Evaluating Audit Opinions via Internal Controls and Procedures

VerifiedAdded on 2022/12/29

|13

|3423

|47

Report

AI Summary

This report provides an overview of the importance of internal controls and audit procedures in the context of forming an audit opinion. It begins with an introduction to auditing, highlighting its purpose and importance in ensuring the credibility of financial statements. The report then delves into the significance of internal control and risk management, discussing the objectives and components of internal control, including risk assessment, control activities, and monitoring. It also explains the role of risk registers in identifying and mitigating potential risks. Furthermore, the report assesses audit procedures for obtaining audit evidence, such as tests of control and substantive procedures, and explores various methods used by auditors to gather evidence, including inspection of assets and documents, observation, and inquiry. Finally, the report examines the basic elements of an audit report, including the factors considered by auditors when forming an opinion, and discusses unmodified and modified audit opinions, as well as audit procedures for identifying subsequent events.

Importance of Internal controls

and audit procedures to conclude

audit opinion

1

and audit procedures to conclude

audit opinion

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Executive Summary

This report is aimed at highlighting various procedures and aspects related to internal

control. It also aims at discussing aspects related to audit report in which auditors express their

opinions related to their assessment of the financial statements of the entity. This report discusses

all concepts in accordance with the auditing standards prescribed by the International Standards

on Auditing (ISA) and includes discussion about auditing, internal control and its components,

risk management and risk register, audit evidence procedures, elements of audit report and audit

procedures to identify subsequent events. This report determines various concepts and their

theoretical understanding in combination with practical examples to clearly grasp the

aforementioned concepts related to auditing.

2

This report is aimed at highlighting various procedures and aspects related to internal

control. It also aims at discussing aspects related to audit report in which auditors express their

opinions related to their assessment of the financial statements of the entity. This report discusses

all concepts in accordance with the auditing standards prescribed by the International Standards

on Auditing (ISA) and includes discussion about auditing, internal control and its components,

risk management and risk register, audit evidence procedures, elements of audit report and audit

procedures to identify subsequent events. This report determines various concepts and their

theoretical understanding in combination with practical examples to clearly grasp the

aforementioned concepts related to auditing.

2

Table of Contents

Executive Summary.........................................................................................................................2

Chapter 1: Introduction....................................................................................................................4

Chapter 2: Understand how to carry out tests and collect audit evidence.......................................4

2.1 Importance of internal control and risk management.......................................................4

2.2 Assessment of audit procedures to obtain audit evidence................................................6

Chapter 3: Understanding how to carry-out evaluation and preparation audit reporting................8

3.1 Basic element of Audit report...........................................................................................8

3.2 Audit procedures to identify subsequent events.............................................................10

Chapter 4: Conclusion....................................................................................................................12

Chapter 5: References....................................................................................................................13

3

Executive Summary.........................................................................................................................2

Chapter 1: Introduction....................................................................................................................4

Chapter 2: Understand how to carry out tests and collect audit evidence.......................................4

2.1 Importance of internal control and risk management.......................................................4

2.2 Assessment of audit procedures to obtain audit evidence................................................6

Chapter 3: Understanding how to carry-out evaluation and preparation audit reporting................8

3.1 Basic element of Audit report...........................................................................................8

3.2 Audit procedures to identify subsequent events.............................................................10

Chapter 4: Conclusion....................................................................................................................12

Chapter 5: References....................................................................................................................13

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Chapter 1: Introduction

Audit refers to assessment of statements, reports, processes, etc. related to an organisation

to produce opinion on fair and accurate representation of business records. In usual business

sense, audit refers to examination of financial statements of the business organisation. However,

auditor needs to assess some non-financial information as well to identify the impact of non-

financial factors over the financial statements of the business, to present a holistic audit report.

Purpose of audit is to obtain a view that whether all the financial transactions of the business in

the specified period are properly recorded or not and whether all the information presented in

financial statements is according to the defined standards or not (Abernathy and et.al., 2017).

Those standards are either defined or approved by government body such as International

Standards on Auditing (ISA). Audit can be conducted by both internal auditor who is employee

of the company or by external auditor. Scope of internal auditor is much wider than external

auditor, who relies on the data provided by internal auditor and management of the company to

conduct examination and develop a report. Therefore, external audit must be conducted by an

independent party i.e. auditor needs to be someone who is not related to the business, so as to not

have a biased audit report.

