HA3042 Taxation Law Assignment: Individual Assessment, T2 2019

VerifiedAdded on 2022/10/08

|13

|2862

|12

Homework Assignment

AI Summary

This assignment provides a detailed analysis of taxation law, addressing various aspects of tax liabilities and deductions. The first part of the assignment focuses on the capital gains tax (CGT) implications of selling different assets, including a home, a car, a cleaning business, furniture, and paintings. It examines pre-CGT assets, personal use assets, small business concessions, and the specific rules governing the taxation of collectables. The second part of the assignment delves into the depreciation of depreciating assets within the framework of the Income Tax Assessment Act 1997 (ITAA 97). It explores the relevant provisions, including general deductions, capital expenses, and the definition of depreciating assets. The assignment applies these principles to a case study involving a business purchasing a CNC machine, analyzing the cost base, and determining the start time for claiming depreciation deductions. The solution references relevant legislation and case law to support its arguments.

Running head: TAXATION LAW

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1TAXATION LAW

Table of Contents

Answer to question 1:.................................................................................................................2

Answer to question 2:.................................................................................................................6

References:...............................................................................................................................11

Table of Contents

Answer to question 1:.................................................................................................................2

Answer to question 2:.................................................................................................................6

References:...............................................................................................................................11

2TAXATION LAW

Answer to question 1:

Sale of home:

The income tax liability of an individual usually takes into account the net capital

gains. On 20 sept 1985 the CGT began and carries the capital receipts in the tax base. Only

those assets that are purchased after this date is included into the tax base while the assets that

are purchased before this is not included in the tax base (Spence 2016). The purchased before

20/9/1985 is called as Pre-CGT asset and commonly it is exempted from tax.

Jasmine is selling the home in which she lived. She purchased the home in 1981 by

paying $40,000. But she is selling tit for $650,000. So it can be said that Jasmine’s home is a

pre-CGT asset because Jasmine has purchased in 1981 which is before the commencement of

CGT rule in 20/9/1985. The capital gains is exempted from the main home as the asset is a

pre-CGT asset and no tax is payable in this situation by Jasmine.

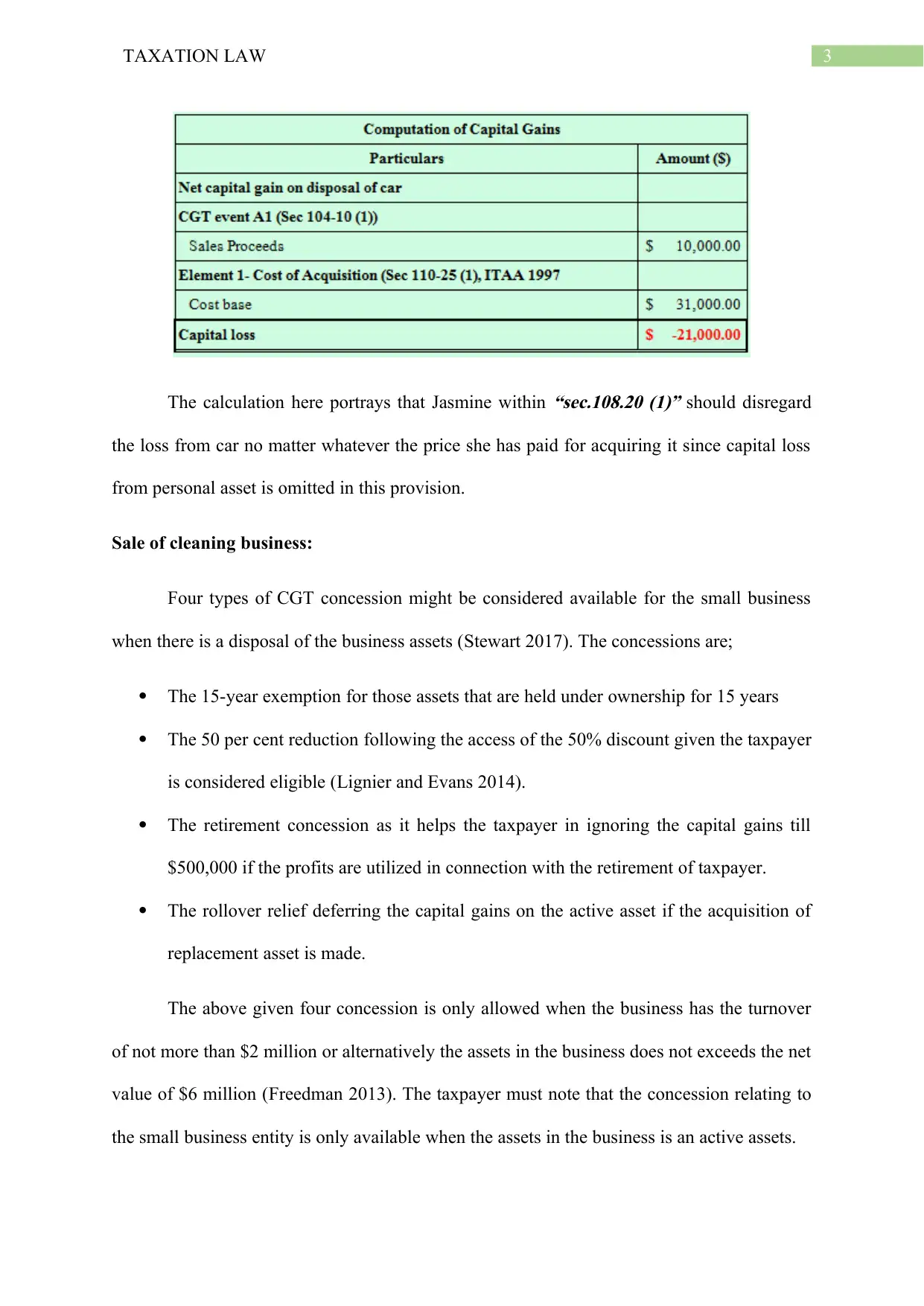

Sale of car:

