Financial Statement Analysis, Ratios, and Project Appraisal Solution

VerifiedAdded on 2023/06/18

|6

|863

|275

Homework Assignment

AI Summary

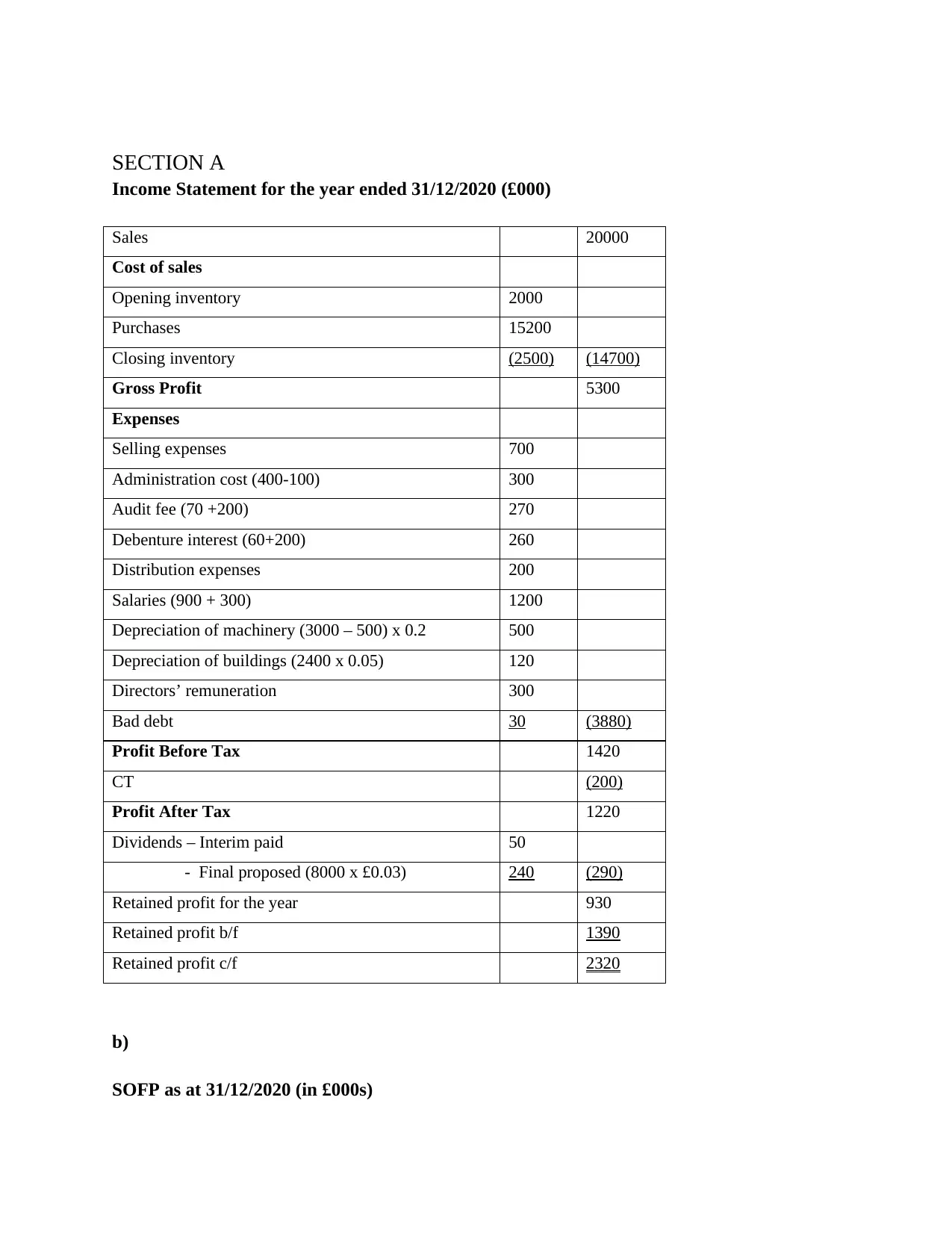

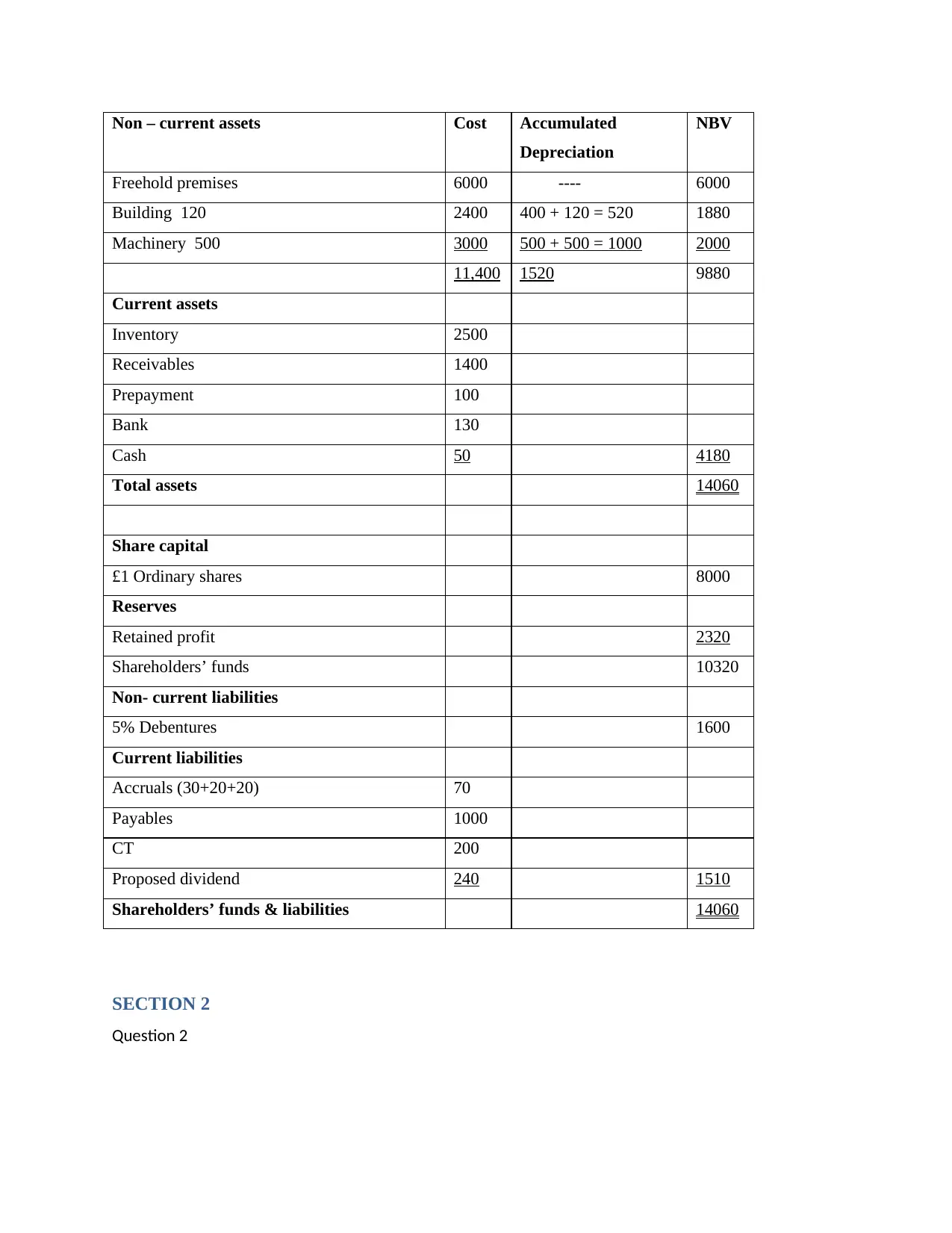

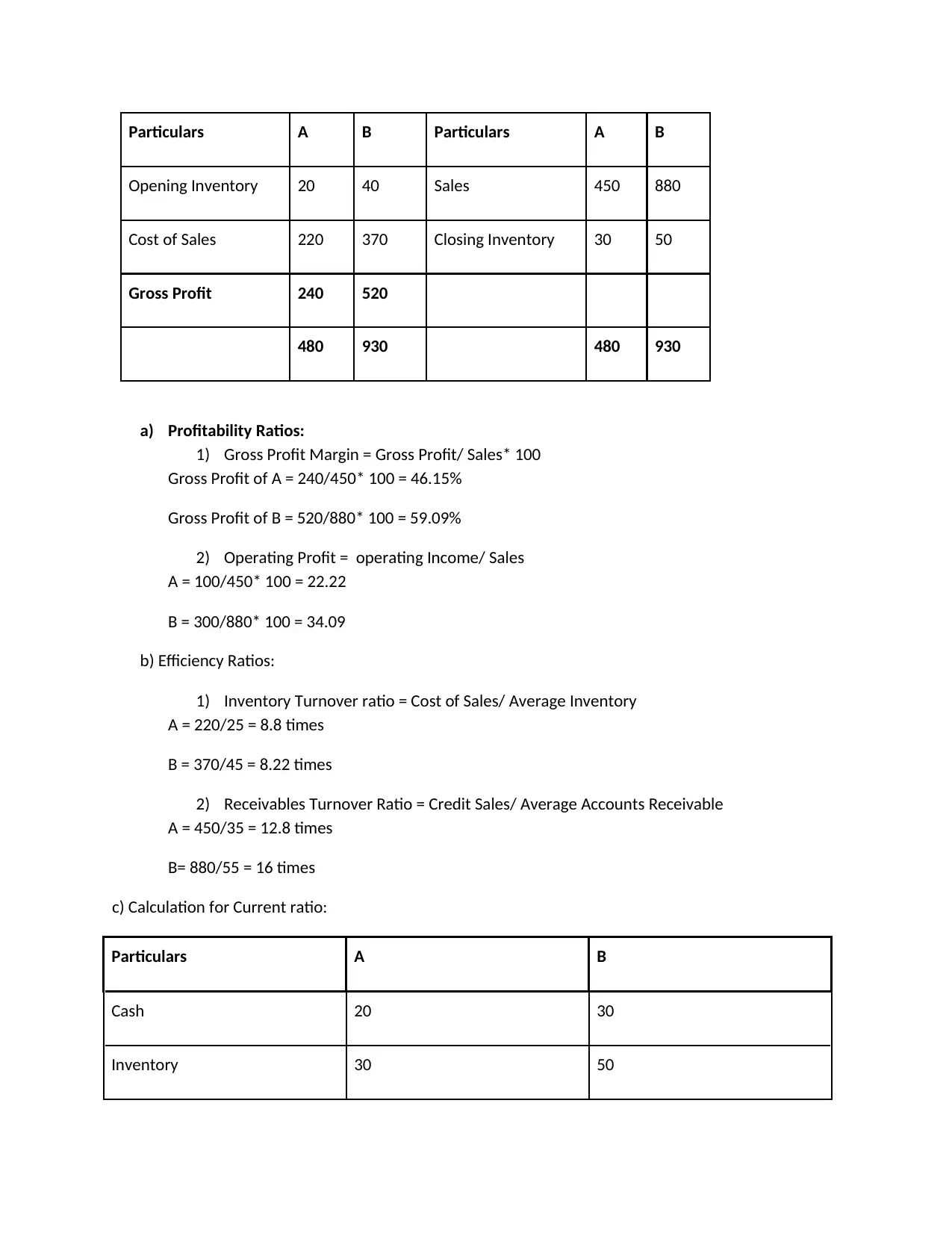