Importance of auditing

Audit is important as it is aimed at ensuring credibility of financial statements. Audit

report helps in having a detailed overview as well as additional perspective of an external party

to improve business processes. It helps company becoming more reliable in the eyes of investors

and promote its accountability to improve its credit rating in the market. Internal audit report acts

as tool for management to identify the lags in their processes and room for improvement. Audit

report by external auditors is very important for all the stakeholders (Bhasin, 2015). For

example, it is used by shareholders to ensure that information provided by company is true, fair

and accurate and by management as a legal evidence to shareholders, creditors, government, etc.

Chapter 2: Understand how to carry out tests and collect audit evidence

2.1 Importance of internal control and risk management

Internal Control and its objectives

Internal control refers to those rules, regulations, mechanisms and procedures which are

put in place by a company to ensure integrity and accountability of the information, processes,

4

Audit refers to assessment of statements, reports, processes, etc. related to an organisation

to produce opinion on fair and accurate representation of business records. In usual business

sense, audit refers to examination of financial statements of the business organisation. However,

auditor needs to assess some non-financial information as well to identify the impact of non-

financial factors over the financial statements of the business, to present a holistic audit report.

Purpose of audit is to obtain a view that whether all the financial transactions of the business in

the specified period are properly recorded or not and whether all the information presented in

financial statements is according to the defined standards or not (Abernathy and et.al., 2017).

Those standards are either defined or approved by government body such as International

Standards on Auditing (ISA). Audit can be conducted by both internal auditor who is employee

of the company or by external auditor. Scope of internal auditor is much wider than external

auditor, who relies on the data provided by internal auditor and management of the company to

conduct examination and develop a report. Therefore, external audit must be conducted by an

independent party i.e. auditor needs to be someone who is not related to the business, so as to not

have a biased audit report.

Importance of auditing

Audit is important as it is aimed at ensuring credibility of financial statements. Audit

report helps in having a detailed overview as well as additional perspective of an external party

to improve business processes. It helps company becoming more reliable in the eyes of investors

and promote its accountability to improve its credit rating in the market. Internal audit report acts

as tool for management to identify the lags in their processes and room for improvement. Audit

report by external auditors is very important for all the stakeholders (Bhasin, 2015). For

example, it is used by shareholders to ensure that information provided by company is true, fair

and accurate and by management as a legal evidence to shareholders, creditors, government, etc.

Chapter 2: Understand how to carry out tests and collect audit evidence

2.1 Importance of internal control and risk management

Internal Control and its objectives

Internal control refers to those rules, regulations, mechanisms and procedures which are

put in place by a company to ensure integrity and accountability of the information, processes,

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

personnel and resources of the company. It is to be designed, implemented and maintained by

management of the company in compliance with the applicable internal policies, laws and

regulations. Internal control measures are aimed at enhancing reliability of financial reporting

and effectiveness of company's operational processes and therefore includes maintaining proper

records that highlights timely flow of complete information (Cao, Chychyla and Stewart, 2015).

Objectives of putting in place mechanisms of internal control are to ensure effectiveness

of company resources in conducting business as well as prevention and timely detection of fraud

and other unlawful acts. All such controls help in timely preparation of financial statements and

other financial records with completeness and accuracy. Further, it also helps in safeguarding

assets of the company.

Risk management in auditing

Risks refers to those events or actions that are capable of impacting business, its

processes, objectives and strategies adversely. Process of identification and assessment of these

risks within the company comes under risk management process and is basically entrusted to

internal auditors. Auditors are responsible to identify and examine the risk of significant nature

in the financial statements of the company. Auditors are to identify such risk through developing

understanding of the entity and internal control measures deployed within environment of the

company. They not only document such risks in the critical business processes and internal

control but also helps management in developing risk mitigation strategies. These risks are

measured in terms of consequences and likelihood. This process by auditors enable management

to prevent loss of resources, avoid damage to its reputations and several other consequences.

Components of internal control

Risk Assessment process – ISA 315 states that it is duty of auditor to identify and

understand whether organisation has a developed process for business risks identification,

estimating its significance, assessing likelihood of its occurrence and the actions required

to be taken on it. If such process is not there in company, auditor must discuss with

management what process they follow and what they should follow (Jamei, Ranjouri and

Mohammadi Kelareh, 2019).

Control activities – ISA 315 states that auditor shall develop an understanding of the

process adopted by the company relevant to the control activities to prevent, detect and

correct errors, with regards to audit and the responses of the organisation for those risks.

5

management of the company in compliance with the applicable internal policies, laws and

regulations. Internal control measures are aimed at enhancing reliability of financial reporting

and effectiveness of company's operational processes and therefore includes maintaining proper

records that highlights timely flow of complete information (Cao, Chychyla and Stewart, 2015).

