Economics Case Study: Evaluation of a Small Business Performance

VerifiedAdded on 2022/08/13

|11

|1363

|8

Case Study

AI Summary

This case study analyzes the economic performance of a small business, focusing on key concepts like economic depreciation and price elasticity of demand. The analysis is divided into four tasks. Task 1 calculates accounting and economic costs and profits. Task 2 determines the price elasticity of demand based on changes in price and quantity. Task 3 examines how a price increase affects sales, and Task 4 evaluates whether the business earned normal or abnormal profit. The case study concludes that the product's demand is relatively inelastic, and the business generated an above-normal profit. The report includes calculations and explanations in the appendix, demonstrating how the business's financial data and market conditions impact its overall economic performance.

Running head: EVALUATION YOUR SMALL BUSINESS

Evaluation Your Small Business

Name of the Student

Name of the University

Student Number

Evaluation Your Small Business

Name of the Student

Name of the University

Student Number

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1EVALUATION YOUR SMALL BUSINESS

Executive Summary

The business report deals with two of the important aspect of business evaluation. The

first is economic depreciation which captures extent to decline in market value of an asset due to

changing dynamics of an economy. This is a separate concept of accounting depreciation and is

crucial for business owner attempting to sell their productive assets. Another important concept

for the business is price elasticity of demand. The behavior of total revenue or sales give a price

change depends on elasticity of demand.

These two concepts are used to develop a case study analysis for the small business. The

entire evaluation is divided into four tasks. The first task computes different cost and profit of the

business. Task 2 is concerned with estimating price elasticity of demand for the product. Task 3

applies the concept of price elasticity of demand to describe changes in sales for a given change

in price. Finally, Task 4 analyzes whether the business had made a normal profit or not. The

report concludes that elasticity of demand for the product is relatively inelastic and the business

successfully made more than normal profit.

Executive Summary

The business report deals with two of the important aspect of business evaluation. The

first is economic depreciation which captures extent to decline in market value of an asset due to

changing dynamics of an economy. This is a separate concept of accounting depreciation and is

crucial for business owner attempting to sell their productive assets. Another important concept

for the business is price elasticity of demand. The behavior of total revenue or sales give a price

change depends on elasticity of demand.

These two concepts are used to develop a case study analysis for the small business. The

entire evaluation is divided into four tasks. The first task computes different cost and profit of the

business. Task 2 is concerned with estimating price elasticity of demand for the product. Task 3

applies the concept of price elasticity of demand to describe changes in sales for a given change

in price. Finally, Task 4 analyzes whether the business had made a normal profit or not. The

report concludes that elasticity of demand for the product is relatively inelastic and the business

successfully made more than normal profit.

2EVALUATION YOUR SMALL BUSINESS

Table of Contents

1. Introduction..................................................................................................................................3

2. Analytical development...............................................................................................................4

2.1 Task 1.....................................................................................................................................4

2.2 Task 2.....................................................................................................................................4

2.3 Task 3.....................................................................................................................................5

3. Conclusion...................................................................................................................................5

3.1 Task 4.....................................................................................................................................5

4. Appendix......................................................................................................................................7

Task 1...........................................................................................................................................7

Task 2...........................................................................................................................................8

Task 3...........................................................................................................................................8

Task 4...........................................................................................................................................8

References......................................................................................................................................10

Table of Contents

1. Introduction..................................................................................................................................3

2. Analytical development...............................................................................................................4

2.1 Task 1.....................................................................................................................................4

2.2 Task 2.....................................................................................................................................4

2.3 Task 3.....................................................................................................................................5

3. Conclusion...................................................................................................................................5

3.1 Task 4.....................................................................................................................................5

4. Appendix......................................................................................................................................7

Task 1...........................................................................................................................................7

Task 2...........................................................................................................................................8

Task 3...........................................................................................................................................8

Task 4...........................................................................................................................................8

References......................................................................................................................................10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3EVALUATION YOUR SMALL BUSINESS

1. Introduction

The concept of ‘economic depreciation’ is associated with the idea of deterioration of

market value of an asset with passes of time because of the working of some effective economic

factors1. This type of depiction is particularly relevant for the real estate market where value of

assets are highly vulnerable to changes in state of economic condition. The concept of economic

depreciation is distinguished from the accounting depreciation which represents expense of an

asset overtime based on a fixed schedule. The idea of economic depreciation is more important

for the asset owners who are attempting to sell their assets at the current market value2. In

evaluating value of the productive assets in reference to current economic situation the owner

should consider economic depreciation.

