Report on the Importance of Financial Management and Analysis

VerifiedAdded on 2022/12/01

|12

|2904

|338

Report

AI Summary

This report examines the critical role of financial management in business operations. It begins by defining financial management and highlighting its significance in areas such as financial planning, fund procurement, and efficient fund utilization. The report then delves into the analysis of financial statements, including income statements, balance sheets, and cash flow statements, emphasizing their importance in assessing a company's financial health and performance. Furthermore, the report explores the use of various financial ratios, such as net profit ratio, gross profit margin, current ratio, and quick ratio, to evaluate a company's profitability and liquidity. The analysis of these ratios provides insights into a company's financial position, enabling informed decision-making and contributing to long-term profitability and growth. The report concludes by emphasizing the importance of financial management as a cornerstone for business success.

Importance of financial

management

management

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Table of Contents

Table of Contents.............................................................................................................................2

INTRODUCTION...........................................................................................................................1

SECTION 1.....................................................................................................................................1

Financial Management and its Importance..................................................................................1

SECTION 2.....................................................................................................................................2

Discussing financial statements and use of ratios........................................................................2

SECTION 3.....................................................................................................................................3

CONCLUSION................................................................................................................................5

REFERENCES................................................................................................................................7

APPENDIX......................................................................................................................................8

Table of Contents.............................................................................................................................2

INTRODUCTION...........................................................................................................................1

SECTION 1.....................................................................................................................................1

Financial Management and its Importance..................................................................................1

SECTION 2.....................................................................................................................................2

Discussing financial statements and use of ratios........................................................................2

SECTION 3.....................................................................................................................................3

CONCLUSION................................................................................................................................5

REFERENCES................................................................................................................................7

APPENDIX......................................................................................................................................8

INTRODUCTION

Business financing refers to the money and credit that a company uses to achieve its

goals and objectives (Fan and Chatterjee, 2019). Finance is essential for companies to supply

products and service to customers from the purchase of raw material. Business financing

comprises the purchase of funds for the purpose of fulfilling business demand. It provides

funding for the need of business operating capital, and also provides funding diversification.

Financial management and market value are included in this study. The financial statement and

use of the ratio for financial reporting are also different.

SECTION 1

Financial Management and its Importance

Financial management is the method of an organization's financing and finance-related

operations being managed. It ensures that funds are available to meet everyday business needs

and that funds are used efficiently. Financial management entails making decisions on

investments, fixed asset purchases, and funding sources, among other things. It aids in the

planning, organisation, and management of financial operations. It also includes decisions on the

return on investment for shareholders. It provides information on the company's benefit, loss,

and costs, allowing managers to make informed decisions. Managers will be able to see where

their company's cash is being spent and will be able to cut down on waste. Financial

management plays an important role in the growth of a company for the following reasons:

Financial Planning: Financial management aids in corporate financial planning. It

entails preparing for business sources, budgets, and funding requirements, among other things. It

aids businesses in preparing for tough situations that arise as a result of environmental changes.

Financial preparation assists businesses in reaching their defined objectives. It has power over

the firm's costs, expenses, credit, and profits.

Procurement of funds: Financial management aids the company in obtaining funds from

less expensive sources that are appropriate for the company's needs. Funds are essential for a

company's operations to run smoothly. It ensures that funds are available when a company needs

them. It is needed for day-to-day operations, acquisition, debt repayment, and the procurement of

raw materials, among other things (Guironnet, Attuyer and Halbert, 2016).

Business financing refers to the money and credit that a company uses to achieve its

goals and objectives (Fan and Chatterjee, 2019). Finance is essential for companies to supply

products and service to customers from the purchase of raw material. Business financing

comprises the purchase of funds for the purpose of fulfilling business demand. It provides

funding for the need of business operating capital, and also provides funding diversification.

Financial management and market value are included in this study. The financial statement and

use of the ratio for financial reporting are also different.

SECTION 1

Financial Management and its Importance

Financial management is the method of an organization's financing and finance-related

operations being managed. It ensures that funds are available to meet everyday business needs

and that funds are used efficiently. Financial management entails making decisions on

investments, fixed asset purchases, and funding sources, among other things. It aids in the

planning, organisation, and management of financial operations. It also includes decisions on the

return on investment for shareholders. It provides information on the company's benefit, loss,

and costs, allowing managers to make informed decisions. Managers will be able to see where

their company's cash is being spent and will be able to cut down on waste. Financial

management plays an important role in the growth of a company for the following reasons:

Financial Planning: Financial management aids in corporate financial planning. It

entails preparing for business sources, budgets, and funding requirements, among other things. It

aids businesses in preparing for tough situations that arise as a result of environmental changes.

