Income Tax Assessment Act (ITAA) 1997 Assignment on Deductions

12 Pages2489 Words61 Views

Added on 2020-04-07

Income Tax Assessment Act (ITAA) 1997 Assignment on Deductions

Added on 2020-04-07

ShareRelated Documents

TAXATION LAW

TABLE OF CONTENTSQUESTION 1..................................................................................................................................1Introduction..................................................................................................................................1Legal Provisions...........................................................................................................................1Application...................................................................................................................................1Conclusion...................................................................................................................................3QUESTION 2..................................................................................................................................3Introduction..................................................................................................................................3Legal Provisions...........................................................................................................................3Application...................................................................................................................................4Conclusion...................................................................................................................................4Question 3........................................................................................................................................5Issue.............................................................................................................................................5Legal provisions...........................................................................................................................5Application of legal provisions....................................................................................................5Calculation...................................................................................................................................5Question 4........................................................................................................................................5Issue.............................................................................................................................................5Legal provisions...........................................................................................................................5Application of legal provisions....................................................................................................5Calculation...................................................................................................................................5REFERENCES................................................................................................................................6

QUESTION 1IntroductionThis segment explains whether the discussed scenarios are allowable as deductions unders 8-1 of the ITAA 1997 or not. Legal ProvisionsIncome tax is computed based on the assessable income of an individual. This assessableincome is computed by subtracting “specific” and “general” deductions from the gross income ofthe taxpayer for that year. A general deduction as per ITAA 1997 s 8-1 refers to a loss oroutgoing which is related to some income generating operations (e.g. investment or businessactivity), and is not of domestic, capital or private nature. On the contrary, a specific deduction isa sum which a provision except the general deduction provision permits as a deduction(Woellner et al., 2011). There are several deduction rejection provisions as well which prohibit deductions forcertain amounts. General Deductions under s 8-1 ITAA 1997:8-1(1) The tax payer can deduct from his/her taxable income any outgoing or loss to the limitthat:a)It is incurred in producing or gaining the taxable income; orb)It is incurred essentially to carry on a business to gain or produce the taxable income(D'Ascenzo and England, 2005).8-1(2) Nonetheless, the taxpayer cannot subtract any outgoing or loss under this Act to the limitthat:a)It is capital or of similar nature; or b)It is of domestic or private nature; orc)It is incurred to produce or gain the non-taxable non-exempt income or the exemptincome; ord)Any subsection of this section prohibits it from being deducted (Mete, Dick andMoerman, 2010). 1

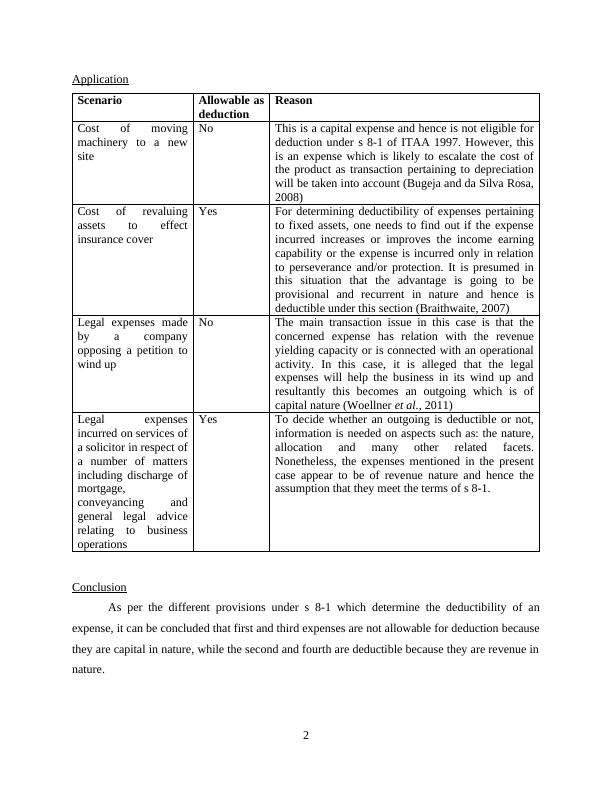

ApplicationScenarioAllowable asdeductionReasonCost of movingmachinery to a newsiteNoThis is a capital expense and hence is not eligible fordeduction under s 8-1 of ITAA 1997. However, thisis an expense which is likely to escalate the cost ofthe product as transaction pertaining to depreciationwill be taken into account (Bugeja and da Silva Rosa,2008)Cost of revaluingassets to effectinsurance coverYesFor determining deductibility of expenses pertainingto fixed assets, one needs to find out if the expenseincurred increases or improves the income earningcapability or the expense is incurred only in relationto perseverance and/or protection. It is presumed inthis situation that the advantage is going to beprovisional and recurrent in nature and hence isdeductible under this section (Braithwaite, 2007)Legal expenses madeby a companyopposing a petition towind upNoThe main transaction issue in this case is that theconcerned expense has relation with the revenueyielding capacity or is connected with an operationalactivity. In this case, it is alleged that the legalexpenses will help the business in its wind up andresultantly this becomes an outgoing which is ofcapital nature (Woellner et al., 2011)Legal expensesincurred on services ofa solicitor in respect ofa number of mattersincluding discharge ofmortgage,conveyancing andgeneral legal advicerelating to businessoperationsYesTo decide whether an outgoing is deductible or not,information is needed on aspects such as: the nature,allocation and many other related facets.Nonetheless, the expenses mentioned in the presentcase appear to be of revenue nature and hence theassumption that they meet the terms of s 8-1.ConclusionAs per the different provisions under s 8-1 which determine the deductibility of anexpense, it can be concluded that first and third expenses are not allowable for deduction becausethey are capital in nature, while the second and fourth are deductible because they are revenue innature.2

End of preview

Want to access all the pages? Upload your documents or become a member.

Related Documents

HI3042- Taxation Law Assignmentlg...

|10

|1743

|33

Income Tax Assessment Act 1997 (ITAA) | Taxation Law Assignmentlg...

|12

|2214

|82

HA3042 Assessment 2 Australian taxation law TABLE OF CONTENTSlg...

|10

|1522

|91

Taxation Law: Calculation of Net Income from Partnership and Fringe Benefit Taxationlg...

|13

|2590

|334

HI3042 Assignment on Taxation Lawlg...

|11

|2646

|38

Taxation Law Assignment Helplg...

|16

|4267

|69