Another concept reverent for analysis of business is “price elasticity of demand”. This is

a computational measure which shows percentage change in demand because of a given

percentage change in price of the product. With various magnitude of change in demand for a

given change in price there are different types of price elasticity of demand3. Given proportionate

change in demand is less than proportionate change in price, elasticity measure is smaller than 1

meaning relatively inelastic demand. Relatively elastic demand represents demand where change

in demand is more than change in price giving a measured elasticity of 1. If demand changes by

exactly same magnitude of price, demand is considered as unitary elastic where elasticity

measured equals 1. Two polar cases of elasticity of demand are perfectly elastic demand and

1 Crosby, Neil, Steven Devaney, and Anupam Nanda. "Which factors drive rental depreciation rates for office and

industrial properties?." Journal of Real Estate Research 38.3 (2016): 359-392.

2 Livdan, Dmitry, and Alexander Nezlobin. "Accounting rules, equity valuation, and growth options." Review of

Accounting Studies 22.3 (2017): 1122-1155.

3 Fine, Ben. "Microeconomics." University of Chicago Press Economics Books (2016).

1. Introduction

The concept of ‘economic depreciation’ is associated with the idea of deterioration of

market value of an asset with passes of time because of the working of some effective economic

factors1. This type of depiction is particularly relevant for the real estate market where value of

assets are highly vulnerable to changes in state of economic condition. The concept of economic

depreciation is distinguished from the accounting depreciation which represents expense of an

asset overtime based on a fixed schedule. The idea of economic depreciation is more important

for the asset owners who are attempting to sell their assets at the current market value2. In

evaluating value of the productive assets in reference to current economic situation the owner

should consider economic depreciation.

Another concept reverent for analysis of business is “price elasticity of demand”. This is

a computational measure which shows percentage change in demand because of a given

percentage change in price of the product. With various magnitude of change in demand for a

given change in price there are different types of price elasticity of demand3. Given proportionate

change in demand is less than proportionate change in price, elasticity measure is smaller than 1

meaning relatively inelastic demand. Relatively elastic demand represents demand where change

in demand is more than change in price giving a measured elasticity of 1. If demand changes by

exactly same magnitude of price, demand is considered as unitary elastic where elasticity

measured equals 1. Two polar cases of elasticity of demand are perfectly elastic demand and

1 Crosby, Neil, Steven Devaney, and Anupam Nanda. "Which factors drive rental depreciation rates for office and

industrial properties?." Journal of Real Estate Research 38.3 (2016): 359-392.

2 Livdan, Dmitry, and Alexander Nezlobin. "Accounting rules, equity valuation, and growth options." Review of

Accounting Studies 22.3 (2017): 1122-1155.

3 Fine, Ben. "Microeconomics." University of Chicago Press Economics Books (2016).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4EVALUATION YOUR SMALL BUSINESS

perfectly inelastic demand. Elasticity measure is infinite in case of perfectly elastic demand as

demand can change infinitely for a slight or no change in price4. Elasticity measure is zero when

demand is perfectly inelastic since demand here remains almost fixed irrespective of change in

price.