Well-defined as one of the asset, under

“sec 108.20 (2)”, personal use asset that is

kept or used for private purpose includes the TV at home, private use mobile phone, private

use vehicle or a bicycle (Steyn et al. 2018). When there is a capital loss suffered from sale of

personal asset it is omitted in

“s.108.20 (1)”. Jasmine here acquired a car at a cost of $31,000

in 2011. Accordingly, within

“s.108.20 (2)”, car is a personal use asset.

Answer to question 1:

Sale of home:

The income tax liability of an individual usually takes into account the net capital

gains. On 20 sept 1985 the CGT began and carries the capital receipts in the tax base. Only

those assets that are purchased after this date is included into the tax base while the assets that

are purchased before this is not included in the tax base (Spence 2016). The purchased before

20/9/1985 is called as Pre-CGT asset and commonly it is exempted from tax.

Jasmine is selling the home in which she lived. She purchased the home in 1981 by

paying $40,000. But she is selling tit for $650,000. So it can be said that Jasmine’s home is a

pre-CGT asset because Jasmine has purchased in 1981 which is before the commencement of

CGT rule in 20/9/1985. The capital gains is exempted from the main home as the asset is a

pre-CGT asset and no tax is payable in this situation by Jasmine.

Sale of car:

Well-defined as one of the asset, under

“sec 108.20 (2)”, personal use asset that is

kept or used for private purpose includes the TV at home, private use mobile phone, private

use vehicle or a bicycle (Steyn et al. 2018). When there is a capital loss suffered from sale of

personal asset it is omitted in

“s.108.20 (1)”. Jasmine here acquired a car at a cost of $31,000

in 2011. Accordingly, within

“s.108.20 (2)”, car is a personal use asset.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3TAXATION LAW

The calculation here portrays that Jasmine within

“sec.108.20 (1)” should disregard

the loss from car no matter whatever the price she has paid for acquiring it since capital loss

from personal asset is omitted in this provision.

Sale of cleaning business:

Four types of CGT concession might be considered available for the small business

when there is a disposal of the business assets (Stewart 2017). The concessions are;

The 15-year exemption for those assets that are held under ownership for 15 years

The 50 per cent reduction following the access of the 50% discount given the taxpayer

is considered eligible (Lignier and Evans 2014).

The retirement concession as it helps the taxpayer in ignoring the capital gains till

$500,000 if the profits are utilized in connection with the retirement of taxpayer.

The rollover relief deferring the capital gains on the active asset if the acquisition of

replacement asset is made.

The above given four concession is only allowed when the business has the turnover

of not more than $2 million or alternatively the assets in the business does not exceeds the net

value of $6 million (Freedman 2013). The taxpayer must note that the concession relating to

the small business entity is only available when the assets in the business is an active assets.

The calculation here portrays that Jasmine within

“sec.108.20 (1)” should disregard

the loss from car no matter whatever the price she has paid for acquiring it since capital loss

from personal asset is omitted in this provision.

Sale of cleaning business:

Four types of CGT concession might be considered available for the small business

when there is a disposal of the business assets (Stewart 2017). The concessions are;

The 15-year exemption for those assets that are held under ownership for 15 years

The 50 per cent reduction following the access of the 50% discount given the taxpayer

is considered eligible (Lignier and Evans 2014).

The retirement concession as it helps the taxpayer in ignoring the capital gains till

$500,000 if the profits are utilized in connection with the retirement of taxpayer.

The rollover relief deferring the capital gains on the active asset if the acquisition of

replacement asset is made.

The above given four concession is only allowed when the business has the turnover

of not more than $2 million or alternatively the assets in the business does not exceeds the net

value of $6 million (Freedman 2013). The taxpayer must note that the concession relating to

the small business entity is only available when the assets in the business is an active assets.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4TAXATION LAW

The circumstances that has contributed to the scenario of Jasmine portrays that she is

retiring from her small business of cleaning that she has operated from a long time. Jasmine

has found a buyer that agreed to take up the assets for $65,000 and the goodwill of business

for $60,000. The taxpayer here Jasmine is considered qualified under

“Div 152” of the small

business concession regime because the net value of asset is not higher than $6 million and

the assets that she is selling is an active asset. The 15-year concession is allowed to Jasmine

under

“SubDiv 152-B” because she kept the asset under her ownership for 15 years and also

the minimum qualifying age of 55 years or more is also satisfied by Jasmine.

