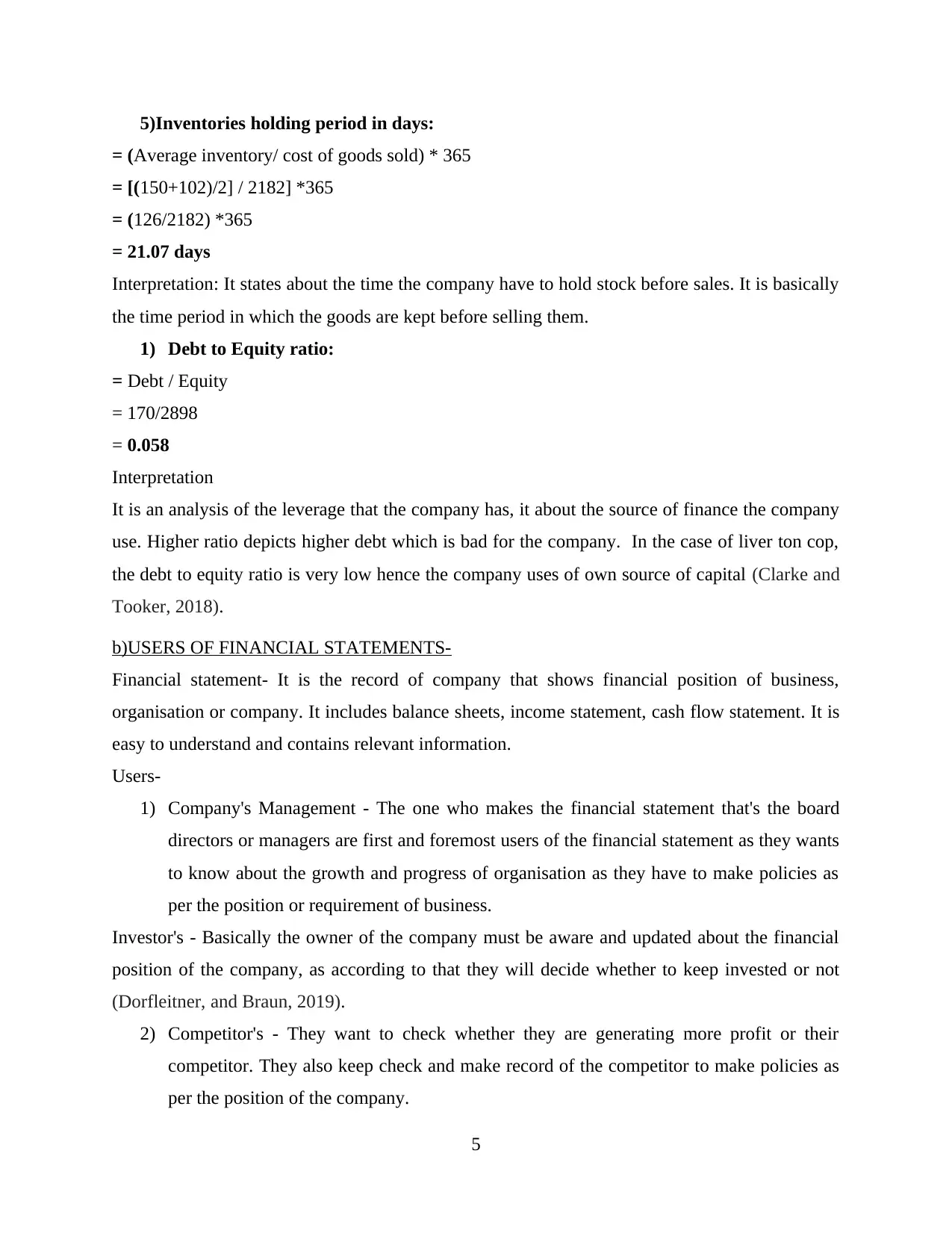

5)Inventories holding period in days:

= (Average inventory/ cost of goods sold) * 365

= [(150+102)/2] / 2182] *365

= (126/2182) *365

= 21.07 days

Interpretation: It states about the time the company have to hold stock before sales. It is basically

the time period in which the goods are kept before selling them.

1) Debt to Equity ratio:

= Debt / Equity

= 170/2898

= 0.058

Interpretation

It is an analysis of the leverage that the company has, it about the source of finance the company

use. Higher ratio depicts higher debt which is bad for the company. In the case of liver ton cop,

the debt to equity ratio is very low hence the company uses of own source of capital (Clarke and

Tooker, 2018).

b)USERS OF FINANCIAL STATEMENTS-

Financial statement- It is the record of company that shows financial position of business,

organisation or company. It includes balance sheets, income statement, cash flow statement. It is

easy to understand and contains relevant information.

Users-

1) Company's Management - The one who makes the financial statement that's the board

directors or managers are first and foremost users of the financial statement as they wants

to know about the growth and progress of organisation as they have to make policies as

per the position or requirement of business.

Investor's - Basically the owner of the company must be aware and updated about the financial

position of the company, as according to that they will decide whether to keep invested or not

(Dorfleitner, and Braun, 2019).

2) Competitor's - They want to check whether they are generating more profit or their

competitor. They also keep check and make record of the competitor to make policies as

per the position of the company.

5

= (Average inventory/ cost of goods sold) * 365

= [(150+102)/2] / 2182] *365

= (126/2182) *365

= 21.07 days

Interpretation: It states about the time the company have to hold stock before sales. It is basically

the time period in which the goods are kept before selling them.

1) Debt to Equity ratio:

= Debt / Equity

= 170/2898

= 0.058

Interpretation

It is an analysis of the leverage that the company has, it about the source of finance the company

use. Higher ratio depicts higher debt which is bad for the company. In the case of liver ton cop,

the debt to equity ratio is very low hence the company uses of own source of capital (Clarke and

Tooker, 2018).

b)USERS OF FINANCIAL STATEMENTS-

Financial statement- It is the record of company that shows financial position of business,

organisation or company. It includes balance sheets, income statement, cash flow statement. It is

easy to understand and contains relevant information.