Objectives of putting in place mechanisms of internal control are to ensure effectiveness

of company resources in conducting business as well as prevention and timely detection of fraud

and other unlawful acts. All such controls help in timely preparation of financial statements and

other financial records with completeness and accuracy. Further, it also helps in safeguarding

assets of the company.

Risk management in auditing

Risks refers to those events or actions that are capable of impacting business, its

processes, objectives and strategies adversely. Process of identification and assessment of these

risks within the company comes under risk management process and is basically entrusted to

internal auditors. Auditors are responsible to identify and examine the risk of significant nature

in the financial statements of the company. Auditors are to identify such risk through developing

understanding of the entity and internal control measures deployed within environment of the

company. They not only document such risks in the critical business processes and internal

control but also helps management in developing risk mitigation strategies. These risks are

measured in terms of consequences and likelihood. This process by auditors enable management

to prevent loss of resources, avoid damage to its reputations and several other consequences.

Components of internal control

Risk Assessment process – ISA 315 states that it is duty of auditor to identify and

understand whether organisation has a developed process for business risks identification,

estimating its significance, assessing likelihood of its occurrence and the actions required

to be taken on it. If such process is not there in company, auditor must discuss with

management what process they follow and what they should follow (Jamei, Ranjouri and

Mohammadi Kelareh, 2019).

Control activities – ISA 315 states that auditor shall develop an understanding of the

process adopted by the company relevant to the control activities to prevent, detect and

correct errors, with regards to audit and the responses of the organisation for those risks.

5

Monitoring of controls – It is the process that assesses the effectiveness of performance

of internal control measures placed by the entity. It includes timely assessment of the

operations and taking necessary corrective measures required to mitigate risks and

likelihood of its occurrence (Khelil, Hussainey and Noubbigh, 2016).