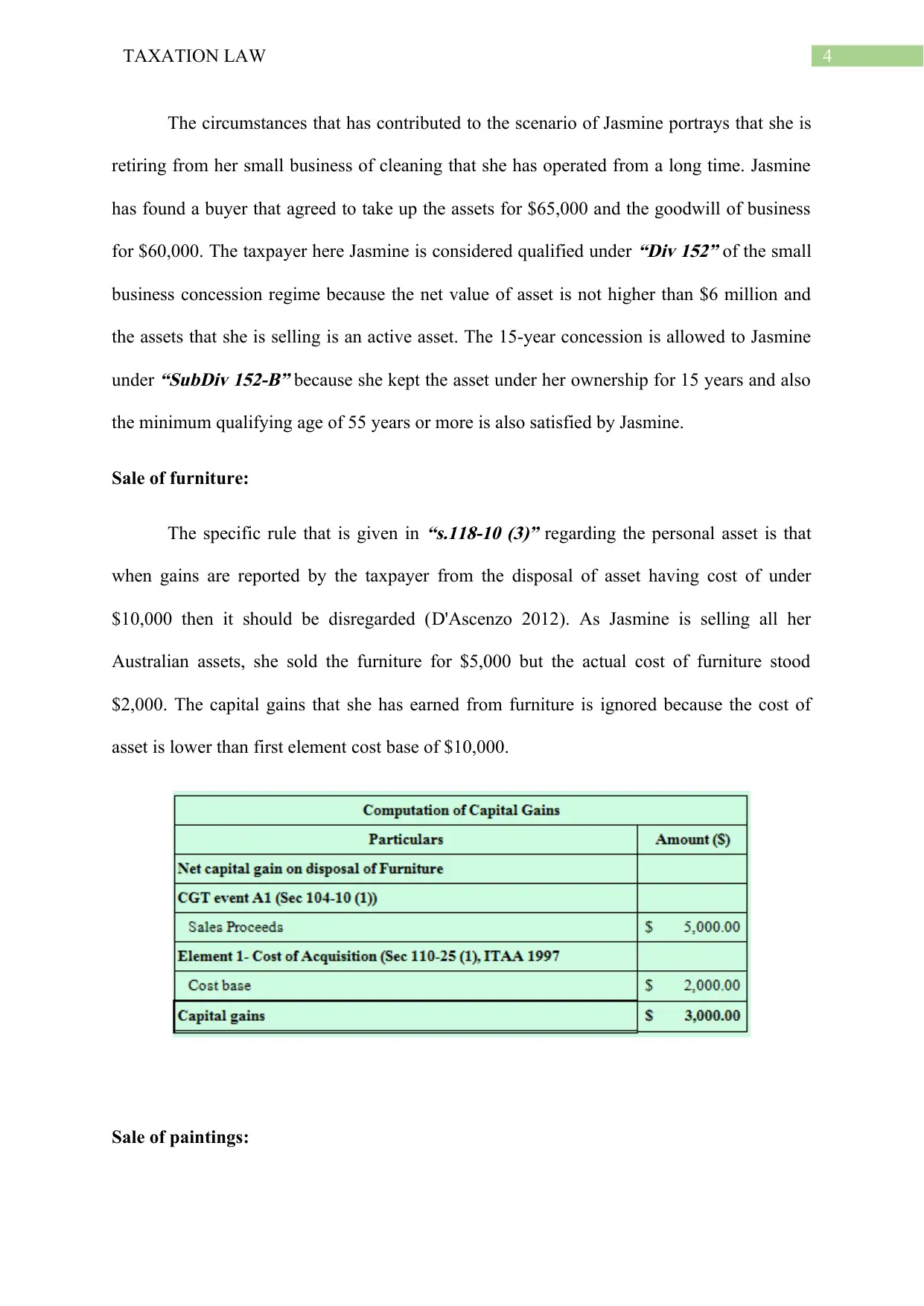

Sale of furniture:

The specific rule that is given in

“s.118-10 (3)” regarding the personal asset is that

when gains are reported by the taxpayer from the disposal of asset having cost of under

$10,000 then it should be disregarded (D'Ascenzo 2012). As Jasmine is selling all her

Australian assets, she sold the furniture for $5,000 but the actual cost of furniture stood

$2,000. The capital gains that she has earned from furniture is ignored because the cost of

asset is lower than first element cost base of $10,000.

Sale of paintings:

The circumstances that has contributed to the scenario of Jasmine portrays that she is

retiring from her small business of cleaning that she has operated from a long time. Jasmine

has found a buyer that agreed to take up the assets for $65,000 and the goodwill of business

for $60,000. The taxpayer here Jasmine is considered qualified under

“Div 152” of the small

business concession regime because the net value of asset is not higher than $6 million and

the assets that she is selling is an active asset. The 15-year concession is allowed to Jasmine

under

“SubDiv 152-B” because she kept the asset under her ownership for 15 years and also

the minimum qualifying age of 55 years or more is also satisfied by Jasmine.

Sale of furniture:

The specific rule that is given in

“s.118-10 (3)” regarding the personal asset is that

when gains are reported by the taxpayer from the disposal of asset having cost of under

$10,000 then it should be disregarded (D'Ascenzo 2012). As Jasmine is selling all her

Australian assets, she sold the furniture for $5,000 but the actual cost of furniture stood

$2,000. The capital gains that she has earned from furniture is ignored because the cost of

asset is lower than first element cost base of $10,000.