Users-

1) Company's Management - The one who makes the financial statement that's the board

directors or managers are first and foremost users of the financial statement as they wants

to know about the growth and progress of organisation as they have to make policies as

per the position or requirement of business.

Investor's - Basically the owner of the company must be aware and updated about the financial

position of the company, as according to that they will decide whether to keep invested or not

(Dorfleitner, and Braun, 2019).

2) Competitor's - They want to check whether they are generating more profit or their

competitor. They also keep check and make record of the competitor to make policies as

per the position of the company.

5

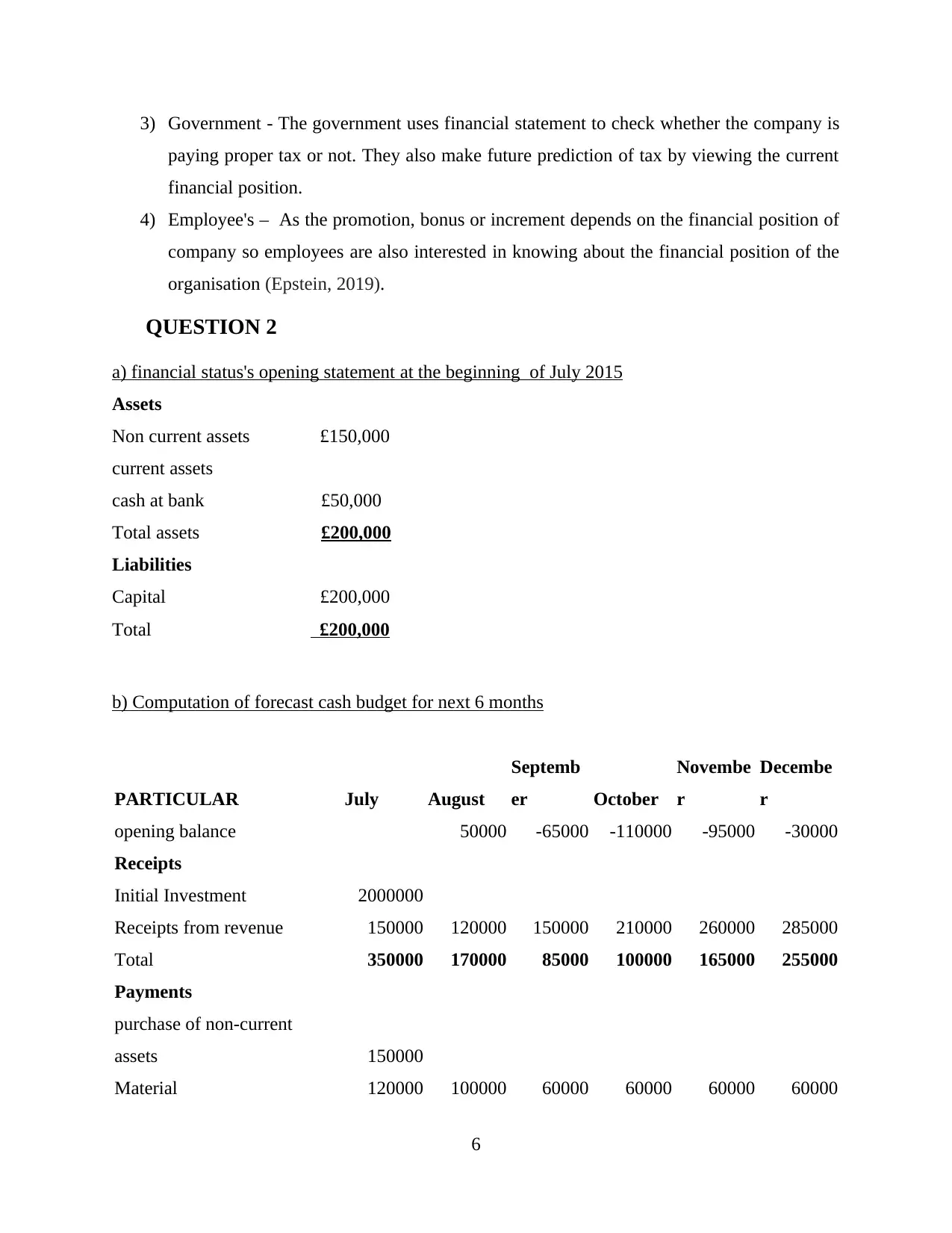

3) Government - The government uses financial statement to check whether the company is

paying proper tax or not. They also make future prediction of tax by viewing the current

financial position.

4) Employee's – As the promotion, bonus or increment depends on the financial position of

company so employees are also interested in knowing about the financial position of the

organisation (Epstein, 2019).

QUESTION 2

a) financial status's opening statement at the beginning of July 2015

Assets

Non current assets £150,000

current assets

cash at bank £50,000

Total assets £200,000

Liabilities

Capital £200,000

Total £200,000

b) Computation of forecast cash budget for next 6 months

PARTICULAR July August

Septemb

er October

Novembe

r

Decembe

r

opening balance 50000 -65000 -110000 -95000 -30000

Receipts

Initial Investment 2000000

Receipts from revenue 150000 120000 150000 210000 260000 285000

Total 350000 170000 85000 100000 165000 255000

Payments

purchase of non-current

assets 150000

Material 120000 100000 60000 60000 60000 60000

6

paying proper tax or not. They also make future prediction of tax by viewing the current

financial position.

4) Employee's – As the promotion, bonus or increment depends on the financial position of

company so employees are also interested in knowing about the financial position of the

organisation (Epstein, 2019).

