Indirect Tax VAT Report for Tesco: Analysis and Implications

VerifiedAdded on 2020/10/22

|12

|3945

|181

Report

AI Summary

This report provides a comprehensive analysis of Value Added Tax (VAT) with a focus on Tesco, a UK-based retail company. It begins by identifying different sources of information on VAT and explaining how an organization should interact with the relevant government agency, HMRC. The report then details VAT registration requirements, the information required on business documentation, and the requirements and frequencies of reporting under different VAT schemes, including annual accounting, cash accounting, flat rate, and standard methods. The report also emphasizes the importance of maintaining up-to-date knowledge of changes to VAT regulations and codes of practice. Furthermore, it includes the analysis of relevant financial data, calculation of VAT liabilities, and the process of completing and submitting a VAT return. The report concludes by discussing the implications and penalties of non-compliance with VAT regulations, adjustments for errors, and the communication of VAT's impact on cash flow and financial forecasts to management, making it a valuable resource for understanding and navigating the complexities of indirect taxation in a business context.

Indirect Tax

Table of Contents

Table of Contents

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Introduction......................................................................................................................................1

LO1 .................................................................................................................................................1

1.1 Different sources of information on VAT.............................................................................1

1.2Explain how an organisation should interact with the relevant government agency.............1

1.3 Explain VAT registration requirements................................................................................2

1.4 Identify the information that must be included on business documentation of VAT

registered businesses. .................................................................................................................3

1.5 Requirements and frequencies of reporting of VAT in different VAT schemes..................4

1.6 Maintain an up-to-date knowledge of changes to codes of practice, regulation or

legislation....................................................................................................................................4

LO 2.................................................................................................................................................5

2.1 Relevant data of company for relevant period......................................................................5

2.2, 2.3 Calculation of relevant inputs and outputs and VAT liability of due to or from tax

authority......................................................................................................................................6

2.4 Complete and submit a VAT return and any associated payment within the statutory time

limits............................................................................................................................................7

LO 3.................................................................................................................................................7

3.1 Implications and penalties for an organisation resulting from failure to abide by VAT

regulations...................................................................................................................................7

3.2 Make adjustments and declarations for any errors or omissions identified in previous VAT

periods.........................................................................................................................................7

LO 4.................................................................................................................................................9

4.1 Inform managers of the impact that the VAT payment may have on an organisation’s cash

flow and financial forecasts........................................................................................................9

4.2 Advise relevant people of changes in VAT legislation which would have an effect on an

organisation’s recording systems................................................................................................9

Conclusion.......................................................................................................................................9

REFERENCES..............................................................................................................................10

.......................................................................................................................................................10

LO1 .................................................................................................................................................1

1.1 Different sources of information on VAT.............................................................................1

1.2Explain how an organisation should interact with the relevant government agency.............1

1.3 Explain VAT registration requirements................................................................................2

1.4 Identify the information that must be included on business documentation of VAT

registered businesses. .................................................................................................................3

1.5 Requirements and frequencies of reporting of VAT in different VAT schemes..................4

1.6 Maintain an up-to-date knowledge of changes to codes of practice, regulation or

legislation....................................................................................................................................4

LO 2.................................................................................................................................................5

2.1 Relevant data of company for relevant period......................................................................5

2.2, 2.3 Calculation of relevant inputs and outputs and VAT liability of due to or from tax

authority......................................................................................................................................6

2.4 Complete and submit a VAT return and any associated payment within the statutory time

limits............................................................................................................................................7

LO 3.................................................................................................................................................7

3.1 Implications and penalties for an organisation resulting from failure to abide by VAT

regulations...................................................................................................................................7

3.2 Make adjustments and declarations for any errors or omissions identified in previous VAT

periods.........................................................................................................................................7

LO 4.................................................................................................................................................9

4.1 Inform managers of the impact that the VAT payment may have on an organisation’s cash

flow and financial forecasts........................................................................................................9

4.2 Advise relevant people of changes in VAT legislation which would have an effect on an

organisation’s recording systems................................................................................................9

Conclusion.......................................................................................................................................9

REFERENCES..............................................................................................................................10

.......................................................................................................................................................10

Introduction

Indirect tax is a regarded as tax that is levied indirectly on goods and services which

consumers buys from market. It is the tax that helps government to generate revenue by putting

tax on a particular product that may be paid either by the consumers or by the seller of the goods.

There are various ways through which this tax is implemented on consumers. Government has

divided this into VAT or GST. For the making analysis of this Tesco has been taken into

consideration, which is headquartered in UK and is in the business of retail industry. This report

is based on VAT in which the different sources of information on VAT would be identified and

explanation on how an organisation should interact with the relevant governmental agency would

be done. Various requirements that are required for registering as a VAT would be done as well

as when the VAT returns are published are also specified. At last the information that has been

taken would be communicated to the manager.

LO1

1.1 Different sources of information on VAT

Taxation is an important process which is undertaken by government so as to generate

value for the country (Beneke, Lustig and Oliva, 2017). This value raised by government would

help in developing infrastructure in country and would also help in running monetary schemes of

government for social cause. There are different sources of information that are available to an

organisation that helps in knowing how the tax is implemented and collected by government

(Reynolds and Smolensky, 2013). The tax is administered and collected by HM revenue and

customs which is primarily governed by value added tax act, 1994. As VAT is levied on most of

goods and services. This act was adopted on 5th July 1994. This is the law which has been

adopted by legislation of UK. This act is being enacted by queens most excellent majesty and

with the advice and consent of lord spiritual and temporal.