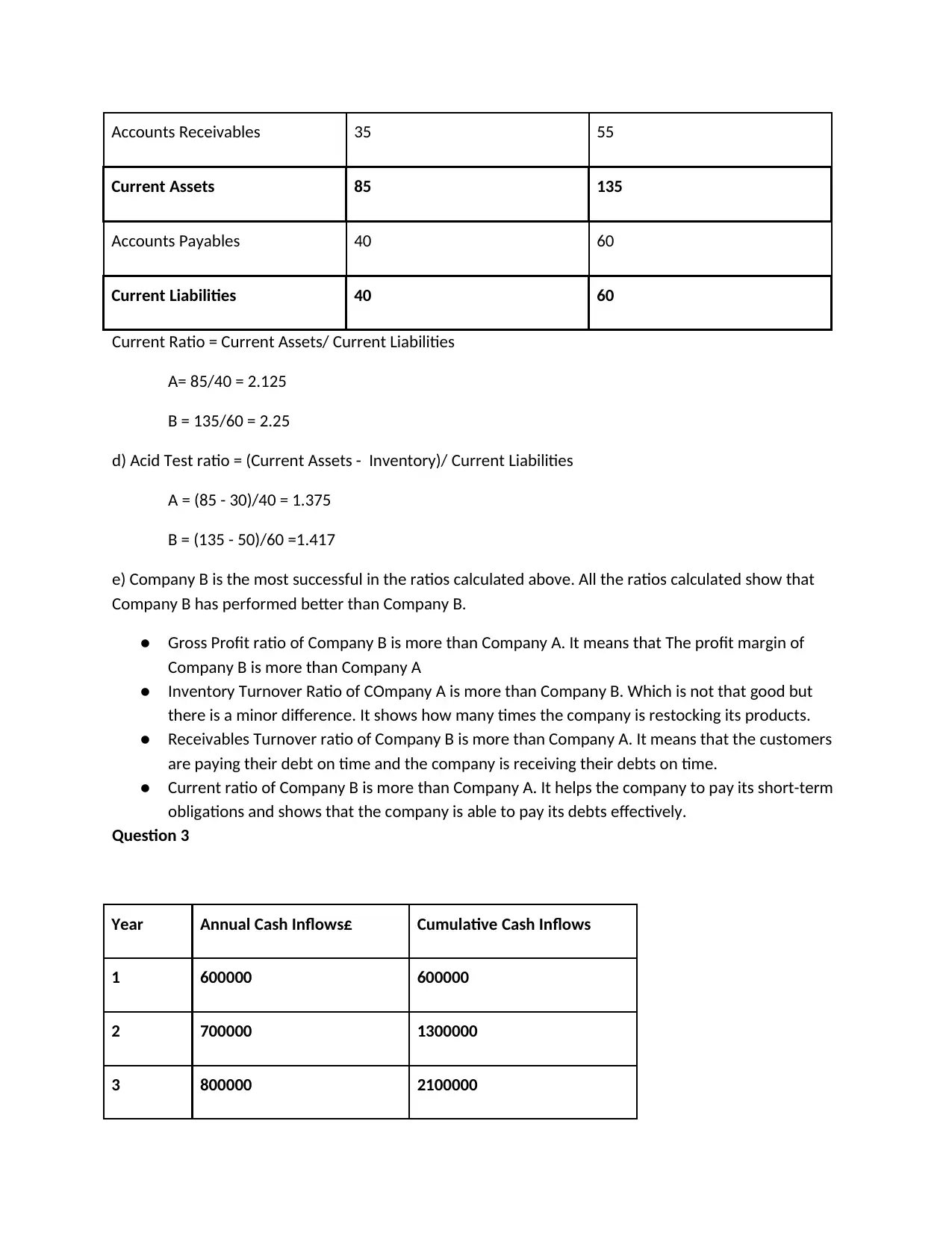

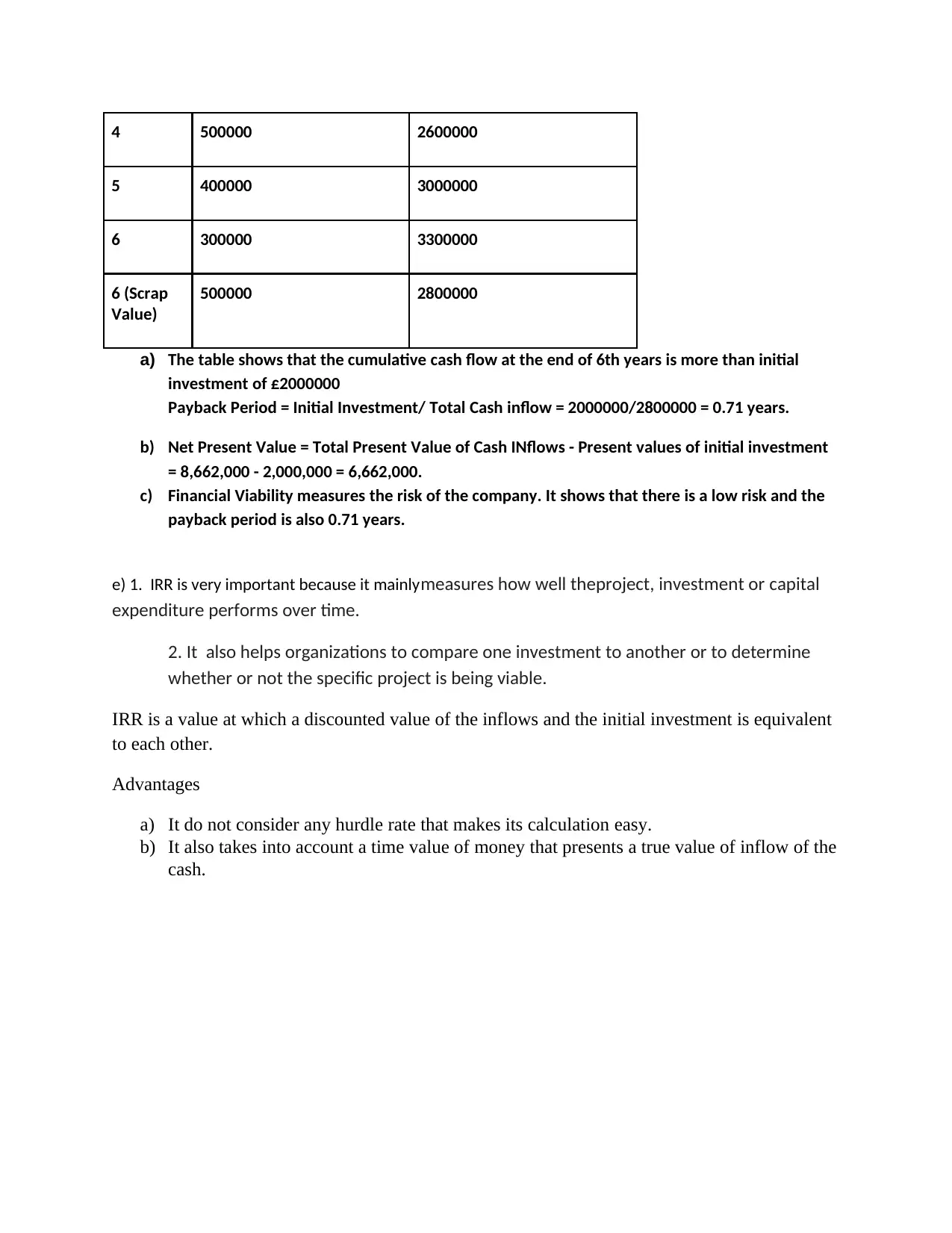

This assignment solution provides a detailed analysis of financial statements, including the preparation of an income statement and statement of financial position (SOFP). It covers the calculation and interpretation of profitability and efficiency ratios, such as gross profit margin, operating profit margin, inventory turnover, and receivables turnover. Furthermore, the solution includes a current ratio and acid-test ratio assessment for Companies A and B, determining Company B to be more successful based on these metrics. The assignment also addresses investment appraisal by calculating the payback period and net present value (NPV) for a project, concluding with an explanation of the importance and advantages of the internal rate of return (IRR). Desklib offers a wide range of solved assignments and past papers to support students in their studies.

1 out of 6

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.