Financial preparation assists businesses in reaching their defined objectives. It has power over

the firm's costs, expenses, credit, and profits.

Procurement of funds: Financial management aids the company in obtaining funds from

less expensive sources that are appropriate for the company's needs. Funds are essential for a

company's operations to run smoothly. It ensures that funds are available when a company needs

them. It is needed for day-to-day operations, acquisition, debt repayment, and the procurement of

raw materials, among other things (Guironnet, Attuyer and Halbert, 2016).

Utilisation of funds: Financial management aids a company's manager in making the

best use of funds by allocating funds in an efficient manner. It provides information on fund

distribution, allowing businesses to see where their money is going and lowering business costs.

Financial decisions: Financial management aids managers in making financial decisions

that have an impact on the organization's operations. Financial decisions would have an impact

on other departments of a company because any department's activities need funds. These

choices assist the company in achieving its long-term objectives (Zhu and Chou, 2020).

Increase profitability: Financial management aids in the proper use of funds in order to

maximise a company's profitability. It improves business profitability by controlling costs

through budgetary control, cost analysis, and other tools. It also encourages employees to save,

lowering the cost of borrowing money.

SECTION 2

Discussing financial statements and use of ratios

Financial statements are metrics that aid the organisation in conducting the reporting

period and in providing a complete image of the company's financial situation and success

(Wuebker, Baumgarten and Koderisch, 2017). The following are three forms of financial

statements that aid in the preparation of operations and functions:

Income statements- This statement represents an enterprise's success over time, as well

as the company's productivity and the inputs needed to achieve that result. This is the

profit and loss account, which justifies the company's financial status by displaying

accurate profits and expenditures. This is a crucial aspect of comparing revenues and

expenditures from various fluctuations in operating costs, research and development

costs, and raw material costs that influence the company's results.

Balance sheet- This is a crucial aspect of financial statements because it depicts the

company's final status by depicting a straightforward and precise image of management.

This includes assets and liabilities, as well as equity expressed in monetary terms, both of

which must be equal at the end of the calculations. Some equations demonstrate that

economic resources represented by assets are equivalent to debts and capital. As a result,

according to the basic concept of Asset = Liabilities, the two sides of a balance sheet

must always be identical (Nyagadza, 2019).

best use of funds by allocating funds in an efficient manner. It provides information on fund

distribution, allowing businesses to see where their money is going and lowering business costs.

Financial decisions: Financial management aids managers in making financial decisions

that have an impact on the organization's operations. Financial decisions would have an impact

on other departments of a company because any department's activities need funds. These

choices assist the company in achieving its long-term objectives (Zhu and Chou, 2020).

Increase profitability: Financial management aids in the proper use of funds in order to

maximise a company's profitability. It improves business profitability by controlling costs

through budgetary control, cost analysis, and other tools. It also encourages employees to save,

lowering the cost of borrowing money.

SECTION 2

Discussing financial statements and use of ratios

Financial statements are metrics that aid the organisation in conducting the reporting

period and in providing a complete image of the company's financial situation and success

(Wuebker, Baumgarten and Koderisch, 2017). The following are three forms of financial

statements that aid in the preparation of operations and functions:

Income statements- This statement represents an enterprise's success over time, as well

as the company's productivity and the inputs needed to achieve that result. This is the

profit and loss account, which justifies the company's financial status by displaying

accurate profits and expenditures. This is a crucial aspect of comparing revenues and

expenditures from various fluctuations in operating costs, research and development

costs, and raw material costs that influence the company's results.

Balance sheet- This is a crucial aspect of financial statements because it depicts the

company's final status by depicting a straightforward and precise image of management.

This includes assets and liabilities, as well as equity expressed in monetary terms, both of

which must be equal at the end of the calculations. Some equations demonstrate that

economic resources represented by assets are equivalent to debts and capital. As a result,

according to the basic concept of Asset = Liabilities, the two sides of a balance sheet

must always be identical (Nyagadza, 2019).

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Cash flow statements- This research focuses on the cash receipts and payments made by

a company during a particular time span. This financial statement shows how much

money is going out and coming in from three different types of activities: operating,

investing, and financing. These practises calculate and analyse a company's financial

performance, making it easier for analysts and shareholders to assess the results

accurately. This aids in the making of informed management decisions and the avoidance

of financial risk. This section summarises the cash positions, which indicate how well the

organisation will cover its debt obligations and operating expenses.