1.2Explain how an organisation should interact with the relevant government agency

An organisation while working in country should work according to the rules and

regulations as specified by the government. It is the main task of the company to adhere to

established rules for paying their tax liability and to compute tax responsibility that is on

company for the current year. UK government has established an institution which is named as

HMRC, that helps the taxpayers to pay the tax and ask the questions which are related to

1

Indirect tax is a regarded as tax that is levied indirectly on goods and services which

consumers buys from market. It is the tax that helps government to generate revenue by putting

tax on a particular product that may be paid either by the consumers or by the seller of the goods.

There are various ways through which this tax is implemented on consumers. Government has

divided this into VAT or GST. For the making analysis of this Tesco has been taken into

consideration, which is headquartered in UK and is in the business of retail industry. This report

is based on VAT in which the different sources of information on VAT would be identified and

explanation on how an organisation should interact with the relevant governmental agency would

be done. Various requirements that are required for registering as a VAT would be done as well

as when the VAT returns are published are also specified. At last the information that has been

taken would be communicated to the manager.

LO1

1.1 Different sources of information on VAT

Taxation is an important process which is undertaken by government so as to generate

value for the country (Beneke, Lustig and Oliva, 2017). This value raised by government would

help in developing infrastructure in country and would also help in running monetary schemes of

government for social cause. There are different sources of information that are available to an

organisation that helps in knowing how the tax is implemented and collected by government

(Reynolds and Smolensky, 2013). The tax is administered and collected by HM revenue and

customs which is primarily governed by value added tax act, 1994. As VAT is levied on most of

goods and services. This act was adopted on 5th July 1994. This is the law which has been

adopted by legislation of UK. This act is being enacted by queens most excellent majesty and

with the advice and consent of lord spiritual and temporal.

1.2Explain how an organisation should interact with the relevant government agency

An organisation while working in country should work according to the rules and

regulations as specified by the government. It is the main task of the company to adhere to

established rules for paying their tax liability and to compute tax responsibility that is on

company for the current year. UK government has established an institution which is named as

HMRC, that helps the taxpayers to pay the tax and ask the questions which are related to

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

payment and collection of tax. The organisation is able to interact with the government agency

through various departments which are made by HMRC. They made 25 ministerial departments

that helps company to administer and pay the debts. Also if company has any problems regarding

calculation or levy of tax then they can check the site and the rules that defines the tax rate on

particular item (Nye, 2018). If this process does not help company then company can write a

letter or an Email to department seeking their advise on particular situation by paying relevant

fees. They have also issued a website for letting the taxpayers have a knowledge about various

rules and regulations, which is timely updated as and when required. Department is open from

Monday to Friday between 8 am to 8 pm and from 8 am to 4 pm on Saturday while on Sunday it

is open from 9 am to 5 pm. Department is closed on bank holidays and any other occasion that is

public holiday.

1.3 Explain VAT registration requirements

Registration for VAT is not a typical task and is a compulsory one if any of the threshold

that has been prescribed by government has been reached. The requirement to register for VAT

is achieved when the turnover of the company reaches the threshold limit of euro 85,000. this is

the current limit for the year so as to register for VAT. However, if threshold is not reached then

they can voluntarily register for the VAT. For registering for VAT company has to apply to

HMRC. Department has established an online service portal which helps the company to make

registration on the online basis. Also department has given a flexibility so as to register for VAT

through an accountant or an agent. Various steps are there which has to be followed for capturing

a registration of VAT certificate (Mason, and Stephenson Jr, 2017). There is an implication when

applying for online VAT registration. If company wants to apply for registration as an exception

then they have to do this through process of Post and have to use VAT1 form. Also this case may

apply when company wants to apply for Agriculture flat rate or if company is registering the

division or business units of a body corporate under a separate VAT numbers. Company has to

file VAT1A if there business is in Europe and is in distance selling, company has to file VAT1B

if they are selling goods worth more than Euro 85,000 from another country. And the last form

that is available is VAT1C if the company is disposing asset in which 8th or 13th directive refunds

have been claimed. After receiving VAT number from HMRC you can submit returns.

2

through various departments which are made by HMRC. They made 25 ministerial departments

that helps company to administer and pay the debts. Also if company has any problems regarding

calculation or levy of tax then they can check the site and the rules that defines the tax rate on

particular item (Nye, 2018). If this process does not help company then company can write a

letter or an Email to department seeking their advise on particular situation by paying relevant

fees. They have also issued a website for letting the taxpayers have a knowledge about various

rules and regulations, which is timely updated as and when required. Department is open from

Monday to Friday between 8 am to 8 pm and from 8 am to 4 pm on Saturday while on Sunday it

is open from 9 am to 5 pm. Department is closed on bank holidays and any other occasion that is

public holiday.