QUESTION 2

a) financial status's opening statement at the beginning of July 2015

Assets

Non current assets £150,000

current assets

cash at bank £50,000

Total assets £200,000

Liabilities

Capital £200,000

Total £200,000

b) Computation of forecast cash budget for next 6 months

PARTICULAR July August

Septemb

er October

Novembe

r

Decembe

r

opening balance 50000 -65000 -110000 -95000 -30000

Receipts

Initial Investment 2000000

Receipts from revenue 150000 120000 150000 210000 260000 285000

Total 350000 170000 85000 100000 165000 255000

Payments

purchase of non-current

assets 150000

Material 120000 100000 60000 60000 60000 60000

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Other expenses 55000 55000 55000 55000 55000 55000

Labour expenses 80000 80000 80000 80000 80000 80000

Tax paid 20000

Total 405000 235000 195000 195000 195000 215000

closing (bank overdraft) 50000 -65000 -110000 -95000 -30000 40000

In the above question it is to be concluded that the sassy cloth has over expenses

than the income which gives negative cash balance. In the upcoming 6 months, the organisation

is expecting £1,175,000. They need to minimize their expenses and try to increase its

productivity. They need to find out the sources which provide them cheap resources and

minimize their production cost. This will help in earning more, also the company should improve

their method of production by installing new technology and inventories which helps in doing

the work faster (Karim, Rabbani, and Bawazir, 2022).

c) Clarification of additional disbursements

The company have the to control the payment in the month of July and December

expenses such as software bills, rent, running fees and charge to the suppliers. The company

need to use various facilities of overdraft so that supplier paid on time the is no accumulated debt

that company need to pay back. This helps in maintain a good track with suppliers and other

creditors. The help of financial institution company can get growth and expansion.

QUESTION 3

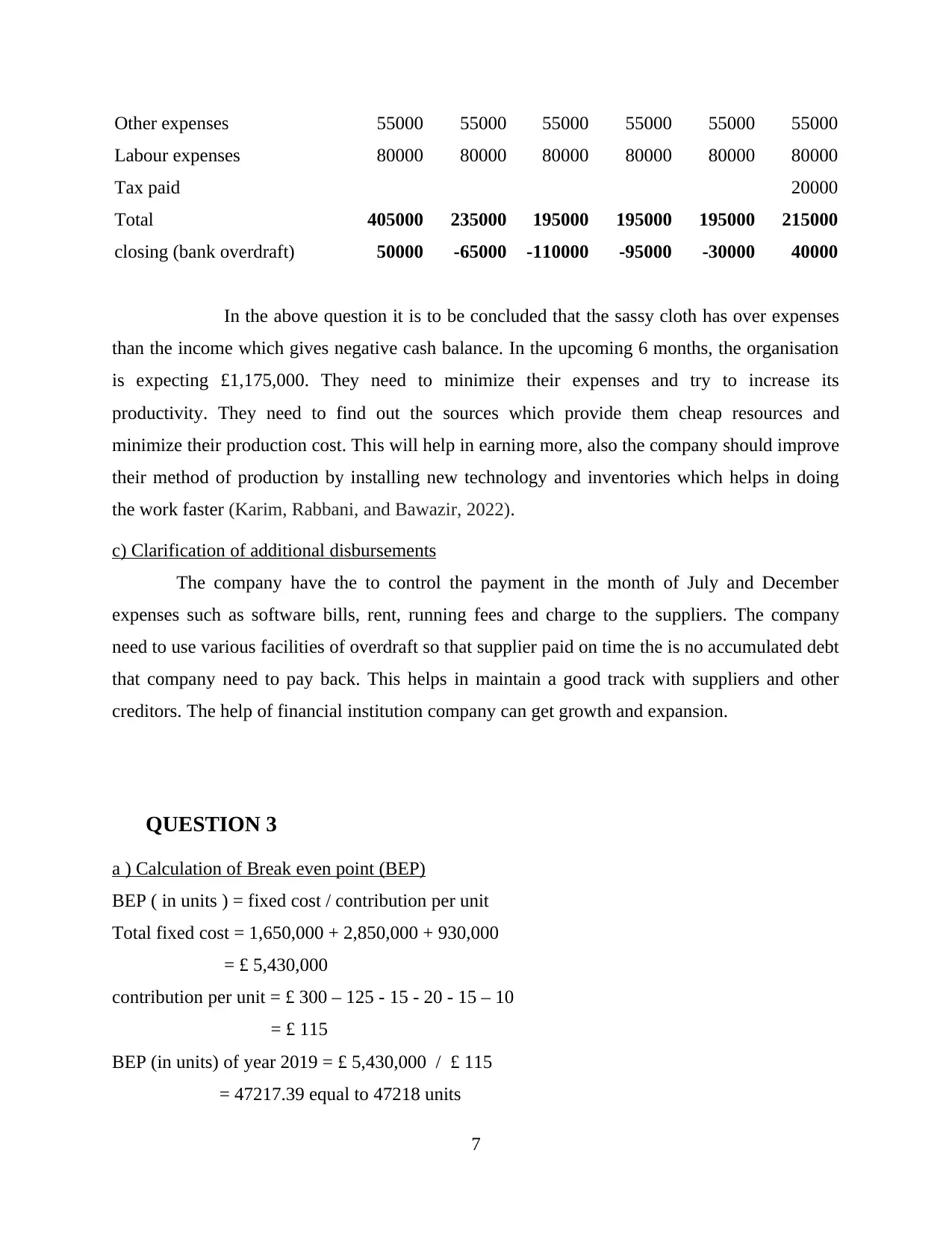

a ) Calculation of Break even point (BEP)

BEP ( in units ) = fixed cost / contribution per unit

Total fixed cost = 1,650,000 + 2,850,000 + 930,000

= £ 5,430,000

contribution per unit = £ 300 – 125 - 15 - 20 - 15 – 10

= £ 115

BEP (in units) of year 2019 = £ 5,430,000 / £ 115

= 47217.39 equal to 47218 units

7

Labour expenses 80000 80000 80000 80000 80000 80000

Tax paid 20000

Total 405000 235000 195000 195000 195000 215000

closing (bank overdraft) 50000 -65000 -110000 -95000 -30000 40000

In the above question it is to be concluded that the sassy cloth has over expenses

than the income which gives negative cash balance. In the upcoming 6 months, the organisation

is expecting £1,175,000. They need to minimize their expenses and try to increase its

productivity. They need to find out the sources which provide them cheap resources and

minimize their production cost. This will help in earning more, also the company should improve

their method of production by installing new technology and inventories which helps in doing

the work faster (Karim, Rabbani, and Bawazir, 2022).

c) Clarification of additional disbursements

The company have the to control the payment in the month of July and December

expenses such as software bills, rent, running fees and charge to the suppliers. The company

need to use various facilities of overdraft so that supplier paid on time the is no accumulated debt

that company need to pay back. This helps in maintain a good track with suppliers and other

creditors. The help of financial institution company can get growth and expansion.

