TLAW 303 - Taxation Law: Income Tax Application & Calculation

VerifiedAdded on 2023/06/12

|8

|1837

|204

Homework Assignment

AI Summary

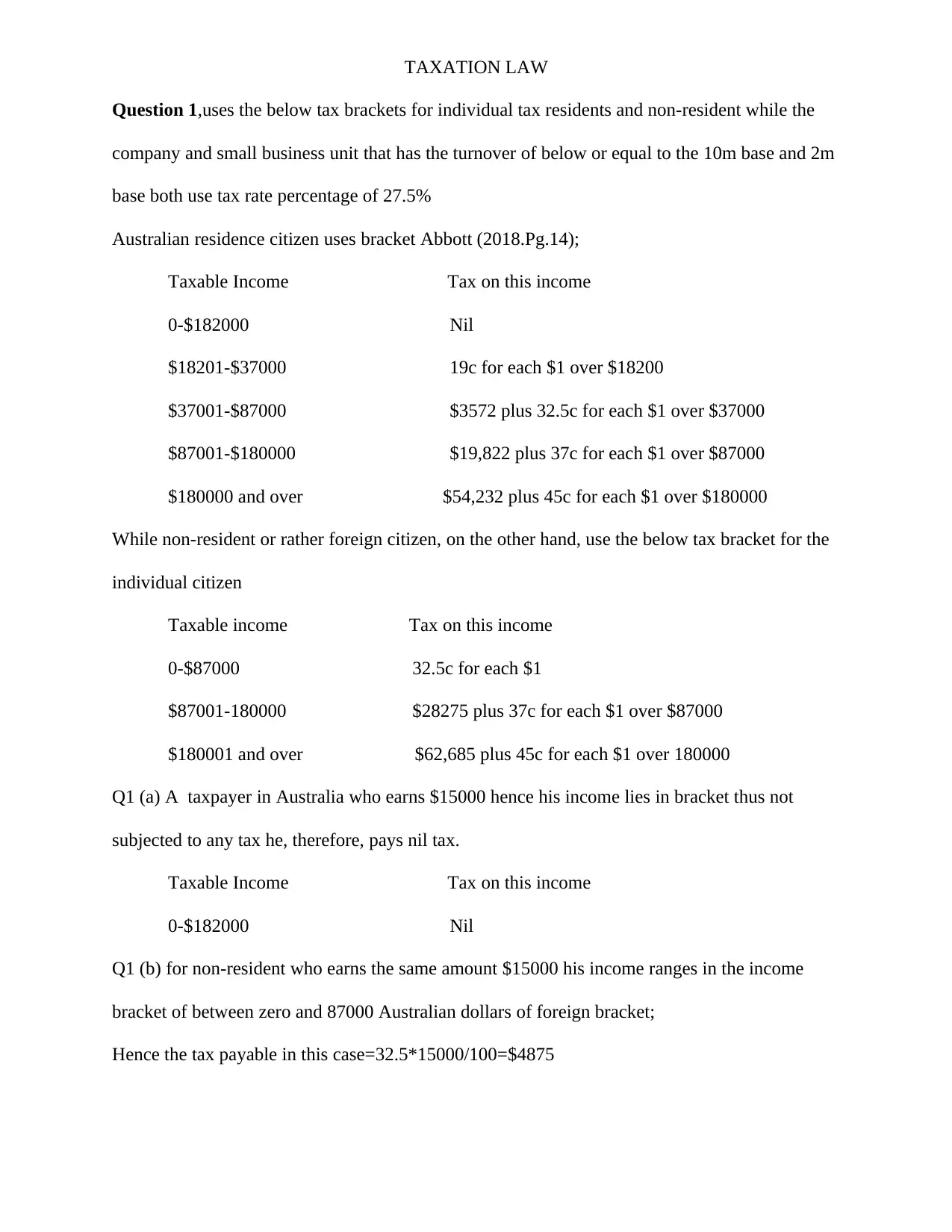

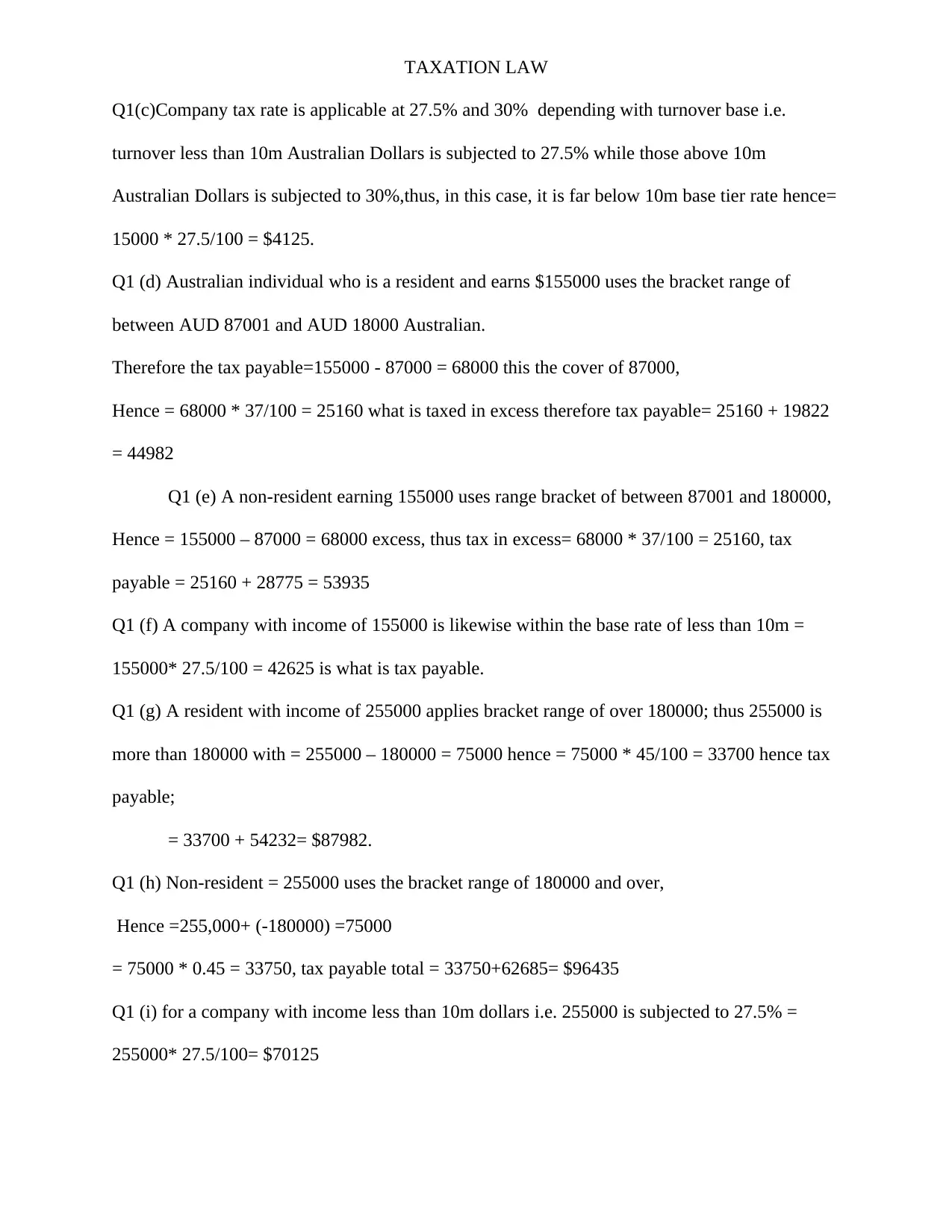

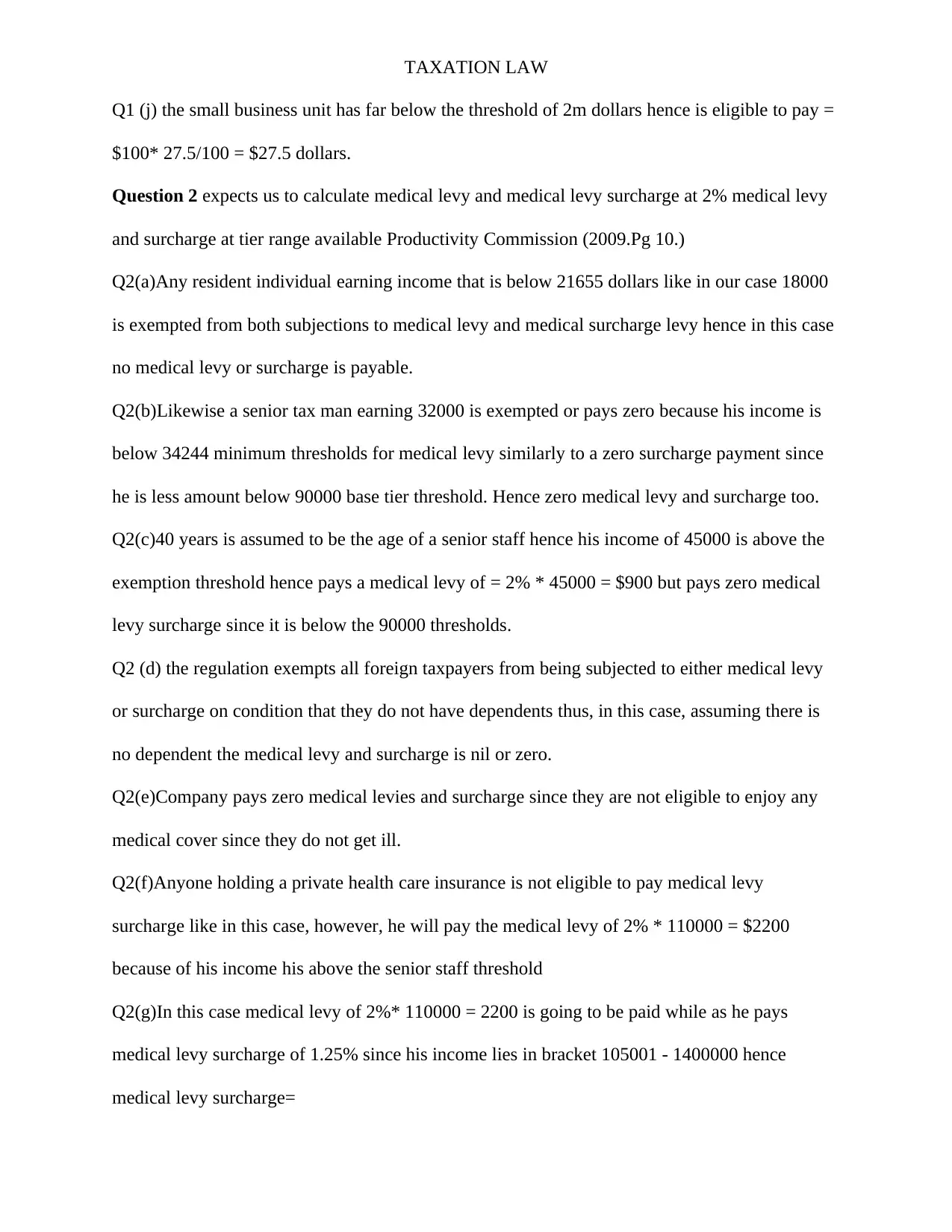