1.3 Explain VAT registration requirements

Registration for VAT is not a typical task and is a compulsory one if any of the threshold

that has been prescribed by government has been reached. The requirement to register for VAT

is achieved when the turnover of the company reaches the threshold limit of euro 85,000. this is

the current limit for the year so as to register for VAT. However, if threshold is not reached then

they can voluntarily register for the VAT. For registering for VAT company has to apply to

HMRC. Department has established an online service portal which helps the company to make

registration on the online basis. Also department has given a flexibility so as to register for VAT

through an accountant or an agent. Various steps are there which has to be followed for capturing

a registration of VAT certificate (Mason, and Stephenson Jr, 2017). There is an implication when

applying for online VAT registration. If company wants to apply for registration as an exception

then they have to do this through process of Post and have to use VAT1 form. Also this case may

apply when company wants to apply for Agriculture flat rate or if company is registering the

division or business units of a body corporate under a separate VAT numbers. Company has to

file VAT1A if there business is in Europe and is in distance selling, company has to file VAT1B

if they are selling goods worth more than Euro 85,000 from another country. And the last form

that is available is VAT1C if the company is disposing asset in which 8th or 13th directive refunds

have been claimed. After receiving VAT number from HMRC you can submit returns.

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1.4 Identify the information that must be included on business documentation of VAT registered

businesses.

After registering for VAT company has to procure many documents and has to change

the way of trading. After company gets registered on VAT then they have to provide vat invoice

to every customer that they have. After getting the registration company has to follow regulation

16 that provides them the some points that are to be followed while issuing invoice which

includes the following:

An identifying number

The time of supply of goods to be mentioned in invoice.

Date of issue of document must be entered.

On the top of invoice name, address and registration number of supplier must be entered.

Also name, address and registration of buyer must be entered and if registration number

not available then it should be left as blank.

The invoice must contain a type of supply which may be categorised as:

▪ A supply by sale

▪ A supply on hire purchase

▪ A supply by loan

▪ Supply by way of exchange

▪ Supply made through customers material

▪ Supply by sale on commission etc.

the invoice must contain the identification of goods or services supplied.

For every item they must include the rate of tax that is applicable on it in a separate

column.

In separate column MRP and amount of VAT must be entered so as to determine the

value of separately.

It should separately mention any of the cash discount if offered to supplier.

The company should also have maintain the books of accounts which help them to file

the VAT return and if any misstatement is found in the return that has been filed by company

then they have to furnish these books of accounts to authority (Llerena and et. al., 2015). The

company should keep the record of all the invoices that are required by them.

3

businesses.

After registering for VAT company has to procure many documents and has to change

the way of trading. After company gets registered on VAT then they have to provide vat invoice

to every customer that they have. After getting the registration company has to follow regulation

16 that provides them the some points that are to be followed while issuing invoice which

includes the following:

An identifying number

The time of supply of goods to be mentioned in invoice.

Date of issue of document must be entered.

On the top of invoice name, address and registration number of supplier must be entered.

Also name, address and registration of buyer must be entered and if registration number

not available then it should be left as blank.

The invoice must contain a type of supply which may be categorised as:

▪ A supply by sale

▪ A supply on hire purchase

▪ A supply by loan

▪ Supply by way of exchange

▪ Supply made through customers material

▪ Supply by sale on commission etc.

the invoice must contain the identification of goods or services supplied.

For every item they must include the rate of tax that is applicable on it in a separate

column.

In separate column MRP and amount of VAT must be entered so as to determine the

value of separately.

It should separately mention any of the cash discount if offered to supplier.

The company should also have maintain the books of accounts which help them to file

the VAT return and if any misstatement is found in the return that has been filed by company

then they have to furnish these books of accounts to authority (Llerena and et. al., 2015). The

company should keep the record of all the invoices that are required by them.

3

1.5 Requirements and frequencies of reporting of VAT in different VAT schemes.

There are different reporting styles and schemes that are required by registered person to

fulfil and follow while performing their duties and task. This includes the following

Annual Accounting Scheme: this is the scheme in which business has to make quarterly

or monthly payment towards their annual VAT bill but has to submit only one return per

year. This includes the payment that has to be made for a period of year in instalment by

business and is considered as flexible for business concern (Kaplanoglou, 2015). For

being able to register under annual accounting scheme they should have a taxable

turnover of under Euro 1.35Mn. If the scheme is being left in previous 12 months or have

not paid the returns then business ceases to be compatible to avail this service.

Cash Accounting scheme: it is a scheme in which business concerns have to pay VAT

on the basis of sales that are made and the payment that has been received on the basis of

sales. In this business organisation has to issue VAT invoice even if the customer has not

paid VAT on the same. This is basically adopted by small business enterprises. Under

this the return has to filed by organisation not on the basis of invoices that it receives but

on the basis of payment that business receives or makes.

Flat rate scheme: This scheme allows the small business organisation to use an

alternative to the normal method of accounting for VAT. Under this scheme company can

calculate a the amount through a flat rate that has been decide by government on the total

turnover (Higgins and Pereira, 2014). Under this scheme the business entrepreneur who

have a turnover of under Euro 150,000 can avail this method. For this companies must

follow a flat rate turnover for the period of accounting also the flat rate percentage should

be used for this purpose. For paying VAT under this scheme company can use online

returns filling tools which would help them in filling return electronically

Standard method: It is a method that allows recording and reporting of VAT where

VAT is paid on the basis of invoices that are issued. Under this system companies has to

submit returns at least four times a year. Which includes a quarterly payments. Also if

any VAT refunds are due to business would be paid in quarterly basis.