QUESTION 3

a ) Calculation of Break even point (BEP)

BEP ( in units ) = fixed cost / contribution per unit

Total fixed cost = 1,650,000 + 2,850,000 + 930,000

= £ 5,430,000

contribution per unit = £ 300 – 125 - 15 - 20 - 15 – 10

= £ 115

BEP (in units) of year 2019 = £ 5,430,000 / £ 115

= 47217.39 equal to 47218 units

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

BEP (sales revenue ) For the year 2019 = fixed cost / profit volume ratio (P/V)

= 5,430,000 / 38.33 %

= £ 14,166,449.26

for the year 2020, there will be few changes in accordance with chief executive in Income

statement are

Particulars Price per unit Amount ( £ )

Sales 309 13905000

Less : variable cost

Direct material 125 5625000

Direct labour 13 585000

Manufacturing overhead 19.5 877500

Selling expenses 15 675000

Administration expenses 8 360000

CONTRIBUTION 128.5 5782500

Less : fixed cost

Manufacturing overhead 1650000

Selling and distribution overhead 2850000

Administration overhead 930000

New manufacturing facility 1450000

PROFIT -1097500

Break even point (BEP) for the year 2020 in units = fixed cost / contribution per unit

= 6880000 / 128.5

= 53540.86 equivalent to 53541 units

Break even point (BEP) for the year 2020 in sales revenue = fixed cost / Profit volume ratio (p/v)

= 6880000 / 41.59 %

= £ 16542438.09

8

= 5,430,000 / 38.33 %

= £ 14,166,449.26

for the year 2020, there will be few changes in accordance with chief executive in Income

statement are

Particulars Price per unit Amount ( £ )

Sales 309 13905000

Less : variable cost

Direct material 125 5625000

Direct labour 13 585000

Manufacturing overhead 19.5 877500

Selling expenses 15 675000

Administration expenses 8 360000

CONTRIBUTION 128.5 5782500

Less : fixed cost

Manufacturing overhead 1650000

Selling and distribution overhead 2850000

Administration overhead 930000

New manufacturing facility 1450000

PROFIT -1097500

Break even point (BEP) for the year 2020 in units = fixed cost / contribution per unit

= 6880000 / 128.5

= 53540.86 equivalent to 53541 units

Break even point (BEP) for the year 2020 in sales revenue = fixed cost / Profit volume ratio (p/v)

