Tax Law Assignment: Receipts and Ordinary Income under ITAA97

VerifiedAdded on 2023/04/06

|11

|1612

|430

Homework Assignment

AI Summary

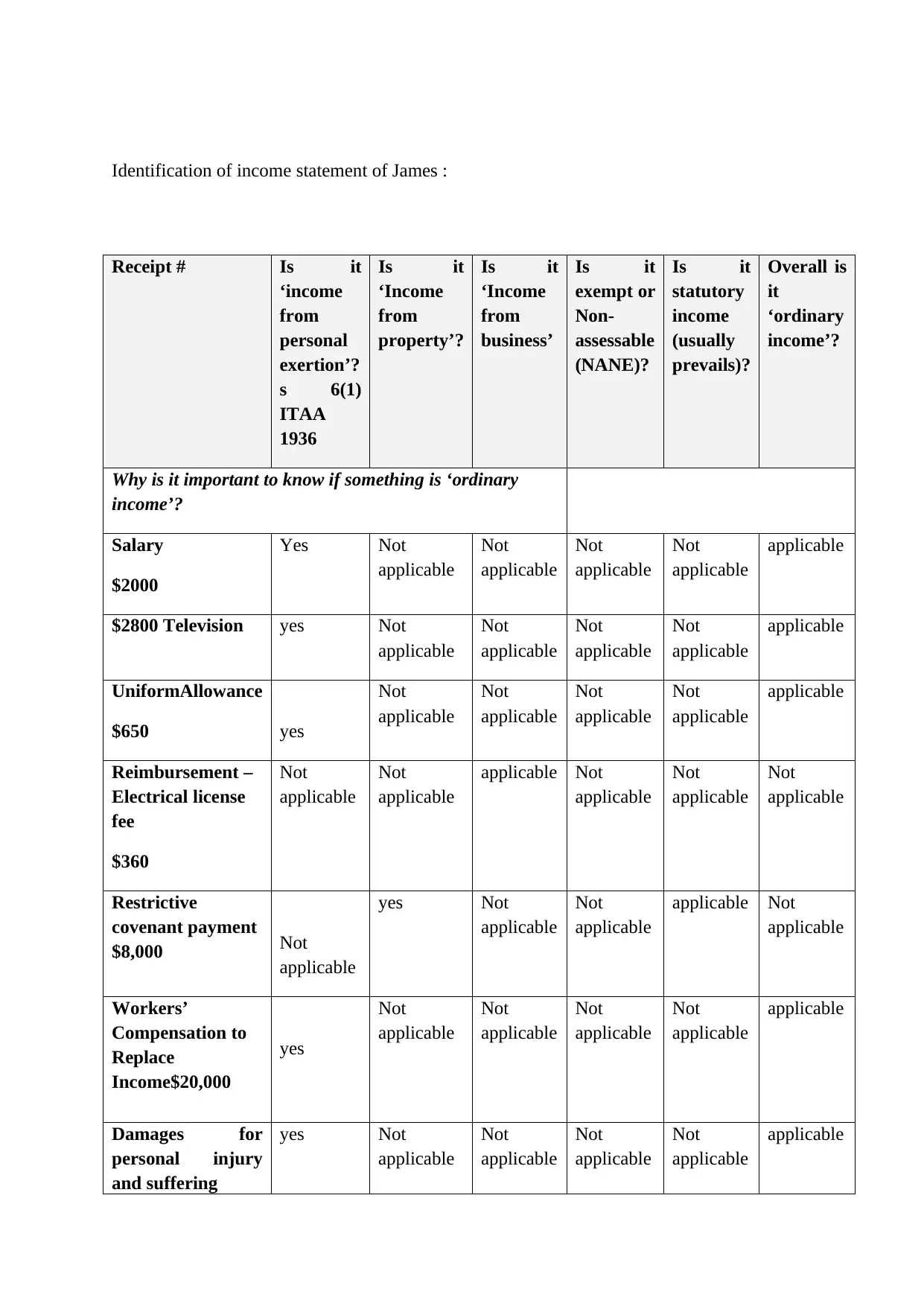

This assignment examines the concept of ordinary income as defined by the ITAA97, focusing on assessing various receipts received by an electrician named James. The assignment begins with a legislative definition of ordinary income and an introduction to the Australian tax system, followed by an analysis of case law. It then categorizes James's receipts, including salary, television, uniform allowance, reimbursements, restrictive covenant payments, workers' compensation, damages for personal injury, bank interest, royalties, and found money, into 'income from personal exertion,' 'income from property,' and 'income from business' to determine if they constitute ordinary income. Each receipt is assessed to determine if it is exempt or non-assessable and if any specific provisions apply. The assignment concludes with a detailed analysis of each receipt, providing justifications for the classifications and determination of assessable income. The analysis covers the characteristics of ordinary income, the effect of payments by third parties, and the application of relevant sections of the ITAA97.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.