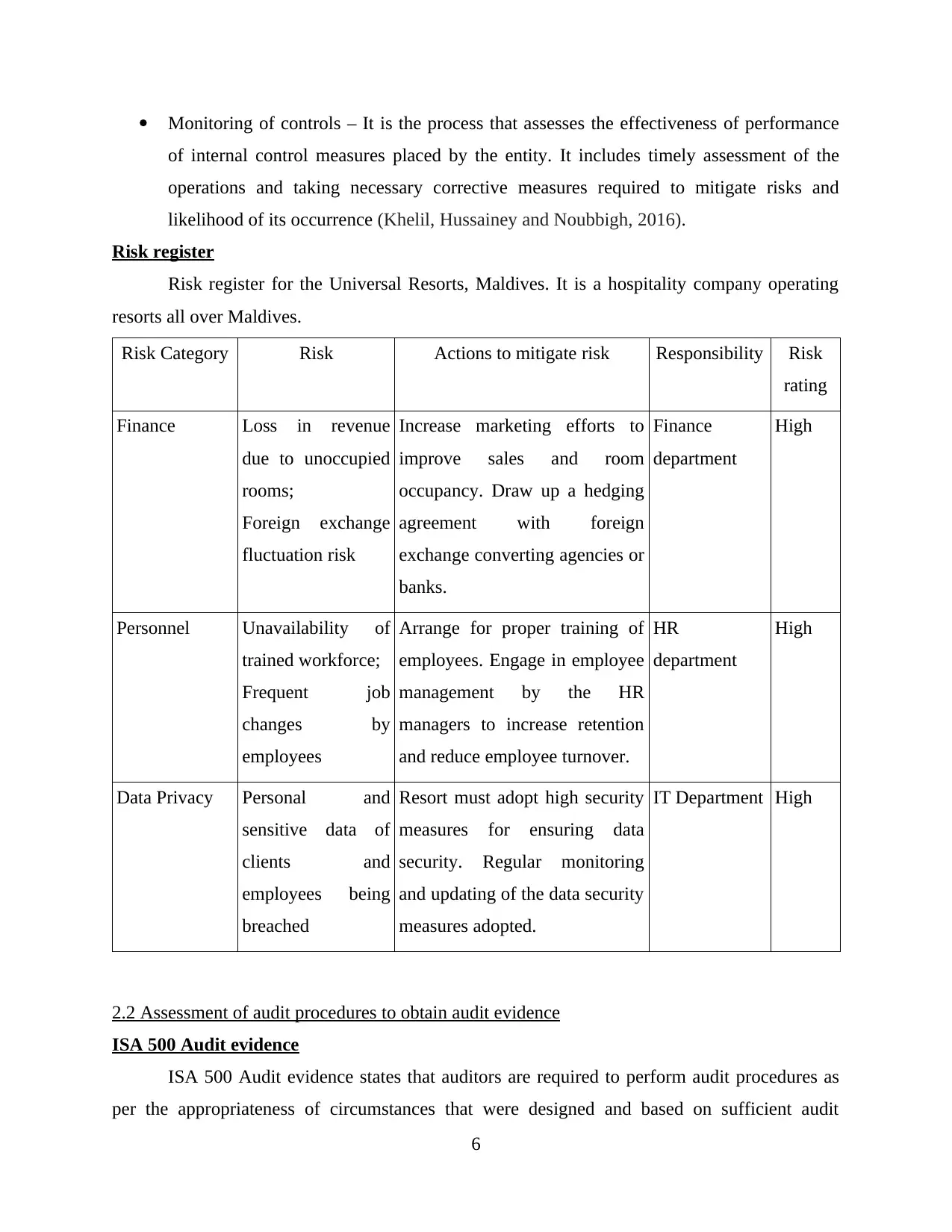

Risk register

Risk register for the Universal Resorts, Maldives. It is a hospitality company operating

resorts all over Maldives.

Risk Category Risk Actions to mitigate risk Responsibility Risk

rating

Finance Loss in revenue

due to unoccupied

rooms;

Foreign exchange

fluctuation risk

Increase marketing efforts to

improve sales and room

occupancy. Draw up a hedging

agreement with foreign

exchange converting agencies or

banks.

Finance

department

High

Personnel Unavailability of

trained workforce;

Frequent job

changes by

employees

Arrange for proper training of

employees. Engage in employee

management by the HR

managers to increase retention

and reduce employee turnover.

HR

department

High

Data Privacy Personal and

sensitive data of

clients and

employees being

breached

Resort must adopt high security

measures for ensuring data

security. Regular monitoring

and updating of the data security

measures adopted.

IT Department High

2.2 Assessment of audit procedures to obtain audit evidence

ISA 500 Audit evidence

ISA 500 Audit evidence states that auditors are required to perform audit procedures as

per the appropriateness of circumstances that were designed and based on sufficient audit

6

of internal control measures placed by the entity. It includes timely assessment of the

operations and taking necessary corrective measures required to mitigate risks and

likelihood of its occurrence (Khelil, Hussainey and Noubbigh, 2016).

Risk register

Risk register for the Universal Resorts, Maldives. It is a hospitality company operating

resorts all over Maldives.

Risk Category Risk Actions to mitigate risk Responsibility Risk

rating

Finance Loss in revenue

due to unoccupied

rooms;

Foreign exchange

fluctuation risk

Increase marketing efforts to

improve sales and room

occupancy. Draw up a hedging

agreement with foreign

exchange converting agencies or

banks.

Finance

department

High

Personnel Unavailability of

trained workforce;

Frequent job

changes by

employees

Arrange for proper training of

employees. Engage in employee

management by the HR

managers to increase retention

and reduce employee turnover.

HR

department

High

Data Privacy Personal and

sensitive data of

clients and

employees being

breached

Resort must adopt high security

measures for ensuring data

security. Regular monitoring

and updating of the data security

measures adopted.

IT Department High

2.2 Assessment of audit procedures to obtain audit evidence

ISA 500 Audit evidence

ISA 500 Audit evidence states that auditors are required to perform audit procedures as

per the appropriateness of circumstances that were designed and based on sufficient audit

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

evidence. Sufficiency and appropriateness are said to be interrelated and are needed to be applied

on both tests of control and substantive procedures.

Tests of control and substantive procedures

Test of control - These are part of audit procedure and are designed to evaluate whether

control measures adopted during audit are effective in preventing, detecting and correcting

material misstatement or significant errors at the assertion level (Nelson, Proell and Randel,

2016).

Substantive procedures – These are the part of complete audit procedures which are

designed to detect material misstatement or significant errors at the assertion level. These

procedures include test of details such as transactions, account balances, disclosures, etc. and

substantive analytical procedures. Substantive analytical procedures is a type of audit procedure

which is performed by auditor to address identified risk of significant nature in the financial

statements.

Procedures used by auditors to gather evidences

Inspection of tangible assets – It is the physical inspection of assets to confirm existence

of the asset however, it cannot guarantee whether the book value entered in the accounts

is correct or not.