= 6880000 / 41.59 %

= £ 16542438.09

8

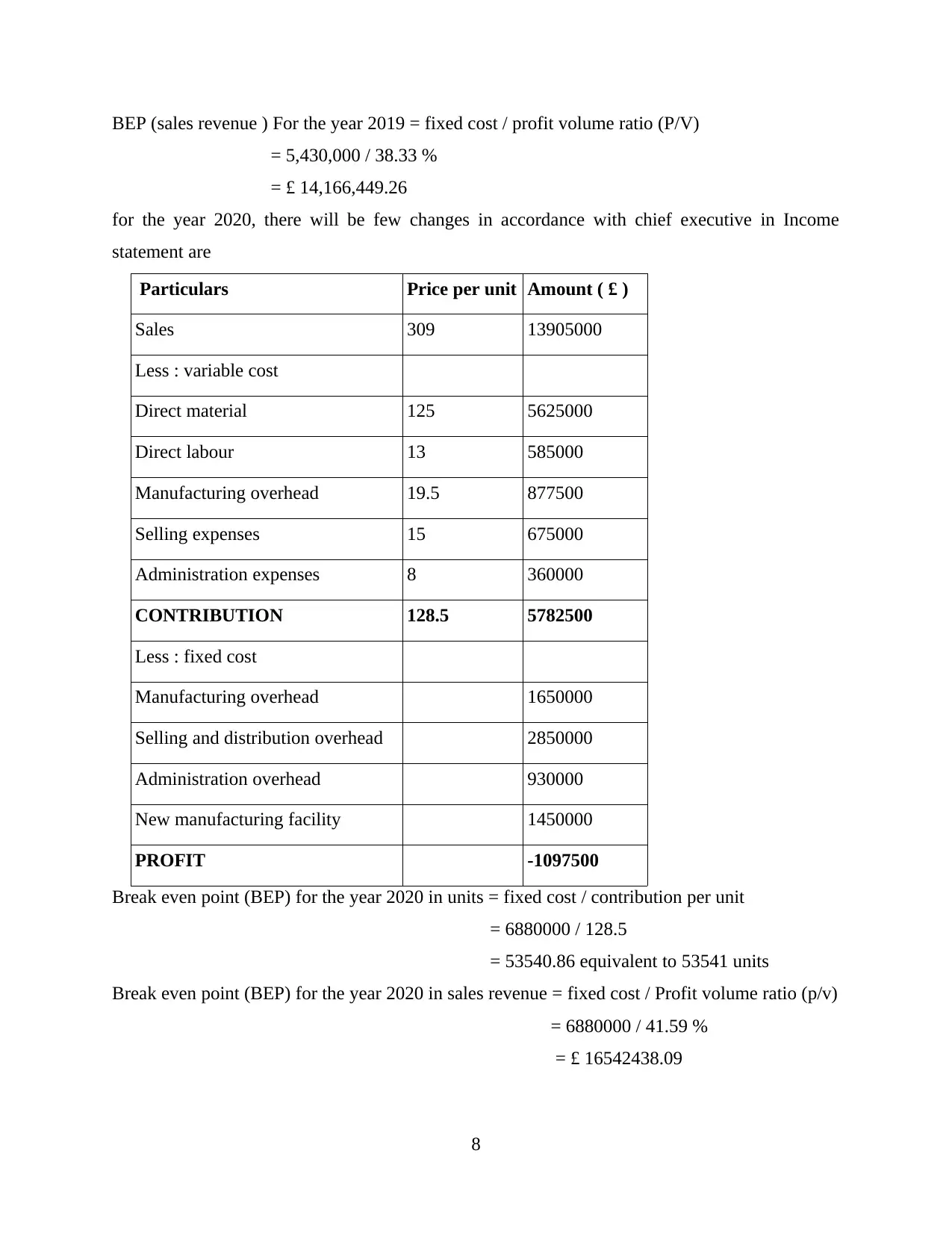

b) Margin of safety ( MOS ) for the year ended 2019 and 2020

MOS in terms of units for the year 2019 = profit / contribution per unit

= -255000 / 115

= - 2217 units

MOS in terms of units for the year 2020 = -1097500 / 128.5

= -8541 units

MOS in terms of sales revenue for the year 2019 = profit / p/v ratio

= -255000 / 38.33 %

= £ - 665275

MOS in terms of sales revenue for the year 2020 = profit / p/v ratio (Morris, 2018)

= -1097500 / 41.59 %

= £-2638855.49

c) Evaluate the new strategies that can be made by Jessica

in the above calculation two strategies have been used for analysis namely BEP AND MOS for

the two consecutive year 2019 and 2020. The results are as follows the breakeven point where

there is no profit nor loss for the year 2019 and 2020 is produced 47218 units and 53541 units

roughly. Margin of safety is negative in both years which mean that company is not earning

enough to cover the cost. Years 2019 and 2020 are -2217 units and -8541 units respectively.

Sales revenue is very less and company need to make efforts towards increasing its productivity

and sales revenue. They have already spent 1450000 in the fixed cost which is not used

effectively company need to work towards it (Poongodi, and et al., 2020).