Sale of paintings:

5TAXATION LAW

Defined as asset in

“sec.108-10 (2)”, collectable involves the artwork, medals, rare

stamps, coins etc. If they are acquired for more than $500 then capital gains is taxed and any

loss is carried forward to next year under

“sec.108.10 (1)” (Evans et al. 2014).

Finally Jasmine lot of paintings and none of the paintings has the cost of higher than

$500. While Jasmine sold all the paintings and made $35,000. Accordingly Jasmine has sold

all the paintings for capital gains but not of her painting cost more than $500 so capital gains

is exempted

“sec.108.10 (1)”.

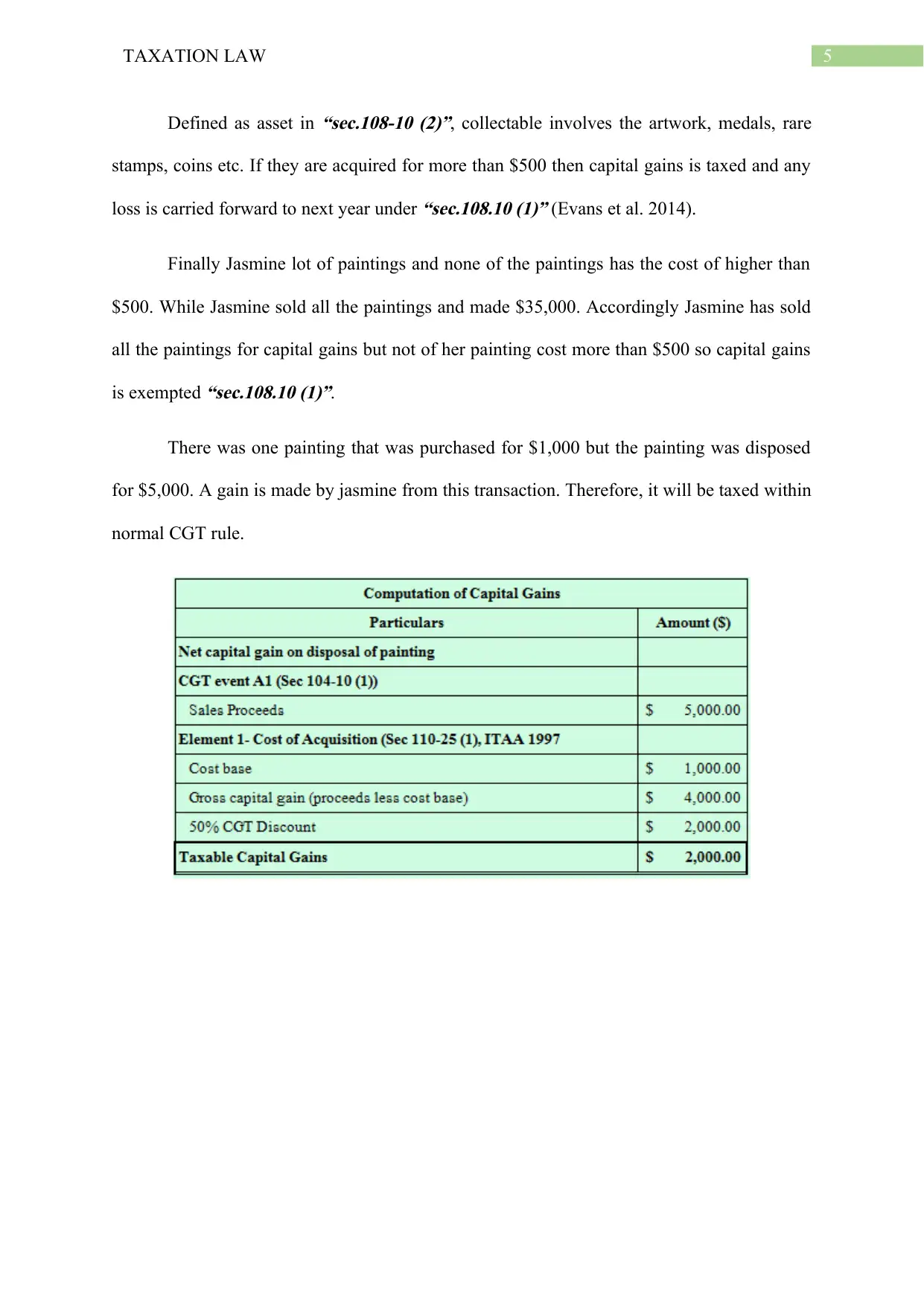

There was one painting that was purchased for $1,000 but the painting was disposed

for $5,000. A gain is made by jasmine from this transaction. Therefore, it will be taxed within

normal CGT rule.

Defined as asset in

“sec.108-10 (2)”, collectable involves the artwork, medals, rare

stamps, coins etc. If they are acquired for more than $500 then capital gains is taxed and any

loss is carried forward to next year under

“sec.108.10 (1)” (Evans et al. 2014).

Finally Jasmine lot of paintings and none of the paintings has the cost of higher than

$500. While Jasmine sold all the paintings and made $35,000. Accordingly Jasmine has sold

all the paintings for capital gains but not of her painting cost more than $500 so capital gains

is exempted

“sec.108.10 (1)”.