Inspection of documentation or records – It includes inspection of both paper and digital

documents and records. It is aimed at gathering evidence of varied reliability, nature,

source and effectiveness of control process. It can also ensure existence of transaction or

event but is unable to ensure the value entered in the books of accounts.

Observation – This includes individual observation by auditors of the business processes

and treating it as evidence but it requires additional evidence to support that the process

displayed in front of auditor was not fabricated or manipulated (Rajgopal, Srinivasan and

Zheng, 2020).

Enquiry – Evidence can be gathered by enquiring both internal and external sources like

employees, clients, staff of clients, etc. However, it is unable to ensure integrity of the

evidence and might require additional evidence.

7

on both tests of control and substantive procedures.

Tests of control and substantive procedures

Test of control - These are part of audit procedure and are designed to evaluate whether

control measures adopted during audit are effective in preventing, detecting and correcting

material misstatement or significant errors at the assertion level (Nelson, Proell and Randel,

2016).

Substantive procedures – These are the part of complete audit procedures which are

designed to detect material misstatement or significant errors at the assertion level. These

procedures include test of details such as transactions, account balances, disclosures, etc. and

substantive analytical procedures. Substantive analytical procedures is a type of audit procedure

which is performed by auditor to address identified risk of significant nature in the financial

statements.

Procedures used by auditors to gather evidences

Inspection of tangible assets – It is the physical inspection of assets to confirm existence

of the asset however, it cannot guarantee whether the book value entered in the accounts

is correct or not.

Inspection of documentation or records – It includes inspection of both paper and digital

documents and records. It is aimed at gathering evidence of varied reliability, nature,

source and effectiveness of control process. It can also ensure existence of transaction or

event but is unable to ensure the value entered in the books of accounts.

Observation – This includes individual observation by auditors of the business processes

and treating it as evidence but it requires additional evidence to support that the process

displayed in front of auditor was not fabricated or manipulated (Rajgopal, Srinivasan and

Zheng, 2020).

Enquiry – Evidence can be gathered by enquiring both internal and external sources like

employees, clients, staff of clients, etc. However, it is unable to ensure integrity of the

evidence and might require additional evidence.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Chapter 3: Understanding how to carry-out evaluation and preparation audit

reporting

3.1 Basic element of Audit report

Auditors report

The auditor is required to make a report at the end of the audit which are sets with their

own opinion on the truth and fairness of the financial statements. The audit report contains a

number of elements so that the auditor has been conducted according to the recognised standard.

This audit report has been submitted to the shareholders who have appointed them as the auditors

(Rusmin, and Evans, 2017). Thus, it can be said that the auditors save the interest of the

shareholders through audit report. There are four parts which are covered by ISA:

ISA 700- Analysis an opinion and reporting in the financial statement.

ISA 701- In the audit report, proper communication is needed for maintaining the

independent audit report.

ISA 705- Modification in the audit report if necessary.

ISA 706- Accent of matter paragraph and other matter paragraph report.

Factors considered by auditors when forming audit opinion

In order to make the opinion, the auditor must need to complete the conclusion related to

the audit report whether the reasonable authority has been used as the financial statement which

are free from material misstatement. Hence the auditor's conclusion is needed to considered the

following factors related to their opinion.

whether the company provide the sufficient audit evidence which has been obtained by

the auditor in order to make the audit report.

Whether the statement which are provided by the company are misstatement or

uncorrected (Turner, Weickgenannt and Copeland, 2020).

Whether the company applied and disclose the important accounting policies which are

needed in the financial statement.

The overall presentation, structure and content which are used by the companies are

accurate and correct so that the auditor can easily make the audit report.

Basic elements of auditors’ report

Basic element of the auditor's report is described as follows:

8

reporting

3.1 Basic element of Audit report

Auditors report

The auditor is required to make a report at the end of the audit which are sets with their

own opinion on the truth and fairness of the financial statements. The audit report contains a

number of elements so that the auditor has been conducted according to the recognised standard.

This audit report has been submitted to the shareholders who have appointed them as the auditors

(Rusmin, and Evans, 2017). Thus, it can be said that the auditors save the interest of the

shareholders through audit report. There are four parts which are covered by ISA:

ISA 700- Analysis an opinion and reporting in the financial statement.

ISA 701- In the audit report, proper communication is needed for maintaining the

independent audit report.

ISA 705- Modification in the audit report if necessary.

ISA 706- Accent of matter paragraph and other matter paragraph report.

Factors considered by auditors when forming audit opinion

In order to make the opinion, the auditor must need to complete the conclusion related to

the audit report whether the reasonable authority has been used as the financial statement which

are free from material misstatement. Hence the auditor's conclusion is needed to considered the

following factors related to their opinion.

whether the company provide the sufficient audit evidence which has been obtained by

the auditor in order to make the audit report.