QUESTION 4

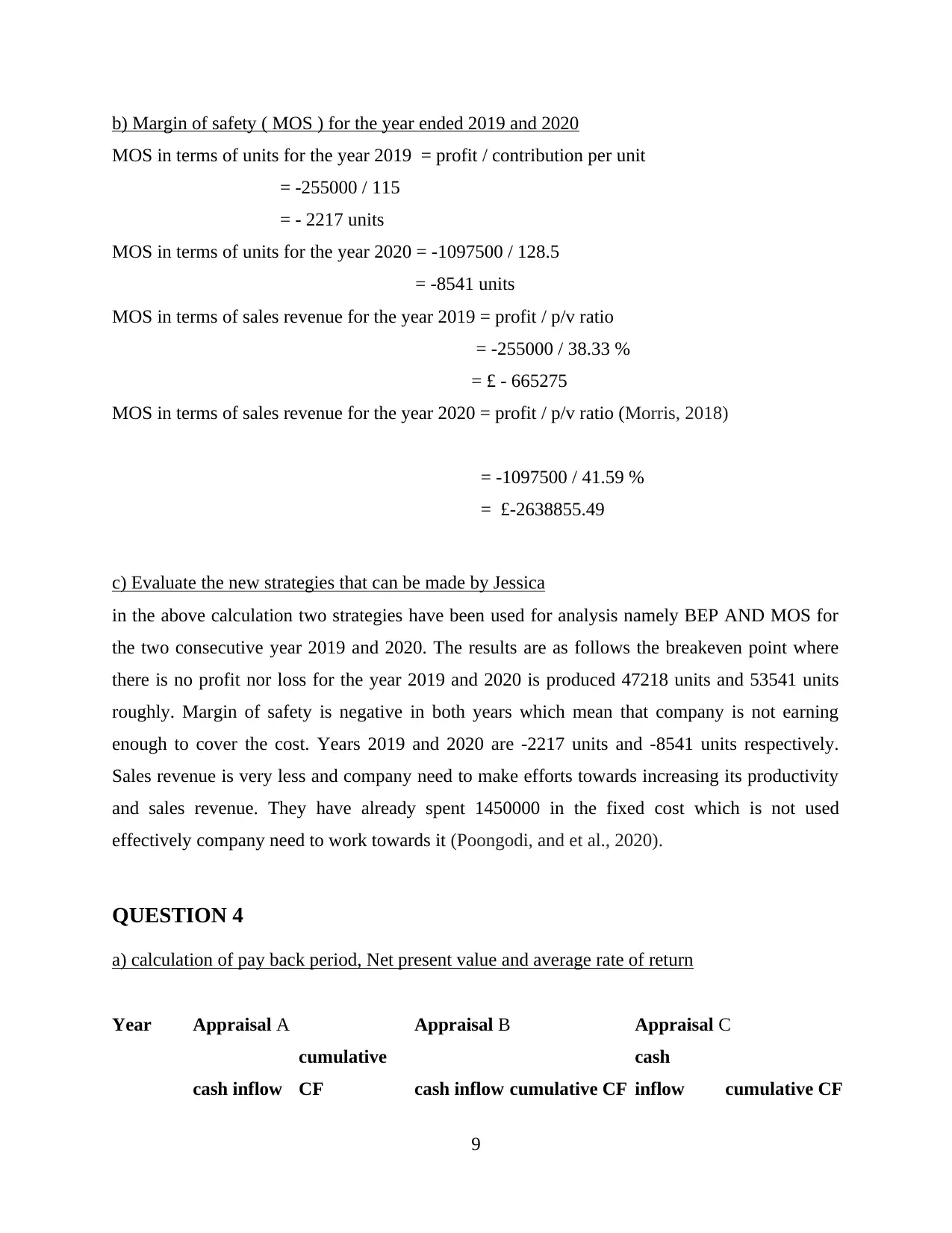

a) calculation of pay back period, Net present value and average rate of return

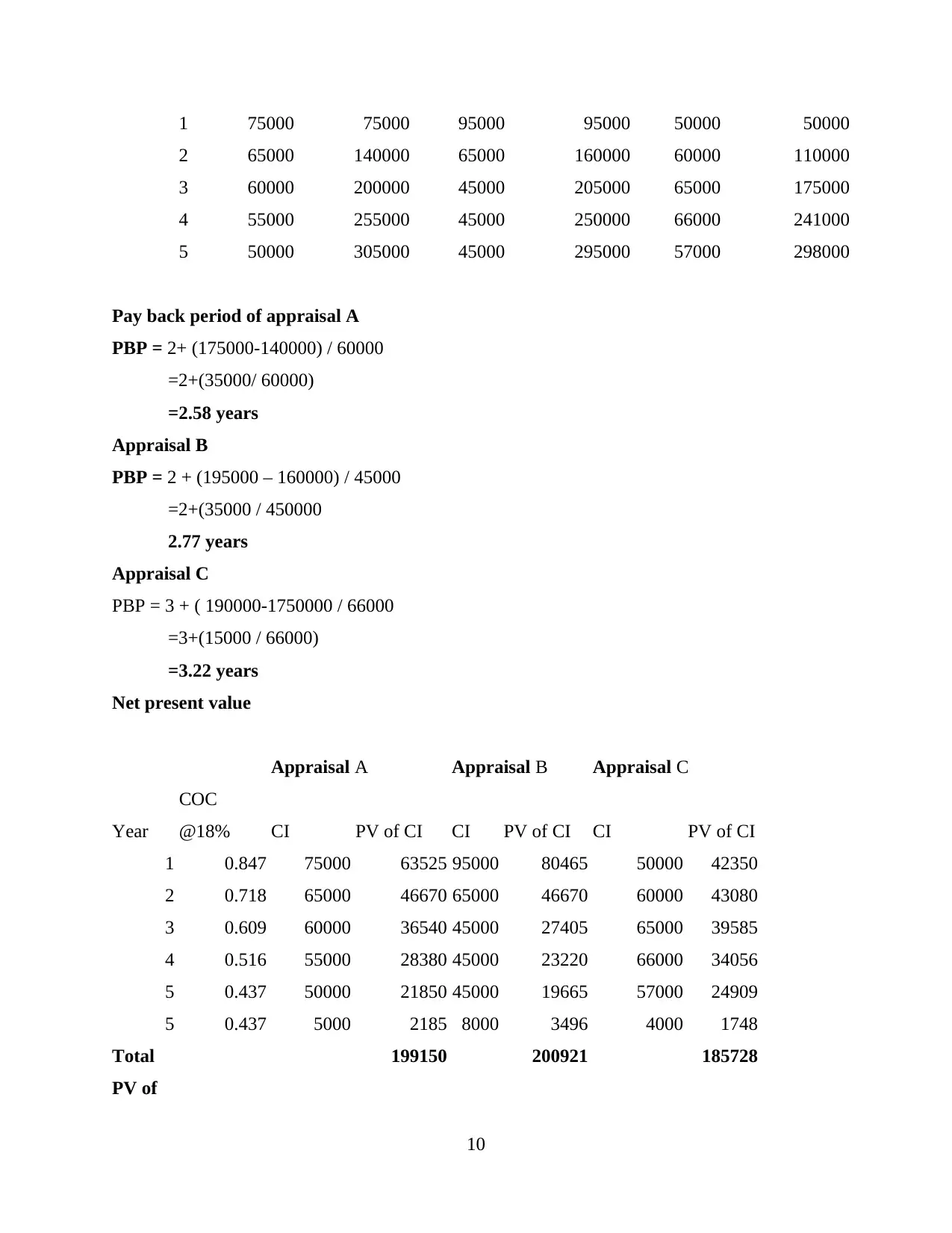

Year Appraisal A Appraisal B Appraisal C

cash inflow

cumulative

CF cash inflow cumulative CF

cash

inflow cumulative CF

9

MOS in terms of units for the year 2019 = profit / contribution per unit

= -255000 / 115

= - 2217 units

MOS in terms of units for the year 2020 = -1097500 / 128.5

= -8541 units

MOS in terms of sales revenue for the year 2019 = profit / p/v ratio

= -255000 / 38.33 %

= £ - 665275

MOS in terms of sales revenue for the year 2020 = profit / p/v ratio (Morris, 2018)

= -1097500 / 41.59 %

= £-2638855.49

c) Evaluate the new strategies that can be made by Jessica

in the above calculation two strategies have been used for analysis namely BEP AND MOS for

the two consecutive year 2019 and 2020. The results are as follows the breakeven point where

there is no profit nor loss for the year 2019 and 2020 is produced 47218 units and 53541 units

roughly. Margin of safety is negative in both years which mean that company is not earning

enough to cover the cost. Years 2019 and 2020 are -2217 units and -8541 units respectively.

Sales revenue is very less and company need to make efforts towards increasing its productivity

and sales revenue. They have already spent 1450000 in the fixed cost which is not used

effectively company need to work towards it (Poongodi, and et al., 2020).

QUESTION 4

a) calculation of pay back period, Net present value and average rate of return

Year Appraisal A Appraisal B Appraisal C

cash inflow

cumulative

CF cash inflow cumulative CF

cash

inflow cumulative CF

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 75000 75000 95000 95000 50000 50000

2 65000 140000 65000 160000 60000 110000

3 60000 200000 45000 205000 65000 175000

4 55000 255000 45000 250000 66000 241000

5 50000 305000 45000 295000 57000 298000

Pay back period of appraisal A

PBP = 2+ (175000-140000) / 60000

=2+(35000/ 60000)

=2.58 years

Appraisal B

PBP = 2 + (195000 – 160000) / 45000

=2+(35000 / 450000

2.77 years

Appraisal C

PBP = 3 + ( 190000-1750000 / 66000

=3+(15000 / 66000)