Ratios are used to calculate the profitability and liquidity of a company's financials and

encompass a broad range of calculations. The following are some examples of how ratios are

used in financial management:

Helps in comparison- Ratios are very useful in providing an organisation with a

comparison outlook which can assist in taking proactive steps that are needed. This were

scrutinised by shareholders and investors in order to equate previous year's results to

current year's performance (Potrich and Vieira, 2018).

Useful in decision making- They were prepared to assist management in making

effective decisions and taking necessary actions in the business. As they provide useful

information about the company's results, analysts may draw conclusions based on it.

Supports in forecasting and planning- They were extremely helpful in financial

planning and predicting events and roles for the future by estimating the number of years.

These aid in the provision of sufficient information to shareholders and investors in order

for them to formulate their investment strategies. This often gives external parties with an

interest in the business an understanding of the company's financial situation.

SECTION 3

Net profit ratio: The profit margin or simply net margin determines how much net income

or profit as a percentage of the income is earned. It is the ratio of a company's or business

segment's net income to revenues. The net profit margin is generally expressed as a ratio, but it

can also be interpreted as a decimal. The net profit margin shows how much profit a corporation

makes out of dollar of revenue it receives. It is a measure of a company's profitability. It exposes

a company's profitability by subtracting all of the company's expenditures from the revenue

created by sales.

a company during a particular time span. This financial statement shows how much

money is going out and coming in from three different types of activities: operating,

investing, and financing. These practises calculate and analyse a company's financial

performance, making it easier for analysts and shareholders to assess the results

accurately. This aids in the making of informed management decisions and the avoidance

of financial risk. This section summarises the cash positions, which indicate how well the

organisation will cover its debt obligations and operating expenses.

Ratios are used to calculate the profitability and liquidity of a company's financials and

encompass a broad range of calculations. The following are some examples of how ratios are

used in financial management:

Helps in comparison- Ratios are very useful in providing an organisation with a

comparison outlook which can assist in taking proactive steps that are needed. This were

scrutinised by shareholders and investors in order to equate previous year's results to

current year's performance (Potrich and Vieira, 2018).

Useful in decision making- They were prepared to assist management in making

effective decisions and taking necessary actions in the business. As they provide useful

information about the company's results, analysts may draw conclusions based on it.

Supports in forecasting and planning- They were extremely helpful in financial

planning and predicting events and roles for the future by estimating the number of years.

These aid in the provision of sufficient information to shareholders and investors in order

for them to formulate their investment strategies. This often gives external parties with an

interest in the business an understanding of the company's financial situation.

SECTION 3

Net profit ratio: The profit margin or simply net margin determines how much net income

or profit as a percentage of the income is earned. It is the ratio of a company's or business

segment's net income to revenues. The net profit margin is generally expressed as a ratio, but it

can also be interpreted as a decimal. The net profit margin shows how much profit a corporation

makes out of dollar of revenue it receives. It is a measure of a company's profitability. It exposes

a company's profitability by subtracting all of the company's expenditures from the revenue

created by sales.