Whether the statement which are provided by the company are misstatement or

uncorrected (Turner, Weickgenannt and Copeland, 2020).

Whether the company applied and disclose the important accounting policies which are

needed in the financial statement.

The overall presentation, structure and content which are used by the companies are

accurate and correct so that the auditor can easily make the audit report.

Basic elements of auditors’ report

Basic element of the auditor's report is described as follows:

8

Title- The auditor's report must include the title that clearly indicate the auditor's

independent report.

Addressee- This will be determined by the laws and regulation but mostly they are

shareholders of the company.

Opinion paragraph- In this part, auditor stated that financial report has been audited and a

brief summery is provided regarding the policies and applications.

Basis for opinion- These bases for opinion are stated that the audit report was conducted

on the basis of ISA rules.

Going concern- Here the auditor used a material uncertainty related to the going concern

exists of the company.

Brief discussion about:

Unmodified audit opinion – It is an opinion or judgement by independent auditor which

states that a company's financial statements are true, fair and appropriately presented

without having any identified material misstatement and are in compliance with the

accounting standards specified or other applicable reporting framework (Wiley, 2017).

Modified opinion – If the auditor's opinion is that the company accounts are not free from

material misstatement, they modify their opinion in accordance with ISA 705. There are

three types of modified opinions:

Qualified opinion: This opinion is given in the case when either auditor is of the

opinion that misstatements are material but not all in the financial statements of the

entity or the auditor is of the opinion that since sufficient appropriate audit evidence

was not obtained, there are possibilities of undetected misstatement which could be of

material nature although not pervasive.

Adverse opinion: When auditor is of opinion on the basis of sufficient appropriate

evidence that material misstatements exist in the financial statements of the entity

which are also of pervasive nature, an adverse opinion is given.

Disclaimer of opinion: When auditor is unable to obtain sufficient appropriate

evidence on which audit opinion can be given, a disclaimer of opinion is given that

financial statements can have both ways.

9

independent report.

Addressee- This will be determined by the laws and regulation but mostly they are

shareholders of the company.

Opinion paragraph- In this part, auditor stated that financial report has been audited and a

brief summery is provided regarding the policies and applications.

Basis for opinion- These bases for opinion are stated that the audit report was conducted

on the basis of ISA rules.

Going concern- Here the auditor used a material uncertainty related to the going concern

exists of the company.

Brief discussion about:

Unmodified audit opinion – It is an opinion or judgement by independent auditor which

states that a company's financial statements are true, fair and appropriately presented

without having any identified material misstatement and are in compliance with the

accounting standards specified or other applicable reporting framework (Wiley, 2017).

Modified opinion – If the auditor's opinion is that the company accounts are not free from

material misstatement, they modify their opinion in accordance with ISA 705. There are

three types of modified opinions:

Qualified opinion: This opinion is given in the case when either auditor is of the

opinion that misstatements are material but not all in the financial statements of the

entity or the auditor is of the opinion that since sufficient appropriate audit evidence

was not obtained, there are possibilities of undetected misstatement which could be of

material nature although not pervasive.

Adverse opinion: When auditor is of opinion on the basis of sufficient appropriate

evidence that material misstatements exist in the financial statements of the entity

which are also of pervasive nature, an adverse opinion is given.

Disclaimer of opinion: When auditor is unable to obtain sufficient appropriate

evidence on which audit opinion can be given, a disclaimer of opinion is given that

financial statements can have both ways.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3.2 Audit procedures to identify subsequent events

Test of controls in the procurement systems

Test of control in procurement system includes books of accounts – purchase journal,

purchase ledger, general ledger, suppliers’ statements and invoices, purchase order, requisition

notes, etc. These will be tested on a sample basis to ascertain whether all entries that have been

recorded exist and are accurate and whether all transactions that should have been recorded have

been completely recorded as per the accurate value. They must be verified against corroborative

evidences to be sure of their correct existence (Zgarni, Hlioui and Zehri, 2016).