1.6 Maintain an up-to-date knowledge of changes to codes of practice, regulation or legislation

Maintenance of an up to date information is important for company so as to calculate the

amount of VAT that has to be paid to government. It is required as the rate of tax changes from

4

There are different reporting styles and schemes that are required by registered person to

fulfil and follow while performing their duties and task. This includes the following

Annual Accounting Scheme: this is the scheme in which business has to make quarterly

or monthly payment towards their annual VAT bill but has to submit only one return per

year. This includes the payment that has to be made for a period of year in instalment by

business and is considered as flexible for business concern (Kaplanoglou, 2015). For

being able to register under annual accounting scheme they should have a taxable

turnover of under Euro 1.35Mn. If the scheme is being left in previous 12 months or have

not paid the returns then business ceases to be compatible to avail this service.

Cash Accounting scheme: it is a scheme in which business concerns have to pay VAT

on the basis of sales that are made and the payment that has been received on the basis of

sales. In this business organisation has to issue VAT invoice even if the customer has not

paid VAT on the same. This is basically adopted by small business enterprises. Under

this the return has to filed by organisation not on the basis of invoices that it receives but

on the basis of payment that business receives or makes.

Flat rate scheme: This scheme allows the small business organisation to use an

alternative to the normal method of accounting for VAT. Under this scheme company can

calculate a the amount through a flat rate that has been decide by government on the total

turnover (Higgins and Pereira, 2014). Under this scheme the business entrepreneur who

have a turnover of under Euro 150,000 can avail this method. For this companies must

follow a flat rate turnover for the period of accounting also the flat rate percentage should

be used for this purpose. For paying VAT under this scheme company can use online

returns filling tools which would help them in filling return electronically

Standard method: It is a method that allows recording and reporting of VAT where

VAT is paid on the basis of invoices that are issued. Under this system companies has to

submit returns at least four times a year. Which includes a quarterly payments. Also if

any VAT refunds are due to business would be paid in quarterly basis.

1.6 Maintain an up-to-date knowledge of changes to codes of practice, regulation or legislation

Maintenance of an up to date information is important for company so as to calculate the

amount of VAT that has to be paid to government. It is required as the rate of tax changes from

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

time to time and every year. A company should follow all rules and regulations which are

prescribed and changed from time to time. If these changes are not implemented by company

then it would result in penalties on company (Herger, Kotsogiannis and McCorriston, 2016). As

from January 1, 2018 new rules has been introduced by government on disclosure and avoidance

schemes covering value added tax and other indirect tax which was alternatively avoided to

disclose. Also new rule of applying online for fulfilment house due diligence schemes were

implemented.

LO 2

2.1 Relevant data of company for relevant period.

1. Cash sales amounted to £50,400, of which £46,200 was in respect of standard rated sales

and £4,200 was in respect of zero-rated sales. All of these sales were to non-VAT

registered customers.

2. Sales invoices totalling £128,000 were issued in respect of credit sales to VAT registered

customers. These sales were all standard rated. Tesco gives their customers a 3%

discount for payment within 30 days of the date of the sales invoice, and 80% of the

customers pay within this period.

3. Standard rated materials amounted to £32,400, of which £600 were taken by Tesco for

their personal use.

4. Standard rated expenses amounted to £24,800. This includes £1,200 for entertaining UK

customers.

5. On 15 March 2014 Tesco sold a motor car for £9,600, and purchased a new motor car at a

cost of £16,800. Both motor cars were used for business and private mileage, but no fuel

was provided for private mileage (Flues and Thomas, 2015). These figures are inclusive

of VAT where applicable.

6. On 28 March 2014 Tesco sold machinery for £3,600, and purchased new machinery at a

cost of £21,600. She paid for the new machinery on this date, but did not take delivery or

receive an invoice until 6 April 2014. These figures are inclusive of VAT where

applicable.

7. On 31 March 2014 Tesco wrote off impairment losses in respect of three invoices that

were due for payment on 15 August 2013, 15 September 2013 and 15 October 2013

5

prescribed and changed from time to time. If these changes are not implemented by company

then it would result in penalties on company (Herger, Kotsogiannis and McCorriston, 2016). As

from January 1, 2018 new rules has been introduced by government on disclosure and avoidance

schemes covering value added tax and other indirect tax which was alternatively avoided to

disclose. Also new rule of applying online for fulfilment house due diligence schemes were

implemented.

LO 2

2.1 Relevant data of company for relevant period.

1. Cash sales amounted to £50,400, of which £46,200 was in respect of standard rated sales

and £4,200 was in respect of zero-rated sales. All of these sales were to non-VAT

registered customers.

2. Sales invoices totalling £128,000 were issued in respect of credit sales to VAT registered

customers. These sales were all standard rated. Tesco gives their customers a 3%

discount for payment within 30 days of the date of the sales invoice, and 80% of the

customers pay within this period.

3. Standard rated materials amounted to £32,400, of which £600 were taken by Tesco for

their personal use.

4. Standard rated expenses amounted to £24,800. This includes £1,200 for entertaining UK

customers.