There was one painting that was purchased for $1,000 but the painting was disposed

for $5,000. A gain is made by jasmine from this transaction. Therefore, it will be taxed within

normal CGT rule.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6TAXATION LAW

Answer to question 2:

Issues:

The problem that is taken in the existing case is related to the entitlement associated

depreciation of depreciating asset inside the

“Div 40 of the ITAA 97”.

Rule:

The specific provision enables an in individual taxpayer with the deduction based on

the period of time given that the expenditure is mostly happened for deriving a benefit. There

are three types of deductible capital expenses namely the depreciation deduction, capital

works deduction and the black expenditure. Within the negative limbs of

“sec.8-1(2)(a)” a

general deduction is not given to the taxpayer for the capital items (Burman 2014). This is

because upon purchasing the depreciating asset, it is treated as having capital in nature and no

deduction for the same is permitted inside

“sec.8.1”. Outgoings that happens on the plant and

equipment portrays the manner in which a business earns profit and the manner in which the

plant is used for deriving income. In

“FC of T v SunNewspaper [1938]” the income making

arrangement portrays that the outgoing occurred in regard to the business unit is regarded as

capital.

By focussing on the

“Div-40” when certain are employed in the production of income

the deductions relating to it is allowed to the taxpayers. As allowed in

“sec.40.25 (1)”

depreciation should not be interpreted as costs or charge and when an asset is purchased it is

termed as capital in nature so the provision of

“s.8.1” is not allowed to operate (Grudnoff

2015). While inside the

“sec.40-25(2)” the private use of the depreciating asset is simply

apportioned and only taxable purpose is included for depreciation under

“sec.40.25 (1)”. As

noted in the

“s.40.25 (1)” deduction may be allowed for claim only to the extent of falling

Answer to question 2:

Issues:

The problem that is taken in the existing case is related to the entitlement associated

depreciation of depreciating asset inside the

“Div 40 of the ITAA 97”.

Rule:

The specific provision enables an in individual taxpayer with the deduction based on

the period of time given that the expenditure is mostly happened for deriving a benefit. There

are three types of deductible capital expenses namely the depreciation deduction, capital

works deduction and the black expenditure. Within the negative limbs of

“sec.8-1(2)(a)” a

general deduction is not given to the taxpayer for the capital items (Burman 2014). This is

because upon purchasing the depreciating asset, it is treated as having capital in nature and no

deduction for the same is permitted inside

“sec.8.1”. Outgoings that happens on the plant and

equipment portrays the manner in which a business earns profit and the manner in which the

plant is used for deriving income. In

“FC of T v SunNewspaper [1938]” the income making

arrangement portrays that the outgoing occurred in regard to the business unit is regarded as

capital.

By focussing on the

“Div-40” when certain are employed in the production of income

the deductions relating to it is allowed to the taxpayers. As allowed in

“sec.40.25 (1)”

depreciation should not be interpreted as costs or charge and when an asset is purchased it is

termed as capital in nature so the provision of

“s.8.1” is not allowed to operate (Grudnoff

2015). While inside the

“sec.40-25(2)” the private use of the depreciating asset is simply

apportioned and only taxable purpose is included for depreciation under

“sec.40.25 (1)”. As

noted in the

“s.40.25 (1)” deduction may be allowed for claim only to the extent of falling

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION LAW

value of

“depreciating asset”. As eminent deduction for depreciation is only permitted till

the projected useful life of the asset.

The rules of the depreciation is not applicable in some of the circumstances. These are

as follows;

a. Outgoings occurred on the capital works such as buildings

b. Car expenditure where the deduction is computed on the basis of the cents per

kilometre method (Twite 2014).

c. Depreciating asset that is used of installed within the residential rental property.

It is to be noted that inside

“sec.40.30 (1)” explanation amounting to depreciating

asset is given. An asset which only has estimated active life and also the asset is further likely

to decrease in price with the passage of time over its use. The definition does not takes into

the account the following assets;

Land

An item associated to the trading stock; or

Certain forms of intangible assets, unless it is listed in the

“sec.40.30 (2)” such

as the in-house software, items associated to intellectual property.

The common items of depreciating asset includes the furniture, cars, machinery etc.

The taxpayers are required to note that the expression asset has no own definition and

consequently should be provided its ordinary meaning, based on the specific appropriateness

of the capital allowance provision (Evans et al. 2014). The ordinary meaning of the plant was

considered by court in

“France v Yarmouth [1987]”. Based on the ordinary sense plant

amounts to whatsoever apparatus that a business man make use of in conducting their

business.

value of

“depreciating asset”. As eminent deduction for depreciation is only permitted till

the projected useful life of the asset.

The rules of the depreciation is not applicable in some of the circumstances. These are

as follows;

a. Outgoings occurred on the capital works such as buildings

b. Car expenditure where the deduction is computed on the basis of the cents per

kilometre method (Twite 2014).

c. Depreciating asset that is used of installed within the residential rental property.

It is to be noted that inside

“sec.40.30 (1)” explanation amounting to depreciating

asset is given. An asset which only has estimated active life and also the asset is further likely

to decrease in price with the passage of time over its use. The definition does not takes into

the account the following assets;

Land

An item associated to the trading stock; or

Certain forms of intangible assets, unless it is listed in the

“sec.40.30 (2)” such

as the in-house software, items associated to intellectual property.

The common items of depreciating asset includes the furniture, cars, machinery etc.