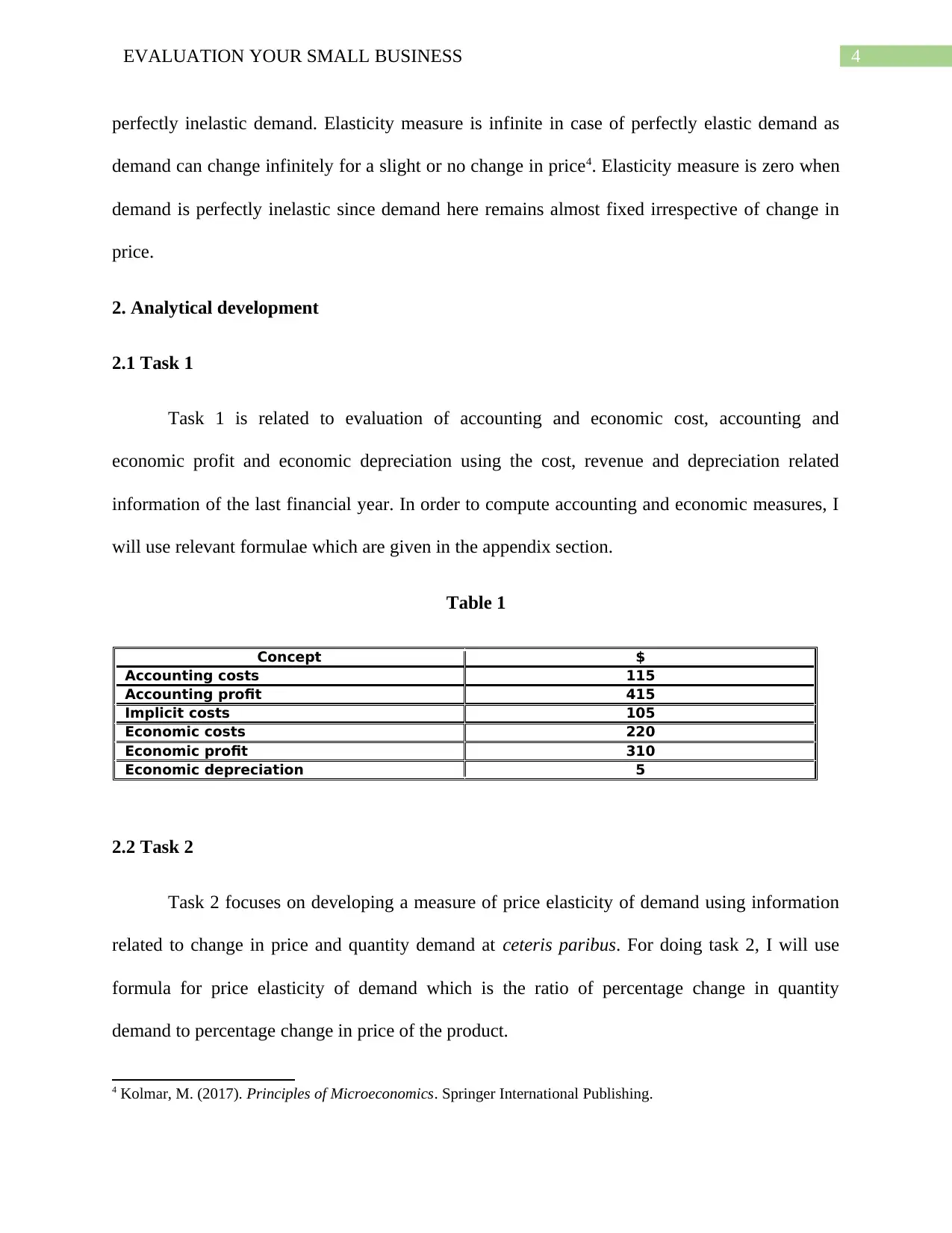

2. Analytical development

2.1 Task 1

Task 1 is related to evaluation of accounting and economic cost, accounting and

economic profit and economic depreciation using the cost, revenue and depreciation related

information of the last financial year. In order to compute accounting and economic measures, I

will use relevant formulae which are given in the appendix section.

Table 1

Concept $

Accounting costs 115

Accounting profit 415

Implicit costs 105

Economic costs 220

Economic profit 310

Economic depreciation 5

2.2 Task 2

Task 2 focuses on developing a measure of price elasticity of demand using information

related to change in price and quantity demand at ceteris paribus. For doing task 2, I will use

formula for price elasticity of demand which is the ratio of percentage change in quantity

demand to percentage change in price of the product.

4 Kolmar, M. (2017). Principles of Microeconomics. Springer International Publishing.

perfectly inelastic demand. Elasticity measure is infinite in case of perfectly elastic demand as

demand can change infinitely for a slight or no change in price4. Elasticity measure is zero when

demand is perfectly inelastic since demand here remains almost fixed irrespective of change in

price.

2. Analytical development

2.1 Task 1

Task 1 is related to evaluation of accounting and economic cost, accounting and

economic profit and economic depreciation using the cost, revenue and depreciation related

information of the last financial year. In order to compute accounting and economic measures, I

will use relevant formulae which are given in the appendix section.

Table 1

Concept $

Accounting costs 115

Accounting profit 415

Implicit costs 105

Economic costs 220

Economic profit 310

Economic depreciation 5

2.2 Task 2

Task 2 focuses on developing a measure of price elasticity of demand using information

related to change in price and quantity demand at ceteris paribus. For doing task 2, I will use

formula for price elasticity of demand which is the ratio of percentage change in quantity

demand to percentage change in price of the product.