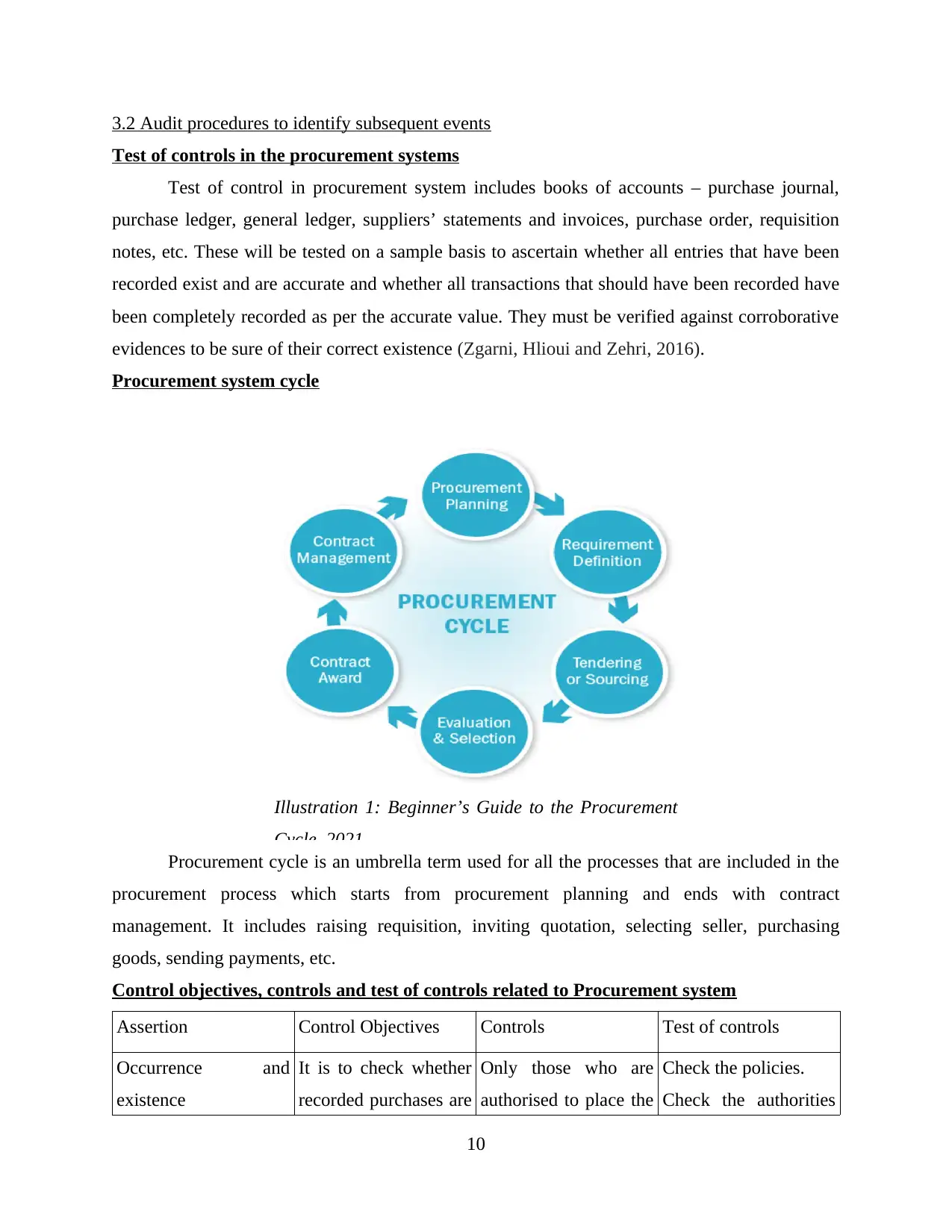

Procurement system cycle

Procurement cycle is an umbrella term used for all the processes that are included in the

procurement process which starts from procurement planning and ends with contract

management. It includes raising requisition, inviting quotation, selecting seller, purchasing

goods, sending payments, etc.

Control objectives, controls and test of controls related to Procurement system

Assertion Control Objectives Controls Test of controls

Occurrence and

existence

It is to check whether

recorded purchases are

Only those who are

authorised to place the

Check the policies.

Check the authorities

10

Illustration 1: Beginner’s Guide to the Procurement

Cycle, 2021

Test of controls in the procurement systems

Test of control in procurement system includes books of accounts – purchase journal,

purchase ledger, general ledger, suppliers’ statements and invoices, purchase order, requisition

notes, etc. These will be tested on a sample basis to ascertain whether all entries that have been

recorded exist and are accurate and whether all transactions that should have been recorded have

been completely recorded as per the accurate value. They must be verified against corroborative

evidences to be sure of their correct existence (Zgarni, Hlioui and Zehri, 2016).

Procurement system cycle

Procurement cycle is an umbrella term used for all the processes that are included in the

procurement process which starts from procurement planning and ends with contract

management. It includes raising requisition, inviting quotation, selecting seller, purchasing

goods, sending payments, etc.