5. On 15 March 2014 Tesco sold a motor car for £9,600, and purchased a new motor car at a

cost of £16,800. Both motor cars were used for business and private mileage, but no fuel

was provided for private mileage (Flues and Thomas, 2015). These figures are inclusive

of VAT where applicable.

6. On 28 March 2014 Tesco sold machinery for £3,600, and purchased new machinery at a

cost of £21,600. She paid for the new machinery on this date, but did not take delivery or

receive an invoice until 6 April 2014. These figures are inclusive of VAT where

applicable.

7. On 31 March 2014 Tesco wrote off impairment losses in respect of three invoices that

were due for payment on 15 August 2013, 15 September 2013 and 15 October 2013

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

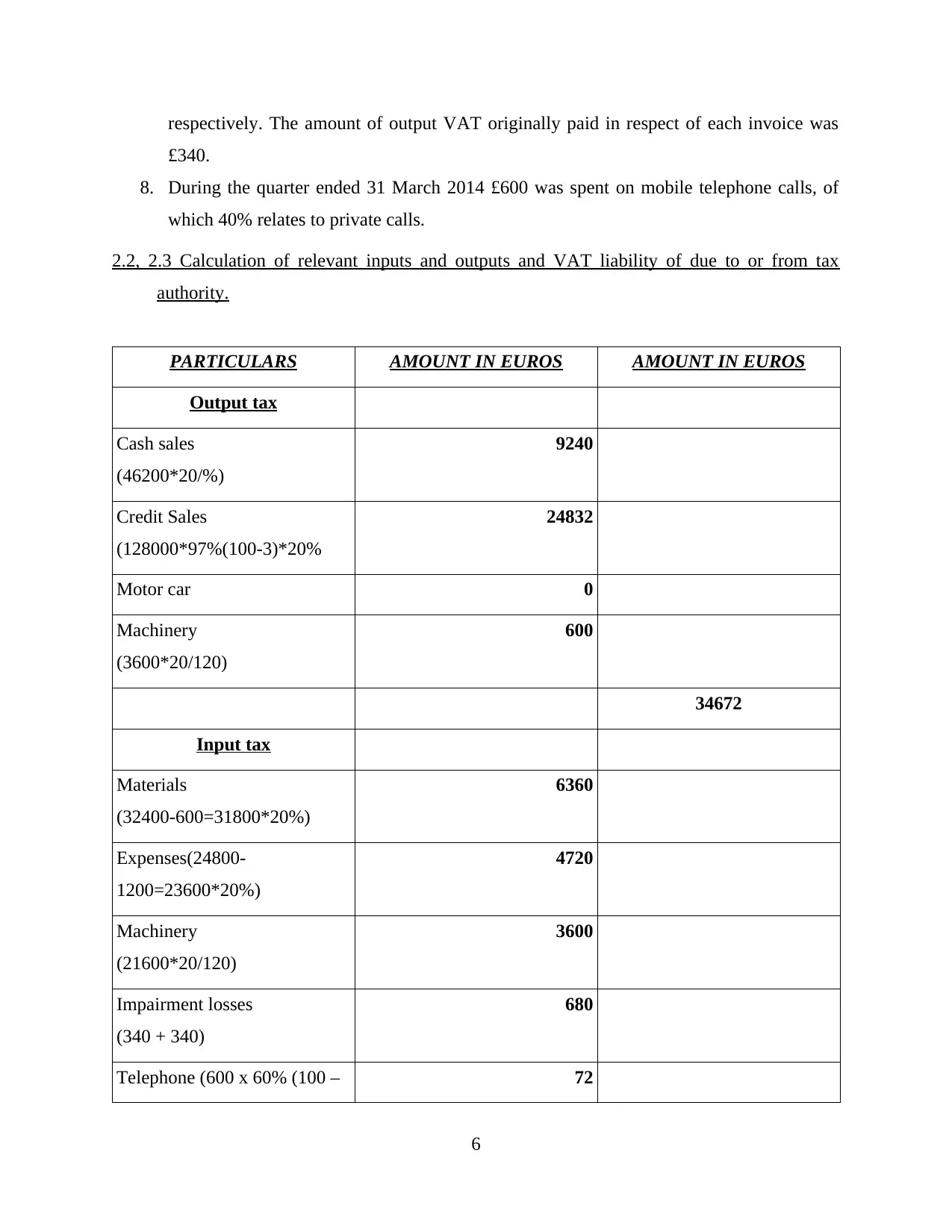

respectively. The amount of output VAT originally paid in respect of each invoice was

£340.

8. During the quarter ended 31 March 2014 £600 was spent on mobile telephone calls, of

which 40% relates to private calls.

2.2, 2.3 Calculation of relevant inputs and outputs and VAT liability of due to or from tax

authority.

PARTICULARS AMOUNT IN EUROS AMOUNT IN EUROS

Output tax

Cash sales

(46200*20/%)

9240

Credit Sales

(128000*97%(100-3)*20%

24832

Motor car 0

Machinery

(3600*20/120)

600

34672

Input tax

Materials

(32400-600=31800*20%)

6360

Expenses(24800-

1200=23600*20%)

4720

Machinery

(21600*20/120)

3600

Impairment losses

(340 + 340)

680

Telephone (600 x 60% (100 – 72

6

£340.