4 Kolmar, M. (2017). Principles of Microeconomics. Springer International Publishing.

5EVALUATION YOUR SMALL BUSINESS

Table 2

Concept Value

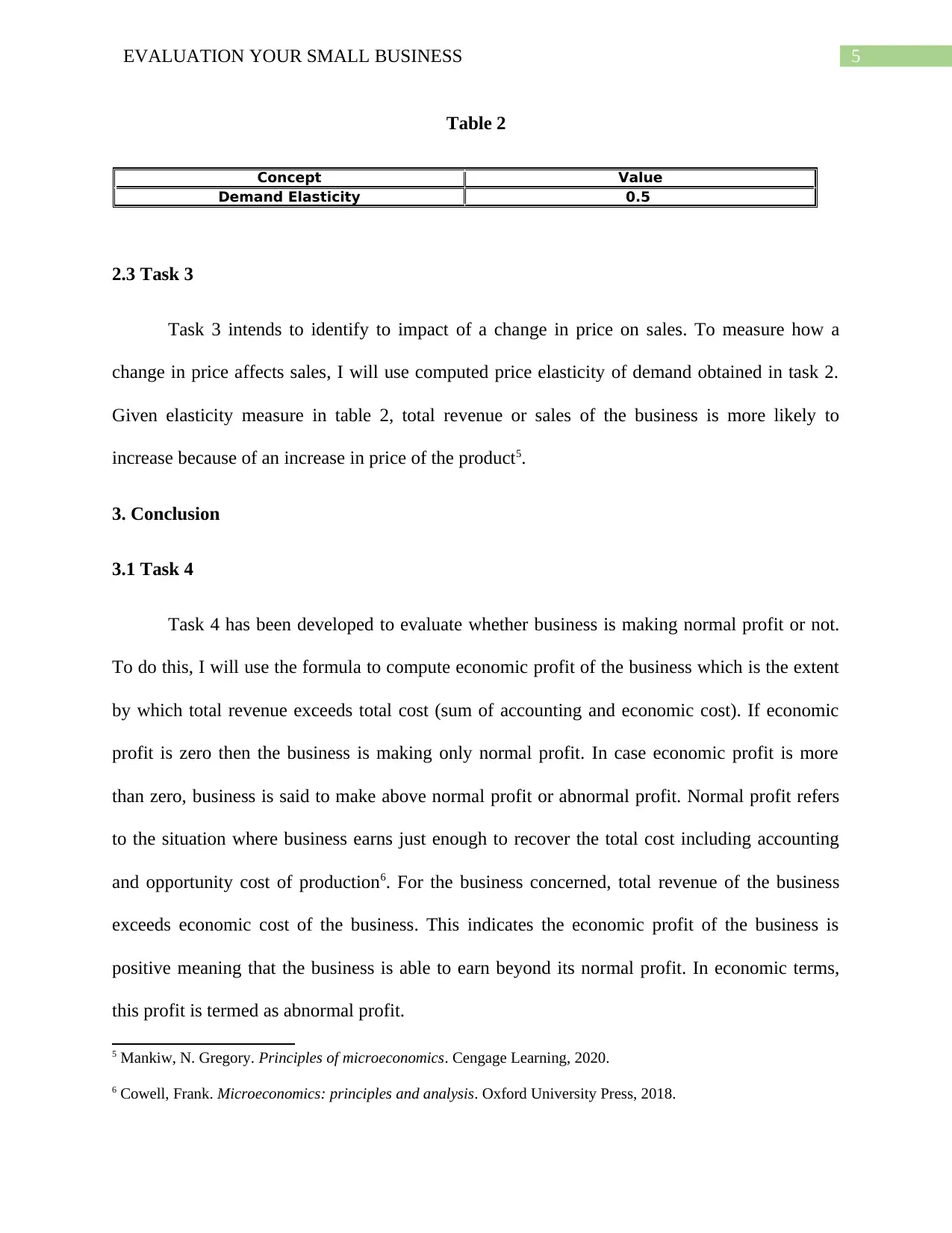

Demand Elasticity 0.5

2.3 Task 3

Task 3 intends to identify to impact of a change in price on sales. To measure how a

change in price affects sales, I will use computed price elasticity of demand obtained in task 2.

Given elasticity measure in table 2, total revenue or sales of the business is more likely to

increase because of an increase in price of the product5.

3. Conclusion

3.1 Task 4

Task 4 has been developed to evaluate whether business is making normal profit or not.

To do this, I will use the formula to compute economic profit of the business which is the extent

by which total revenue exceeds total cost (sum of accounting and economic cost). If economic

profit is zero then the business is making only normal profit. In case economic profit is more

than zero, business is said to make above normal profit or abnormal profit. Normal profit refers

to the situation where business earns just enough to recover the total cost including accounting

and opportunity cost of production6. For the business concerned, total revenue of the business

exceeds economic cost of the business. This indicates the economic profit of the business is

positive meaning that the business is able to earn beyond its normal profit. In economic terms,

this profit is termed as abnormal profit.

5 Mankiw, N. Gregory. Principles of microeconomics. Cengage Learning, 2020.

6 Cowell, Frank. Microeconomics: principles and analysis. Oxford University Press, 2018.

Table 2

Concept Value

Demand Elasticity 0.5

2.3 Task 3

Task 3 intends to identify to impact of a change in price on sales. To measure how a

change in price affects sales, I will use computed price elasticity of demand obtained in task 2.