The taxpayers are required to note that the expression asset has no own definition and

consequently should be provided its ordinary meaning, based on the specific appropriateness

of the capital allowance provision (Evans et al. 2014). The ordinary meaning of the plant was

considered by court in

“France v Yarmouth [1987]”. Based on the ordinary sense plant

amounts to whatsoever apparatus that a business man make use of in conducting their

business.

8TAXATION LAW

The cost of the depreciating asset mostly needs to be calculated and the rules

regarding the calculation of the cost of asset is listed in

“Subdiv. 40-C”. In most likely

situation the depreciation asset cost does not generally considers only the purchase price.

Apart from this there is also the incidental cost that is incurred at the time of delivery of asset

and the installation cost occurred in installing the asset (Marsden, Sadiq and Wilkins 2013).

There may be instances when some small expense may also happen or be incurred in

rearranging removing for accommodation of the new plant. Any such expenses incurred in

this respect is also added in the cost. The deprecating asset cost under

“sec.40.175” is

classified inside two elements. The specific rules is related to first element under

“sec.40-

180” that normally involves the purchase price. While

“sec.40.190” widely consists of the

delivery charge, installation charge and improvements made to the asset that are capital in

nature.

When it is noticed that a taxpayer is holding the asset then the decrease in worth

happens based on its start time. The start time of asset commonly involves the first use made

by taxpayer under

“sec.40.60 (1)”. The start time for decline in value happens when the

machine is also installed as all ready to use for producing income in business (Burkhauser,

Hahn and Wilkins 2015). It may also include the private purpose when the asset is used by

the taxpayer for non-taxable purpose and no deduction is permitted in this regard.

Application:

Referring to the rulings that is explained in context of the capital allowance regime,

the same has been applied in the given facts of John. The facts that is gained upon looking in

the case of John it is agreed that he is the producer of BMW vehicle parts. John arrived in

Germany to inspect about the computer numerical machine in the CNC machine factory. On

making the inspection about the machine he ultimately decided to purchase it. The purchase

The cost of the depreciating asset mostly needs to be calculated and the rules

regarding the calculation of the cost of asset is listed in

“Subdiv. 40-C”. In most likely

situation the depreciation asset cost does not generally considers only the purchase price.

Apart from this there is also the incidental cost that is incurred at the time of delivery of asset

and the installation cost occurred in installing the asset (Marsden, Sadiq and Wilkins 2013).

There may be instances when some small expense may also happen or be incurred in

rearranging removing for accommodation of the new plant. Any such expenses incurred in

this respect is also added in the cost. The deprecating asset cost under

“sec.40.175” is

classified inside two elements. The specific rules is related to first element under

“sec.40-

180” that normally involves the purchase price. While

“sec.40.190” widely consists of the

delivery charge, installation charge and improvements made to the asset that are capital in

nature.

When it is noticed that a taxpayer is holding the asset then the decrease in worth

happens based on its start time. The start time of asset commonly involves the first use made

by taxpayer under

“sec.40.60 (1)”. The start time for decline in value happens when the

machine is also installed as all ready to use for producing income in business (Burkhauser,

Hahn and Wilkins 2015). It may also include the private purpose when the asset is used by

the taxpayer for non-taxable purpose and no deduction is permitted in this regard.

Application:

Referring to the rulings that is explained in context of the capital allowance regime,

the same has been applied in the given facts of John. The facts that is gained upon looking in

the case of John it is agreed that he is the producer of BMW vehicle parts. John arrived in

Germany to inspect about the computer numerical machine in the CNC machine factory. On

making the inspection about the machine he ultimately decided to purchase it. The purchase

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9TAXATION LAW

for the machinery stood $300,000. Upon purchasing the CNC machine, it is treated as having

capital in nature and no deduction for the machinery is permitted inside

“sec.8.1”. Referring

to

“FC of T v SunNewspaper [1938]” the CNC machine is an income making arrangement

that represents outgoing occurred in regard to the business unit and must be regarded as

capital outgoing.

John instead to emphasis on the Div-40 as deductions relating to it CNC is allowed in

“sec.40.25 (1)”. Noting the

“s.40.25 (1)” deduction may be allowed for claim only to the

extent of falling value of CNC machine. The CNC machine is meeting the definition of

depreciating asset within

“sec.40.30 (1)” because CNC only has estimated active life and it is

further likely to decrease in price with the passage of time over its use (Dabner 2015).

Referring

“France v Yarmouth [1987]” the CNC machine is an apparatus that John intends

to make use of in conducting his business activities.