8. During the quarter ended 31 March 2014 £600 was spent on mobile telephone calls, of

which 40% relates to private calls.

2.2, 2.3 Calculation of relevant inputs and outputs and VAT liability of due to or from tax

authority.

PARTICULARS AMOUNT IN EUROS AMOUNT IN EUROS

Output tax

Cash sales

(46200*20/%)

9240

Credit Sales

(128000*97%(100-3)*20%

24832

Motor car 0

Machinery

(3600*20/120)

600

34672

Input tax

Materials

(32400-600=31800*20%)

6360

Expenses(24800-

1200=23600*20%)

4720

Machinery

(21600*20/120)

3600

Impairment losses

(340 + 340)

680

Telephone (600 x 60% (100 – 72

6

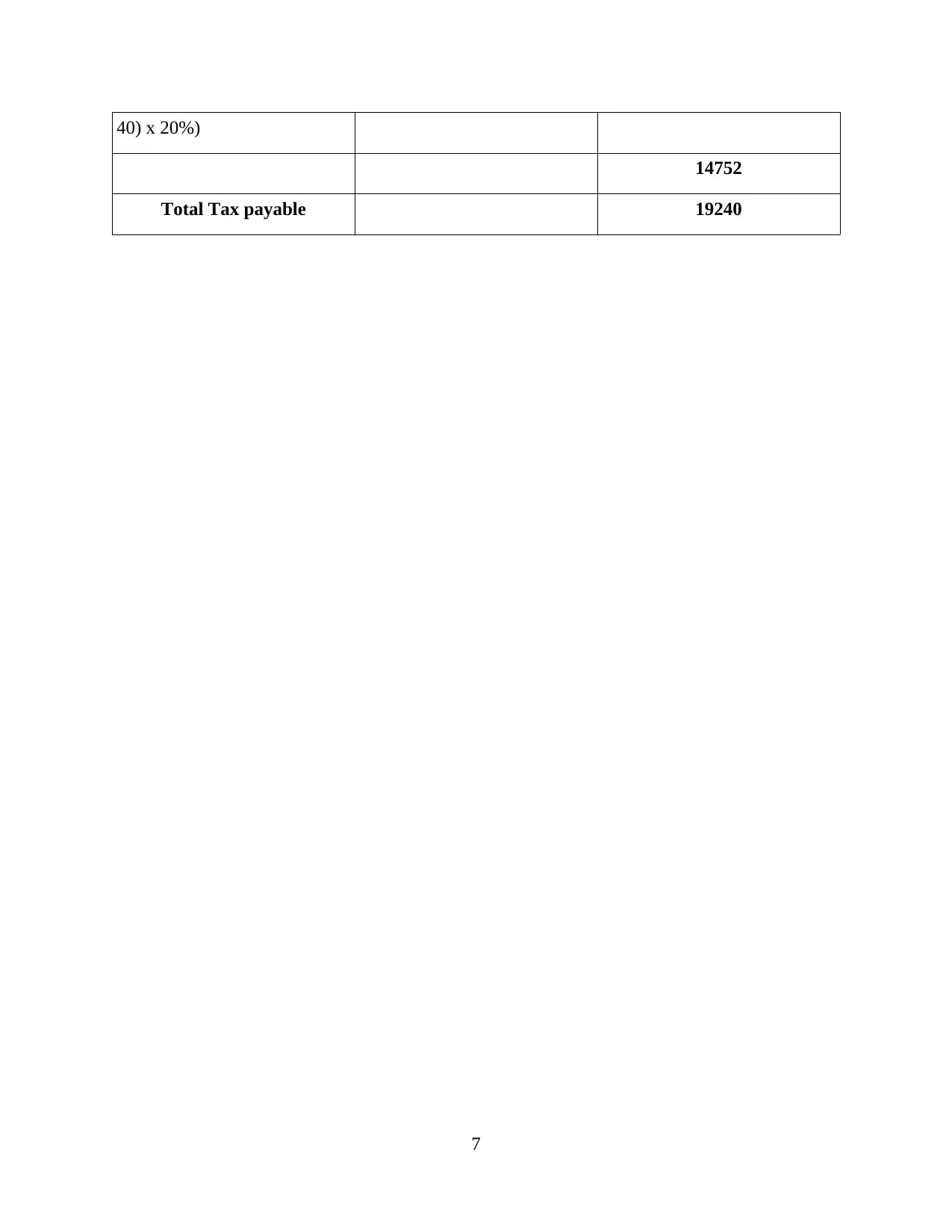

40) x 20%)

14752

Total Tax payable 19240

7

14752

Total Tax payable 19240

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

2.4 Complete and submit a VAT return and any associated payment within the statutory time

limits

A VAT return is a return that summarise the sales and purchase of company. This

includes a sales total and output tax that has to be made by the company. This return should be

filled online on portal of HMRC. Company should fill the appropriate boxes under which the

entries falls. As Tesco has the liability of paying tax of 19,240 which is required to be paid to

authority.

LO 3

3.1 Implications and penalties for an organisation resulting from failure to abide by VAT

regulations.