Given elasticity measure in table 2, total revenue or sales of the business is more likely to

increase because of an increase in price of the product5.

3. Conclusion

3.1 Task 4

Task 4 has been developed to evaluate whether business is making normal profit or not.

To do this, I will use the formula to compute economic profit of the business which is the extent

by which total revenue exceeds total cost (sum of accounting and economic cost). If economic

profit is zero then the business is making only normal profit. In case economic profit is more

than zero, business is said to make above normal profit or abnormal profit. Normal profit refers

to the situation where business earns just enough to recover the total cost including accounting

and opportunity cost of production6. For the business concerned, total revenue of the business

exceeds economic cost of the business. This indicates the economic profit of the business is

positive meaning that the business is able to earn beyond its normal profit. In economic terms,

this profit is termed as abnormal profit.

5 Mankiw, N. Gregory. Principles of microeconomics. Cengage Learning, 2020.

6 Cowell, Frank. Microeconomics: principles and analysis. Oxford University Press, 2018.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6EVALUATION YOUR SMALL BUSINESS

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7EVALUATION YOUR SMALL BUSINESS

4. Appendix

Task 1

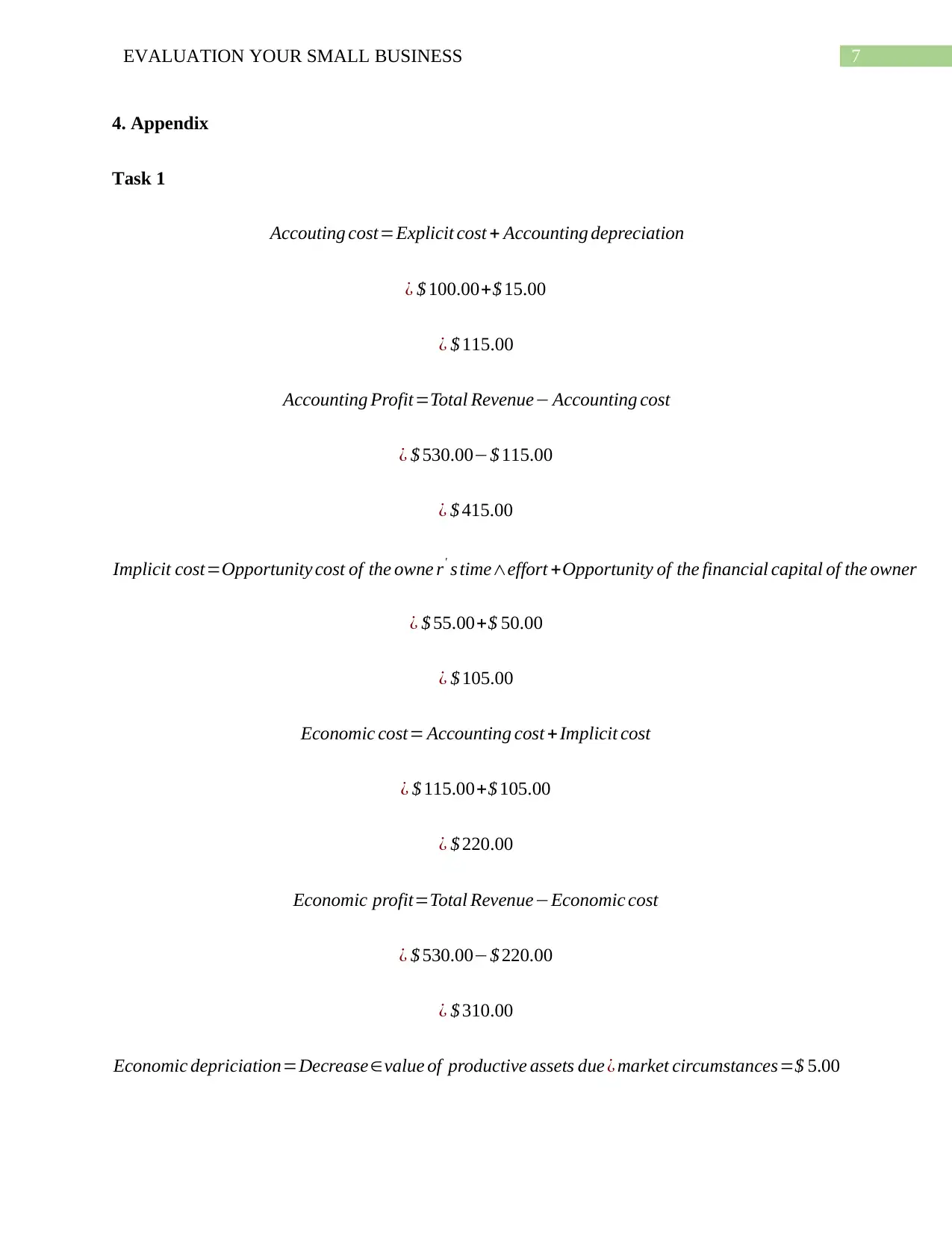

Accouting cost=Explicit cost + Accounting depreciation

¿ $ 100.00+$ 15.00

¿ $ 115.00

Accounting Profit=Total Revenue− Accounting cost

¿ $ 530.00−$ 115.00

¿ $ 415.00

Implicit cost=Opportunity cost of the owne r' s time∧effort +Opportunity of the financial capital of the owner

¿ $ 55.00+$ 50.00

¿ $ 105.00

Economic cost= Accounting cost +Implicit cost

¿ $ 115.00+$ 105.00

¿ $ 220.00

Economic profit=Total Revenue−Economic cost

¿ $ 530.00−$ 220.00

¿ $ 310.00

Economic depriciation=Decrease∈value of productive assets due ¿ market circumstances=$ 5.00

4. Appendix

Task 1

Accouting cost=Explicit cost + Accounting depreciation

¿ $ 100.00+$ 15.00

¿ $ 115.00

Accounting Profit=Total Revenue− Accounting cost

¿ $ 530.00−$ 115.00

¿ $ 415.00

Implicit cost=Opportunity cost of the owne r' s time∧effort +Opportunity of the financial capital of the owner

¿ $ 55.00+$ 50.00

¿ $ 105.00

Economic cost= Accounting cost +Implicit cost

¿ $ 115.00+$ 105.00

¿ $ 220.00

Economic profit=Total Revenue−Economic cost

¿ $ 530.00−$ 220.00

¿ $ 310.00

Economic depriciation=Decrease∈value of productive assets due ¿ market circumstances=$ 5.00