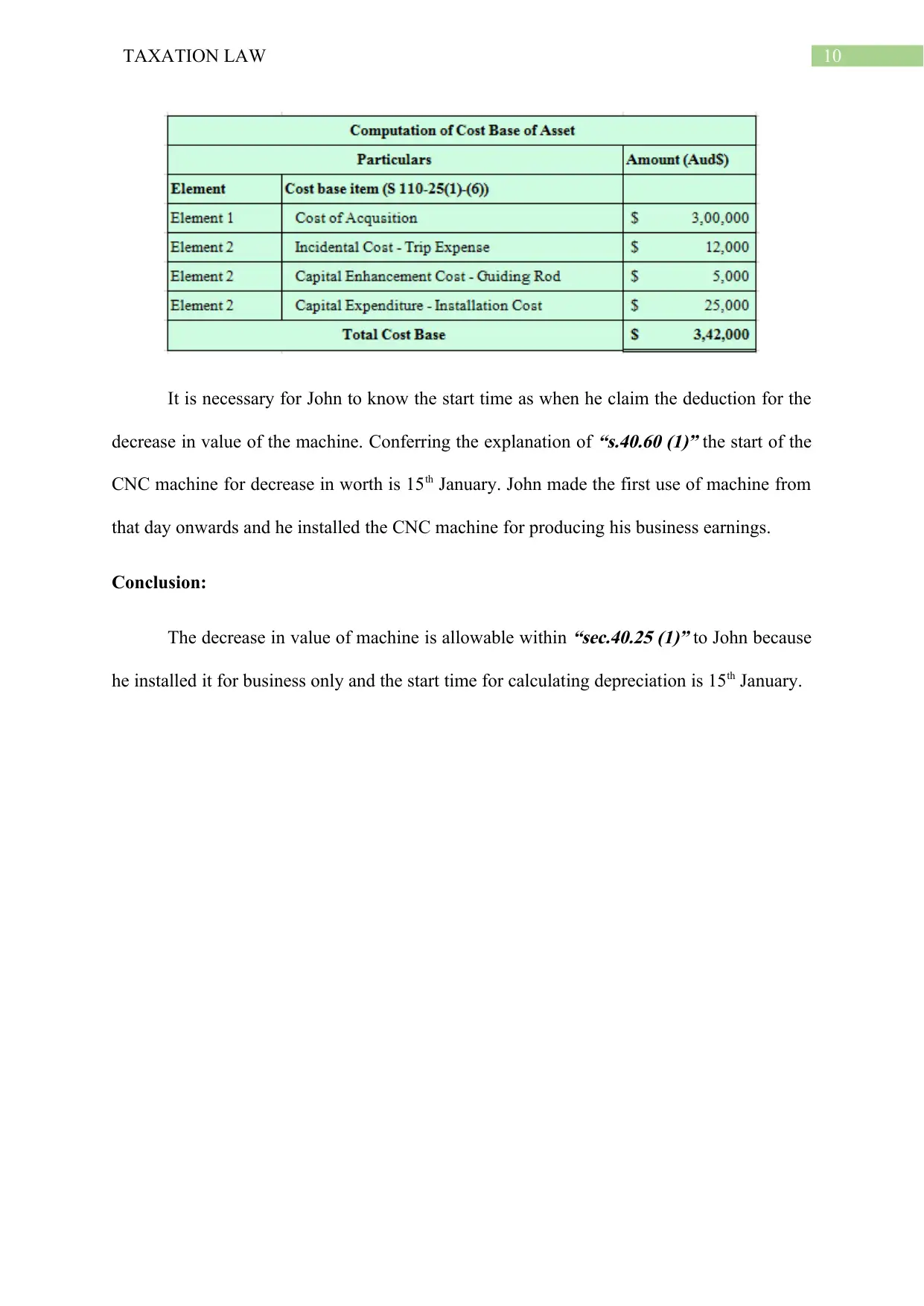

To compute the cost of CNC machine for depreciation purpose

“Subdiv. 40-C” is

referred in case of John. The purchase price that John has paid for the machine is added in

first element cost base. John paid cost for installing the machine and also made a capital

improvement on it by further installing a guiding rod to extract better performance from the

machine. These cost will be added in the second element cost base with respect to

“sec.40.190”.

The cost base of CNC machine are as follows;

for the machinery stood $300,000. Upon purchasing the CNC machine, it is treated as having

capital in nature and no deduction for the machinery is permitted inside

“sec.8.1”. Referring

to

“FC of T v SunNewspaper [1938]” the CNC machine is an income making arrangement

that represents outgoing occurred in regard to the business unit and must be regarded as

capital outgoing.

John instead to emphasis on the Div-40 as deductions relating to it CNC is allowed in

“sec.40.25 (1)”. Noting the

“s.40.25 (1)” deduction may be allowed for claim only to the

extent of falling value of CNC machine. The CNC machine is meeting the definition of

depreciating asset within

“sec.40.30 (1)” because CNC only has estimated active life and it is

further likely to decrease in price with the passage of time over its use (Dabner 2015).

Referring

“France v Yarmouth [1987]” the CNC machine is an apparatus that John intends

to make use of in conducting his business activities.

To compute the cost of CNC machine for depreciation purpose

“Subdiv. 40-C” is

referred in case of John. The purchase price that John has paid for the machine is added in

first element cost base. John paid cost for installing the machine and also made a capital

improvement on it by further installing a guiding rod to extract better performance from the

machine. These cost will be added in the second element cost base with respect to

“sec.40.190”.

The cost base of CNC machine are as follows;

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10TAXATION LAW

It is necessary for John to know the start time as when he claim the deduction for the

decrease in value of the machine. Conferring the explanation of

“s.40.60 (1)” the start of the

CNC machine for decrease in worth is 15th January. John made the first use of machine from

that day onwards and he installed the CNC machine for producing his business earnings.

Conclusion:

The decrease in value of machine is allowable within

“sec.40.25 (1)” to John because

he installed it for business only and the start time for calculating depreciation is 15th January.