The organisation records a default In favour of company if they are not able to pay of

their VAT liability. There are certain condition that are to be followed by the company for filling

returns and for filing the tax online (Dowell, 2013). The conditions if fulfilled by company

would result in default, these conditions include if the company has not filled the return by the

deadline. Or full payment for VAT due on return has not been paid by the organisation. If these

conditions are fulfilled and company does not pays their debts then it would go into surcharge of

a period of 12 months. If company is able to pay VAT as a late return then it would not attract

surcharge on it. The amount of surcharge is the percentage of VAT which is outstanding on the

due date for the accounting period which is in default. This rate increases every time the default

is made. Whereas the company does not have to pay surcharge for the first default that it makes.

While from the second default the amount is 2% and increases like wise as prescribed by

department. HMRC also charges penalties which may extend up to 100% of any tax understated

or over stated if you send a return that contains a careless or deliberate inaccuracy. 30% of

assessment If HMRC sends a notice regarding the amount that you have paid and if company

does not replie within 30 days. And if company submits a paper VAT return than penalty of Euro

400 would be required by the company to be paid.

3.2 Make adjustments and declarations for any errors or omissions identified in previous VAT

periods.

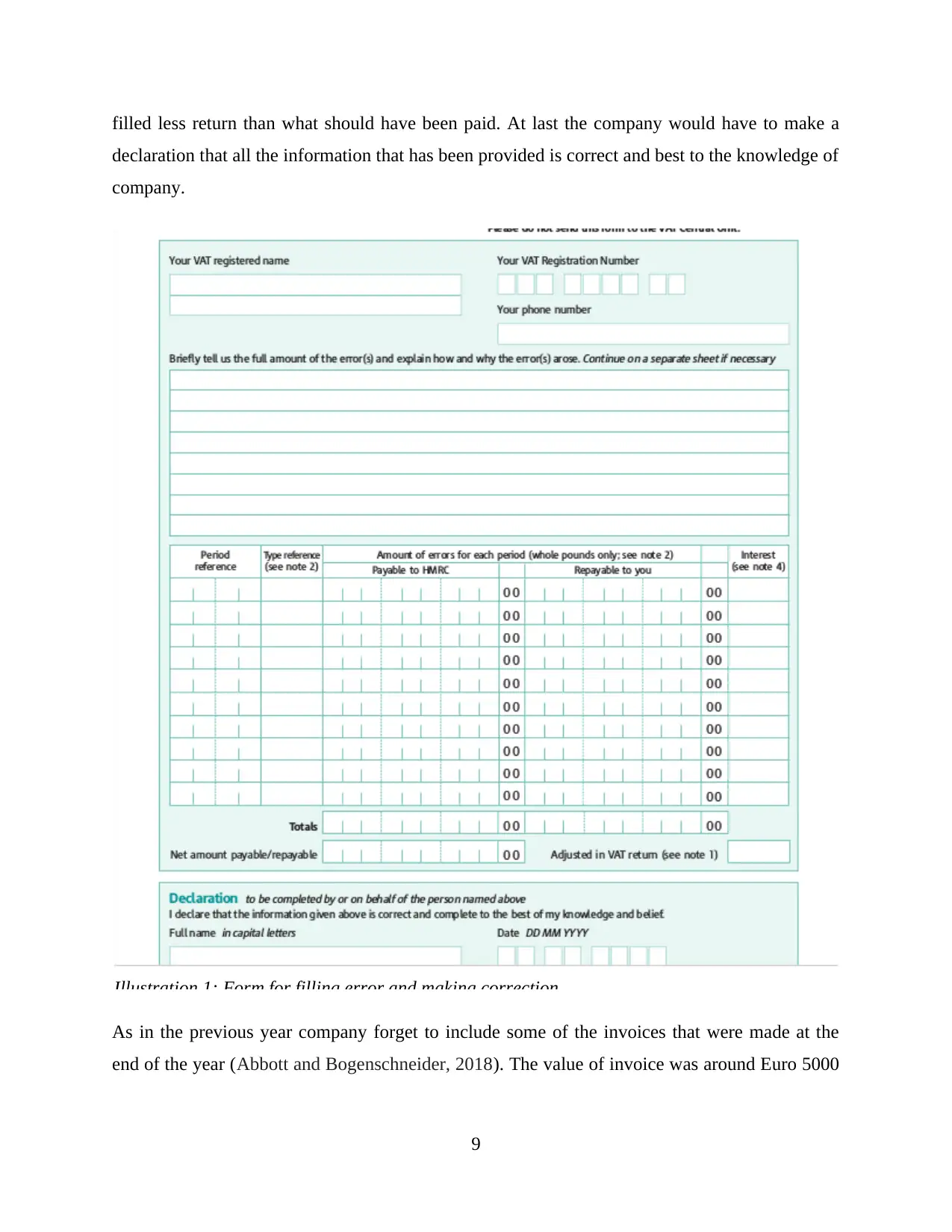

For making adjustment and declaration of any errors company has to file a VAT 652

online to department. This form is filled if company has made an error in filing the return or has

8

limits

A VAT return is a return that summarise the sales and purchase of company. This

includes a sales total and output tax that has to be made by the company. This return should be

filled online on portal of HMRC. Company should fill the appropriate boxes under which the

entries falls. As Tesco has the liability of paying tax of 19,240 which is required to be paid to

authority.

LO 3

3.1 Implications and penalties for an organisation resulting from failure to abide by VAT

regulations.