=3.22 years

Net present value

Appraisal A Appraisal B Appraisal C

Year

COC

@18% CI PV of CI CI PV of CI CI PV of CI

1 0.847 75000 63525 95000 80465 50000 42350

2 0.718 65000 46670 65000 46670 60000 43080

3 0.609 60000 36540 45000 27405 65000 39585

4 0.516 55000 28380 45000 23220 66000 34056

5 0.437 50000 21850 45000 19665 57000 24909

5 0.437 5000 2185 8000 3496 4000 1748

Total

PV of

199150 200921 185728

10

2 65000 140000 65000 160000 60000 110000

3 60000 200000 45000 205000 65000 175000

4 55000 255000 45000 250000 66000 241000

5 50000 305000 45000 295000 57000 298000

Pay back period of appraisal A

PBP = 2+ (175000-140000) / 60000

=2+(35000/ 60000)

=2.58 years

Appraisal B

PBP = 2 + (195000 – 160000) / 45000

=2+(35000 / 450000

2.77 years

Appraisal C

PBP = 3 + ( 190000-1750000 / 66000

=3+(15000 / 66000)

=3.22 years

Net present value

Appraisal A Appraisal B Appraisal C

Year

COC

@18% CI PV of CI CI PV of CI CI PV of CI

1 0.847 75000 63525 95000 80465 50000 42350

2 0.718 65000 46670 65000 46670 60000 43080

3 0.609 60000 36540 45000 27405 65000 39585

4 0.516 55000 28380 45000 23220 66000 34056

5 0.437 50000 21850 45000 19665 57000 24909

5 0.437 5000 2185 8000 3496 4000 1748

Total

PV of

199150 200921 185728

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

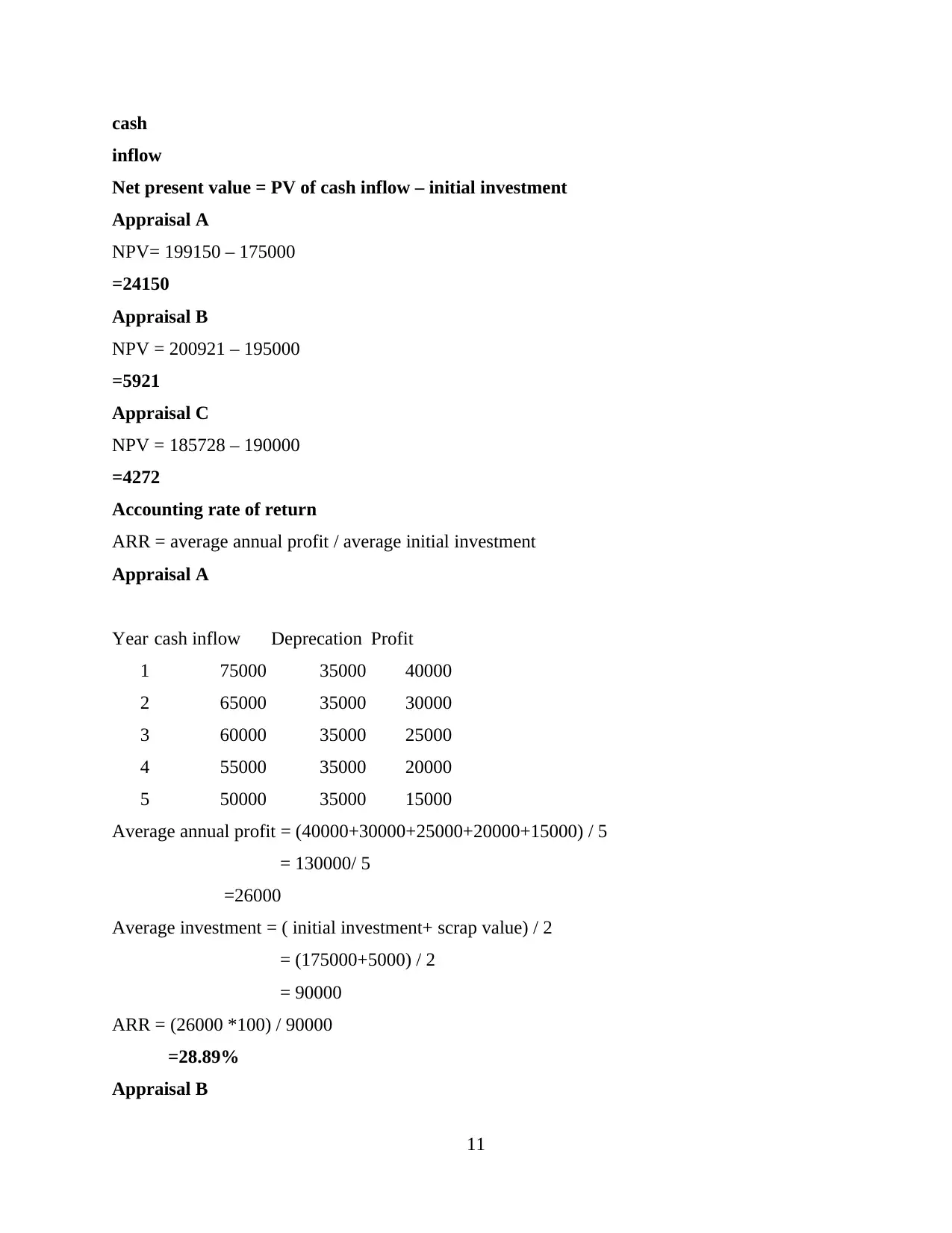

cash

inflow

Net present value = PV of cash inflow – initial investment

Appraisal A

NPV= 199150 – 175000

=24150

Appraisal B

NPV = 200921 – 195000

=5921

Appraisal C

NPV = 185728 – 190000

=4272

Accounting rate of return

ARR = average annual profit / average initial investment

Appraisal A

Year cash inflow Deprecation Profit

1 75000 35000 40000

2 65000 35000 30000

3 60000 35000 25000

4 55000 35000 20000

5 50000 35000 15000

Average annual profit = (40000+30000+25000+20000+15000) / 5

= 130000/ 5

=26000

Average investment = ( initial investment+ scrap value) / 2

= (175000+5000) / 2