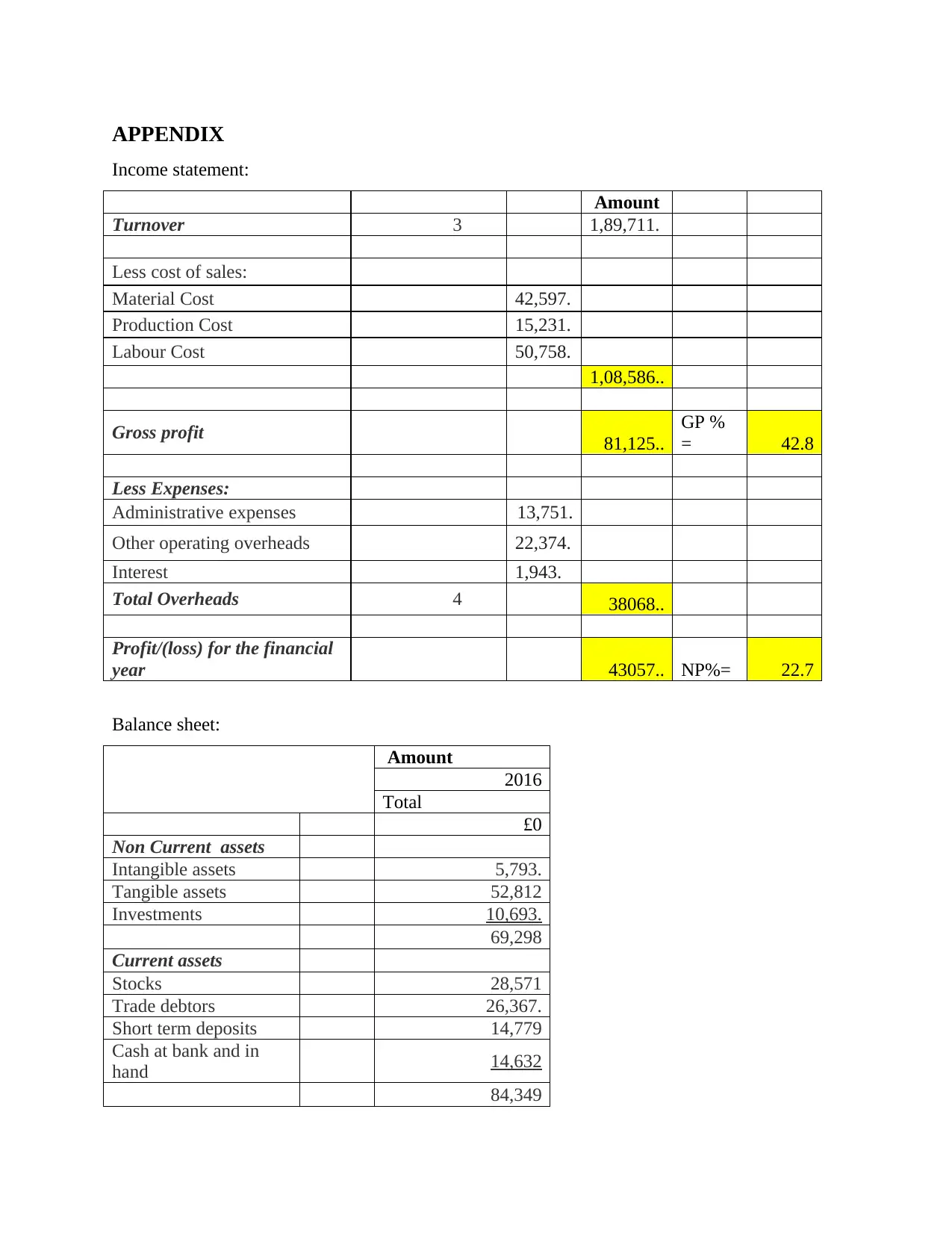

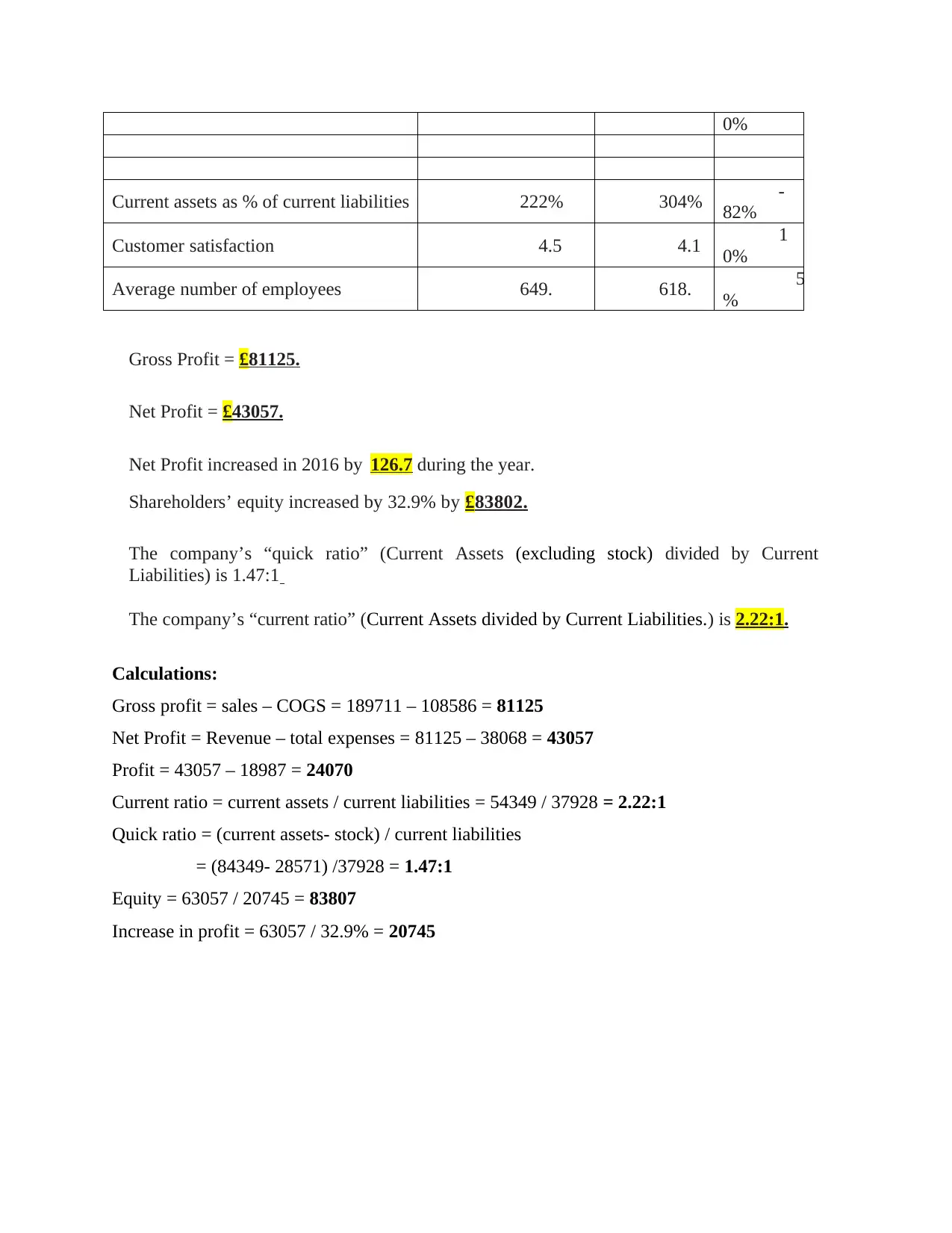

Net profit margin = 43057 / 189711 * 100

= 22.69%

Gross profit: Analysts use gross profit margin to measure a company's financial health

by measuring the amount of money left over after subtracting the cost of products sold from

product revenues (COGS). Gross profit margin is often expressed as a percentage of revenue and

is often referred to as the gross margin ratio. This analytical metric allows an organization's

profit obtained from its core activities to be expressed. It is calculated by subtracting a company's

operating costs from its net revenues.

Gross profit margin= 81125 / 189711 * 100

= 42.76%

Current ratio: The current ratio is a liquidity ratio that assesses a company's ability to

meet its short-term obligations. The current ratio measures a company's liquidity. Current ratios

that are considered acceptable differ by industry. A creditor will prefer a high current ratio to a

low current ratio in many cases because a high current ratio means that the business is more

likely to repay the creditor. For investors, high current ratios aren't necessarily a positive sign. If

a company's current ratio is too high, it can mean that its current assets or short-term lending

facilities are not being used effectively. This liquidity ratio ensures that an organization's

capacity to pay is assessed in the sense of short-term obligations. It includes all existing

liabilities and current assets (Steinhoff, Lewis and Everson, 2018). The current ratio would be

less than one if current liabilities outweigh current assets. If the current ratio is less than one, the

organisation may have difficulty fulfilling its short-term obligations. However, some companies

will function with a current ratio of less than one. If inventory transforms into cash even faster

than accounts payable are due, the company's current ratio will comfortably stay below one.

Inventory is valued at the cost of acquisition, with the company intending to sell it for a higher

price. As a result, the sale would produce far more cash than the inventory value on the balance

sheet. Low current ratios can also be justified by companies that can raise cash from consumers

before paying their suppliers.

Current ratio = Current assets / current liabilities

= 54349 / 37928

= 2.22:1

= 22.69%

Gross profit: Analysts use gross profit margin to measure a company's financial health

by measuring the amount of money left over after subtracting the cost of products sold from

product revenues (COGS). Gross profit margin is often expressed as a percentage of revenue and

is often referred to as the gross margin ratio. This analytical metric allows an organization's

profit obtained from its core activities to be expressed. It is calculated by subtracting a company's

operating costs from its net revenues.