8EVALUATION YOUR SMALL BUSINESS

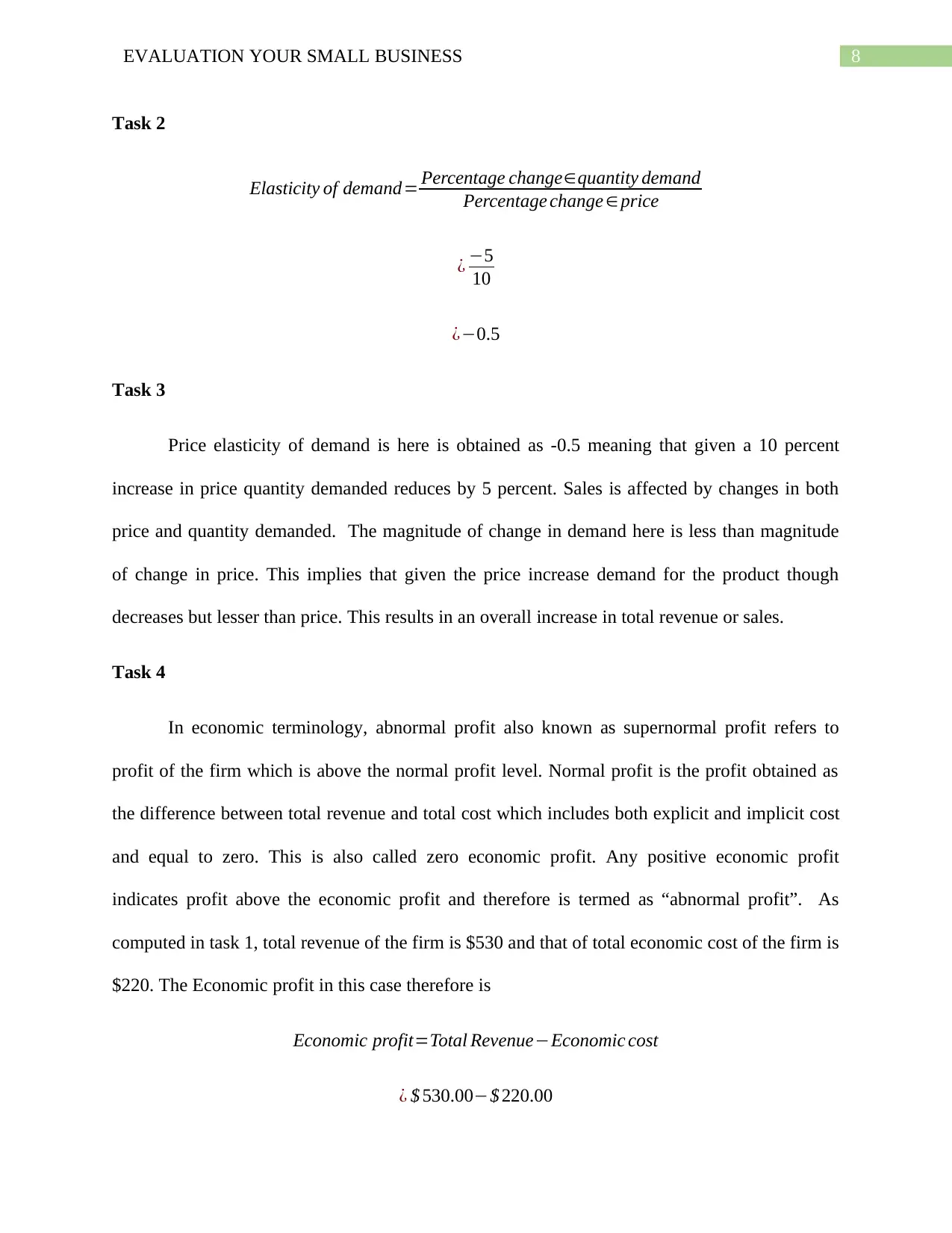

Task 2

Elasticity of demand= Percentage change∈quantity demand

Percentage change ∈price

¿ −5

10

¿−0.5

Task 3

Price elasticity of demand is here is obtained as -0.5 meaning that given a 10 percent

increase in price quantity demanded reduces by 5 percent. Sales is affected by changes in both

price and quantity demanded. The magnitude of change in demand here is less than magnitude

of change in price. This implies that given the price increase demand for the product though

decreases but lesser than price. This results in an overall increase in total revenue or sales.

Task 4

In economic terminology, abnormal profit also known as supernormal profit refers to

profit of the firm which is above the normal profit level. Normal profit is the profit obtained as

the difference between total revenue and total cost which includes both explicit and implicit cost

and equal to zero. This is also called zero economic profit. Any positive economic profit

indicates profit above the economic profit and therefore is termed as “abnormal profit”. As

computed in task 1, total revenue of the firm is $530 and that of total economic cost of the firm is

$220. The Economic profit in this case therefore is

Economic profit=Total Revenue−Economic cost

¿ $ 530.00−$ 220.00

Task 2

Elasticity of demand= Percentage change∈quantity demand

Percentage change ∈price

¿ −5

10

¿−0.5

Task 3

Price elasticity of demand is here is obtained as -0.5 meaning that given a 10 percent

increase in price quantity demanded reduces by 5 percent. Sales is affected by changes in both

price and quantity demanded. The magnitude of change in demand here is less than magnitude

of change in price. This implies that given the price increase demand for the product though

decreases but lesser than price. This results in an overall increase in total revenue or sales.

Task 4

In economic terminology, abnormal profit also known as supernormal profit refers to

profit of the firm which is above the normal profit level. Normal profit is the profit obtained as

the difference between total revenue and total cost which includes both explicit and implicit cost

and equal to zero. This is also called zero economic profit. Any positive economic profit

indicates profit above the economic profit and therefore is termed as “abnormal profit”. As

computed in task 1, total revenue of the firm is $530 and that of total economic cost of the firm is

$220. The Economic profit in this case therefore is

Economic profit=Total Revenue−Economic cost

¿ $ 530.00−$ 220.00

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9EVALUATION YOUR SMALL BUSINESS