= 90000

ARR = (26000 *100) / 90000

=28.89%

Appraisal B

11

inflow

Net present value = PV of cash inflow – initial investment

Appraisal A

NPV= 199150 – 175000

=24150

Appraisal B

NPV = 200921 – 195000

=5921

Appraisal C

NPV = 185728 – 190000

=4272

Accounting rate of return

ARR = average annual profit / average initial investment

Appraisal A

Year cash inflow Deprecation Profit

1 75000 35000 40000

2 65000 35000 30000

3 60000 35000 25000

4 55000 35000 20000

5 50000 35000 15000

Average annual profit = (40000+30000+25000+20000+15000) / 5

= 130000/ 5

=26000

Average investment = ( initial investment+ scrap value) / 2

= (175000+5000) / 2

= 90000

ARR = (26000 *100) / 90000

=28.89%

Appraisal B

11

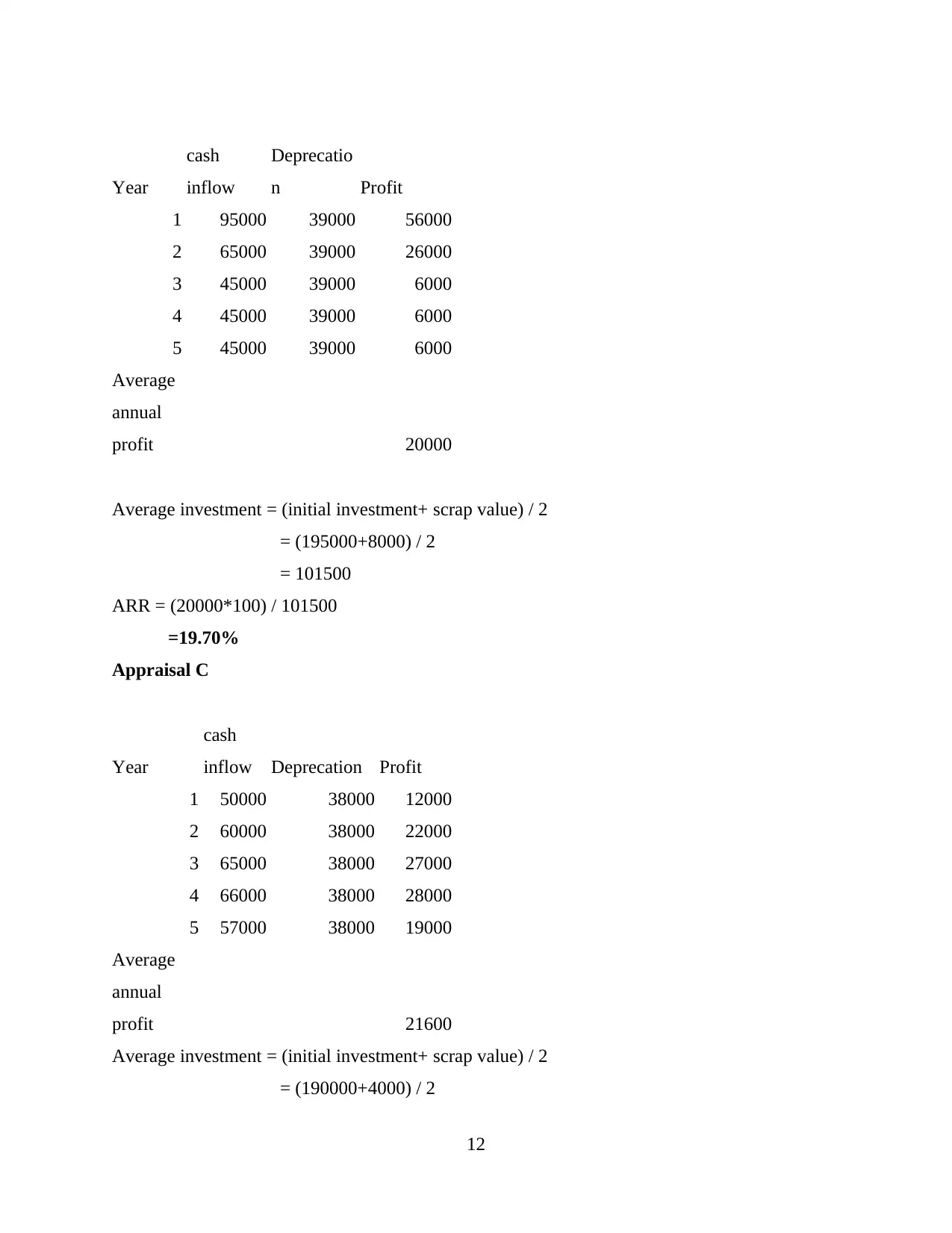

Year

cash

inflow

Deprecatio

n Profit

1 95000 39000 56000

2 65000 39000 26000

3 45000 39000 6000

4 45000 39000 6000

5 45000 39000 6000

Average

annual

profit 20000

Average investment = (initial investment+ scrap value) / 2

= (195000+8000) / 2

= 101500

ARR = (20000*100) / 101500

=19.70%

Appraisal C

Year

cash

inflow Deprecation Profit

1 50000 38000 12000

2 60000 38000 22000

3 65000 38000 27000

4 66000 38000 28000

5 57000 38000 19000

Average

annual

profit 21600

Average investment = (initial investment+ scrap value) / 2

= (190000+4000) / 2

12

cash

inflow

Deprecatio

n Profit

1 95000 39000 56000

2 65000 39000 26000

3 45000 39000 6000

4 45000 39000 6000

5 45000 39000 6000

Average

annual

profit 20000

Average investment = (initial investment+ scrap value) / 2

= (195000+8000) / 2

= 101500

ARR = (20000*100) / 101500

=19.70%

Appraisal C

Year

cash

inflow Deprecation Profit

1 50000 38000 12000

2 60000 38000 22000

3 65000 38000 27000

4 66000 38000 28000

5 57000 38000 19000

Average

annual

profit 21600

Average investment = (initial investment+ scrap value) / 2

= (190000+4000) / 2

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.