Gross profit margin= 81125 / 189711 * 100

= 42.76%

Current ratio: The current ratio is a liquidity ratio that assesses a company's ability to

meet its short-term obligations. The current ratio measures a company's liquidity. Current ratios

that are considered acceptable differ by industry. A creditor will prefer a high current ratio to a

low current ratio in many cases because a high current ratio means that the business is more

likely to repay the creditor. For investors, high current ratios aren't necessarily a positive sign. If

a company's current ratio is too high, it can mean that its current assets or short-term lending

facilities are not being used effectively. This liquidity ratio ensures that an organization's

capacity to pay is assessed in the sense of short-term obligations. It includes all existing

liabilities and current assets (Steinhoff, Lewis and Everson, 2018). The current ratio would be

less than one if current liabilities outweigh current assets. If the current ratio is less than one, the

organisation may have difficulty fulfilling its short-term obligations. However, some companies

will function with a current ratio of less than one. If inventory transforms into cash even faster

than accounts payable are due, the company's current ratio will comfortably stay below one.

Inventory is valued at the cost of acquisition, with the company intending to sell it for a higher

price. As a result, the sale would produce far more cash than the inventory value on the balance

sheet. Low current ratios can also be justified by companies that can raise cash from consumers

before paying their suppliers.

Current ratio = Current assets / current liabilities

= 54349 / 37928

= 2.22:1

Quick ratio: The fast ratio is a measure of a company's ability to fulfil short-term

obligations with its most liquid assets and is an indication of its short-term liquidity status. It's

also known as the acid test ratio because it shows a company's ability to pay down current

liabilities rapidly using near-cash assets (assets that can be converted quickly to cash). A fast test

designed to produce instant results is referred to as an "acid test." It shows a company's short-

term liquidity status and allows for the calculation of a company's ability to pay off short-term

debt. It's also known as the acid test ratio. A good short ratio is one to one. Liquidity ratio is a

measurement of an organization's liquidity status.

Quick ratio = (Current assets – inventory) / current liabilities

= (84349 – 28571) / 37928

= 1.47: 1

According to the above ratio review, an organization's productivity level is producing a

high level of profitability in relation to its core operations. It can be claimed by examining an

enterprise's gross profit margin, as the company generates a high gross profit margin. In the other

hand, the company has to improve its net profit margin, which can be measured by reducing

excessive expenditures. Aside from that, a company's financial condition is sound. As a result,

the company must improve its productivity by minimising unnecessary costs and maintaining

proper financial control, which allows the company to improve its business proficiency level

(Tang, 2017).

CONCLUSION

The above study concludes that financial management is a business's lifeline. It denotes

the practise of controlling or handling an organization's financial operations. Finance

management allows an organization's success to be assessed. This approach combines a number

of finance-related roles, including fixed asset management, revenue identification, accounting,

and payment processing. Furthermore, financial statements provide an analysis of an entity's

financial situation. A financial statement gives a summary of a company's financial health. It

refers to a structured record that details a company's financial activities. It contains all finance-

related information that is applicable to companies. As a result, financial statements assist a

company in formulating successful methods for improving a firm's financial position.

Furthermore, financial statement computation allows an organization's management team to

make well-informed decisions, which helps the company improve its performance and achieve

obligations with its most liquid assets and is an indication of its short-term liquidity status. It's

also known as the acid test ratio because it shows a company's ability to pay down current

liabilities rapidly using near-cash assets (assets that can be converted quickly to cash). A fast test

designed to produce instant results is referred to as an "acid test." It shows a company's short-

term liquidity status and allows for the calculation of a company's ability to pay off short-term

debt. It's also known as the acid test ratio. A good short ratio is one to one. Liquidity ratio is a

measurement of an organization's liquidity status.

Quick ratio = (Current assets – inventory) / current liabilities

= (84349 – 28571) / 37928

= 1.47: 1

According to the above ratio review, an organization's productivity level is producing a

high level of profitability in relation to its core operations. It can be claimed by examining an

enterprise's gross profit margin, as the company generates a high gross profit margin. In the other

hand, the company has to improve its net profit margin, which can be measured by reducing

excessive expenditures. Aside from that, a company's financial condition is sound. As a result,

the company must improve its productivity by minimising unnecessary costs and maintaining

proper financial control, which allows the company to improve its business proficiency level

(Tang, 2017).