It is necessary for John to know the start time as when he claim the deduction for the

decrease in value of the machine. Conferring the explanation of

“s.40.60 (1)” the start of the

CNC machine for decrease in worth is 15th January. John made the first use of machine from

that day onwards and he installed the CNC machine for producing his business earnings.

Conclusion:

The decrease in value of machine is allowable within

“sec.40.25 (1)” to John because

he installed it for business only and the start time for calculating depreciation is 15th January.

11TAXATION LAW

References:

Burkhauser, R.V., Hahn, M.H. and Wilkins, R., 2015. Measuring top incomes using tax

record data: A cautionary tale from Australia. The Journal of Economic Inequality, 13(2),

pp.181-205.

Burman, L., 2014. Taxing Capital Gains in Australia: Assessment and

Recommendations'. Australian Business Tax Reform in Retrospect and Prospect.

Dabner, J., 2015. Tax Simplification–An Accident Looking for a Place to

Happen?. Available at SSRN 2707910.

D'Ascenzo, M., 2012. Taxation Law Design. J. Austl. Tax'n, 5, p.34.

Evans, C., Hansford, A., Hasseldine, J., Lignier, P., Smulders, S. and Vaillancourt, F., 2014.

Small business and tax compliance costs: A cross-country study of managerial benefits and

tax concessions. eJTR, 12, p.453.

Evans, C., Hansford, A., Hasseldine, J., Lignier, P., Smulders, S. and Vaillancourt, F., 2014.

Small business and tax compliance costs: A cross-country study of managerial benefits and

tax concessions. eJTR, 12, p.453.

Freedman, J., 2013. Small business taxation: Policy issues and the UK. Taxing Small

Business: Developing Good Tax Policies, pp.13-43.

Grudnoff, M., 2015. Top gears: how negative gearing and the capital gains tax discount

benefit the top 10 per cent and drive up house prices.

Lignier, P. and Evans, C., 2014, August. The rise and rise of tax compliance costs for the

small business sector in Australia. In Australian Tax Forum (Vol. 27, No. 3, pp. 615-672).

References:

Burkhauser, R.V., Hahn, M.H. and Wilkins, R., 2015. Measuring top incomes using tax

record data: A cautionary tale from Australia. The Journal of Economic Inequality, 13(2),

pp.181-205.

Burman, L., 2014. Taxing Capital Gains in Australia: Assessment and

Recommendations'. Australian Business Tax Reform in Retrospect and Prospect.

Dabner, J., 2015. Tax Simplification–An Accident Looking for a Place to

Happen?. Available at SSRN 2707910.

D'Ascenzo, M., 2012. Taxation Law Design. J. Austl. Tax'n, 5, p.34.

Evans, C., Hansford, A., Hasseldine, J., Lignier, P., Smulders, S. and Vaillancourt, F., 2014.

Small business and tax compliance costs: A cross-country study of managerial benefits and

tax concessions. eJTR, 12, p.453.

Evans, C., Hansford, A., Hasseldine, J., Lignier, P., Smulders, S. and Vaillancourt, F., 2014.

Small business and tax compliance costs: A cross-country study of managerial benefits and

tax concessions. eJTR, 12, p.453.

Freedman, J., 2013. Small business taxation: Policy issues and the UK. Taxing Small

Business: Developing Good Tax Policies, pp.13-43.

Grudnoff, M., 2015. Top gears: how negative gearing and the capital gains tax discount

benefit the top 10 per cent and drive up house prices.

Lignier, P. and Evans, C., 2014, August. The rise and rise of tax compliance costs for the

small business sector in Australia. In Australian Tax Forum (Vol. 27, No. 3, pp. 615-672).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

12TAXATION LAW

Marsden, S., Sadiq, K. and Wilkins, T., 2013. Small business entity tax concessions: Through

the eyes of the practitioner. Revenue Law Journal, 22(1), p.6731.

Spence, K., 2016. The evolution of corporate taxation-a work in progress. Austl. Tax F., 31,

p.481.

Stewart, M., 2017. Australia’s Hybrid International Tax System: Limited Focus on Tax and

Development. In Taxation and Development-A Comparative Study (pp. 17-41). Springer,

Cham.

Steyn, T., Smulders, S., Stark, K. and Penning, I., 2018. Capital gains tax research: an initial

synthesis of the literature. eJTR, 16, p.278.

Twite, G., 2014. Capital structure choices and taxes: Evidence from the Australian dividend

imputation tax system. International Review of Finance, 2(4), pp.217-234.

Marsden, S., Sadiq, K. and Wilkins, T., 2013. Small business entity tax concessions: Through

the eyes of the practitioner. Revenue Law Journal, 22(1), p.6731.

Spence, K., 2016. The evolution of corporate taxation-a work in progress. Austl. Tax F., 31,

p.481.

Stewart, M., 2017. Australia’s Hybrid International Tax System: Limited Focus on Tax and

Development. In Taxation and Development-A Comparative Study (pp. 17-41). Springer,

Cham.

Steyn, T., Smulders, S., Stark, K. and Penning, I., 2018. Capital gains tax research: an initial

synthesis of the literature. eJTR, 16, p.278.

Twite, G., 2014. Capital structure choices and taxes: Evidence from the Australian dividend

imputation tax system. International Review of Finance, 2(4), pp.217-234.

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.