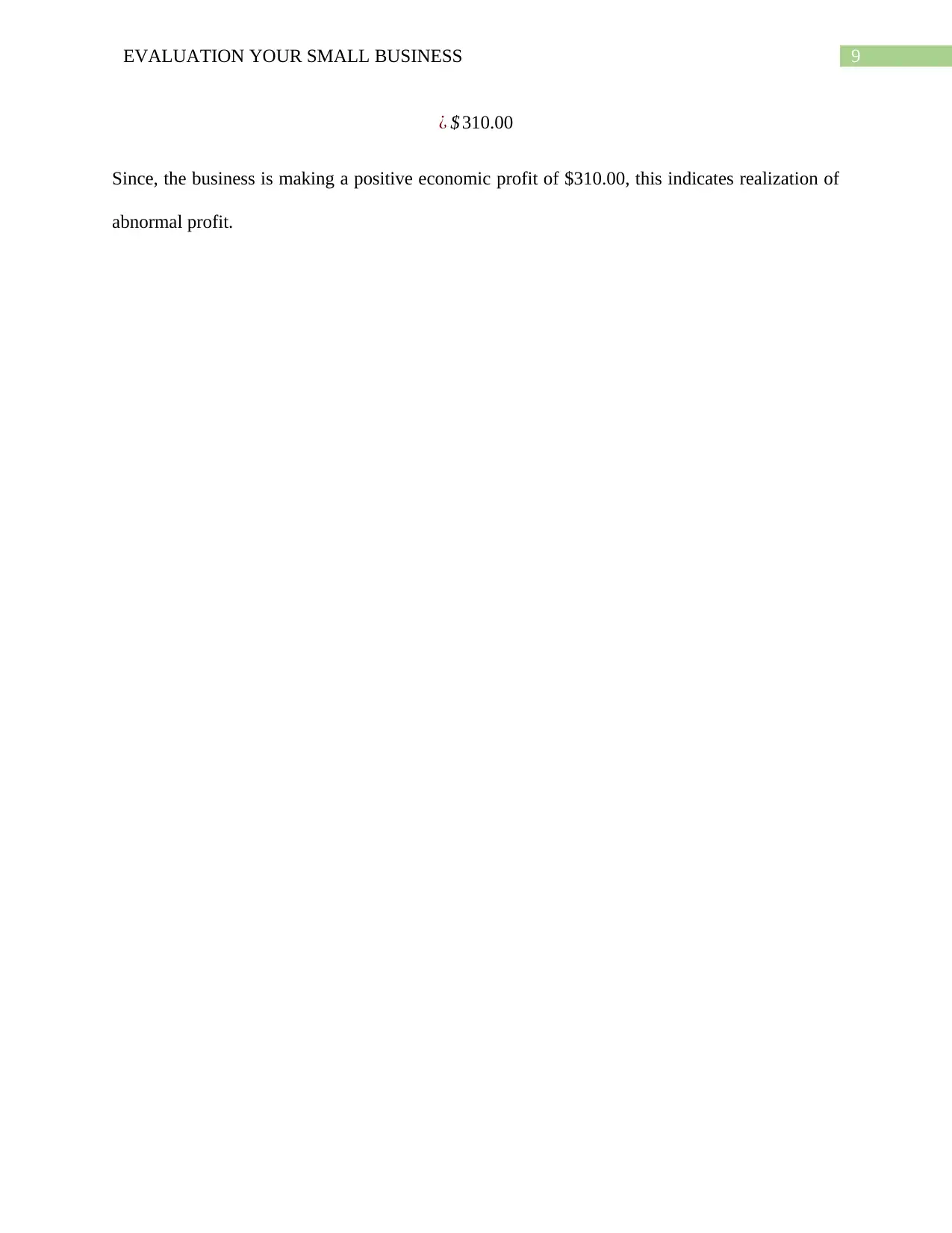

¿ $ 310.00

Since, the business is making a positive economic profit of $310.00, this indicates realization of

abnormal profit.

¿ $ 310.00

Since, the business is making a positive economic profit of $310.00, this indicates realization of

abnormal profit.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10EVALUATION YOUR SMALL BUSINESS

References

Cowell, Frank. Microeconomics: principles and analysis. Oxford University Press, 2018.

Crosby, Neil, Steven Devaney, and Anupam Nanda. "Which factors drive rental depreciation

rates for office and industrial properties?." Journal of Real Estate Research 38.3 (2016): 359-

392.

Fine, Ben. "Microeconomics." University of Chicago Press Economics Books (2016).

Kolmar, M. (2017). Principles of Microeconomics. Springer International Publishing.

Livdan, Dmitry, and Alexander Nezlobin. "Accounting rules, equity valuation, and growth

options." Review of Accounting Studies 22.3 (2017): 1122-1155.

Mankiw, N. Gregory. Principles of microeconomics. Cengage Learning, 2020.

References

Cowell, Frank. Microeconomics: principles and analysis. Oxford University Press, 2018.

Crosby, Neil, Steven Devaney, and Anupam Nanda. "Which factors drive rental depreciation

rates for office and industrial properties?." Journal of Real Estate Research 38.3 (2016): 359-

392.

Fine, Ben. "Microeconomics." University of Chicago Press Economics Books (2016).

Kolmar, M. (2017). Principles of Microeconomics. Springer International Publishing.

Livdan, Dmitry, and Alexander Nezlobin. "Accounting rules, equity valuation, and growth

options." Review of Accounting Studies 22.3 (2017): 1122-1155.

Mankiw, N. Gregory. Principles of microeconomics. Cengage Learning, 2020.

1 out of 11