CONCLUSION

The above study concludes that financial management is a business's lifeline. It denotes

the practise of controlling or handling an organization's financial operations. Finance

management allows an organization's success to be assessed. This approach combines a number

of finance-related roles, including fixed asset management, revenue identification, accounting,

and payment processing. Furthermore, financial statements provide an analysis of an entity's

financial situation. A financial statement gives a summary of a company's financial health. It

refers to a structured record that details a company's financial activities. It contains all finance-

related information that is applicable to companies. As a result, financial statements assist a

company in formulating successful methods for improving a firm's financial position.

Furthermore, financial statement computation allows an organization's management team to

make well-informed decisions, which helps the company improve its performance and achieve

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

long-term profitability and growth. The balance sheet, income statement, and cash flow

statement are all examples of financial statements. Apart from that, ratio analysis aids an

organisation in assessing an entity's liquidity, profitability, organisational, and efficiency levels

in order to assess its success and productivity.

statement are all examples of financial statements. Apart from that, ratio analysis aids an

organisation in assessing an entity's liquidity, profitability, organisational, and efficiency levels

in order to assess its success and productivity.

REFERENCES

Books and Journal

Fan, L. and Chatterjee, S., 2019. Financial socialization, financial education, and student loan

debt. Journal of Family and Economic Issues, 40(1), pp.74-85.

Guironnet, A., Attuyer, K. and Halbert, L., 2016. Building cities on financial assets: The

financialisation of property markets and its implications for city governments in the

Paris city-region. Urban Studies, 53(7), pp.1442-1464.

Nyagadza, B., 2019. Conceptual model for financial inclusion development through agency

banking in competitive markets. Africanus, 49(2), pp.1-22.

Potrich, A.C.G. and Vieira, K.M., 2018. Demystifying financial literacy: a behavioral

perspective analysis. Management Research Review.

Steinhoff, J.C., Lewis, A.C. and Everson, K.E., 2018. The march of the robots. The Journal of

Government Financial Management, 67(1), p.26.

Tang, N., 2017. Like father like son: how does parents' financial behavior affect their children's

financial behavior?. Journal of Consumer Affairs, 51(2), pp.284-311.

Wuebker, G., Baumgarten, J. and Koderisch, M., 2017. Price management in Financial services:

Smart strategies for growth. Routledge.

Zhu, A.Y.F. and Chou, K.L., 2020. Financial literacy among Hong Kong’s Chinese Adolescents:

Testing the validity of a scale and evaluating two conceptual models. Youth & Society,

52(4), pp.548-573.

Books and Journal

Fan, L. and Chatterjee, S., 2019. Financial socialization, financial education, and student loan

debt. Journal of Family and Economic Issues, 40(1), pp.74-85.

Guironnet, A., Attuyer, K. and Halbert, L., 2016. Building cities on financial assets: The

financialisation of property markets and its implications for city governments in the

Paris city-region. Urban Studies, 53(7), pp.1442-1464.

Nyagadza, B., 2019. Conceptual model for financial inclusion development through agency

banking in competitive markets. Africanus, 49(2), pp.1-22.

Potrich, A.C.G. and Vieira, K.M., 2018. Demystifying financial literacy: a behavioral

perspective analysis. Management Research Review.

Steinhoff, J.C., Lewis, A.C. and Everson, K.E., 2018. The march of the robots. The Journal of

Government Financial Management, 67(1), p.26.

Tang, N., 2017. Like father like son: how does parents' financial behavior affect their children's

financial behavior?. Journal of Consumer Affairs, 51(2), pp.284-311.

Wuebker, G., Baumgarten, J. and Koderisch, M., 2017. Price management in Financial services:

Smart strategies for growth. Routledge.

Zhu, A.Y.F. and Chou, K.L., 2020. Financial literacy among Hong Kong’s Chinese Adolescents:

Testing the validity of a scale and evaluating two conceptual models. Youth & Society,

52(4), pp.548-573.

APPENDIX

Income statement:

Amount

Turnover 3 1,89,711.

Less cost of sales:

Material Cost 42,597.

Production Cost 15,231.

Labour Cost 50,758.

1,08,586..

Gross profit 81,125..

GP %

= 42.8

Less Expenses:

Administrative expenses 13,751.

Other operating overheads 22,374.

Interest 1,943.

Total Overheads 4 38068..

Profit/(loss) for the financial

year 43057.. NP%= 22.7

Balance sheet:

Amount

2016

Total

£0

Non Current assets

Intangible assets 5,793.

Tangible assets 52,812

Investments 10,693.

69,298

Current assets

Stocks 28,571

Trade debtors 26,367.

Short term deposits 14,779

Cash at bank and in

hand 14,632

84,349

Income statement:

Amount

Turnover 3 1,89,711.