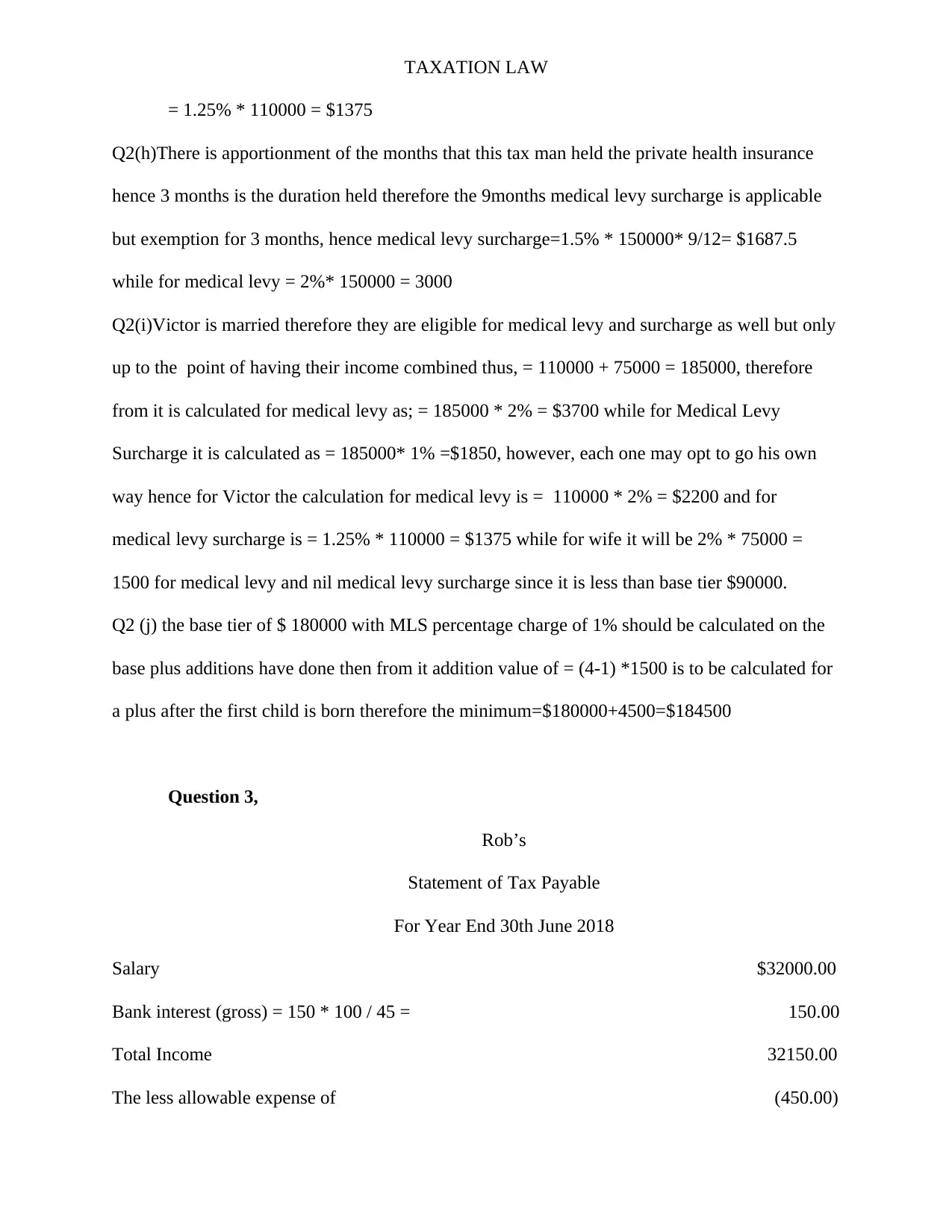

This assignment provides detailed solutions to several taxation law problems in the Australian context. It covers income tax calculations for both residents and non-residents, considering different income brackets and company tax rates. The assignment also addresses medical levy and medical levy surcharge calculations, taking into account factors such as private health insurance and family status. Furthermore, it includes calculations for taxable income, PAYG, and tax on dividends. The document is helpful for students studying Australian taxation law and looking for examples of tax calculations. Desklib offers more resources like this, including past papers and solved assignments.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.