Control objectives, controls and test of controls related to Procurement system

Assertion Control Objectives Controls Test of controls

Occurrence and

existence

It is to check whether

recorded purchases are

Only those who are

authorised to place the

Check the policies.

Check the authorities

10

Illustration 1: Beginner’s Guide to the Procurement

Cycle, 2021

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

actually those goods

and services which are

received by the

company.

order or requisition as

per policies are

making the order.

signing the requisition

orders.

Observe the whole

procurement cycle on

a sample basis.

Completeness Objective is to check

whether all the

transactions that have

been recorded have

actually been made or

vice versa.

Purchase order, pre-

numbered GRN,

supplier statement –

all must reconcile with

purchase journal.

Check invoice against

requisition and

supplier statement

independently on a

sample basis.

Check purchase orders

and pre-numbered

GRN of the

accounting period in a

sample basis.

Rights and obligations Objective is to check

whether recorded

supplier purchases are

also being reflected as

creditor liability to the

company.

Purchase order, pre-

numbered GRN are to

be matched with

supplier statement and

invoices

Check supporting

documents as well to

be ensured of the

matching purchase

orders and invoices.

Accuracy, valuation

and allocation and

classification

Objective is to check

proper recording of all

purchase entries in the

books of accounts.

Purchase order being

reconciled with

suppliers’ invoices.

Check mathematical

accuracy of entries

posted in purchase

ledger and whether

they are correctly

being reconciled in

Verify authority and

signature on invoices

on a sample basis.

Review journal and

general ledger to

check reconciliation.

11

and services which are

received by the

company.

order or requisition as

per policies are

making the order.

signing the requisition

orders.

Observe the whole

procurement cycle on

a sample basis.

Completeness Objective is to check

whether all the

transactions that have

been recorded have

actually been made or

vice versa.

Purchase order, pre-

numbered GRN,

supplier statement –

all must reconcile with

purchase journal.

Check invoice against

requisition and

supplier statement

independently on a

sample basis.

Check purchase orders

and pre-numbered

GRN of the

accounting period in a

sample basis.

Rights and obligations Objective is to check

whether recorded

supplier purchases are

also being reflected as

creditor liability to the

company.

Purchase order, pre-

numbered GRN are to

be matched with

supplier statement and

invoices

Check supporting

documents as well to

be ensured of the

matching purchase

orders and invoices.

Accuracy, valuation

and allocation and

classification

Objective is to check

proper recording of all

purchase entries in the

books of accounts.

Purchase order being

reconciled with

suppliers’ invoices.

Check mathematical

accuracy of entries

posted in purchase

ledger and whether

they are correctly

being reconciled in

Verify authority and

signature on invoices

on a sample basis.

Review journal and

general ledger to

check reconciliation.

11

general ledger.

Chapter 4: Conclusion

Internal controls are determined and implemented by the company management to ensure

minimum risks and maximum profitability. Strengthening these internal control processes

reduces the risk of asset loss, revenue leakage as well as helps in ensuring that company is

preparing complete and accurate financial statements which can be relied upon. These control

measures are designed according to applicable laws and regulations and strengthening them will

ensure that company follows all rules that are applicable on it (Krarti, 2020). Not only that, these

measures are aimed at assessing governance of the company in terms of accountability,

transparency and integrity. Strengthening these measures and assessing them through internal

audit function is capable of producing positive impact on quality of business production function

as well as distribution function as it helps in minimising intentional and unintentional errors,

frauds and harms to the company processes. Also, strengthened internal control function helps in

detection of such processes where there a possibility lies to occurrence of errors in the near

future.

12

Chapter 4: Conclusion

Internal controls are determined and implemented by the company management to ensure

minimum risks and maximum profitability. Strengthening these internal control processes

reduces the risk of asset loss, revenue leakage as well as helps in ensuring that company is

preparing complete and accurate financial statements which can be relied upon. These control

measures are designed according to applicable laws and regulations and strengthening them will

ensure that company follows all rules that are applicable on it (Krarti, 2020). Not only that, these

measures are aimed at assessing governance of the company in terms of accountability,

transparency and integrity. Strengthening these measures and assessing them through internal

audit function is capable of producing positive impact on quality of business production function

as well as distribution function as it helps in minimising intentional and unintentional errors,

frauds and harms to the company processes. Also, strengthened internal control function helps in

detection of such processes where there a possibility lies to occurrence of errors in the near

future.

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.