Less cost of sales:

Material Cost 42,597.

Production Cost 15,231.

Labour Cost 50,758.

1,08,586..

Gross profit 81,125..

GP %

= 42.8

Less Expenses:

Administrative expenses 13,751.

Other operating overheads 22,374.

Interest 1,943.

Total Overheads 4 38068..

Profit/(loss) for the financial

year 43057.. NP%= 22.7

Balance sheet:

Amount

2016

Total

£0

Non Current assets

Intangible assets 5,793.

Tangible assets 52,812

Investments 10,693.

69,298

Current assets

Stocks 28,571

Trade debtors 26,367.

Short term deposits 14,779

Cash at bank and in

hand 14,632

84,349

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Current liabilities

Bank loans and

overdrafts 9,610.

Trade creditors 19,493

Other Creditors 678

Income tax payable 3,585.

Other creditors

including tax and social

security

4,562

37,928.

working capital 46,421

Total assets less

current liabilities 1,15,719.

Non-Current

Liabilities

Bank loans and

overdrafts 16,506

Other Liabilities 7,304

23,810.

Provisions for

liabilities 8,094.

Net assets 83,815

Capital and reserves

Called up share capital 39,436

Reserves 1322.

Retained earnings 43,057

Total equity 83,802

Business review:

2016 2015 Change

£’000 £’000 %

Turnover (continuing operations) 1,89,711. 1,79,587. 5.60

%

Profit for the financial year 43057 18,987 126.7%

Shareholder’s equity 83802. 63,057 32.9

Bank loans and

overdrafts 9,610.

Trade creditors 19,493

Other Creditors 678

Income tax payable 3,585.

Other creditors

including tax and social

security

4,562

37,928.

working capital 46,421

Total assets less

current liabilities 1,15,719.

Non-Current

Liabilities

Bank loans and

overdrafts 16,506

Other Liabilities 7,304

23,810.

Provisions for

liabilities 8,094.

Net assets 83,815

Capital and reserves

Called up share capital 39,436

Reserves 1322.

Retained earnings 43,057

Total equity 83,802

Business review:

2016 2015 Change

£’000 £’000 %

Turnover (continuing operations) 1,89,711. 1,79,587. 5.60

%

Profit for the financial year 43057 18,987 126.7%

Shareholder’s equity 83802. 63,057 32.9

0%

Current assets as % of current liabilities 222% 304% -

82%

Customer satisfaction 4.5 4.1 1

0%

Average number of employees 649. 618. 5

%

Gross Profit = £81125.

Net Profit = £43057.

Net Profit increased in 2016 by 126.7 during the year.

Shareholders’ equity increased by 32.9% by £83802.

The company’s “quick ratio” (Current Assets (excluding stock) divided by Current

Liabilities) is 1.47:1

The company’s “current ratio” (Current Assets divided by Current Liabilities.) is 2.22:1.

Calculations:

Gross profit = sales – COGS = 189711 – 108586 = 81125

Net Profit = Revenue – total expenses = 81125 – 38068 = 43057

Profit = 43057 – 18987 = 24070

Current ratio = current assets / current liabilities = 54349 / 37928 = 2.22:1

Quick ratio = (current assets- stock) / current liabilities

= (84349- 28571) /37928 = 1.47:1

Equity = 63057 / 20745 = 83807

Increase in profit = 63057 / 32.9% = 20745

Current assets as % of current liabilities 222% 304% -

82%

Customer satisfaction 4.5 4.1 1

0%

Average number of employees 649. 618. 5

%

Gross Profit = £81125.

Net Profit = £43057.

Net Profit increased in 2016 by 126.7 during the year.

Shareholders’ equity increased by 32.9% by £83802.

The company’s “quick ratio” (Current Assets (excluding stock) divided by Current

Liabilities) is 1.47:1

The company’s “current ratio” (Current Assets divided by Current Liabilities.) is 2.22:1.

Calculations:

Gross profit = sales – COGS = 189711 – 108586 = 81125

Net Profit = Revenue – total expenses = 81125 – 38068 = 43057

Profit = 43057 – 18987 = 24070

Current ratio = current assets / current liabilities = 54349 / 37928 = 2.22:1

Quick ratio = (current assets- stock) / current liabilities

= (84349- 28571) /37928 = 1.47:1

Equity = 63057 / 20745 = 83807

Increase in profit = 63057 / 32.9% = 20745

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.