The organisation records a default In favour of company if they are not able to pay of

their VAT liability. There are certain condition that are to be followed by the company for filling

returns and for filing the tax online (Dowell, 2013). The conditions if fulfilled by company

would result in default, these conditions include if the company has not filled the return by the

deadline. Or full payment for VAT due on return has not been paid by the organisation. If these

conditions are fulfilled and company does not pays their debts then it would go into surcharge of

a period of 12 months. If company is able to pay VAT as a late return then it would not attract

surcharge on it. The amount of surcharge is the percentage of VAT which is outstanding on the

due date for the accounting period which is in default. This rate increases every time the default

is made. Whereas the company does not have to pay surcharge for the first default that it makes.

While from the second default the amount is 2% and increases like wise as prescribed by

department. HMRC also charges penalties which may extend up to 100% of any tax understated

or over stated if you send a return that contains a careless or deliberate inaccuracy. 30% of

assessment If HMRC sends a notice regarding the amount that you have paid and if company

does not replie within 30 days. And if company submits a paper VAT return than penalty of Euro

400 would be required by the company to be paid.

3.2 Make adjustments and declarations for any errors or omissions identified in previous VAT

periods.

For making adjustment and declaration of any errors company has to file a VAT 652

online to department. This form is filled if company has made an error in filing the return or has

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

filled less return than what should have been paid. At last the company would have to make a

declaration that all the information that has been provided is correct and best to the knowledge of

company.

As in the previous year company forget to include some of the invoices that were made at the

end of the year (Abbott and Bogenschneider, 2018). The value of invoice was around Euro 5000

9

Illustration 1: Form for filling error and making correction

declaration that all the information that has been provided is correct and best to the knowledge of

company.

As in the previous year company forget to include some of the invoices that were made at the

end of the year (Abbott and Bogenschneider, 2018). The value of invoice was around Euro 5000

9

Illustration 1: Form for filling error and making correction

on which output tax was to paid by company. So company has to make declaration in this form

and has to file tax accordingly.

LO 4

4.1 Inform managers of the impact that the VAT payment may have on an organisation’s cash

flow and financial forecasts.

VAT is considered as one of the main source of income for government that helps them

in raising money indirectly (Bucheli, Lustig, Rossi and Amábile, 2013). If the company is

registered under VAT act then they have to pay VAT that has been collected by them through

consumers. It impacts the financial performance of business in positive way as it reduced the cost

of production to the goods by reducing and lowering the cost of raw material to compensate for

the value of added percentage. As the money is collected by seller of the goods and has to be

paid at the end of month or the year so the amount that is available to them helps in maintaining

the cash flow without having any charge or interest that has to be paid.

4.2 Advise relevant people of changes in VAT legislation which would have an effect on an

organisation’s recording systems

VAT is considered as the key issue for the small business enterprises in UK. The

companies has to follow the guidelines regardless of size and profit if they got themselves

registered in VAT act. As VAT act changes every year so the company has to maintain a team

that would help them in calculating and submitting the VAT returns on timely basis. As Tesco is

working in the retail segment so it is the duty of the company to identify the different rate of

VAT on different articles that they sell (Boadway and Pestieau, 2011). It is important for the

company to analyse the impact of change in VAT that is made on timely basis. So the employees

of the company should check and comply with the all the updates which would impact the

recording styles.

Conclusion

From the above report it is analysed that VAT has main effect on the performance of the

business and it is the liability of the company to pay of any tax which is the liability of company.

Company should check and be up to date about the various changes that has the effect on the

performance and the management of the business. A company should check on timely basis

about changes of that is done every year.

10

and has to file tax accordingly.

LO 4

4.1 Inform managers of the impact that the VAT payment may have on an organisation’s cash

flow and financial forecasts.

VAT is considered as one of the main source of income for government that helps them

in raising money indirectly (Bucheli, Lustig, Rossi and Amábile, 2013). If the company is

registered under VAT act then they have to pay VAT that has been collected by them through

consumers. It impacts the financial performance of business in positive way as it reduced the cost

of production to the goods by reducing and lowering the cost of raw material to compensate for

the value of added percentage. As the money is collected by seller of the goods and has to be

paid at the end of month or the year so the amount that is available to them helps in maintaining

the cash flow without having any charge or interest that has to be paid.

4.2 Advise relevant people of changes in VAT legislation which would have an effect on an

organisation’s recording systems

VAT is considered as the key issue for the small business enterprises in UK. The

companies has to follow the guidelines regardless of size and profit if they got themselves

registered in VAT act. As VAT act changes every year so the company has to maintain a team

that would help them in calculating and submitting the VAT returns on timely basis. As Tesco is

working in the retail segment so it is the duty of the company to identify the different rate of

VAT on different articles that they sell (Boadway and Pestieau, 2011). It is important for the

company to analyse the impact of change in VAT that is made on timely basis. So the employees

of the company should check and comply with the all the updates which would impact the

recording styles.

Conclusion

From the above report it is analysed that VAT has main effect on the performance of the

business and it is the liability of the company to pay of any tax which is the liability of company.

Company should check and be up to date about the various changes that has the effect on the

performance and the management of the business. A company should check on timely basis

about changes of that is done every year.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.